Investor ESG Reporting Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

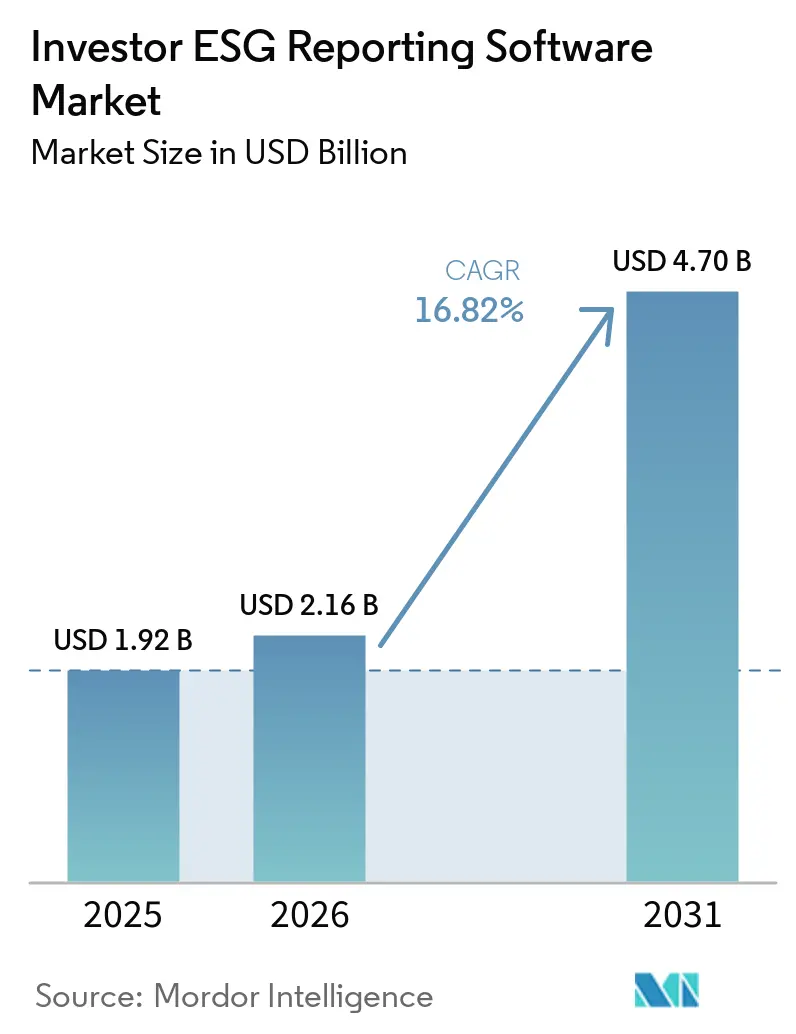

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 4.70 Billion |

| Growth Rate (2026 - 2031) | 16.82% CAGR |

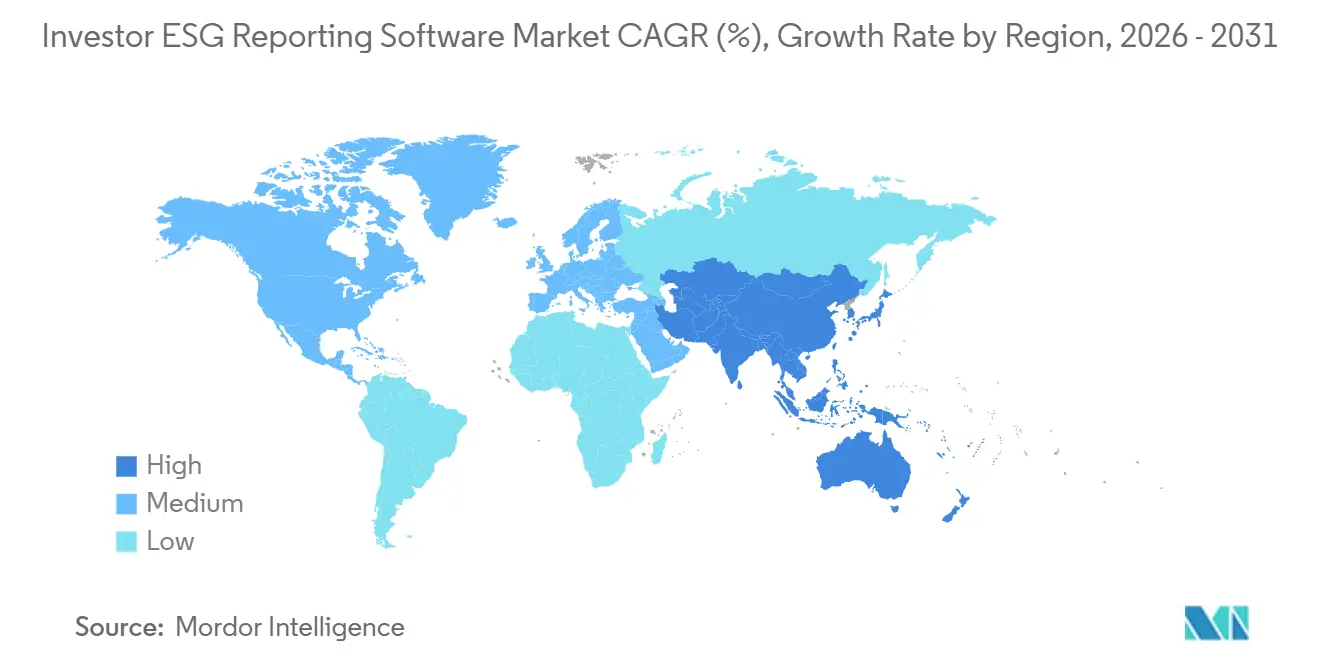

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Investor ESG Reporting Software Market Analysis by Mordor Intelligence

The investor ESG reporting software market size is expected to increase from USD 1.92 billion in 2025 to USD 2.16 billion in 2026 and reach USD 4.70 billion by 2031, growing at a CAGR of 16.82% over 2026-2031. The market is moving from a voluntary disclosure tool toward a core reporting system used by asset managers, private equity firms, pension funds, insurance companies, and sovereign wealth funds that now treat ESG reporting as a fiduciary and governance requirement. Demand is being driven by overlapping sustainability disclosure frameworks across major regions, leading buyers to increasingly want a single platform that supports multiple reporting standards. Procurement decisions are also shifting because chief financial officers and chief investment officers are becoming more involved when software is positioned as a way to reduce recurring reporting effort and improve audit readiness. Product development is moving beyond data capture alone, with vendors placing greater focus on AI-assisted monitoring, workflow controls, and multi-framework reporting outputs that can replace spreadsheet-heavy processes. The main risks remain regulatory recalibration, uneven portfolio company data quality, and the high effort required to connect ESG platforms with portfolio management and finance systems.

Key Report Takeaways

- By functionality, ESG reporting and disclosure management accounted for 29.18% of the investor ESG reporting software market share in 2025, while ESG risk assessment and materiality analysis are projected to expand at a 18.43% CAGR through 2031.

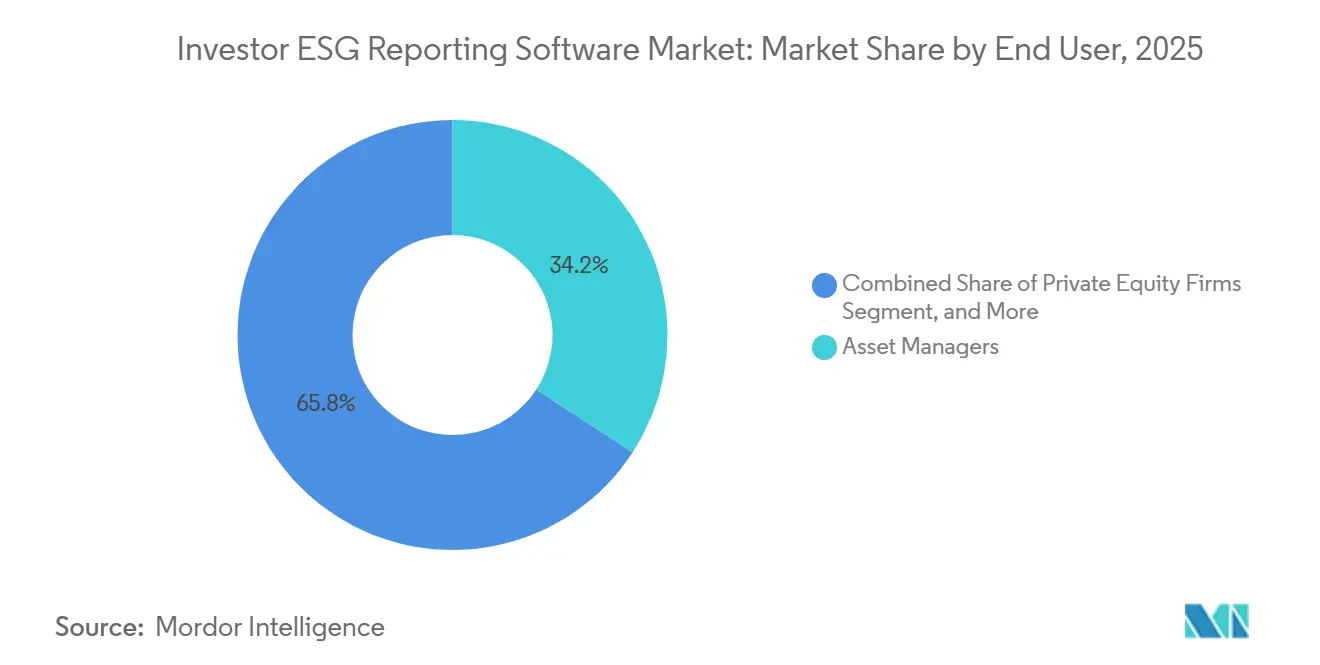

- By end user, asset managers accounted for 34.17% share in 2025, while private equity firms are projected to record the highest CAGR at 17.53% through 2031.

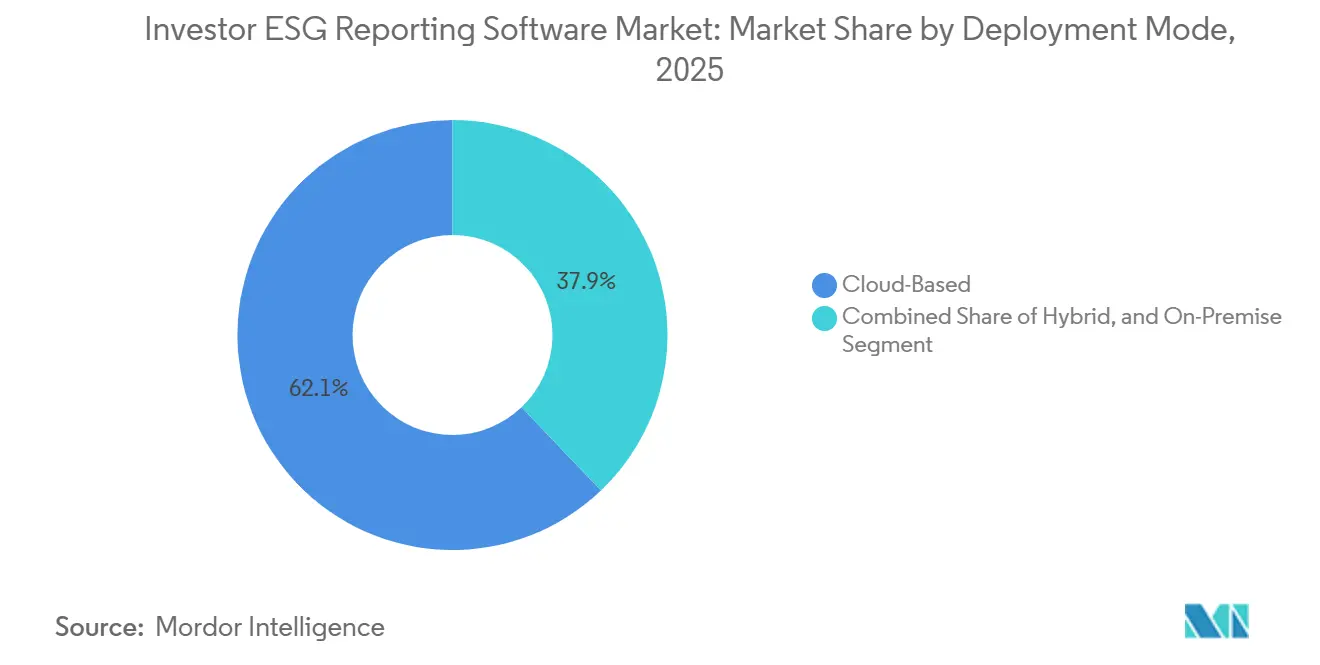

- By deployment mode, cloud-based deployment captured 62.13% share in 2025, while the same segment is expected to grow at the fastest CAGR of 16.83% through 2031.

- By enterprise size, large enterprises held 78.12% of the market share in 2025, while SMEs are projected to expand at a 18.13% CAGR through 2031.

- By geography, North America led with a 34.83% share in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 17.93% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Investor ESG Reporting Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Convergence Across Reporting Regimes | +3.1% | Global, most acute in Europe, Japan, South Korea, and Australia | Short term (≤ 2 years) |

| Rising Demand For Auditable ESG Disclosure Workflows | +2.7% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Expansion Of ESG Data Volumes From Portfolio Companies | +2.0% | Global, with highest intensity in Europe, North America, and core Asia-Pacific markets | Medium term (2-4 years) |

| Pressure To Reduce Spreadsheet Reporting Risk | +1.7% | Global | Short term (≤ 2 years) |

| ESG Metrics In Capital Allocation Decisions | +1.4% | North America, Europe, and core Asia-Pacific markets | Medium term (2-4 years) |

| Need For Multi-Entity Reporting Standardization | +1.1% | Global, most relevant for cross-border institutional investors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Convergence Across Sustainability Reporting Regimes

The strongest force behind current demand is the steady overlap of sustainability reporting rules across major capital markets, which is pushing institutions to replace narrow tools with broader software platforms. By 2026, the ISSB baseline had been adopted or aligned to by regulators in more than 40 jurisdictions, expanding the need for systems that can map one data set across several disclosure regimes without repeated manual work.[1]IFRS Foundation, “ISSB Standards Adoption Around the World,” ifrs.org In Europe, investor disclosure obligations remained active even as the Omnibus I Directive reduced the size of the CSRD corporate reporting population, so fund managers still needed structured workflows for investor-facing reporting. This favors vendors that can support ISSB, ESRS, and SFDR in a single environment, because buyers are less willing to manage separate tools by framework or region. The investor ESG reporting software market is therefore being shaped more by cross-border reporting alignment than by any single national mandate.

Rising Investor Demand for Auditable ESG Disclosure Workflows

Institutional investors are no longer satisfied with static ESG reports; they increasingly want traceable data flows that can withstand internal review, external assurance, and fund due diligence. That shift is driving demand for platforms that preserve data lineage from portfolio company inputs through fund-level aggregation to final disclosure outputs. The pressure persists in the United States even after the SEC proposed rescinding its 2024 climate-related disclosure rules in May 2026, because fiduciary expectations and cross-border investor requirements continue to carry weight beyond federal rulemaking.[2]Securities and Exchange Commission, “SEC Proposes Rescission of Climate-Related Disclosure Rules,” sec.gov A clear sign of this behavior came in May 2026, when La Caisse and Novisto announced a strategic partnership to expand access to sustainability data management technology across portfolio companies, showing that capital providers are willing to back reporting infrastructure directly. The investor ESG reporting software market is benefiting from auditable workflows now being treated as part of fund credibility rather than a narrow back-office function.[3]La Caisse, “La Caisse Partners With Novisto to Help Organizations Prepare for Their Sustainability Transition,” lacaisse.com

Expansion of ESG Data Volumes from Portfolio Companies

Portfolio managers now collect a wider set of ESG metrics from a much broader range of investee companies, and that data comes in different formats, reporting cycles, and quality levels. As the number of required indicators rises, manual collection and consolidation become harder to defend on both cost and control grounds. This is especially visible in private markets, where firms need to gather structured information from companies that often lack mature internal reporting systems. Vendors are responding by building more connected data collection, validation, and workflow layers, so the investor ESG reporting software market is moving further into operational process design and less toward one-time report production alone. The trend also means that products with better portfolio intake workflows, clearer ownership controls, and stronger exception handling are likely to gain ground as reporting volumes continue to rise.[4]Workiva, “Sustainability Release Notes for May 2026,” workiva.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Architecture Supports Scale Across Portfolios

Cloud-based deployment held 62.13% of the investor ESG reporting software market share in 2025, and it is projected to record the fastest CAGR at 16.83% through 2031. The segment leads because institutional buyers need multi-tenant architecture, fast update cycles, and easier integration across geographically dispersed portfolio companies. Cloud deployment also fits the reporting reality of funds that must coordinate inputs from many entities while keeping templates, controls, and deadlines consistent. On-premises systems still matter in some large financial institutions, especially where data residency and internal governance rules slow migration.

Hybrid deployment is gaining attention because it gives institutions a transition path between legacy environments and newer reporting tools. Some firms prefer to keep sensitive data processing inside internal systems while using cloud-hosted modules for disclosure generation and regulatory content updates. That model is helping the investor ESG reporting software market reach buyers that are not ready for full migration but still need better reporting controls. SAP’s May 2026 announcement of sustainability AI agents also showed how large enterprise software providers are lowering the cloud adoption barrier by linking ESG workflows with finance, procurement, and supply chain systems that clients already use

By Enterprise Size: Large Institutions Anchor Revenue While SME Demand Rises Faster

Large enterprises accounted for 78.12% of revenue in 2025, while the investor ESG reporting software market size for SMEs is projected to expand at an 18.13% CAGR through 2031. Large institutions remain the core revenue base because they manage more entities, more funds, and more reporting lines than smaller peers. They also have dedicated compliance, sustainability, and technology teams that can support implementation and ongoing governance. In contrast, SMEs are adopting faster because investor expectations are moving downward into smaller private equity managers, boutique asset managers, and emerging-market-focused funds.

The gap between buyer groups is shaping product design across the investor ESG reporting software industry. Large firms usually want deep configurability, stronger system integration, and broad framework support, while smaller buyers value quicker deployment, clearer pricing, and ready-to-use templates. Mid-market private equity and private credit firms are finding that structured ESG reporting is increasingly difficult to avoid as they seek capital from institutional LPs that expect cleaner data and more consistent documentation. The investor ESG reporting software market is therefore expanding at the lower end, not because smaller firms suddenly want more features, but because they need workable reporting systems that can be adopted with less time and less internal effort.

By End User: Private Markets Add Momentum To Institutional Demand

Asset managers held the largest share at 34.17% in 2025, while the investor ESG reporting software market size for private equity firms is projected to grow at a 17.53% CAGR through 2031. Asset managers lead because they sit at the main aggregation point between portfolio company information and investor disclosure requirements. They need repeatable workflows that can turn large volumes of mixed data into fund-level outputs for clients, boards, and regulators. Private equity is growing faster because ESG reporting has become more closely tied to fundraising, due diligence, and exit preparation across private market portfolios.

The end-user mix is widening, and each institutional group brings different operating needs to the investor ESG reporting software market. Venture capital firms usually need lighter tools for early-stage portfolios with sparse data, while pension funds often need tighter links between reporting and long-horizon portfolio oversight. Insurance companies tend to emphasize governance and documentation discipline, and sovereign wealth funds may combine ESG evaluation with broader policy and geopolitical screening. Novisto’s May 2026 strategic investment agreement with La Caisse shows how investor-backed technology relationships are reinforcing the role of platforms in private market reporting workflows

By Functionality: Risk And Materiality Tools Move Ahead Of Basic Reporting

ESG reporting and disclosure management retained the largest share of functionality at 29.18% in 2025, while the investor ESG reporting software market for ESG risk assessment and materiality analysis is projected to grow at an 18.43% CAGR through 2031. This pattern shows that buyers still depend on core reporting modules, but spending is moving toward tools that help connect ESG information with forward-looking risk review and investment decisions. Basic disclosure functionality remains important because many firms began their digital journey with report generation and compliance support. At the same time, institutions now want systems that do more than package output at year-end.

The investor ESG reporting software industry is shifting toward fuller platforms rather than isolated point tools. Data collection, validation, benchmarking, compliance, and governance features are increasingly linked because buyers prefer a single, controlled environment over multiple disconnected products. Recent releases in February and May 2026 reflected this direction by adding readiness tools, questionnaire content, and intelligence support tied to evolving sustainability standards. As reporting cycles become more continuous, the value of functionality is shifting from simple output production toward better regulatory interpretation, stronger auditability, and clearer data governance.

Geography Analysis

North America held 34.83% of the investor ESG reporting software market share in 2025. The region stayed in front because it has the deepest pool of institutional asset management activity and a mature mix of platform vendors and specialist providers. The SEC’s May 29, 2026, proposal to rescind its 2024 climate-related disclosure rules created policy uncertainty in the United States, but did not remove the reporting pressure arising from fiduciary expectations and cross-border investor relationships. Canadian institutions are also adding momentum as climate risk disclosure expectations continue to move through regulated financial channels. South America remains at the forefront of adoption, with Brazil standing out as the most active market, as investor pressure and IFRS-aligned disclosure development are driving forward reporting practices.

Europe remained a core revenue center for the investor ESG reporting software market in 2026, as investor-level SFDR obligations remained in place even after the Omnibus I Directive narrowed the corporate CSRD population. That distinction matters because it reduced some corporate-side demand while leaving fund managers with ongoing disclosure responsibilities. Germany, France, the Netherlands, and the UK remain important demand centers because institutions there face dense framework overlap and higher expectations around portfolio-level reporting. The region is also keeping platform investment active because buyers are preparing for future framework refinement rather than waiting for complete regulatory stability.

Asia-Pacific is projected to record the fastest growth at a 17.93% CAGR, and the investor ESG reporting software market size is rising there faster than in any other region through 2031. New mandatory disclosure frameworks across Japan, South Korea, Australia, and India are broadening the buyer base and making multi-jurisdiction reporting support more valuable. The region also has meaningful local language and workflow requirements, which opens the door for domestic vendors to tailor reporting tools more closely to national rules. The Middle East and Africa are still smaller markets, but disclosure expectations are gradually strengthening in Gulf markets and South Africa, which is helping build a future pipeline. The investor ESG reporting software market is therefore becoming more geographically balanced, with future expansion relying more heavily on Asia-Pacific than in earlier regulatory cycles.

Competitive Landscape

The investor ESG reporting software market shows moderate concentration at the enterprise tier, where Workiva, Diligent, and Sphera are recognized leaders with established positions in disclosure, governance, and environmental management workflows. The mid-market is becoming more fragmented, with Novisto, Datamaran, Persefoni AI, and Optro expanding beyond narrower use cases into broader institutional reporting needs. Buyers are no longer comparing vendors solely on automation breadth, because product selection now depends more on how quickly a platform can absorb new regulatory changes and turn them into usable workflow support. Workiva’s 2026 product updates are a good example, as the company added tools for simplified ESRS readiness, CDP content, and AI-assisted disclosure interpretation within the same reporting environment. That keeps the investor ESG reporting software market competitive in terms of release speed and standards coverage, not only in core workflow functionality.

White-space opportunities still exist in private market portfolio data collection and in materiality benchmarking across different disclosure structures. Vendors that can handle weak data inputs from unlisted portfolio companies are likely to gain an edge, as this remains one of the hardest operational problems for buyers. SAP’s May 2026 sustainability AI agent announcement showed how enterprise incumbents are embedding ESG reporting into wider finance and procurement workflows rather than treating it as a stand-alone application. Novisto’s strategic agreement with La Caisse also showed that some capital providers are actively helping scale reporting infrastructure through direct technology partnerships. These moves raise pressure on specialist vendors that lack broad integration reach or strong investor relationships.

Enterprise buyers still place high value on auditability, integration depth, and multi-framework support, while smaller buyers focus more on deployment speed, usability, and transparent pricing. That split means the investor ESG reporting software market is unlikely to settle into one uniform vendor model in the near term. A few recognized leaders are likely to stay strong in large accounts, but challengers still have room to win where buyers want faster implementation or more targeted functionality. Competitive outcomes will depend less on who can produce a basic ESG report and more on who can translate regulatory change into usable reporting workflows with the least operational friction.

Investor ESG Reporting Software Industry Leaders

Workiva Inc.

Diligent Corporation

Sphera Solutions, Inc.

Enablon SAS

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP announced at SAP Sapphire that new sustainability AI agents, covering multi-step workflows including sustainability reporting preparation, carbon footprint simulation, and packaging compliance assessments, would be made generally available by end of 2026. The agents connect finance teams, procurement, supply chain operations, and sustainability functions through a shared data layer, reducing the multi-team coordination overhead that has historically constrained ESG reporting throughput.

- May 2026: Novisto and La Caisse, a global investment group managing assets aligned with the organization's 2025-2030 Climate Strategy, announced a strategic investment agreement on May 20, 2026. The transaction accelerates Novisto's international expansion and strengthens access to sustainability data management technology for La Caisse's portfolio companies, including CAE, Boralex, and Couche-Tard, demonstrating that institutional LPs are directly financing ESG platform capacity as a condition of capital deployment.

- May 2026: Workiva added 2026 CDP Corporate and SME questionnaire content and a Simplified ESRS Intelligence knowledge base, allowing clients to use Workiva AI to clarify disclosure requirements from EFRAG's December 2025 simplified ESRS draft, to its Sustainability Explorer tool in the May 2026 product release cycle.

- February 2026: Workiva released the ESRS Transition Accelerator on the Workiva Marketplace, providing readiness tooling for organizations preparing for the draft simplified European Sustainability Reporting Standards based on EFRAG's December 2025 publications. The release positions Workiva clients to voluntarily apply simplified ESRS for FY2026 ahead of the mandatory 2027 effective date.

Global Investor ESG Reporting Software Market Report Scope

The Investor ESG Reporting Software market refers to platforms and services that enable institutional investors and asset managers to collect, validate, and disclose environmental, social, and governance (ESG) data across portfolios. These solutions provide functionalities such as ESG data integration, disclosure management, portfolio benchmarking, risk assessment, and compliance reporting, helping investors align with global sustainability frameworks, enhance transparency, and strengthen stakeholder trust. By embedding ESG intelligence into investment workflows, these platforms support informed decision-making, regulatory compliance, and long-term value creation while balancing financial performance with environmental and social responsibility.

The Investor ESG Reporting Software market report is segmented by Deployment Mode (On-Premises, Cloud-Based, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End User (Asset Managers, Private Equity Firms, Venture Capital Firms, Pension Funds, Insurance Companies, Sovereign Wealth Funds, and Other Institutional Investors), Functionality (ESG Data Collection, Integration and Validation, ESG Reporting and Disclosure Management, Portfolio ESG Analytics and Benchmarking, ESG Risk Assessment and Materiality Analysis, and Compliance, Audit and Governance Management), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud-Based |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Asset Managers |

| Private Equity Firms |

| Venture Capital Firms |

| Pension Funds |

| Insurance Companies |

| Sovereign Wealth Funds |

| Other Institutional Investors |

| ESG Data Collection, Integration and Validation |

| ESG Reporting and Disclosure Management |

| Portfolio ESG Analytics and Benchmarking |

| ESG Risk Assessment and Materiality Analysis |

| Compliance, Audit and Governance Management |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Mode | On-Premises | ||

| Cloud-Based | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End User | Asset Managers | ||

| Private Equity Firms | |||

| Venture Capital Firms | |||

| Pension Funds | |||

| Insurance Companies | |||

| Sovereign Wealth Funds | |||

| Other Institutional Investors | |||

| By Functionality | ESG Data Collection, Integration and Validation | ||

| ESG Reporting and Disclosure Management | |||

| Portfolio ESG Analytics and Benchmarking | |||

| ESG Risk Assessment and Materiality Analysis | |||

| Compliance, Audit and Governance Management | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the investor ESG reporting software market size in 2026 and how fast will it grow?

The investor ESG reporting software market was valued at USD 2.16 billion in 2026 and is projected to reach USD 4.70 billion by 2031 at a 16.82% CAGR.

What is driving demand for investor ESG reporting software?

Demand is being driven by overlapping disclosure rules, stronger investor expectations for auditable data, rising portfolio data volumes, and the need to move away from spreadsheet-heavy reporting.

Which functionality is growing fastest in this space?

ESG risk assessment and materiality analysis is projected to grow the fastest, at an 18.43% CAGR through 2031, while ESG reporting and disclosure management remained the largest functionality segment in 2025.

Why are private equity firms adopting these platforms faster than other end users?

Private equity firms are projected to grow at a 17.53% CAGR because ESG reporting is becoming more important in fundraising, LP due diligence, portfolio oversight, and exit preparation.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to expand at a 17.93% CAGR, supported by newly activated disclosure frameworks across major regional markets.

What matters most when institutions choose an ESG reporting software vendor?

Large buyers usually prioritize auditability, integration depth, and multi-framework coverage, while smaller firms focus more on speed of deployment, simpler workflows, and transparent pricing.

Page last updated on: