Anti-Pollution Nasal Spray Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

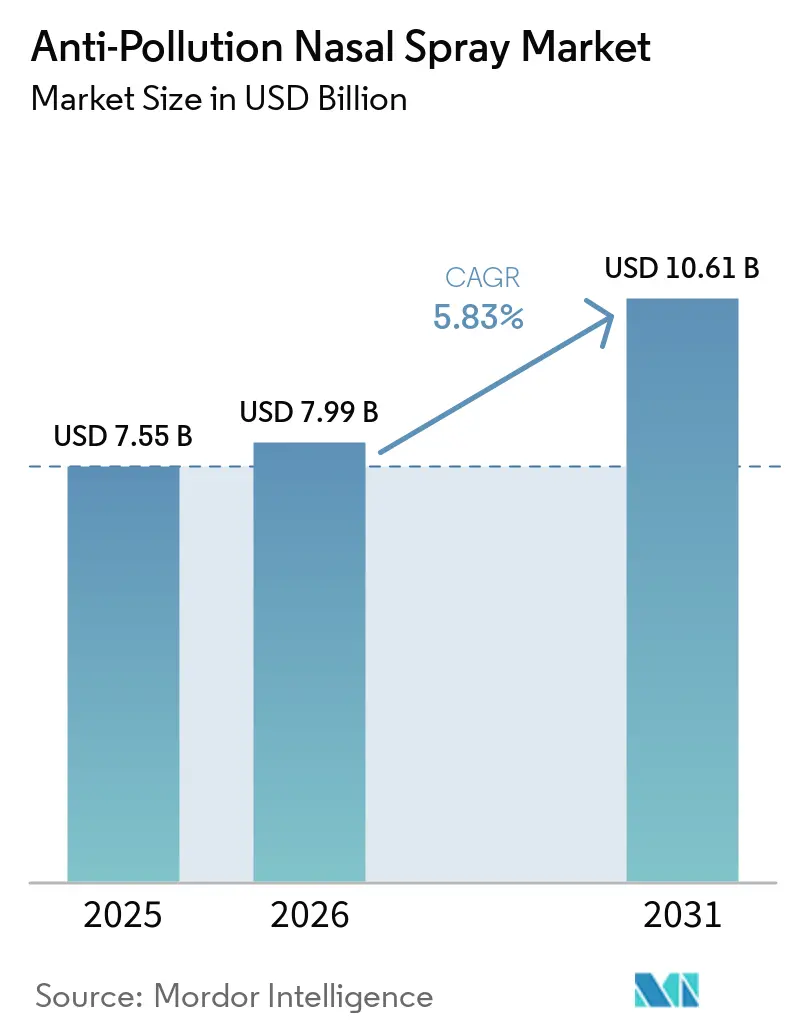

| Market Size (2026) | USD 7.99 Billion |

| Market Size (2031) | USD 10.61 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-Pollution Nasal Spray Market Analysis by Mordor Intelligence

The Anti-Pollution Nasal Spray Market size is expected to increase from USD 7.55 billion in 2025 to USD 7.99 billion in 2026 and reach USD 10.61 billion by 2031, growing at a CAGR of 5.83% over 2026-2031.

Urban consumers are increasingly integrating nasal hygiene into their daily respiratory care routines, driving the anti-pollution nasal spray market from reactive symptom relief to preventive use. This market offers a diverse range of formulations, including barrier sprays, saline solutions, herbal variants, cleansing agents, and hydrating products, enabling brands to address both protection-focused and comfort-driven demands. Public awareness of air pollution, supported by the WHO's 2025 air quality and health framework, highlights the long-term health risks of polluted air and strengthens the demand for preventive upper airway care. While major consumer health companies dominate pharmacy shelf space, specialty players with clinical evidence and advanced barrier-forming technologies are gaining traction, challenging undifferentiated saline products.

Key Report Takeaways

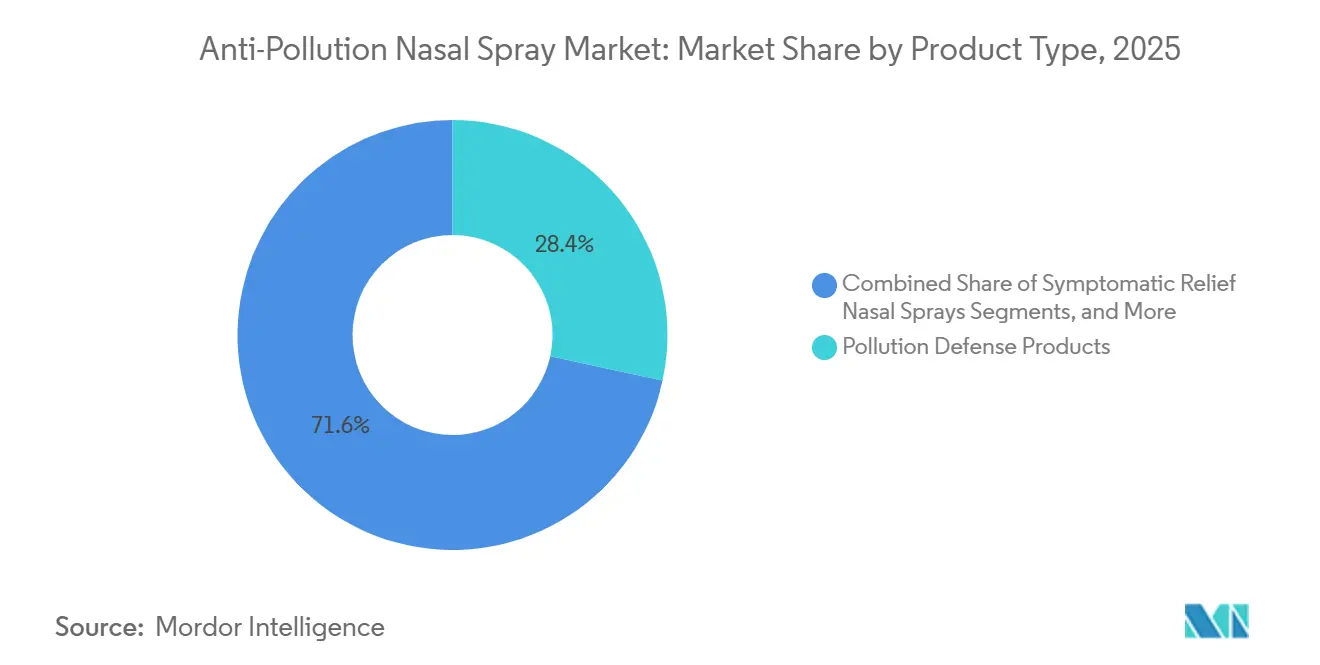

- By product type, pollution defense products held 28.40% of the anti-pollution nasal spray market in 2025, while symptomatic relief nasal sprays are projected to grow at 7.80% CAGR through 2031.

- By distribution channel, retail pharmacies held 42.87% of the anti-pollution nasal spray market share in 2025, while online channels are projected to expand at 8.25% CAGR through 2031.

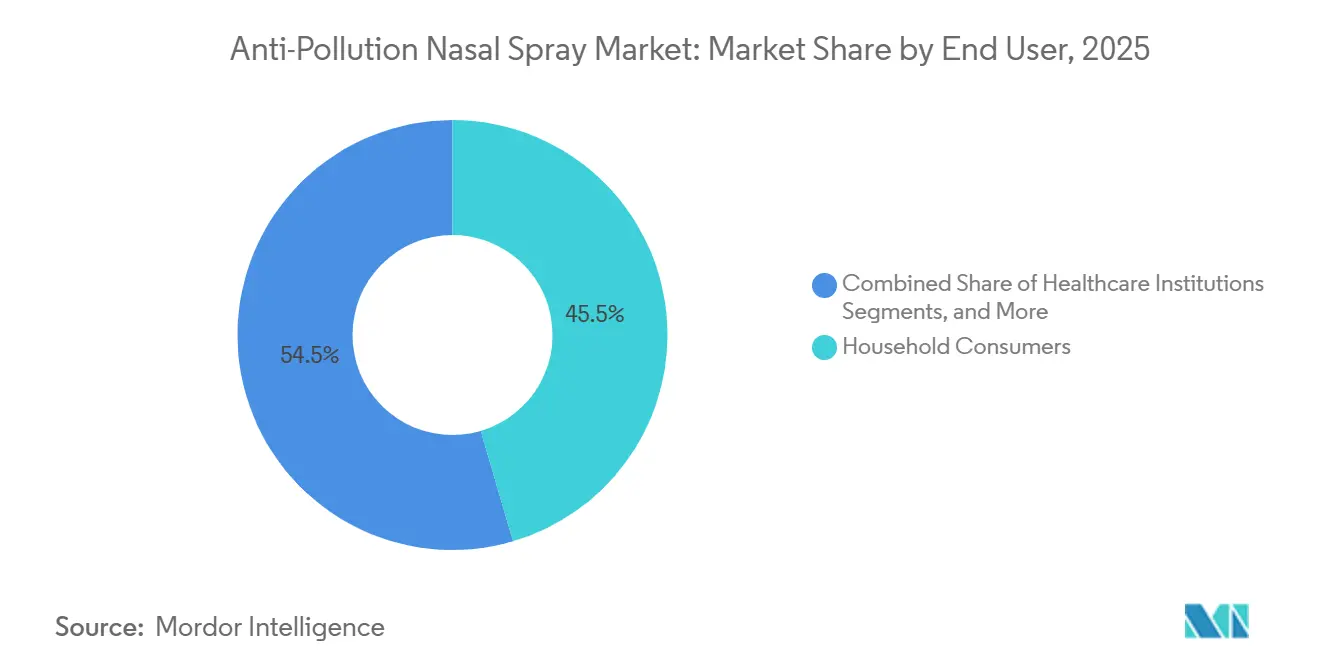

- By end user, household consumers accounted for 45.45% of the anti-pollution nasal spray market in 2025, while occupational and industrial users are projected to grow at 6.69% CAGR through 2031.

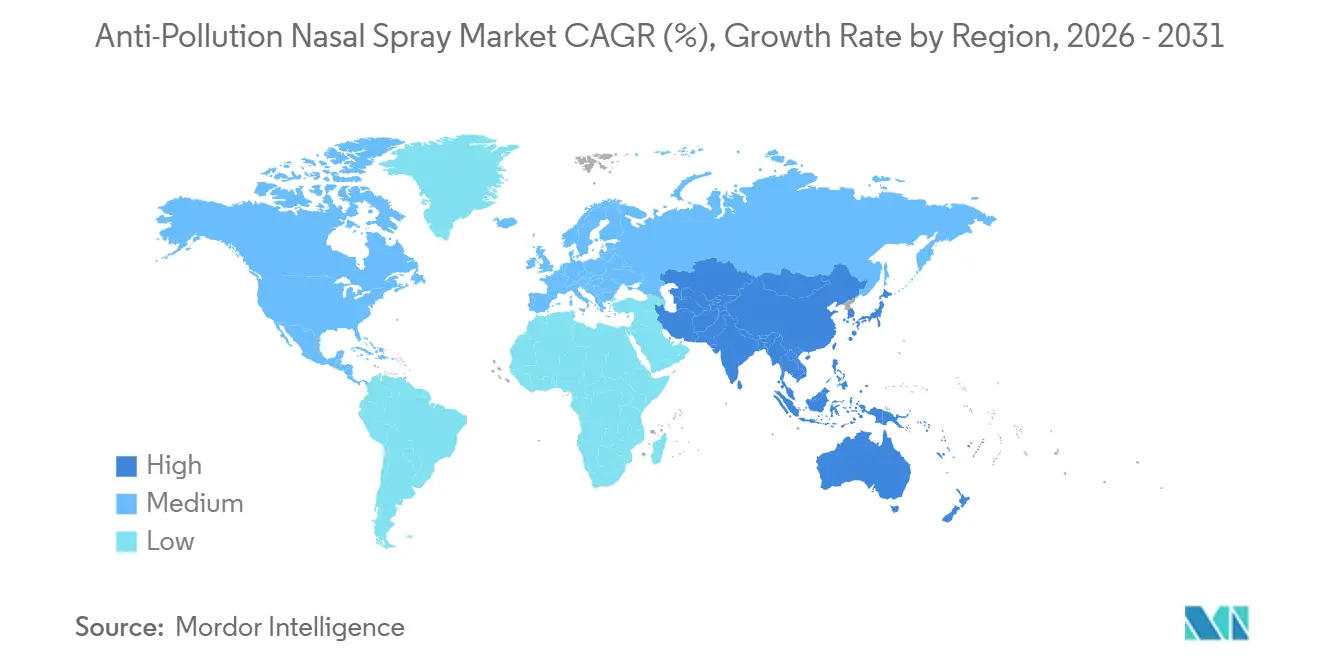

- By geography, North America held 38.07% of the anti-pollution nasal spray market share in 2025, while Asia-Pacific is expected to advance at 7.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anti-Pollution Nasal Spray Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising urban air pollution and smog exposure | +1.8% | Global, particularly APAC core, India and China, and MEA | Short term (≤ 2 years) |

| Rising consumer preference for preventive nasal care | +1.4% | North America and Europe | Medium term (2-4 years) |

| Expansion of e-commerce and omnichannel pharmacy access | +1.1% | APAC core, with spillover to North America and Europe | Short term (≤ 2 years) |

| Growing demand for natural, herbal, and drug-free formulations | +0.9% | Global, with APAC and Europe leading | Medium term (2-4 years) |

| Rising product positioning around allergy and pollution co-protection | +0.7% | North America and Europe | Medium term (2-4 years) |

| Wider acceptance of barrier-forming and microfilm technologies | +0.6% | Global premium markets, including the United States, Europe, Japan, and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Urban Air Pollution and Smog Exposure

As cities face worsening air quality, the demand for anti-pollution nasal sprays continues to rise. The nose, being the primary entry point for polluted air, is highly susceptible to fine particles. Research published in 2025 revealed that urban particulate exposure disrupts the upper respiratory tract microbiome, increasing vulnerability to conditions like allergic rhinitis and rhinosinusitis.[1]Respiratory Research Editorial Team, “Effects of Urban Airborne Particulate Matter Exposure on the Human Upper Respiratory Tract Microbiome, A Systematic Review,” Respiratory Research, link.springer.com PM10 and similar particles heavily deposit in the nasal cavity, emphasizing the need for preventive nasal protection. Another 2025 study highlighted that school-age children face 2-3 times higher pollutant exposure in winter, reducing nasal microbiome diversity. These findings drive the adoption of anti-pollution nasal sprays, particularly in Asia-Pacific and Europe, where upper airway exposure remains a public health concern.[2]Journal of Personalized Medicine Editorial Team, “The Relationship between Fine Particle Matter, PM2.5, Exposure and Upper Respiratory Tract Diseases,” Journal of Personalized Medicine, mdpi.com

Expansion of E-Commerce and Omnichannel Pharmacy Access

Online platforms are the fastest-growing distribution channel for anti-pollution nasal sprays, with an 8.25% growth rate projected through 2031. Digital pharmacy platforms simplify repeat orders and home delivery, aligning with the daily preventive use of these sprays. Nasal therapy brands are also shifting to direct commercialization to control consumer acquisition and refill behavior. For instance, Glenmark's 2026 direct commercialization of RYALTRIS in the U.S., coupled with BlinkRx's home delivery, reflects this trend. As this approach expands, online channels are expected to see stronger repeat consumption compared to physical stores, where refill discipline is weaker.

Growing Demand for Natural, Herbal, and Drug-Free Formulations

Consumer demand for ingredient-transparent products is reshaping the anti-pollution nasal spray market. Buyers increasingly prefer sprays suitable for regular use without synthetic pharmaceuticals. Multi-functional products combining environmental protection with soothing or allergy-relief benefits are gaining popularity. A 2025 trial showed that AM-301, a drug-free mineral-based barrier spray, outperformed saline in reducing seasonal allergic rhinitis symptoms, strengthening the market for natural and drug-free products.[3]National Library of Medicine, “AM-301, a Barrier-Forming Nasal Spray, Versus Saline Spray in Seasonal Allergic Rhinitis, A Randomized Clinical Trial,” PubMed, pubmed.ncbi.nlm.nih.gov

Wider Acceptance of Barrier-Forming and Microfilm Technologies

Barrier-forming and microfilm technologies are emerging as key innovations in the anti-pollution nasal spray market. These technologies create a protective layer on the nasal mucosa, focusing on prevention rather than post-exposure treatment. Trial data confirm the efficacy of drug-free barrier sprays in reducing allergic rhinitis symptoms. Regulatory advancements, such as Altamira Medica's Bentrio receiving EU Medical Device Regulation certification in November 2025, further validate this segment. This milestone positions the market as a premium, technology-driven category in Europe and other regulated regions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited long-term clinical evidence for daily prophylactic use | -0.9% | Global | Medium term (2-4 years) |

| Regulatory ambiguity around claims, classification, and labeling | -0.5% | North America and Europe | Medium term (2-4 years) |

| Consumer substitution from masks, air purifiers, and saline rinses | -0.6% | Global | Short term (≤ 2 years) |

| Trust gap from inconsistent formulation quality across brands | -0.4% | Emerging markets across APAC, MEA, and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Long-Term Clinical Evidence for Daily Prophylactic Use

The anti-pollution nasal spray market faces a key challenge due to limited long-term clinical evidence supporting year-round daily use. Most studies focus on short-term efficacy, leaving questions about habitual use in chronic exposure conditions unanswered. This gap impacts physician endorsements, which are crucial for consumers seeking preventive solutions in health-conscious markets. Additionally, the market operates within a complex regulatory framework, where product classification varies based on its positioning as a cosmetic, wellness product, or medical device. Without consistent evidence and regulatory clarity, some brands may struggle with adoption in primary care and cautious recommendations from healthcare professionals.

Consumer Substitution From Masks, Air Purifiers, and Saline Rinses

The anti-pollution nasal spray market competes with alternatives like masks, portable air purifiers, and saline rinses, particularly in price-sensitive urban markets. Saline irrigation poses a direct challenge, offering similar cleansing benefits at a lower cost. To sustain premium positioning in emerging economies, the market must emphasize the distinction between post-exposure rinsing and barrier-based prevention. Without this clarity, consumers may initially opt for cheaper or familiar options before considering specialized nasal protection products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pollution Defense Anchors Volume, Symptom Relief Accelerates

In 2025, Pollution Defense Products held a 28.40% share of the anti-pollution nasal spray market, leading a six-part product landscape that includes saline-based, herbal and natural, symptomatic relief, cleansing, and hydrating sprays. Urban consumers initially adopted these products, focusing on visible pollution and particulate exposure rather than broader nasal wellness. North America and Europe have favored these products due to their clear barrier-led positioning, which aligns with urban challenges like commuting, smog, and outdoor activities. Products using polymer-film barriers, bentonite-based gels, and carrageenan formats have gained traction due to their defined first-use cases.

Symptomatic Relief Nasal Sprays are projected to grow at a 7.80% CAGR through 2031, making them the fastest-growing segment. This growth reflects a shift from single-purpose protection to addressing issues like irritation, congestion, and inflammation caused by pollution exposure. A 2024 study linked PM2.5 exposure to inflammatory conditions, highlighting the need for products beyond cleansing. Herbal and natural variants are gaining popularity in Asia-Pacific and the Middle East, where consumers prefer botanical ingredients like xylitol, aloe vera, and eucalyptus. The industry is evolving toward a diverse product mix emphasizing performance, comfort, and formulation transparency.

By Distribution Channel: Retail Dominates, Online Disrupts

In 2025, Retail Pharmacies accounted for 42.87% of the anti-pollution nasal spray market, underscoring their role in driving visibility and guided purchases. Nasal care products benefit from pharmacist recommendations, strategic shelf placement, and impulse purchases during respiratory discomfort. Hospital and Clinic Pharmacies hold a smaller share but provide credibility for clinically supported products. Supermarkets and General Retail Stores cater to cleansing and hydrating formats, bridging wellness and therapeutic needs.

Online Channels are expected to grow at an 8.25% CAGR through 2031, making them the fastest-growing distribution channel. Digital platforms support refill behavior, recurring purchases, and consumer education, aligning with prevention-focused categories. Glenmark’s 2026 commercialization of RYALTRIS and BlinkRx’s home delivery rollout highlight the shift toward direct consumer relationships. While online channels offer pricing and subscription advantages, they require significant investment in digital marketing and fulfillment. Smaller brands may benefit from online visibility but need strong clinical positioning to compete effectively.

By End User: Household Consumers Lead, Occupational Segment Emerges

In 2025, Household Consumers represented 45.45% of the anti-pollution nasal spray market, driven by OTC self-care among urban adults and families. This segment benefits from retail accessibility and everyday use cases like commuting, allergy seasons, and indoor air concerns. Digital air quality notifications further support this segment by encouraging preemptive or post-exposure usage. Healthcare Institutions, while smaller, are gaining relevance as clinicians and occupational health teams explore barrier sprays for environments with frequent particulate exposure.

Occupational and Industrial Users are projected to grow at a 6.69% CAGR through 2031, the fastest among end-user groups. This segment includes workers in construction, mining, agriculture, and wildfire response, who face high-intensity exposure to airborne irritants. In January 2025, NeilMed’s donation of Sinus Rinse products to Los Angeles wildfire responders highlighted the importance of occupational nasal care. Over time, the market may develop a distinct B2B channel as employers and health teams adopt nasal barrier products alongside respiratory safety measures. Travel and Outdoor Users will remain significant due to seasonal pollution spikes and pollen periods, driving demand among cyclists, hikers, and frequent travelers.

Geography Analysis

In 2025, North America dominated the anti-pollution nasal spray market, capturing 38.07% of the share. The region's success is attributed to its established OTC infrastructure, extensive pharmacy network, and a consumer base willing to invest in respiratory self-care. The U.S. remains the primary revenue hub due to brand visibility, ingrained allergy care habits, and a regulatory environment that supports growth in nasal therapies. Canada and Mexico add regional depth, though consumer adoption outside the U.S. is uneven due to lower retail intensity and category awareness. The market is also witnessing growth in institutional use, driven by increased focus on indoor air quality and occupational respiratory health.

Europe remains a significant market for anti-pollution nasal sprays, supported by pharmacy-led healthcare practices and high allergic rhinitis prevalence. However, the EU MDR imposes stricter compliance requirements. France is positioned for strong growth as consumer trust in pharmacy recommendations aligns with the barrier-spray concept. Germany, another key market, saw Sandoz intensify competition in March 2026 with the Hexal launch of an azelastine-fluticasone combination product ahead of allergy season. Companies that balance regulatory compliance with clinically supported formulations are likely to succeed in this market.

Asia-Pacific is the fastest-growing region for anti-pollution nasal sprays, with a projected 7.45% CAGR through 2031. China and India drive growth due to urban pollution, rising disposable incomes, and expanding pharmacy access, which are converting awareness into regular product use. Altamira's December 2025 approval of Bentrio in Mainland China highlights the region's importance as a regulatory and commercial destination. The market benefits from increased visibility in organized pharmacy chains and the growing role of digital commerce in respiratory care purchases. Smaller markets like the Middle East, Africa, South America, Brazil, and Argentina are gaining relevance due to rising pollution awareness and pharmacy-led preventive care campaigns.

Competitive Landscape

The anti-pollution nasal spray market is moderately concentrated, with a few established consumer health companies dominating pharmacy shelves, while smaller specialty brands focus on niche segments. Companies like Haleon, Reckitt Benckiser, NeilMed, and Merck benefit from strong distribution networks, recognized brands, and widespread consumer familiarity in nasal and respiratory care. Meanwhile, technology-driven specialists such as Altamira Medica and Nasaleze are intensifying competition with barrier-forming products based on distinct scientific propositions, differentiating them from standard saline offerings. This dynamic has created a market divided between scale-driven incumbents and evidence-based challengers, rather than being controlled by a single dominant player.

Recent strategic moves reflect how companies are strengthening their positions in the anti-pollution nasal spray market. Sandoz launched Hexal in March 2026 in Germany and Switzerland, strategically aligning with allergy season to capitalize on predictable respiratory demand peaks. Glenmark’s 2026 shift to direct commercialization of RYALTRIS in the U.S., supported by BlinkRx home delivery, highlights a focus on digital access, patient convenience, and streamlined commercial pathways. Altamira’s EU MDR certification in November 2025 and approval in China in December 2025 demonstrate a strategy of leveraging regulatory milestones to access premium markets and validate its drug-free barrier technology platform.

Natural and saline-based brands continue to hold a significant share of the anti-pollution nasal spray market, as many consumers prefer familiar ingredients and simple daily-use formats. Bayer, Church and Dwight, and Xlear compete in this space by positioning products around xylitol, saline, or botanical ingredients, helping them stand out despite similar core functions. Regional players also play a key role, as localized formulations cater to varying nasal care habits and retail advice patterns. For example, Himalaya Wellness remains strong in South Asia with its herbal positioning, while JGL maintains a solid presence in parts of Central and Eastern Europe through established pharmacy relationships. The industry is expected to remain diverse, driven by innovation, regulatory developments, and regional preferences, preventing high market concentration in the near future.

Anti-Pollution Nasal Spray Industry Leaders

GSK plc

Haleon plc

Himalaya Wellness Company

NeilMed Pharmaceuticals, Inc.

Xlear, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sandoz Group AG, through its Hexal subsidiary, launched a fixed-dose combination azelastine-fluticasone nasal spray in Germany and Switzerland, targeting approximately 15 million allergy sufferers in Germany during the spring allergy season.

- April 2026: Glenmark Pharmaceuticals began direct commercialization of RYALTRIS in the U.S. and expanded its availability to 55 countries, with home delivery options signaling a shift toward direct-to-consumer sales.

- March 2026: Beijing Grand Jiuhe Pharmaceutical launched Ryaltris for allergic rhinitis in China, covering six cities and involving over 60 experts across relevant medical disciplines.

- January 2026: Altamira Medica received marketing approval in China for Bentrio nasal spray, enabling Nuance Pharma to begin distribution in a market with an estimated 200 million allergic rhinitis patients.

- November 2025: Altamira Medica's Bentrio became the first drug-free nasal barrier spray certified under the EU Medical Device Regulation, setting a precedent for non-pharmacological nasal products in the EU.

Global Anti-Pollution Nasal Spray Market Report Scope

As per the scope of the report, Anti-pollution nasal sprays are preventative medical devices designed to block or wash away harmful airborne pollutants, dust, pollen, and fine particulate matter (like PM2.5) from the nasal cavity. They reduce respiratory irritation and prevent contaminants from reaching the lungs.

The anti-pollution nasal spray market is segmented by product type, distribution channel, end-user, and geography. By product type, the market includes pollution defense products, saline-based nasal sprays, herbal and natural nasal sprays, symptomatic relief nasal sprays, cleansing nasal sprays, and hydrating nasal sprays. By distribution channel, the market is segmented into retail pharmacies, online channels, supermarkets and general retail stores, and hospital and clinic pharmacies. By end-user, the market is categorized into household consumers, healthcare institutions, travel and outdoor users, and occupational and industrial users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Pollution Defense Products |

| Saline-Based Nasal Sprays |

| Herbal and Natural Nasal Sprays |

| Symptomatic Relief Nasal Sprays |

| Cleansing Nasal Sprays |

| Hydrating Nasal Sprays |

| Retail Pharmacies |

| Online Channels |

| Supermarkets and General Retail Stores |

| Hospital and Clinic Pharmacies |

| Household Consumers |

| Healthcare Institutions |

| Travel and Outdoor Users |

| Occupational and Industrial Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Pollution Defense Products | |

| Saline-Based Nasal Sprays | ||

| Herbal and Natural Nasal Sprays | ||

| Symptomatic Relief Nasal Sprays | ||

| Cleansing Nasal Sprays | ||

| Hydrating Nasal Sprays | ||

| By Distribution Channel | Retail Pharmacies | |

| Online Channels | ||

| Supermarkets and General Retail Stores | ||

| Hospital and Clinic Pharmacies | ||

| By End User | Household Consumers | |

| Healthcare Institutions | ||

| Travel and Outdoor Users | ||

| Occupational and Industrial Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the anti-pollution nasal spray market?

The anti-pollution nasal spray market is valued at USD 7.99 billion in 2026 and is forecast to reach USD 10.61 billion by 2031 at a CAGR of 5.83%.

Which product category leads revenue in anti-pollution nasal sprays?

Pollution Defense Products led with 28.40% share in 2025, reflecting strong demand for barrier-led solutions tied to urban particulate exposure.

Which distribution channel is growing the fastest for nasal protection products?

Online Channels are forecast to grow at 8.25% CAGR through 2031 as direct commercialization, refill convenience, and home delivery improve repeat purchase behavior.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is the fastest-growing region at 7.45% CAGR, supported by severe urban pollution, rising incomes, and growing pharmacy and digital commerce access.

What is the biggest barrier to wider adoption of anti-pollution nasal sprays?

Limited long-term clinical evidence for year-round preventive use remains the main barrier because short-duration trials do not fully address habitual daily use questions for clinicians and consumers.

How are leading companies competing in this category?

Companies are using different strategies, including pharmacy scale, direct-to-consumer distribution, and regulatory validation of barrier technologies, as shown by Sandoz, Glenmark, BlinkRx, and Altamira in 2025 and 2026.

Page last updated on: