Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

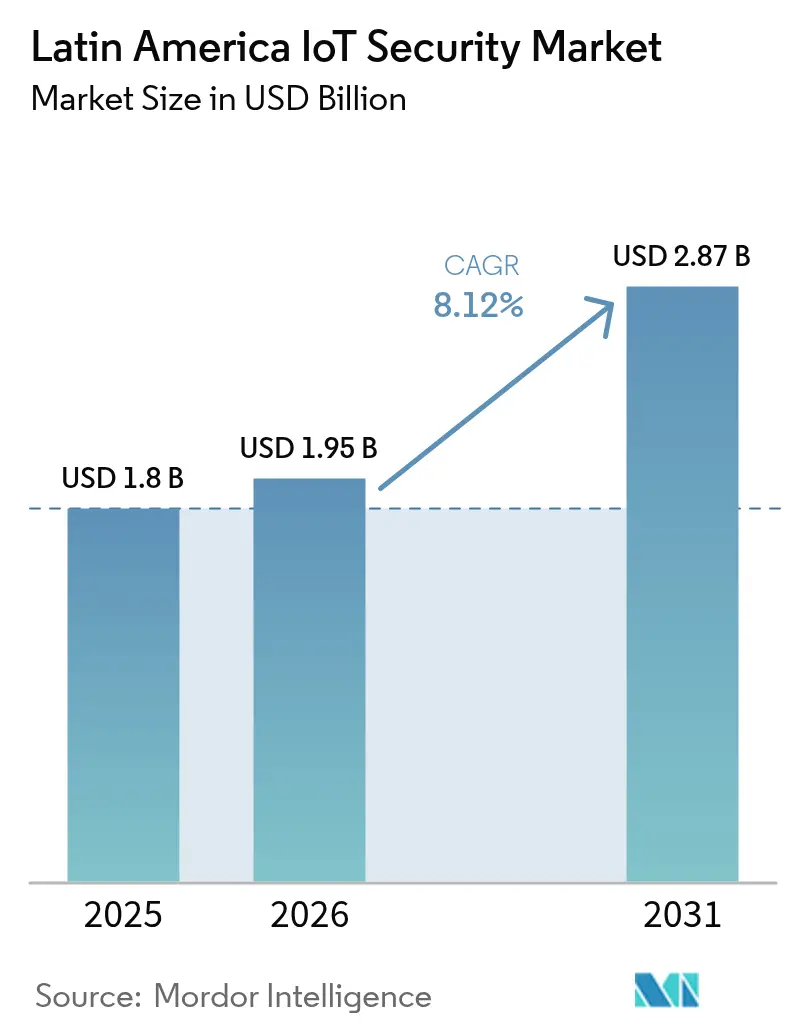

| Base Year Market Size (2025) | USD 1.8 Billion |

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America IoT Security Market Analysis by Mordor Intelligence

Latin America IoT security market size in 2026 is estimated at USD 1.95 billion, growing from 2025 value of USD 1.8 billion with 2031 projections showing USD 2.87 billion, growing at 8.12% CAGR over 2026-2031. Expanding smart-city surveillance programs in Brazil, mandatory Zero-Trust rules for Chilean critical infrastructure, and rapid 5G rollouts across Mexico propel spending on connected-device protection. Investments accelerate as enterprises confront record healthcare breaches that exposed 182.4 million people in 2024, while semiconductor shortages and fragmented privacy laws temper near-term deployment velocity. Rising NB-IoT network hardening contracts signed by mobile operators reflect a strategic shift toward bundled security services that monetize connectivity upgrades. Regional manufacturers also increase cloud-based threat-detection subscriptions to compensate for limited access to crypto-chips required for hardware-level encryption.

Key Report Takeaways

- By geography, Brazil led with 40.62% revenue share in 2025; Mexico is forecast to expand at a 9.78% CAGR through 2031.

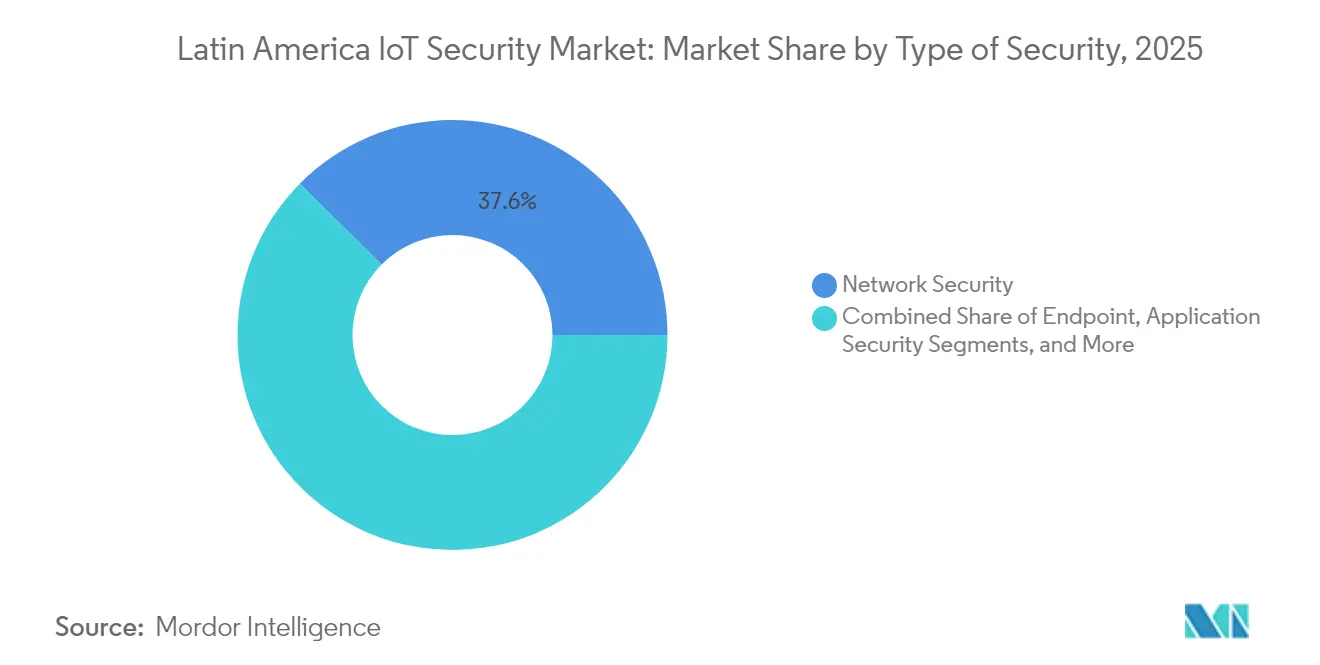

- By type of security, Network Security held 37.57% of the Latin America IoT security market share in 2025, while Cloud Security is poised for an 11.05% CAGR to 2031.

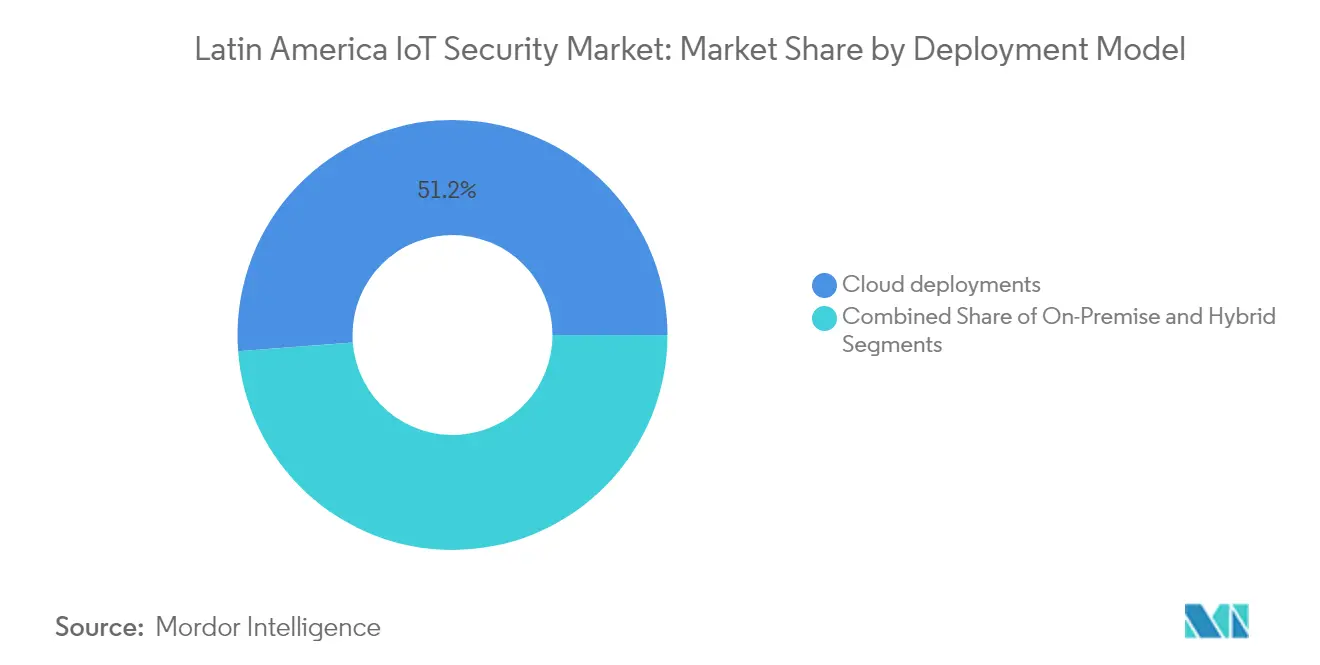

- By deployment model, Cloud captured 51.20% of the Latin America IoT security market size in 2025 and is growing at a 12.06% CAGR to 2031.

- By end-user, Manufacturing accounted for 25.58% revenue share in 2025; Healthcare is advancing at a 12.92% CAGR through 2031.

- By solution, Identity and Access Management held 23.68% share in 2025, whereas Security and Vulnerability Management is set for a 12.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America IoT Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Roll-out of Smart-Surveillance Cities (Brazil PAC 4.0) | +1.8% | Brazil, with spillover to urban centers across LATAM | Medium term (2-4 years) |

| Telco NB-IoT Network Hardening Upsell | +1.2% | Global, with early gains in Mexico, Colombia, Chile | Short term (≤ 2 years) |

| Zero-Trust Mandate in Chile Critical-Infra Law | +0.9% | Chile, with regulatory influence across LATAM | Long term (≥ 4 years) |

| IoT Insurance-Premium Discounts | +0.7% | Brazil, Mexico, Colombia core markets | Medium term (2-4 years) |

| Open-source SBOM Tooling in Edge-Linux | +0.5% | Global, with technical adoption in Brazil, Argentina | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Roll-out of Smart-Surveillance Cities (Brazil PAC 4.0)

Brazil’s PAC 4.0 program obliges municipalities to protect video sensors and data lakes with strong encryption, micro-segmentation, and AI-driven anomaly detection. City procurements reference international standards, prompting vendors to certify devices for ISO / IEC 27001 compliance. Neighbouring capitals replicate procurement templates, enlarging the addressable base for endpoint and network-access controls. Integrators report that surveillance contracts specify centralised security-operations dashboards able to correlate OT and IT events in real time. The requirement for tamper-proof audit trails also drives demand for secure hardware modules that remain scarce due to global crypto-chip shortages.[1]Organisation for Economic Co-operation and Development, “Going Digital in Brazil,” oecd.org

Telco NB-IoT Network Hardening Upsell

Mobile operators now package fraud-prevention APIs, secure bootstrapping, and SIM-level encryption with every NB-IoT line activation, turning connectivity into a security-enhanced service. Mexico’s four carriers jointly unveiled Open Gateway security APIs in 2024, and early adopter banks use these tools to cut SIM-swap fraud incidents by double digits. Similar offerings appear in Colombia and Chile as 5G standalone cores come online. Contract terms increasingly bundle AI-based threat scoring engines that analyse signalling traffic to block botnet formation. For operators, these services raise average revenue per user while locking in enterprise customers for multiyear periods.

Zero-Trust Mandate in Chile Critical-Infra Law

Chile’s 2025 law compels electric, water, and port operators to authenticate every device request and log each transaction for at least five years. The statute triggers retrofit projects in neighbouring markets where multinational utilities harmonise policies across operations. Consulting budgets expand for identity-governance rollouts, privileged-access vaults, and micro-segmentation gateways that separate OT and IT domains. Vendors offering reference architectures aligned with NIST SP 800-207 capture early design-win advantages.

IoT Insurance-Premium Discounts

Insurers now use automated cyber-health reports to calibrate policy pricing. SentinelOne’s WatchTower service grades firmware patch levels, attack-surface exposure, and threat-response times, allowing underwriters to reward firms that exceed baseline scores with premium reductions. CFOs leverage these savings to justify incremental security budgets, creating a virtuous cycle of continuous improvement. Industry analysts note that discounted policies stimulate uptake of managed detection and response services among small and midsize enterprises that previously lacked dedicated security talent. Over time, actuarial datasets generated through these programs inform evidence-based ROI metrics for security investments.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crypto-chip Supply Crunch (FAB shift to AI) | -1.50% | Global, with acute impact on Brazil, Mexico manufacturing | Short term (≤ 2 years) |

| Fragmented Privacy Regimes across LATAM | -0.80% | Regional, with compliance complexity in Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Legacy 3G Devices with Un-patchable Firmware | -0.60% | Regional, concentrated in rural areas across LATAM | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crypto-Chip Supply Crunch (FAB Shift to AI)

Foundries redirect capacity toward high-margin AI accelerators, limiting secure element shipments that protect IoT credentials at hardware level. Device makers face lead-times that exceed 40 weeks, forcing many to ship boards equipped with software-only key storage that attackers can bypass. Price hikes of up to 70% for trusted-platform modules inflate bill-of-materials costs, squeezing margins for local OEMs supplying municipal projects. Some buyers postpone rollouts until supply stabilises, translating into slower endpoint security revenue recognition for vendors. Governments consider temporary import-tariff waivers to encourage rapid sourcing from alternate geographies.

Fragmented Privacy Regimes Across Latin America

Brazil’s LGPD, Argentina’s PDP, and Chile’s draft data-protection bill differ on breach-notification windows and cross-border transfer rules. Multinationals therefore maintain separate data-sovereignty zones, duplicating logging infrastructure and compliance audits. Legal uncertainty prolongs procurement cycles as buyers insist that vendors demonstrate localisation controls. Compliance overheads absorb security budgets that could otherwise fund threat-hunting or posture-management projects. Regional standardisation talks have yet to yield harmonised guidelines, implying persistent complexity through the decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Security: Network Dominance Amid Cloud Acceleration

Network Security generated USD 676.3 million in 2025, equal to 37.57% of the Latin America IoT security market share, as perimeter firewalls and secure gateways remained baseline safeguards for expanding device fleets. The Cloud Security segment is forecast to add USD 492 million by 2031, climbing at an 11.05% CAGR as enterprises migrate workloads and insist on policy consistency across multi-cloud tenancy. Hybrid work models also fuel demand for zero-trust network-access solutions that blend on-premises and SaaS controls.

Cloud-native platforms now bundle posture management, runtime protection, and software bill-of-materials scanning in one subscription, reducing tool sprawl. Microsoft’s firmware analysis preview underscores a pivot toward deep code visibility that spans device, network, and cloud layers. As these converged offerings mature, analysts expect the Latin America IoT security market to rebalance, yet network appliances will still sell into brownfield industrial sites where cloud reach remains limited.

By Solutions: IAM Leadership Challenged by SVM Innovation

Identity and Access Management tools booked USD 426.3 million in 2025, translating to 23.68% contribution to the Latin America IoT security market size. They form the authentication backbone for millions of sensors plugging into corporate clouds. Security and Vulnerability Management grows fastest at a 12.28% CAGR, reflecting heightened board-level focus on continuous exposure scoring after high-profile ransomware incidents. Automated SBOM generation enters mainstream procurement criteria, aligning products with forthcoming EU Cyber Resilience Act requirements.

Intrusion Prevention Systems stay relevant for manufacturing lines that demand deterministic latency and immediate packet blocking. Data Loss Protection enjoys regulatory pull in healthcare where electronic patient-record breaches carry steep fines. Consolidated threat-management bundles gain traction among mid-tier firms that cannot staff specialist teams for each protection layer. Vendors that integrate telemetry across these modules position themselves to capture cross-sell revenue streams as compliance obligations tighten.

By Deployment Model: Cloud Supremacy Reinforces Growth

Cloud deployments commanded 51.20% of the Latin America IoT security market size in 2025 and post the highest growth at 12.06% CAGR, signalling broad acceptance of managed security updates delivered via multi-tenant platforms. Subscription models let buyers sidestep capital outlays while benefiting from global threat-intelligence feeds. On-premises installations persist in defence and critical-infrastructure settings where data sovereignty or deterministic latency is non-negotiable.

Hybrid architectures gain momentum in regulated industries that gradually transition archives and non-critical workloads to public clouds but keep real-time control loops local. Vendors cater to these needs with Kubernetes-based security stacks deployable on edge clusters that sync with central analytics. Compliance dashboards now display unified risk scores across cloud and on-premises nodes, easing audit preparation. Such capabilities underpin sustained cloud-centric momentum even as hardware supply shortages temporarily slow new device onboarding.

By End-User: Manufacturing Base Faces Healthcare Disruption

Manufacturing plants accounted for USD 460.5 million and 25.58% of the Latin America IoT security market in 2025, defending programmable-logic controllers and robotic cells against operational shutdowns. Yet hospitals and clinics deliver the fastest future gains, with the healthcare sector on track for a 12.92% CAGR to 2031 as medical-device vulnerabilities expose patient safety risks. Over half of hospital-connected assets carry exploitable flaws, prompting boards to earmark dedicated OT-security budgets. Utilities maintain a steady run-rate for grid-edge node protection, whereas BFSI institutions invest in tokenisation and transaction-integrity services for real-time payments.

Retailers turn to secure point-of-sale gateways that combine malware resistance with location analytics. Government demand expands through public-safety camera rollouts and connected-street-light projects anchored in Brazil’s PAC 4.0 blueprint. Agriculture and transport operators also join pilot programs for secure telemetry, indicating untapped vertical upside once low-earth-orbit connectivity becomes affordable.

Geography Analysis

Brazil retained a 40.62% revenue share in 2025, powered by its National IoT Plan and PAC 4.0 projects that mandate advanced cryptography for municipal camera feeds. The country also suffered 19% of regional cyber incidents, prompting continuous upgrades to SOC automation and endpoint detection pipelines. Large-scale smart-factory pilots in automotive and agro-processing clusters stimulate adoption of secure-boot microcontrollers despite ongoing component shortages.

Mexico is the fastest riser with a 9.78% CAGR through 2031. Government allocations of USD 1.2 billion to national cybersecurity programs accelerate 5G-enabled smart-manufacturing corridors along the US border. Four mobile operators’ Open Gateway APIs fuel an ecosystem of fintech and e-commerce developers that embed SIM-level fraud detection by default. Cloud-security subscriptions expand sharply among local banks seeking to protect real-time payments and customer-data lakes.

Argentina, Colombia, Chile, and Peru together form a tier of emerging demand. Colombia’s cybersecurity revenues grew 14.70% in 2024, driven by AI-assisted threat hunting for oil-pipeline telemetry and smart-office campuses. Chile’s Zero-Trust law spawns niche integrators specialising in continuous verification architectures, while Argentina’s cloud-first digital government programme boosts hybrid deployment sales. Peru pilots secure smart-meter networks in Lima that may replicate across Andean utilities. Collectively, these markets diversify vendor revenue and cushion downside risk from single-country slowdowns.

Competitive Landscape

The Latin America IoT security market remains moderately fragmented. Global cybersecurity suites, regional telcos, and niche IoT-specific start-ups all claim meaningful shares. Telefónica Tech, recognised as a Gartner leader in IoT managed connectivity services for eleven consecutive years, leverages fibre and LTE backbones to bundle device management, SIM provisioning, and threat monitoring under one invoice.

Cloud hyperscalers embed firmware-analysis and edge-security add-ons that deepen account stickiness. Microsoft’s public-preview firmware scanner extends Azure Defender coverage down to binary level, signalling platform players’ intent to own the full security stack. Meanwhile, equipment vendors such as Zyxel issue frequent firmware advisories and over-the-air patch tools to retain trust among broadband operators. [4]Zyxel, “Security Advisory for Command Injection and Insecure Default Credentials Vulnerabilities in Certain Legacy DSL CPE,” zyxel.com

Private equity backed consolidators acquire Latin American MSSPs that hold key public-sector contracts. At the same time, open-source communities release lightweight intrusion-detection agents optimised for low-memory microcontrollers, challenging proprietary vendors on cost. AI-native start-ups focusing on device-behaviour baselining differentiate through unsupervised learning techniques that reduce alert fatigue. Price competition intensifies in entry-level cloud-firewall tiers, yet premium compliance bundles sustain margin resilience.

Latin America IoT Security Industry Leaders

Cisco Systems Inc.

IBM Corporation

Microsoft Corporation

Palo Alto Networks Inc.

Fortinet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Telefónica reported that digital services including IoT and cybersecurity delivered more than 40% of its 2024 B2B revenue, up double digits year-on-year.

- January 2025: he Federal Communications Commission adopted rules requiring telecom carriers to implement formal cybersecurity and supply-chain risk-management plans, a framework likely to influence Latin American regulators.

- October 2024: CrowdStrike and Fortinet launched an integrated offering that combines AI-native endpoint defence with next-generation firewalls to secure distributed IoT environments.

- June 2024: TD SYNNEX created a 250-member cybersecurity practice dedicated to helping Latin American partners design and deploy IoT security solutions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Latin American Internet of Things security market as every hardware-agnostic and software-based safeguard, device authentication, secure gateways, encryption, data-loss prevention, and related managed services that protects industrial and commercial connected endpoints across Brazil, Mexico, Argentina, and the wider region.

We deliberately exclude purely consumer smart-home gadgets without business connectivity, as well as generic enterprise firewalls deployed outside an IoT stack.

Segmentation Overview

- By Type of Security

- Network Security

- Endpoint Security

- Application Security

- Cloud Security

- Others

- By Solutions

- Identity and Access Management (IAM)

- Intrusion Prevention System (IPS)

- Data Loss Protection (DLP)

- Unified Threat Management (UTM)

- Security and Vulnerability Management (SVM)

- Network Security Forensics (NSF)

- Others

- By Deployment Model

- On-Premise

- Cloud

- Hybrid

- By End-User

- Healthcare

- Manufacturing

- Utilities

- BFSI

- Retail

- Government

- Others

- By Geography

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Peru

- Rest of Latin America

Detailed Research Methodology and Data Validation

Primary Research

We then interview CISOs of utilities, plant automation managers, telecom integrators, and regional policy experts, reaching respondents in São Paulo, Mexico City, Bogotá, and Buenos Aires. Their insights clarify average spend per endpoint, security pain points after 5G rollout, and realistic adoption lags, information that desk research rarely quantifies, allowing us to fine-tune penetration assumptions and stress-test early findings.

Desk Research

Our analysts first map the connected-device landscape using freely accessible tier-1 sources such as ITU's "Measuring Digital Development" series, UN Comtrade shipment codes for sensors and modules, CEPALSTAT trade dashboards, and national cybersecurity agency advisories from Brazil and Mexico. Financial signal checks rely on public 10-Ks, IPO prospectuses, and regional telecom filings, while news screening through Dow Jones Factiva and supplier intelligence on D&B Hoovers helps validate vendor footprints. These sources, among several others, provide baseline volumes, price ranges, and regulatory triggers, yet remain only one piece of the evidence puzzle and are not exhaustive.

Market-Sizing & Forecasting

A hybrid top-down build begins with regional connected-device stock, reconstructed from import volumes and mobile-M2M subscriptions, which is then multiplied by verified security attach rates and blended average selling prices. Selective bottom-up checks, supplier revenue roll-ups, and channel price audits flag outliers for adjustment. Key modeling variables include: 1) connected industrial device base, 2) share of devices governed by new Brazilian LGPD compliance, 3) 5G subscriber growth, 4) average annual security spend per endpoint, and 5) incidence of reported IoT breaches. A multivariate regression, cross-validated against three-year breach incidence, projects totals through 2030; scenario analysis buffers currency volatility and policy shifts. Data gaps, such as unreported gray-market hardware, are bridged using weighted proxies derived from customs data and expert estimates.

Data Validation & Update Cycle

Outputs undergo anomaly scans, variance checks against external macro indicators, and a two-step peer review before release. Mordor's team refreshes the dataset every twelve months, while material events, large M&A or landmark regulation, trigger an interim update, ensuring clients always receive a freshly vetted view.

Why Mordor's Latin America Iot Security Baseline Proves Dependable

Published estimates often diverge because firms pick different device universes, layer consumer gadgets unevenly, or refresh models on contrasting cadences.

Key Gap Drivers: some studies fold general cybersecurity revenues into IoT line items, others assume uniform attach rates across verticals, and several convert currencies using static exchange assumptions. By anchoring to device-level evidence, regional price audits, and annually reviewed compliance milestones, Mordor mitigates these pitfalls and delivers a balanced, reproducible baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.8 billion (2025) | Mordor Intelligence | - |

| USD 2.06 billion (2024) | Global Consultancy A | Includes consumer smart-home devices; limited primary outreach; last refresh 2024 |

| USD 7.8 billion (2025) | Industry Advisory B | Bundles wider cybersecurity segments; projects uniform 21 % CAGR from global share; minimal trade recalibration |

The comparison shows that while external figures swing widely, Mordor's disciplined scope selection, variable transparency, and annual update rhythm provide decision-makers with a dependable anchor they can confidently reference when shaping strategy or validating investments.

Key Questions Answered in the Report

What is the current value of the Latin America IoT security market?

The market stands at USD 1.95 billion in 2026 and is projected to reach USD 2.87 billion by 2031.

Which security segment is expanding the fastest?

Cloud Security is advancing at an 11.05% CAGR as enterprises migrate IoT workloads to multi-cloud environments.

Why is healthcare driving future demand?

Hospitals face rising ransomware attacks, and over half of connected medical devices show exploitable flaws, prompting a 12.92% CAGR in healthcare security spending.

How are mobile operators monetising IoT security?

Carriers bundle NB-IoT connectivity with API-level fraud-prevention and threat-intelligence services, boosting average revenue per user.

What limits hardware-based IoT security adoption?

A global crypto-chip shortage diverts semiconductor capacity toward AI accelerators, raising costs and extending lead-times for secure elements.

Which country leads regional spending today?

Brazil accounts for 40.62% of regional revenue thanks to its National IoT Plan and PAC 4.0 smart-city initiatives.

Page last updated on: