Nasal Splints Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

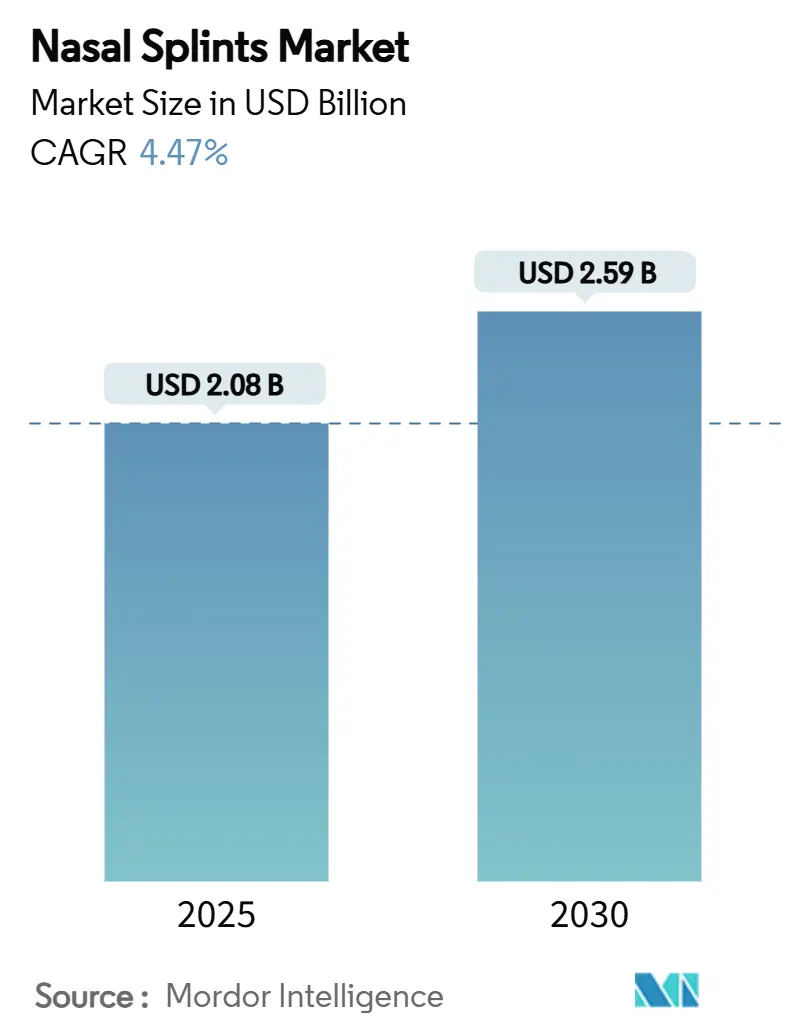

| Market Size (2025) | USD 2.08 Billion |

| Market Size (2030) | USD 2.59 Billion |

| Growth Rate (2025 - 2030) | 4.47% CAGR |

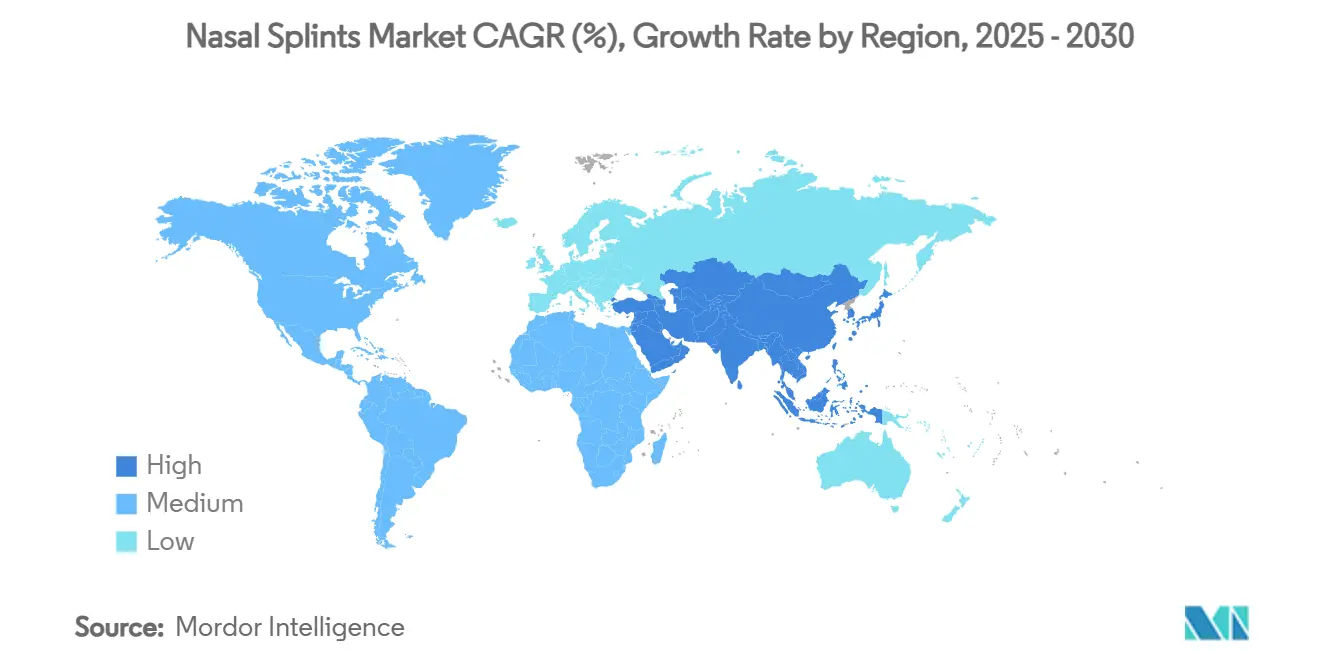

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

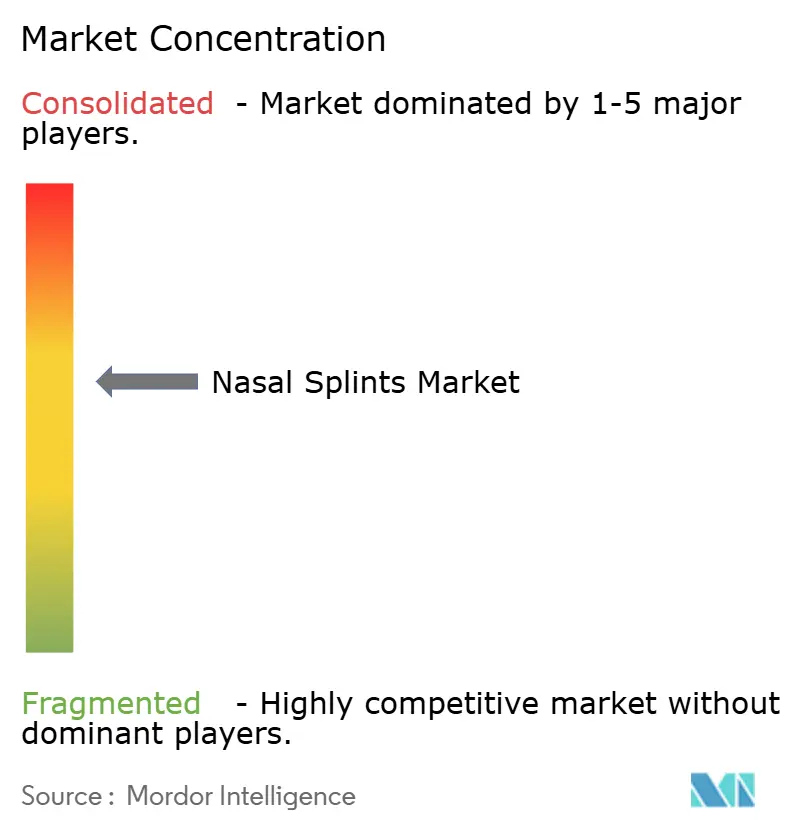

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nasal Splints Market Analysis by Mordor Intelligence

The nasal splints market size stands at USD 2.08 billion in 2025 and is projected to reach USD 2.59 billion by 2030, expanding at a 4.47% CAGR over the forecast period. Rising demand for bioabsorbable devices that dissolve in situ, the popularity of office-based ENT procedures, and cost pressures linked to silicone shortages are reshaping procurement strategies. Bioabsorbable implants such as Stryker’s LATERA system generate average savings of USD 2,200 per case by eliminating operating-room revision time. Endorsements from the American Rhinologic Society have secured payer coverage for these implants, reinforcing adoption momentum. Rapid uptake in Asia-Pacific, where growing surgical volumes intersect with rising healthcare expenditures, underscores the global shift toward minimally invasive interventions. Supply chain volatility—chiefly a 60% jump in silicone prices—continues to accelerate material substitution strategies.

Key Report Takeaways

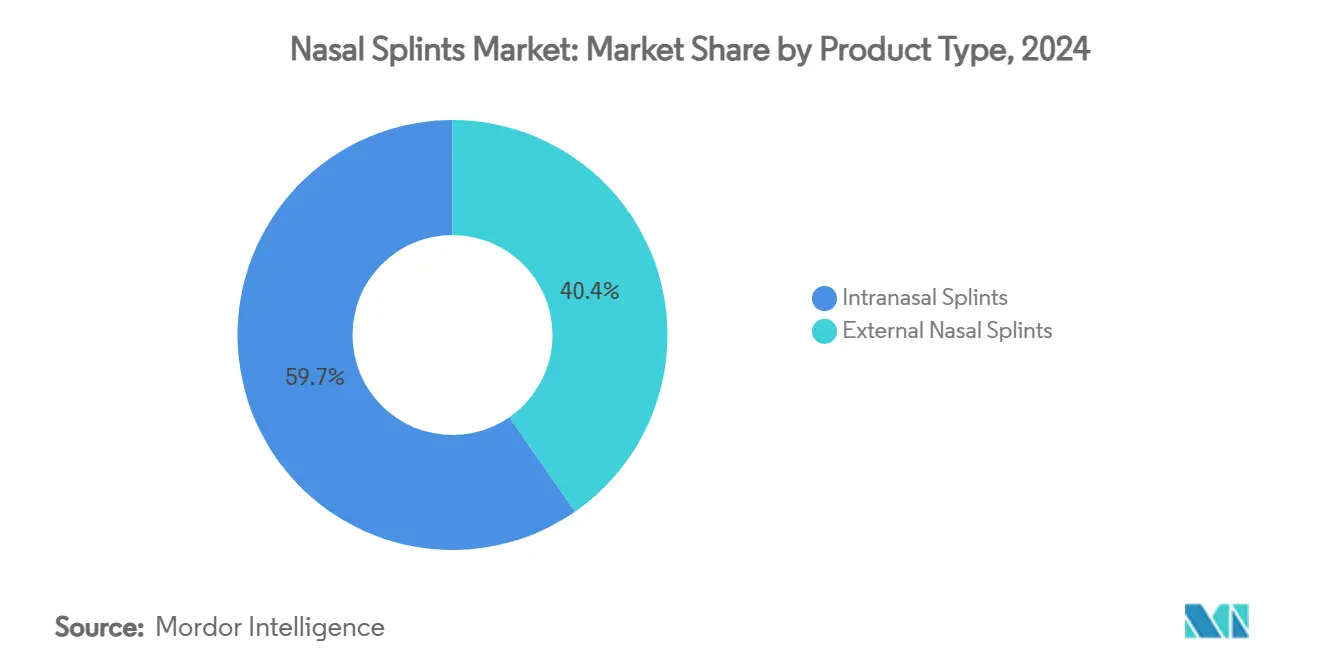

- By product type, intranasal splints captured 59.65% of nasal splints market share in 2024, while external splints are on track to post the fastest 7.67% CAGR through 2030.

- By material, silicone retained 43.72% of nasal splints market share in 2024, but bio-absorbable polymers lead growth with an 8.82% CAGR to 2030.

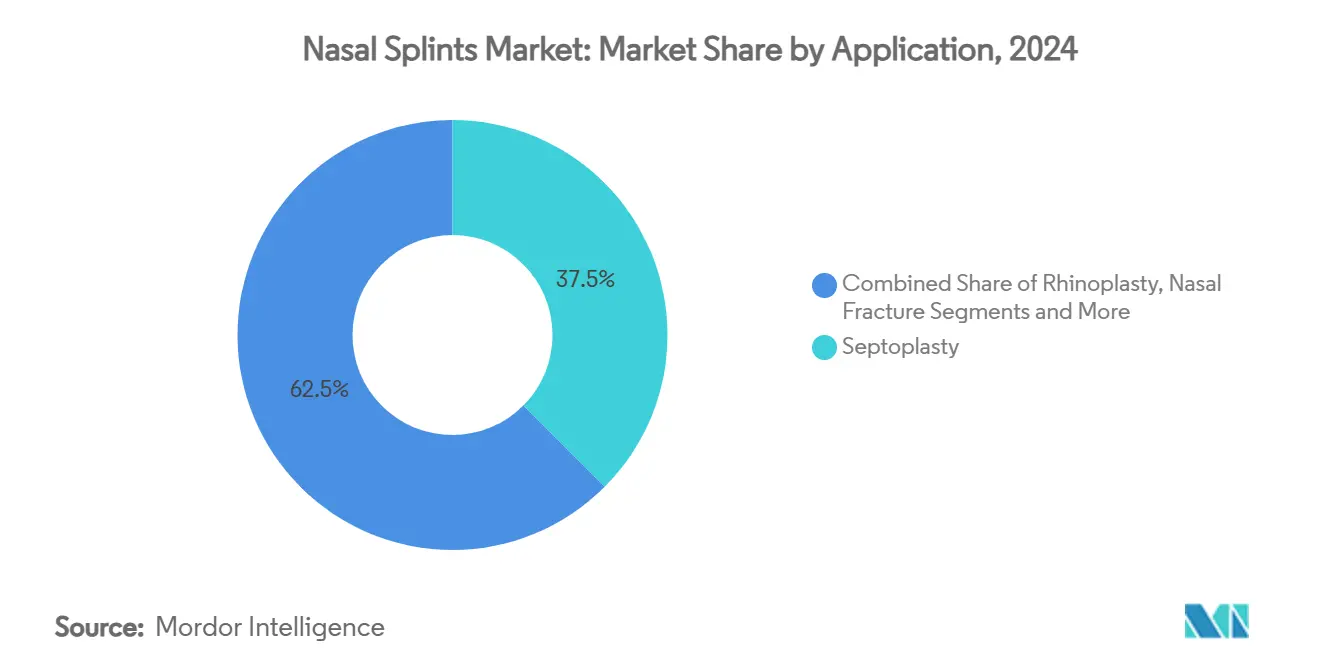

- By application, septoplasty procedures generated 37.48% of the nasal splints market size in 2024, whereas sinus surgery shows the highest 7.49% CAGR outlook through 2030.

- By end user, hospitals held 53.23% of global nasal splints market share in 2024, yet ambulatory surgical centers represent the fastest-growing channel at a 6.52% CAGR to 2030.

- By geography, North America accounted for 34.77% of global revenue in 2024, while Asia-Pacific leads expansion with a 6.43% CAGR forecast through 2030.

Global Nasal Splints Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of nasal injuries & sinus surgeries | +5.4% | North America, Europe | Medium term (2-4 years) |

| Growing adoption of minimally invasive ENT procedures | +3.6% | North America, EU, APAC | Short term (≤ 2 years) |

| Increasing healthcare spending in emerging markets | +2.7% | APAC core, MEA spill-over | Long term (≥ 4 years) |

| Surge in demand for bioabsorbable nasal splints | +4.0% | Global, led by North America | Medium term (2-4 years) |

| Integration of 3D printing for patient-specific splints | +2.2% | North America, EU, selective APAC | Long term (≥ 4 years) |

| Expansion of outpatient surgery centers | +3.1% | North America, Europe, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Nasal Injuries & Sinus Surgeries

Greater sports participation and a growing elderly population have elevated the incidence of nasal trauma and chronic sinusitis. Clinical audits show that 73% of severe nasal airway obstruction cases trace back to nasal valve collapse, an indication ideally treated with advanced splints.[1]Patel, Chirag, “Bioabsorbable Nasal Implants,” American Rhinologic Society, american-rhinologic.orgEndoscopic sinus surgery protocols now emphasize short-window splinting, as delayed removal beyond 3 days escalates mucosal crusting and revision risk. Demand is especially strong in markets with mature insurance coverage, where reimbursements favor superior patient-reported outcomes. Dissolvable chitosan-based packs that degrade in 7–14 days have reduced follow-up visits while maintaining antibacterial activity. Heightened awareness of occupational injuries and youth sports safety further sustains external splint consumption.

Growing Adoption of Minimally Invasive ENT Procedures

Office-based interventions cut operating-room costs and speed patient recovery. Stryker’s LATERA implant allows in-clinic correction of nasal valve collapse, trimming facility fees and delivering USD 2,200 savings per patient. Mayo Clinic reports durable symptom relief for up to 24 months, with most individuals returning to routine activities within a day. Olympus’s CELERIS disposable debrider, with blades that flex 60 degrees, eliminates multiple tip changes and lowers infection risk. Smith+Nephew’s COBLATION platform removes tissue through plasma energy, minimizing collateral thermal damage. The cumulative effect is broader access to ENT care and faster throughput in busy ambulatory settings.

Increasing Healthcare Spending in Emerging Markets

Asia-Pacific governments are channeling resources into ENT infrastructure, stimulating the nasal splints market. India’s tier-2 and tier-3 cities now support specialized ENT clinics, expanding distribution footprints without relying solely on metropolitan hubs. Medical tourism drives regional patient flow, with Singapore and Thailand offering advanced sinus procedures that require high-quality splints. Latin America mirrors this trajectory, as Brazil and Mexico revamp public hospital networks. While unit price sensitivity remains acute, manufacturers targeting volume-tier products gain early mover advantage.

Surge in Demand for Bioabsorbable Nasal Splints

Bioabsorbable polymers achieve an 8.82% CAGR, driven by patient desire to avoid painful removal sessions. FDA recognition of ASTM F2579-18 standards clarifies regulatory pathways for PLA and PGA devices.. Zinc chloride-coated variants inhibit biofilm formation by Staphylococcus aureus and Pseudomonas aeruginosa, reducing reliance on systemic antibiotics.[2]Noach, N. et al., “Zinc Chloride Is Effective as an Antibiotic in Biofilm Prevention Following Septoplasty,” nature.com Stryker’s NasoPore maintains scaffold strength for 36–48 hours before resorption, easing postoperative care. Chitosan-lactate hybrids have demonstrated superior hemostasis, assuaging surgeon concerns about bleeding control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-operative discomfort & non-compliance | -1.8% | Global, price-sensitive markets | Short term (≤ 2 years) |

| Infection & toxic shock risk with intranasal splints | -1.3% | Global, higher in emerging markets | Medium term (2-4 years) |

| Volatile supply of medical-grade silicone & polymers | -2.7% | Global, manufacturing hubs | Short term (≤ 2 years) |

| Regulatory uncertainty for novel bioabsorbables | -0.9% | North America, EU, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Operative Discomfort & Non-Compliance

Patient reluctance to endure splint removal undermines adherence, particularly where bioabsorbable options remain cost-prohibitive. Studies confirm a rise in mucosal crusting when silicone devices stay in place beyond 72 hours, compelling surgeons to balance healing objectives with comfort. Pediatric cases are especially challenging because anxiety and limited cooperation impede routine follow-up. Customized 3D-printed splints mitigate pressure points yet remain expensive. Health systems now factor satisfaction metrics into procurement tenders, pushing vendors to prioritize ergonomic design.

Infection & Toxic Shock Risk With Intranasal Splints

Intranasal splints can harbor gram-negative bacteria; Klebsiella pneumoniae prevalence has prompted many clinics to run pre-surgical screens.[3]Ofir Zavdy, Gabriel Nakache, Uri Alkan, Alain Hazan, Ella Reifen, and Amit Ritter, “Gram-Negative Colonization in Septal Splints,” Wiley Online Library, wiley.com Zinc chloride coatings sharply reduce biofilm formation but adoption lags due to limited long-term data. Short prophylactic antibiotic courses help, yet overuse risks antimicrobial resistance. A few rare cases document down-migration of silicone splints into the esophagus, underscoring the importance of secure fixation. Regulators now scrutinize clinical protocols that mitigate infection, adding compliance overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Intranasal Dominance Faces Bioabsorbable Disruption

Intranasal devices captured 59.65% of global revenue in 2024, underpinning the nasal splints market size leadership thanks to established use in septoplasty and rhinoplasty. The sling-bridge technique for complex deviations shows 90% success in achieving a straight nasal profile without dorsal irregularities, reinforcing reliance on internal supports. External splints are set to grow at 7.67% CAGR through 2030, propelled by sports injury prevalence and lighter thermoplastic offerings that favor patient comfort.

Advances such as Olympus’s malleable CELERIS blade reduce set-up time by eliminating multiple tips and lessen infection risk. External units now integrate aluminum alloys with soft PVC padding, producing rigid protection without nasal bridge irritation. Patient-specific printed external frames promise superior aesthetics, yet economies of scale remain elusive, limiting deployment to tertiary centers and private cosmetic practices.

By Material: Bio-Absorbable Polymers Reshape Market Dynamics

Silicone still leads at 43.72% share in 2024, but procurement officers now confront steep input costs that squeeze margins, accelerating trials of substitute formulations. Bio-absorbable polymers post the fastest 8.82% CAGR, supported by ASTM-aligned regulatory guidance that clarifies PLA/PGA device requirements. Thermoplastics such as ABS gain favor for external trauma units, valued for easy thermoforming on site.

Zinc chloride-coated intranasal splints demonstrate marked reductions in bacterial adhesion, potentially setting a new performance benchmark. Composite hybrids marry silicone familiarity with polymer stability, offering a hedge against raw-material shocks. End users benchmark new entrants against proven mechanical retention and predictable resorption timelines to preserve surgical workflow continuity.

By Application: Sinus Surgery Emerges as Growth Driver

Septoplasty represented 37.48% of total revenue in 2024, reflecting clinical routine and high prevalence of septal deviation. Functional endoscopic sinus surgery now underpins a 7.49% CAGR for sinus surgery splints, as surgeons tackle complex polyposis and chronic rhinosinusitis. High-definition scopes and narrow-band imaging methods boost confidence in executing delicate ethmoid and sphenoid interventions, which depend on precise splint positioning.

Rhinoplasty benefits from novel four-step septal-extension graft approaches, reporting 9.3/10 satisfaction after a year. Nasal fracture management maintains steady growth as contact-sport participation rises. Revision surgery volumes climb as patients seek functional and aesthetic optimization, demanding splints that permit intricate cartilage manipulation without compromising airway patency.

By End User: Ambulatory Centers Drive Market Evolution

Hospitals accounted for 53.23% of nasal splints market share in 2024 owing to trauma and complex cases requiring overnight monitoring. Ambulatory surgical centers post a 6.52% CAGR through 2030, capitalizing on lower bundled payments and streamlined patient flow. Stryker’s LATERA exemplifies outpatient suitability, yielding USD 2,200 savings per intervention.

Specialty ENT clinics embrace disposable systems such as CELERIS to remove sterilization cycles, trimming operational overhead. Hospitals now split pathways, keeping complex reconstruction in inpatient theaters while delegating routine splint checks to outpatient wings. Tele-ENT platforms facilitate remote observation of bioabsorbable dissolutions, sparing patients repeat travel.

Geography Analysis

North America controlled 34.77% revenue in 2024, supported by early technology adoption and favorable reimbursement. Newly created ICD-10-CM codes for nasal valve collapse sharpen diagnostic accuracy and ensure billing clarity for advanced implants. Canadian uptake benefits from hospital modernization grants, whereas Mexico expands insurance coverage for functional rhinoplasty.

Asia-Pacific is the fastest mover with 6.43% CAGR to 2030. China and India invest aggressively in ENT centers across secondary cities, while Japan pioneers bioabsorbable trials under tight quality benchmarks. South Korea and Australia serve as regional springboards for emerging suppliers testing patient-specific printed frames. Tourism inflows to Thailand and Singapore for sinus surgery amplify premium device demand.

Europe maintains steady momentum. Germany and the United Kingdom lead scope and implant adoption. France and Italy witness growing elective rhinoplasty volumes, driving external-splint orders. Spain and Russia gain traction amid broader healthcare reforms. The Middle East concentrates orders in Saudi Arabia and UAE, with South Africa anchoring distribution across sub-Saharan Africa. Nigeria and Egypt see volume growth in cost-efficient silicone splints as surgical capacity rises.

Competitive Landscape

The nasal splints market exhibits moderate concentration. Medtronic, Stryker, and Smith+Nephew claim an estimated 41% share, leveraging patented bioabsorbable chemistries and single-use instrumentation. Integra LifeSciences expanded its ENT footprint by acquiring Acclarent in April 2024, adding USD 1 billion to its addressable market. Olympus differentiates through disposables that eradicate reprocessing costs and reduce infection exposure.

Patent litigation intensifies; the US ITC opened an investigation into alleged infringement involving nasal device components in March 2025. Material science remains the core battleground, with vendors testing zinc chloride coatings and PLA/PGA copolymers to curb biofilm risk. Pediatric indications attract innovators like Sonu Band, the first drug-free acoustic therapy cleared for congestion relief in children.

Start-ups focusing on 3D-printed bespoke frames and AI-guided imaging tools pose niche threats, although scaling production to hospital volume levels remains a hurdle. Supply chain shocks surrounding silicone prompt incumbents to dual-source raw materials, enhancing resilience but raising costs. Overall rivalry centers on outcome-based value propositions and post-operative comfort metrics that drive physician loyalty.

Nasal Splints Industry Leaders

Medtronic plc

Stryker Corporation

Smith & Nephew plc

Boston Scientific Corporation

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: FDA approved the Sonu Band, an AI-enabled wearable for pediatric nasal congestion, marking the first drug-free device of its kind.

- April 2025: American Rhinologic Society endorsed bioabsorbable nasal implants as non-experimental, urging payers to support reimbursement.

- April 2024: Integra LifeSciences completed its acquisition of Acclarent, expanding its ENT product portfolio.

Global Nasal Splints Market Report Scope

| Intranasal Splints |

| External Nasal Splints |

| Silicone |

| Thermoplastics (ABS, PVC) |

| Aluminum |

| Bio-absorbable Polymers (PLA, PGA) |

| Composite & Hybrid Materials |

| Septoplasty |

| Rhinoplasty |

| Nasal Fracture |

| Sinus Surgery |

| Revision Surgery |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty ENT Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| Product Type | Intranasal Splints | |

| External Nasal Splints | ||

| Material | Silicone | |

| Thermoplastics (ABS, PVC) | ||

| Aluminum | ||

| Bio-absorbable Polymers (PLA, PGA) | ||

| Composite & Hybrid Materials | ||

| Application | Septoplasty | |

| Rhinoplasty | ||

| Nasal Fracture | ||

| Sinus Surgery | ||

| Revision Surgery | ||

| End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty ENT Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current size of the nasal splints market?

The nasal splints market size is USD 2.08 billion in 2025 and is expected to reach USD 2.59 billion by 2030.

2. Which product category dominates global revenue?

Intranasal splints lead with 59.65% revenue share because they are routinely used in septoplasty and rhinoplasty.

3. Why are bioabsorbable nasal splints gaining popularity?

Bioabsorbable devices dissolve in the body, eliminate painful removal sessions, and generate cost savings of about USD 2,200 per case.

4. Which region is growing fastest?

Asia-Pacific registers the highest regional CAGR at 6.43% through 2030 due to rising surgical volumes and expanding healthcare spending.

Page last updated on: