IoT Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

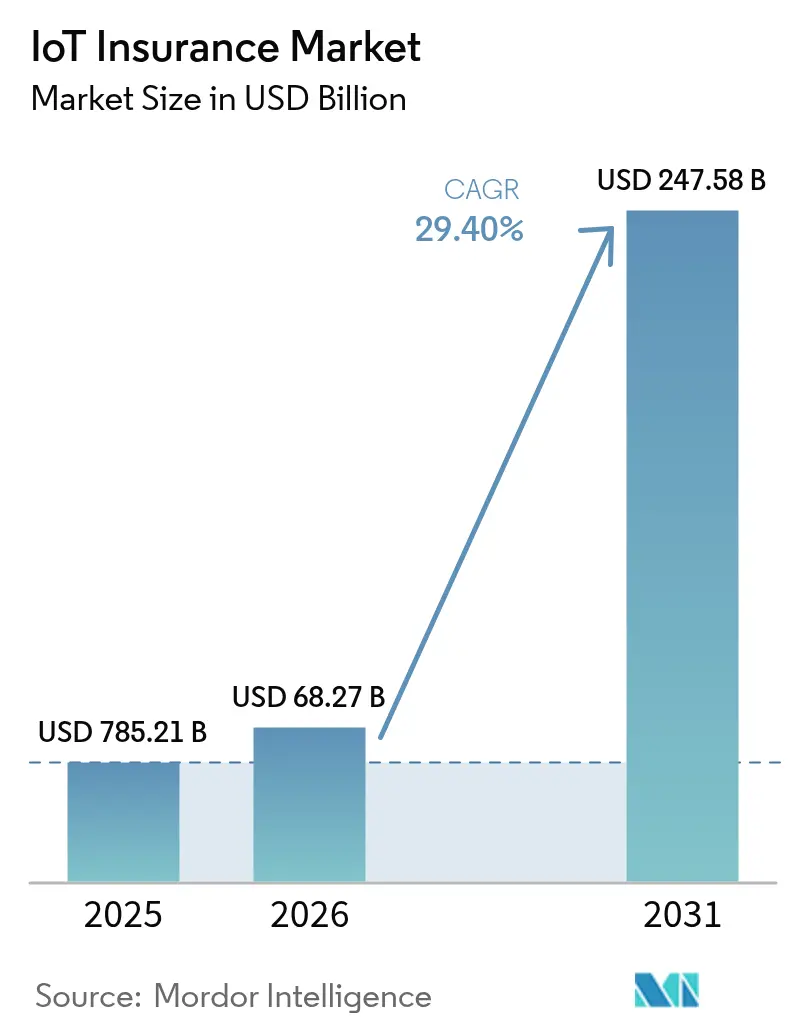

| Market Size (2026) | USD 68.27 Billion |

| Market Size (2031) | USD 247.58 Billion |

| Growth Rate (2026 - 2031) | 29.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT Insurance Market Analysis by Mordor Intelligence

The IoT Insurance Market size was valued at USD 52.78 billion in 2025 and estimated to grow from USD 68.27 billion in 2026 to reach USD 247.58 billion by 2031, at a CAGR of 29.40% during the forecast period (2026-2031). Continuous telemetry from connected vehicles, smart-home devices, wearables, and industrial sensors is moving risk transfer away from claims reimbursement toward real-time loss prevention. Falling sensor prices, reliable cellular and LPWAN coverage, and data-driven pricing mandates in key jurisdictions jointly accelerate adoption. [1]Telnyx, “The Future of IoT Technology: Trends to Watch in 2025,” telnyx.com

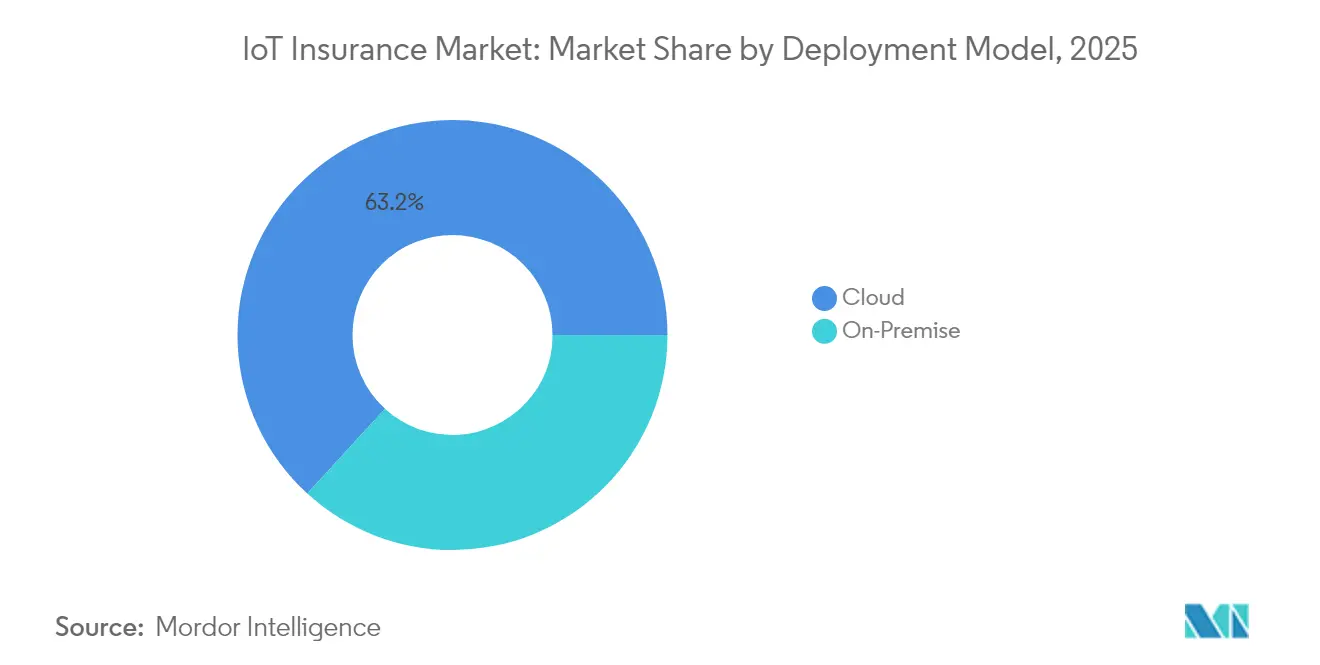

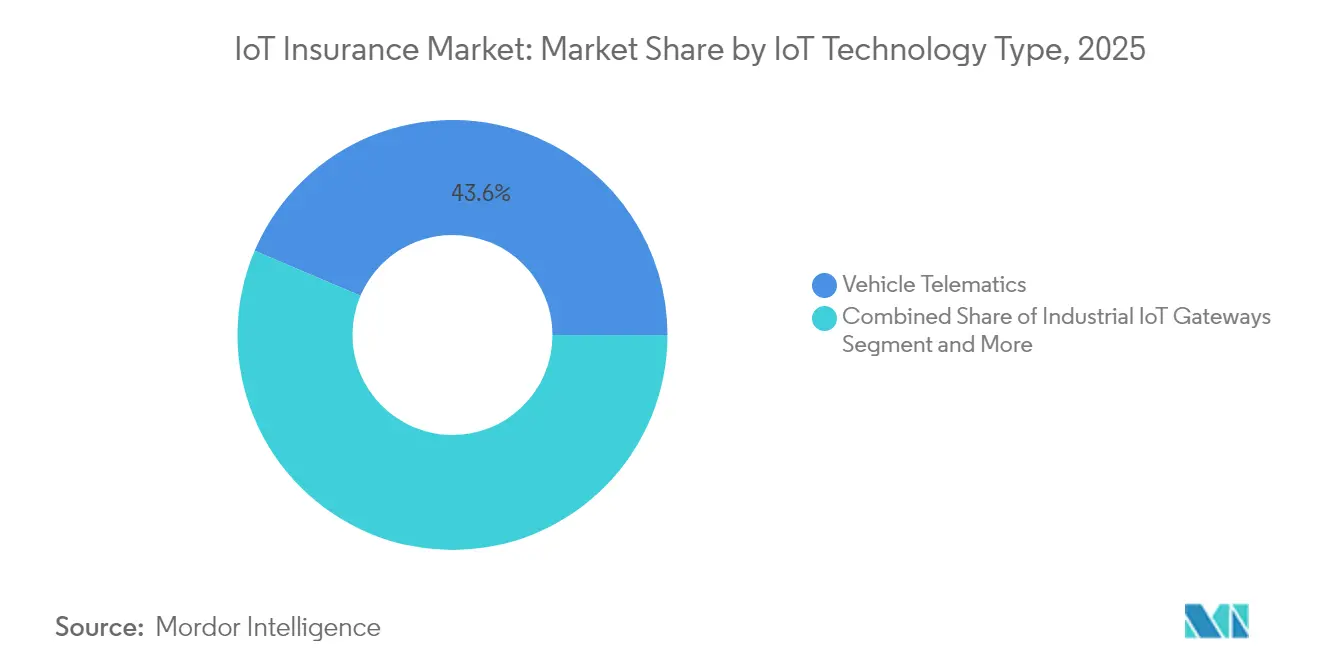

Cloud deployment models capture 63.7% of the IoT insurance market share in 2024 and are expanding at 33.8% CAGR as carriers prioritize elastic computing over capital-intensive on-premise data centers. Property and Casualty products still account for 48.3% of revenue, yet life underwriters are registering the fastest 35.1% CAGR by embedding wearable analytics into underwriting. Vehicle telematics holds a 44.1% share, but the surge of wearables at 34.1% growth confirms that richer biometric data is redefining actuarial models. Regionally, North America leads with 37.8% revenue, while Asia-Pacific’s 34.5% CAGR signals an imminent shift in geographic weight. Competitive intensity is moderate; incumbents such as Munich Re and Zurich are acquiring data-centric insurtechs, whereas focused entrants leverage analytics depth to serve niche verticals. Persistent headwinds include cybersecurity exposure, legacy-core integration, and sensor-data drift, yet early movers with resilient cloud and edge architectures enjoy sizeable first-mover advantages.

Key Report Takeaways

- By deployment model, cloud platforms secured 63.20% of the IoT insurance market share in 2025; hybrid cloud deployments are rising at 32.60% CAGR through 2031.

- By line of insurance, Property and Casualty dominated with 47.80% revenue in 2025, whereas life products are forecast to expand at a 33.20% CAGR to 2031.

- By IoT technology, vehicle telematics accounted for 43.60% share of the IoT insurance market size in 2025 and faces the fastest growth from wearables, advancing at 32.80% CAGR.

- By end-user industry, automotive retained 33.00% revenue in 2025; healthcare is projected to grow at 31.60% CAGR owing to continuous health-metric monitoring.

- By geography, North America led with 37.20% revenue in 2025, while Asia-Pacific is poised for a 33.00% CAGR, reflecting rapid digitalization and regulatory liberalization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IoT Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Usage-based insurance (UBI) proliferation | +8.2% | North America and Europe | Medium term (2-4 years) |

| Smart-home and industrial sensor uptake | +6.8% | North America and EU → APAC | Long term (≥ 4 years) |

| Declining IoT hardware and connectivity cost | +5.4% | Global | Short term (≤ 2 years) |

| Regulatory pressure for data-driven pricing | +4.1% | EU and selected US states | Medium term (2-4 years) |

| Parametric, trigger-based P&C products | +3.7% | Global | Long term (≥ 4 years) |

| Reinsurers’ demand for live portfolio data | +2.8% | Major reinsurance hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Usage-Based Insurance (UBI)

Telematics-enabled UBI is redefining personal and commercial auto premiums as real-time driver behavior replaces static demographic factors. Progressive wrote USD 6.684 billion in net premiums during February 2025, a 17% year-over-year rise driven chiefly by telematics policies that now represent 18% of its book. Fleet operators replicate those gains; a luxury transport provider cut insurance spend by 15% after implementing Samsara’s connected-operations suite, confirming enterprise appetite for granular behavioral scoring. [2]StockTitan, “How Samsara’s AI Platform Transformed This Luxury Transport Fleet,” stocktitan.net AI-driven pattern recognition further predicts collision-prone maneuvers, enabling proactive coaching that lowers claims frequency and ultimately reduces loss ratios for carriers.

Adoption of Smart-Home and Industrial Sensors

Water escape, fire, and equipment failure account for a majority of property and industrial losses; low-cost sensors address these pain points by alerting users and insurers before damage escalates. State Farm has shipped 2 million Ting electrical-fire sensors, reporting an 80% reduction in related claims across 700,000 connected homes. In commercial settings, HSB’s Relayr analytics suite lifts revenue for elevator maintenance partners by 12% through predictive servicing that prevents business interruption. Insurers match these preventive gains with premium discounts ranging from 5% to 20% to encourage wider device adoption.

Rapid Fall in IoT Hardware and Connectivity Costs

Global cellular IoT subscriptions will surpass 3 billion by 2027 as economies of scale and specialized chipsets lower unit cost and energy consumption. Qualcomm alone generated more than USD 1 billion from IoT chips in 2024, proving the commercial maturity of purpose-built silicon. Innovations such as eSIMs streamline device onboarding, while battery-free sensors minimize field maintenance. These cost curves unlock access for SMEs that historically lacked capital to employ telemetric risk controls, expanding the addressable IoT insurance market.

Regulatory Push for Data-Driven Pricing

Legislation is mandating transparent data usage and robust cybersecurity as prerequisites for IoT-enabled underwriting. Europe’s Data Act obliges manufacturers to guarantee user-friendly data portability from January 2024, removing a long-standing barrier to multi-brand sensor ecosystems. California’s SB 354 codifies consumer consent and limits secondary data sharing, nudging carriers toward permission-based analytics. Strict timelines around breach notification and product security incentivize investment in secure-by-design hardware and cloud infrastructures, accelerating trust-led growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cyber vulnerability | -4.3% | Global, stricter in EU and CA | Short term (≤ 2 years) |

| Legacy-core system integration | -3.1% | North America and Europe | Medium term (2-4 years) |

| Sensor-data reliability drift | -2.8% | Global industrial use | Long term (≥ 4 years) |

| Antitrust scrutiny of OEM–insurer data | -1.9% | US and EU automotive | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Exposure

A global IT outage in July 2024 struck 8.5 million systems and inflicted USD 10-15 billion in economic loss, underscoring the systemic risk of interconnected devices. Zurich lists cyber threats among the top five risks facing electronics manufacturers, warning that compromised firmware can trigger cascading losses for both carriers and insureds. Compliance with Europe’s forthcoming Cyber Resilience Act can cost non-conforming vendors up to EUR 15 million in penalties, creating adoption friction yet offering a competitive moat for firms that build secure architectures upfront.

Legacy-Core Integration Complexity

Many global insurers still operate COBOL-based policy systems that cannot ingest high-velocity IoT data streams. Modernization projects often span multiple years and budgets in the hundreds of millions, producing short-term capability gaps between greenfield digital entrants and traditional carriers. Hybrid “strangler-fig” approaches that wrap legacy cores with microservices are emerging as pragmatic paths, yet the learning curve continues to delay scalable IoT roll-outs, especially within multiline incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Dominates Digital Transformation

Cloud environments control 63.20% of the IoT insurance market and will expand at a 30.70% CAGR, lifting the IoT insurance market size for cloud platforms to USD 166.31 billion by 2031. Elastic compute, API openness, and managed security patches free carriers from maintaining capital-intensive data centers. Samsara’s connected-operations cloud reached USD 1.458 billion in ARR in Q4 2025, illustrating how scalable telemetry architectures translate into enterprise adoption.

On-premise deployments persist in heavily regulated jurisdictions or where data sovereignty statutes prohibit offshore processing. Even so, security certifications such as FedRAMP High and ISO 27018 have reduced the perceived risk of multi-tenant clouds, prompting phased migration away from local servers. Edge nodes are increasingly integrated into cloud stacks, ensuring ultra-low latency for autonomous vehicle coverage while central analytics refine pricing algorithms. As hybrid models mature, carriers gain situational flexibility without compromising centralized actuarial oversight.

By Insurance Line: Property and Casualty Leadership Faces Life Disruption

Property and Casualty lines hold 47.80% of 2025 revenue, representing the largest IoT insurance market size by product class. Smart-home and industrial sensors deliver tangible loss-avoidance, making P&C a natural first adopter. However, life underwriters are growing at 33.20% CAGR; they leverage continuous wearable data to refine mortality assumptions and incentivize healthy behavior through dynamic premiums.

Commercial lines increasingly embed industrial IoT into workers’ compensation, where predictive maintenance lowers injury frequency. The shift from retrospective claims adjustment to preventive analytics compresses combined ratios and appeals to reinsurers seeking demonstrable portfolio telemetry. Longer term, cross-line bundling—such as combining life, auto, and home policies around a single sensor suite—will blur historic product boundaries and reward data-centric platforms.

By IoT Technology Type: Vehicle Telematics Maturity Meets Wearables Innovation

Vehicle telematics contributed 43.60% IoT insurance market share in 2025 and remains foundational to usage-based pricing. Mature ELD mandates in North America and Europe have created a robust device footprint, allowing carriers to apply risk scoring at scale. Yet wearables and health devices exhibit 32.80% CAGR, confirming a pivot toward biometric-driven underwriting where loss prevention directly correlates with sustained behavior change.

Smart-home sensors sharply reduce water escape and electrical fire claims, gaining traction among homeowners attracted by instant alerts and policy discounts. Industrial gateways funnel real-time equipment metrics into predictive maintenance models that curtail business interruption. Environmental sensors underpin parametric cover; for example, remote flood gauges automatically trigger payouts to protect SMEs against extreme weather volatility, strengthening customer trust through rapid claims settlement.

By End-user Industry: Automotive Maturity Enables Healthcare Innovation

Automotive fleets and personal lines accounted for 33.00% revenue in 2025, underpinned by decades of telematics evolution. In 2025, Japanese carrier Aioi Nissay Dowa rolled out a tourist-focused telematics app to improve road safety while stimulating regional travel. However, healthcare is growing fastest at 31.60% CAGR as insurers harness continuous glucose, heart-rate, and sleep data to build dynamic mortality models and preventive care incentives.

Residential markets capitalize on water-leak and fire-sensor discounts, while industrial facilities deploy vibration and temperature probes to slash unscheduled downtime that often costs millions per outage. Logistics and public-infrastructure projects leverage cargo trackers and structural-health monitoring to reduce transit losses and extend asset life. The future competitive edge lies in synthesizing multi-domain signals across auto, home, health, and commercial assets to generate a holistic customer-level risk graph.

Geography Analysis

North America’s 37.20% revenue share in 2025 derives from well-established telematics regulations and widespread consumer acceptance. State Farm’s mass deployment of Ting sensors and Progressive’s 18% policy-in-force growth illustrate a broad shift toward sensor-mediated value propositions. Canadian regulators are tailoring AIDA and CPPA privacy laws to balance innovation with consumer sovereignty, fostering gradual yet steady device uptake.

Europe experiences cohesive growth through the EU Data Act and forthcoming Cyber Resilience Act, which standardize device security and data sharing across 27 member states. EIOPA notes that 17% of carriers already offer motor insurance linked to IoT and expects penetration to climb as compliance frameworks build consumer confidence. Germany, France, and the United Kingdom spearhead adoption, while newer EU members benefit from cohesion funds that expand broadband coverage required for massive IoT roll-outs.

Asia-Pacific records a 33.00% CAGR, driven by India’s FDI ceiling lift to 100% that invites multinational capital, and China’s NFRA guidelines that delineate AI and data-governance rules. Australian and New Zealand fleets will rise from 1.6 million telematics units in 2023 to 2.7 million by 2028, cementing regional auto dominance. Japan pursues incremental generative-AI pilots within insurers like Mitsui Sumitomo to complement meticulous risk cultures, thereby avoiding abrupt operational shifts.

Latin America and the Middle East and Africa remain nascent yet promising. Mexico’s improving 5G coverage and Brazil’s open-insurance regime are expected to shorten the adoption lag. Gulf Cooperation Council countries invest in smart-city megaprojects where embedded sensor grids naturally dovetail with commercial IoT coverage for infrastructure, property, and cyber lines.

Competitive Landscape

The IoT insurance market balances traditional insurer depth with venture-backed insurtech agility. Munich Re’s purchase of Next Insurance embeds digital underwriting into its ERGO subsidiary and reflects a broader reinsurer strategy to secure real-time portfolio data feeds. Travelers finalized a USD 435 million acquisition of Corvus to fortify cyber expertise, further blending telematics and cyber underwriting.

Partnerships eclipse outright M&A for many carriers. Allianz Partners joined helmet-maker Cosmo Connected to bundle micromobility coverage into connected headgear at the point of sale. Bamboo Insurance distributes Whisker Labs’ Ting sensors free of charge, illustrating how device subsidies convert risk avoidance into loyalty. Start-ups such as Descartes Underwriting focus on parametric models that transfer flood risk via dense sensor networks deployed by partners like Previsico, tackling underserved SMB segments.

Intellectual property race is intensifying around sensor-data ingestion, predictive analytics, and instant claims automation. Patent filings from carriers and chipmakers alike underscore the strategic value of controlling unique algorithms that translate raw telemetry into pricing and loss-avoidance recommendations. As the cost of telemetry hardware falls, sustainable differentiation increasingly pivots on analytic depth, ecosystem reach, and brand trust.

IoT Insurance Industry Leaders

Octo Telematics S.p.A.

Cambridge Mobile Telematics, Inc.

Geotab Inc.

CalAmp Corp.

Samsara Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Soracom and Marubeni created a joint venture to scale global IoT connectivity that underpins multi-industry insurance applications.

- April 2025: Bamboo Insurance launched the Ting program, distributing Whisker Labs’ fire-prevention sensors to 5,000 homeowners.

- March 2025: Munich Re completed its acquisition of Next Insurance to accelerate IoT-enabled products within ERGO.

- March 2025: Selective Insurance integrated Ting into its value-added homeowner services catalogue.

- February 2025: Allianz Partners collaborated with Cosmo Connected to embed micro-mobility insurance directly into connected helmets.

- January 2025: Aioi Nissay Dowa Insurance launched a telematics app in Okayama targeting foreign tourists to enhance road safety.

Global IoT Insurance Market Report Scope

IoT-connected insurance has opened up new scope for insurance companies and also for IoT solutions providers. The companies can utilize sensors to monitor the state of an insured risk and analyze it throughout the insurance value chain.

The IoT Insurance Market is segmented by End-user Industry (Retail and Commercial, Residential (Smart homes), Automotive, Industrial, Healthcare), and by Geography (North America, Europe, Asia-Pacific, Latin America, Middle, East & Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Cloud |

| On-Premise |

| Property and Casualty |

| Life |

| Health |

| Commercial Lines |

| Vehicle Telematics |

| Smart-Home Sensors |

| Wearables and Health Devices |

| Industrial IoT Gateways |

| Environmental and Parametric Sensors |

| Retail and Commercial |

| Residential (Smart-homes) |

| Automotive |

| Industrial |

| Healthcare |

| Public Infrastructure |

| Logistics and Navigation |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| By Insurance Line | Property and Casualty | ||

| Life | |||

| Health | |||

| Commercial Lines | |||

| By IoT Technology Type | Vehicle Telematics | ||

| Smart-Home Sensors | |||

| Wearables and Health Devices | |||

| Industrial IoT Gateways | |||

| Environmental and Parametric Sensors | |||

| By End-user Industry | Retail and Commercial | ||

| Residential (Smart-homes) | |||

| Automotive | |||

| Industrial | |||

| Healthcare | |||

| Public Infrastructure | |||

| Logistics and Navigation | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the IoT insurance market?

The IoT insurance market is valued at USD 68.27 billion in 2026 and is projected to reach USD 247.58 billion by 2031.

Which deployment model is growing fastest?

Cloud platforms lead with 63.20% share in 2025 and a 30.70% CAGR because they support real-time data processing without heavy capital expense.

Why is life insurance the fastest-growing line?

Wearable sensors supply continuous biometric data that enables personalized premiums, pushing life products to a 33.20% CAGR.

Which region offers the highest growth potential?

Asia-Pacific is advancing at 33.00% CAGR due to rapid digital adoption and liberalized foreign-investment rules in markets such as India and China.

How do connected devices reduce insurance losses?

Sensors detect anomalies—like excessive speed, water leaks, or electrical faults—in real time, allowing preventive action that lowers claim frequency and severity.

What are the main barriers to IoT insurance adoption?

Cybersecurity threats, stringent data-privacy laws, and complex integration with legacy policy-administration systems remain the top challenges.

Page last updated on: