Absorbable Nasal Implant Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

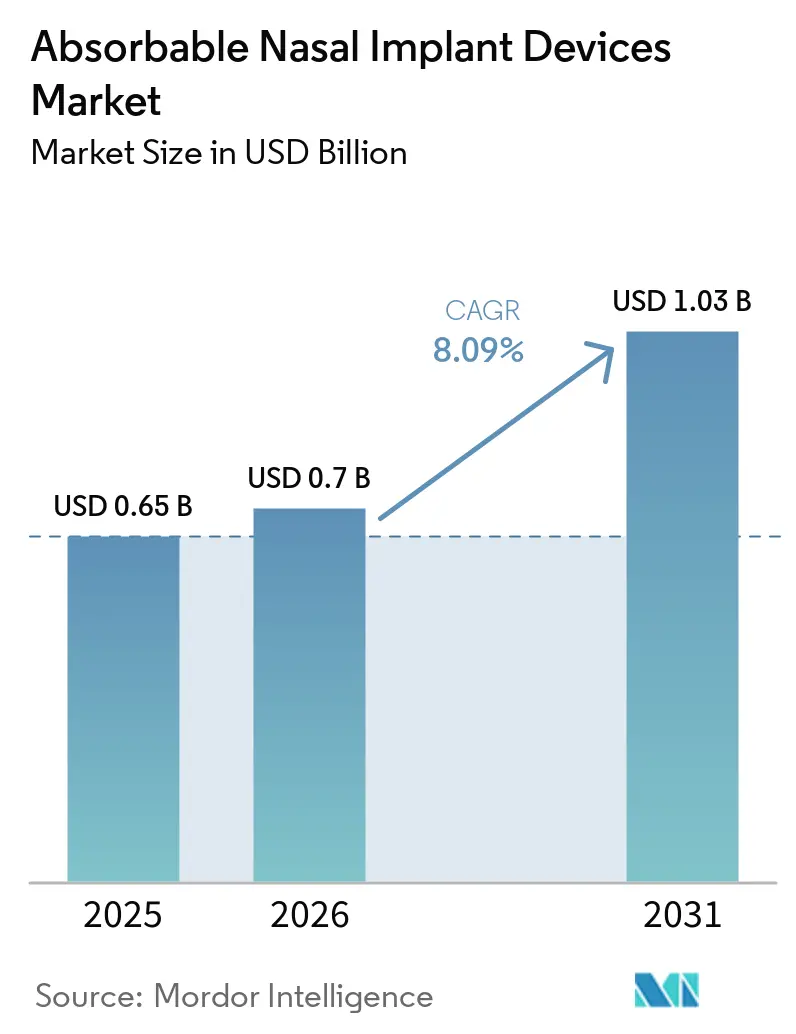

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 1.03 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

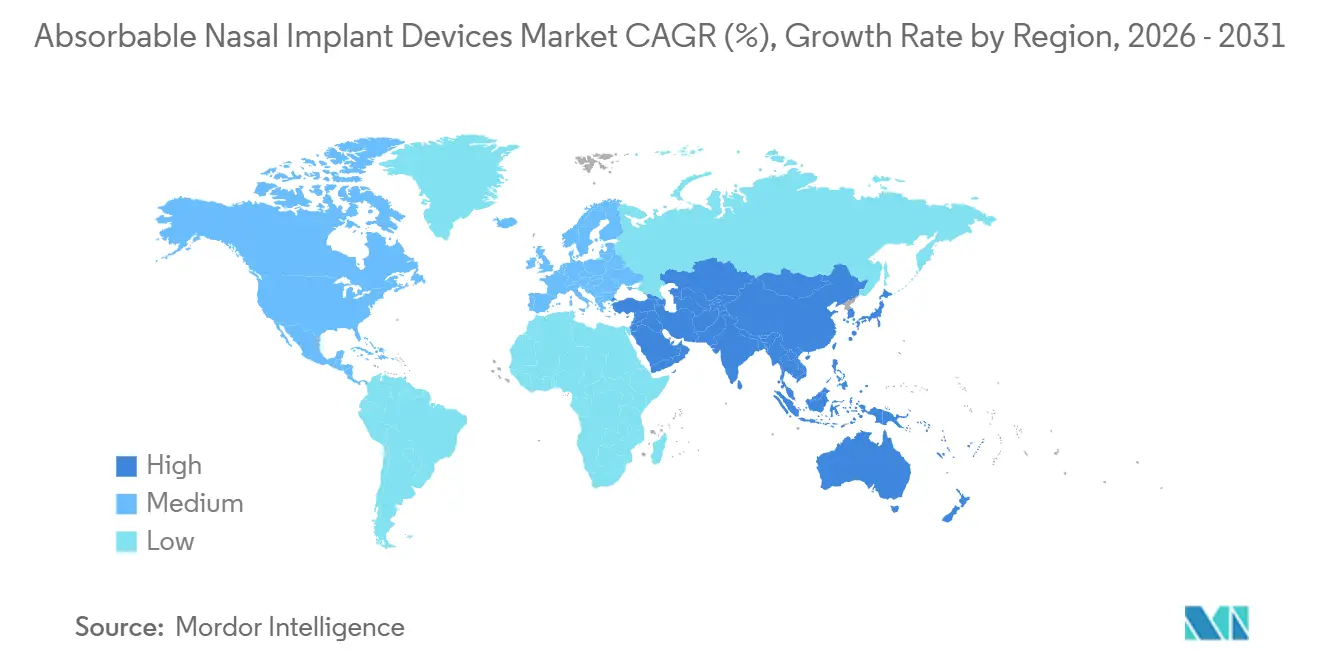

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

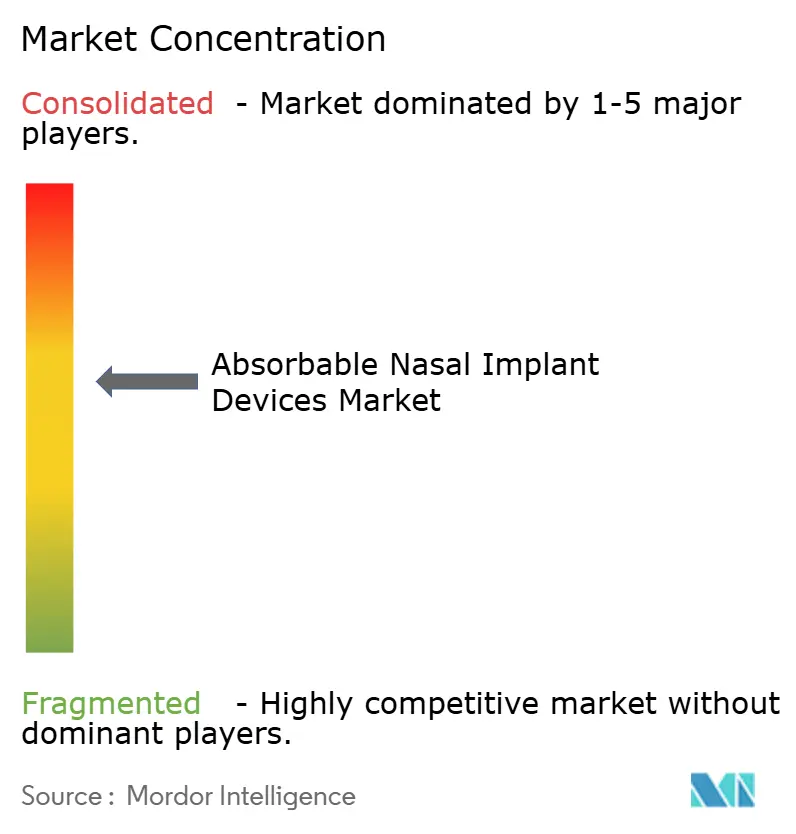

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Absorbable Nasal Implant Devices Market Analysis by Mordor Intelligence

The Absorbable Nasal Implant Devices Market size is projected to expand from USD 0.65 billion in 2025 and USD 0.7 billion in 2026 to USD 1.03 billion by 2031, registering a CAGR of 8.09% between 2026 to 2031.

Clinical validation and coding clarity are lifting barriers to adoption as hospital and outpatient teams standardize postoperative care that integrates drug-eluting implants and absorbable dressings[1]U.S. National Library of Medicine, “PROPEL Mometasone Furoate Implant,” DailyMed, dailymed.nlm.nih.gov. Reimbursement remains mixed in the United States, yet targeted policy updates for select use cases are opening structured coverage pathways that support stable utilization in facility settings. Surgeons favor in-office placement options for recurrent polyps and valve repair because shorter visits and local anesthesia improve patient experience and trim total episode costs. Manufacturers are expanding office-ready portfolios with bioabsorbable implants that do not require removal, which aligns with the shift to ambulatory and clinic workflows. The absorbable nasal implant devices market benefits from real-world evidence that shows fewer postoperative interventions and lower reliance on systemic steroids when steroid-eluting devices are used as part of structured postoperative care.

Key Report Takeaways

- By product type, drug-eluting sinus implants led with 33.60% revenue share in 2025, while absorbable nasal valve support implants are forecast to expand at a 10.86% CAGR through 2031.

- By application, post-functional endoscopic sinus surgery accounted for a 38.92% share of the absorbable nasal implant devices market size in 2025, while nasal valve collapse support is projected to advance at a 11.80% CAGR through 2031.

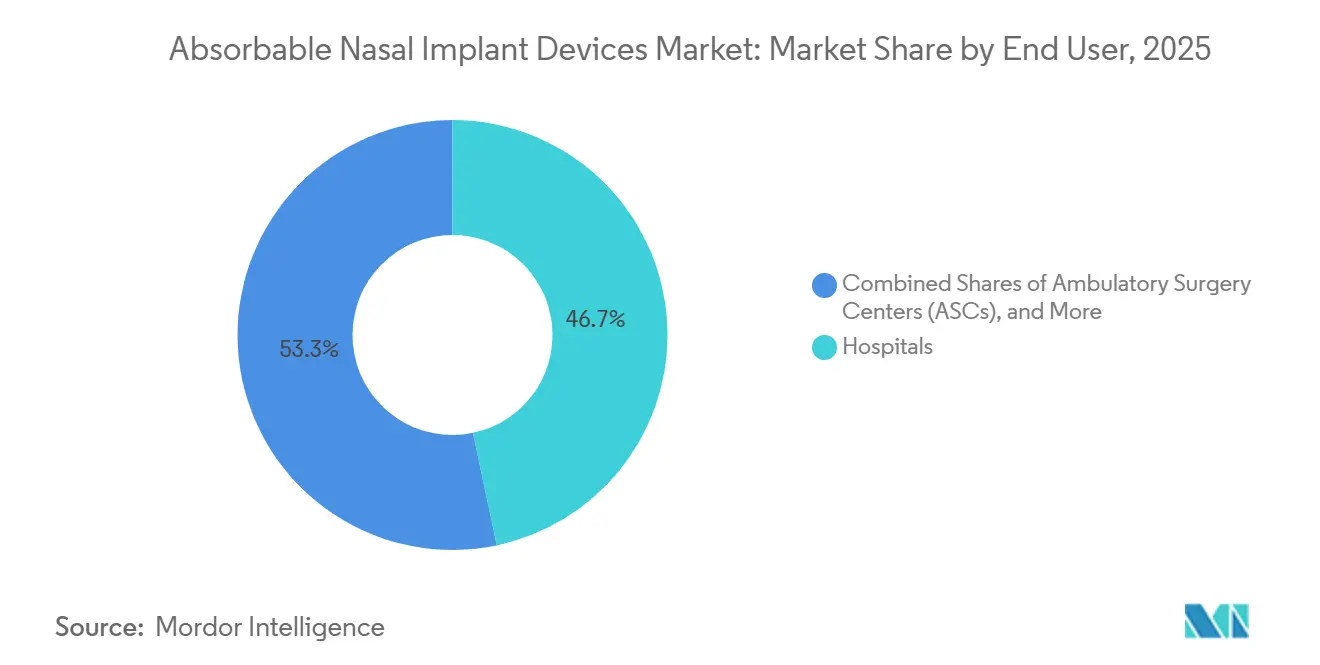

- By end user, hospitals held 46.70% in 2025, while ambulatory surgery centers are projected to grow at a 10.07% CAGR through 2031.

- By geography, North America commanded 41.80% in 2025, while Asia-Pacific is projected to record the fastest growth at a 12.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Absorbable Nasal Implant Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CRD prevalence and surgical volumes sustain demand for in-sinus dressings and implants | +2.4% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Shift to office/ASC rhinology increases adoption of in-office implants and dressings | +2.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Clinical evidence for steroid-eluting and valve-support implants improves outcomes and reduces revisions | +1.8% | Global, led by North America | Medium term (2-4 years) |

| Established coding (CPT 30468) and device approvals enable procedure standardization | +1.6% | United States, with spillover to Canada | Short term (≤ 2 years) |

| Six-month programmable drug-eluting platforms expand addressable pool | +1.3% | Global, pending regulatory clearances in Asia-Pacific and Europe | Long term (≥ 4 years) |

| Supply localization in Asia and India for absorbable dressings lowers cost-to-serve | +0.9% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising CRD Prevalence And Surgical Volumes Sustain Demand For In-Sinus Dressings And Implants

The growing prevalence of chronic rhinosinusitis and stable sinus surgery volumes support consistent device utilization in both hospital and ambulatory settings. Postoperative inflammation control and ostial patency maintenance are central goals of care after endoscopic sinus procedures, which have kept drug-eluting and non-drug absorbable implants in routine consideration for postoperative management. Evidence summaries from U.S. clinical and payer reviews report reductions in postoperative interventions when mometasone-eluting implants are placed, which reinforces a data-driven rationale for surgeon adoption.[2]Cigna Healthcare, “Drug-Eluting Devices for Use Following Endoscopic Sinus Surgery,” Cigna, cigna.com

Specialty societies highlight the role of office-based and ambulatory workflows for select rhinology interventions, which expands the procedural sites where absorbable implants can be used. As the absorbable nasal implant devices market matures, clinicians are combining in-sinus implants with optimized topical steroid regimens to lower revision risk in recurrent polyp cohorts. This steady procedural backdrop helps the absorbable nasal implant devices market sustain predictable demand through the forecast period.

Shift To Office/ASC Rhinology Increases Adoption Of In-Office Implants And Dressings

Ambulatory and office settings are gaining share in rhinology because minimally invasive techniques and local anesthesia can compress care timelines while maintaining patient comfort. SINUVA is indicated for in-office endoscopic placement and delivers mometasone furoate locally over 90 days, which allows clinics to treat recurrent polyps without an operating-room slot or general anesthesia[3]U.S. National Library of Medicine, “SINUVA Mometasone Furoate Sinus Implant,” DailyMed, dailymed.nlm.nih.gov. Coding clarity through CPT 30468 for nasal valve repair defines a billable pathway for submucosal lateral wall implants, which reduces uncertainty for clinic-based valve support procedures. Payer updates that define medical-necessity criteria for sinus surgery and related implants give facilities a clearer view of documentation and coverage expectations for device-enabled care plans.

New office-optimized implants, such as bioabsorbable devices designed for simple one-pass placement and no removal, improve workflow predictability and reduce follow-up burden for busy ENT practices. The Absorbable nasal implant devices market is therefore positioned to benefit from the migration of appropriate cases to outpatient and clinic settings where device-enabled protocols have clear time and cost advantages.

Clinical Evidence For Steroid-Eluting And Valve-Support Implants Improves Outcomes And Reduces Revisions

Coverage assessments conducted in 2026 summarize randomized and real-world evidence showing that steroid-eluting sinus implants reduce the need for postoperative and surgical interventions and lower systemic steroid use compared to non-drug controls. For recurrent polyposis, data cited in payer policies report that patients treated with in-office mometasone-eluting implants avoided repeat endoscopic surgery more often than control cohorts in sham or standard-care groups. For nasal valve support, peer-reviewed evidence indicates that bioabsorbable lateral-wall implants can improve Nasal Obstruction Symptom Evaluation scores and endoscopic measures of lateral wall motion compared to baseline, with benefits extending up to one year in several studies.

Mild adverse events such as localized discomfort and transient foreign-body sensation are commonly reported, while extrusion risk around 4% in larger cohorts underscores the need for operator training and careful patient selection. Specialty society statements referenced in payer reviews describe drug-eluting implants as devices that reduce inflammation, maintain patency, and decrease scarring, which aligns with clinical endpoints valued by surgeons and patients. These findings lift clinician confidence and support broader use as part of standardized postoperative care plans in the absorbable nasal implant devices market.

Established Coding (E.G., CPT 30468) And Device Approvals Enable Procedure Standardization

A distinct CPT code 30468 for nasal valve collapse repair using submucosal lateral wall implants reduces reliance on unlisted codes and improves claims predictability for office-based valve support. CMS releases for the CY 2026 HOPPS and ASC rule clarify device-intensive designations for relevant endoscopic sinus procedures, which helps hospitals and ASCs plan for implant costs inside outpatient payment bundles. CMS transmittals further anchor billing and documentation pathways that clinical and revenue cycle teams use to standardize device-enabled sinus procedures. Payer decisions that recognize new rhinology procedures, including targeted ablation for chronic rhinitis, help clinics build complementary care pathways where absorbable dressings can be used to manage postoperative mucosal irritation and bleeding.

Next-generation absorbable implants secure regulatory clearances that emphasize simple placement and no removal, which aligns with clinic workflow and helps standardize postoperative protocols across heterogeneous care settings. As codes, coverage criteria, and clearances converge, device selection and postoperative pathways become more uniform, which supports scalable adoption across the absorbable nasal implant devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Payer policies labeling nasal valve implants and drug-eluting stents investigational limit coverage | -1.7% | United States, concentrated in commercial insurance | Medium term (2-4 years) |

| Adverse events, foreign-body reactions, and extrusion risks necessitate careful selection | -0.9% | Global | Short term (≤ 2 years) |

| Biologics for CRSwNP shift some candidates away from implant-based therapy | -1.4% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Office and ASC reimbursement variability and lack of device-intensive status pressure margins | -1.1% | United States and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Payer Policies Labeling Nasal Valve Implants/Drug Eluting Stents Investigational Limit Coverage

Commercial payer policies in 2026 classify drug-eluting sinus implants as investigational, citing small sample sizes, limited follow-up, and a lack of direct comparisons against standard topical steroid therapy, which restricts coverage in key U.S. plans. The same dynamic affects absorbable lateral nasal implants for valve collapse, where several plans categorize the technology as investigational even as clinical studies show symptomatic benefit, which complicates patient access and suppresses utilization growth[4]Blue Cross Blue Shield of Massachusetts, “Absorbable Nasal Implant for Treatment of Nasal Valve Collapse,” Blue Cross MA, bluecrossma.org. Investigational labeling drives benefit exclusions in many employer-sponsored plans and shifts costs to patients, which in turn dampens the economics for clinics contemplating broader adoption outside surgical bundles. Other plans maintain investigational status for both absorbable nasal implants and radiofrequency procedures targeted at the nasal valve, emphasizing limitations such as loss to follow-up and lack of head-to-head comparisons with other structural surgeries.

The policy environment remains fluid, which requires device manufacturers to invest in outcomes research and payer education that addresses evidence gaps in a way that aligns with each plan’s coverage criteria. This variability slows near-term growth in the absorbable nasal implant devices market despite surgeon interest and supportive real-world experiences.

Adverse Events/Foreign-Body Reactions And Extrusion Risks Necessitate Careful Selection

Device event summaries in payer reviews list complications such as foreign-body sensation, swelling, localized infections, and implant migration, which generally resolve but may require retrieval or early removal in a minority of cases. Reported implant extrusion rates near 4% in larger cohorts highlight the importance of correct depth and placement angle for valve support devices, especially in regions of thin vestibular skin and high inspiratory forces. Patient selection becomes critical since anatomical variants and prior infections can predispose to mucosal erosion or granulomatous reactions that complicate healing and increase retrieval likelihood.

Product labeling outlines contraindications related to hypersensitivity toward constituent polymers and stresses that foreign-body responses or incomplete debridement can elevate adverse event risk, which guides pre-procedural planning and patient counseling. These safety considerations underscore the need for training, protocolized placement techniques, and post-placement monitoring to keep event rates low and harness expected symptom benefits. Awareness of these risks tempers the adoption curve in the Absorbable nasal implant devices market while reinforcing the value of standardized technique and patient selection checklists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Drug-Eluting Platforms Anchor Share, While Valve-Support Implants Capture Fastest Growth

Drug-eluting sinus implants captured 33.60% of absorbable nasal implant devices market share in 2025 and absorbable nasal valve support implants are projected to grow at a 10.86% CAGR from 2026 through 2031, reflecting strong clinician confidence in local corticosteroid delivery for postoperative inflammation control. Evidence summarized for payer decisions shows that steroid-eluting devices reduce postoperative interventions and systemic steroid use compared to non-drug controls, which reinforces their role as core adjuncts after sinus surgery. The PROPEL family delivers mometasone furoate via a bioabsorbable scaffold and has labeling that details elution profiles designed for early healing phases, which anchors clinical utility in the first month after surgery. In-office mometasone-eluting implants target patients with recurrent nasal polyps after prior surgery, providing a 90-day local steroid source to defer or avoid revision procedures for select candidates.

Nondrug absorbable dressings remain essential for septoplasty, rhinoplasty, and sinus procedures where surgeons select degradation timelines that match healing expectations to reduce discomfort and clinic workload. Bioabsorbable spacers and septal splints meet more specialized needs like perforation repair or donor-site coverage in complex reconstructions, which supports premium pricing per case in niche indications. Supply localization in China and India strengthens global availability of compliant absorbable dressings, which protects against logistics shocks and keeps cost-to-serve attractive for public and private hospitals in price-sensitive markets.

By Application: Post-FESS Dominates, Yet Nasal Valve Collapse Support Surges

Post-functional endoscopic sinus surgery held 38.92% share of the Absorbable nasal implant devices market size in 2025 and is projected to grow by 2031, supported by sustained case volumes and standardized postoperative protocols that integrate absorbable devices for hemostasis, patency, and inflammation control. Clinical evidence summarized in payer policies reports that patients receiving steroid-eluting implants after surgery require fewer postoperative interventions and less systemic steroid exposure than patients managed with non-drug packing, which underpins surgeon confidence in these platforms. Drug delivery for chronic rhinosinusitis with nasal polyps in postoperative and in-office settings remains a critical application because long-term polyp recurrence risk requires ongoing local therapy for symptom control in high-risk cohorts. Epistaxis management relies on absorbable hemostatic dressings that provide tamponade without removal, which is important for elderly and anticoagulated patients, where trauma from nonabsorbable packs can cause complications.

The absorbable nasal implant devices market benefits from consistent demand across these applications because adoption improves patient comfort, reduces clinic workload, and aligns with value-based care goals in ENT departments. Nasal valve collapse support is the fastest-growing application with an 11.80% CAGR forecast because CPT 30468 defines a clear billing pathway for office placement of lateral wall implants that relieve inspiratory collapse in appropriate candidates. Office-based valve support fills a gap for patients who prefer to avoid cartilage grafting and general anesthesia, which accelerates case scheduling and lowers total episode costs for providers and payers. New bioabsorbable devices designed for one-pass insertion and no removal further smooth the recovery experience and simplify aftercare, which is valued by clinics that rely on tight schedules and limited postoperative slots. Clinics also use bioabsorbable implants to stabilize turbinates after sinus surgery, which reinforces the role of absorbable devices as structural adjuncts in both surgical suites and offices.

By End User: Hospitals Lead, ASCs Accelerate

Hospitals accounted for 46.7% in 2025, reflecting the concentration of complex sinus cases, specialist ENT teams, and procurement frameworks that support premium drug-eluting implants in formulary plans. In adult patients with polypoid disease and prior surgery, plan updates have documented scenarios where sinus implants can meet medical-necessity criteria, which supports structured claims submission and facility-based purchasing. Hospitals tend to perform multi-implant placements per case where indicated, which strengthens the economic rationale for carrying a full range of steroid-eluting and contour-specific devices in inventory. The Absorbable nasal implant devices market benefits from hospitals’ ability to collect outcomes and protocolize care, which contributes to internal evidence generation that sustains procurement and surgeon buy-in.

Ambulatory surgery centers are projected to grow at a 10.07% CAGR because ENT aligns well with same-day care pathways and monitored anesthesia care that keep throughput high and recovery brief. ASC economics improve when devices fit seamlessly into bundled payments and carve-out frameworks for device-intensive procedures that can help offset acquisition costs, a trend visible in recent outpatient payment updates. Specialty clinics and ENT group practices carry in-office devices optimized for local anesthesia placement that do not require removal, which matches patient preferences for less invasive options and enables quick scheduling. The absorbable nasal implant devices market therefore expands through channel strategies that balance hospital depth with ASC and clinic speed, while payer documentation and coding completeness remain essential to sustain margins across all sites.

Geography Analysis

North America held 41.80% in 2025 as operating-room and clinic-based protocols normalize device use despite payer variability for select indications. U.S. outpatient payment updates that define device-intensive sinus procedures help facilities plan implant utilization within bundles, which supports continued adoption in hospitals and ASCs. Coding and coverage clarity for defined clinical scenarios, including in-office placement for recurrent polyps after prior surgery, supports claims predictability in targeted use cases for facility-based care teams. Specialty societies and payer policy updates provide guardrails that surgeons and administrators use to shape postoperative plans, which support steady demand in the absorbable nasal implant devices market. As coding, training, and outcomes data converge, clinical leaders in the region continue to integrate steroid-eluting and absorbable structural devices into standardized pathways that prioritize patient comfort and reduced revision risk.

Europe demonstrates solid adoption supported by a mature regulatory environment and a strong base of ENT centers that can standardize protocols at scale. Pan-European launches proceed under harmonized regulations that prioritize safety and post-market surveillance for absorbable Class III devices, which aligns with provider expectations for long-term outcomes tracking. Leading markets such as France, the United Kingdom, Italy, and Spain provide an installed base of experienced rhinologists who are familiar with both drug-eluting and nondrug absorbable options, which supports methodical expansion of device-enabled postoperative care. Collaboration across academic and clinical sites supports investigator-initiated research, surgeon training, and clinical audits that reinforce the role of absorbable implants in symptom control and revision reduction in appropriate cohorts. In this environment, the absorbable nasal implant devices market advances through disciplined procurement and surgeon-led protocols that emphasize consistent outcomes across public and private hospitals.

Asia-Pacific is the fastest-growing region with a projected 12.24% CAGR through 2031 as domestic manufacturing and expanding ENT infrastructure increase availability and affordability. Certified manufacturers in China and India supply absorbable dressings and related products to regional and export markets, which reduces logistics risk and supports public-sector procurement at competitive price points. ENT capacity expansion in tier-2 and tier-3 cities drives demand for absorbable dressings and supports adoption of office-optimized implants in private clinics that serve growing middle-income populations. As disposable income and patient awareness rise, ENT providers integrate absorbable implants into postoperative and in-office protocols that emphasize comfort, fewer follow-up procedures, and local therapy for symptom control. The Absorbable nasal implant devices market therefore benefits from volume growth in Asia-Pacific that complements steady adoption in North America and Europe, balancing premium drug-eluting implants with cost-effective absorbable dressings to match local purchasing power and care models.

Competitive Landscape

The absorbable nasal implant devices market features moderate to high concentration across drug-eluting platforms, absorbable dressings, and office-ready structural implants. Drug-eluting portfolios for postoperative and in-office use anchor the category because consistent reductions in postoperative interventions and systemic steroid use build clinical confidence that persists across care settings. Labeling that details local delivery and elution periods aligns with early healing windows after sinus surgery and supports predictable postoperative protocols for surgeons and care teams. Nondrug absorbable dressings remain essential because their degradation timelines and conformability allow customization to target hemostasis, edema control, and structural support without removal, which improves patient experience. This mix allows companies to serve hospitals, ASCs, and clinics with portfolios that match care pathways and patient preferences across the Absorbable nasal implant devices market.

Market leaders invest in clinical evidence, surgeon education, and post-market surveillance to support premium positioning for drug-eluting devices. Evidence synthesis in 2026 payer policies describes meaningful reductions in surgical and oral-steroid interventions with steroid-eluting implants, which underpins value arguments that resonate with procurement teams and clinicians. Companies operating in absorbable dressings emphasize quality certifications and variant designs that match degradation windows, which bolster their presence in high-volume ENT centers and cost-sensitive markets. The Absorbable nasal implant devices market continues to respond to coding improvements and payer education, which can translate clinical benefits into broader covered use cases over time. Strategic emphasis on training for patient selection and placement depth helps companies protect safety profiles and maintain low adverse event rates at scale.

Absorbable Nasal Implant Devices Industry Leaders

Medtronic

Stryker

Smith+Nephew

Regenity

Hemostasis LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Lyra Therapeutics announced suspension of further development for LYR-210, its lead bioabsorbable nasal implant for chronic rhinosinusitis, despite positive Phase 3 ENLIGHTEN 2 trial results meeting primary endpoints.

- October 2025: Aerin Medical launched its next-generation RhinAer+ Stylus for chronic rhinitis relief, coinciding with expanding payor coverage, including UnitedHealthcare Medicare Advantage approval for RhinAer treatment of the posterior nasal nerve.

Global Absorbable Nasal Implant Devices Market Report Scope

As per the scope of the report, absorbable nasal implant devices are medical implants designed for nasal correction procedures that gradually dissolve and are absorbed by the body over time. They are used to provide structural support or improve nasal shape without the need for permanent implants, reducing the risk of long-term complications.

The absorbable nasal implant devices market is segmented by product type, which includes absorbable nasal dressings, drug-eluting sinus implants, absorbable nasal valve support implants, absorbable sinonasal spacers, and others. Also, the market is segmented into application areas by post-functional endoscopic sinus surgery, epistaxis management, CRS with nasal polyps drug delivery, nasal valve collapse support, septal perforation/donor-site repair, and others. Additionally, in terms of end users, it is segmented into hospitals, ambulatory surgery centers, specialty clinics, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Absorbable Nasal Dressings |

| Drug-eluting Sinus Implants |

| Absorbable Nasal Valve Support Implants |

| Absorbable Sinonasal Spacers |

| Others (Bioabsorbable Sinonasal Repair Grafts, Absorbable Septal Splints etc.) |

| Post-Functional Endoscopic Sinus Surgery |

| Epistaxis Management |

| CRS with Nasal Polyps Drug Delivery |

| Nasal Valve Collapse Support |

| Septal Perforation / Donor-site Repair |

| Others (Post-Traumatic Repair, Iatrogenic Sinonasal Repair) |

| Hospitals |

| Ambulatory Surgery Centers (ASCs) |

| Specialty Clinics |

| Others (Academic Institues, Research Institutes) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Absorbable Nasal Dressings | |

| Drug-eluting Sinus Implants | ||

| Absorbable Nasal Valve Support Implants | ||

| Absorbable Sinonasal Spacers | ||

| Others (Bioabsorbable Sinonasal Repair Grafts, Absorbable Septal Splints etc.) | ||

| By Application | Post-Functional Endoscopic Sinus Surgery | |

| Epistaxis Management | ||

| CRS with Nasal Polyps Drug Delivery | ||

| Nasal Valve Collapse Support | ||

| Septal Perforation / Donor-site Repair | ||

| Others (Post-Traumatic Repair, Iatrogenic Sinonasal Repair) | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers (ASCs) | ||

| Specialty Clinics | ||

| Others (Academic Institues, Research Institutes) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast growth rate for the Absorbable nasal implant devices market through 2031?

The absorbable nasal implant devices market is projected to grow at an 8.09% CAGR from 2026 to 2031, reaching USD 1.03 billion by 2031.

Which product segment leads revenue and which is growing fastest?

Drug-eluting sinus implants led in 2025 with 33.60% share, while absorbable nasal valve support implants are projected to grow fastest at 10.86% CAGR through 2031.

Which region holds the largest share and which region is expected to grow the fastest?

North America led with 41.80% in 2025, and Asia-Pacific is expected to be the fastest-growing region at 12.24% CAGR through 2031.

How are payer coverage decisions shaping adoption in the United States?

Investigational designations for steroid-eluting and nasal valve implants limit coverage in several commercial plans, which slows adoption and keeps documentation requirements high for covered use cases.

What clinical outcomes support the use of steroid-eluting sinus implants?

Evidence synthesized in 2026 payer policies highlights reductions in postoperative and surgical interventions and lower systemic steroid use compared with non-drug controls, which supports their use after sinus surgery.

What factors are driving the shift toward office-based rhinology procedures?

Coding clarity, clinic-friendly implant designs that do not require removal, and patient preference for local anesthesia visits are accelerating in-office placement and supporting growth in clinic settings.

Page last updated on: