India IT Hardware Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 21.17 Billion |

| Market Size (2026) | USD 22.61 Billion |

| Market Size (2031) | USD 31.39 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

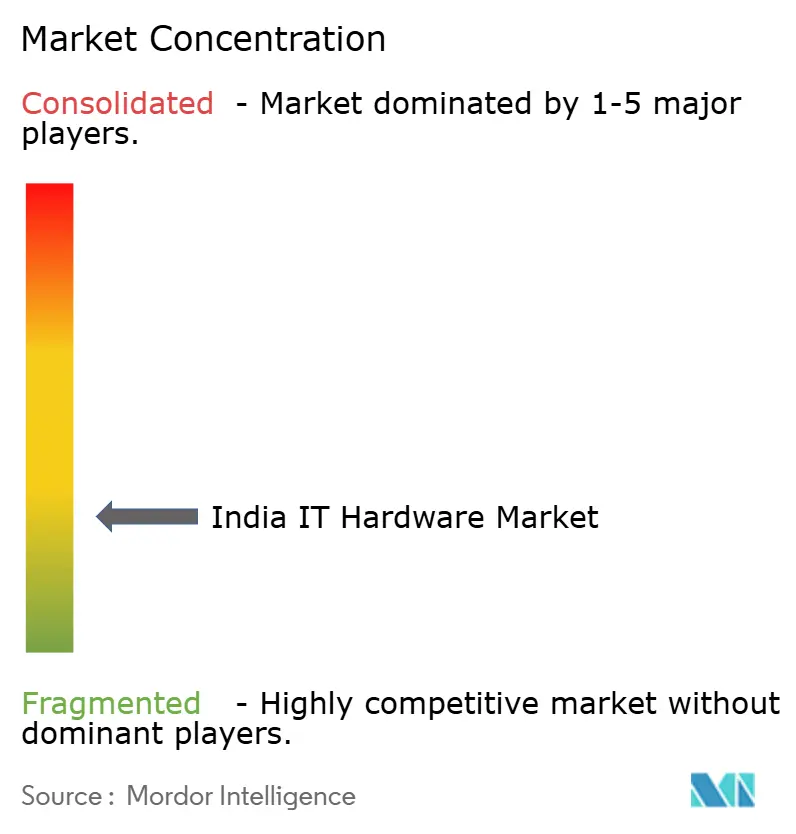

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India IT Hardware Market Analysis by Mordor Intelligence

India IT Hardware Market size in 2026 is estimated at USD 22.61 billion, growing from 2025 value of USD 21.17 billion with 2031 projections showing USD 31.39 billion, growing at 6.78% CAGR over 2026-2031. The growth path reflects rising enterprise digitization, persistent hybrid-work demand, and policy-led incentives that are localizing production at scale. Government backing through the Production Linked Incentive (PLI) 2.0 program has already attracted investments exceeding INR 1.61 lakh crore (USD 19.3 billion) and enabled electronics output worth INR 14 lakh crore (USD 168 billion).[1]India Semiconductor Mission, “Semicon India 2025,” ism.gov.in Foxconn alone more than doubled its domestic workforce to 80,000 employees and crossed USD 20 billion in India revenue in fiscal 2024-25, demonstrating how contract manufacturers are shifting global supply chains toward India. Edge data-center builds outside the four metros, AI-optimized infrastructure orders from enterprises, and a mandated 5% annual reduction in laptop imports beginning 2025 have further accelerated local demand for servers, storage, and PCs. Supply-chain resilience is emerging as a strategic differentiator as indigenous alliances, such as Tata Electronics’ tie-up with Powerchip Semiconductor Manufacturing Corporation and Himax Technologies, reduce the current 60-65% import dependence for display components.

Key Report Takeaways

- By product type, PCs and workstations maintained a 42.08% share trajectory, whereas enterprise storage captured 8.08% CAGR growth leadership through 2031.

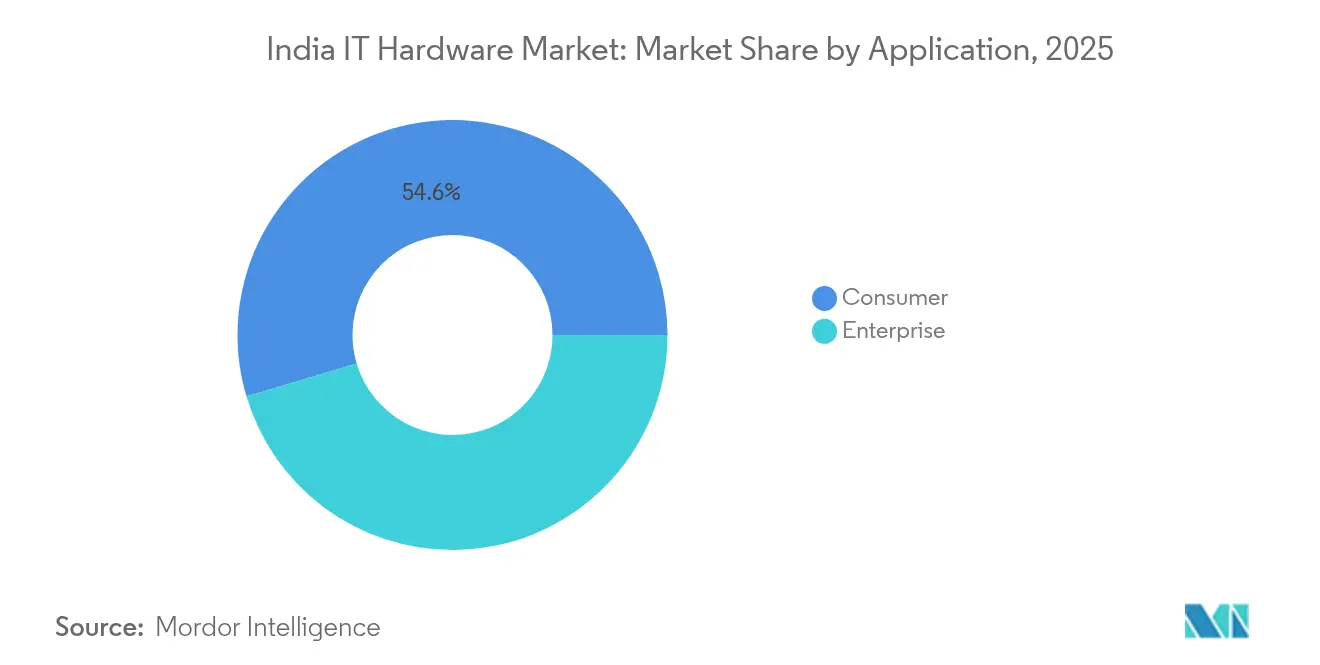

- By application, consumer retained the 54.62% revenue share of the India IT Hardware market size in 2025, whereas enterprise accounted for the fastest expansion at 7.65% CAGR through 2031.

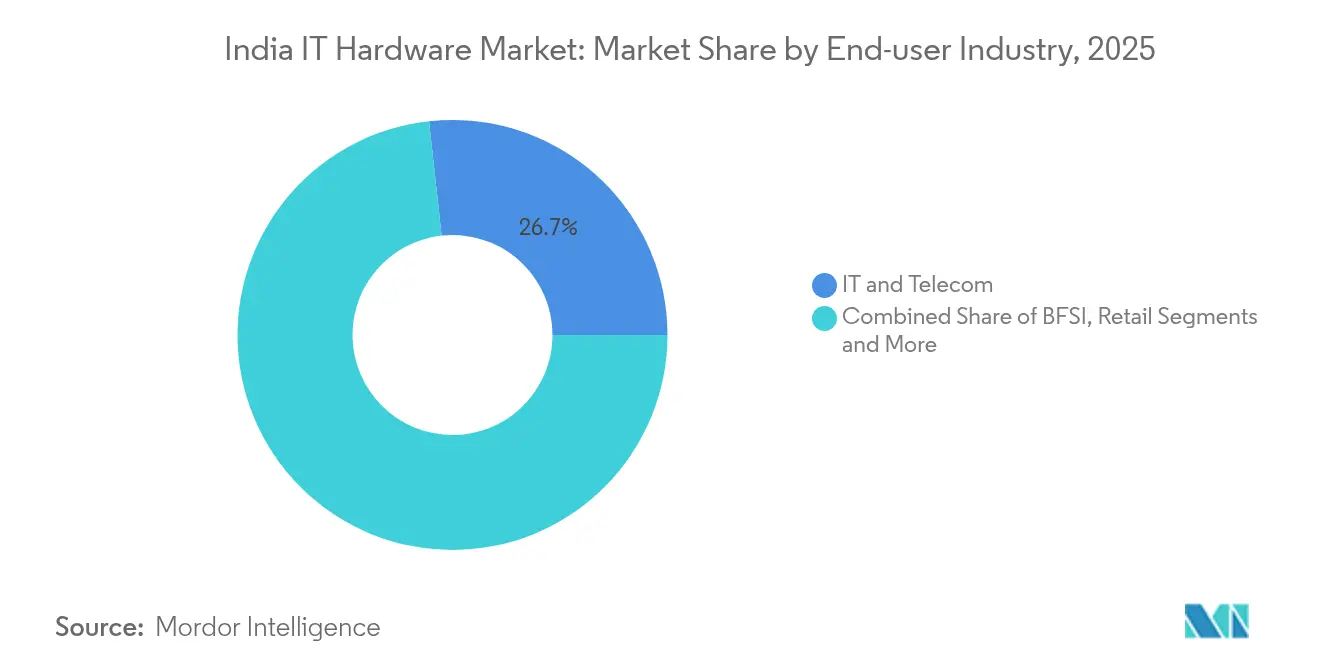

- By end-user industry, IT and Telecom held a 26.74% share of the India IT Hardware market size in 2025, whereas retail recorded the highest 7.12% CAGR through 2031.

- By region, South India led with 42.70% of the India IT Hardware market share in 2025, whereas East India commanded 8.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on it hardware market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India IT Hardware Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in laptop demand under hybrid-work policies | + 1.1% | National, with concentration in metros and Tier-1 cities | Short term (≤ 2 years) |

| Elevated need for high-performance computing in AI workloads | +1.3% | National, with early gains in Bangalore, Hyderabad, Chennai | Medium term (2-4 years) |

| Public-sector digitization push via Digital India and NIC projects | +0.9% | National, with focus on rural and semi-urban areas | Long term (≥ 4 years) |

| Make-in-India incentives for local PC/server manufacturing (PLI 2.0) | +1.0% | South India, West India with spillover to North India | Medium term (2-4 years) |

| Rising demand for edge data-centre servers in Tier-2 cities | +0.6% | Tier-2 cities across all regions | Medium term (2-4 years) |

| Corporate ESG mandates favour energy-efficient hardware | +0.4% | National, with early adoption in large enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Need for High-Performance Computing in AI Workloads

Enterprise AI projects require 3-5 times more compute capacity than traditional applications, pushing firms to specify accelerators, advanced memory, and liquid cooling even for mid-range racks. Dell Technologies projects USD 15 billion in AI server revenue in fiscal 2025, up from USD 10 billion a year earlier.[2]Joseph Kovar, “NetApp Leads AI Innovation,” crn.com Ola’s partnership with Lenovo to build Krutrim 3, a 700-billion-parameter model, necessitates India’s largest supercomputer and an initial INR 2,000 crore (USD 240 million) hardware outlay. Such flagship deployments set procurement baselines that ripple into Tier-2 enterprises, increasing the India IT Hardware market’s average selling price and shifting vendor roadmaps toward purpose-built AI nodes.

Make-in-India Incentives for Local PC/Server Manufacturing (PLI 2.0)

The PLI framework offers 4-6% incremental incentive on net incremental sales of locally manufactured PCs and servers, encouraging global OEMs to relocate higher-value assembly lines. Dixon Technologies invested USD 115 million in Tamil Nadu to manufacture HP notebooks, with output slated at 2 million laptops annually. Lenovo targets 100% local PC production and plans to assemble AI servers domestically, cutting a USD 10.1 billion laptop import bill that previously constrained foreign-exchange reserves. Early localization also seeds ancillary component ecosystems. Foxconn has committed USD 1 billion for display module assembly in Tamil Nadu, reducing dependence on East Asian imports.

Public-Sector Digitization Push via Digital India and NIC Projects

Government buying criteria now emphasize total cost of ownership, local value addition, and long-term service reliability over lowest upfront bids. The INR 15,000 crore (USD 1.8 billion) TCS-BSNL program to establish four hyperscale data centers illustrates how procurement volumes for servers, storage, and networking migrate toward vendors with domestic manufacturing credentials. IBM’s new Lucknow lab, focusing on Generative and Agentic AI, deepens regional skills, attracting hardware suppliers that bundle integrated AI stacks. These projects accelerate refresh cycles in state departments and public sector enterprises, sustaining demand for ruggedized devices and edge servers engineered for India’s power and climate realities.

Rising Demand for Edge Data-Center Servers in Tier-2 Cities

India’s installed data-center capacity is expected to rise from 950 MW in 2024 to 1,800 MW by 2026, with 30% of new racks landing in Tier-2 cities. CtrlS committed INR 400 crore (USD 48 million) for a Patna edge facility designed for low-latency workloads serving Bihar and neighboring states, indicating that proximity computing is moving beyond metro clusters. OEMs are responding with compact, dust-resistant chassis and advanced telemetry for unmanned sites, opening new product adjacencies in KVM-less management modules and battery-free UPS hardware. The pivot expands the India IT Hardware market’s addressable base by tapping enterprises previously limited by latency and bandwidth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating e-waste compliance costs | -0.6% | National, with higher impact in manufacturing hubs | Short term (≤ 2 years) |

| Semiconductor supply-chain volatility | -0.9% | National, with critical impact on assembly operations | Medium term (2-4 years) |

| Persistent grey-market imports in peripherals | -0.4% | National, with concentration in urban markets | Short term (≤ 2 years) |

| Slow enterprise refresh cycles in public-sector tenders | -0.5% | National, with focus on government and PSU segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Volatility

India still imports 65-70% of its semiconductors, exposing manufacturers to volatile DRAM and NAND pricing that rose 15-20% over 2024-25.[3]Ankita Garg, “India’s first homegrown semiconductor chip by 2025,” indiatoday.in Local fabrication will not ship commercial wafers until Tata-PSMC’s Gujarat fab comes online in late 2025, prompting OEMs to hold larger safety stocks and hedge currency in component sourcing. High-performance GPUs remain the tightest node, stretching lead times to 52-60 weeks and stalling AI server rollouts. The bottleneck inflates working capital needs and dampens margin profiles, carving 90 basis points off the projected India IT Hardware market CAGR.

Escalating E-Waste Compliance Costs

Formal recyclers handle only 16-43% of India’s 3.8-4.1 million MT annual e-waste stream, pushing regulators to raise Extended Producer Responsibility (EPR) surcharges to INR 22 per kg for consumer electronics and INR 34 per kg for smartphones. Compliance now adds 2-8% to unit production costs, especially painful for contract assemblers running low-margin consumer hardware lines. OEMs must fund collection centers or partner with recyclers whose capacity remains limited in Tier-2 cities, elevating logistics complexity and offsetting part of the PLI incentive gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enterprise Storage Drives AI Infrastructure Boom

Enterprise storage accounted for the fastest 8.08% CAGR through 2031 as enterprises deployed AI-optimized arrays and NVMe-over-Fabrics architectures. NetApp’s hybrid-cloud revenue reached USD 5.66 billion in fiscal 2024, and its AIPod reference design became a blueprint for domestic data-center upgrades. Servers followed at 7.18% CAGR, fueled by edge deployments and public-sector demand. PCs and workstations maintained a 6.94% CAGR, buttressed by hybrid-work refreshes. The India IT Hardware market size for enterprise storage represented a significant share, while PCs retained 42.08% of the India IT Hardware market share. Printers and copiers trailed, reflecting digital document workflows and cloud forms adoption. Vendors integrated AI-inference accelerators inside notebooks to protect ASPs, signaling the convergence of client and server design philosophies.

The evolution also reshaped value chains. Component suppliers focusing on PCIe 5.0 controllers and CXL-ready DIMMs secured longer-term orders as hyperscalers demanded deterministic latency. Networking hardware pivoted toward software-defined overlays, cannibalizing traditional chassis switch revenues but opening opportunities in secure SD-WAN appliances tuned for branch edge. The shift enlarged the India IT Hardware market as consumption moved from capex purchases to hybrid device-plus-subscription bundles.

By Application: Consumer Dominance Meets Enterprise Acceleration

Consumer applications commanded a 54.62% share, underscoring India's swift embrace of technology, spurred by hybrid work models and a push for digital education. This consumer segment's lead is bolstered by India's youthful demographic, boasting over 600 million smartphone users, which in turn fuels a robust demand for related hardware like laptops, tablets, and peripherals. Thanks to PLI scheme incentives, device costs have dropped, and local availability has surged. Notably, HP has rolled out competitively priced AI-enhanced laptops, integrated with Microsoft Copilot, starting at INR 99,999 (USD 1,200). Meanwhile, enterprise applications are on a rapid ascent, projected to grow at a 7.65% CAGR through 2031, fueled by corporate shifts towards digitalization and hefty investments in AI infrastructure.

By End-user Industry: Retail Transformation Leads Hardware Adoption

Retail led with a 7.12% CAGR as omnichannel pivots forced chains to install IoT-enabled shelves, AI checkout kiosks, and real-time inventory servers. Roughly 80% of medium-sized retailers plan to expand AI-based analytics in 2025, translating to orders for GPU-enabled edge appliances and handheld scanners. IT and Telecom followed at 7.01% CAGR, powered by 5G rollouts and network-core modernizations; Airtel and Jio earmarked USD 2 billion for equipment upgrades. BFSI trailed at 6.88% CAGR, still substantial due to RBI compliance and digital-banking pushes. Other verticals, including manufacturing and healthcare, are provisioning IoT gateways and rugged tablets for shop-floor analytics, broadening hardware SKUs sold into non-traditional segments, and deepening the India IT Hardware market footprint.

Geography Analysis

South India continues to anchor manufacturing, bolstered by cumulative commitments exceeding INR 10 lakh crore (USD 120 billion) since 2021. Tamil Nadu’s electronics policy offers 30% capital subsidies, helping Dixon and Pegatron accelerate laptop and smartphone lines. Bengaluru hosts the highest concentration of AI chip design centers, ensuring local access to specialized talent that shortens product-development lifecycles. Contracts such as Foxconn’s iPhone enclosure project at Oragadam Industrial Park extend value capture beyond final assembly into precision machining.

North India’s proximity to federal ministries keeps it central to public-sector spending. The Digital India e-Governance stack is expected to award over USD 3 billion in IT hardware tenders between 2025-27, including rugged tablets for field-level agencies. IBM’s Lucknow lab gives the state its first Fortune 500 R&D center focused on Generative AI, drawing peripheral hardware suppliers seeking co-design opportunities. Data localization rules enacted in 2025 further stimulate server installations in NCR colocation sites.

East India’s rise hinges on strategic logistics routes to Southeast Asia via Kolkata port and the upcoming deep-sea terminal at Dhamra. CtrlS’s Patna edge facility, built to Tier-4 standards, exemplifies how lower-cost real estate offsets transmission-loss overheads, enabling hyperscale economics outside traditional hubs. State-level incentives on stamp duty and power tariffs strengthen the business case for greenfield plants, positioning East India to capture incremental export-oriented orders as China+1 strategies mature.

West and Central India combine industrial demand from auto and petrochemical majors with financial-services IT refreshes in Mumbai. The upcoming Mumbai–Ahmedabad high-speed rail corridor is expected to spur suburban data-center campuses linked via dark fiber, improving redundancy for disaster-recovery sites. Gujarat’s emerging semiconductor cluster around Dholera, led by Tata-PSMC, promises localized wafer supply, mitigating part of the supply-chain volatility by 2027.

Competitive Landscape

The India IT Hardware market remains moderately concentrated. HP, Dell, and Lenovo hold a significant share in PCs, while HPE, Dell, and Cisco lead enterprise servers and networking. HP retained 31.5% of PC unit shipments despite a 6.6% volume decline, demonstrating its pricing latitude in commercial accounts. Global players maintain R&D scale, yet contractual partnerships with Dixon, Foxconn, and Tata Electronics enable faster localization, trimming landed costs by 8-12% and protecting margins against currency swings. Foreign OEMs increasingly cede low-value assembly to domestic EMS partners while focusing on firmware, design, and channel enablement.

Vertical integration is reshaping strategic positions. Tata Electronics’ acquisition of Wistron’s operations, followed by a Himax partnership, extends its reach from chassis to display drivers, advancing toward a silicon-to-systems stack. Foxconn’s diversification into display modules and potential semiconductor back-end operations illustrates similar moves to lock in component security. Lenovo’s intent to assemble AI servers locally gives it a first-mover advantage in premium infrastructure bids, particularly in public-sector HPC clusters.

Disruptive entrants are emerging. Indkal Technologies, licensed to build Acer smartphones, targets the INR 15,000-50,000 (USD 180-600) bracket once dominated by Chinese brands, underscoring how local branding plus manufacturing incentives can upend existing value hierarchies.[5]Gulveen Aulakh, “Indkal licensing pact,” livemint.com Channel ecosystems are consolidating as partners add managed services to offset shrinking margins on hardware alone. Regulatory oversight by the Bureau of Indian Standards and MeitY standardizes quality levels, lowering entry barriers for smaller domestic brands to compete on features rather than mere compliance.

India IT Hardware Industry Leaders

Dell Inc.

Lenovo Group Ltd

ASUS Tek Computer Inc.

HP Inc.

Acer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Foxconn confirmed a Tamil Nadu unit for iPhone enclosures at Oragadam’s ESR Industrial Park, expanding into high-precision component production.

- May 2025: HP India started laptop and desktop manufacturing with Dixon at a Chennai plant capable of 2 million units yearly.

- April 2025: Dixon Technologies committed USD 115 million to a new Tamil Nadu notebook facility expected to hire 5,000 workers.

- April 2025: IBM opened a Generative AI lab in Lucknow, positioning the city as an emerging AI R&D node.

- March 2025: Ola partnered with Lenovo to create India’s largest supercomputer for Krutrim 3, with an INR 2,000 crore initial spend.

India IT Hardware Market Report Scope

Within the realm of technology, hardware encompasses the tangible components that constitute a computer or electronic system. This study specifically monitors the revenue generated from IT hardware sales in India. The scope of IT hardware includes PCs and workstations, networking hardware, servers, and storage devices. The scope of the study focuses on the market analysis of IT hardware across India, and market sizing encompasses the revenue generated through IT hardware sales across India by various market players. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which support the market estimation and growth rates over the forecast period. The study further analyses the industry ecosystem.

The India IT hardware market report is segmented by PC and workstations (end-user [consumer, enterprise [SMEs, large enterprises], and industry [BFSI, retail, IT and telecom, other industries]), by enterprise networking hardware (enterprise [SMEs, and large enterprises] and industry (BFSI, retail, IT and telecom, other industries]), by enterprise storage devices (enterprise [SMEs, large enterprises], industry [BFSI, retail, IT and telecom]), by server (enterprise [SMEs, large enterprises], industry [BFSI, retail, IT and telecom]), by other hardware [includes hard copy peripherals such as printers and copiers], and by region (north India, east India, west and central India, south India). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| PCs and Workstations |

| Enterprise Networking Hardware |

| Enterprise Storage Devices |

| Servers |

| Other Hardware (Printers and Copiers) |

| Consumer | |

| Enterprise | SMEs |

| Large Enterprises |

| BFSI |

| Retail |

| IT and Telecom |

| Other End-user Industries |

| North India |

| East India |

| West and Central India |

| South India |

| By Product Type | PCs and Workstations | |

| Enterprise Networking Hardware | ||

| Enterprise Storage Devices | ||

| Servers | ||

| Other Hardware (Printers and Copiers) | ||

| By Application | Consumer | |

| Enterprise | SMEs | |

| Large Enterprises | ||

| By End-user Industry | BFSI | |

| Retail | ||

| IT and Telecom | ||

| Other End-user Industries | ||

| By Region | North India | |

| East India | ||

| West and Central India | ||

| South India | ||

Key Questions Answered in the Report

What is the current India IT Hardware market size?

The India IT Hardware market size stands at USD 22.61 billion in 2026.

How fast is the India IT Hardware market expected to grow?

The market is projected to expand at a 6.78% CAGR, reaching USD 31.39 billion by 2031.

Which product category shows the highest growth?

Enterprise storage leads with an 8.08% CAGR driven by AI data-center deployments.

How is policy impacting local manufacturing?

PLI 2.0 incentives and a mandated 5% yearly cut in laptop imports are pushing OEMs like HP, Lenovo, and Foxconn to localize high-value assembly lines.

Which region offers the strongest growth prospects?

East India records the highest regional CAGR at 8.25%, supported by new data-center and electronics manufacturing investments.

Page last updated on: