Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Iot in Construction Market is Segmented by Type (Hardware, Software, Services), Deployment Mode (On-Premise, Cloud), End-User (Commercial and Industrial, Residential), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

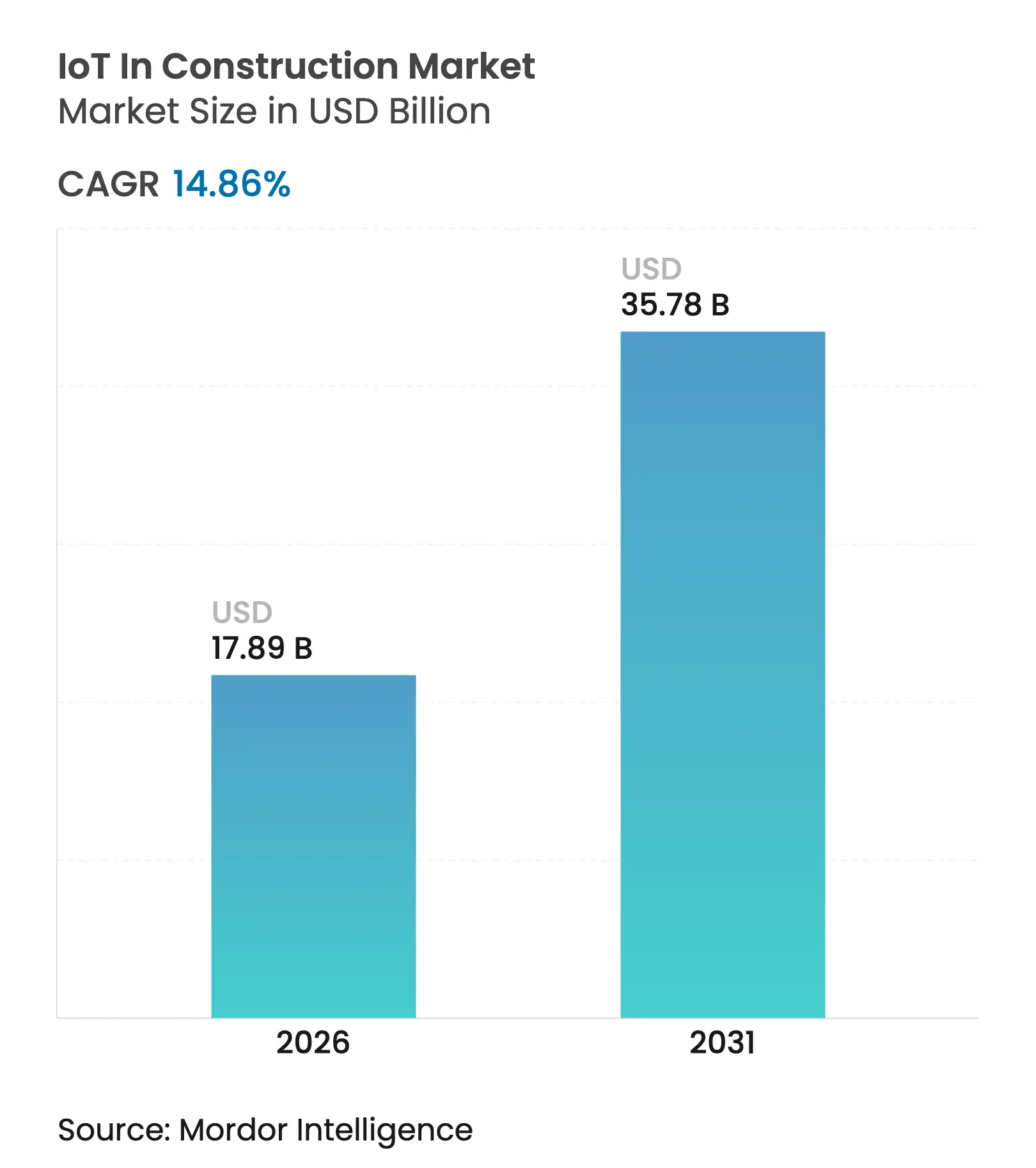

| Market Size (2026) | USD 17.89 Billion |

| Market Size (2031) | USD 35.78 Billion |

| Growth Rate (2026 - 2031) | 14.86 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The IoT in construction market size is expected to grow from USD 15.58 billion in 2025 to USD 17.89 billion in 2026 and is forecast to reach USD 35.78 billion by 2031 at 14.86% CAGR over 2026-2031. The expansion rests on three mutually reinforcing forces: the rollout of 5G connectivity, the maturing of edge‐computing architectures, and a steady decline in sensor prices. Together these elements allow contractors to analyze large data volumes in near real time, automate maintenance schedules, and comply with tightening carbon-tracking mandates. Falling hardware costs are particularly important for mid-tier builders because they lower the up-front investment required to retrofit older assets. Safety analytics platforms are another powerful catalyst, helping firms cut incident rates while collecting data that reduces insurance premiums by 10-15% on monitored sites. Competitive pressure also fuels adoption: equipment makers such as Caterpillar and technology specialists like Trimble are embedding connectivity into their core products, turning traditional machinery into data-rich platforms.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Improved safety-at-site

analytics

Improved safety-at-site

analytics

| +2.8% | North America, EU | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.8%

|

Geographic Relevance

:

North America, EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Real-time asset tracking and

predictive maintenance

Real-time asset tracking and

predictive maintenance

| +3.2% | Global, strongest in Asia-Pacific | Short term (≤ 2 years) | |||

5G and edge computing roll-out

on jobsites

5G and edge computing roll-out

on jobsites

| +2.5% | North America, Asia-Pacific | Medium term (2-4 years) | |||

Mandatory carbon-emission

logging on projects

Mandatory carbon-emission

logging on projects

| +1.9% | EU, North America, Asia-Pacific | Long term (≥ 4 years) | |||

Falling cost of digital-twin

sensors for mid-tier firms

Falling cost of digital-twin

sensors for mid-tier firms

| +2.1% | Global | Short term (≤ 2 years) | |||

Insurance premium discounts for

IoT-monitored sites

Insurance premium discounts for

IoT-monitored sites

| +1.7% | North America, EU | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Improved safety-at-site analytics

IoT wearables and environmental sensors continuously capture data on noise, dust, motion, and proximity. Platforms analyze these streams and alert supervisors within seconds, lowering incident rates while creating auditable safety records that insurance companies now recognize with premium reductions.[1]AXA XL, “Connected Jobsite Safety and Insurance Benefits,” axaxl.com Users report fewer lost-time injuries and faster root-cause analysis, reinforcing the business case for connected safety gear.

Real-time asset tracking and predictive maintenance

Linking IoT sensors to machine-learning models allows contractors to service equipment according to condition rather than calendar schedules. Trackunit’s global network of more than 1 million connected machines demonstrates how remote diagnostics can cut downtime by 20-25% and maintenance outlays by 18%.[2]Cisco, “Trackunit Expands Global Construction IoT,” cisco.com The same telemetry data supports emissions reporting, helping firms meet new regulatory requirements on fuel usage and idle time.

5G and edge computing roll-out on jobsites

Fifth-generation networks carry massive sensor loads with latency measured in single-digit milliseconds, unlocking autonomous equipment and immersive collaboration tools. China Construction’s Beijing “smart site” deploys 5G-enabled AI glasses and health-monitoring wearables to boost productivity 15-20% through low-latency data exchange.[3]KHL, “Beijing Smart Construction Site Uses 5G,” khl.com Edge gateways preprocess high-volume video and LiDAR data on-site, minimizing bandwidth bottlenecks.

Mandatory carbon-emission logging on projects

Public agencies increasingly require realtime disclosure of construction-site emissions. Turner Construction used connected sensors to save 9,583 gallons of diesel and avoid 97.85 metric tons of CO₂ on a California university project The data flow feeds ESG dashboards and blockchain ledgers that preserve audit trails for regulators and investors.

Restraints Impact Analysis

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High implementation and

retrofit costs

High implementation and

retrofit costs

| -2.4% | Global, SMEs | Short term (≤ 2 years) |

( ) % Impact on CAGR Forecast

:

-2.4%

|

Geographic Relevance

:

Global, SMEs

|

Impact Timeline

:

Short term (≤ 2 years)

|

Data-security and privacy

liabilities

Data-security and privacy

liabilities

| -1.8% | Global, stringent in EU | Medium term (2-4 years) | |||

Sensor-equipment

interoperability gaps

Sensor-equipment

interoperability gaps

| -1.5% | Global | Medium term (2-4 years) | |||

Job-site skills shortage in IoT

data analytics

Job-site skills shortage in IoT

data analytics

| -2.1% | North America, EU | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High implementation and retrofit costs

Although sensor prices have fallen, full integration requires gateways, connectivity, and software configuration that often doubles budgets when legacy equipment must be adapted. Financing models such as Trimble’s tiered subscriptions spread costs over time, but capital outlays remain a hurdle for small contractors.

Data-security and privacy liabilities

A wider attack surface accompanies every new connected device. IoT-related breaches rose 25% across industrial sectors, and the mobile, temporary networks common on construction sites heighten exposure. Privacy issues also arise from wearables that track worker biometrics, driving additional compliance costs under regulations like GDPR.

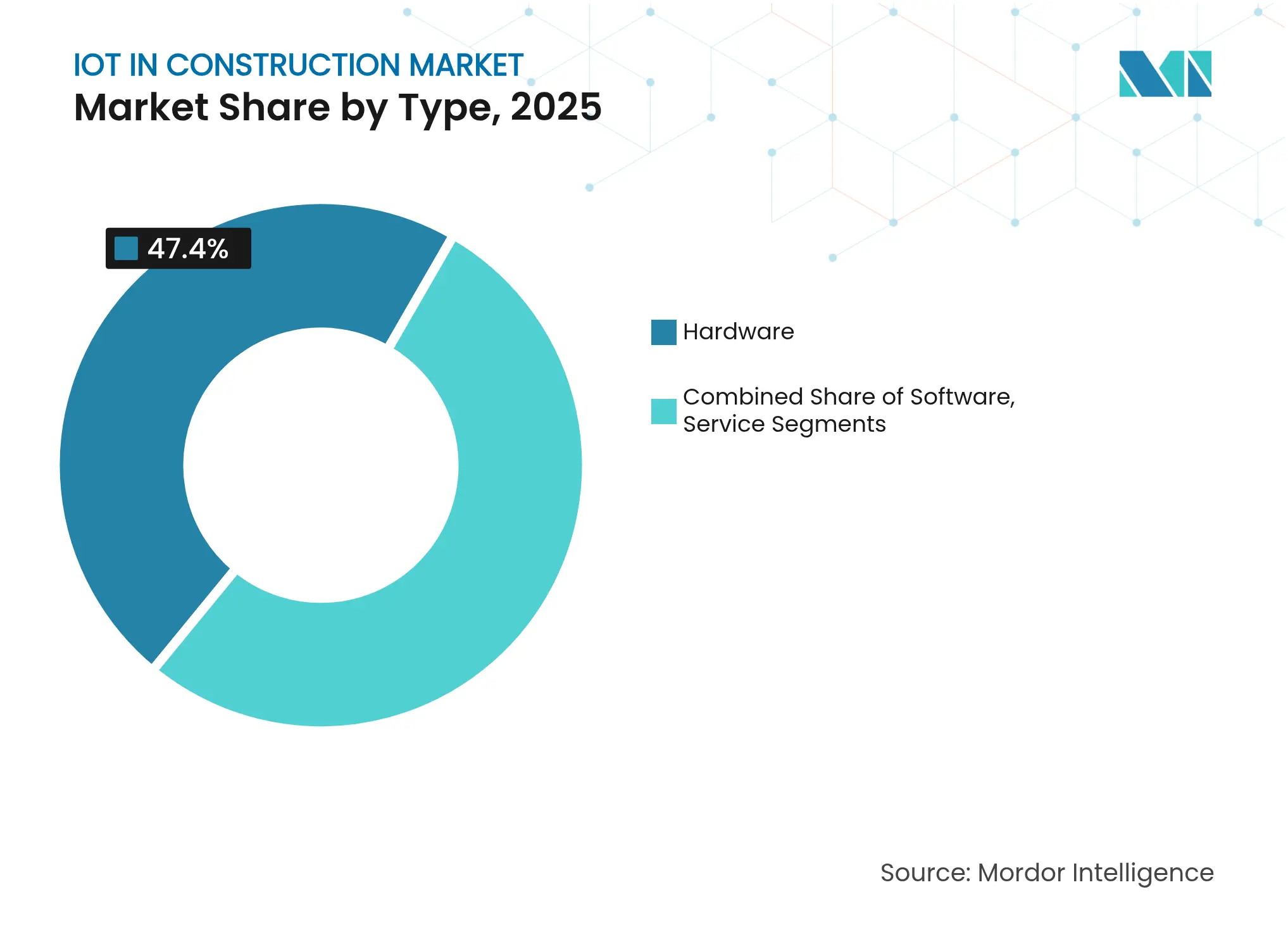

By Type: Hardware Foundation Enables Software Innovation

Hardware captured 47.40% of IoT in construction market share in 2025, anchored by environmental sensors, wearables, asset tags, and edge computing hardware that form the essential data-gathering layer. The strong base reflects the sector’s need for ruggedized devices able to endure dust, vibration, and extreme temperatures. Software claimed roughly 32.85% and focuses on analytics, digital twins, and workflow orchestration, translating raw data into actionable insights for planners and site managers. Services, though representing 19.75%, are advancing quickest at an 17.55% CAGR as contractors outsource integration, management, and data science to specialized vendors. Trimble now earns 75% of revenue from software and services, underscoring the shift to subscription models that smooth cash flow and reduce up-front risk.

Hardware vendors increasingly bundle managed services, positioning themselves as one-stop partners rather than component suppliers. The result is tighter alignment of incentives: providers gain recurring revenue while clients receive performance guarantees tied to uptime or energy savings. AI modules embedded in service packages automate parameter tuning and generate predictive alerts, reinforcing the ROI narrative and expanding the overall IoT in construction market. This interplay of physical assets and cloud intelligence keeps the IoT in construction industry on a steep innovation curve.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: Cloud Dominance Accelerates Digital Transformation

Cloud platforms held 52.40% share in 2025 and simultaneously posted the highest growth rate at 19.05% CAGR, illustrating a decisive swing toward scalable, location-agnostic systems. Remote management became mission-critical during the pandemic, prompting firms such as Swinerton to move document workflows and digital twins entirely online, thereby eliminating client travel and cutting review cycles. On-premise solutions still run 47.60% of workloads, favored by large enterprises with proprietary security policies or limited Internet connectivity on certain sites.

The market is now gravitating toward hybrid architectures: sensitive design files remain on local servers while analytics engines spin up in the cloud to crunch telematics data. Hexagon’s Reality Cloud Studio combines web-based visualization with optional edge processing for latency-sensitive tasks. Edge computing thus complements the cloud, enabling millisecond responses for autonomous machines without sacrificing the macro-level insights that only scalable analytics can provide. These flexible arrangements enlarge the IoT in construction market size by lowering the switching cost for firms still operating onsite data centers.

By End-user: Commercial Dominance Meets Residential Acceleration

Commercial and industrial projects controlled 61.25% of the IoT in construction market size in 2025 on the back of complex infrastructure builds, large capital budgets, and clear productivity metrics that justify technology spend. Corporate campuses, manufacturing plants, and transportation hubs already track heavy equipment fleets, monitor structural health, and optimize energy use. General contractors such as Skanska and Turner formalize innovation budgets and measure returns, giving their pilot programs scale and longevity.

Residential adoption, while smaller at 38.75%, is growing by 19.85% CAGR as smart-home expectations spill into new-build specifications. Developers integrate climate control, intrusion detection, and leak monitoring during construction, lowering retrofit costs for owners. The crossover between consumer IoT and jobsite technology blurs traditional categories and brings volume buying power that further reduces sensor prices. As mid-market builders bundle these features into multi-family housing, the IoT in construction market gains breadth and resilience. The trend also seeds a new service layer for post-handover maintenance contracts, reinforcing the long-term revenue profile for technology providers.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

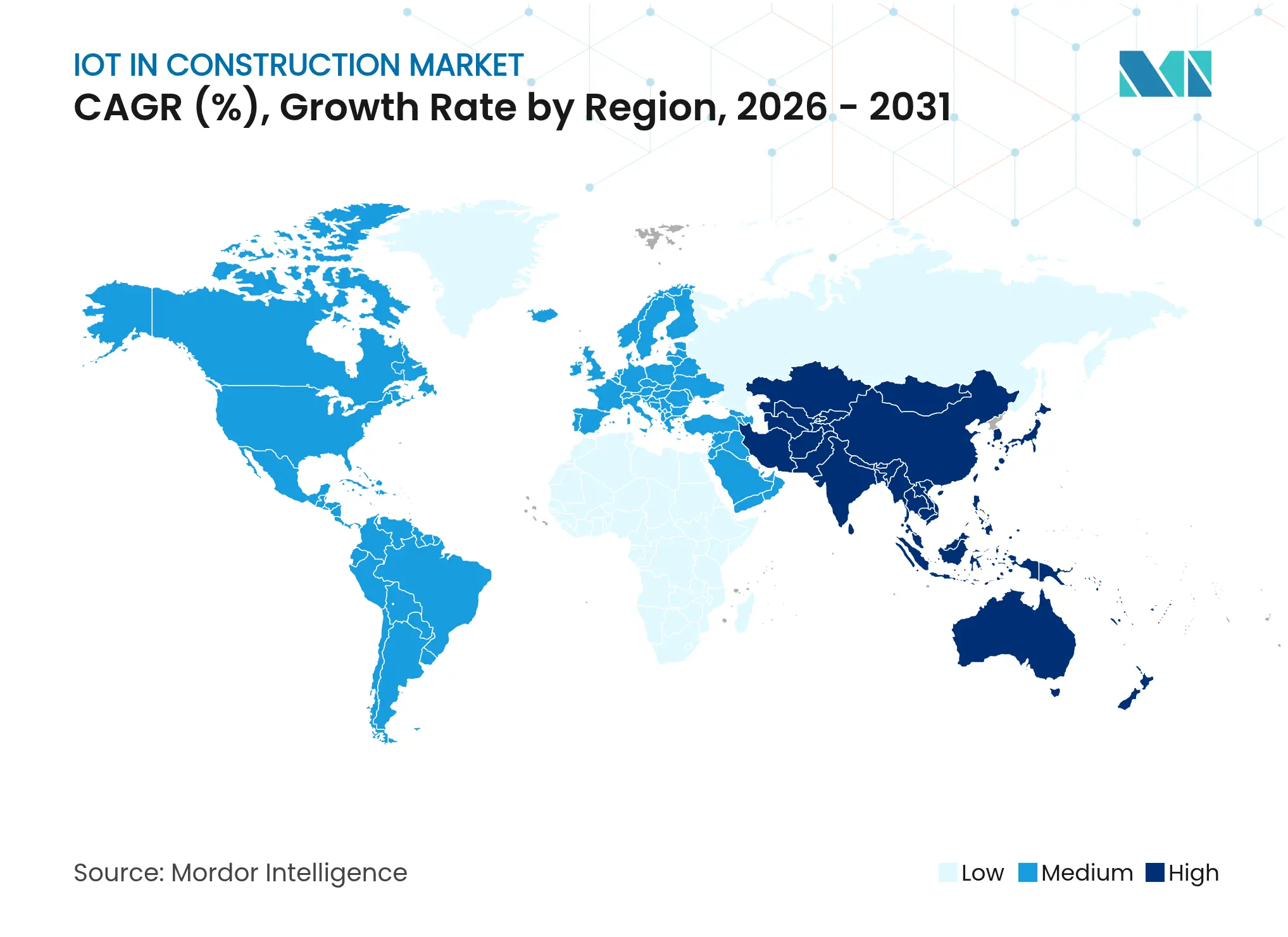

North America retained leadership with a 38.10% share of the IoT in construction market in 2025 thanks to early 5G rollouts, clear legal frameworks, and strong collaboration between equipment makers and software firms. Major cloud providers host data in regionally distributed centers, easing compliance with state regulations. Insurance carriers headquartered in the United States actively promote IoT-enabled risk mitigation, further accelerating uptake.

Asia-Pacific is advancing at a 19.25% CAGR through 2031, the fastest regional growth trajectory, propelled by large urbanization projects and supportive national strategies in China, India, and members of ASEAN. Infrastructure megaprojects adopt sensor packages to manage asset lifecycles, while government agencies standardize data formats that encourage vendor competition and price declines. Indigenous technology suppliers now account for a growing share of deployments, tailoring solutions to local languages and regulations.

Europe shows steady expansion as the bloc’s Green Deal mandates rigorous carbon accounting. Builders deploy connected meters and blockchain-verified logs to meet public tender requirements. Meanwhile, the Middle East and Africa remain nascent markets but display rising demand as multibillion-dollar transport corridors and smart-city programs specify IoT from project inception. Taken together, these dynamics ensure that the IoT in construction market maintains geographic diversification, reducing exposure to regional downturns.

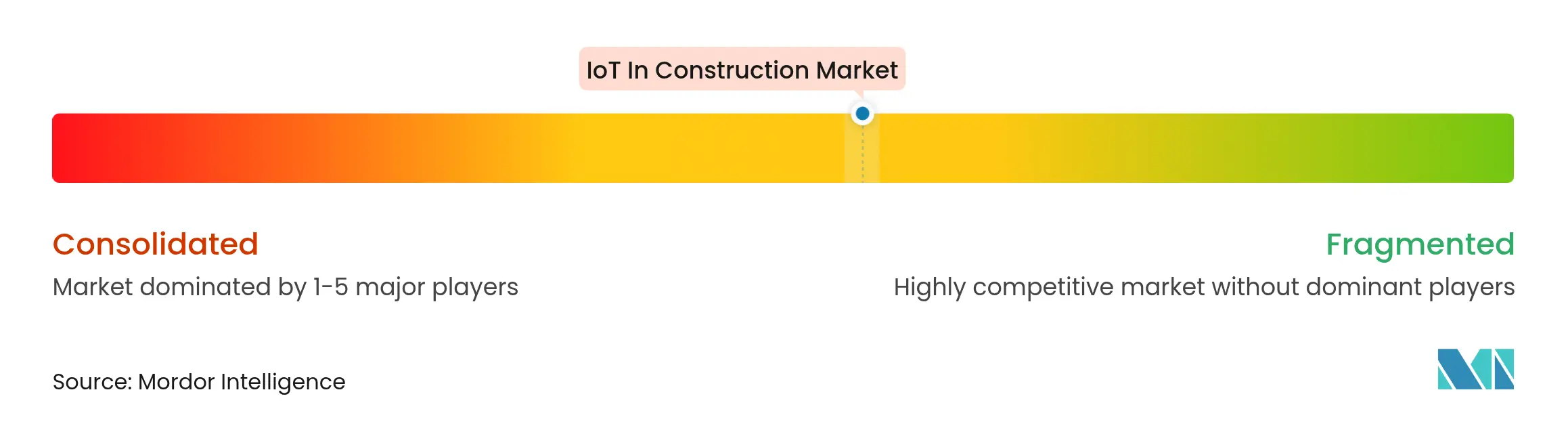

Market Concentration

Competition is intensifying as traditional equipment manufacturers converge with pure-play software vendors. Caterpillar, Komatsu, and Volvo embed telematics modules as standard equipment, transforming heavy machinery into rolling data nodes. Trimble pursues a “Connect & Scale” agenda that links field hardware to cloud analytics and posts USD 2.03 billion in annual recurring revenue, demonstrating market appetite for subscription models. Hexagon prepares a USD 1.578 billion spin-off of its Asset Lifecycle Intelligence unit, signaling confidence in specialized platforms focused on construction workflows.

Smaller innovators such as Converge and Brickeye address niche pain points—concrete curing and environmental monitoring respectively—then expand through partnerships with incumbents. Platform interoperability has become a prime battleground: builders demand seamless integration across scheduling, cost control, safety, and sustainability dashboards. Consequently, open APIs and neutral data hubs distinguish market leaders from locked-in ecosystems.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

IoT devices can help with digital transformation by allowing software construction companies to access real-time data. The information allows faster, more accurate insights and better management. Digital transformation also allows for the automation of time-consuming tasks.

The IoT in construction market is segmented by type (hardware, software, services), by end-user (commercial, residential), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.