Nasal Packing Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 210.40 Million |

| Market Size (2030) | USD 285.10 Million |

| Growth Rate (2025 - 2030) | 6.50% CAGR |

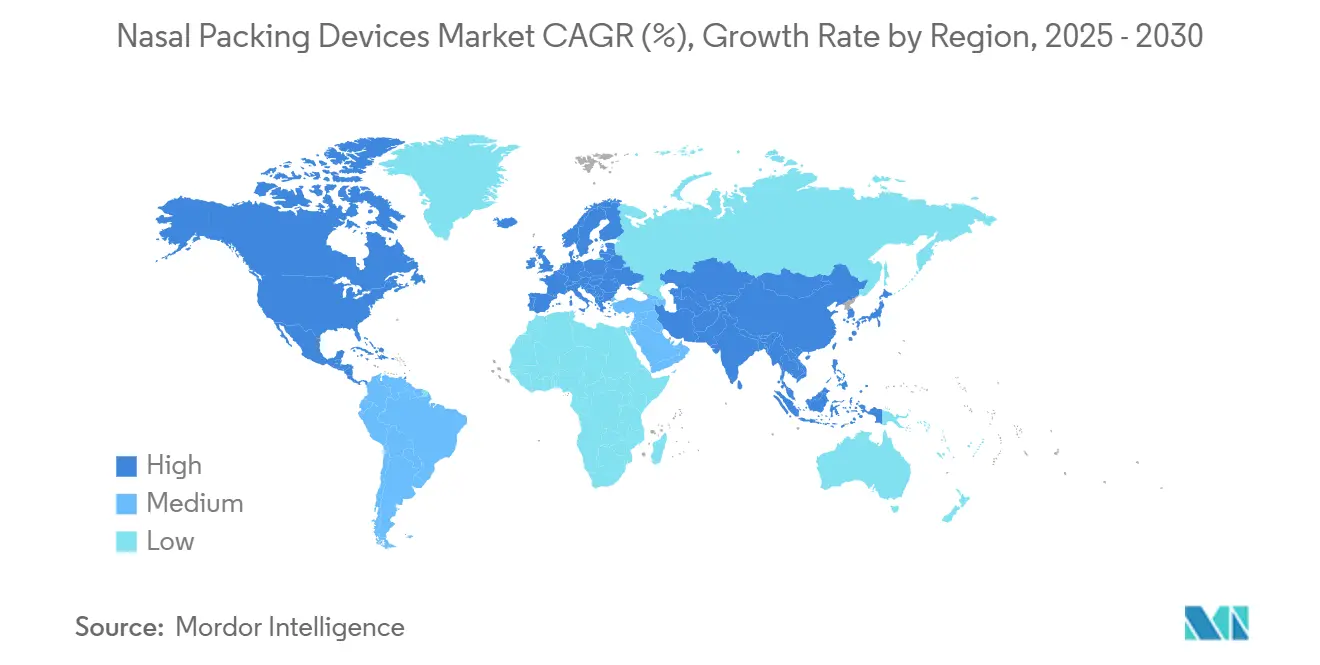

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nasal Packing Devices Market Analysis by Mordor Intelligence

The nasal packing devices market size stood at USD 210.4 million in 2025 and is projected to reach USD 285.1 million by 2030, reflecting a 6.5% CAGR over the forecast period. This growth trajectory is tied to the transition from gauze-based offerings toward bio-absorbable materials that remove the need for painful extraction and enable better hemostasis. Demand is amplified by a global shift to outpatient ear, nose and throat (ENT) procedures, hospital adoption of value-based procurement, and rising epistaxis cases in elderly anticoagulant users. Material innovation—especially chitosan derivatives—has improved antimicrobial protection, while artificial-intelligence-guided endoscopy enhances surgical accuracy and can reduce the quantity of packing required. Competitive intensity is moderate yet climbing as incumbents acquire niche innovators to broaden bio-absorbable portfolios and reinforce intellectual-property barriers.

Key Report Takeaways

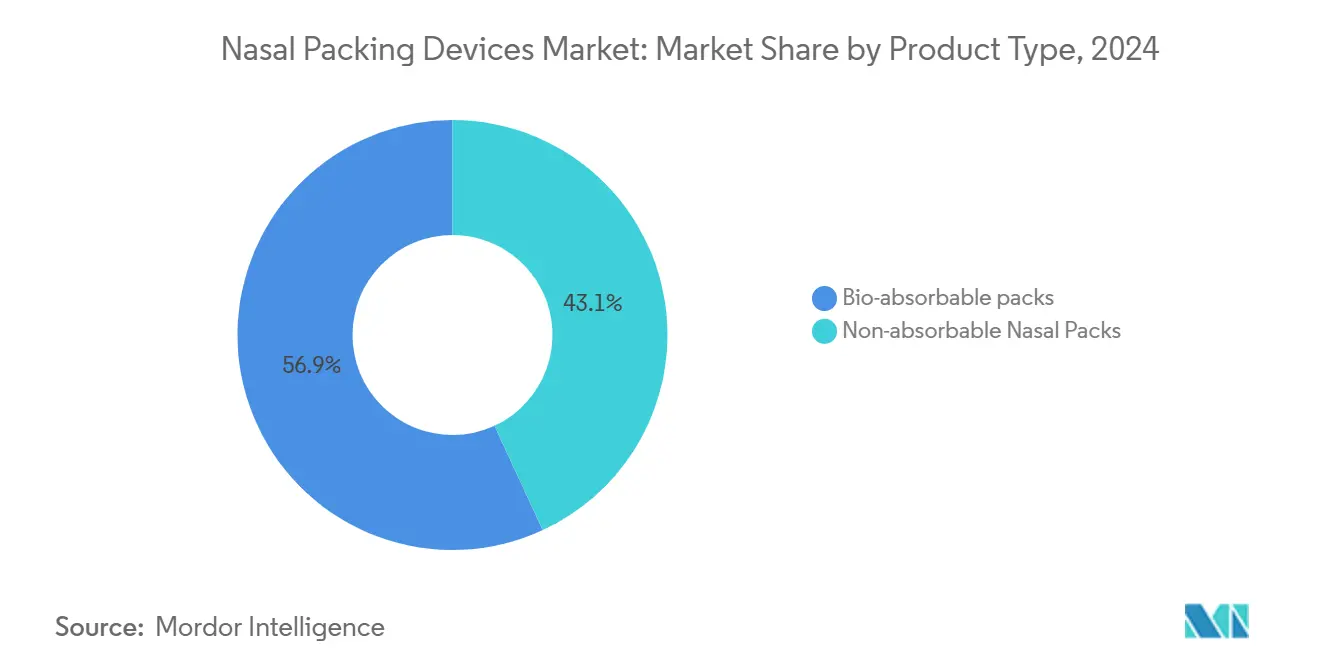

- By product type, bio-absorbable nasal packs led with 56.9% revenue share in 2024, while the same segment is set to expand at an 8.9% CAGR through 2030, underscoring their widening clinical acceptance.

- By material, polyvinyl alcohol held 38.4% of nasal packing devices market share in 2024; chitosan derivatives are projected to grow at a 9.6% CAGR through 2030 on the strength of their dual hemostatic and antimicrobial benefits.

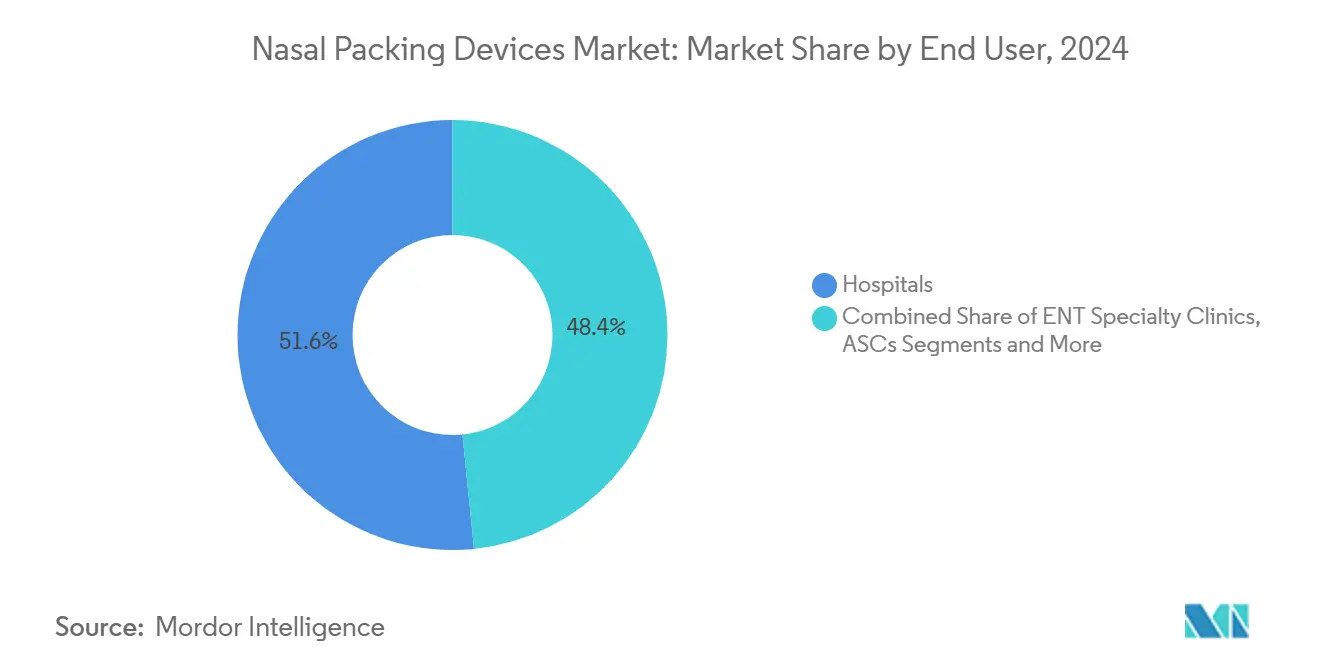

- By end user, hospitals accounted for 51.6% share of the nasal packing devices market size in 2024, whereas ambulatory surgical centers are advancing at an 8.4% CAGR through 2030 as outpatient ENT volumes accelerate.

- By geography, North America captured 38.5% revenue share in 2024; Asia Pacific is on track for an 8.3% CAGR to 2030, propelled by expanding surgical infrastructure.

Global Nasal Packing Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth In Outpatient ENT Procedures | +1.20% | Global, with North America leading adoption | Medium term (2-4 years) |

| Increasing Adoption Of Bio-Resorbable Materials | +1.50% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Rising Burden Of Epistaxis Among Anticoagulant Users | +0.80% | Global, particularly aging populations | Short term (≤ 2 years) |

| Surge In Functional Endoscopic Sinus Surgery (FESS) Volumes | +1.10% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Hospitals Shifting To Value-Based Procurement Contracts | +0.70% | North America & EU | Long term (≥ 4 years) |

| AI-Guided Tampon Inflation & Pressure Monitoring Systems | +0.20% | North America, early adoption phase | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Outpatient ENT Procedures

Ambulatory surgical centers have become central to ENT care as payers reward shorter stays and patients seek same-day discharge. ASC facility fees have risen while physician reimbursement lags, encouraging providers to migrate sinus surgeries from inpatient wards.[1]AAO-HNSF Journals, “Poster Presentations,” aao-hnsfjournals.onlinelibrary.wiley.com Administrators favor devices that lower post-operative monitoring needs, creating premium demand for bio-absorbable packs that dissolve without follow-up visits. Complication avoidance has a direct profit impact since emergency readmissions erode slim outpatient margins. Manufacturers that evidence lower rebleed rates are winning formularies, especially among chains operating multiple ASCs. As a result, the nasal packing devices market continues pivoting toward products suited to outpatient protocols.

Increasing Adoption of Bio-Resorbable Materials

Clinical society endorsements now position bio-absorbable implants as standard care for nasal valve collapse and post-sinus-surgery hemostasis. Resorbable chitosan dressings combine clotting efficiency and antimicrobial action, directly addressing hospital stewardship goals amid antibiotic-resistance concerns. Payers recognize that eliminating removal appointments lowers total episode cost, so reimbursement pathways increasingly cover premium packs. Guidelines recommend resorbable options for patients on anticoagulants, broadening indications. Manufacturers equipped with robust real-world evidence are accelerating conversions from gauze to bio-absorbable across the nasal packing devices market.

Rising Burden of Epistaxis Among Anticoagulant Users

Dual antiplatelet therapies and direct oral anticoagulants have lifted the procedural burden for intractable nosebleeds, with intervention rates in emergency settings climbing above 10%.[2]Journal of Biomedical Science, “Chitosan-Based Formulations,” jbiomedsci.biomedcentral.com Traditional cotton packs fail to control active bleeding in these patients, so clinicians prefer chitosan-based or liquid self-expanding devices that exert uniform pressure and speed clotting. Hospitals are issuing epistaxis pathways specifying dissolvable packing to avoid traumatic extraction that could trigger rebleeds. Vendors able to validate efficacy in anticoagulated cohorts gain fast-track access, supporting growth in the nasal packing devices market.

Surge In Functional Endoscopic Sinus Surgery Volumes

Chronic rhinosinusitis prevalence and expanding surgical capacity, especially in Asia Pacific, continue to push FESS procedures upward. Minimally invasive tools such as coblation have improved recovery and broadened patient eligibility. Surgeons choose bio-absorbable dressings to maintain sinus patency and deter adhesion formation, aligning with enhanced-recovery protocols. Health ministries fund specialist training that elevates procedure volumes, driving regional demand for advanced materials. Consequently, bio-absorbable innovation remains central to value creation in the nasal packing devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Removal Discomfort & Pain In Non-Absorbable Packs | -0.90% | Global, particularly cost-sensitive markets | Short term (≤ 2 years) |

| Re-Bleeding Risk In Elderly Poly-Pharmacy Patients | -0.60% | Global, concentrated in aging populations | Medium term (2-4 years) |

| Supply-Chain Fragility Of Medical-Grade Chitosan | -0.40% | Global, with APAC manufacturing concentration | Medium term (2-4 years) |

| Lack Of Reimbursement For Home-Based Epistaxis Kits | -0.30% | Primarily emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Removal Discomfort & Pain in Non-Absorbable Packs

Gauze extraction routinely triggers pain scores exceeding 6 on a 10-point scale, fostering patient reluctance to seek timely care for recurrent bleeds.[3]Medicine, “Comfort of Patients with Different Nasal Packings,” journals.lww.com Emergency departments stick with gauze because of low unit cost and immediate availability, yet the negative experience undermines adherence to follow-up protocols. In cost-constrained systems, administrators hesitate to approve bio-absorbables despite evidence of fewer complications. This resistance tempers the nasal packing devices market, although rising patient-satisfaction metrics in reimbursement formulas are gradually shifting procurement decisions.

Supply-Chain Fragility of Medical-Grade Chitosan

Production hubs for high-purity chitosan clusters in select Asian economies, leaving manufacturers exposed to geopolitical or logistics shocks that already account for 27% of device supply disruptions. Quality variability across suppliers forces lengthy validation, inflating costs and inventory needs. Regulatory agencies now demand documented resiliency plans that smaller firms struggle to implement. As sustainable insect-derived chitosan scales up, supply diversity may ease risk, but for now, the constraint acts as a mild drag on the nasal packing devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bio-Absorbable Dominance Reshapes Standards

Bio-absorbable packs commanded 56.9% of 2024 revenues, demonstrating how clinician priorities have shifted toward patient comfort and complication avoidance. The segment is forecast for an 8.9% CAGR, outpacing non-absorbables as payers embrace total-cost savings. Steroid-eluting variants extend the addressable pool by cutting revision procedures, while integrated pressure sensors represent the next innovation wave.

Non-absorbable offerings retain footholds in trauma rooms and budget-constrained facilities, but reimbursement models tied to readmission penalties are eroding that share. As regulatory bodies tighten evidence requirements, firms with long-term biocompatibility data consolidate their advantage, steering the growth of the nasal packing devices market.

By Material: Chitosan Derivatives Drive Innovation

Polyvinyl alcohol held a 38.4% share yet faces growth headwinds as clinicians prefer materials with antimicrobial attributes. Chitosan derivatives, expanding at a 9.6% CAGR, leverage superior clotting kinetics and infection control to win over infection-prevention committees. Hybrid PVA-chitosan composites marry structure with biologic action, illustrating material-science convergence in the nasal packing devices industry.

Supply-chain fragility spurs research into synthetic or insect-sourced chitosan to bolster resilience and sustainability. Regulatory harmonization under FDA 21 CFR 874.3620 is pushing standardization, favoring companies with validated platform chemistries and GMP controls, underpinning orderly expansion of the nasal packing devices market.

By End User: ASCs Accelerate Market Transformation

Hospitals generated 51.6% of 2024 spending owing to complex case management, yet ASC revenue is set for an 8.4% CAGR as payers tilt toward lower-cost outpatient settings. ASCs demand packs that dissolve rapidly to align with same-day discharge pathways.

ENT specialty clinics occupy a niche between high-volume hospitals and lean ASCs, adopting premium bio-absorbables for tailored care protocols. Nasal packing devices market size growth here depends on clinics’ ability to bill bundled episodes that reward fewer follow-ups. Remote home-care remains nascent because reimbursement remains unclear, limiting uptake of simplified anterior-bleed kits even as telehealth infrastructure matures.

Geography Analysis

North America led with a 38.5% 2024 share due to robust reimbursement and early adoption of minimally invasive ENT technologies. Medicare’s pass-through device codes encourage hospitals to specify premium bio-absorbables, reinforcing domestic demand. Canada’s publicly funded model likewise values devices that shorten length of stay, sustaining regional traction for the nasal packing devices market.

Asia Pacific is the fastest-growing theater, expected to log an 8.3% CAGR through 2030 as China and India expand surgical infrastructure and surgeon training. Japanese demand concentrates on senior populations seeking less painful post-operative experiences, while South Korea’s innovation incentives speed adoption of AI-enabled packing solutions. Fragmented payer structures nonetheless challenge uniform penetration, so companies deploy tiered portfolios to match diverse affordability levels.

Europe maintains its position through strict Medical Device Regulation requirements that prioritize clinical evidence and post-market vigilance. Germany and the United Kingdom show strong uptake of chitosan derivatives, underpinned by centralized health-technology assessments that favor total-cost savings. Sustainability mandates stimulate interest in biodegradable materials, and manufacturers tout life-cycle analyses to win hospital tenders. Consequently, Europe acts as a standards setter, influencing global specifications within the nasal packing devices market.

Competitive Landscape

Market fragmentation is moderate, with leading firms employing acquisitions to deepen ENT portfolios—Integra LifeSciences’ USD 1 billion purchase of Acclarent is emblematic. Medtronic, Stryker, and Smith+Nephew anchor the top tier, leveraging scale to invest in bio-absorbable R&D and navigate evolving regulation. Mid-size challengers target niches such as drug-eluting chitosan or pressure-sensing tampons, adding diversity to the nasal packing devices market.

Strategic thrusts center on demonstrating lower total-episode cost rather than unit price, in harmony with value-based procurement. Partnership with digital-health firms enables connected packaging capable of monitoring nasal pressure, an emerging differentiation lever despite current nascent adoption. Intellectual-property fortifications around polymer chemistry and eluted drugs raise entry barriers, while EU MDR documentation hurdles strain smaller venders.

Supply-chain resilience and sustainable sourcing have become competitive variables after raw-material shocks underscored vulnerability. Players able to dual-source chitosan or pivot to synthetic analogs secure hospital confidence. Those strengths, coupled with real-world economic data, shape purchasing decisions across the nasal packing devices market.

Nasal Packing Devices Industry Leaders

Medtronic plc

Stryker Corporation

Smith+Nephew plc

Summit Medical (Innovia)

Teleflex Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Aptar Pharma acquired SipNose’s nasal-delivery technology assets, enhancing its drug-delivery platform.

- April 2024: Integra LifeSciences completed its acquisition of Acclarent, broadening ENT offerings by USD 1 billion.

- April 2024: FDA cleared Spirair’s SeptAlign system for septal deviation repair, potentially altering packing requirements post-procedure.

Global Nasal Packing Devices Market Report Scope

| Non-absorbable Nasal Packs |

| Bio-absorbable/Bio-resorbable Nasal Packs |

| Polyvinyl Alcohol (PVA) |

| Polyurethane |

| Chitosan & Derivatives |

| Carboxymethyl Cellulose (CMC) |

| Gelatin/Collagen & Others |

| Hospitals |

| ENT Specialty Clinics |

| Ambulatory Surgical Centers (ASCs) |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Non-absorbable Nasal Packs | |

| Bio-absorbable/Bio-resorbable Nasal Packs | ||

| By Material | Polyvinyl Alcohol (PVA) | |

| Polyurethane | ||

| Chitosan & Derivatives | ||

| Carboxymethyl Cellulose (CMC) | ||

| Gelatin/Collagen & Others | ||

| By End User | Hospitals | |

| ENT Specialty Clinics | ||

| Ambulatory Surgical Centers (ASCs) | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What revenue growth is expected for nasal packing devices by 2030?

Sales are projected to increase from USD 210.4 million in 2025 to USD 285.1 million by 2030, reflecting a 6.5% CAGR.

Which segment shows the fastest expansion?

Bio-absorbable products are forecast for an 8.9% CAGR through 2030 as hospitals and ASCs pursue patient-friendly solutions.

Why is Asia Pacific the quickest-growing region?

Rising surgical volumes, expanding healthcare infrastructure, and wider access to chronic sinusitis treatment lift regional demand at an 8.3% CAGR.

How are value-based contracts influencing purchasing?

Hospitals weigh total episode cost, so packs that avoid removal visits and reduce rebleeds have procurement advantage.

What material advances underpin new product launches?

Chitosan derivatives offer combined hemostatic and antimicrobial benefits, while hybrid PVA-chitosan constructs add structural support.

How is regulation affecting suppliers?

EU MDR documentation and U.S. supply-chain resilience requirements favor manufacturers with robust quality systems and diversified sourcing.

Page last updated on: