ESG and Human Capital Disclosure Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.57 Billion |

| Market Size (2031) | USD 22.75 Billion |

| Growth Rate (2026 - 2031) | 18.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ESG and Human Capital Disclosure Platform Market Analysis by Mordor Intelligence

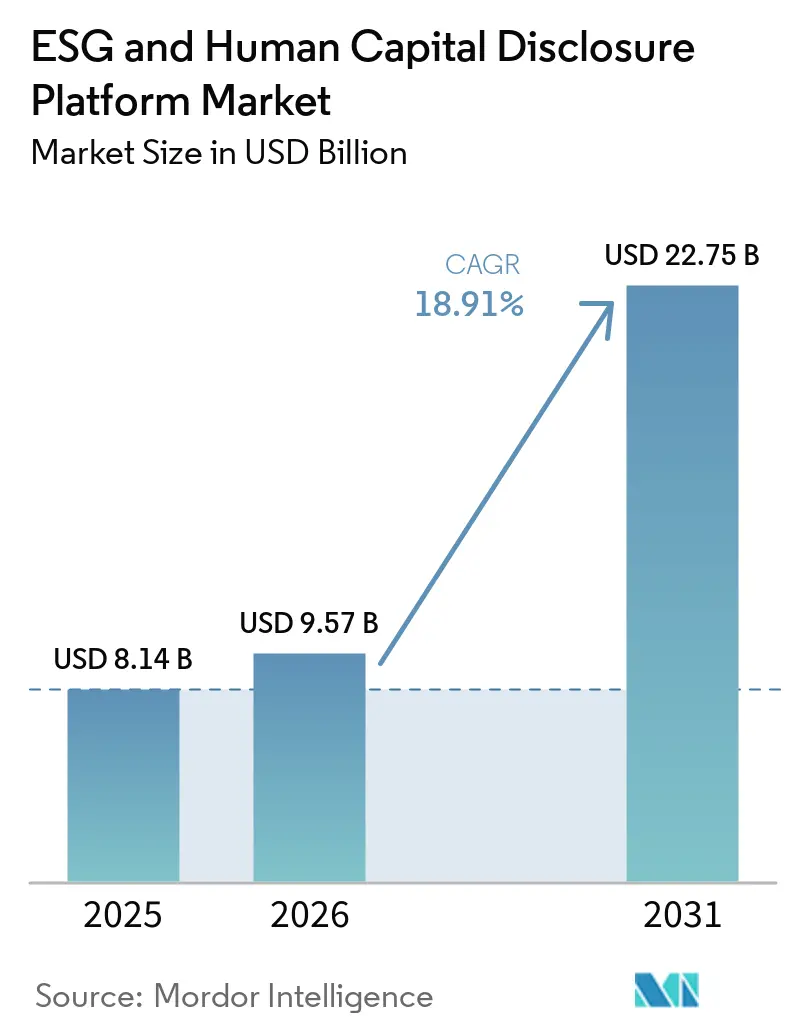

The ESG and Human Capital Disclosure Platform Market size is projected to be USD 8.14 billion in 2025, USD 9.57 billion in 2026, and reach USD 22.75 billion by 2031, growing at a CAGR of 18.91% from 2026 to 2031. Growth is being driven by the overlap of mandatory disclosure rules across Europe, North America, and parts of Asia-Pacific, which is forcing enterprises to move beyond spreadsheet-led reporting into governed systems that can support audit needs. The demand profile is also changing because companies now need a single environment that connects environmental metrics, workforce information, governance controls, and financial data with clear lineage. Europe led the ESG and Human Capital Disclosure Platform Market in 2025 because the CSRD rollout began early, and large enterprises across the region already had stronger governance infrastructure than many peers in other regions. Asia-Pacific is set to post the fastest expansion as sustainability reporting rules in markets such as Japan, Australia, and Singapore reshape enterprise reporting architecture. Procurement cycles are still affected by standards changes and data-integration complexity, yet the need for audit-ready disclosures, cross-functional controls, and supplier data collection continues to support broad platform demand.

Key Report Takeaways

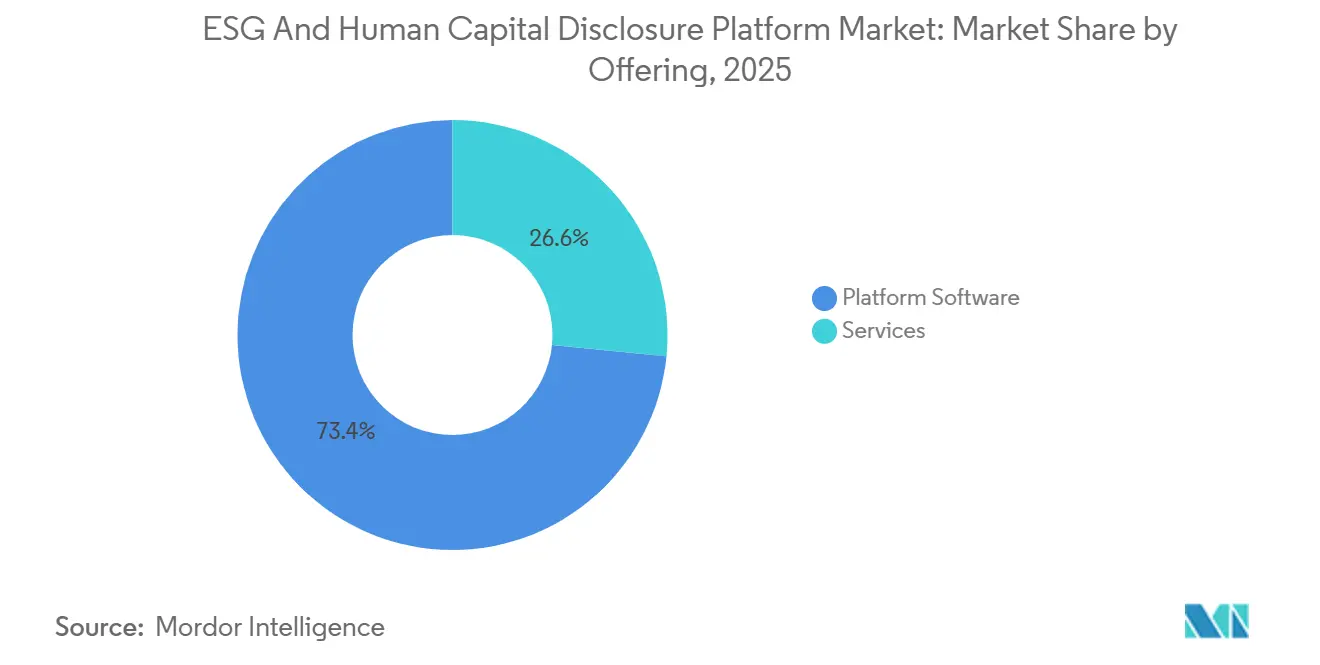

- By offering, Platform Software held 74.16% of the ESG and Human Capital Disclosure Platform Market in 2025, while Services is projected to expand at a 19.72% CAGR through 2031.

- By deployment model, Cloud held 71.12% of revenue in 2025, while Hybrid is projected to grow at a 20.14% CAGR through 2031.

- By end-user enterprise size, Large Enterprises accounted for 62.39% of revenue in 2025, while SMEs are projected to expand at a 21.08% CAGR through 2031.

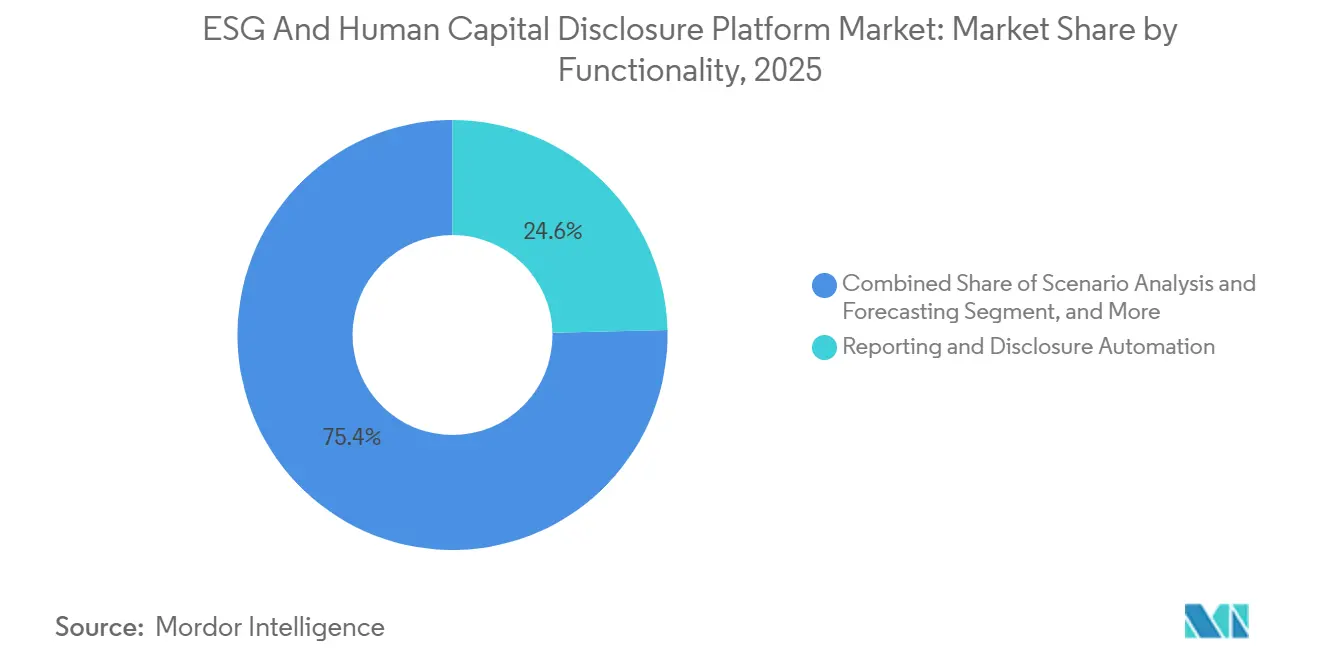

- By functionality, Reporting and Disclosure Automation held a 24.63% share in 2025, while Scenario Analysis and Forecasting is projected to advance at a 22.41% CAGR through 2031.

- By end-user industry, BFSI accounted for 25.87% of revenue in 2025, while Healthcare and Life Sciences are projected to grow at a 20.36% CAGR through 2031.

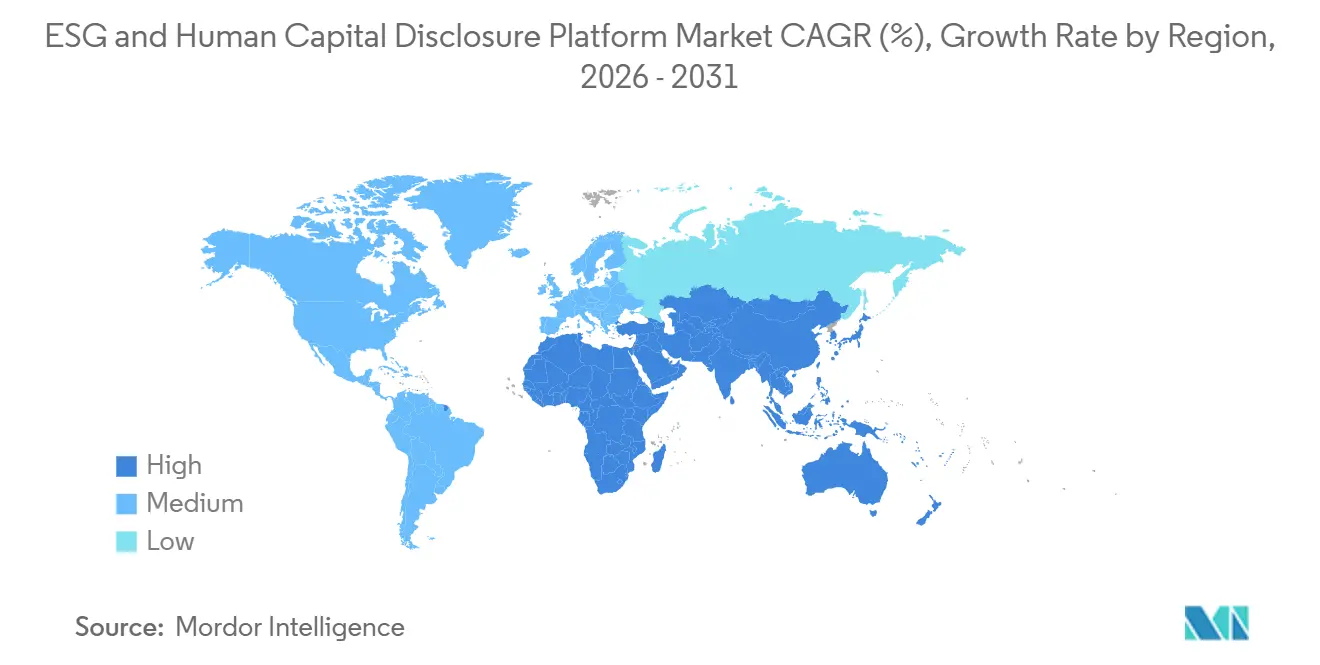

- By geography, Europe held 38.92% of revenue in 2025, while Asia-Pacific is projected to expand at a 23.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ESG and Human Capital Disclosure Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory CSRD, ISSB, and California Climate Disclosure Rollouts | +4.5% | Global, concentrated in EU and North America | Short term (≤ 2 years) |

| Investor and Lender Demand for Audit-Ready Non-Financial Data | +3.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Shift From Spreadsheet Workflows to Unified Finance-HR-Sustainability Platforms | +3.2% | Global | Medium term (2-4 years) |

| Rising Supplier and Scope 3 Reporting Burdens Across Enterprise Value Chains | +2.7% | Global, APAC spill-over from EU and North America supply chains | Medium term (2-4 years) |

| XBRL-Ready Digital Tagging and Assurance Workflows for Sustainability Statements | +2.1% | Europe and North America, early adoption in Australia | Medium term (2-4 years) |

| Workforce and Contingent Labor Metrics Moving Into Procurement and Risk Reviews | +1.6% | Global, concentrated in EU and progressively in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory CSRD, ISSB, and California Climate Disclosure Rollouts

Mandatory disclosure rules now span several major economies, which removes the option to delay investment in the ESG and Human Capital Disclosure Platform Market. The CSRD scope under the EU sustainability package now centers on companies with more than 1,000 employees and revenue above EUR 450 million (USD 486 million), which reduced the company count in scope but increased the compliance burden for those that remain covered. California also fixed a near-term reporting deadline when SB 253 required U.S. companies with annual revenue above USD 1 billion that do business in California to disclose Scope 1 and Scope 2 emissions by August 10, 2026.[1]California Air Resources Board, “California Greenhouse Gas Reporting and Climate-Related Financial Risk Disclosure Initial Regulation,” California Air Resources Board, arb.ca.gov These parallel rules are pushing enterprises to replace disconnected files with governed disclosure systems that can support environmental, governance, and workforce reporting in one place. The effect is spreading into supply chains as large reporters standardize data requests across suppliers and expect structured disclosures even from firms that are not directly in scope yet.

Investor And Lender Demand for Audit-Ready Non-Financial Data

Investors and lenders are treating non-financial information as part of core risk review, which is strengthening demand across the ESG and Human Capital Disclosure Platform Market. This shift is raising expectations for traceability, controls, and review standards that look closer to financial reporting than narrative sustainability communication. Enterprises that can show evidence trails, controlled source data, and review-ready outputs are in a stronger position during financing, diligence, and portfolio monitoring. That is why buyers are giving more weight to platforms that can support assurance workflows, standardized reporting, and cross-functional governance instead of point tools that only aggregate metrics. The result is durable demand for systems that can turn sustainability and workforce data into auditable records even when individual reporting rules continue to evolve.

Shift From Spreadsheet Workflows to Unified Finance-HR-Sustainability Platforms

The shift from spreadsheets to integrated systems remains one of the most durable demand drivers in the ESG and Human Capital Disclosure Platform Market. Enterprises still collect energy, emissions, workforce, procurement, and governance data from various systems, which slows and makes manual reconciliation error-prone. ISO 30414:2025 provides companies with a structured baseline for human capital reporting across workforce composition, diversity, productivity, safety, and turnover, underscoring the need to operationalize these metrics within existing HR data environments. As a result, buyers are favoring platform designs that connect directly to ERP, HRIS, and finance systems rather than relying on uploads and spreadsheet versions. Vendors with deep connectors to SAP, Oracle, and Microsoft Dynamics environments are gaining preference because enterprises want lower reconciliation effort and clearer data lineage.

Rising Supplier and Scope 3 Reporting Burdens Across Enterprise Value Chains

Supplier and Scope 3 reporting is expanding the functional reach of the ESG and Human Capital Disclosure Platform Market beyond direct entity disclosures. The GHG Protocol Phase 1 update proposed deeper Scope 3 rules that would require companies to separate primary supplier data from proxy-based estimates, classify inventories by data type, and work toward a 95% emissions-coverage floor.[2]Greenhouse Gas Protocol, “Scope 3 Standard Revisions Phase 1 Progress Update,” Greenhouse Gas Protocol, ghgprotocol.org That direction increases demand for supplier questionnaires, automated ingestion workflows, and supplier engagement modules inside broader disclosure platforms. It also widens the need for quality controls because companies can no longer rely as heavily on broad, spend-based assumptions when suppliers can provide direct input. ESRS S2 adds another layer by requiring disclosures on workers in the value chain, which means platforms must increasingly connect supplier labor information with emissions reporting workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Standards and Jurisdictional Rule Changes | -1.8% | Global | Short term (≤ 2 years) |

| High Integration Complexity Across ERP, HRIS, Finance, and EHS Data Stacks | -1.6% | Global | Medium term (2-4 years) |

| Sensitive Workforce Data Privacy and Cross-Border Data Localization Constraints | -1.3% | EU, APAC core, spill-over to North America | Long term (≥ 4 years) |

| Weak Data Availability for Contractors and Value-Chain Workers | -0.9% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Standards and Jurisdictional Rule Changes

The ESG and Human Capital Disclosure Platform Market still faces a near-term drag from overlapping standards and rolling jurisdictional updates. Enterprises operating across the EU, California, and multiple ISSB-linked markets need systems that can support different scope rules, timing assumptions, and disclosure structures from a single set of underlying data. The EU sustainability package changed scope thresholds in 2026, while California also set its own phased reporting path, meaning many buyers are still adjusting their implementation plans as rule details settle.[3]European Data Protection Board, “Europrivacy as a Data Transfer Mechanism - EDPB 2026,” IGDPR, igdpr.eu This moving target can delay procurement, as enterprises prefer not to lock into complex configurations before internal compliance teams are comfortable with the regulatory path. The result is longer sales cycles and a stronger preference for modular architectures that can absorb rule updates without major reimplementation.

High Integration Complexity Across ERP, HRIS, Finance, And EHS Data Stacks

Integration complexity remains a practical restraint on adoption in the ESG and Human Capital Disclosure Platform Market. A full deployment often requires data flows from ERP, HRIS, EHS, finance, procurement, payroll, and utility systems, and these systems rarely share clean definitions, refresh cycles, or ownership models. Human capital reporting adds another layer because workforce metrics such as pay gaps, incident rates, turnover, and contractor counts often sit in separate systems and need common taxonomy rules before disclosure can be controlled. SMEs feel this more sharply because they often lack standardized enterprise architecture and therefore incur higher integration costs per employee. These barriers help incumbents with broad connector libraries, but they also slow switching and lengthen implementation timelines beyond what many buyers initially expect.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Software Holds The Largest Revenue Base

Platform Software captured 74.16% of the ESG and Human Capital Disclosure Platform Market size in 2025, making it the largest offering category in the current revenue mix. This reflects adoption across ESG Data Management, Human Capital Disclosure and Workforce Analytics, Reporting and Regulatory Disclosure, ESG Performance Management and Analytics, and Risk, Audit and Assurance Platforms. The category benefits from enterprise demand for systems that manage controlled workflows rather than simply storing sustainability metrics. Risk, Audit, and Assurance Platforms are expanding quickly within this layer because assurance obligations are making reviewability and evidence trails more important in enterprise buying decisions. Workiva, which serves more than 6,600 organizations, including over 85% of Fortune 1,000 companies, reported USD 885 million in revenue for fiscal 2025 and guided to nearly USD 1 billion in fiscal 2026, demonstrating the scale available to integrated disclosure platforms.[4]Workiva, Inc., “Fiscal Year 2025 Financial Results and 2026 Guidance,” Workiva Investor Relations, investors.workiva.com

Services are projected to grow at a 19.72% CAGR through 2031, making it the fastest-growing offering in the ESG and Human Capital Disclosure Platform Market. First-time reporters entering mandatory disclosure cycles in 2026 and 2027 are still buying implementation, advisory, XBRL support, and assurance-readiness work alongside software licenses. This is narrowing the line between software subscriptions and service-led compliance delivery. Vendors are increasingly packaging configuration support and regulatory updates into recurring contracts rather than selling them as one-time projects. That model supports higher contract values and reduces the likelihood of replacement at renewal because the vendor becomes part of the client’s operating process.

By Deployment Model: Cloud Leads Adoption While Hybrid Gains In Regulated Settings

Cloud deployment accounted for 71.12% of the ESG and Human Capital Disclosure Platform Market in 2025, leaving it well ahead of other deployment models. Buyers have favored cloud because it scales more easily across entities and geographies, and because vendor-led regulatory updates reduce internal IT workload. The model is especially attractive when enterprises need to move quickly across multiple reporting jurisdictions simultaneously. North America and Northern Europe remain the strongest centers of cloud adoption because enterprise technology estates are more cloud-oriented, and compliance workflow benefits are immediate. Proposed digital tagging requirements for ESRS statements also support cloud adoption because cloud platforms can keep taxonomies current without heavy enterprise intervention.

Hybrid deployment is projected to expand at a 20.14% CAGR in the ESG and Human Capital Disclosure Platform Market size through 2031, making it the fastest-growing model. This pattern is strongest in financial services, healthcare, and government environments where buyers want cloud flexibility but still prefer to keep sensitive workforce or governance data under tighter local control. Hybrid architecture lets enterprises retain certain data sets on-premises while using cloud engines for data disclosure, workflow management, and reporting. The European Data Protection Board recognized Europrivacy certification in April 2026 as a mechanism that can support international personal data transfers under GDPR Articles 42 and 46, which may help platforms handling employee data across borders. On-premises deployment is still in use, but its role is narrowing to sovereignty-heavy use cases and to organizations with older EHS and governance systems that they do not want to move yet.

By End-User Enterprise Size: Large Enterprises Lead Revenue While SMEs Accelerate

Large Enterprises held 62.39% of the ESG and Human Capital Disclosure Platform Market share in 2025, reflecting their early exposure to mandatory reporting and their ability to fund integration across multiple systems. Many of these organizations already manage reporting programs across numerous frameworks, so they need multi-entity consolidation, permissions control, and broad mapping across disclosure standards. That requirement fits larger buyers because they can support longer implementation cycles and cross-functional governance committees. The need to connect workforce reporting with sustainability reporting is also reinforcing this segment’s lead because large enterprises are more likely to treat disclosure as an enterprise architecture issue rather than a standalone reporting task. ESRS S1 requirements on own-workforce topics such as composition, pay gaps, health and safety, and turnover are pushing these buyers to integrate human capital data into the same reporting environment.

SMEs are projected to expand at a 21.08% CAGR through 2031, making them the fastest-growing enterprise-size segment in the ESG and Human Capital Disclosure Platform Market. Demand is being pulled through supply chains because large CSRD reporters are requesting more structured environmental and workforce data from smaller partners. SMEs are also being drawn in by sustainability-linked financing programs that increasingly expect measurable emissions and disclosure capability. Singapore’s Green 100 program, launched in May 2025, was designed to mobilize 100 SMEs for each large enterprise in supply-chain sustainability disclosure, creating a scaled route into platform adoption. The European Commission’s public consultation on voluntary sustainability reporting for SMEs also supports a more proportionate disclosure architecture, which should improve adoption once standards are finalized.

By Functionality: Disclosure Automation Holds The Largest Base While Scenario Tools Expand Fastest

Reporting and Disclosure Automation accounted for 24.63% of the ESG and Human Capital Disclosure Platform market in 2025, making it the largest functionality layer. This leadership reflects the fact that most enterprise buying still starts with immediate filing deadlines rather than long-range analytics needs. Buyers needed systems that could populate ESRS-aligned disclosures, test completeness, and generate machine-readable outputs without repeated manual formatting. The ESRS Set 1 XBRL taxonomy, published in August 2024, provided a practical reason for enterprises to automate reporting workflows: digital tagging requires a consistent structure and governed source mapping. Data Collection and Aggregation, as well as Materiality Assessment and Benchmarking, remain closely linked functions because enterprises often build upstream data quality only after disclosure automation is in place.

Scenario Analysis and Forecasting is projected to grow at a 22.41% CAGR in the ESG and Human Capital Disclosure Platform Market size through 2031, making it the fastest-growing functionality. Boards and executive teams increasingly want forward-looking climate transition views alongside historical disclosure, so the demand is moving beyond filing support alone. Audit and Assurance Management is also gaining momentum as companies need traceable evidence, workflow control, and review history to meet increasing assurance expectations. Stakeholder Engagement and Questionnaire Management are becoming increasingly important as enterprises collect supplier data from broad tier-1 and tier-2 networks and seek to reduce dependence on proxy-based estimates. Over time, the strongest platforms in the ESG and Human Capital Disclosure Platform industry are likely to be those that integrate collection, tagging, scenario modeling, and assurance within a single, controlled data chain.

By End-User Industry: BFSI Leads Current Spending While Healthcare And Life Sciences Expands Faster

BFSI accounted for 25.87% of the ESG and Human Capital Disclosure Platform Market share in 2025, making it the largest end-user industry. Financial institutions face dual pressure because they must disclose their own sustainability and workforce data while also using similar data in lending, investment, and product governance decisions. That combination creates a strong case for unified platforms with controlled data lineage and repeatable reporting outputs. It also explains why banks, insurers, and asset managers have remained among the earliest and most active enterprise buyers in this space. In the ESG and Human Capital Disclosure Platform industry, BFSI demand is reinforced by the need to connect internal disclosures with external credit, investment, and green finance workflows.

Healthcare and Life Sciences is projected to expand at a 20.36% CAGR through 2031, making it the fastest-growing end-user industry in the ESG and Human Capital Disclosure Platform Market. Growth is supported by the widening disclosure scope for large hospital groups and pharmaceutical companies, as well as by the sector’s need to handle both environmental and workforce reporting within one system. Supply chain emissions and purchased-goods reporting remain important for pharmaceutical operations, while ESRS S1 keeps workforce indicators such as safety, turnover, and pay metrics central to the reporting agenda. Information Technology and Telecom, Retail and E-commerce, and Industrial Manufacturing also remain meaningful contributors, with Industrial Manufacturing particularly exposed to supplier and value-chain disclosure requirements. The government and the Public Sector are still earlier in the adoption curve, but their roles should increase as more jurisdictions formalize disclosure programs aligned with global sustainability frameworks.

Geography Analysis

Europe held 38.92% of the ESG and Human Capital Disclosure Platform Market share in 2025, maintaining its leading position. The region’s lead came from the phased rollout of CSRD and from the growing need to support digital tagging for sustainability statements under the ESRS reporting structure. Germany, the United Kingdom, France, and the Netherlands remained the core centers of enterprise adoption because they housed many of the large entities facing the earliest reporting deadlines. The EU sustainability package that took effect in 2026 raised the main threshold to companies with more than 1,000 employees and revenue above EUR 450 million (USD 486 million), narrowing the number of companies in scope but concentrating spend among larger enterprises with stronger budgets and governance capacity. Italy and Spain remained important follow-on markets, while Russia stayed smaller and more isolated from the EU-aligned disclosure architecture.

North America remained a major contributor to the ESG and Human Capital Disclosure Platform Market, as the United States and Canada both moved toward stronger sustainability reporting requirements. California created a strong near-term implementation trigger by requiring large U.S. businesses operating in the state to prepare Scope 1 and Scope 2 disclosures by August 10, 2026. Canada is also moving through ISSB-aligned reporting development, while Mexico remains earlier in adoption and is influenced more by export-chain reporting expectations from U.S. and European customers. In South America, Brazil and Argentina lead regional adoption, while the rest of South America remains at an earlier stage.

Asia-Pacific is projected to expand at a 23.18% CAGR in the ESG and Human Capital Disclosure Platform Market size through 2031, making it the fastest-growing regional market. Japan is a key driver because sustainability disclosures have moved into the annual securities report structure, and vendor investment has followed, as shown by Workiva’s November 2025 addition of support for the Australian Sustainability Reporting Standards to its Sustainability Explorer. China is seeing stronger demand from international investors and export-market buyers, while India and South Korea remain in early-to-mid adoption, and Singapore is using programs such as Green 100 to widen SME participation in disclosure workflows. In the Middle East, Saudi Arabia and the UAE are moving faster than the rest of the region, and in Africa, South Africa leads while Nigeria is emerging, and the rest of the continent remains at a nascent stage.

Competitive Landscape

The ESG and Human Capital Disclosure Platform Market remained moderately fragmented, with no single provider controlling all major software categories or regions. Competition came from governance and risk incumbents, dedicated ESG software specialists, and ERP-adjacent offerings, each approaching compliance depth and integration in different ways. Diligent expanded its position in January 2026 through the acquisition of 3rdRisk, adding AI-native third-party risk management capabilities tied to vendor ecosystem oversight and supply-chain risk visibility. Novisto deepened its platform in March 2026 by acquiring Minimum, which brought carbon management capabilities into its broader enterprise ESG environment and strengthened its footprint in the United Kingdom and Europe. Workiva and EcoVadis have pursued a partnership route instead, linking supplier-reported emissions information into a broader audit-ready reporting environment that supports Scope 3 disclosure use cases.

A meaningful share of the open opportunity in the ESG and Human Capital Disclosure Platform Market still sits with mid-market enterprises in Asia-Pacific and South America, which remain underserved in pricing, language support, and regulatory localization. Another gap remains in human capital disclosure because many tools still handle environmental data more deeply than HRIS-linked workforce information. AI-enabled assurance automation is also becoming a visible battleground as enterprises want faster review cycles without custom project work for every reporting change. Persefoni’s Analytics Agent launch in May 2026 reflects that product direction by bringing plain-language emissions analysis, benchmarking, and auditable exploration into the workflow.

EHS-focused vendors such as Sphera, Cority, Intelex, and VelocityEHS continue to benefit from deeper operational system links, which matters when buyers prioritize source-level environmental data integration. At the same time, enterprises are favoring vendors that can connect ERP, HRIS, finance, and supplier data without creating a heavy manual control layer. Cross-border data rules are becoming a second decision factor because platforms handling employee data need stronger transfer mechanisms, stronger privacy controls, and greater architectural flexibility. These conditions keep consolidation active in the ESG and Human Capital Disclosure Platform Market, but they also prevent a single vendor from establishing dominant control across the full category.

ESG and Human Capital Disclosure Platform Industry Leaders

Workiva Inc.

Diligent Corporation

Sphera Solutions, Inc.

Cority Software Inc.

Intelex Technologies ULC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Novisto received strategic investment from La Caisse to expand sustainability platform adoption aligned with CSRD and California rules.

- April 2026: Sweep and CFGI partnered to combine sustainability data management with compliance expertise for audit-ready disclosures.

- March 2026: Novisto acquired Minimum, adding carbon management capabilities and expanding into UK/Europe.

- March 2026: Workiva released updated CSRD double-materiality templates aligned with ESRS 2.0.

Global ESG and Human Capital Disclosure Platform Market Report Scope

The ESG and Human Capital Disclosure Platform market comprises technology solutions and services that enable organizations to collect, manage, analyze, and disclose environmental, social, and governance (ESG) data, as well as workforce-related data. These platforms support functions such as reporting automation, compliance management, materiality assessment, scenario forecasting, audit and assurance, and stakeholder engagement. Delivered through cloud, on-premises, and hybrid models, they serve both large enterprises and SMEs across industries, including BFSI, healthcare, IT and telecom, retail, manufacturing, government, and others. The core purpose of this market is to enhance transparency, ensure regulatory compliance, improve risk management, and provide data-driven insights that strengthen sustainability strategies and human capital management practices.

The ESG and Human Capital Disclosure Platform market report is segmented by Offering (Platform Software, [ESG Data Management Platforms, Human Capital Disclosure and Workforce Analytics Platforms, Reporting and Regulatory Disclosure Platforms, ESG Performance Management and Analytics Platforms, and Risk, Audit and Assurance Platforms] and Services), Deployment Model (Cloud, On-premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-sized Enterprises), Functionality (Reporting and Disclosure Automation, Data Collection and Aggregation, Materiality Assessment and Benchmarking, Scenario Analysis and Forecasting, Audit and Assurance Management, and Stakeholder Engagement and Questionnaire Management), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform Software | ESG Data Management Platforms |

| Human Capital Disclosure and Workforce Analytics Platforms | |

| Reporting and Regulatory Disclosure Platforms | |

| ESG Performance Management and Analytics Platforms | |

| Risk, Audit and Assurance Platforms | |

| Services |

| Cloud |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Reporting and Disclosure Automation |

| Data Collection and Aggregation |

| Materiality Assessment and Benchmarking |

| Scenario Analysis and Forecasting |

| Audit and Assurance Management |

| Stakeholder Engagement and Questionnaire Management |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Offering | Platform Software | ESG Data Management Platforms |

| Human Capital Disclosure and Workforce Analytics Platforms | ||

| Reporting and Regulatory Disclosure Platforms | ||

| ESG Performance Management and Analytics Platforms | ||

| Risk, Audit and Assurance Platforms | ||

| Services | ||

| By Deployment Model | Cloud | |

| On-premises | ||

| Hybrid | ||

| By end user Enteprise size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Functionality | Reporting and Disclosure Automation | |

| Data Collection and Aggregation | ||

| Materiality Assessment and Benchmarking | ||

| Scenario Analysis and Forecasting | ||

| Audit and Assurance Management | ||

| Stakeholder Engagement and Questionnaire Management | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the ESG and Human Capital Disclosure Platform Market?

The ESG and Human Capital Disclosure Platform Market stood at USD 8.14 billion in 2025 and is valued at USD 9.57 billion in 2026. It is forecast to reach USD 22.75 billion by 2031 at a CAGR of 18.91% during 2026-2031.

Which region currently leads spending on ESG and human capital disclosure platforms?

Europe led with 38.92% of revenue in 2025, supported by the phased rollout of CSRD and stronger enterprise governance infrastructure.

Which region is growing the fastest through 2031?

Asia-Pacific is expected to post the fastest growth at a 23.18% CAGR during 2026-2031 as mandatory sustainability reporting expands across key regional economies.

What is the leading offering category in this space?

Platform Software was the largest offering segment in 2025 with a 74.16% share, reflecting broad demand for governed disclosure, data management, and assurance workflows.

Why are services growing so quickly in this category?

Services are projected to grow at a 19.72% CAGR because enterprises need implementation, advisory, XBRL support, and managed compliance help as first-time mandatory reporting deadlines arrive.

Which buyer groups are shaping demand the most?

Large Enterprises generated 62.39% of revenue in 2025 because they were exposed earlier to mandatory reporting, while SMEs are growing faster at 21.08% CAGR due to supply-chain requests and financing-linked disclosure needs.

Page last updated on: