High Performance Computing (HPC) Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

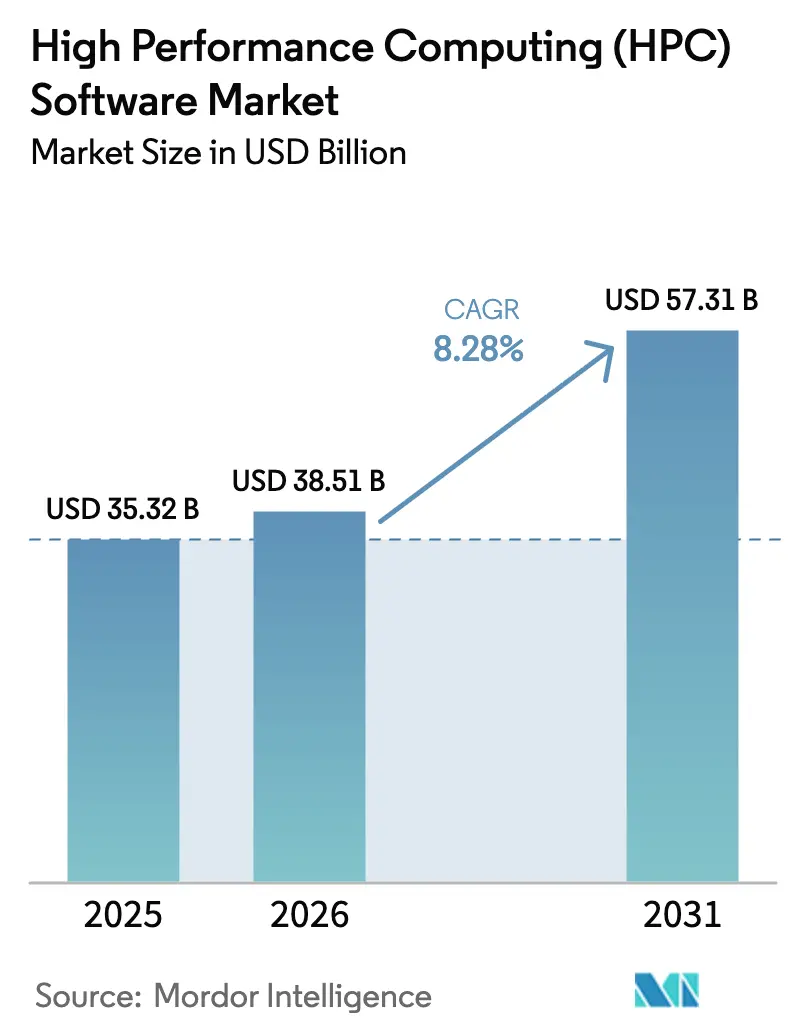

| Market Size (2026) | USD 38.51 Billion |

| Market Size (2031) | USD 57.31 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

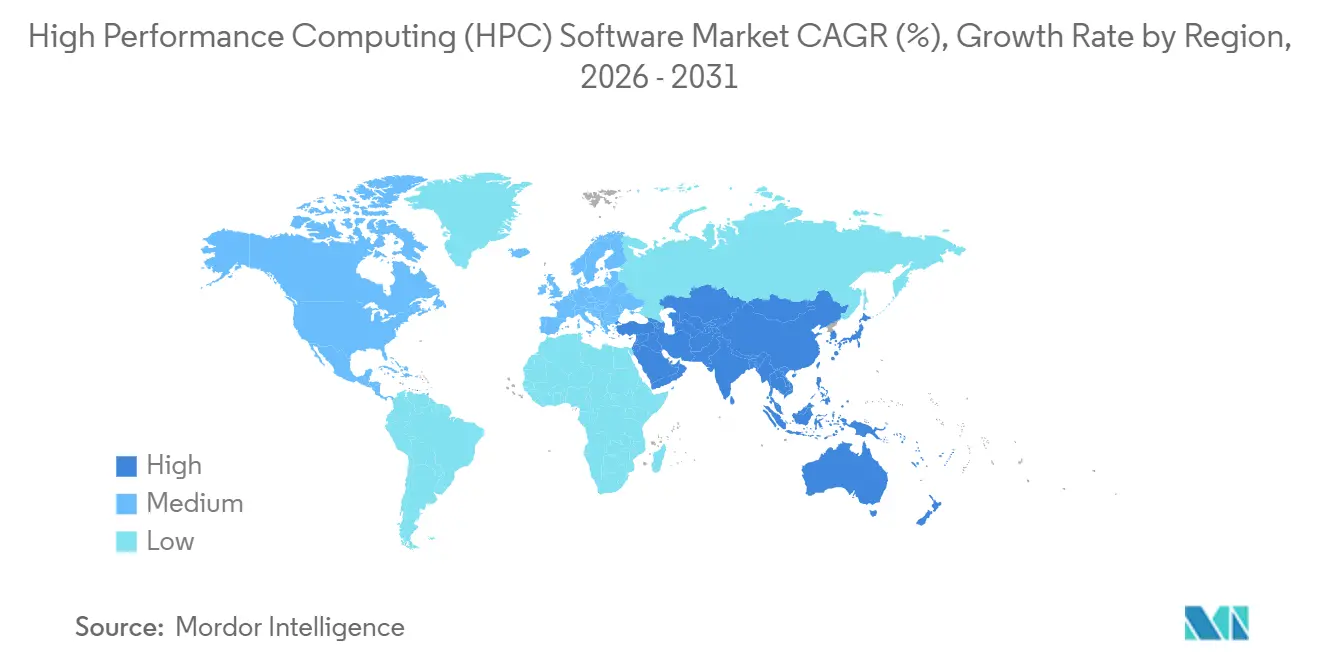

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Performance Computing (HPC) Software Market Analysis by Mordor Intelligence

The High Performance Computing Software Market size is expected to increase from USD 35.32 billion in 2025 to USD 38.51 billion in 2026 and reach USD 57.31 billion by 2031, growing at a CAGR of 8.28% over 2026-2031.

Expanding cloud-native architectures, GPU-dense “neoclouds,” and sovereign AI mandates are redrawing procurement priorities, steering workloads away from capital-intensive on-premises clusters toward elastic consumption models. Vendors that optimize schedulers for heterogeneous GPU stocks, embed compliance toolkits for data-residency rules, and expose real-time cost controls are capturing disproportionate growth. Competitive dynamics favour platforms that fuse open-source flexibility with managed-service ease, allowing enterprises to shift simulation, life-science, and AI training jobs across geographies for price arbitrage. Neocloud entrants, financed through GPU-backed credit lines, are undercutting hyperscalers on GPU-hour pricing while licensing the same workload managers that power exascale systems, intensifying software differentiation pressures.

Key Report Takeaways

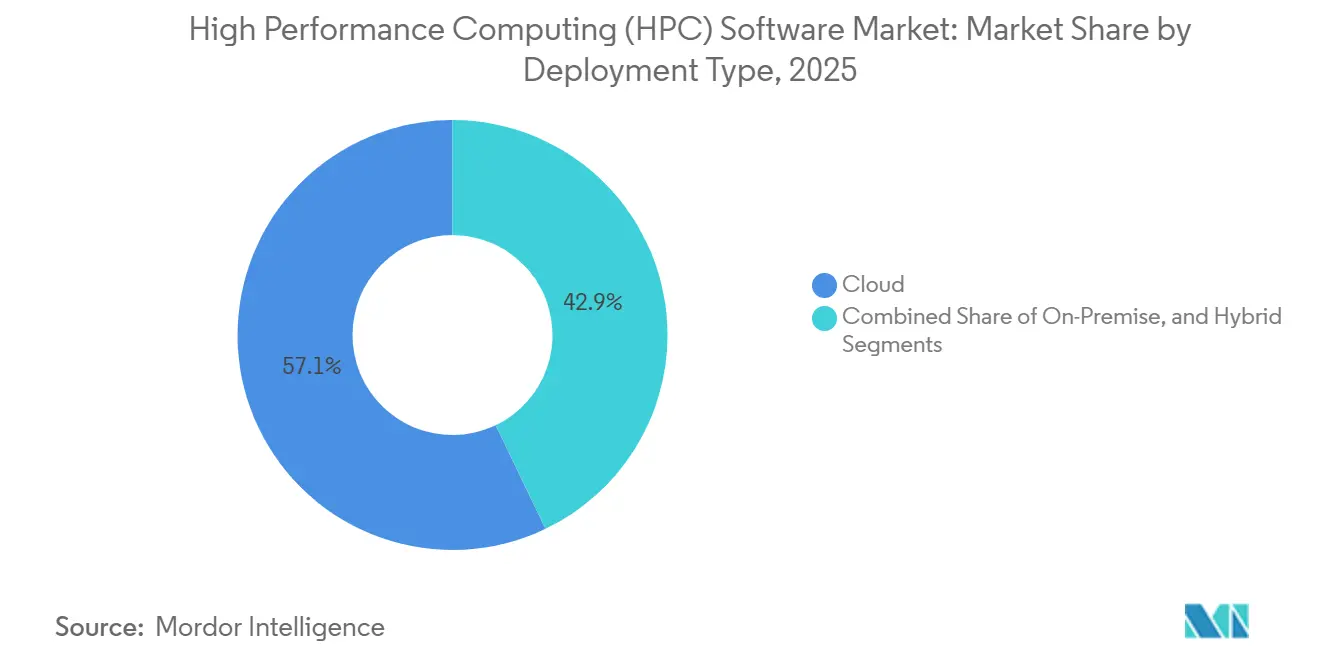

- By deployment type, cloud commanded 57.12% revenue share in 2025 while hybrid configurations are advancing at 8.82% CAGR through 2031.

- By software category, workload managers and schedulers held 28.41% of the HPC software market share in 2025, whereas data management and file systems are expanding at 9.26% CAGR through 2031.

- By service model, HPC infrastructure-as-a-service captured 41.29% revenue share in 2025; HPC software-as-a-service is growing at 8.76% CAGR through 2031.

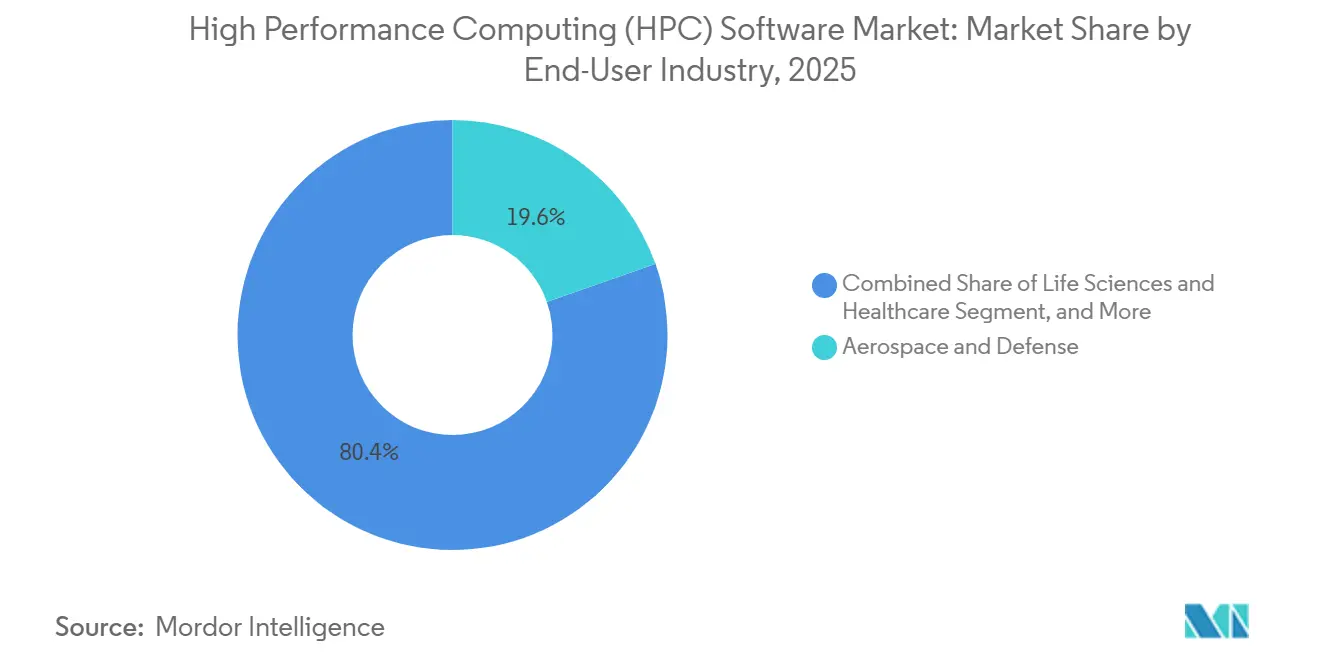

- By end-user industry, aerospace and defense represented 19.63% of spending in 2025, yet life sciences and healthcare are accelerating at 9.55% CAGR through 2031.

- By organization size, large enterprises accounted for 64.89% of revenue in 2025, while medium enterprises are expanding at 8.95% CAGR through 2031.

- By geography, North America held 38.92% share in 2025, and Asia Pacific is surging at 9.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High Performance Computing (HPC) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of cloud-based HPC software | +9.20% | Global, with hyperscaler concentration in North America and Europe | Short term (≤ 2 years) |

| Rising AI/ML training complexity requiring advanced schedulers | +11.80% | Global, led by North America and Asia Pacific AI hubs | Medium term (2-4 years) |

| Expansion of GPU-dense neoclouds creating new software TAM | +8.70% | North America and Europe core, spillover to Middle East | Short term (≤ 2 years) |

| Open-source ecosystem lowers entry barriers for SMEs | +6.40% | Global, with strongest uptake in Asia Pacific and South America | Medium term (2-4 years) |

| Energy-aware scheduling to optimize power-constrained data centers | +5.30% | Europe and North America, expanding to Asia Pacific | Long term (≥ 4 years) |

| Sovereignty-focused compliance modules in HPC stacks | +7.10% | Europe, Asia Pacific, Middle East with data localization mandates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud-Based HPC Software

Cloud-native clusters let organizations spin up thousands of CPU and GPU cores within hours, bypassing multi-year depreciation cycles that burden capital budgets. Enhanced network fabrics now deliver 400 Gbps instance-to-instance throughput, closing the latency gap that once relegated tightly coupled CFD jobs to on-premises systems.[1]Amazon Web Services, “AWS ParallelCluster,” amazon.com Schedulers integrated into these services automatically mix spot and on-demand capacity, lowering unit costs while preserving deadline guarantees. Open-source images, reference architectures, and managed installer scripts shrink deployment time from days to minutes, freeing R&D teams to iterate on models instead of racking servers. Finance and governance functions also favour the switch: shifting HPC spend from capex to opex improves cash-flow optics and aligns expenses with project milestones.[2]Google Cloud, “High-Performance Computing Toolkit,” google.com

Rising AI/ML Training Complexity Requiring Advanced Schedulers

Foundation-model training now spans tens of thousands of H100-class GPUs, stressing legacy queue managers that lack GPU topology awareness. New algorithms in Slurm 24.05 capture fabric bandwidth metadata, assign jobs to tightly knit NVLink islands, and cut all-reduce overheads by up to 35%, trimming training runs by days.[3]NVIDIA Corporation, “NVLink and NVSwitch Architecture,” nvidia.com Checkpoint sizes approaching multi-terabytes force schedulers to coordinate parallel I/O, fault tolerance, and pre-emption policies across cloud burst nodes. Kubernetes-based operators extend these capabilities, but enterprises running Fortran-heavy CFD codes alongside PyTorch workloads still rely on hybrid schedulers that bridge batch scripts and containers. Vendors that wrap these complexities into templates and blueprints see rapid uptake, particularly in pharmaceutical and climate-modelling labs that cannot tolerate restart delays.

Expansion of GPU-Dense Neoclouds Creating New Software TAM

CoreWeave, Lambda, and similar specialists financed billions of USD by pledging GPU inventory as collateral, creating new infrastructure capacity outside hyperscaler procurement cycles. Their differentiation rests on software, not metal: custom Kubernetes operators expose real-time pricing APIs and automatically migrate jobs to the cheapest zone within seconds. Lacking in-house scheduler teams, most license commercial workload managers or contribute patches to open-source projects, expanding total addressable revenue for software vendors. Contracts such as the multi-year GPU agreement between CoreWeave and OpenAI highlight that orchestration features such as cost capping, burst scaling, and audit trails are now key bidding criteria rather than raw teraflop counts. The resulting competition pressures hyperscalers to accelerate feature roadmaps, benefiting the broader high performance computing (HPC) software market.

Sovereignty-Focused Compliance Modules in HPC Stacks

The EuroHPC Joint Undertaking mandates auditable, domestically controlled software layers on publicly funded clusters, forcing vendors to publish source code or allow code escrow. Similar rules in India’s National Supercomputing Mission compel middleware to tag data with geographic metadata and block cross-border model training. U.S. export controls push multinationals to implement region-locked feature sets, fragmenting code bases yet creating demand for policy-driven configuration engines. Compliance modules that automate audit logging, permit granular key management, and integrate with regional identity providers, thus become critical purchase criteria. Open-source projects gain traction because sovereign buyers can self-inspect code paths, while commercial vendors win deals by bundling validation reports and secure-boot binaries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data security and IP concerns in multi-tenant cloud | -3.80% | Global, acute in regulated industries (BFSI, healthcare, defense) | Short term (≤ 2 years) |

| Shortage of skilled HPC software administrators | -4.20% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Rising software license and support costs | -2.60% | North America and Europe, impacting academic and SME segments | Medium term (2-4 years) |

| Fragmented standards impeding interoperability | -2.10% | Global, with vendor lock-in concentrated in proprietary ecosystems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Security and IP Concerns in Multi-Tenant Cloud

Side-channel exploits demonstrated on shared GPU memory hierarchies raise red flags for pharmaceutical and semiconductor firms that treat model weights as proprietary IP. Financial institutions managing Basel III capital models hesitate to move to shared clusters without hardware-rooted tenant isolation. Ambiguity around encryption-key custody under cloud shared-responsibility agreements further complicates risk assessments. Enterprises therefore add application-layer encryption or homomorphic techniques that inflate runtime costs and latencies, tempering the migration pace. Regulators have begun drafting sector-specific cloud assurance frameworks, but until hardware vendors ship default tenant-isolation features, the restraint persists.

Shortage of Skilled HPC Software Administrators

The blending of MPI-tuned networks with container orchestration demands talent fluent in both domains, yet universities favour ML-centric curricula, shrinking the pipeline of parallel-computing specialists. Median time-to-hire for senior HPC administrators exceeds six months, forcing enterprises to lean on managed-service providers that charge premium rates for turnkey clusters. The shortage delays hybrid-cloud projects, because few engineers can script job-submission gateways that span on-premises Slurm partitions and cloud Kubernetes pods. Vendors in the high performance computing (HPC) software market respond with no-code portals and “autoscaler” plugins, but the skill gap remains a drag on adoption until training programs realign.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Configurations Reconcile Latency and Elasticity

Hybrid deployments account for the fastest growth trajectory at a 8.82% CAGR, pairing on-premises clusters for latency-critical CFD with cloud bursts for Monte Carlo sweeps. Enterprises integrate Slurm cloud-burst plugins or Azure CycleCloud’s on-premises node federation, creating a unified queue that masks infrastructure boundaries. Authentication hurdles lessen as AWS Direct Connect and Active Directory federation allow consistent credential handling, reducing deployment friction. Organizations size owned hardware to average utilization and burst peaks to cloud, shrinking idle capital and smoothing operating budgets.

Hybrid adoption also advances compliance goals because sensitive data reside on dedicated racks while transient workloads exploit elasticity elsewhere, satisfying ISO 27001 audits. Data-transfer bottlenecks persist for tightly coupled I/O, but emerging cache-coherent file systems mitigate latency penalties. As regional spot markets widen, schedulers weigh network egress fees against queue times, routing jobs to the cheapest geography that still meets SLAs. Consequently, the high performance computing (HPC) software market embeds dynamic cost-forecast modules directly in job submission dashboards, letting users preview spend before launch.

By Software Category: Data Management Overtakes Schedulers in Growth Velocity

Schedulers remain foundational, yet their 28.41% share in 2025 grows modestly because open-source versions cap monetization. In contrast, data management and file systems post a 9.26% CAGR as genomics and real-time inference push read-write throughput toward multi-terabytes per second. WekaFS, with NVMe-over-Fabrics, marries SSD performance to object-store economics, securing deals at cryo-EM labs that previously maxed out traditional parallel file systems.

As clusters stretch across cloud regions, global-namespace file systems and license consumption monitors become indispensable, prompting vendors to bundle telemetry engines that correlate cost and performance. Middleware libraries, though commoditized by OpenMPI, still generate maintenance revenue where validated code stacks preclude version drift. Application software, locked into decades of validated simulations, pursues subscription models that integrate with cloud marketplace billing. Across categories, vendors weave energy-aware features and compliance hooks to differentiate, underscoring the HPC software market’s shift from raw performance to policy-driven value.

By Service Model: SaaS Abstracts Operational Complexity for Premium Margins

HPC software-as-a-service is growing at 8.76% CAGR through 2031 because it eliminates the scheduler expertise barrier. Platforms such as Rescale wrap job submission in browser forms, spot-bid automatically, and archive outputs, charging only for consumed compute minutes. In contrast, infrastructure-as-a-service, which captured 41.29% revenue share in 2025, suits enterprises with in-house teams capable of compiling custom toolchains and tuning network fabrics.

Platform-as-a-service splits the difference, bundling compilers and libraries but leaving queue management to users; it appeals to research labs migrating from grant-funded clusters to cloud credits. Managed services target regulated industries that require SLA-backed uptime and compliance audits, embedding policy engines that enforce data localization automatically. Consumption-based billing shields CFOs from surprise overruns because dashboards expose projected cost before job launch. As marketplace listings proliferate, vendor competition centers on security certifications, compliance reports, and localized payment options.

By End-User Industry: Life Sciences Accelerates on Structure Prediction Breakthroughs

Life sciences and healthcare are on track for a 9.55% CAGR courtesy of AlphaFold3, which slashed in silico screening times and spawned new pipelines for protein-ligand docking. Whole-genome initiatives like UK Biobank pour exabytes into variant-calling workflows parallelized across thousands of nodes, sustaining demand for high-throughput file systems. Aerospace and defense, while commanding 19.63% of 2025 spend, grow more modestly due to budget cycles and export-control compliance.

Banking and financial services employ HPC for real-time risk analytics but tread cautiously on cloud migrations until encryption and audit solutions mature. Energy companies run reservoir simulations on tightly coupled GPU clusters and adopt carbon-aware schedulers to align with emissions-reduction targets. Manufacturing relies on generative-design loops that spike compute needs irregularly, making pay-per-use SaaS attractive. Academic and government users gravitate toward open-source stacks to fit constrained budgets, yet rely on commercial support for compliance verification.

By Organization Size: Medium Enterprises Exploit Open-Source Economics

Large enterprises retained 64.89% of revenue in 2025 owing to global HPC centers and volume-discounted licenses. Yet medium enterprises enjoy the fastest climb at 8.95% CAGR because Slurm’s zero-license model and containerized stacks wipe out six-figure entry costs. Community forums, GitHub recipes, and cloud vendor credits let R&D-heavy firms spin up 100-node clusters without hiring dedicated admins.

Small enterprises embrace HPC SaaS to sidestep any infrastructure management, turning compute into a metered utility. Venture capital flows tilt toward startups that embed HPC workloads directly into drug discovery or materials modelling, confident that elastic capacity removes hardware constraints. The democratization effect fuels broader software consumption: performance monitors, cost analyzers, and license trackers become must-have add-ons as cluster counts rise.

Geography Analysis

Asia Pacific records the steepest trajectory at a 9.06% CAGR through 2031, driven by state-funded sovereign AI programs in China, India, and Japan. China’s 14th Five-Year Plan backs indigenous operating systems and MPI libraries to circumvent export controls, spawning a localized software ecosystem that plugs directly into exascale builds. India’s National Supercomputing Mission deploys middleware that enforces data-residency rules, creating a captive buyer base for domestically maintained schedulers. Japan’s ARM-based Fugaku success galvanizes compiler and library vendors to optimize for non-x86 silicon, broadening platform diversity.

North America, holding 38.92% share in 2025, benefits from hyperscale scale economies and defense procurement but shows moderating growth as enterprises optimize existing reservations rather than expanding footprints. Sovereign clouds within the United States carve new niches for compliance-centric workloads, yet Neocloud entrants siphon overflow demand via GPU-hour discounts. Europe’s policy landscape mandates auditable software layers and carbon-aware operations, pushing vendors to certify compliance with both the Cyber Resilience Act and Energy Efficiency Directive.

The Middle East and Africa leverage petrodollar-funded AI clusters to diversify economies, contracting Neocloud partners for capacity until domestic data centers scale. South America’s academic consortia pioneer open-source adoption but face intermittent funding, relying on regional cloud credits for burst capacity. Across all regions, the high performance computing (HPC) software market embeds language packs, localized billing, and regional data-residency toggles to meet country-specific procurement clauses.

Regulatory Landscape

High performance computing (HPC) software vendors and operators face a tightening set of constraints at the intersection of export controls, AI governance, and sovereignty requirements, which increasingly shape where clusters can be built and how orchestration layers are configured. In the United States, the Bureau of Industry and Security (BIS) has continued to refine advanced computing and supercomputer controls through rules and guidance spanning April 2024 and January 2025 actions. May 2026 guidance clarified licensing triggers tied not only to destination, but also to the headquarters or ultimate parent location of entities associated with Country Group D:5 or Macau. These measures affect procurement, feature availability, and compliance workflows for GPU-centric HPC environments used for AI training and simulation.

In Europe, the EU AI Act introduces horizontal obligations for high-risk AI systems, with an August 2026 enforcement milestone for key high-risk requirements. Buyers are therefore pressing vendors for stronger documentation, traceability, and governance capabilities across the HPC software stack. For global deployments, the practical outcome is a more explicit need for region-aware software configuration, auditable controls, and policy-driven segmentation in hybrid and multi-tenant environments, as organizations reconcile US ECCN-driven controls with EU-wide AI governance requirements.

Competitive Landscape

Competition is moderate, with no single vendor exceeding a monopolistic footprint, yet pockets of high concentration emerge around CUDA and Slurm. NVIDIA’s CUDA toolchain enjoys entrenched loyalty, but open alternatives like ROCm and oneAPI lure cross-vendor portability seekers. Slurm’s presence on over 60% of TOP500 machines creates network effects that deter migrations, especially where administrator skills and scripts have ossified over years. Hyperscalers layer proprietary cost-optimization APIs atop open schedulers, capturing value while keeping exit costs low for customers.

Neocloud providers differentiate by shipping orchestration features ahead of hyperscalers, such as per-second GPU billing and real-time zone arbitrage. Legacy simulation vendors defend margins by wading into SaaS, integrating license metering and browser-based CAD connectors. Energy-aware scheduling and compliance automation represent white-space opportunities because few commercial suites deliver out-of-the-box support despite demonstrated cost savings. Patent filings for GPU-aware bin-packing and containerized MPI rose 40% in 2024, underscoring a pivot from hardware differentiation to algorithmic optimization.

Strategic moves illustrate the shift in the high performance computing (HPC) software market: Microsoft Azure’s HBv4 launch pairs high-core AMD silicon with Slurm cost optimizers; HPE’s Juniper buy marries AI-native networking to Cray software stacks; and Dell’s liquid-cooled XE9680 servers integrate Bright Cluster Manager to tame 700-watt GPUs. Each underscores that hardware launches now arrive bundled with management software tuned to shrink time-to-value.

High Performance Computing (HPC) Software Industry Leaders

Dell EMC

Hewlett Packard Enterprise Development LP

IBM Corporation

Intel Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Sovereign compute buildouts and AI-centered public programs are driving near-term procurement activity for schedulers, data management, and governance layers that can operate across heterogeneous, multi-tenant environments. In April 2026, the Government of Canada opened applications for its AI Sovereign Compute Infrastructure Program (funded via Budget 2024 and 2025) to build large-scale, AI-optimized HPC systems. In parallel, the UK government funded compute expansions including the Cambridge supercomputing center upgrade (announced January 2026, operational in Spring 2026) and the UK Atomic Energy Authority Sunrise AI supercomputer at Culham (45 million GBP announced March 2026, targeted to begin operations in June 2026). Together, these initiatives increase demand for software supporting secure partitioning, usage tracking, and compliance-ready operations across national facilities and affiliated research ecosystems.

Vendor roadmaps are also converging HPC and AI operations around containerized, hybrid-capable environments, creating room for tooling that reduces administrator burden while improving cost and power governance. In June 2026, Siemens Digital Industries Software released HPCWorks 2026.1, adding enhanced GPU scheduling and hybrid scaling, along with cost-control integration via HPCWorks Navops. Around the same period, HPE introduced Supercomputing Programming Software to unify vendor and open-source tools in a containerized programming environment, and it highlighted multi-tenancy-oriented Slingshot 400 software updates. These moves point to opportunities in license-aware scheduling, data management for multi-terabyte checkpoint and analytics workflows, and compliance modules that codify residency, audit logging, and tenant isolation across cloud, on-premises, and hybrid HPC.

Recent Industry Developments

- June 2026: Dell Technologies expanded its Dell AI Factory with NVIDIA portfolio with new PowerEdge platforms positioned for supercomputing-class HPC and AI workloads, including systems aligned to NVIDIA Vera CPU and Vera Rubin roadmaps. The releases tie compute platforms to higher-level stack integration needs, increasing demand for workload management, storage orchestration, and cost governance software that can scale across GPU-dense configurations.

- March 2026: HPE unveiled next-generation AI factory and supercomputing advancements with NVIDIA, including support for NVIDIA Mission Control for workload orchestration. The move reinforces a shift toward integrated, software-defined operations across AI and HPC environments, where scheduling, policy enforcement, and multi-tenant controls become key differentiators for enterprise and public-sector deployments.

- September 2024: Hewlett Packard Enterprise finalized its acquisition of Juniper Networks, aiming to converge AI-native networking with Cray supercomputing stacks. The transaction strengthened HPEs ability to deliver tighter integration between network fabrics and HPC software, supporting features such as performance isolation and automation that are increasingly required for large, shared clusters.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers software revenue from tools used to run, manage, develop, and optimize high performance computing workloads, across on-premises and cloud deployments. The scope includes core layers that show up in HPC environments, such as operating systems, development tools, system management, and virtualization.

Scope exclusions: Hardware systems, networking equipment, and standalone data center infrastructure spending are excluded unless the spending is packaged as software revenue.

Segmentation Overview

- By Deployment Type

- On-Premise

- Cloud

- Hybrid

- By Software Category

- Workload Managers and Schedulers

- Middleware and Libraries

- Application Software

- Performance Monitoring and Analytics

- License and Cost Management

- Data Management and File Systems

- By Service Model

- HPC IaaS

- HPC PaaS

- HPC SaaS

- Managed Services

- By End-User Industry

- Aerospace and Defense

- BFSI

- Energy and Utilities

- Life Sciences and Healthcare

- Manufacturing

- Media and Entertainment

- Academic and Research Institutions

- Government

- By Organization Size

- Large Enterprises

- Medium Enterprises

- Small Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Benelux

- Nordics

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East

- Turkey

- Israel

- GCC

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

For scoping and context, we start with public and official references that explain where HPC demand is coming from and how IT spending shifts by geography. Common inputs include indicators and releases from sources such as the World Bank, OECD, the International Telecommunication Union, national statistics offices, and national science and research funding agencies, alongside publications from supercomputing centers.

We also review company filings, earnings transcripts, investor presentations, product documentation, and reputed press coverage to understand pricing models, licensing terms, and how providers describe cloud adoption. Where it helps with validation, paid databases are used for company financials and news screening, patent databases for software innovation signals, and shipment-level import and export databases to cross-check related infrastructure activity. These desk sources are not exhaustive, and multiple additional references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what is counted as HPC software revenue and what is treated as adjacent spend, especially when cloud and managed models blur category lines. We speak with software publishers, cloud and managed HPC providers, channel partners, and enterprise users across APAC, EMEA, and the Americas, then we re-check key assumptions when responses conflict or when the implied numbers move sharply.

The respondent input is used to tighten boundary rules on items that are sometimes bundled in commercial agreements, and to confirm deployment mix assumptions for the modeling step.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | APAC: 49% |

| Mid tier: 46% | Functional/Unit leaders: 26% | EMEA: 32% |

| Smaller Players: 18% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down approach where enterprise IT and research computing spend is translated into an HPC-software demand pool using adoption and mix indicators, then the pool is filtered by deployment. After the demand pool is established, it is split using market fingerprints such as cloud versus on-premises workload share, licensing versus subscription mix, the intensity of AI plus simulation workloads, and the pace of cluster upgrades that drive software refresh cycles.

Those totals are corroborated with selective bottom-up approximations, including sampled vendor revenue splits, channel feedback on average contract values, and user-side checks on seats or nodes covered under software agreements. When visibility is uneven in a region or category, gaps are handled through proxy variables such as research funding direction, cloud region expansion signals, and enterprise cloud migration progress, and then the assumptions are pressure-tested again through expert feedback. For forecasting, scenario analysis is used with a base case guided by interview consensus on cloud adoption, subscription conversion, and budget outlooks, followed by conservative and aggressive cases to frame downside and upside.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including technology spending indicators, public research funding direction, and observed shifts in cloud consumption models. Variances are flagged when growth rates, deployment splits, or regional shares drift away from what expert inputs and public indicators imply, and then the drivers are adjusted before sign-off.

A second analyst review is completed to confirm scope logic, math consistency, and year-over-year reasonableness, followed by targeted re-contact when a key input changes or when conflicts remain. Reports are refreshed annually, with interim updates when material events affect pricing, deployment behavior, or demand timing. Before delivery, an analyst performs a final pass so clients receive the latest updated view.

Mordor Intelligence's High Performance Computing Software Market Estimate Compared With Other Published Estimates

Published market values for HPC software can appear far apart, even when the topic sounds identical. The gaps usually come from what is counted as software revenue versus services, how cloud HPC usage fees are treated, and whether adjacent platform spend is blended into the number.

The table shows a spread that is mainly explained by scope and counting rules, and then by timing choices such as base-year currency conversion and how frequently assumptions are refreshed. The most common difference is whether managed HPC and support services are added into software totals, which can lift the value even if end demand has not changed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 35.32 B (2025) | |

| Global Research Group A | USD 48.87 B (2025) | Uses a wider revenue pool that blends software with adjacent services and packaged solution revenue, which lifts the base-year total even before growth assumptions are applied. |

| Industry Publisher B | USD 33.10 B (2025) | Presents software alongside service splits and mixed component totals in parts of the sizing, which can reduce the standalone software value when revenue is reallocated across components. |

The table points to scope as the main driver behind the difference, and in Mordor Intelligence's model, only software categories such as workload managers and schedulers, middleware and libraries, application software, performance monitoring and analytics, license and cost management, and data management and file systems are counted, with services kept separate from the software total. This keeps the number traceable to clear software revenue lines, and it also makes year-to-year changes easier to explain with consistent deployment and pricing assumptions.

Key Questions Answered in the Report

How fast is the HPC software market expected to grow?

The HPC software market is projected to expand from USD 38.51 billion in 2026 to USD 57.31 billion by 2031, reflecting an 8.28% CAGR.

Which deployment model is gaining the most traction?

Hybrid configurations are advancing at a 8.82% CAGR because they balance on-premise latency control with cloud elasticity.

Why are life-science companies investing heavily in HPC software?

Protein-structure prediction breakthroughs such as AlphaFold3 have compressed drug-discovery timelines, supporting life sciences and healthcare growth at a 9.55% CAGR through 2031.

What role do neocloud providers play in the current landscape?

GPU-focused neoclouds like CoreWeave and Lambda offer competitive GPU-hour pricing and specialized orchestration features, expanding overall software demand.

Which region is forecast to be the fastest growing?

Asia Pacific leads with a 9.06% CAGR, buoyed by sovereign AI programs and large-scale national supercomputing initiatives.

What is the main barrier hindering wider adoption of cloud HPC?

Data-security concerns around multi-tenant GPU clusters and a shortage of administrators skilled in both traditional schedulers and cloud orchestration slow migration.

Page last updated on: