Asset Finance Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

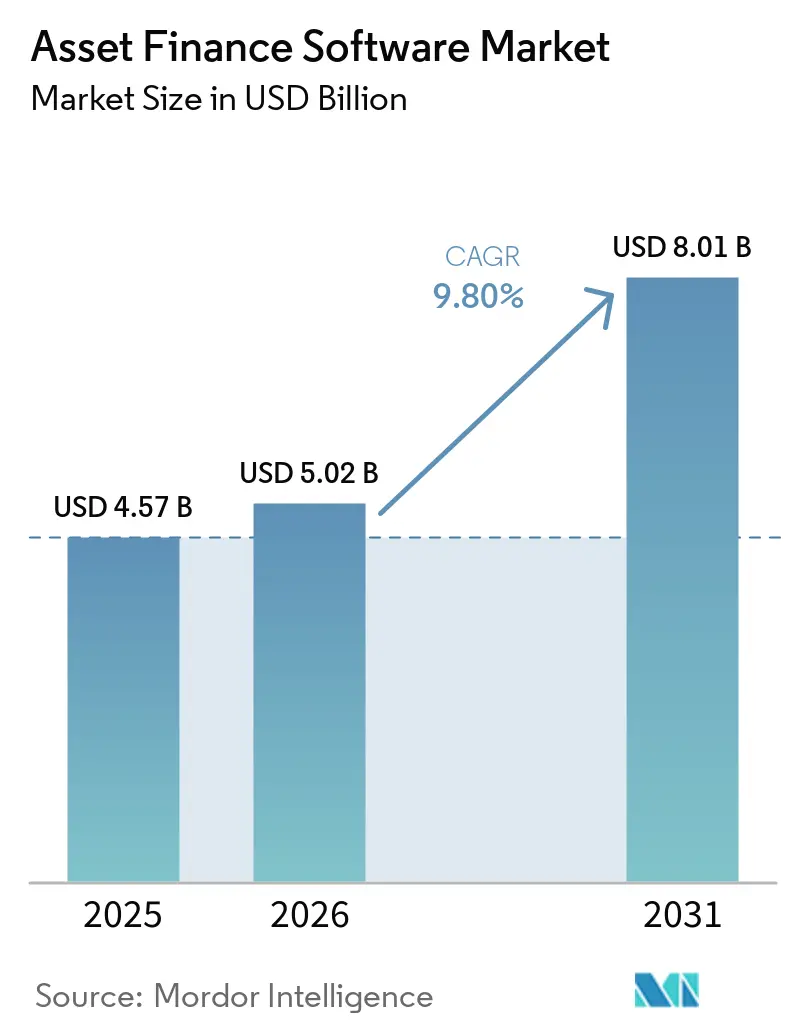

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 8.01 Billion |

| Growth Rate (2026 - 2031) | 9.80% CAGR |

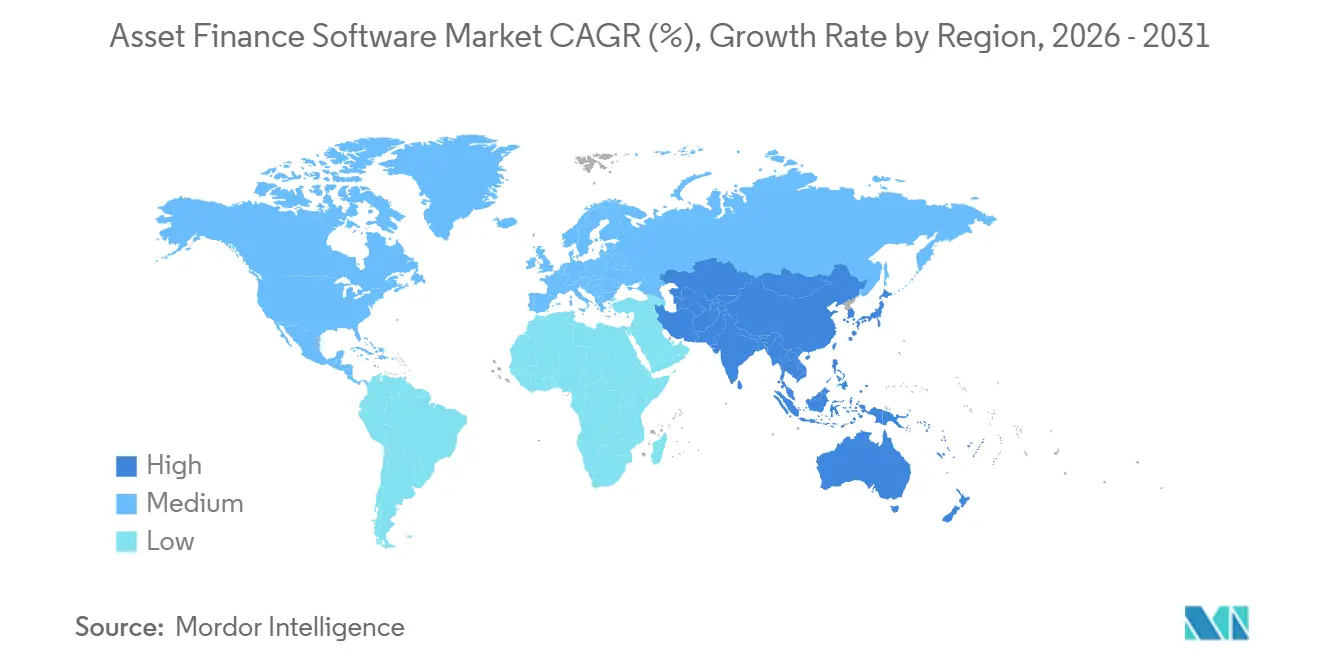

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asset Finance Software Market Analysis by Mordor Intelligence

The asset finance software market size is projected to expand from USD 4.57 billion in 2025 and USD 5.02 billion in 2026 to USD 8.01 billion by 2031, registering a CAGR of 9.8% between 2026 and 2031. Rising cloud adoption, embedded-finance integrations, and compliance obligations are prompting banks, captives, and FinTech lenders to upgrade legacy leasing platforms. Vendors that deliver API-ready, multi-asset coverage gain traction as lessors diversify into alternative energy, circular-economy equipment, and cross-border syndication. Competition centers on time-to-market and AI-based analytics, with SaaS models lowering upfront costs for mid-market leasing firms and SMEs. Platform consolidation accelerates as private-equity sponsors pursue recurring revenue and global scalability.

Key Report Takeaways

- By deployment model, cloud commanded 57.8% of the asset finance software market revenue in 2025 and is forecast to post a 13.5% CAGR through 2031.

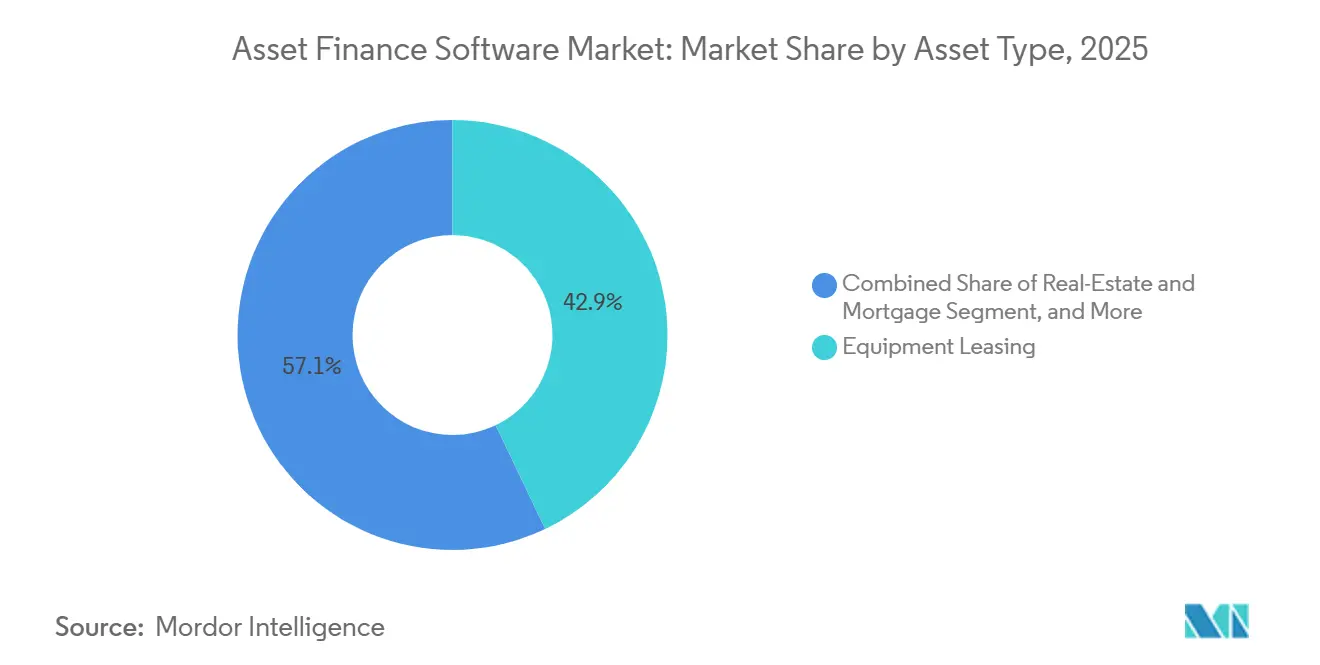

- By asset type, equipment leasing represented 42.9% of the asset finance software market share in 2025, while aircraft and marine are forecast to post a 11.9% CAGR to 2031.

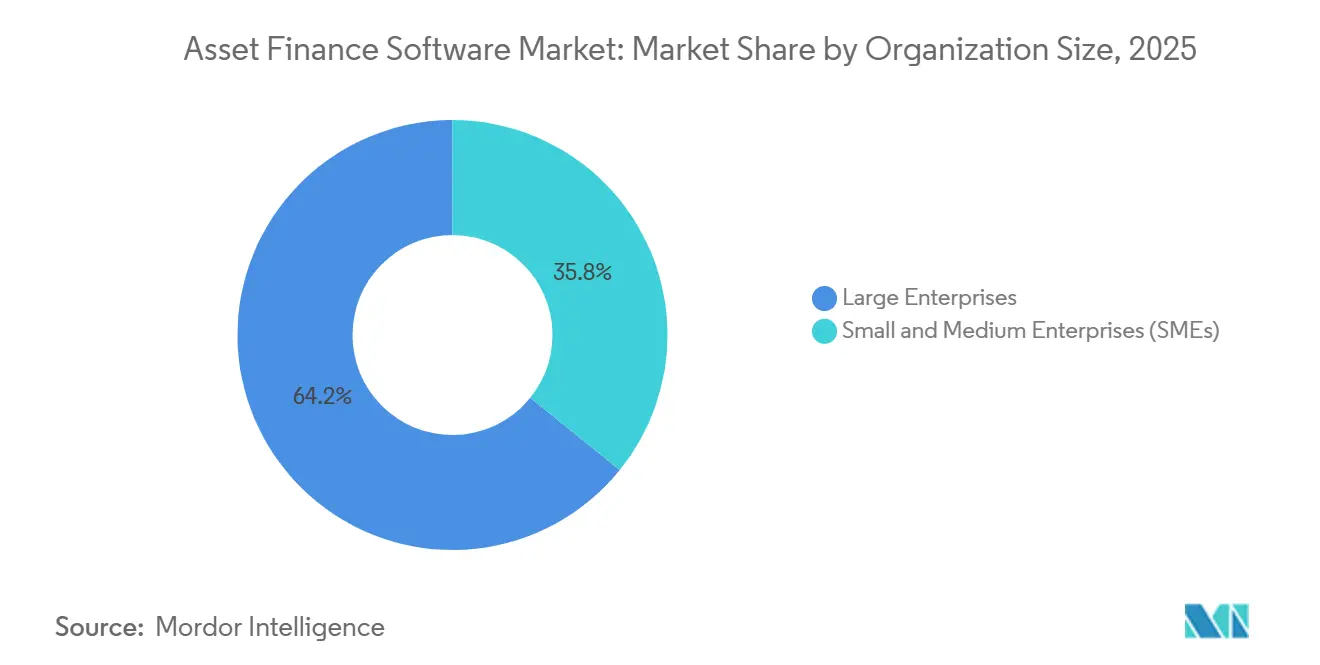

- By organization size, large enterprises held 64.2% share of the asset finance software market size in 2025; SMEs are set to expand at a 12.4% CAGR to 2031.

- By end-user industry, banks and captive finance subsidiaries led with 39.9% of the asset finance software market in 2025, whereas FinTech lenders record the fastest projected CAGR at 15.2% through 2031.

- By geography, North America accounted for 32.4% revenue of the asset finance software market in 2025, whereas Asia-Pacific is projected to grow at a 12.8% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Asset Finance Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Digitalization and Automation in Asset-Finance Workflows | +2.5% | Global, early gains in North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Rising Demand for Cloud-Based Deployment Models | +2.8% | North America and Europe lead; APAC and Middle East accelerating | Short term (≤ 2 years) |

| Expanding Equipment Leasing and Rental Volumes Worldwide | +1.8% | APAC, South America, Western Europe | Medium term (2-4 years) |

| Strengthening Regulatory Push for Granular Compliance and Reporting | +1.2% | Europe, North America, expanding to APAC | Long term (≥ 4 years) |

| AI-Driven Residual-Value Analytics and Predictive Maintenance Integration | +1.0% | North America and Europe early adopters | Medium term (2-4 years) |

| Rise of API-First Platforms Enabling Embedded Asset Finance | +0.9% | North America FinTech hubs, APAC digital-lending ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Digitalization and Automation in Asset-Finance Workflows

Manual origination once absorbed up to 40% of a lessor’s operating costs. Platforms such as Odessa Auto now parse dealer invoices with intelligent document processing and trigger credit-risk APIs in real time, shrinking cycle times from three days to half a day.[1]Odessa, “Odessa Auto Platform Launch,” odessainc.com UniCredit’s 2025 migration to Google Cloud allowed sub-hourly portfolio analytics, letting the bank reprice residual values daily.[2]Google Cloud, “UniCredit Migrates Italian Leasing Operations,” cloud.google.com Robotic process automation (RPA) manages payment posting and delinquency queues, while AI chatbots handle routine borrower queries. Labor-intensive Western markets adopted first, yet digital-native lessors in India and Indonesia leapfrog directly to fully automated stacks.

Rising Demand for Cloud-Based Deployment Models

Cloud deployments save capital, shorten implementation, and support elastic scaling during seasonal peaks. FIS’s 2025 release lets mid-market lessors spin up new product lines in weeks.[3]FIS, “FIS Cloud Asset Finance Suite,” fisglobal.com Sopra Banking Software’s 2026 Lending Suite launches with pre-integrated APIs to bureaus, telematics, and payments, eliminating year-long on-premise buildouts.[4]Sopra Banking Software, “SBS Lending Suite Launch,” soprabanking.com APAC greenfield entrants prefer subscription pricing, while European incumbents embrace cloud to meet DORA resilience testing. A Singapore-based lessor can now activate an Indonesian instance with localized compliance settings in days instead of months.

Expanding Equipment Leasing and Rental Volumes Worldwide

Argentina signed 6,390 leasing contracts in 2025, up 56% year on year, lifting the portfolio to ARS 1,009.6 billion (USD 608 million). Brazil’s receivables climbed 46.5% between 2024 and 2025, fueled by machinery (40.8%) and aircraft (36.8%). In February 2026, UK asset-finance volumes rose 18% as electric-vehicle fleets scaled.[5]Finance Leasing Association, “UK Asset Finance Volumes February 2026,” fla.org.uk Such growth forces lessors to replace spreadsheets with platforms capable of multi-asset, multi-jurisdiction servicing.

Strengthening Regulatory Push for Granular Compliance and Reporting

The Digital Operational Resilience Act (DORA) became fully applicable in January 2025, mandating annual ICT testing and major-incident reporting. IFRS 16 continues to require right-of-use asset calculations, while Basel III enforces capital buffers tied to collateral values. Vendors embed audit trails, role-based access, and ready-made disclosure templates to shorten reporting cycles. Institutions in Europe and North America lead adoption, but APAC regulators increasingly mirror these frameworks, extending the compliance tailwind into the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Integration Costs for Complex Legacy Estates | -0.8% | North America and Europe | Medium term (2-4 years) |

| Persistent Data-Security and Privacy Concerns | -0.6% | Europe, North America, APAC | Short term (≤ 2 years) |

| Legacy Core-Banking Lock-In Limiting Migration Velocity | -0.5% | North America and Europe | Long term (≥ 4 years) |

| Shortage of Domain-Specific Tech Talent for Asset-Finance Software | -0.3% | North America, Western Europe, emerging APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Integration Costs for Complex Legacy Estates

Tier-1 banks spend nearly half their IT budget on maintaining 15-year-old core systems, stretching new platform rollouts to two years. On-premise licenses plus professional services can top USD 500,000 for just 50 users. Even SaaS adoptions must fund data migration, dual-running, and staff retraining, raising total ownership. Vendor-imposed proprietary APIs further lock incumbents into staged roadmaps that slow competitive response.

Persistent Data-Security and Privacy Concerns

Financial-sector breaches averaged USD 6.08 million in 2024, exceeding the cross-industry mean by 22%. Asset finance platforms store borrower IDs, collateral serials, and payment histories, tempting ransomware actors. GDPR fines and new state privacy laws drive demand for encryption, granular consent logs, and regional data residency. China and Indonesia require in-country storage, compelling vendors to build multi-tenant, local-cloud instances that inflate costs and complicate rollout schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Type: Equipment Leasing Dominates While Aircraft Finance Accelerates

Equipment leasing accounted for 42.9% of revenue in 2025, highlighting its breadth across machinery, IT, and medical devices. The segment benefits from large installed bases and predictable upgrade cycles, anchoring the asset finance software market. Aircraft and marine financing is forecast to post an 11.9% CAGR through 2031 as IoT sensors feed real-time engine data into residual-value analytics, reducing remarketing risk. Vendors that model component-level depreciation and multi-currency cash flows stand out.

Regional nuances sustain growth. North American hospitals lease surgical robots to preserve cash, while Southeast Asian airlines deploy software to align lease rentals with usage. Alfa Start’s rapid-launch cloud suite trims go-live to 16 weeks for European mid-market lessors, illustrating demand for configurable, multi-asset coverage. As sustainability regulations tighten, platforms increasingly track carbon metrics alongside financial KPIs, differentiating offers for green fleets.

By Deployment Model: Cloud Momentum Outpaces On-Premise Installations

Cloud accounted for 57.8% of installations in 2025 and is projected to grow at a 13.5% CAGR, far exceeding on-premise expansions. The shift reflects subscription economics, vendor-managed infrastructure, and weekly feature drops that reduce backlog risk. Svea Bank’s Nordic migration enabled seasonal scaling without hardware over-provisioning. Oracle’s 2026 Agentic AI, offered only in cloud form, underscores the innovation gap widening between deployment models.

On-premise persists where data-sovereignty laws or mainframe ties prevail, especially among state-owned lenders. These customers accept a higher total cost for perceived control. Over time, however, R&D budgets tilt toward cloud, prompting legacy users to consider hybrid models. The asset finance software market size linked to cloud is expected to surpass USD 5 billion by 2031, reflecting this structural pivot.

By Organization Size: SMEs Accelerate Through API-First Offerings

In 2025, large enterprises accounted for 64.2% of deployments, leveraging enterprise-grade suites to oversee portfolios worth billions. These organizations rely on robust software solutions to manage complex operations and ensure scalability. Their dominance in the market is attributed to their ability to invest in advanced technologies that streamline portfolio management. Meanwhile, SMEs are projected to grow at an annual rate of 12.4%, driven by API-first vendors integrating leasing modules into their accounting and e-commerce platforms. This growth highlights the increasing adoption of modular and cost-effective solutions by smaller businesses. LoanOptions.ai, post-merger, boasts a platform that auto-fills 90% of applications, swiftly linking borrowers to over 90 lenders, significantly reducing the time and effort required for loan approvals.

SMEs appreciate the benefits of pay-per-contract pricing and the absence of hardware maintenance, which aligns with their need for cost-efficient solutions. These features allow smaller businesses to adopt technology without significant upfront investments. Additionally, flexible underwriting practices enable credit access for borrowers with limited credit histories, addressing a critical gap in the market. Conversely, larger institutions dominate intricate asset classes, like rail and energy, where the complexities of multi-year, multi-currency waterfalls necessitate extensive customization. Their expertise and resources allow them to handle these sophisticated financial structures effectively. This divided landscape compels suppliers to differentiate their offerings: opting for lighter SaaS solutions for speed or comprehensive suites for in-depth features, catering to the diverse needs of both SMEs and large enterprises.

By End-User Industry: FinTech Lenders Disrupt Bank Primacy

Banks and captive subsidiaries controlled 39.9% of installations in 2025, leveraging cheap funding and existing dealer networks. These entities benefit from their established infrastructure and relationships, allowing them to dominate the market. However, FinTech lenders are growing rapidly, with a 15.2% CAGR, as they embed financing solutions directly at the point of sale. QuickFi’s multi-agent AI reduces approval times to mere minutes, attracting merchants who were previously underserved by traditional banks. Additionally, Basikon enhances checkout conversion rates by 20-30% by integrating financing options seamlessly into vendor portals, making it a preferred choice for businesses. This shift highlights the growing competition between traditional players and innovative FinTech solutions.

Independent leasing firms occupy a middle ground by combining deep asset expertise with flexible underwriting processes. These firms are increasingly forming partnerships with ERP providers and telematics suppliers, creating opportunities for cross-selling and improving customer retention. Such collaborations enhance their service offerings and make them more competitive in the evolving market. The asset finance software market is also witnessing significant growth, with digital-only players expected to double their market share by 2031. This growth is driven by the rise of embedded finance, which is transforming the origination process and enabling more seamless financing solutions. As a result, independent leasing firms are well-positioned to capitalize on these trends and expand their market presence.

Geography Analysis

North America accounted for 32.4% of revenue in 2025, supported by a mature equipment-leasing sector, deep captive-finance penetration, and early cloud adoption. DORA-style resilience rules have not yet arrived, but U.S. regulators are intensifying cyber-incident reporting, nudging cloud migrations. Software vendors co-develop residual-value analytics with fleet telematics providers to address the region’s electrification drive. Europe benefits from DORA’s January 2025 enforcement. Institutions prioritize platforms with built-in ICT testing, third-party oversight, and automated incident logs.

Germany, the United Kingdom, and France are advancing fastest, while Eastern Europe is accelerating as cross-border lessors unify systems to cut compliance overhead. The asset finance software market size in Europe is forecast to reach USD 2.6 billion by 2031. Asia-Pacific posts the highest regional CAGR at 12.8% through 2031. India and China ride SME equipment-finance booms embedded in e-commerce and supply-chain portals.

Nucleus Software’s FinnOne Neo 8.5 targets these needs with localized language packs and plug-and-play bureau APIs. Southeast Asian lessors favor SaaS to bypass data-center buildouts, while Australia’s miners seek AI-driven predictive maintenance for yellow-goods fleets. South America revives after currency volatility subsides. Argentina and Brazil both recorded above-40% leasing growth in 2025, driven by logistics and aircraft upgrades. Platforms with hedging modules and inflation indexing gain favor. The Middle East and Africa remain smaller but show bursts of activity as Islamic-finance houses digitize ijarah leasing and sovereign funds finance infrastructure.

Competitive Landscape

No single vendor dominates the market, resulting in a market concentration score of 4. The landscape features established players like Odessa, Alfa, FIS, and Oracle, competing alongside nimble SaaS newcomers such as Cloud Lending, Basikon, and QuickFi. The established players focus on tier-1 banks, offering advanced solutions like multi-currency syndication, waterfall accounting, and robust core integrations to meet complex needs. On the other hand, the agile challengers cater to mid-market and FinTech clients, leveraging their strengths in rapid deployment, embedded-finance APIs, and AI-driven underwriting. This division highlights the contrasting strategies of incumbents and challengers as they vie for market share in a competitive environment.

As deal-making heats up, notable acquisitions are reshaping the market landscape. Solifi's 2025 takeover of Leasepath expands its reach in the mid-market segment, strengthening its position. Diversis Capital's 2026 acquisition of LTi Technology Solutions introduces AI capabilities into the ASPIRE platform, enhancing its technological edge. Similarly, Liventus’s 2026 purchase of Tamarack consolidates seven equipment-finance modules, creating a unified solution. Private-equity firms are increasingly drawn to the predictable revenue streams of SaaS models and the potential for cross-border expansion. These firms are paying a premium, with valuations reaching 6.4 times EV/LTM for North American targets, compared to 4.4 times globally, reflecting the region's higher growth potential.

Emerging opportunities are evident in sectors such as renewable energy, battery storage, and circular-economy leasing. These areas remain underexplored due to the challenges posed by uncertain residual values, which deter traditional lenders. However, vendors that integrate carbon tracking and end-of-life valorization analytics are positioning themselves to capitalize on this next wave of growth. Partnerships with ERP systems, telematics providers, and payment-gateway suppliers are becoming critical to building ecosystems that enhance customer retention. These collaborations not only lock in customers but also increase switching costs, providing vendors with a competitive advantage in these evolving markets.

Asset Finance Software Industry Leaders

Odessa, Inc.

Alfa Financial Software Holdings Plc

Linedata Services S.A.

NETSOL Technologies, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Oracle rolled out Agentic AI, a cloud-only corporate-banking suite with natural-language portfolio queries.

- April 2026: Sopra Banking Software unveiled SBS Lending Suite, a cloud-native offering with pre-integrated bureau and telematics APIs.

- April 2026: NETSOL Technologies upgraded Toyota Leasing Thailand, adding mobile-first apps and instant AI decisioning.

- March 2026: Liventus acquired Tamarack, bringing seven equipment-finance platforms under one 150-engineer umbrella.

Global Asset Finance Software Market Report Scope

The Asset Finance Software Market refers to solutions that enable financial institutions, leasing companies, and enterprises to manage the lifecycle of asset-based financing, including leasing, loans, and hire purchase agreements. These platforms support functions such as credit assessment, contract management, payment processing, asset tracking, and regulatory compliance. The software helps streamline operations, improve risk management, and enhance customer experience through automation and analytics.

The Asset Finance Software Report is Segmented by Asset Type (Equipment Leasing, Automotive Finance, Real-Estate and Mortgage, Aircraft and Marine, Other), Deployment Model (On-Premise, Cloud), Organization Size (Large Enterprises, SMEs), End-User Industry (Banks and Captives, Independent Lessors, FinTech Lenders, Other), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are in Value (USD).

| Equipment Leasing |

| Automotive Finance |

| Real-Estate and Mortgage |

| Aircraft and Marine |

| Other Asset Types |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banks and Captive Finance Subsidiaries |

| Independent Finance and Leasing Companies |

| FinTech and Digital-Only Lenders |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Asset Type | Equipment Leasing | ||

| Automotive Finance | |||

| Real-Estate and Mortgage | |||

| Aircraft and Marine | |||

| Other Asset Types | |||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | Banks and Captive Finance Subsidiaries | ||

| Independent Finance and Leasing Companies | |||

| FinTech and Digital-Only Lenders | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the asset finance software market be by 2031?

Mordor Intelligence projects the asset finance software market size to reach USD 8.01 billion by 2031, expanding at a 9.8% CAGR over 2026-2031.

Which deployment model is growing fastest?

Cloud deployments post a 13.5% CAGR through 2031 as lessors favor subscription pricing, elastic scaling, and built-in compliance modules.

What asset type drives the most software demand?

Equipment leasing led with 42.9% revenue in 2025 and remains the anchor segment, while aircraft and marine financing shows the quickest growth at 11.9% CAGR.

Which region will contribute the highest incremental revenue?

Asia-Pacific records a 12.8% CAGR through 2031 thanks to SME equipment-finance booms in India, China, and Southeast Asia.

Why are FinTech lenders important to future growth?

FinTech and digital-only lenders expand at 15.2% CAGR by embedding finance at the point of sale, capturing clients that traditional banks overlook.

What is the main barrier to platform migration for incumbents?

High integration costs tied to 15-year-old core systems delay rollouts by up to 24 months and consume nearly half of IT budgets, slowing cloud transitions.

Page last updated on: