IoT Device Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

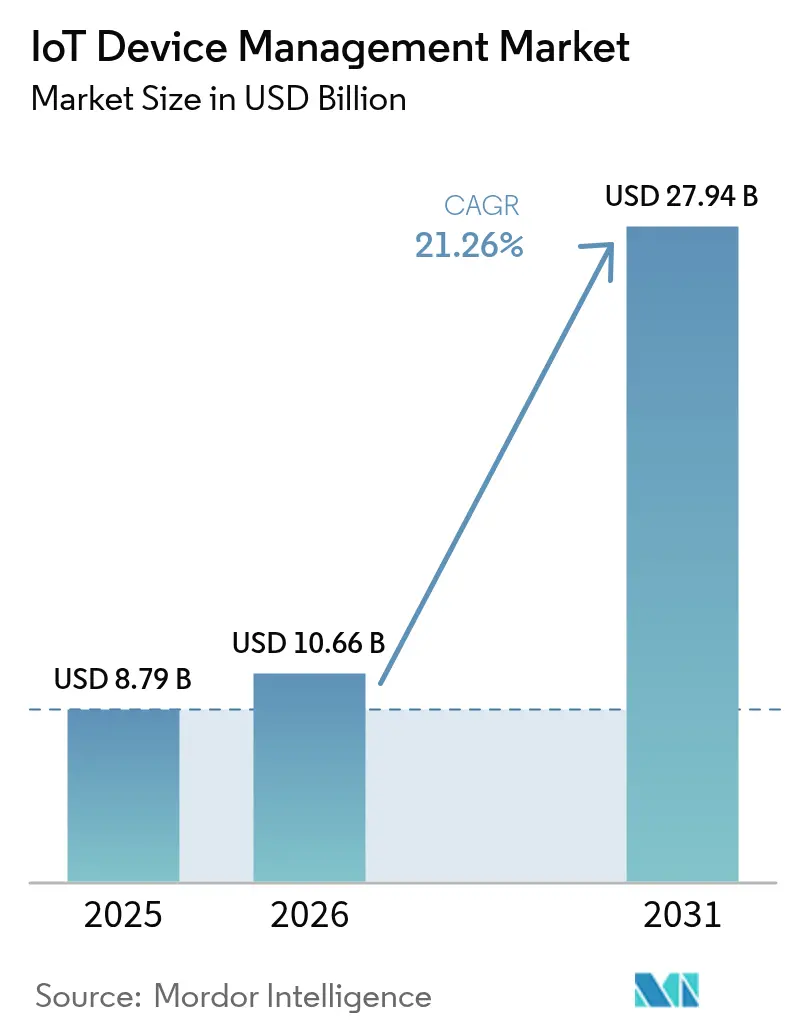

| Market Size (2026) | USD 10.66 Billion |

| Market Size (2031) | USD 27.94 Billion |

| Growth Rate (2026 - 2031) | 21.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Device Management Market Analysis by Mordor Intelligence

The IoT Device Management Market size was valued at USD 8.79 billion in 2025 and estimated to grow from USD 10.66 billion in 2026 to reach USD 27.94 billion by 2031, at a CAGR of 21.26% during the forecast period (2026-2031).

Device fleet expansion, 5G roll-outs, and maturing edge computing architectures are shifting enterprises from reactive break-fix approaches toward predictive, AI-orchestrated lifecycle management. Integrated security has become a decisive purchase factor as regulatory frameworks tighten, and monthly attack volumes surpass 5,000. North America leads in current deployments, yet Asia Pacific is scaling fastest as governments fund smart-city and industrial automation programs. Competitive intensity is rising as hyperscale cloud vendors, industrial specialists, and edge-native start-ups converge on unified, chip-to-cloud platforms.

Key Report Takeaways

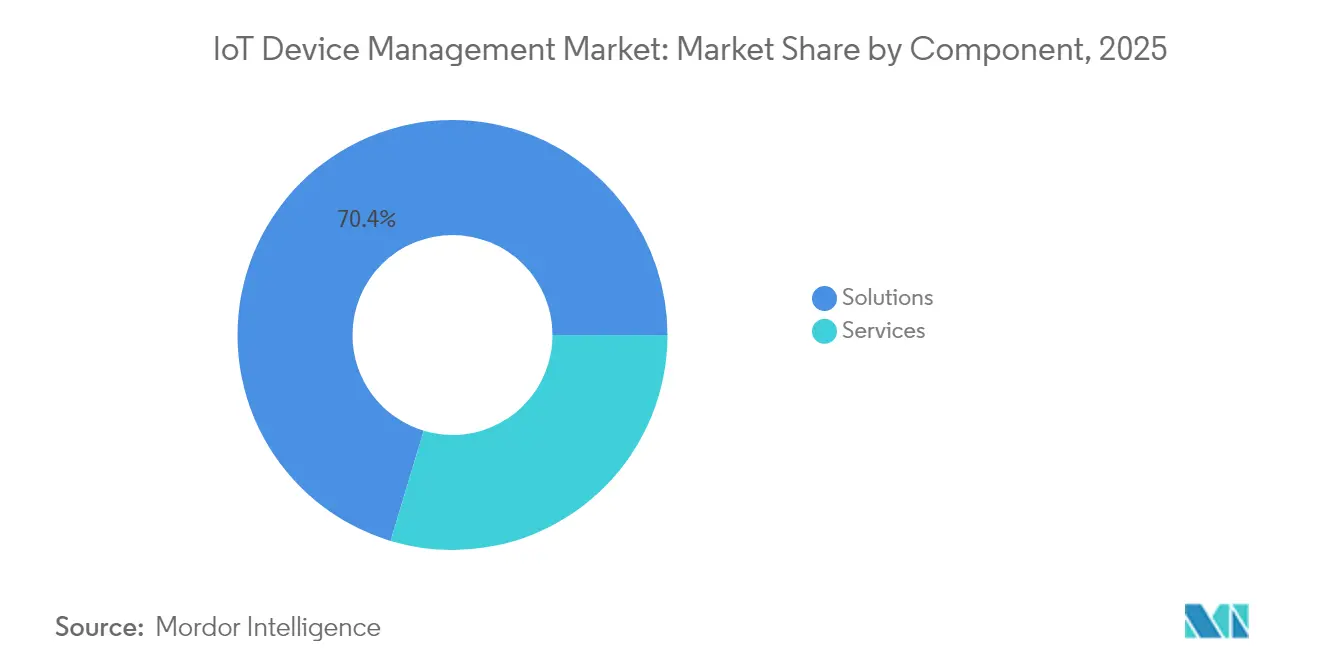

- By component, Solutions retained 70.35% revenue share in 2025, while Services are expanding at a 22.10% CAGR through 2031.

- By deployment type, Cloud held 67.85% of the IoT Device Management market share in 2025, yet Edge-native architectures are advancing at a 26% CAGR to 2031.

- By connectivity, Cellular technologies commanded 45.80% of the IoT Device Management market size in 2025; LPWAN protocols are the fastest-growing at 23.70% CAGR.

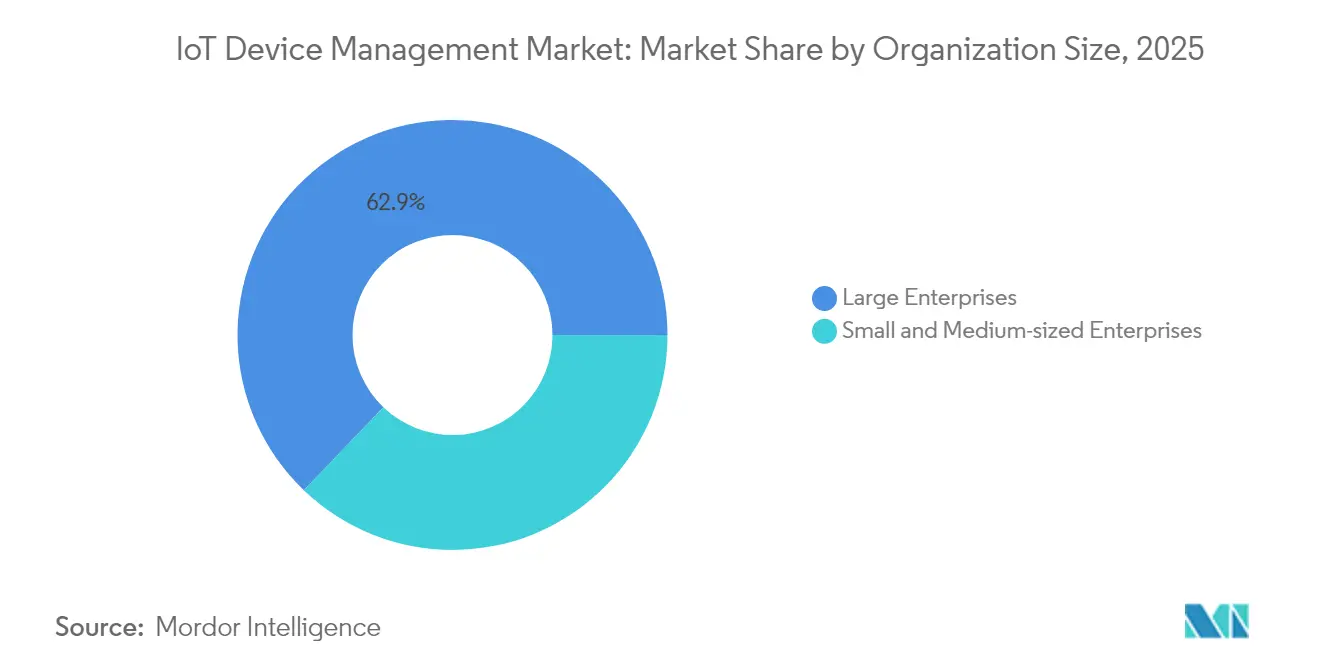

- By organization size, large enterprises led with a 62.85% share in 2025; SMEs are increasing adoption at a 22% CAGR through 2031.

- By end-user vertical, Manufacturing captured 24.35% revenue share in 2025, whereas Smart Cities and Public Safety are forecast to grow at 22.60% CAGR.

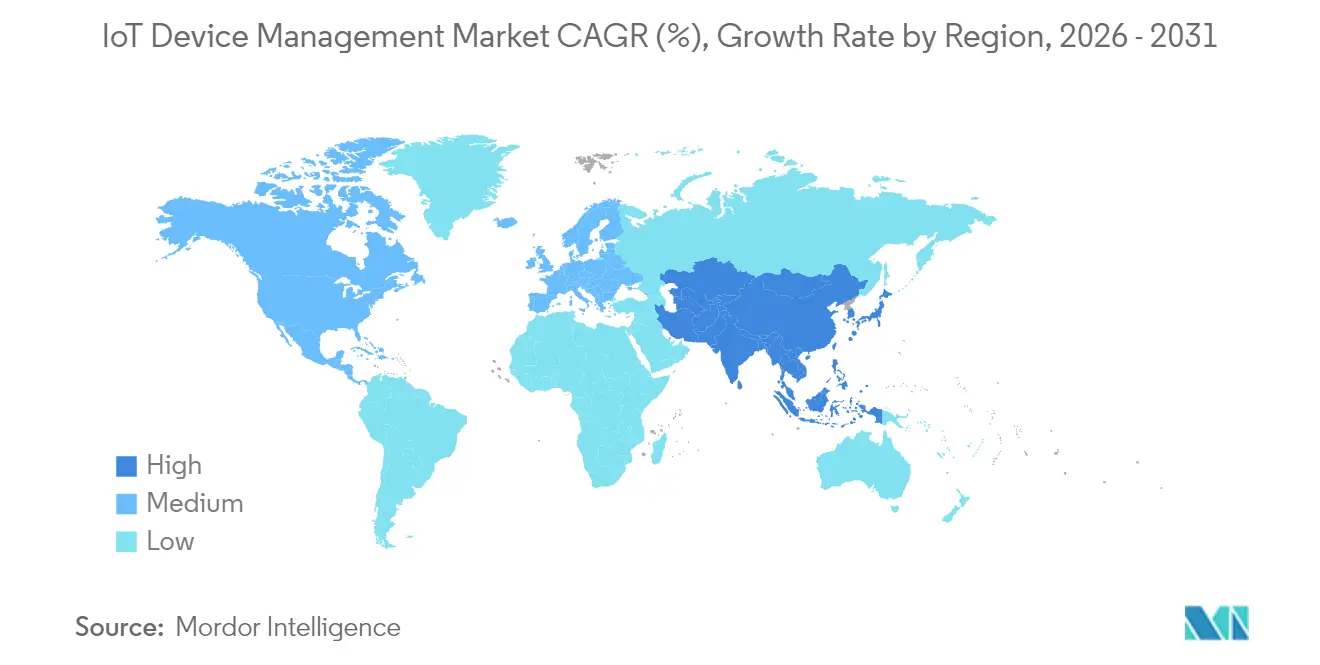

- By geography, North America accounted for 31.75% revenue share in 2025, while Asia Pacific is set to expand at a 24.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IoT Device Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of IoT endpoints | +4.20% | Global (APAC leading) | Medium term (2-4 years) |

| Security and compliance mandates | +3.80% | North America & EU | Short term (≤ 2 years) |

| Edge-cloud convergence | +3.10% | Global | Medium term (2-4 years) |

| 5G and LPWAN roll-outs | +2.90% | APAC core; MEA spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of IoT Endpoints Driving Lifecycle-Management Demand

Global connected-device counts will exceed 75 billion units by 2030, overwhelming traditional IT oversight models and elevating centralized orchestration as a board-level requirement. Factory floors now deploy thousands of heterogeneous sensors that demand automated provisioning, continuous observability, and over-the-air (OTA) firmware governance. Platform engineering teams are standardizing automation templates and security baselines in order to harmonize multi-vendor fleets and ensure auditability across jurisdictions.

Heightened Security and Compliance Mandates for Device Fleets

The EU Cyber Resilience Act, enacted in 2024, mandates secure-by-design principles, software bills of materials, and continuous vulnerability management, with non-compliance fines up to EUR 15 million. Parallel directives in the United States and Japan, combined with the average 5,200 monthly attacks on IoT endpoints, are steering buyers toward platforms that embed zero-trust architectures and real-time threat detection. Thales reports that 55% of organizations now rank IoT security among their top three enterprise risks.

Edge-Cloud Shift Requiring Unified OTA and Remote Diagnostics

Latency-sensitive use cases such as collaborative robotics and autonomous guided vehicles process data locally yet still require centralized policy enforcement. Microsoft’s Azure IoT Edge allows containerized workloads to run at the equipment layer while syncing configuration, telemetry, and OTA updates with the cloud. Compact “delta” patches reduce bandwidth by up to 90%, extending battery life in remote sensors.

5G and LPWAN Roll-outs Unlocking Hyperscale Connection Volumes

5G network slicing delivers deterministic bandwidth and low latency for critical applications, whereas LPWAN variants such as LoRaWAN and NB-IoT provide low-power, wide-area reach for smart-city infrastructure. Cisco forecasts that massive machine-type communications will account for 52% of 5G traffic by 2030. LORIOT projects non-cellular LPWAN links will outnumber legacy 2G/3G M2M connections by 2026, reinforcing the need for protocol-agnostic management back-planes.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented interoperability standards | -2.10% | Global | Medium term (2-4 years) |

| Cross-border data-sovereignty constraints | -1.80% | EU-US-APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Interoperability Standards

Although initiatives such as Matter and OPC UA promote common schemas, the absence of universal frameworks across industrial, consumer, and municipal domains forces enterprises to juggle multiple device-management portals. An MDPI study finds that 67% of multi-vendor deployments still rely on bespoke APIs, inflating integration costs and elongating time-to-value[1]MDPI, “Challenges in IoT Interoperability,” mdpi.com.

Cross-border Data-Sovereignty Constraints

GDPR, India’s Digital Personal Data Protection Act, and China’s CSL impose residency rules that require edge gateways or in-region data lakes, complicating global fleet visibility. Multinational manufacturers must often deploy regionally segmented instances of their device-management stacks, driving up operating expenses and complicating firmware-signing workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Maturation Spurs Service Uptake

Solutions held a commanding 70.35% share in 2025, anchored by modules for security, provisioning, and analytics. The segment is on track for a 21.90% CAGR as enterprises re-architect brownfield assets into policy-driven, cloud-native frameworks. Security management modules are the breakout sub-category, reflecting relentless compliance pressure. Services, at 29.65%, are edging ahead in growth (22.10% CAGR) as brownfield retrofits require systems integration and as-a-service management. Managed services resonate with SMEs that lack embedded engineering teams, while professional services drive complex, multi-factory rollouts. The convergence of the two components signals commoditization at the core platform level and shifts differentiation to vertical accelerators and AI co-pilots.

By Deployment Type: Edge-Native Architectures Gain Share

Cloud continues to dominate with 67.85% share in 2025, but latency-critical workloads are pushing compute to factory floors, utility substations, and roadside cabinets. Edge-native deployments are forecast to log a 26% CAGR, propelled by 5G MEC nodes and GPU-equipped gateways. Hybrid blueprints blend global cloud scalability with deterministic local control, ensuring firmware governance and anomaly detection even during backhaul outages. AI inferencing at the edge reduces raw data backhaul up to 75%, shrinking carbon footprints and lowering carrier fees. Vendors are embedding Kubernetes-compatible runtimes, enabling DevOps-style CI/CD pipelines for OTA firmware and container updates.

By Connectivity Technology: LPWAN Momentum Accelerates

Cellular links (2G/4G/5G) constituted 45.80% of all managed endpoints in 2025, benefiting from a global footprint and SLA guarantees. However, LPWAN alternatives LoRaWAN, NB-IoT, and Sigfox are the fastest-growing cohort at 23.70% CAGR because they offer multi-kilometer reach, multi-year battery life, and sub-USD 1 modules. Netmore’s February 2025 purchase of Senet doubled its LoRa coverage footprint in North America, signaling consolidation toward nationwide public LoRaWAN grids. Device-management platforms must now auto-select optimal bearers based on power profile, data payload, and tariff.

By Organization Size: Democratization Extends to SMEs

Although large enterprises held 62.85% of 2025 revenue, small and medium enterprises are accelerating at 22% CAGR. Low-code orchestration dashboards, subscription-based security add-ons, and pre-certified LTE-M modules are lowering barriers. Over 40% of firms below USD 50 million revenue cite skills shortages as their main obstacle; turnkey managed services and self-service templates mitigate that constraint. The shift expands total addressable units and encourages vendors to tier pricing models by fleet size and SLA levels.

By End-user Vertical: Smart-City Investments Outpace Industry 4.0

Manufacturing led with a 24.35% share in 2025, reflecting decades of SCADA and PLC modernization. Yet municipal digitization budgets are driving a 22.60% CAGR in Smart Cities and Public Safety as urban planners deploy adaptive lighting, waste-management telemetry, and computer-vision surveillance networks. Transportation, healthcare, and energy remain robust adopters as each sector battles downtime risk and regulatory audits. Agriculture is emerging: precision-farming pilots using LoRaWAN soil sensors cut water usage 18% in 2024 field trials conducted in California’s Central Valley

Geography Analysis

North America captured 31.75% revenue in 2025, leveraging mature cloud ecosystems and early adoption in aerospace, automotive, and healthcare. Federal funding for smart-grid resilience and the National Cybersecurity Strategy further stimulates platform upgrades. Asia Pacific is the primary growth engine, expanding at a 24.10% CAGR as governments subsidize factory automation and smart-city rollouts. IDC projects 38.9 billion connected devices in the region by 2030, underpinned by widespread 5G Stand-Alone deployments that simplify SIM provisioning.

China dominates absolute volumes, yet India and Indonesia are posting double-digit growth as carriers light up NB-IoT networks across industrial corridors. Japanese and South Korean OEMs are embedding eSIM/iSIM modules to support post-sale connectivity brokering, fueling regional demand for carrier-agnostic management consoles. Europe holds a substantial share due to GDPR and the Cyber Resilience Act, which obligate rigorous vulnerability patching regimes. These mandates favor vendors offering dependency mapping and cryptographically verifiable OTA pipelines.

Emerging regions in the Middle East and Africa are leapfrogging legacy M2M by adopting satellite-augmented LoRaWAN for oil-field telemetry and remote utility metering. South America’s adoption curve is tied to spectrum liberalization and utility modernization programs, with Brazil piloting AMI projects covering six million smart meters. Across all geographies, sovereign-cloud requirements are driving localized control planes, spurring partnerships between global hyperscalers and in-country data-center operators.

Competitive Landscape

The market remains moderately fragmented, yet consolidation is underway. Gartner’s 2024 Magic Quadrant places AWS, Microsoft, and IBM in the Leaders quadrant, each extending device management with native AI and digital-twin capabilities. Nordic Semiconductor’s USD 165 million acquisition of Memfault in June 2025 created the first silicon vendor offering an integrated chip-to-cloud lifecycle stack, pressuring MCU rivals to emulate similar vertical integration[3]Nordic Semiconductor, “Nordic to acquire Memfault,” nordicsemi.com.

Differentiation is shifting from raw connectivity orchestration toward secure OTA, AI-based anomaly remediation, and vertical accelerators. PTC leverages its ThingWorx platform, paired with Microsoft Azure, to deliver turnkey industrial kits optimized for OEE gains[4]PTC, “ThingWorx and Azure Strengthen Industrial IoT,” ptc.com. Aeris introduced IoT Watchtower in February 2025, bundling cellular connectivity with on-device agent-based intrusion detection, aimed at OEMs requiring NIST compliance out of the box.

Edge-native specialists such as EdgeIQ promote “workflow-as-code” orchestration that treats devices as first-class software objects, offering coarse-grained RBAC and event-driven rule engines. Hardware incumbents Advantech and Huawei embed Kubernetes-light runtimes on gateways, enabling DevOps-style CICD within Brownfield OT estates. The competitive narrative now revolves around who can deliver seamless, policy-driven governance across heterogeneous chipsets, networks, and regulatory zones.

IoT Device Management Industry Leaders

Microsoft

Smith Micro Software

Advantech

Bosch.IO

IBM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Nordic Semiconductor acquired Memfault, forming an end-to-end chip-to-cloud lifecycle platform.

- March 2025: Samsung demonstrated AI-powered vRAN interoperability with NVIDIA at MWC 2025.

- March 2025: T-Mobile, Thales, and SIMPL collaborated on flexible, secure IoT connectivity for global deployments.

- December 2024: Trasna acquired IoTerop to bolster standards-based device management.

Global IoT Device Management Market Report Scope

IoT Device Management makes it effortless to securely register, monitor, organize, and remotely manage IoT devices at scale. IoT Device Management registers connected devices individually or in bulk and easily manages permissions to keep devices secure. IoT Device Management is agnostic to devise type and OS so that devices can be managed from constrained microcontrollers to connected cars, all with the same service, enabling scale fleets and decreasing the cost and effort of managing large and various IoT device deployments.

The IoT device management market is segmented by component (solutions (security solutions, data management, remote monitoring), services (professional services, managed services), organization size (small and medium-sized enterprises (SMEs), large enterprises), end-user vertical (retail, healthcare, utilities, transportation and logistics, manufacturing), and geography (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Security Management |

| Device Provisioning and On-boarding | |

| OTA Firmware and Software Updates | |

| Remote Monitoring and Diagnostics | |

| Data Management and Analytics | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-premise |

| Hybrid |

| Edge-native |

| Cellular (2G/3G/4G/5G) |

| LPWAN (NB-IoT, LoRaWAN, Sigfox) |

| Wi-Fi/Bluetooth |

| Satellite and Others |

| Small and Medium-sized Enterprises |

| Large Enterprises |

| Manufacturing |

| Transportation and Logistics |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Energy and Utilities |

| Smart Cities and Public Safety |

| Agriculture |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Solutions | Security Management | |

| Device Provisioning and On-boarding | |||

| OTA Firmware and Software Updates | |||

| Remote Monitoring and Diagnostics | |||

| Data Management and Analytics | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Type | Cloud | ||

| On-premise | |||

| Hybrid | |||

| Edge-native | |||

| By Connectivity Technology | Cellular (2G/3G/4G/5G) | ||

| LPWAN (NB-IoT, LoRaWAN, Sigfox) | |||

| Wi-Fi/Bluetooth | |||

| Satellite and Others | |||

| By Organization Size | Small and Medium-sized Enterprises | ||

| Large Enterprises | |||

| By End-user Vertical | Manufacturing | ||

| Transportation and Logistics | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Energy and Utilities | |||

| Smart Cities and Public Safety | |||

| Agriculture | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the IoT Device Management market?

The market stands at USD 10.66 billion in 2026 and is forecast to grow to USD 27.94 billion by 2031.

Which region is growing fastest for IoT device management solutions?

Asia Pacific is set to expand at a 24.10% CAGR through 2031, propelled by smart-city funding and industrial automation rollouts.

Why are edge-native deployments gaining traction?

Latency-sensitive applications and on-premises data-sovereignty rules are pushing compute closer to devices, resulting in a 26% CAGR for edge-native architectures.

How are security regulations affecting platform demand?

Frameworks such as the EU Cyber Resilience Act require continuous vulnerability management and penalties up to EUR 15 million, prompting enterprises to favor platforms with integrated, zero-trust security features.

Which connectivity technology is rising fastest?

LPWAN protocols, particularly LoRaWAN and NB-IoT, are growing at a 23.70% CAGR owing to their long-range, low-power profile suitable for smart-city and industrial sensors.

What strategic moves are reshaping the competitive landscape?

Nordic Semiconductor’s acquisition of Memfault, Netmore’s purchase of Senet, and Aeris’ launch of IoT Watchtower exemplify consolidation toward integrated, secure chip-to-cloud stacks.

Page last updated on: