LTE IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

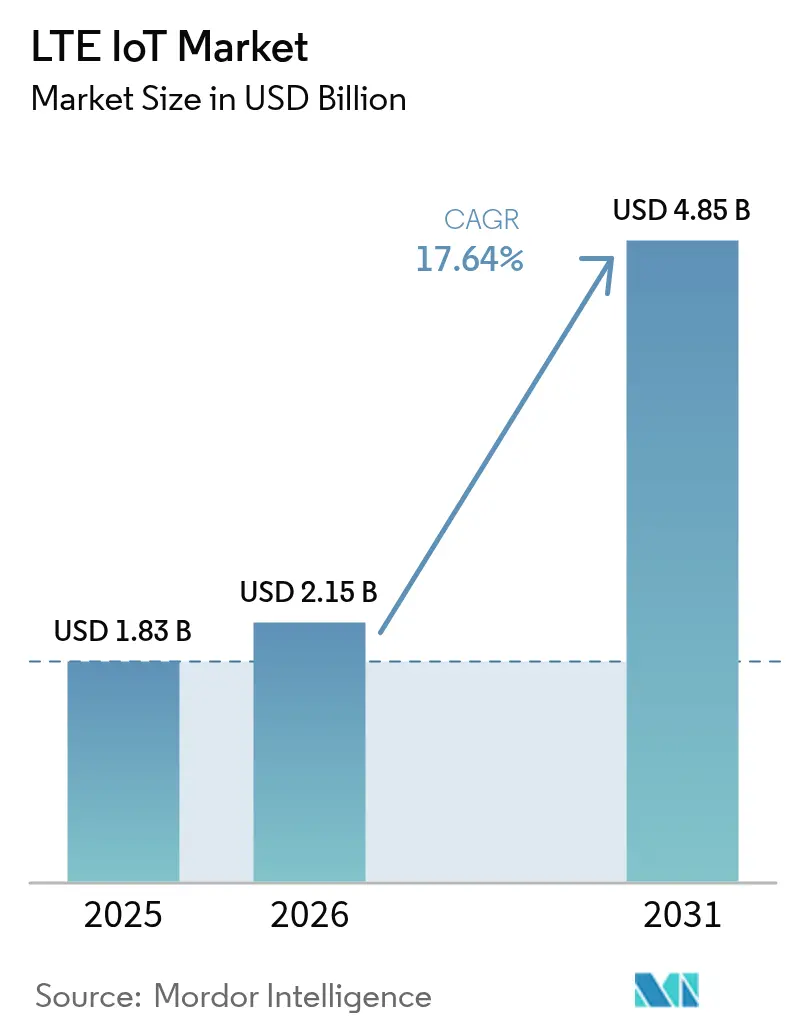

| Market Size (2026) | USD 2.15 Billion |

| Market Size (2031) | USD 4.85 Billion |

| Growth Rate (2026 - 2031) | 17.64% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

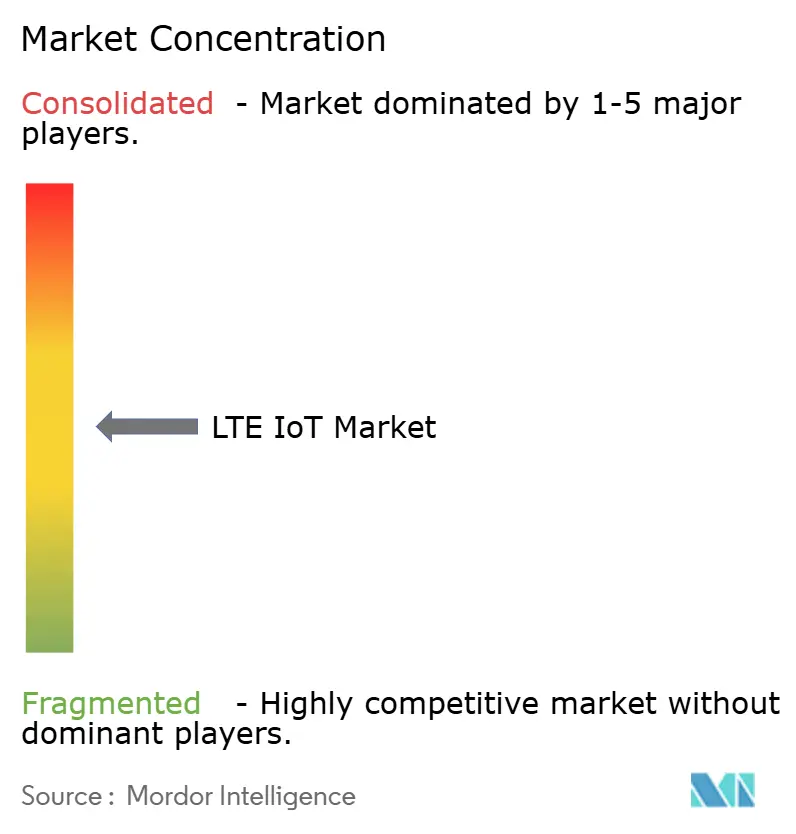

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LTE IoT Market Analysis by Mordor Intelligence

LTE IoT market size in 2026 is estimated at USD 2.15 billion, growing from 2025 value of USD 1.83 billion with 2031 projections showing USD 4.85 billion, growing at 17.64% CAGR over 2026-2031.

This rapid growth reflects accelerating 2G and 3G network sunsets, falling low-power cellular module costs, and government smart-meter mandates that lock utilities into licensed-spectrum connectivity. Asia-Pacific (APAC) leads current adoption with 55% revenue share, propelled by China Mobile’s deployment of 1.7 million 5G base stations and 595 million cellular IoT lines. Parallel smart-city spending in the Middle East, exemplified by Qatar’s USD 60 million Lusail City contract, positions the region as the fastest climber at 19.8% CAGR. Enterprises are shifting from outright ownership toward managed connectivity, lifting the managed-services CAGR to 15.4% as operators monetize network slicing and automated provisioning. Demand is strongest in industrial automation today, yet healthcare registers the sharpest upswing thanks to remote patient-monitoring programs riding cellular LPWA backbones.

Key Report Takeaways

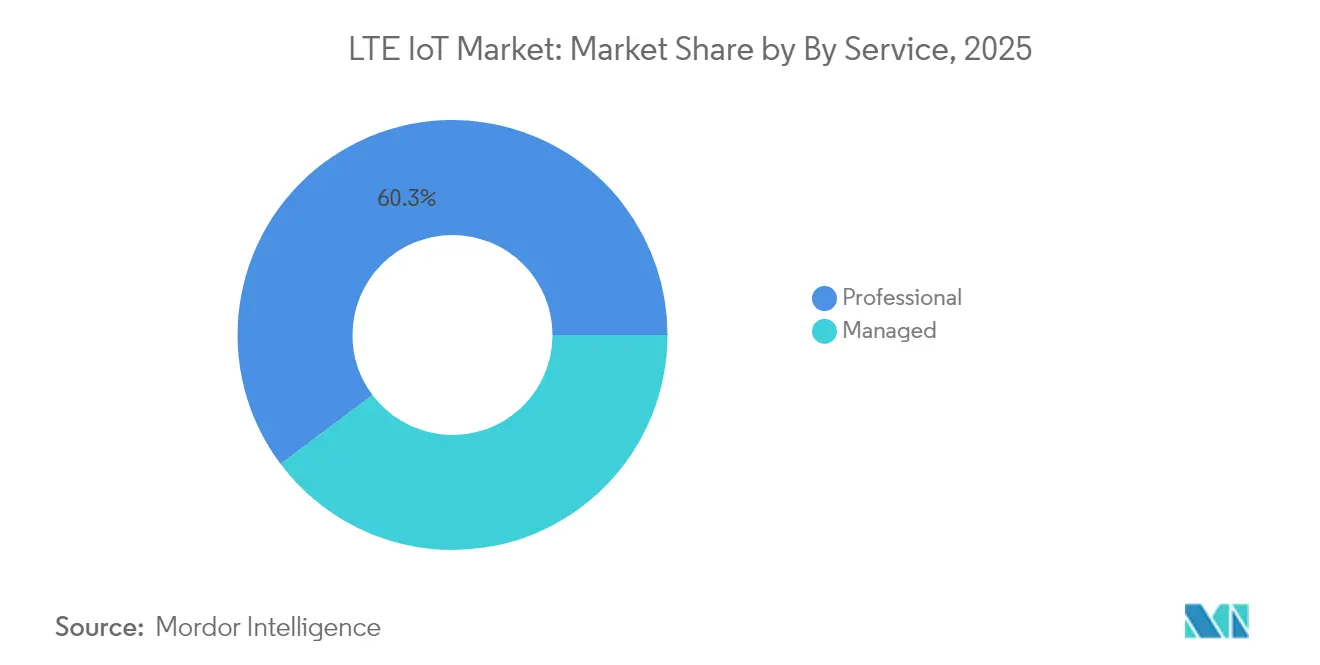

- By service, professional services held 60.25% of the LTE IoT market share in 2025, whereas managed services are projected to post the fastest 14.92% CAGR through 2031.

- By product type, NB-IoT dominated with 64.20% LTE IoT market share in 2025, but LTE-M is forecast to grow at an 17.95% CAGR to 2031.

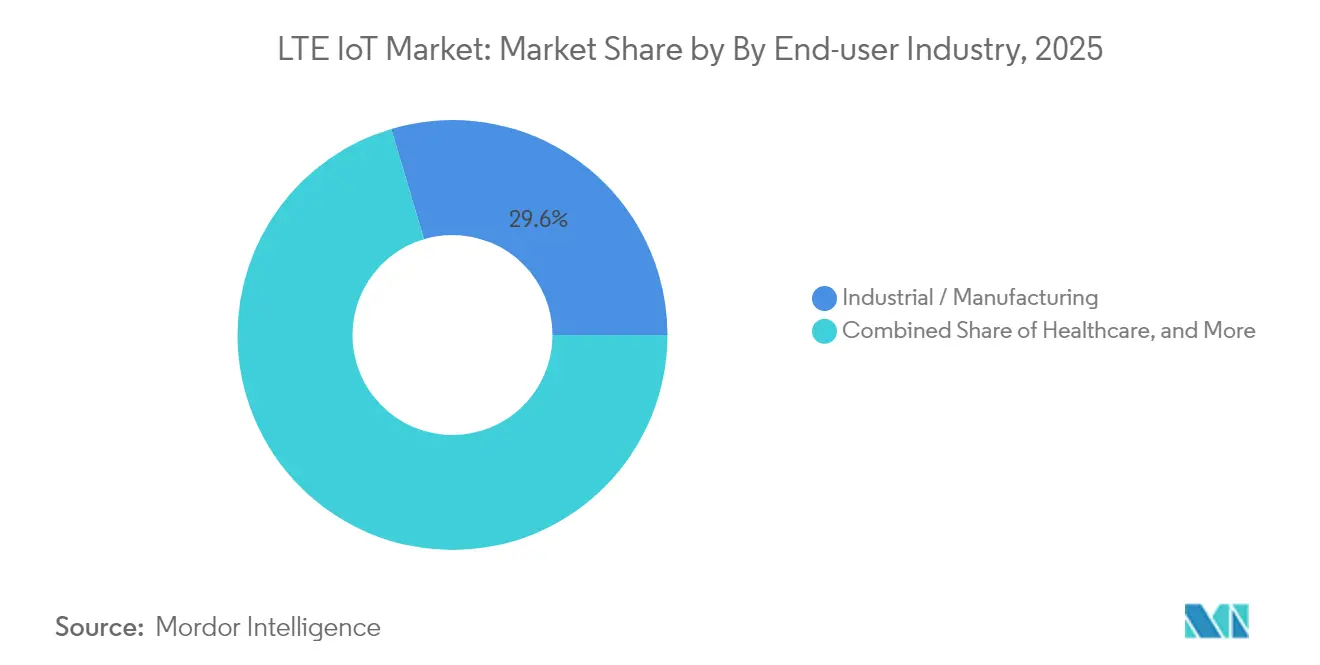

- By end user, industrial applications captured 29.60% revenue in 2025; healthcare is advancing at a 17.18% CAGR over 2026-2031.

- By geography, APAC accounted for 54.40% of 2025 revenue, while the Middle East is set to expand at 19.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global LTE IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-power cellular LPWA standards reach sub-USD 4 module cost | +4.20% | Global, with early adoption in China and Europe | Medium term (2-4 years) |

| Smart utility-meter mandates in >60 countries | +3.80% | Global, concentrated in Europe, North America, APAC | Long term (≥ 4 years) |

| 2G/3G sunsets forcing device migration to LTE IoT | +5.10% | Global, accelerated in Europe and North America | Short term (≤ 2 years) |

| 3GPP Rel-17 RedCap halves LTE-M power draw | +2.30% | Global, with early deployment in developed markets | Medium term (2-4 years) |

| Network-slicing-based QoS tiers lift average IoT ARPU | +1.90% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low-power cellular LPWA modules fall below USD 4

Nordic Semiconductor’s nRF9151 shows how a 64 MHz Arm Cortex-M33 and integrated multimode modem can cut bill-of-materials and approach a sub-USD 4 headline price, encouraging agriculture, logistics, and environmental-sensing deployments that once relied on unlicensed LPWAN. Chinese vendors already quote USD 3 NB-IoT modules for utility meters, reinforcing cost-down momentum . While most global catalogs still list USD 10-15 parts, operators in Europe and APAC have begun subsidizing hardware to accelerate LTE IoT market uptake and lift network utilization.

Smart-meter mandates reinforce cellular connectivity

Over 60 jurisdictions have enacted regulations that oblige gas, electricity, or water utilities to install communicating meters able to upgrade remotely. Telia’s rollout of 2 million Swedish electric meters on NB-IoT and LTE-M cut truck-roll costs and established a 5G-ready distribution grid. Netinium’s SIM-profile orchestration with Telit Cinterion allows remote provisioning, solving the historic lock-in that deterred utilities from wide-area cellular links. [3]Telia Company, “Smart Metering Sweden,” ericsson.comThese programs create multiyear visibility for the LTE IoT market while displacing proprietary mesh networks.

Legacy network sunsets stimulate immediate migration

More than 55 cellular networks were switched off between 2021 and 2025, forcing embedded devices to re-register on LTE-based LPWA protocols. Europe has prioritized 3 G retirement while holding 2G for emergency voice, whereas North America plans synchronized sunsets of both layers. Device makers rush to certify LTE-M and NB-IoT boards that guarantee roaming continuity and battery life, accelerating overall LTE IoT market expansion.

RedCap improves LTE-M energy profile

3GPP Release 17 scales down bandwidth and antenna requirements through RedCap, halving LTE-M power draw and enabling up to 10 Mbps peak rates for mid-tier IoT gadgets. Expected uptake spans smart wearables and process-control sensors that need more than NB-IoT’s tens-of-kilobits yet less than full 5G throughput. Because RedCap operates on existing LTE-M layers until standalone 5G coverage matures, it offers an incremental path to enriched services without ripping out infrastructure.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-GHz spectrum congestion | -2.10% | Global, acute in dense urban areas | Short term (≤ 2 years) |

| Module price premium vs LoRaWAN/BLE alternatives | -1.80% | Global, particularly in cost-sensitive applications | Medium term (2-4 years) |

| Patchy NB-IoT roaming causing firmware forks | -1.30% | Global, affecting multinational deployments | Medium term (2-4 years) |

| Carbon-emission reporting pushes firms toward ultra-low-energy LPWAN | -0.90% | EU and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sub-GHz spectrum congestion limits capacity

Multiple LPWAN formats now compete inside finite 700–960 MHz slices. Duty-cycle rules and power caps curb cell density, and network-side interference management costs rise sharply. The FCC opened new 6 GHz indoor allocations in 2024, yet sub-GHz propagation remains critical for underground or rural IoT reach. Operators therefore invest in dynamic-spectrum access and narrowband filtering, adding cost and slowing LTE IoT market rollouts in megacities.

Carbon-footprint rules favor ultra-low-energy designs

Under the EU Energy Efficiency Directive 2023/1791, enterprises must disclose the climate impact of connected assets, nudging them toward sensors able to function for years from tiny batteries or harvested energy. Vodafone’s 2040 net-zero roadmap imposes internal thresholds that may exclude energy-intensive cellular endpoints. This pushes designers to hybrid topologies where NB-IoT transmits data only when thresholds are breached, while a passive local network gathers routine measurements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Integration complexity sustains professional spend

Professional services generated 60.25% of LTE IoT market revenue in 2025 through consulting, device certification, and edge-cloud integration projects. Managed-service uptake is forecast to accelerate at 14.92% CAGR as enterprises transfer lifecycle tasks, from SIM logistics to security patching, to specialist providers. Deutsche Telekom's business-to-business arm bundles connectivity with analytics in outcome-based contracts that shift capital budgets into operating fees. Over time, AI-enabled orchestration platforms will trim manual engineering hours, yet the transition itself fuels recurring revenue for managed-service vendors.

Standardized onboarding APIs and eUICC provisioning already shorten pilot phases, but brownfield industrial estates still need bespoke radio-planning and protocol translation. As a result, professional engagements remain pivotal for multiyear retrofits even while new-build projects lean more heavily on managed packages. Managed services in the LTE IoT market are projected to outgrow professional services beyond 2029, with both segments together reinforcing operator stickiness through 2031.

By Product Type: NB-IoT retains reach while LTE-M gains mobility

NB-IoT accounted for 64.20% LTE IoT market share in 2025, owing to its 20 dB link-budget advantage and 10-year battery potential in fixed meters. The LTE IoT market size tied to NB-IoT endpoints is projected to climb at 15.48% CAGR, albeit slower than LTE-M’s 17.95% pace. LTE-M supports voice, mobility, and FOTA block sizes up to 1 MB, making it the preferred choice for fleet trackers and safety wearables. RedCap extensions will further compress its power gap to NB-IoT, while operators harmonize roaming rates.

Hybrid terrestrial–satellite deals illustrate both protocols’ evolution. Quectel’s certified module on Skylo’s NTN adds coverage in maritime or mining corridors, broadening NB-IoT’s footprint. Telit Cinterion, meanwhile, offers dual-mode LTE-M NB-IoT modules with fallback to GEO satellite for uninterrupted cargo monitoring. The commercial narrative, therefore, shifts from either-or to application-fit, reinforcing coexistence within the LTE IoT industry.

By End User: Healthcare surges while factories keep scale

Industrial automation held 29.60% revenue share in 2025, driven by predictive-maintenance algorithms that depend on continuous vibration feeds from machinery. Yet healthcare endpoints—ranging from cardiac patches to infusion pumps—will log a 17.18% CAGR through 2031, narrowing the gap. The Monit4Healthy platform demonstrates how edge preprocessing of ECG, EMG, and PPG reduces backhaul traffic before LTE uplink, preserving battery life in ambulatory settings.

Health-sector momentum is reinforced by aging demographics and reimbursement for remote care, while industrial buyers already account for cellular IoT in factory-digitization roadmaps. Retail, agriculture, and consumer electronics deliver ancillary volumes: Saudi vertical-farming projects use NB-IoT soil sensors, and European smart-lock firms bundle LTE-M for backup connectivity. This diversification cushions volatility in any single vertical and expands total LTE IoT market addressability.

Geography Analysis

APAC contributed 54.40% of global revenue in 2025 as China scaled NB-IoT coverage to 100,000 connections per sector and subsidized module production below USD 3. China Mobile booked CNY 723.5 billion (USD 101.2 billion) telecom income in the first three quarters of 2024, underscoring sustained spectrum and capex commitments. Japan and Korea emphasize smart-factory retrofits, while ASEAN nations pilot traffic management and flood-alert systems riding shared LTE backbone infrastructure.

The Middle East is the fastest-expanding sub-region, projected at 19.12% CAGR to 2031. Qatar’s Lusail City program integrates 450,000 residents into a real-time operations center using NB-IoT and LTE-M sensors for lighting, waste, and transport. Saudi Vision 2030 channels petro surplus into agricultural IoT that combats food-security risks, with cellular LPWA linking greenhouse climate controls and drone irrigation.

Europe and North America display steady renewal of legacy meters and industrial gear, aided by stricter carbon accounting and 3G shutdowns. Telia’s conversion of Swedish meters shows the blueprint: swap proprietary PLC for licensed LTE radios, enable eUICC, and guarantee 15-year contracts. o2 Telefónica’s German footprint reported 132.4% year-over-year M2M subscriber growth in Q1 2025, mostly utility driven . Africa and Latin America remain nascent but are leapfrogging fixed lines with direct LTE IoT adoption in asset-tracking and agriculture.

Regulatory Landscape

The LTE IoT market operates under a mix of spectrum policy, telecom equipment compliance, and evolving cellular standards. In the United States, policy actions involving the FCC and NTIA shape licensed-spectrum availability relevant to LTE-M and NB-IoT deployments, including federal initiatives that direct additional spectrum toward commercial mobile services and 2026 milestones related to repurposing federally used bands. In India, TRAI issued February 2026 recommendations covering multiple auction bands (including 800 MHz, 900 MHz, 1800 MHz, 2100 MHz, and 26 GHz), reinforcing how national spectrum roadmaps influence operator coverage investments and the cost structure of wide-area IoT connectivity.

On the standards side, ETSI and 3GPP continue to publish specifications that affect device certification pathways and network feature roadmaps. ETSI released new 2026 technical specifications (for example, TS 123 369 V19.3.0 and TS 138 191 V19.2.0) connected to low-power IoT evolution within the broader 3GPP release structure, which points to tighter formalization of ultra-low-energy and ambient-style IoT capabilities alongside legacy LTE IoT deployments. This standards cadence sets multi-year expectations for module interoperability, eSIM/eUICC provisioning, and roaming behavior that device makers and operators need to support across regions.

Value Chain Analysis

The LTE IoT value chain starts with standards and IPR (3GPP and ETSI specifications governing NB-IoT and LTE-M features and conformance), then moves through silicon and module design (baseband/modem vendors and RF front-end providers), certified modules (such as Quectel, Fibocom, u-blox, and Telit Cinterion), and device OEMs/ODMs that integrate modules into meters, trackers, industrial sensors, and medical devices. Mobile network operators provide licensed-spectrum access and IoT core capabilities, while connectivity management platforms (for provisioning, lifecycle control, and policy management) and cloud and edge analytics layers capture more value as enterprises shift toward managed connectivity and outcome-based contracts.

Downstream, system integrators and vertical solution providers deliver deployment engineering, device certification support, security hardening, and application integration, sustaining professional services spend in complex industrial and utility rollouts. Recent standardization work in Release 19 and related ETSI publications points to a continuing shift toward newer IoT capability blocks (including non-terrestrial enhancements and ultra-low-power concepts), which affects test labs, module certification cycles, and operator feature enablement. Key bottlenecks and cost sensitivities remain tied to component availability, multi-operator certification across many carrier profiles, and roaming and provisioning fragmentation that can drive firmware variants for global fleets.

Competitive Landscape

The LTE IoT market is moderately concentrated. Ericsson, Nokia, and Huawei supply multiband radio access networks, but value capture tilts toward cloud-core, SIM management, and analytics layers. Qualcomm leverages its patent pool and Snapdragon X line to license modem IP as well as fabless chipsets for consumer wearables, automotive telematics, and industrial sensors.[1]Qualcomm, “Annual Report 2024,” qualcomm.com Cisco’s IoT Control Center enables operators to carve network slices with differentiated latency and packet-loss guarantees, monetizing connected-vehicle service levels worth an estimated USD 65 billion in subscriptions by 2030.

White-space entrepreneurship thrives at the satellite edge. OQ Technology and Transatel fuse non-terrestrial NB-IoT with terrestrial roaming to safeguard supply-chain visibility in remote regions. Module vendors—Quectel, Fibocom, u-blox—compete on bill-of-materials and integrated GNSS while bankrolling certification across more than 200 carrier profiles. Operators differentiate through end-to-end offers: Vodafone’s Digital Asset Broker layers identity, payment, and ESG scoring atop connectivity, aiming to widen subscription margins without raising average data usage.

Pricing pressure persists. Chinese ODMs undercut established brands by 30-40%, yet multinational buyers often pay a premium for fully documented software stacks and long-term BOM stability. Overall, competitive intensity remains moderate because spectrum licensing, roaming-clearing houses, and 3GPP compliance impose high entry barriers, keeping most new entrants in niche device categories rather than full-stack network services.

LTE IoT Industry Leaders

Qualcomm Technologies, Inc

Gemalto N.V.

u-blox AG

Ericsson

Cisco (Jasper)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large-scale migration programs anchored in policy and operator network sunsets create whitespace for LTE-M and NB-IoT device refresh cycles, particularly in utilities and industrial estates where long-life endpoints need licensed-spectrum coverage and remote firmware updates. The report context notes smart-meter mandates in more than 60 jurisdictions and cites deployments such as Telia’s NB-IoT and LTE-M rollout for 2 million Swedish electric meters, showing how regulated replacement cycles translate into multi-year device and connectivity demand. At the same time, ongoing 2G/3G retirements (with numerous shutdowns occurring through 2025 and early 2026) continue to drive replacement of legacy M2M endpoints with LTE-based LPWA solutions that support improved security and lifecycle tooling.

A second opportunity area is the expansion of managed connectivity and mobility-grade service tiers for IoT, where operators monetize automated provisioning, QoS controls, and emerging critical-IoT features instead of selling connectivity alone. Standards work that targets interworking and migration between LTE and 5G systems (for example, ETSI TS 123 632 V19.0.0 published in January 2026) supports solution designs that keep installed LTE IoT fleets operational while adding upgrade paths to newer radio capabilities where needed. Hybrid coverage approaches also broaden addressable use cases, including satellite-augmented IoT for remote asset monitoring and logistics corridors that fall outside terrestrial LTE footprints.

Recent Industry Developments

- July 2026: Ericsson, AT&T, and MediaTek completed an in-field trial of Layer 1/Layer 2 Triggered Mobility (LTM) on the AT&T network. The work targeted reduced handover interruption time versus legacy Layer 3 mobility, improving continuity for mobile and time-sensitive IoT traffic and strengthening operator-grade propositions for critical IoT.

- March 2025: Vodafone Spain and Ericsson kicked off a four-year standalone 5G core rollout targeting 90% population coverage. The program strengthens foundations for network slicing and differentiated QoS tiers that operators use to package managed LTE IoT connectivity and lifecycle services for enterprises.

- December 2024: Quectel and Skylo unveiled a non-terrestrial NB-IoT module concept to extend licensed-spectrum IoT beyond terrestrial coverage. This move broadened the LTE IoT ecosystem toward hybrid terrestrial-satellite connectivity for tracking, maritime, mining, and remote infrastructure monitoring.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The LTE IoT market, in this methodology, covers revenue generated from LTE based IoT connectivity and related services that enable devices to transmit small to moderate data over cellular networks, mainly through NB-IoT and LTE-M, across major end-use industries and regions.

Scope exclusions: Excludes non-LTE IoT connectivity such as 2G/3G IoT, 5G IoT, and non-cellular LPWAN options, and it also excludes purely on-premise short range protocols.

Segmentation Overview

- By Service

- Professional

- Managed

- By Product Type

- NB-IoT (Cat-NB1)

- LTE-M (eMTC Cat-M1)

- By End-user Industry

- IT and Telecom

- Consumer Electronics

- Retail (Digital Commerce)

- Healthcare

- Industrial

- Other Industries

- By Geography

- North America

- South America

- Europe

- Asia-Pacific

- Middle East

- Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by building the demand context for LTE IoT using public, repeatable datasets, then mapping where connectivity value is actually created. Inputs included ITU indicators for mobile subscriptions and network coverage, GSMA public dashboards and papers for IoT connection counts and technology adoption, OECD broadband and digital economy series for digital diffusion context, and FCC and EU telecom regulatory releases to understand spectrum availability and network rollout status.

We also reviewed company filings and investor presentations for modules, chipsets, and connectivity services, plus operator press releases and reputable technology press for launch timing and pricing direction. To reduce gaps for smaller regional markets, we supplemented with a paid subscription for company financials and news intelligence, and a patent database to track filing intensity around NB-IoT and LTE-M feature development. The desk sources listed here are illustrative, and additional public references were also used for cross-checks and clarification during the work.

Primary Interviews and Surveys

Primary work was used to test the assumptions from the desk stage, especially around which verticals are scaling, how pricing changes when device volumes increase, and what share of deployments remain on NB-IoT versus LTE-M. We spoke with connectivity providers, module and chipset ecosystem participants, and large adopters across regions, then rechecked any high-variance inputs through follow-up calls so the final model aligns with live project behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 53% |

| Mid tier: 52% | Functional/Unit leaders: 24% | EMEA: 29% |

| Smaller Players: 18% | Managers: 60% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach where mobile IoT connection counts, LTE coverage readiness, and NB-IoT and LTE-M adoption rates are used to reconstruct addressable revenue by region and key verticals. Since no single data series captures the full market, we then corroborated totals through selective bottom-up checks, including sampling average connectivity and service pricing, validating typical device-to-service attach patterns, and performing light supplier and channel checks to see if implied volumes and value are consistent.

Key inputs that kept the model grounded included active cellular IoT connection growth, module shipment momentum, operator tariff direction, and enterprise rollout pace in utilities, logistics, healthcare, and industrial tracking. We also tracked country-level timing of network feature availability, including deep indoor coverage for NB-IoT. Forecasts were produced using scenario analysis, where adoption curves and pricing trajectories were adjusted based on expert feedback, then stress-tested against macro indicators such as industrial output and telecom capex cycles. Where bottom-up signals were missing for a smaller geography, we used proxy indicators from similar markets and only scaled after a reasonableness check on connections per capita and pricing bands.

Data Validation & Update Cycle

Validation was performed through multiple passes, starting with simple arithmetic checks, then running variance checks across regions, technologies, and end-user industries to explain or correct extreme jumps. Outputs were compared with independent signals such as connection growth statements, public rollout timelines, and implied revenue per connection, then reviewed by another analyst before sign-off.

The report is refreshed on an annual cycle. Interim updates are triggered when material events occur, such as major network sunsets, regulatory changes, or abrupt pricing shifts. Right before delivery, a final update pass is run so clients receive the most current view of the market and its forecast path.

Mordor Intelligence's Lte IOT Market Size Versus Other Published Estimates

Published LTE IoT market sizes can look far apart because each publisher draws the line differently on what counts as LTE IoT revenue, and because the same year can be reported with different FX timing and pricing assumptions. Differences also show up when one estimate is more aggressive on adoption in utilities and logistics, while another assumes slower network readiness and longer proof-of-concept cycles.

Non-cellular LPWAN connectivity and 5G IoT are kept outside Mordor Intelligence's scope, which helps explain why the 2026 total is not inflated by adjacent connectivity revenues. Other figures can also drift when services are treated as a flat add-on, when a single global ASP is used without regional adjustments, or when implied revenue per connection is not re-checked against public rollout and tariff signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.15 B (2026) | |

| Global Consultancy A | USD 2.52 B (2023) | Uses an earlier base year and a broader interpretation of industry coverage, and the CAGR applied to 2030 appears to assume faster adoption without clearly tying pricing to connection mix across regions. |

| Industry Research Firm B | USD 2.70 B (2023) | Leans on a high-growth trajectory to 2032, and the 2023 value can differ when revenue per connection is not normalized by operator tariff levels and when regional weighting is shifted toward Europe. |

The comparison shows that the spread mainly comes from year selection, adjacent-scope inclusions, and how pricing is progressed as deployments scale. By keeping inputs traceable to connection growth, network readiness, and realistic pricing bands, the estimate stays easier to reproduce and to audit when new data points emerge.

Key Questions Answered in the Report

What is the current size of the LTE IoT market?

The LTE IoT market size stood at USD 2.15 Billion in 2026 and is projected to reach USD 4.85 Billion by 2031.

Which region dominates LTE IoT revenue today?

APAC holds 54.40% of 2025 revenue, largely due to China Mobile’s nationwide NB-IoT and LTE-M rollouts.

Why are managed services growing faster than professional services?

Enterprises prefer outsourcing day-to-day connectivity management, pushing managed-service revenue at a 14.92% CAGR while professional services focus on initial integration work.

How do NB-IoT and LTE-M differ?

NB-IoT excels in stationary, ultra-low-power use cases and captured 64.20% share in 2025, whereas LTE-M offers mobility and voice features and is growing faster at 17.95% CAGR.

What is RedCap and why does it matter?

RedCap is a 3GPP Release 17 specification that halves LTE-M power consumption while enabling up to 10 Mbps throughput, expanding cellular IoT into mid-tier wearables and industrial sensors.

Which end-user segment is forecast to grow the quickest?

Healthcare is set to expand at a 17.18% CAGR through 2031, driven by remote patient monitoring and home-care programs requiring reliable wide-area connectivity.

Page last updated on: