IT Hardware Distribution And Channel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

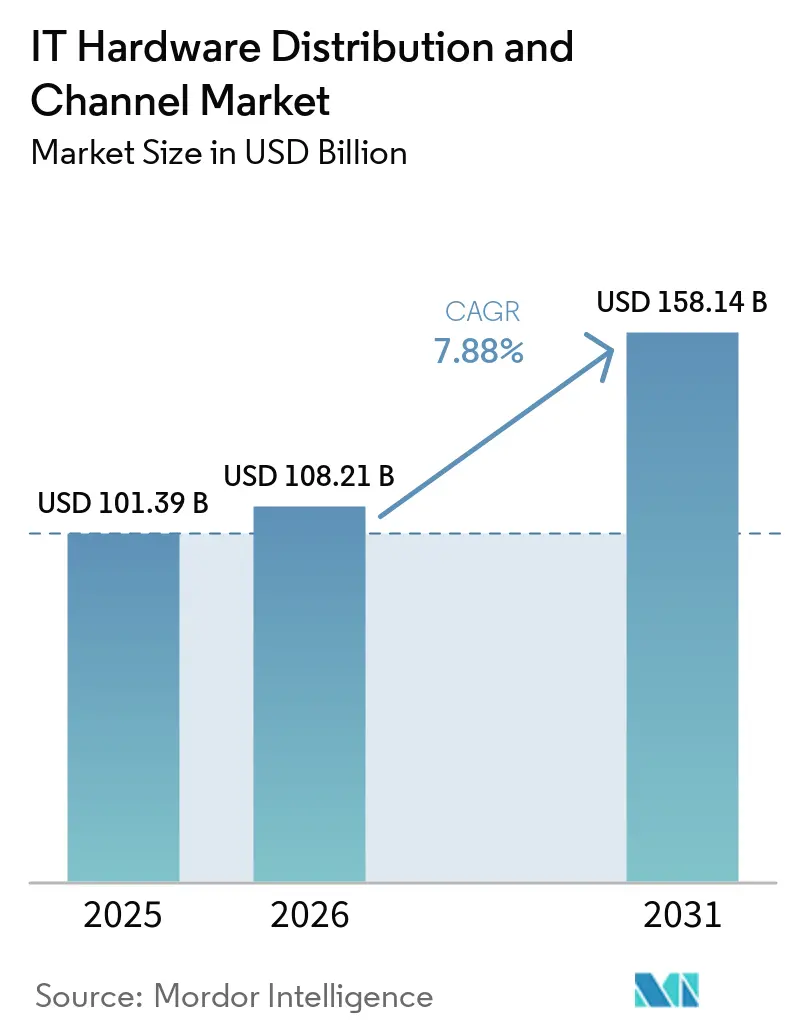

| Market Size (2026) | USD 108.21 Billion |

| Market Size (2031) | USD 158.14 Billion |

| Growth Rate (2026 - 2031) | 7.88% CAGR |

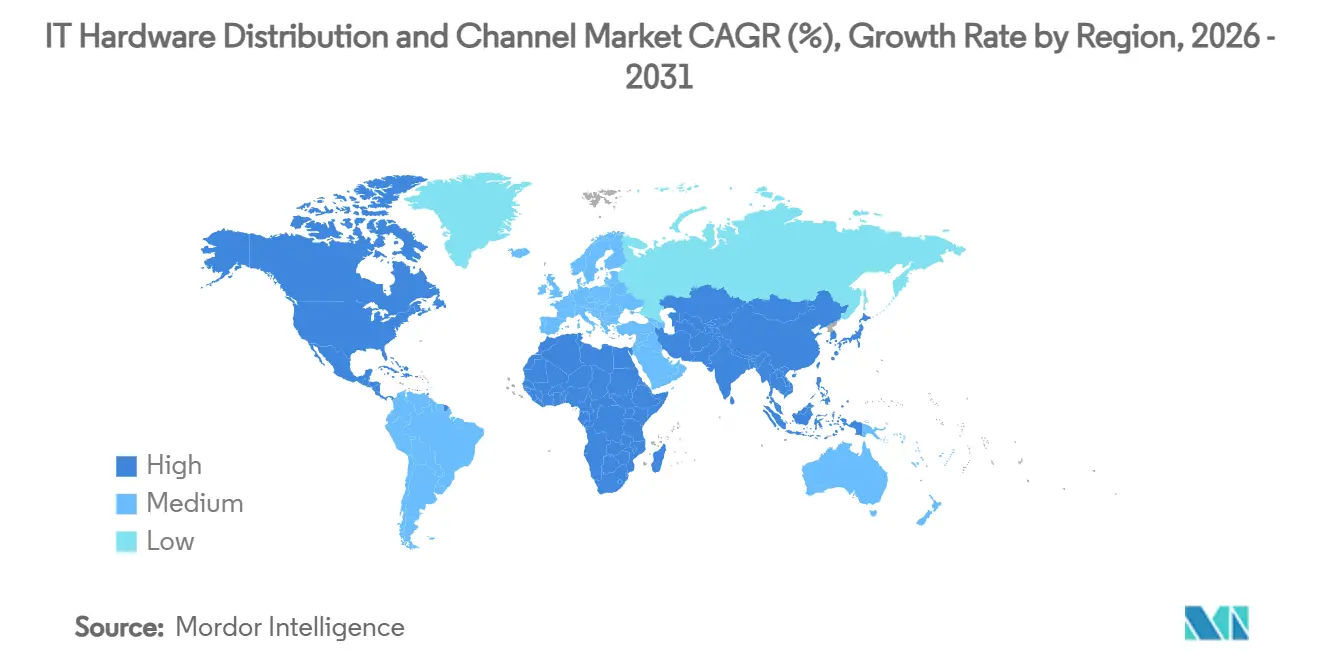

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

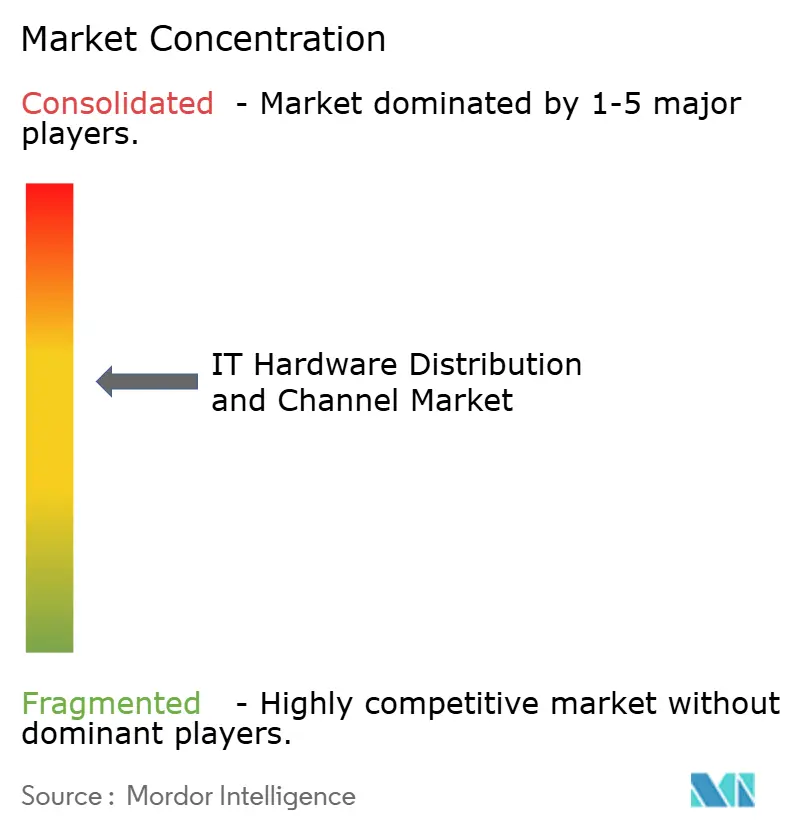

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IT Hardware Distribution And Channel Market Analysis by Mordor Intelligence

The IT hardware distribution market size is expected to increase from USD 101.39 billion in 2025 to USD 108.21 billion in 2026 and reach USD 158.14 billion by 2031, growing at a CAGR of 7.88% over 2026-2031. During the same horizon, cloud and hyperscale buyers are bypassing traditional intermediaries and sourcing directly from original equipment and design manufacturers, shrinking the transactional core of the channel. Distributors that once prospered on volume now pivot toward higher-margin services such as cybersecurity bundling, Device-as-a-Service financing, and reverse logistics, cushioning the impact of OEM disintermediation. Rapid edge-computing adoption creates a fresh layer of demand for ruggedized servers, power-optimized storage, and pre-configured network gear, reinforcing the consultative role of value-added distributors. Meanwhile, procurement teams favor Amazon-like self-service portals, accelerating the shift toward e-commerce storefronts that compress price margins but reward players with deep automation capabilities. Supply-chain volatility, notably the surge in high-bandwidth memory pricing, remains the single largest near-term headwind for the IT hardware distribution market.

Key Report Takeaways

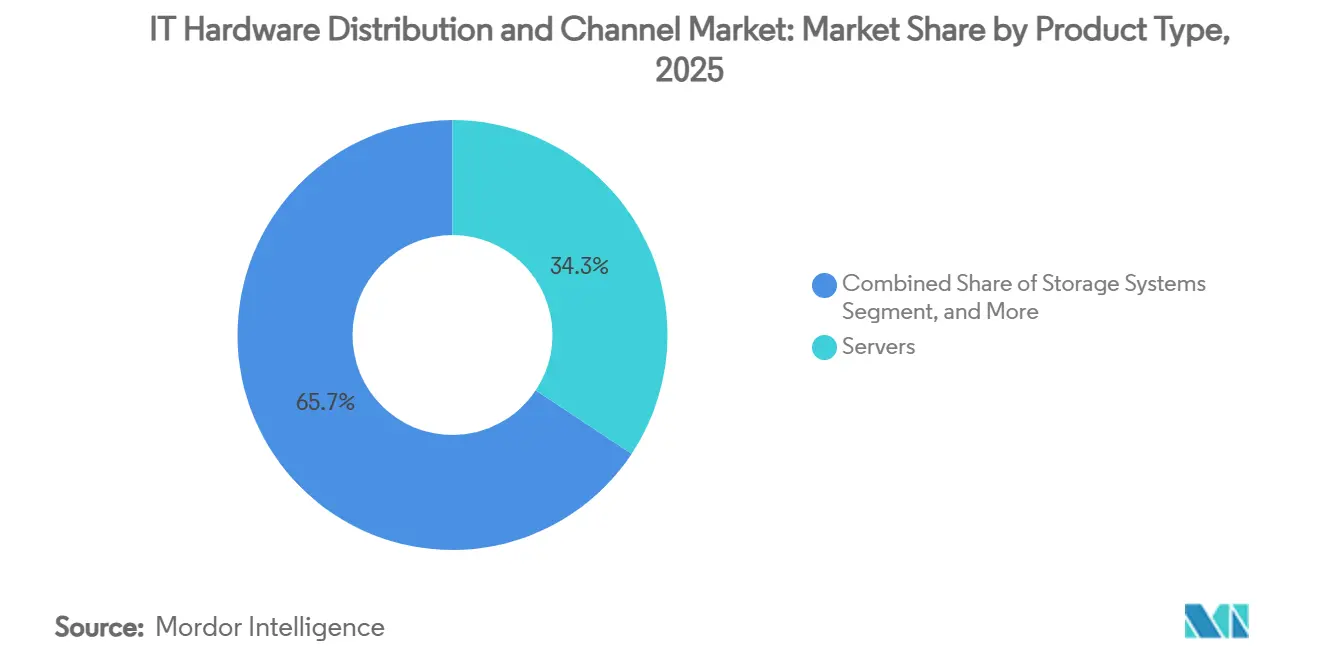

- By product type, servers led with 34.32% revenue share in 2025, while mobility devices are projected to expand at a 9.08% CAGR through 2031.

- By channel type, broadline distributors held 31.28% share in 2025, whereas e-commerce platforms are advancing at a 9.18% CAGR through 2031.

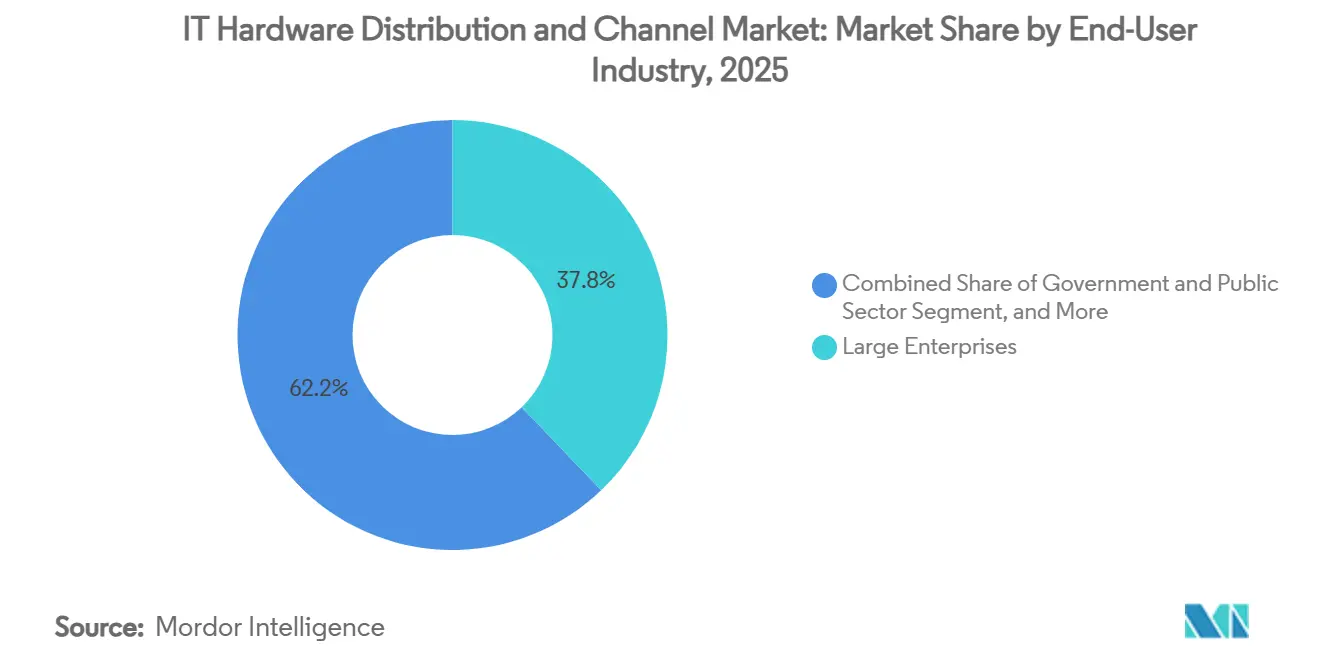

- By end-user vertical, large enterprises commanded 37.84% revenue share in 2025, but cloud service providers are forecast to grow at a 9.36% CAGR through 2031.

- By service model, broadline distribution held a 42.19% share in 2025, while hybrid approaches are set to grow at an 8.68% CAGR over 2026-2031.

- By geography, North America retained a 29.41% share in 2025, whereas Asia-Pacific is anticipated to grow at an 8.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global IT Hardware Distribution And Channel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Cloud Data Center Expansion | +2.1% | Global, highest in North America and Asia-Pacific | Medium term (2-4 years) |

| Increasing Adoption of Edge Computing Infrastructure | +1.3% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Growth of E-Commerce Procurement Channels | +1.0% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Vendor Channel Incentive Programs | +0.9% | Global | Short term (≤ 2 years) |

| Compliance-Driven Boom in Refurbished Hardware Trade | +0.7% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Expansion of Cybersecurity Hardware Bundling by Distributors | +0.6% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cloud Data Center Expansion

Hyperscalers allocated more than USD 600 billion in capital expenditure during 2026, with Amazon, Microsoft, and Google leading multi-region server purchases that often bypass broadline intermediaries. Direct OEM and white-box engagement compresses commodity margins yet opens service adjacencies for distributors that support colocation providers and regional cloud operators. AWS’s USD 12 billion Louisiana buildout underscores the North American concentration of these projects, while India’s 2,070 megawatt pipeline and Japan’s USD 26 billion commitment signal sustained Asia-Pacific momentum. Distributors capable of staging localized inventory, integrating cooling systems, and offering compliance consulting capture incremental revenue despite the trend toward direct sourcing.

Increasing Adoption of Edge Computing Infrastructure

Enterprises are deploying inference nodes in factories, retail stores, and cell towers to reduce latency and cloud egress fees. Edge sites demand NPU-centric servers, E3.S storage, and ruggedized switches that broadline distributors rarely stock at scale, creating white space for niche value-added partners. Margins rise because solutions ship as turnkey bundles that include liquid-cooling modules and orchestration software. Cisco’s 360 Partner Program, launched in 2026, rewards distributors for certifying edge-orchestration engineers, reinforcing technical lock-in. Fragmented vertical requirements favor regional specialists that can customize SKUs and financing in ways global distributors find uneconomical.

Growth of E-Commerce Procurement Channels

Self-service portals now mirror consumer storefronts by offering real-time inventory and automated compliance documentation. Dell’s Premier platform already serves more than 300,000 business buyers, while Ingram Micro’s Xvantage marketplace integrates cloud subscriptions with physical hardware on a single invoice. Although average selling prices remain stable, automated pricing compresses gross margins by as much as 80 basis points, pressuring distributors to layer on configuration, imaging, and asset-tagging services. E-commerce is projected to grow faster than any other channel type through 2031, reinforcing its central role in the future shape of the IT hardware distribution market.

Vendor Channel Incentive Programs

OEMs are countering disintermediation fears by enriching rebate programs that favor solution selling over box moving. HPE’s Partner Ready Vantage tiers and Dell’s New Business Incentives both award incremental points for bundling services or landing green-field enterprise accounts. Cisco’s unified 360 framework streamlines 14 legacy tracks into a single incentive spine, simplifying compliance and hastening payout cycles.[1]Partner Program Office, “Cisco 360 Partner Program Announcement,” Cisco, cisco.com While these rebates improve cash flow, clawback clauses tied to training completion or certification milestones can whipsaw quarterly earnings for smaller partners, underscoring the need for disciplined channel operations management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply-Chain Disruptions | -1.4% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| OEM-Channel Conflict From Direct-to-Customer Sales | -1.1% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Device-as-a-Service Models Curtailing Unit Shipments | -0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| EPR Rules Elevating Asset Take-Back Costs | -0.5% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Disruptions

High-bandwidth memory sold out through year-end 2026, DRAM spot prices nearly doubled in Q1, and 3-nanometer lead times exceeded 50 weeks. OEMs responded with mid-cycle price increases that suppressed enterprise refresh schedules and shaved 120-150 basis points off distributor margins.[2]Investor Relations, “Market Update April 2026,” Dicker Data, dickerdata.com.au Foundry constraints privilege hyperscalers that negotiate direct allocations, leaving channel partners to scour spot markets that add 3%-5% to costs. Distributors with multi-OEM hedging strategies weather price spikes better than peers tethered to single-source pipelines.

OEM-Channel Conflict From Direct-to-Customer Sales

Dell derives roughly 80% of revenue from direct engagements, HP and Lenovo embed financing, imaging, and lifecycle services into Device-as-a-Service contracts, and Apple continues to favor its own retail and online ecosystem. These moves siphon an estimated USD 4-6 billion in annual gross margin away from broadline distributors and force a strategic pivot toward configuration, reverse logistics, and compliance consulting. While occasional OEM retreats, such as Arrow Electronics’ USD 350 million win in Dell's enterprise portfolio, prove the channel’s residual value, the long-run trajectory points to sustained disintermediation pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobility Refresh Surpasses Server Dominance

Server shipments accounted for 34.32% of 2025 revenue, but the segment’s growth rate moderates as hyperscalers source directly, shrinking the distributor addressable base. Mobility devices, in contrast, are forecast to accelerate at 9.08% CAGR through 2031 as enterprises refresh laptops and tablets to enable hybrid work and run on-device AI. The IT hardware distribution market for mobility devices is projected to grow steadily as Windows 11 migration deadlines approach and NPU-equipped notebooks roll out. Distributors protect margins by bundling imaging, asset tagging, and extended warranties, services difficult for OEMs to replicate at scale.

Edge AI workloads spur demand for high-density storage in E3.S form factors, while ruggedized networking hardware remains a distributor staple because enterprises insist on pre-configured firewalls and compliance paperwork. TD SYNNEX’s Hyve Solutions division nearly doubled volume in early 2026 by capturing custom white-box server business from regional cloud operators.[3]Investor Relations, “Q1 FY 2026 Earnings Release,” TD SYNNEX, investors.tdsynnex.com As liquid-cooling and power-efficient GPU racks become mainstream, value-added distributors that employ certified engineers in these technologies enjoy premium pricing. The IT hardware distribution market share for networking gear is further boosted when security appliances, zero-trust gateways, and intrusion detection devices ship as part of integrated bundles.

By Channel Type: E-Commerce Accelerates At The Expense Of Broadline

Broadline distributors accounted for 31.28% of 2025 revenue but face gross-margin erosion as clients migrate to click-to-quote portals. E-commerce storefronts, growing at 9.18% CAGR, meet buyer expectations for instant availability and automated compliance. Ingram Micro’s Xvantage stacks SaaS subscriptions on top of physical hardware, while Dell’s Premier platform already processes hundreds of thousands of corporate transactions daily.

Value-added distributors carve out defensible niches by embedding configuration labs, staging centers, and financing desks, reducing the impact of price transparency. System integrators capture multi-million-dollar projects in which hardware accounts for less than half of the total bill, yet channel control remains critical for warranty and lifecycle services. Retail continues its secular decline, though specialty chains that offer same-day pickup and technical support retain loyal small-business customers. The hybrid blend of broadline inventory and value-added expertise gains traction, signaling an adaptive future for the IT hardware distribution market.

By End-User Vertical: Cloud Growth Outruns Enterprise Steadiness

Large enterprises accounted for 37.84% of 2025 channel revenue, but their shift toward subscription consumption narrows the volume of units purchased outright. Cloud service providers, expanding at a 9.36% CAGR, funnel massive orders directly to OEMs, yet distributors still gain revenue by servicing tier-two colocation and regional cloud players. The IT hardware distribution market for small and medium businesses remains resilient because these buyers lack the scale for direct sourcing and lean on distributors for financing and support.

Government demand is cyclical and compliance-heavy, rewarding partners that hold FedRAMP, ISO 27001, and data-sovereignty credentials. Telecom operators fuel demand for edge servers and optical transport as 5G and fiber rollouts continue. Consumer expenditure is shifting online, truncating retail shelf space but not eliminating the need for last-mile technical service. Collectively, these trends diversify revenue streams and temper volatility in the IT hardware distribution market.

By Service Model: Hybrid Approaches Gain Ground

Broadline fulfillment accounted for 42.19% of 2025 service-model revenue, yet OEM disintermediation and e-commerce pricing compel distributors to mix catalog volume with consultative services. Hybrid structures are projected to grow at 8.68% CAGR because they combine the scalability of bulk inventory with the margin benefits of engineering, managed services, and compliance consulting. The IT hardware distribution industry increasingly sees partners investing in omnichannel platforms that unify online carts with human-assisted quoting to prevent inventory blind spots.

Ingram Micro’s Microsoft Frontier Distributor status, granted in March 2026, illustrates the value of tying Azure consumption incentives to on-premises infrastructure projects. Arrow Electronics reduced quote-to-cash cycle times by nearly one-fifth after rolling out its omnichannel engine, underscoring the operational upside of automation. Specialist distributors that focus on sectors such as healthcare or financial services win business by navigating unique regulatory frameworks, reinforcing the defensibility of hybrid models.

Geography Analysis

North America retained 29.41% of 2025 revenue, buoyed by hyperscale data-center builds and early adoption of subscription hardware models. The United States dominates spending, yet the direct-sourcing behavior of Amazon, Microsoft, and Google diminishes broadline volumes. Canada benefits from public-sector digitalization and proximity to U.S. inventory hubs, while Mexico gains from nearshoring that raises demand for ruggedized edge gear. Distributors in the region offset margin erosion by layering compliance consulting, reverse logistics, and cloud marketplace integration.

Asia-Pacific is set to grow at an 8.88% CAGR, the fastest globally. India plans to build 52 new data center facilities totaling 2,070 megawatts by 2029, creating channel opportunities for cooling, power, and compliance bundles. Japan’s USD 26 billion cloud pipeline confronts multi-year power-grid delays, prompting distributors to stock diesel generators and battery arrays. China’s centralized procurement favors domestic OEMs, complicating routes to market for foreign distributors and increasing compliance overhead. South Korea’s semiconductor ecosystem drives demand for clean-room compliant servers, while Australia and New Zealand spend aggressively on security appliances.

Europe faces a unique blend of circular-economy regulation and macroeconomic headwinds. The Right to Repair Directive and stricter WEEE rules increase operating costs by up to 1.8% of revenue for distributors that lack reverse logistics infrastructure.[4]Policy Division, “Right to Repair Directive 2026,” European Commission, ec.europa.eu Still, refurbished hardware volumes exceed 30% of global totals, creating fresh profit pools for partners with certified remanufacturing lines. The Middle East and Africa, though smaller in absolute value, show strong public-cloud uptake as the United Arab Emirates surpasses 1,000 megawatts of data-center capacity. Currency volatility and fragmented customs regimes remain obstacles, yet distributors with local warehousing and flexible credit win share. South America, led by Brazil, is leveraging nearshoring and 5G rollouts to stimulate demand for edge infrastructure, reinforcing the regional diversity of the IT hardware distribution market.

Competitive Landscape

The market exhibits moderate concentration with TD SYNNEX and Ingram Micro capturing roughly 40% of global broadline revenue, yet face sustained margin compression. TD SYNNEX’s Hyve Solutions nearly doubled sales by supplying custom GPU servers to regional clouds, illustrating the payoff of moving up the configuration stack. Ingram Micro counters price pressure through its Xvantage marketplace, which blends physical hardware and SaaS in a single purchasing workflow.

Arrow Electronics pivoted in March 2026 by integrating Dell’s enterprise portfolio and launching an omnichannel engine that slashed quote-to-cash friction. Westcon-Comstor acquired REAL Security to deepen cybersecurity expertise and expand into the Balkans, signaling a geographic and vertical expansion strategy. Regional challengers across India, Southeast Asia, and Latin America exploit local compliance knowledge and credit flexibility to nip at the heels of global incumbents.

Technology investments create new differentiators, including distributors that embed API-driven inventory feeds, automate rebate reconciliation, and leverage AI-powered demand forecasting, enabling faster turns and lower stockouts. Compliance frameworks such as ISO 27001 and FedRAMP add switching costs for government buyers, insulating qualified partners from pure-play e-commerce rivals. Overall, intensifying specialization and automation are reshaping competitive boundaries within the IT hardware distribution market.

IT Hardware Distribution And Channel Industry Leaders

TD SYNNEX Corporation

Ingram Mircro Inc.

Arrow Electronics, Inc.

Avnet, Inc.

Westcon Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Ingram Micro received the Microsoft Frontier Distributor designation, unlocking Azure consumption incentives tied to hardware projects.

- March 2026: Arrow Electronics unveiled an omnichannel platform and reclaimed USD 350 million in the Dell enterprise business.

- February 2026: Westcon-Comstor signed a pan-European distribution pact with UiPath, adding robotic process automation to its security and networking lineup.

- February 2026: Dell Technologies refreshed its partner incentives to add incremental margin on first-time enterprise wins.

Global IT Hardware Distribution And Channel Market Report Scope

The IT Hardware Distribution and Channel Market encompasses the ecosystem of intermediaries, partners, and service providers that procure, aggregate, manage logistics, add value, and resell IT hardware products from manufacturers to end users. This market facilitates the movement of hardware such as servers, storage systems, networking equipment, personal computers and peripherals, and mobility devices through structured distribution networks, enabling efficient market access, scalability, and customer reach for vendors.

The IT Hardware Distribution and Channel Market Report is Segmented by Product Type (Servers, Storage Systems, Networking Hardware, Personal Computers and Peripherals, Mobility Devices, and Other Product Types), Channel Type (Broadline Distributors, Value-Added Distributors, Resellers, Retail, E-Commerce, and System Integrators), End-User Vertical (Large Enterprises, and Small and Medium Businesses, Government and Public Sector, Telecom Operators, Cloud Service Providers, and Consumer), Service Model (Value-Added Distribution, Broadline Distribution, Specialized Distribution, and Hybrid Model), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Servers |

| Storage Systems |

| Networking Hardware |

| Personal Computers and Peripherals |

| Mobility Devices |

| Other Product Types |

| Broadline Distributors |

| Value-Added Distributors |

| Resellers |

| Retail |

| E-Commerce |

| System Integrators |

| Large Enterprises |

| Small and Medium Businesses |

| Government and Public Sector |

| Telecom Operators |

| Cloud Service Providers |

| Consumer |

| Value-Added Distribution |

| Broadline Distribution |

| Specialized Distribution |

| Hybrid Model |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Servers | ||

| Storage Systems | |||

| Networking Hardware | |||

| Personal Computers and Peripherals | |||

| Mobility Devices | |||

| Other Product Types | |||

| By Channel Type | Broadline Distributors | ||

| Value-Added Distributors | |||

| Resellers | |||

| Retail | |||

| E-Commerce | |||

| System Integrators | |||

| By End-User Vertical | Large Enterprises | ||

| Small and Medium Businesses | |||

| Government and Public Sector | |||

| Telecom Operators | |||

| Cloud Service Providers | |||

| Consumer | |||

| By Service Model | Value-Added Distribution | ||

| Broadline Distribution | |||

| Specialized Distribution | |||

| Hybrid Model | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast will demand from cloud service providers grow?

Revenue linked to cloud service providers is forecast to rise at a 9.36% CAGR through 2031 as hyperscalers keep building new regions.

What segment is losing share to e-commerce portals?

Broadline distributors held 31.28% share in 2025, but their portion keeps sliding as online self-service portals expand 9.18% annually.

Which geography is expected to post the quickest expansion?

Asia-Pacific leads with an 8.88% CAGR, buoyed by new data-center projects in India, Japan, and Southeast Asia.

Why are mobility devices important to distributors?

Mobility devices are projected to grow 9.08% each year through 2031, outpacing servers and generating service revenue from imaging and asset tagging.

How are distributors defending margins against OEM direct sales?

Channel partners are bundling cybersecurity, managed services, and Device-as-a-Service financing to replace lost margin on transactional hardware.

What keeps supply-chain risk elevated in 2026?

Tight high-bandwidth memory and 3-nanometer GPU supply, coupled with 50-week lead times, continue to drive component inflation and allocation challenges.

Page last updated on: