Sinus Dilation Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

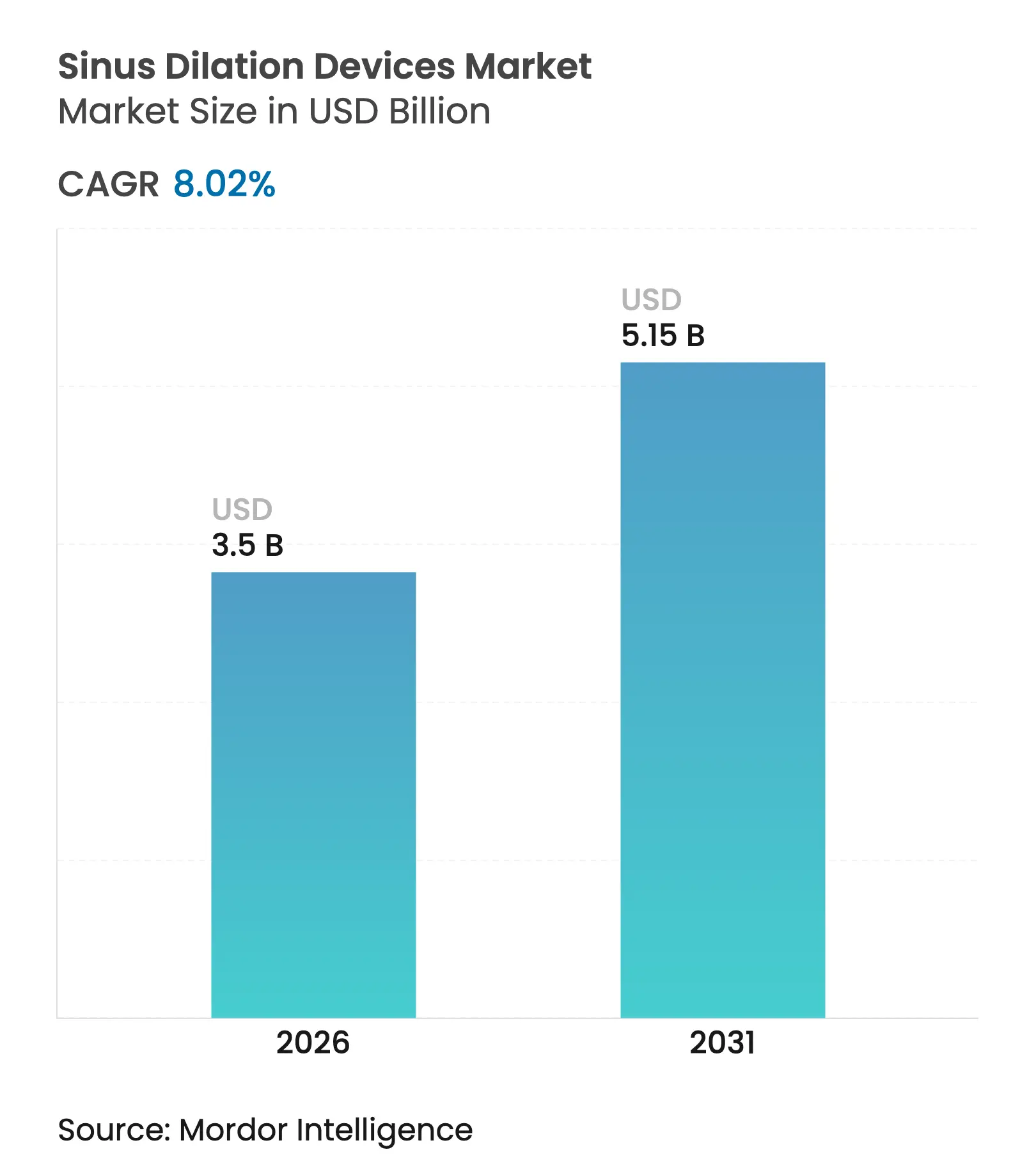

| Market Size (2026) | USD 3.5 Billion |

| Market Size (2031) | USD 5.15 Billion |

| Growth Rate (2026 - 2031) | 8.02 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Sinus Dilation Devices Market Analysis by Mordor Intelligence

The sinus dilation devices market size was valued at USD 3.24 billion in 2025 and estimated to grow from USD 3.5 billion in 2026 to reach USD 5.15 billion by 2031, at a CAGR of 8.02% during the forecast period (2026-2031). The shift from traditional functional endoscopic sinus surgery to balloon-based techniques is anchored in rising chronic rhinosinusitis prevalence, rapid device innovation, and an accelerating move toward office-based care that lowers overall treatment costs. Demand receives further support from drug-eluting implants that keep sinuses patent, AI-guided navigation systems that raise first-pass success, and payer policies that reimburse minimally invasive approaches across major markets. Hospitals still perform most procedures, yet ENT specialty clinics are gaining ground as focused care delivery models show better patient flow and shorter wait times. Regionally, North America holds leadership through well-defined reimbursement codes, while Asia Pacific shows the steepest adoption curve as infrastructure rises and an aging population drives need.

Key Report Takeaways

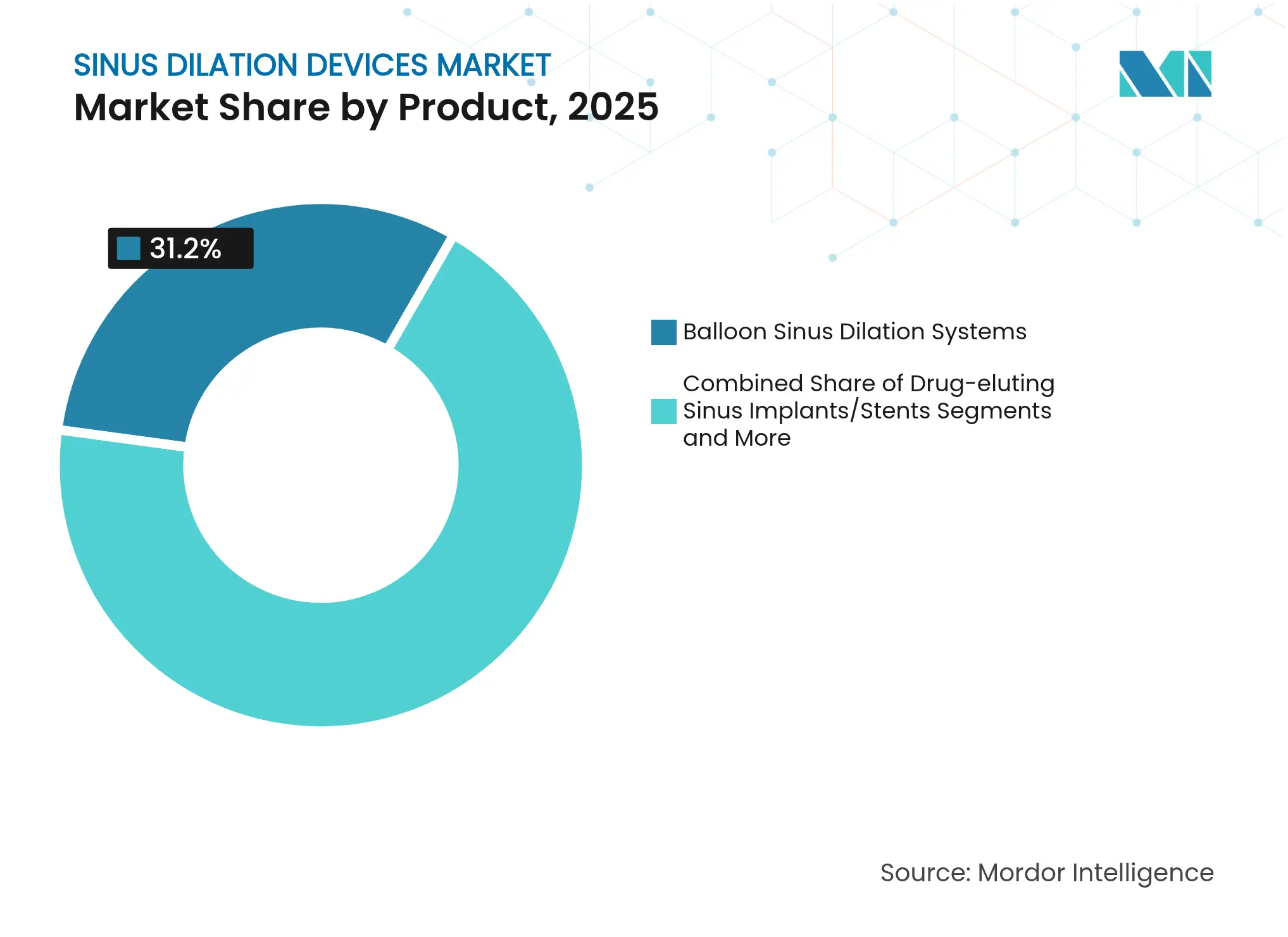

- By product category, balloon sinus dilation systems secured 31.20% of the sinus dilation devices market share in 2025, while navigation software and AI solutions are projected to expand at an 11.23% CAGR to 2031.

- By procedure, stand-alone sinus dilation devices captured 31.60% of the sinus dilation devices market share in 2025; office-based procedures are poised to register the highest growth at a 10.72% CAGR through 2031.

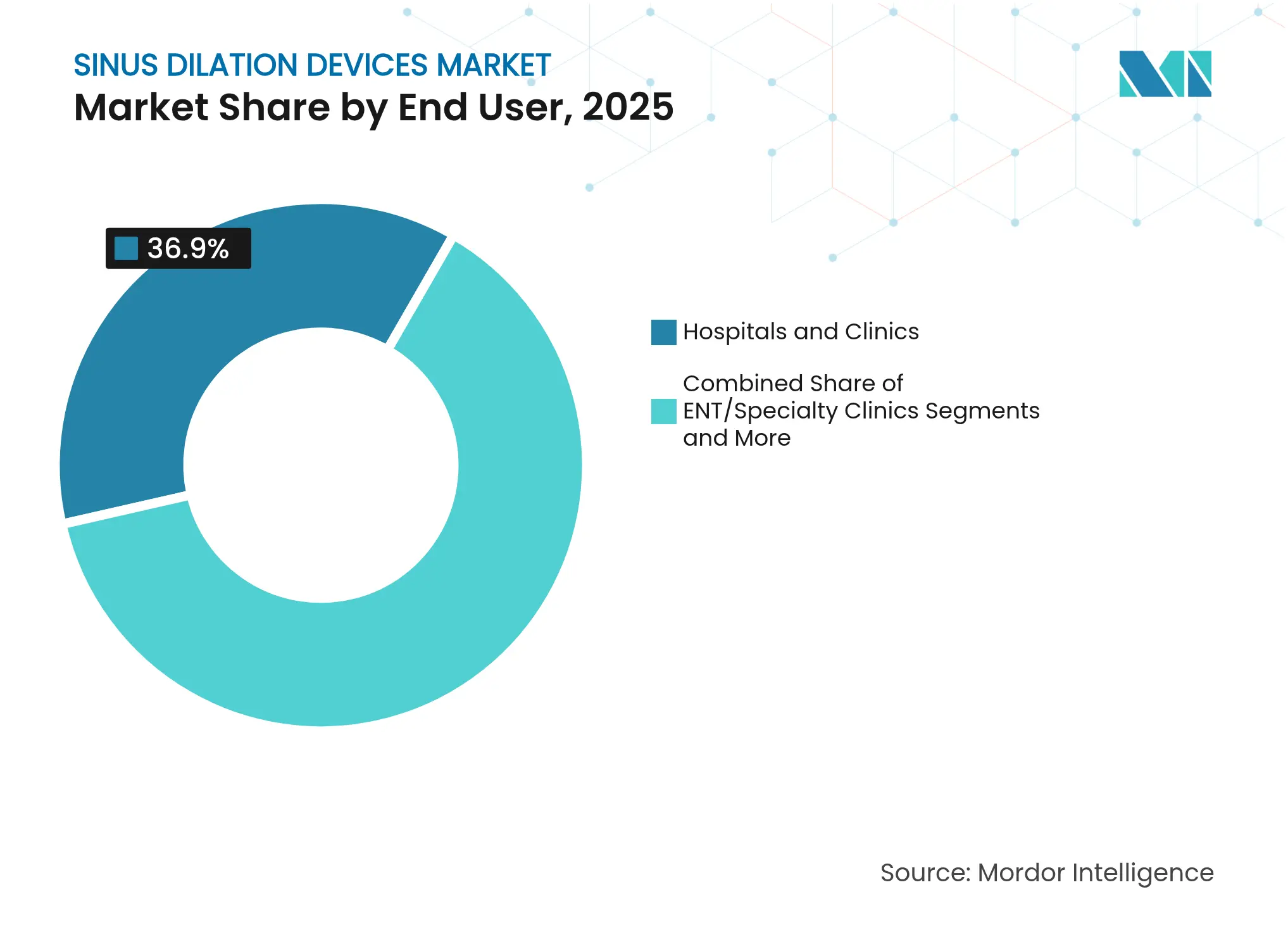

- By end-user, hospitals and clinics commanded 36.90% of the sinus dilation devices market size in 2025, whereas ENT specialty clinics are forecast to grow at an 8.65% CAGR between 2026 and 2031.

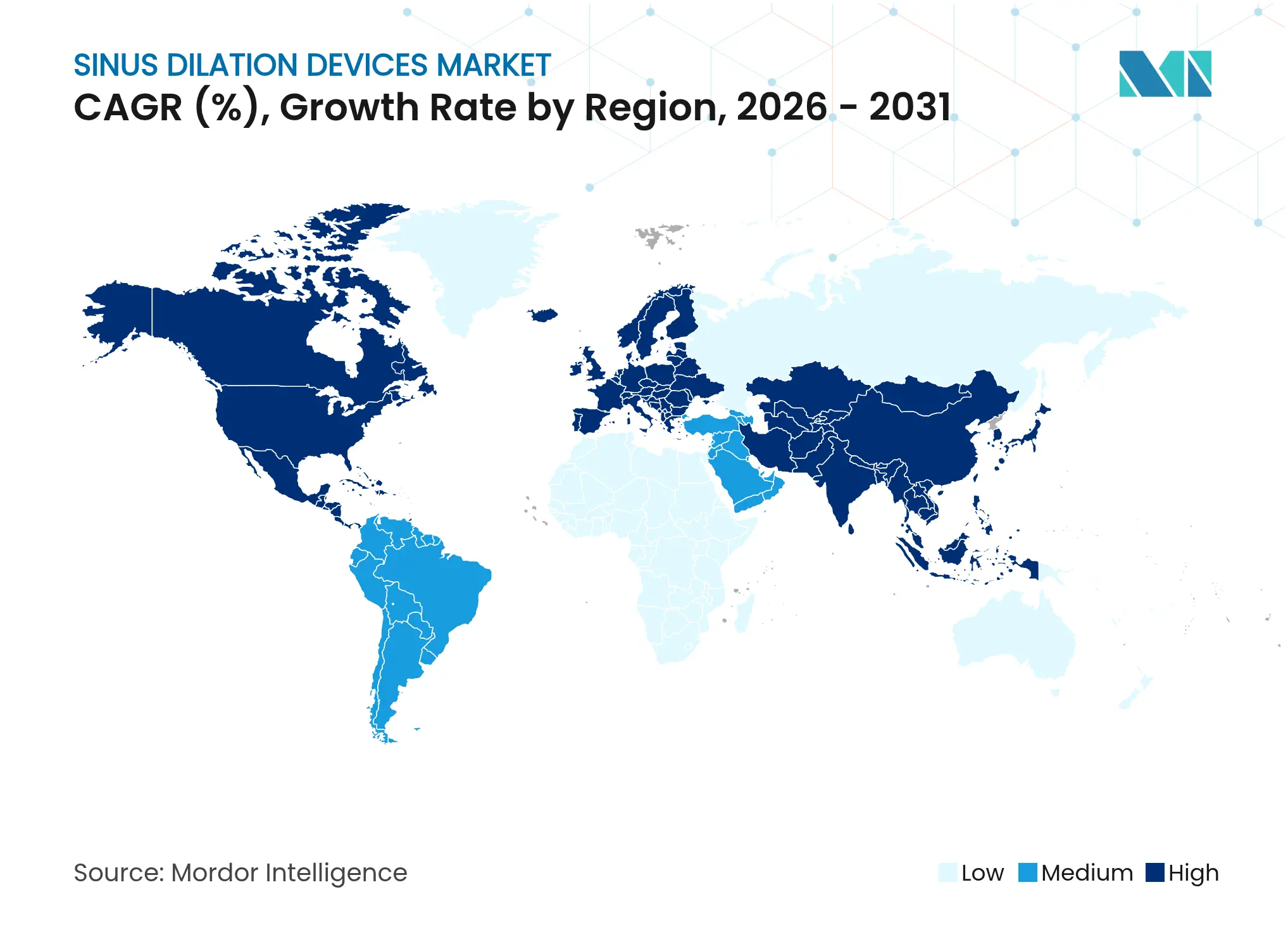

- By geography, North America accounted for 30.00% of the sinus dilation devices market size in 2025, while Asia Pacific is expected to be the fastest-growing region with a 9.43% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sinus Dilation Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of chronic rhinosinusitis Rising prevalence of chronic rhinosinusitis | +1.80% | Global; stronger in North America and Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.80% | Geographic Relevance:Global; stronger in North America and Europe | Impact Timeline:Long term (≥ 4 years) |

Growing preference for minimally invasive sinus dilation devices Growing preference for minimally invasive sinus dilation devices | +2.10% | Global; led by developed markets | Medium term (2-4 years) | |||

Technological advances in drug-eluting stents and image-guided systems Technological advances in drug-eluting stents and image-guided systems | +1.50% | North America and EU core; expanding to Asia Pacific | Medium term (2-4 years) | |||

Favorable reimbursement policies in the US and EU Favorable reimbursement policies in the US and EU | +1.20% | North America and Europe | Short term (≤ 2 years) | |||

Shift toward office-based ENT procedures that lower total cost Shift toward office-based ENT procedures that lower total cost | +0.90% | North America; gaining in developed Asia Pacific markets | Short term (≤ 2 years) | |||

AI-enabled endoscopic visualization that improves first-pass success AI-enabled endoscopic visualization that improves first-pass success | +0.80% | North America and EU; early uptake in Japan | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of Chronic Rhinosinusitis

Chronic rhinosinusitis affects 12% of adults worldwide, expanding the candidate pool for sinus dilation device procedures. Environmental factors such as pollution and urban living intensify mucosal inflammation and shorten the time to surgical intervention when medication fails. Clinical guidance now positions balloon dilation earlier in the treatment pathway, increasing overall procedure volume. Aging populations in developed regions add to the burden, correlating with higher per-capita treatment rates. The resulting uptick in surgical demand boosts device sales and encourages new product launches that target durability and ease of use.

Growing Preference for Minimally Invasive Sinus dilation devices

Patients favor procedures that limit tissue trauma and shorten recovery, prompting a steady migration from conventional sinus surgery to balloon-based dilation. Clinical studies note lower complication rates and a return-to-work window measured in days rather than weeks. Office-based feasibility eliminates general anesthesia and reduces facility fees, easing both payer costs and patient copays. Coverage uniformity across major private insurers lowers financial uncertainty for providers. These dynamics combine to accelerate uptake across hospitals, ambulatory surgery centers, and physician offices.

Technological Advances: Drug-Eluting Stents and Image-Guided Systems

Drug-eluting sinus implants sustain localized steroid delivery for up to 90 days, maintaining ostial patency and cutting revision rates.[1]Wiley Authors, “Drug-Eluting Sinus Implant Reduces Revision Surgery,” wiley.com AI-driven navigation platforms overlay intraoperative imagery onto patient anatomy, raising accuracy and shortening learning curves for newer surgeons.[2]MDPI Editors, “AI Navigation Boosts Diagnostic Accuracy in Rhinology,” mdpi.com The merger of real-time imaging and balloon dilation allows precise deployment while preserving the mucosa. Demand for these integrated systems bolsters premium pricing and skews purchasing decisions toward vendors with robust R&D pipelines.

Favorable Reimbursement Policies in the US and EU

Medicare retains status-quo payment for balloon dilation under the 2025 Physician Fee Schedule, assuring providers' financial viability.[3]Centers for Medicare & Medicaid Services, “Physician Fee Schedule 2025,” cms.gov Clear CPT codes streamline billing, reduce claim denial rates, and encourage more physicians to add the service line. European payers conduct cost-effectiveness reviews that place balloon procedures ahead of conventional surgery on total cost and quality-adjusted life-year metrics, solidifying access within national health systems. Stable reimbursement frameworks lower adoption barriers and support continuous volume growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Peri-operative risks and post-operative complications Peri-operative risks and post-operative complications | -0.70% | Global; higher in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.70% | Geographic Relevance:Global; higher in emerging markets | Impact Timeline:Short term (≤ 2 years) |

Shortage of skilled otolaryngologists in emerging nations Shortage of skilled otolaryngologists in emerging nations | -1.10% | Asia Pacific emerging markets, Middle East and Africa, Latin America | Long term (≥ 4 years) | |||

Average selling price compression from low-cost Asian OEM devices Average selling price compression from low-cost Asian OEM devices | -0.90% | Global; pronounced in price-sensitive markets | Medium term (2-4 years) | |||

EU-MDR uncertainty for biodegradable sinus implants EU-MDR uncertainty for biodegradable sinus implants | -0.60% | Europe; spillover to other regulated markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Peri-Operative Risks and Post-Operative Complications

Although generally safe, balloon dilation can cause orbital injury, cerebrospinal fluid leak, or bleeding when performed without adequate visualization. MAUDE reports cite stent migration and mucosal irritation linked to corticosteroid-eluting implants. Variability in surgeon skill magnifies these risks, especially in settings with limited training resources. Safety concerns may delay adoption in health systems that demand robust outcome data before switching to new techniques. Structured training and clear patient selection criteria remain essential to mitigate complications.

Shortage of Skilled Otolaryngologists in Emerging Nations

Many emerging economies face a low otolaryngologist-to-population ratio that restricts procedure availability. Training programs require time and investment, while brain drain sends specialists to higher-income regions. Limited access slows sinus dilation devices market penetration despite high disease prevalence. Partnerships that combine remote mentoring, simulation centers, and short-course certification aim to close the gap but will take years to mature.

Segment Analysis

By Product: Navigation Systems Drive Innovation

Balloon sinus dilation systems continue to hold 31.20% of the sinus dilation devices market in 2025, reflecting their role as the procedural cornerstone. Navigation software, AI consoles, and real-time imaging hardware, however, are forecast to record an 11.23% CAGR and are pulling the overall sinus dilation devices market toward data-rich, precision-guided workflows. Drug-eluting implants that deliver mometasone furoate for three months reduce revision surgery and open new revenue channels with premium margins. Hand-held dilation tools remain important in cost-constrained settings, ensuring that lower-income markets can still access the therapy.

Accessories and consumables generate predictable revenue for manufacturers. Single-use balloons, guidewires, and irrigation kits form the bulk of procedural spend. Hybrid devices that blend balloon dilation with drug release occupy a growing niche, allowing providers to justify higher per-case reimbursement. The strong link between consumable pull-through and capital unit placement encourages suppliers to create leasing and service models that lower upfront costs and secure long-term account loyalty. The sinus dilation devices market size contribution from high-margin navigation platforms is expected to widen as hospitals refresh fleets to meet digital surgery initiatives.

Note: Segment shares of all individual segments available upon report purchase

By Procedure: Office-Based Growth Accelerates

Stand-alone balloon dilation accounted for 31.60% of the sinus dilation devices market in 2025, yet office-based cases are projected to rise at a 10.72% CAGR due to economic benefits and patient convenience. In-office deployment slashes facility fees and enables same-day discharge, which resonates with payers aiming to control episodic costs. Comparative studies show non-inferior outcomes to operating-room procedures, supporting insurer confidence. The sinus dilation devices market size captured by office settings is therefore expected to expand steadily through 2031.

Hybrid balloon plus FESS techniques remain important for complex anatomies that require both dilation and tissue removal. These combined approaches broaden indications beyond simple ostial blockage, allowing surgeons to tailor interventions per patient. The procedural mix fuels demand for modular instrument sets that can pivot between dilation and resection without costly re-sterilization cycles. Educational workshops and cadaver labs sponsored by device firms aim to shorten learning curves and encourage hybrid adoption.

By End-User: Specialty Clinics Gain Momentum

Hospitals and multispecialty clinics retained 36.90% of the sinus dilation devices market share in 2025, but ENT-dedicated clinics are forecast to outpace them at an 8.65% CAGR. Specialty centers centralize expertise and sustain higher procedural volumes that translate into greater proficiency and patient satisfaction. These facilities often bundle diagnostic imaging and surgery in one visit, improving throughput. The sinus dilation devices market benefits as streamlined workflows permit more cases per day without compromising outcomes.

Ambulatory surgery centers and physician offices leverage lower overhead to offer competitive pricing. Capital-light platforms—such as cart-based navigation coupled with disposable balloons, fit compact spaces and appeal to independent practitioners. Pay-for-performance reimbursement structures further reward practices that demonstrate reduced infection rates and shorter recovery times. As ENT clinics build brand equity around minimally invasive care, referrals shift away from general hospitals, cementing the long-term growth path for this end-user segment.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America accounted for USD 0.97 billion of the sinus dilation devices market size in 2025 and maintained 30.00% share thanks to CPT-coded reimbursement, mature surgeon training programs, and widespread adoption of AI-enhanced navigation. Canada’s single-payer system supports consistent access, while Mexico’s private hospitals drive cross-border procedure volumes.

Europe follows with a diversified payer landscape; Germany, the United Kingdom, France, Italy, and Spain lead uptake under national health insurance frameworks that recognize the cost-benefit of minimally invasive sinus care. EU-MDR compliance, however, introduces timelines that may slow the rollout of biodegradable implants, affecting near-term growth.

Asia Pacific posts the fastest trajectory at 9.43% CAGR. China’s regulatory reforms streamline device approvals, and provincial reimbursement pilots improve affordability. Japan’s aging population and preference for technology drive premium platform sales, whereas India focuses on cost-effective dilation kits paired with training programs that expand specialist coverage. Combined, these factors are set to lift regional revenue past Europe by 2030, reinforcing Asia Pacific as the primary incremental contributor to global sinus dilation devices market expansion.

Competitive Landscape

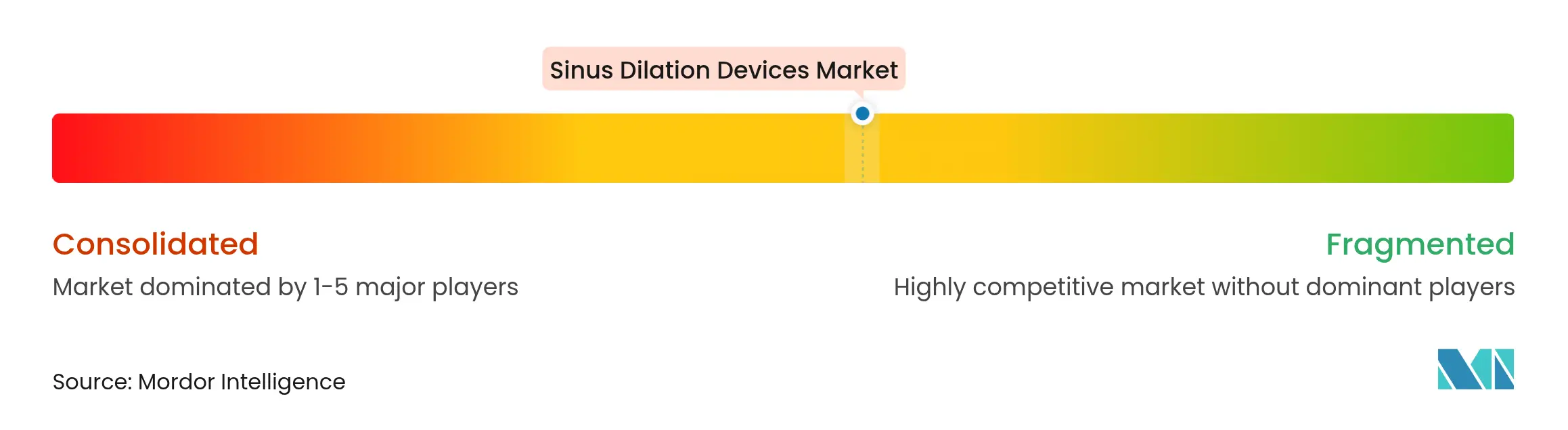

Market Concentration

The sinus dilation devices market shows moderate consolidation. In 2024, Integra LifeSciences acquired Acclarent from Johnson & Johnson for USD 280 million, adding an estimated USD 1 billion to its addressable ENT portfolio. Medtronic strengthened its drug-eluting offerings through the purchase of Intersect ENT, while Stryker refined its XprESS system to improve seeker-based control during dilation.

Mid-tier players such as Smith & Nephew, SinuSys, and Meril Life Sciences pursue differentiated niches that include pediatric-sized balloons and cost-optimized kits for emerging markets. AI navigation remains a white-space opportunity; companies that pair software algorithms with proprietary hardware expect premium valuation multiples. Price competition from domestic Asian OEMs challenges multinationals, prompting a pivot toward service contracts, data analytics packages, and surgeon education programs designed to lock in customer loyalty.

White-label manufacturing partnerships enable regional newcomers to compete quickly, yet regulatory know-how and brand recognition still favor incumbents in markets with strict oversight. Strategic alliances that combine navigation software, drug delivery, and disposable instrumentation are emerging as the next layer of competitive differentiation.

Sinus Dilation Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex agreed to acquire BIOTRONIK’s Vascular Intervention business for EUR 760 million, underscoring consolidation across interventional device segments.

- April 2024: Integra LifeSciences completed the USD 280 million takeover of Acclarent, expanding its sinus surgery portfolio.

- March 2024: FDA approved XHANCE fluticasone propionate nasal spray, the first drug specifically indicated for chronic rhinosinusitis.

- September 2024: Stryker launched an upgraded MiniFESS portfolio that increases balloon flexibility and reduces procedure time.

Table of Contents for Sinus Dilation Devices Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Chronic Rhinosinusitis

- 4.2.2Growing Preference For Minimally?Invasive Balloon Sinuplasty

- 4.2.3Technological Advances: Drug-Eluting Stents & Image-Guided Systems

- 4.2.4Favorable Reimbursement Policies In The US & EU

- 4.2.5Shift Toward Office-Based ENT Procedures Lowers Total Treatment Cost

- 4.2.6AI-Enabled Endoscopic Visualization Improving First-Pass Success

- 4.3Market Restraints

- 4.3.1Peri-Operative Risks & Post-Operative Complications

- 4.3.2Shortage Of Skilled Otolaryngologists In Emerging Nations

- 4.3.3ASP Compression From Influx Of Low-Cost Asian OEM Devices

- 4.3.4EU-MDR Uncertainty For Biodegradable Sinus Implants

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product

- 5.1.1Balloon Sinus Dilation Systems

- 5.1.2Drug-eluting Sinus Implants/Stents

- 5.1.3Hand-held Dilatation Instruments

- 5.1.4Endoscopes & Navigation Systems

- 5.1.5Accessories & Consumables

- 5.1.6Other Products

- 5.2By Procedure

- 5.2.1Standalone Balloon Sinuplasty

- 5.2.2Hybrid Balloon + FESS Procedures

- 5.3By End-User

- 5.3.1Hospitals

- 5.3.2ENT / Specialty Clinics

- 5.3.3Ambulatory Surgical Centers

- 5.3.4Office-based Physician Practices

- 5.4Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products, and Recent Developments)

- 6.3.1Medtronic Plc

- 6.3.2Johnson & Johnson (Acclarent)

- 6.3.3Stryker Corporation (Entellus)

- 6.3.4Smith & Nephew plc

- 6.3.5Olympus Corporation

- 6.3.6Intersect ENT Inc.

- 6.3.7SinuSys Corporation

- 6.3.8Meril Life Sciences Pvt. Ltd.

- 6.3.9Intersect ENT Inc.

- 6.3.10Dalent Medical

- 6.3.11InnAccel Technologies

- 6.3.12Accurate Surgical & Scientific Instruments

- 6.3.13KARL STORZ SE & Co. KG

- 6.3.14Summit Medical LLC

- 6.3.15Boston Scientific Corporation

- 6.3.16Olympus Corporation

- 6.3.17OptiNose Inc.

- 6.3.18Bentley Innomed GmbH

- 6.3.19Jilin Coronado Medical Equipment Co.

- 6.3.20Chengdu Mechan Electronic Technology

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Product

- Balloon Sinus Dilation Systems

- Drug-eluting Sinus Implants/Stents

- Hand-held Dilatation Instruments

- Endoscopes & Navigation Systems

- Accessories & Consumables

- Other Products

- Balloon Sinus Dilation Systems

- By Procedure

- Standalone Balloon Sinuplasty

- Hybrid Balloon + FESS Procedures

- Standalone Balloon Sinuplasty

- By End-User

- Hospitals

- ENT / Specialty Clinics

- Ambulatory Surgical Centers

- Office-based Physician Practices

- Hospitals

- Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Credibility Anchor - Why Our Sinus Dilation Devices Baseline Stands Firm

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 3.24 B | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 3.63 B | Global Consultancy A | Includes nasal drug implants and counts diagnostic endoscopes, inflating totals | ||

USD 3.15 B | Trade Journal B | Applies uniform ASPs across regions and uses 2024 exchange rates without adjustment | ||

USD 2.86 B | Industry Publisher C | Excludes physician-office procedures and assumes 10% higher device reuse |