Internal Nasal Dilators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

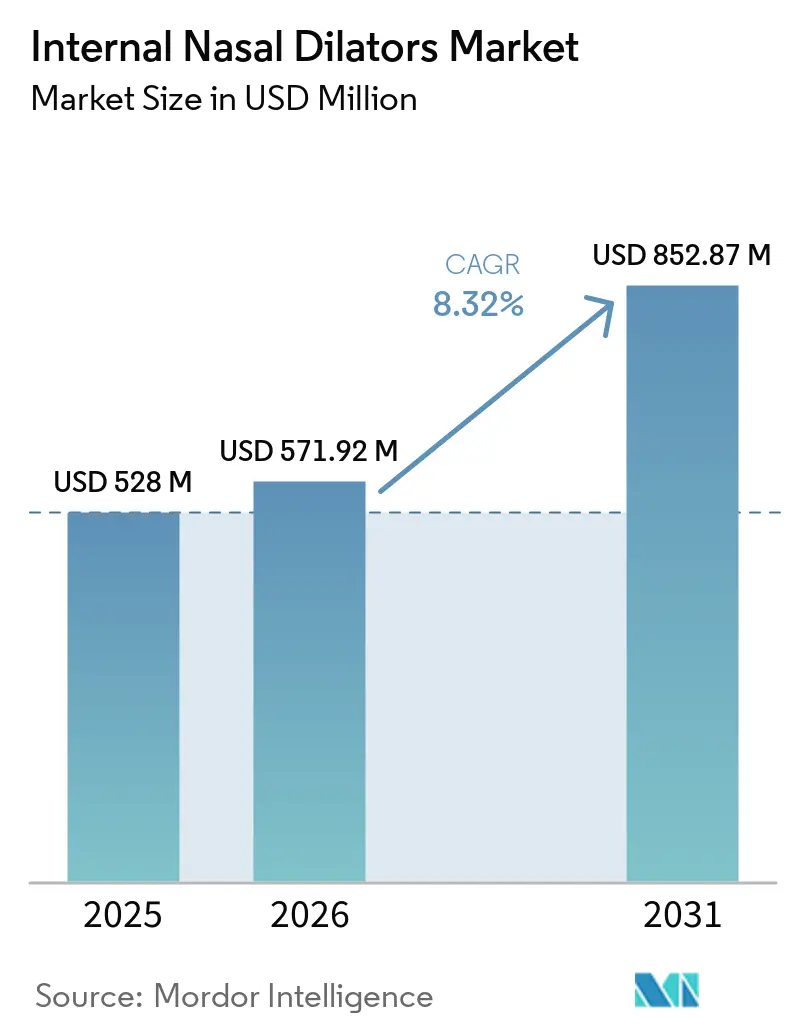

| Market Size (2026) | USD 571.92 Million |

| Market Size (2031) | USD 852.87 Million |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Internal Nasal Dilators Market Analysis by Mordor Intelligence

The Internal Nasal Dilators Market size was valued at USD 528 million in 2025 and is estimated to grow from USD 571.92 million in 2026 to reach USD 852.87 million by 2031, at a CAGR of 8.32% during the forecast period (2026-2031).

The market is expanding because consumers and clinicians are showing stronger preference for drug-free airway support before moving to medicines or surgery, while the underdiagnosed burden of obstructive sleep apnea and chronic snoring keeps first-line demand broad. The internal nasal dilators market is also benefiting from smartwatch-led sleep tracking and wider consumer attention to breathing quality during sleep, which lowers the amount of awareness building that brands need to fund on their own. Digital commerce is changing category access because online pharmacy and direct channels remove shelf-space limits and help specialist brands scale through multi-SKU portfolios, subscription programs, and repeat purchase models. Competitive positioning is moving toward reusable formats, fit improvement, and clinical-adjacent use cases such as CPAP support, while companies still need to manage low-cost polymer competition and labeling discipline under Class I device rules. The internal nasal dilators market still faces pressure from out-of-pocket purchasing and substitute options such as external strips, yet opportunities continue to widen through sports recovery use, online pharmacy expansion, and higher recurring use among consumers who want reusable solutions.

Key Report Takeaways

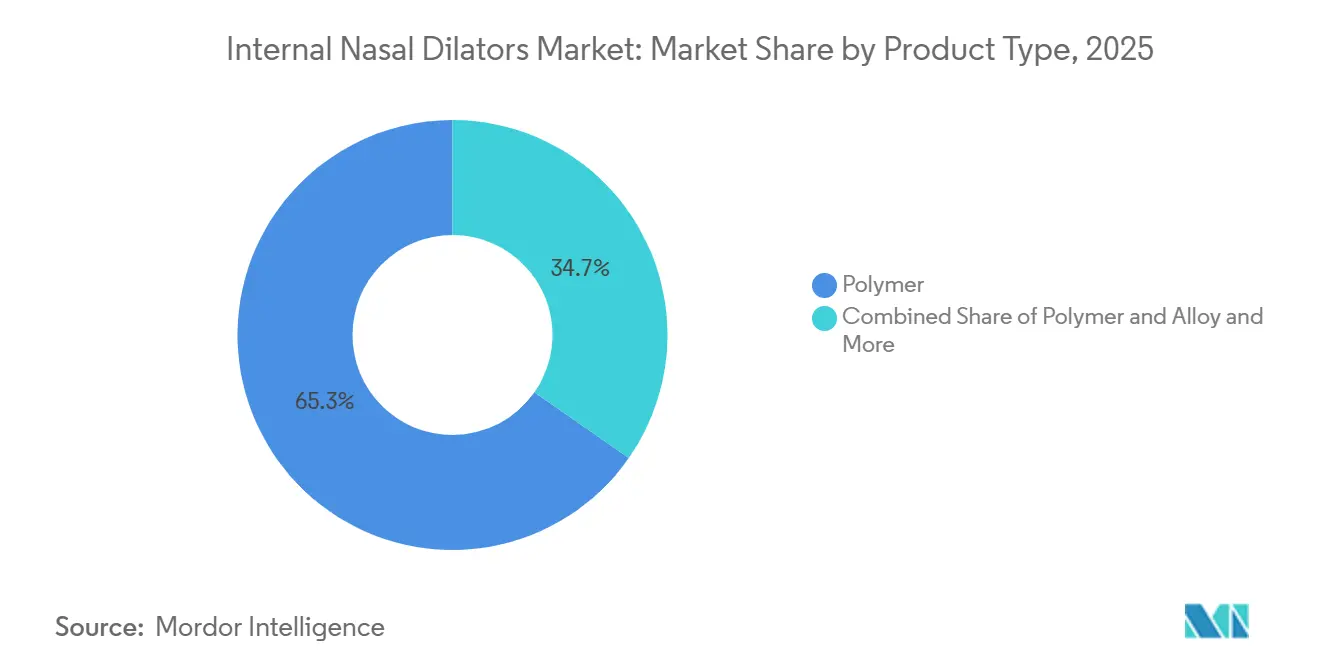

- By product type, pure polymer held 65.31% share in 2025, while polymer and alloy is projected to expand at a 9.38% CAGR through 2031.

- By usability, reusable devices held 59.24% share in 2025 and are expected to record the highest CAGR at 10.52% through 2031.

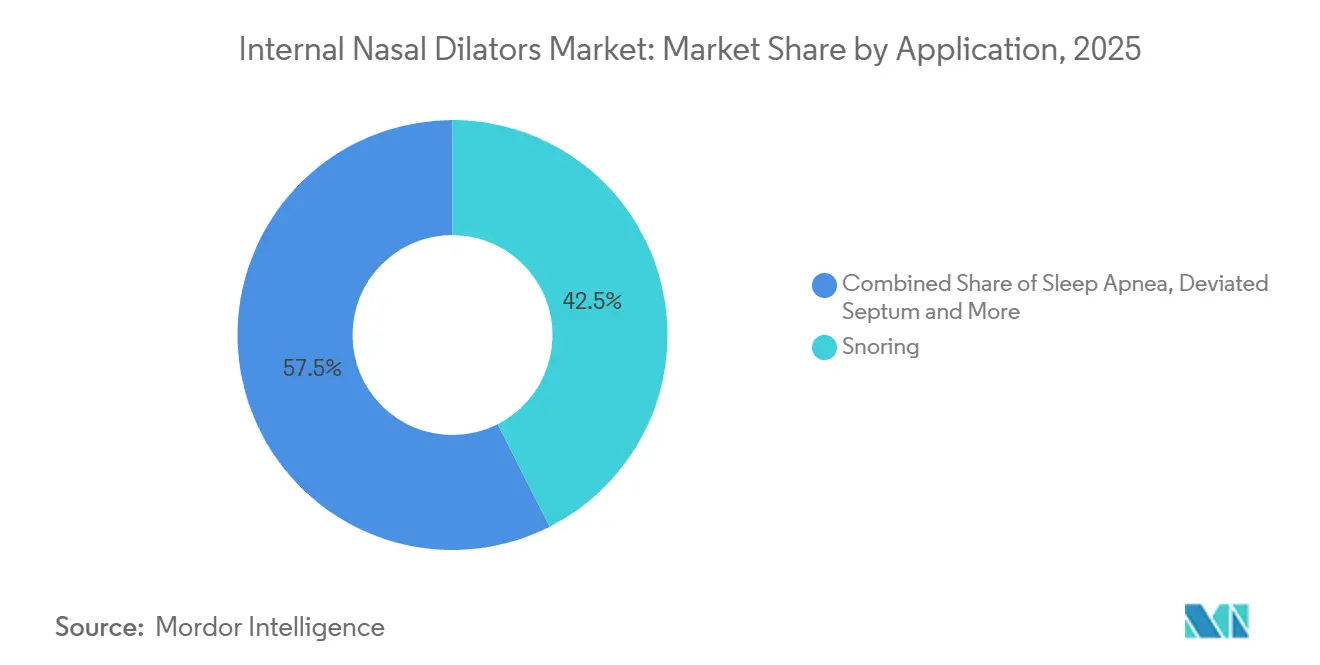

- By application, snoring accounted for 42.52% share in 2025, while sleep apnea is forecast to grow at a 9.25% CAGR through 2031.

- By distribution channel, retail pharmacies held 45.62% share in 2025, while online pharmacies are projected to grow at a 10.25% CAGR through 2031.

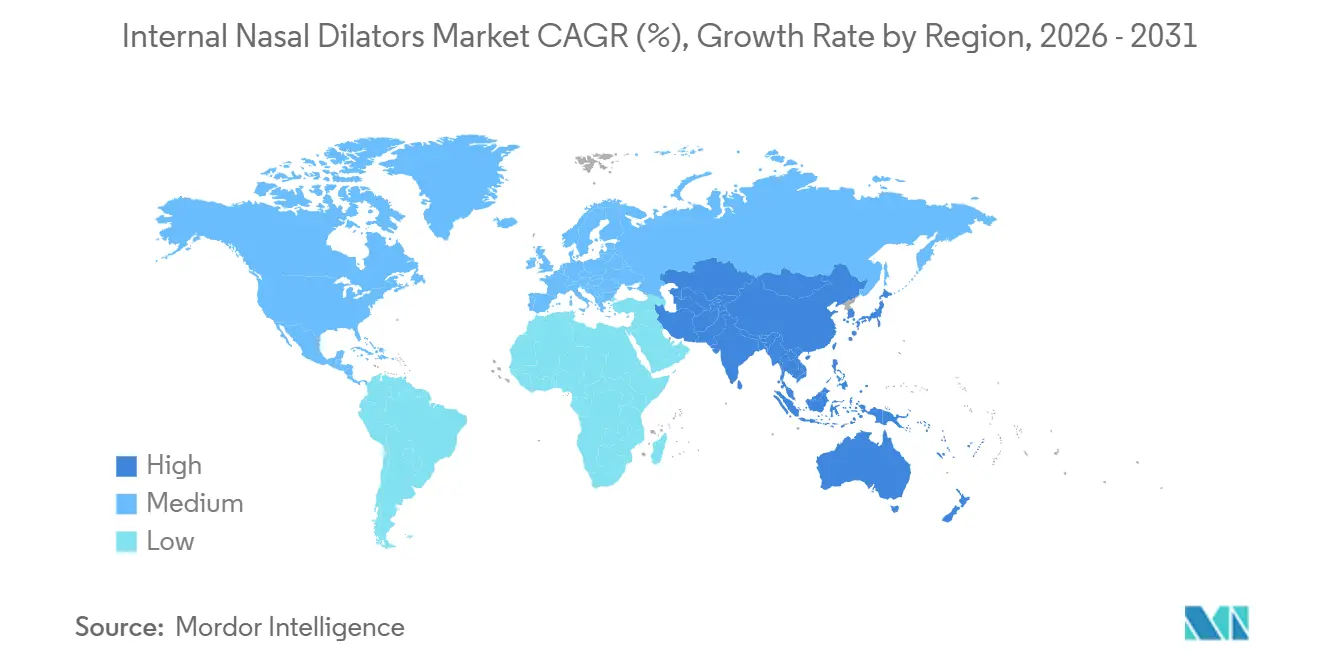

- By geography, North America held 45.22% of the internal nasal dilators market share in 2025, while Asia-Pacific is projected to expand at a 9.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Internal Nasal Dilators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Sleep-Related Breathing Disorders | +1.8% | Global | Long term (≥ 4 years) |

| Preference For Drug-Free, Non-Invasive Breathing Aids | +1.5% | Global, strongest in North America & EU | Medium term (2-4 years) |

| Growth Of Direct-To-Consumer And Online Pharmacy Channels | +1.4% | Global, led by North America & APAC | Medium term (2-4 years) |

| Wider Use In Sports Performance And Recovery | +0.8% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Rising Clinical Interest In CPAP Adjunct And Nasal Airflow Support | +0.9% | North America & EU | Long term (≥ 4 years) |

| Under-Reported Demand From Travel, Shift Work, And Portable Sleep-Routine Use | +0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Sleep-Related Breathing Disorders

The internal nasal dilators market is drawing strength from the large pool of people who live with sleep-disordered breathing but remain outside formal diagnosis pathways. The analysis notes that 80-90% of obstructive sleep apnea cases are undiagnosed at any given time, which keeps self-treatment behavior important for over-the-counter device categories. A 2025 Nature Communications study added a new layer by showing that rising ambient temperatures can worsen upper-airway collapsibility and increase obstructive sleep apnea severity over time. That finding matters because it extends demand drivers beyond aging and obesity and links nighttime breathing disruption to broader environmental conditions. China and India remain especially important because they carry a very large affected population and have many consumers who are more likely to try simple over-the-counter solutions before seeking specialist care. This keeps the internal nasal dilators market tied not only to diagnosed patients, but also to a recurring base of consumers managing congestion, snoring, and airflow discomfort on their own.

Preference For Drug-Free, Non-Invasive Breathing Aids

The internal nasal dilators market continues to benefit from consumers who want airflow support without depending on medicines for long periods. Mechanical dilation addresses physical restriction at the nasal valve and avoids concerns tied to rebound effects, skin adhesives, or routine pharmacological use. Under 21 CFR 874.3900, nasal dilators are classified as Class I devices that are exempt from premarket notification, which lowers commercialization barriers compared with drug-based nasal therapies[1]U.S. Food and Drug Administration, “21 CFR § 874.3900, Nasal Dilator,” Electronic Code of Federal Regulations, law.cornell.edu. A 2024 American Psychiatric Association report showing that 34% of Americans rated their sleep quality as poor or fair and that more than 50 million Americans suffer from chronic sleep disorders, which supports broad consumer interest in non-drug sleep support tools. Internal devices also avoid the skin irritation issues that can reduce adherence to adhesive strips, especially for repeat users who want a reusable option. This supports a premium tier in the internal nasal dilators market where comfort, durability, and repeat nightly use matter more than single-purchase convenience.

Growth Of Direct-To-Consumer And Online Pharmacy Channels

The internal nasal dilators market is being reshaped by online pharmacy and direct-to-consumer channels that reduce dependence on physical shelf placement. This matters because specialist brands do not need the same in-store bargaining power once search-driven discovery, subscriptions, and marketplace reviews become major purchase drivers. Redcare Pharmacy reported 13.9 million active customers in 2025, while its non-Rx over-the-counter revenue grew at 8-10% annually and the company projected 13-15% Group revenue growth in 2026. That scale shows how digital pharmacy can function as a high-velocity route for consumer breathing aids, particularly when repeat use and fast replenishment matter. The internal nasal dilators market is also seeing this logic in product strategy, as WoodyKnows expanded its FDA-registered model range in May 2026 to support a broader multi-SKU online presence[2]M&M Pure Air Systems LLC, “FDA GUDID Device Listings, ND1-ND4 And Related Models,” FDA GUDID Listing, fda.report. Wider use in sports performance, travel routines, and shift-work sleep support also fits digital channels well because these buyers often search online for specific symptoms, use cases, and product formats before trying the category.

Rising Clinical Interest In CPAP Adjunct And Nasal Airflow Support

The internal nasal dilators market is gradually moving closer to formal sleep care through CPAP-adjunct use and broader clinical interest in airflow support. Nasal obstruction can increase the pressure CPAP systems need to maintain airway patency, so improving nasal airflow can help some users tolerate therapy better. A 2026 systematic review covering 17 studies and 496 participants found that internal nasal dilators are not effective as stand-alone obstructive sleep apnea monotherapy, but they can offer adjunct value for selected patients, especially those with mild disease or nasal valve compromise. That matters because it shifts the device from a pure consumer comfort product toward a product that can support established sleep therapy pathways. Hospital pharmacies and sleep clinics are the most direct channels for this position because they can connect device use to defined patient needs. The internal nasal dilators market could therefore add recurring demand from CPAP users even without claiming stand-alone treatment efficacy, which helps widen the addressable base while staying within a more disciplined clinical narrative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product Discomfort And Fit Variability | -1.2% | Global | Short term (≤ 2 years) |

| Reimbursement Gaps And Consumer Out-Of-Pocket Sensitivity | -0.9% | Global, most acute in APAC and MEA | Medium term (2-4 years) |

| Strong Substitution From External Strips And Clinical Alternatives | -1.0% | Global, strongest in North America | Long term (≥ 4 years) |

| Regulatory And Biocompatibility Burden On New Materials And Designs | -0.5% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Product Discomfort And Fit Variability

The internal nasal dilators market still faces a meaningful adoption barrier because device comfort depends heavily on individual nostril geometry and fit. Small differences in nasal valve structure can change how pressure is felt during sleep, which makes a poor first experience more damaging than in many other over-the-counter categories. Common abandonment reasons on e-commerce platforms include intranostril pressure, mid-night displacement, and irritation from contact with nasal hair. Multi-size offerings and adjustable geometries are helping brands reduce these issues, yet they have not removed the category’s core fit challenge. That challenge matters even more in the internal nasal dilators market because purchases are often made without clinical guidance or in-person fitting. Until personalized-fit approaches become widely affordable, weak fit can continue to suppress repurchase, referral, and long-term habit formation.

Reimbursement Gaps And Consumer Out-Of-Pocket Sensitivity

The internal nasal dilators market remains largely dependent on direct consumer spending because standard reimbursement pathways are generally absent in the United States and major European markets. The Class I exempt status and comfort-assist positioning of the category, which keeps these devices outside the reimbursement frameworks available to more formal respiratory therapies. That out-of-pocket model limits adoption among lower-to-middle-income consumers, especially in Asia-Pacific and the Middle East and Africa where discretionary health spending is tighter. The same issue also places a ceiling on premium pricing because many buyers trade down to low-cost polymer options rather than paying for alloy blends or more advanced reusable formats. This makes loyalty programs, direct-to-consumer subscriptions, and sports-focused positioning commercially useful, but it does not fully offset the demand ceiling created by self-pay dependence. The internal nasal dilators market therefore grows best where product affordability, strong digital access, and consumer awareness come together at the same time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polymer Leadership Holds While Alloy Blends Gain Traction

Pure polymer devices held 65.31% of the segment in 2025, while polymer and alloy is projected to record the fastest growth at a 9.38% CAGR through 2031. Pure polymer keeps a large installed base because it is easy to manufacture at scale and it supports lower price points for single-use or basic reusable products. That price accessibility matters in the internal nasal dilators market because many first purchases are trial purchases rather than highly committed medical purchases. Polymer also remains acceptable for short-cycle use where low unit cost matters more than long wear comfort or premium feel. The internal nasal dilators market share for pure polymer therefore stayed high in 2025 because it matched the needs of mass retail and value-seeking buyers.

Polymer and alloy products are growing faster because they are positioned around better structural memory, more stable dilation force, and improved overnight comfort. That premium positioning fits consumers who have already tried basic products and are willing to pay more for a reusable option that feels more consistent. The segment also aligns with the broader shift toward products that can support repeat nightly use rather than occasional symptom relief. Other product types remain small in volume, but they matter because clinical-grade cones and CPAP-adjunct forms can support higher average selling prices. Over time, the internal nasal dilators market is likely to keep pure polymer as the volume anchor while alloy blends capture a larger share of value through upgrade behavior.

By Usability: Reusable Devices Drive Both Scale And Upgrade Spending

Reusable devices held 59.24% of the usability segment in 2025 and are projected to grow at a 10.52% CAGR through 2031. This is important because the dominant format is also the fastest-growing format, which signals broad acceptance rather than a narrow premium niche. The internal nasal dilators market is benefiting from reusable economics because one unit priced at USD 12 to USD 25 can cover weeks or months of use, which improves perceived value versus repeated disposable purchases. That value logic supports habit formation, and habit formation matters in a category that depends on repeat nightly use. The segment also benefits from the fact that reusable devices avoid adhesive contact with skin and can feel more practical for long-term users.

Single-use devices still hold a role in hospitals, post-rhinoplasty support, and first-time trial packs where consumers want to test size and fit before moving up to a reusable product. WoodyKnows highlighted this logic in 2024 through multi-size trial pack offerings designed to reduce abandonment during the first purchase stage[3]WoodyKnows, “Super Support 2024 Standard And Soft Nasal Dilators,” WoodyKnows, woodyknows.com. That approach reflects a broader truth in the internal nasal dilators market, because poor initial fit is one of the strongest reasons for category drop-off. Reusable formats are also better suited to subscription and replenishment ecosystems, where accessories, replacement cycles, and repeat site visits help improve retention. The result is a usability mix where disposables support entry and clinical use, while reusable devices capture more of the long-term revenue base.

By Application: Snoring Leads Today While Sleep Apnea Adds Faster Growth

Snoring accounted for 42.52% of the application segment in 2025, while sleep apnea is projected to expand at a 9.25% CAGR through 2031. Snoring remains the largest application because it is the most visible and immediately disruptive symptom for many households, which makes it a common first reason to try a device. This keeps the internal nasal dilators market closely connected to consumer self-care behavior rather than only to formal respiratory diagnosis. Many buyers enter the category because of nighttime noise, congestion, or partner feedback long before they pursue specialist sleep evaluation. Deviated septum and nasal congestion applications also remain important because those buyers often show stronger willingness to pay for comfort and fit.

Sleep apnea is growing faster because the clinical narrative is becoming more defined around adjunct support rather than stand-alone treatment. The 2026 systematic review confirmed that internal nasal dilators can support selected patient groups as adjunct therapy, especially where mild symptoms or nasal valve compromise are present. That shifts usage toward a more recurring pattern, which lifts lifetime value compared with occasional snoring relief. Other applications also extend the category beyond classic sleep complaints, including allergy management, shift-work sleep optimization, and travel fatigue support. A 2024 study in endurance athletes with nasal valve compromise further showed improved aerobic performance with internal nasal dilation, which helps explain why sports recovery and breathing efficiency remain useful side doors into the internal nasal dilators market.

By Distribution Channel: Retail Pharmacies Lead While Online Pharmacies Set The Pace

Retail pharmacies held 45.62% of the distribution segment in 2025, while online pharmacies are projected to grow at a 10.25% CAGR through 2031. Retail remains important because it is still the main discovery point for many first-time buyers who make symptom-led purchases near sleep aids, congestion products, or respiratory care shelves. Pharmacist recommendation and immediate product availability also support trial in ways that digital channels cannot fully replace. The internal nasal dilators market size in retail stays strong because established chains give brands broad geographic reach and help reinforce category legitimacy. Hospital pharmacies maintain a narrower but stable role through CPAP-adjunct users, ENT practices, and post-procedure use cases where clinician touchpoints matter more.

Online pharmacies are growing faster because they fit the way consumers research sleep support products, compare sizes, read reviews, and reorder without friction. Redcare’s 13.9 million active customers in 2025 show the scale that digital pharmacy can offer to non-prescription health categories. WoodyKnows reinforced the multi-SKU online strategy in May 2026 by expanding its FDA-registered portfolio across several internal nasal dilator models. Other channels such as athletic retailers, health clubs, and biohacking subscription boxes remain smaller, but they are well aligned with sports recovery and performance-oriented use cases. That mix leaves the internal nasal dilators market with a wide access structure where mass retail drives scale and online channels drive the fastest incremental growth.

Geography Analysis

North America held 45.22% of the internal nasal dilators market in 2025, making it the largest regional contributor by a clear margin. The region benefits from high awareness of sleep disorders, stronger diagnosis rates, and a mature over-the-counter pharmacy network that supports trial and repeat purchasing. Rhinomed showed the strength of this route in 2024 when its Mute Nasal Dilator secured shelf space in more than 4,500 CVS stores and 1,500 Walgreens stores in the United States. That kind of chain placement is important because it gives a specialist product broad consumer visibility and helps normalize the category in everyday retail settings. Canada and Mexico remain smaller within the region, but both are supported by improving digital pharmacy access and a similar consumer preference for practical drug-free respiratory support.

Europe remains the second-largest region in the internal nasal dilators market, with Germany, the United Kingdom, and France acting as the main anchors. Consumer familiarity with non-drug breathing support is well established across these countries, which supports steady demand for both value and premium product formats. The regional online pharmacy base also adds speed to category growth, especially for specialist brands that do not depend entirely on store shelf access. Redcare Pharmacy’s 13.9 million active customers in 2025 and its 2026 growth outlook illustrate the depth of that digital channel in Europe. This leaves Europe as a stable region where digital distribution can widen reach without needing the same scale of mass retail penetration seen in North America.

Asia-Pacific is the fastest-growing region with a projected 9.15% CAGR through 2031, and this part of the internal nasal dilators market size is being supported by a very large untreated demand base. China remains central because it carries the largest absolute obstructive sleep apnea population, and the 2025 Nature Communications study suggests that rising temperatures can compound future burden by worsening disease severity. India presents a strong adoption runway through digital pharmacy growth, broader health awareness, and a rising urban middle class that is more willing to spend on consumer sleep products. Japan and South Korea grow more steadily, but they offer stronger premium-device potential because consumers in those markets place more weight on medically validated and comfort-focused formats. South America and the Middle East and Africa remain smaller, with Brazil and Argentina leading in South America and GCC countries showing the clearest demand in MEA because obesity-linked sleep disorder patterns remain a structural tailwind in regional health statistics. The internal nasal dilators market share is still concentrated in North America today, yet the medium-term growth story is increasingly shaped by Asia-Pacific and selected self-pay urban clusters outside the largest developed markets.

Competitive Landscape

The internal nasal dilators market is moderately fragmented, with more than 20 active participants competing across specialty device brands and broader consumer health operators. Competition depends less on absolute scale and more on fit quality, reusable product design, pricing discipline, and channel execution. Structural entry barriers remain limited because nasal dilators fall under Class I exempt rules, which makes product launches easier than in many regulated therapeutic categories. That lower barrier keeps product turnover active and supports a constant flow of new models aimed at comfort, durability, or more precise use-case positioning. The internal nasal dilators market is therefore competitive by design, even though leading brands still benefit from stronger shelf presence, regulatory familiarity, and broader product assortments.

Incumbent brands retain an advantage in retail access because physical shelf placement still matters for first-time buyers who want an immediate solution. Rhinomed’s reported store presence in more than 4,500 CVS locations and 1,500 Walgreens locations showed how important chain distribution remains for mainstream visibility in the United States. At the same time, digitally native players are pressing harder in the online channel through trial packs, multi-size options, and price-per-use arguments that resonate with repeat buyers. WoodyKnows illustrated this posture in May 2026 by registering a broad set of nasal dilator models on FDA GUDID, which supports multi-SKU e-commerce positioning and gives the brand a stronger compliance-backed product story. The internal nasal dilators market is also seeing wider differentiation through sports-recovery messaging and reusable design claims, which helps smaller brands avoid direct competition on shelf dominance alone.

Recent product activity suggests that competitive shifts are likely to come from faster SKU refresh and channel-specific packaging rather than from major consolidation. Breathewave’s December 2025 GUDID publication of a contoured reusable nasal dilator added another anatomically differentiated offer to the U.S. product field. White space still exists around CPAP bundle partnerships, clinician-guided fit programs, and product architectures that can improve first-use comfort enough to raise conversion and retention. For that reason, the internal nasal dilators market is likely to see share movement through execution and product refinement rather than through a single company taking a dominant control position.

Internal Nasal Dilators Industry Leaders

Rhinomed Limited

Splintek, Inc.

SANOSTEC CORP

Scandinavian Formulas Inc.

WoodyKnows (M&M Pure Air Systems LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: WoodyKnows (M&M Pure Air Systems LLC) registered an expanded portfolio of internal nasal dilator models, including ND1 through ND4, MT1, MT2, BP1 through BP3, SD1 through SD3, and UB1 through UB3, on the FDA's Global Unique Device Identification Database (GUDID), significantly broadening its FDA-registered product range. The move signals a deliberate strategy to scale e-commerce multi-SKU presence with full regulatory credentialing.

- December 2025: A contoured internal nasal dilator under the Breathewave brand name was published on the FDA GUDID, classified as an internal reusable nasal breathing aid designed to reduce nasal resistance and increase airflow. The listing expands the roster of FDA-registered internal nasal dilator devices available in the United States, adding a newly contoured anatomical geometry to the competitive product field.

Global Internal Nasal Dilators Market Report Scope

As per the scope of the report, internal nasal dilators are medical devices inserted into the nasal passages to help improve airflow by widening the nasal passages. They are typically used to reduce nasal congestion, snoring, and breathing difficulties during sleep or physical activity.

The internal nasal dilators market is segmented by product type into polymer, polymer and alloy, and other product types. By usability, the market is divided into reusable and single-use. Based on application, it is categorized into snoring, sleep apnea, deviated septum, nasal congestion, and other applications. By distribution channel, the segmentation includes hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Polymer |

| Polymer and Alloy |

| Other Product Types |

| Reusable |

| Single Use |

| Snoring |

| Sleep Apnea |

| Deviated Septum |

| Nasal Congestion |

| Other Applications |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Polymer | |

| Polymer and Alloy | ||

| Other Product Types | ||

| By Usability | Reusable | |

| Single Use | ||

| By Application | Snoring | |

| Sleep Apnea | ||

| Deviated Septum | ||

| Nasal Congestion | ||

| Other Applications | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value and 2031 outlook for internal nasal dilators?

The internal nasal dilators market stands at USD 571.92 million in 2026 and is projected to reach USD 852.87 million by 2031 at an 8.32% CAGR.

Which product type is leading revenue in internal nasal dilators?

Pure polymer led with 65.31% share in 2025 because it offers scale manufacturing, lower prices, and broad retail suitability.

Which format is growing fastest in nasal dilator products?

Reusable devices are the fastest-growing format at a 10.52% CAGR through 2031 and also held the largest usability share at 59.24% in 2025.

Why is sleep apnea becoming a bigger growth area for these devices?

Sleep apnea is projected to grow at a 9.25% CAGR through 2031 because clinical use is shifting toward adjunct support, especially for selected patients with mild symptoms or nasal valve compromise.

Which sales channel is expanding fastest for internal nasal dilators?

Online pharmacies are growing fastest at a 10.25% CAGR through 2031 because they support subscriptions, reviews, multi-SKU comparison, and repeat ordering.

Which region offers the strongest current base and which one grows fastest?

North America held 45.22% share in 2025, while Asia-Pacific is forecast to grow fastest at a 9.15% CAGR through 2031.

Page last updated on: