Nasal Irrigation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.5 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 18.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nasal Irrigation Market Analysis by Mordor Intelligence

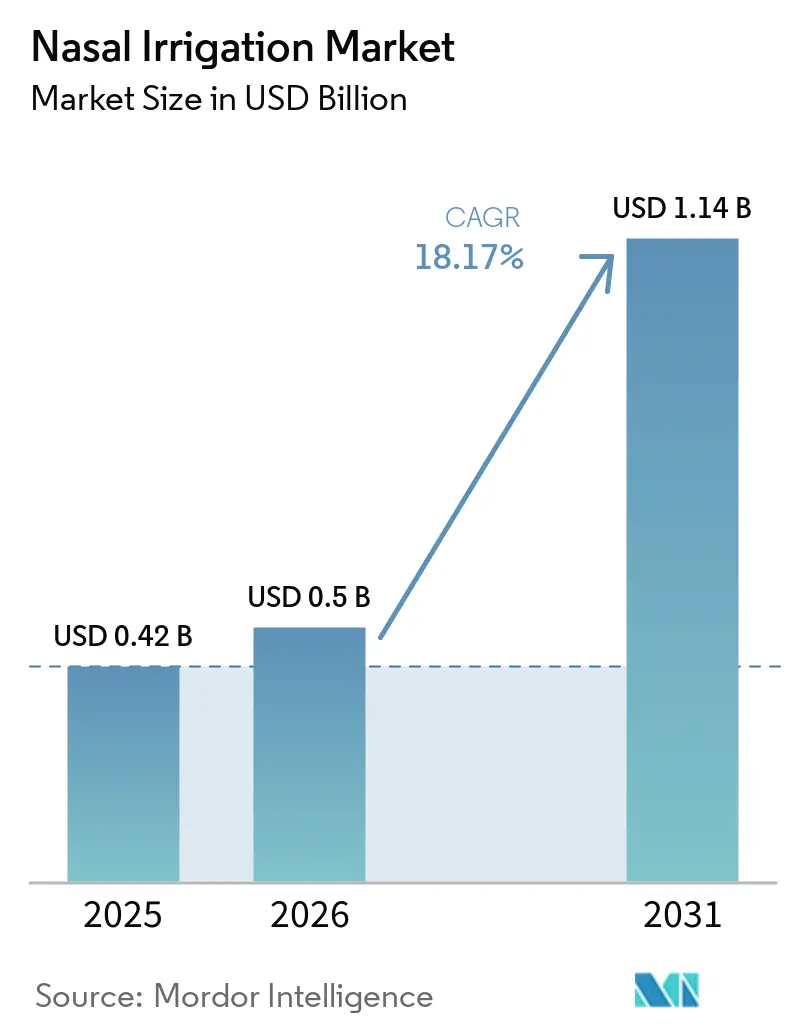

The Nasal Irrigation Market size is projected to expand from USD 0.42 billion in 2025 and USD 0.5 billion in 2026 to USD 1.14 billion by 2031, registering a CAGR of 18.17% between 2026 to 2031.

Awareness that high-volume lavage addresses underlying mucosal inflammation and mucus stasis continues to rise, which supports broader first-line adoption across allergic rhinitis and chronic rhinosinusitis. Postoperative protocols in ENT care normalize early saline irrigation after functional endoscopic sinus surgery, which sustains steady device and consumable purchasing. At-home care expands as patients seek non-pharmacological relief with lower cost of ownership, while subscription models reduce friction in replenishment and user education improves adherence beyond the first week. Water quality guidance from public-health authorities shapes usage norms, as CDC mandates the exclusive use of distilled, sterile, or boiled-then-cooled water for sinus rinsing, which influences device labeling and consumer instructions.

Key Report Takeaways

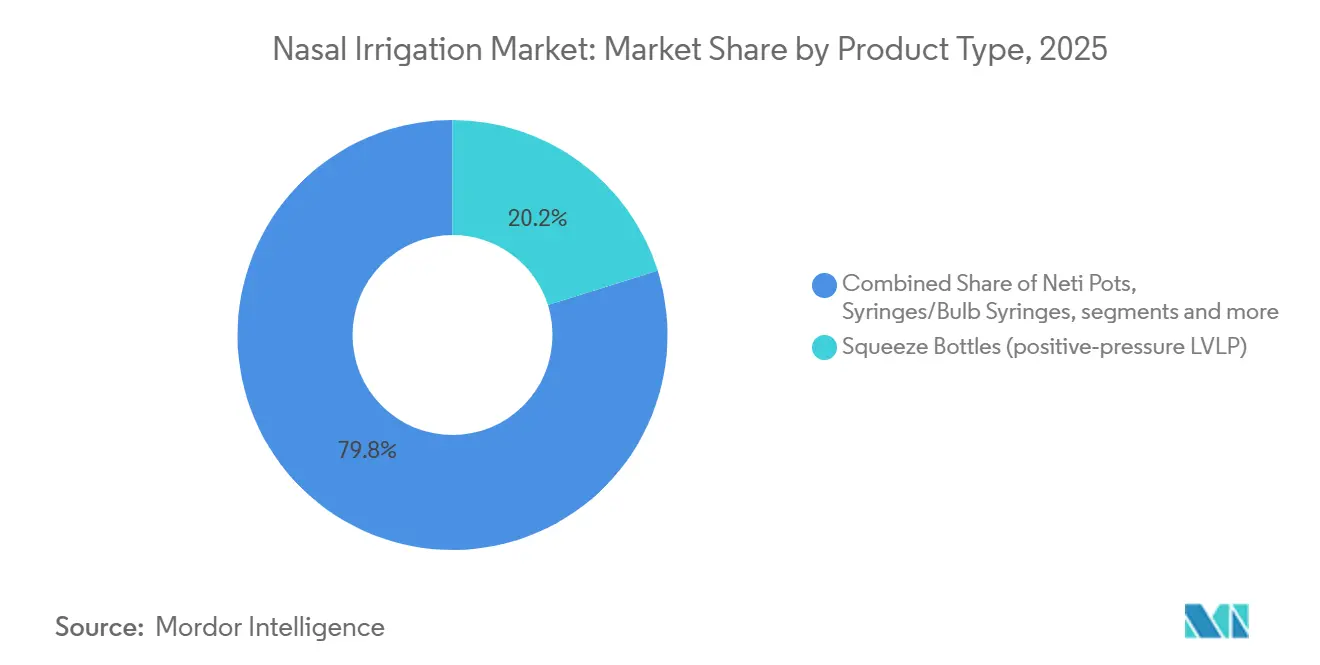

- By product type, squeeze bottles led with a 20.16% revenue share in 2025; powered or pulsatile systems are forecast to expand at a 21.19% CAGR through 2031.

- By technology, manual solutions held 65.23% share in 2025; electric or battery-powered devices are projected to grow at a 20.15% CAGR over 2026-2031.

- By solution type, isotonic saline accounted for a 45.18% share of the nasal irrigation market size in 2025; additive-enhanced solutions are set to advance at a 20.69% CAGR through 2031.

- By indication, allergic rhinitis accounted for 44.90% share in 2025; chronic rhinosinusitis is forecast to post a 21.18% CAGR to 2031.

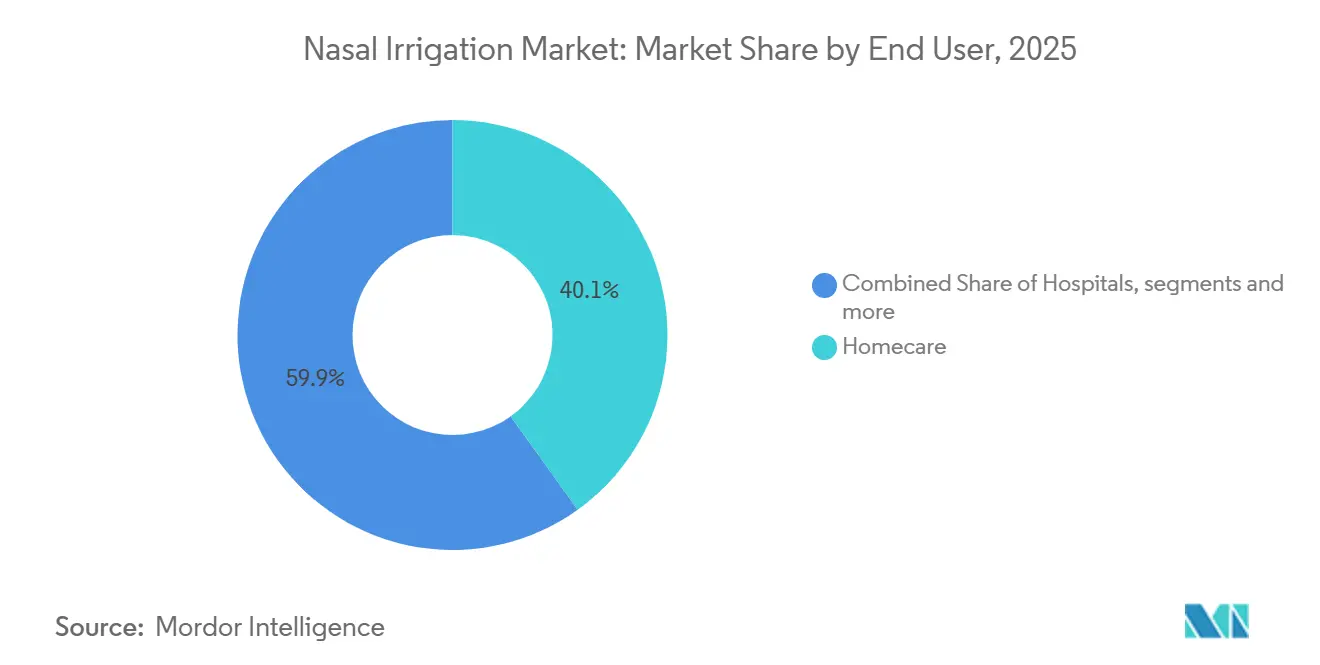

- By end user, homecare accounted for 40.14% share in 2025; it is also the fastest-growing with a 20.16% CAGR through 2031.

- By distribution channel, retail pharmacies held 47.10% share in 2025; e-commerce is projected to grow at a 21.03% CAGR through 2031.

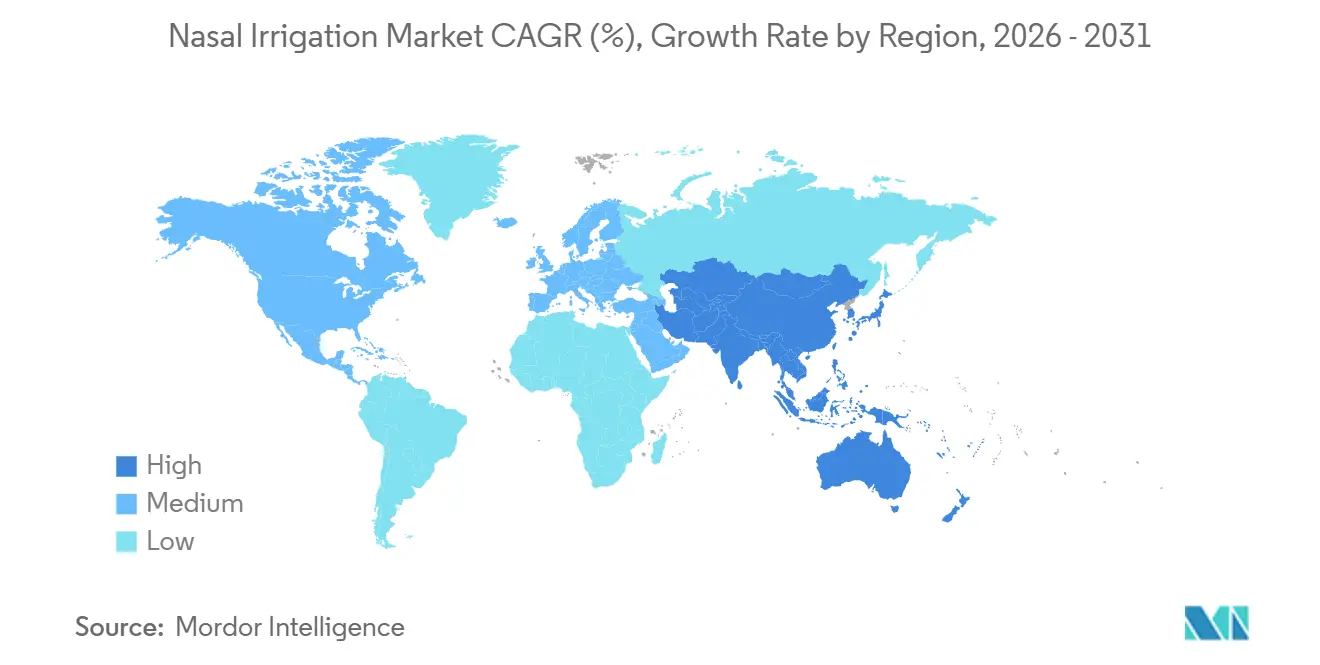

- By region, North America secured 38.17% share in 2025; Asia-Pacific is anticipated to expand at a 20.14% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nasal Irrigation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of allergic rhinitis and chronic rhinosinusitis | +4.2% | Global, with peak burden in North America (50 million sufferers) and urban Asia-Pacific corridors | Medium term (2-4 years) |

| Shift to home-based self-care and OTC nasal hygiene | +3.8% | North America and Europe lead adoption; Asia-Pacific accelerating through e-commerce | Short term (≤ 2 years) |

| Product innovation in powered and pulsatile irrigation systems | +3.1% | North America innovation hubs; Asia-Pacific manufacturing scale-up | Medium term (2-4 years) |

| Expanding use of medicated and antiseptic irrigation (e.g., PVP-iodine, HOCl, xylitol) | +2.7% | Global, spearheaded by clinical trials in US/Europe; regulatory lag in emerging markets | Long term (≥ 4 years) |

| ENT postoperative protocols standardizing high-volume irrigation | +2.4% | North America, Europe, and Australia; clinical-guideline adoption by ENT professional societies | Medium term (2-4 years) |

| Guideline endorsements and antibiotic stewardship elevating saline nasal irrigation as first-line adjunct in rhinosinusitis | +2.3% | North America, Europe adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Allergic Rhinitis and Chronic Rhinosinusitis Fuels Structural Demand

Allergic rhinitis and chronic rhinosinusitis continue to anchor need for daily or seasonal lavage because patients want relief without systemic side effects. Clinical practice in 2026 reflects growing consensus that high-volume irrigation reduces mucosal edema and supports symptom control, especially in chronic rhinosinusitis after surgery. Meta-analytic evidence shows that budesonide nasal irrigation improves disease-specific patient-reported outcomes while maintaining cortisol levels and intraocular pressure within safe ranges, which supports broader clinician confidence.

Patient knowledge remains uneven, as a 2026 cross-sectional study in China reported high current usage of nasal irrigation among rhinosinusitis patients but limited belief in irrigation as an independent disease control strategy, which highlights an education gap that vendors aim to close[1]Feng-ling Yang et al., “The Knowledge, Attitudes and Practice of Nasal Irrigation Among Patients with Rhinosinusitis: A Cross-sectional Study,” Frontiers in Allergy, frontiersin.org. When education is combined with structured follow-up, adherence rises during the first week of a sinusitis episode, although it can taper in week two without ongoing engagement. These patterns sustain demand for both consumables and powered systems as part of seasonal and chronic regimens across the nasal irrigation market.

Home-Based Self-Care Migration Redefines Distribution and Device Design

The nasal irrigation market benefits from a clear migration to home-based care as patients adopt OTC hygiene routines. Adherence support delivered through instructions, video links, and delayed-antibiotic strategies improved week-one compliance in controlled trials, although retention in week two required ongoing feedback loops that digital subscriptions can provide.

Homecare users prize convenience and privacy for a procedure that many initially find unpleasant, which shapes product design toward ergonomic controls and quick-clean components. Retail pharmacists continue to educate on saline mixture, temperature, and pediatric safety, yet online channels expand through automated replenishment and instructional content that address known knowledge deficits documented in recent clinical surveys. Companies adapt packaging and app prompts to sustain weekly routines that align with allergy and infection cycles, which keeps the nasal irrigation market active through both seasonal spikes and chronic daily use.

Product Innovation in Powered and Pulsatile Irrigation Systems

Powered and pulsatile irrigators add pressure modulation and pulsation synchronized to natural ciliary rhythms, which aim to improve mucus clearance and comfort. Commercial systems today advertise 1,200 pulsations per minute and multi-speed modes that personalize flow to anatomy and sensitivity. Competing devices bring rinse-plus-suction in a single pass to reduce cross-flow while improving perceived clearance, and they combine antimicrobial housings with self-clean cycles to address contamination concerns.

Safety engineering has advanced with pressure-release valves that cap output at levels designed to avoid barotrauma and discomfort, which addresses one of the notable barriers to long-term adherence. Battery and charging innovations reduce charging frequency and support travel usage, which extends active user days per month as devices become more portable. These product directions reinforce premium positioning while opening mid-tier price bands in fast-growing regions, which broadens appeal across the nasal irrigation market.

Expanding Use of Medicated and Antiseptic Irrigation

Additive-enhanced irrigations position nasal lavage as a delivery vehicle for antiseptics and anti-inflammatory agents. Phase III evidence in 2025 reported symptomatic benefits for povidone-iodine nasal spray in the common cold, with larger effects when treatment began early, which supports interest in antiseptic-lavage combinations. A growing body of research around hypertonic saline shows clinical improvements post-surgery, albeit with higher local irritation, which guides surgeons to reserve it for specific clinical circumstances.

Budesonide nasal irrigation has a favorable safety profile in pooled analyses and improves validated outcome scores, which aligns with practice trends in chronic rhinosinusitis and post-surgical care. Network meta-analyses also explore novel adjuncts such as resveratrol, although commercial product availability remains limited compared to saline-based and steroid-admixture options. As clinical validation increases, reimbursable pathways and standardized dosing could open, which would expand the nasal irrigation market toward higher-value formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Improper water quality and device contamination risks | -2.3% | Global, with heightened CDC warnings in US following fatal Acanthamoeba cases | Short term (≤ 2 years) |

| Tolerability issues (irritation, epistaxis) limiting adherence | -1.9% | Universal; hypertonic solutions show 2.38x higher irritation risk vs. isotonic (Europe clinical data) | Medium term (2-4 years) |

| Availability of alternative intranasal therapies (steroids, antihistamines, decongestants) | -1.4% | Global, with high intranasal-corticosteroid penetration (USD 7.57 billion market) in North America and Europe | Medium term (2-4 years) |

| Cleaning/maintenance burden reducing long-term adherence | -1.0% | Universal; knowledge gaps (60% deficit on proper technique) more pronounced in Asia-Pacific and older demographics (≥50 years) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Improper Water Quality and Device Contamination Risks Trigger Safety Mandates

A 2023 fatality in New Mexico due to Acanthamoeba encephalitis linked to tap-water use in an electronic nasal irrigator heightened risk awareness, which prompted renewed emphasis on water safety for sinus rinsing. CDC guidance updated in 2025 states that users should choose distilled, sterile, or boiled-then-cooled water or apply specific disinfection steps before irrigation. The same organism risk framework extends to Naegleria fowleri, which has a very high case-fatality rate when tap water enters nasal passages and accesses the central nervous system.

Public-health instructions add preparation steps that may reduce short-term adherence among some users, which motivates device makers to include clear instructions and reminders inside packaging and apps. Recalls in related nasal-care products such as cotton swabs in 2025 further underscored the need for stringent manufacturing controls and validated cleaning protocols for components that contact mucosa.

Tolerability Issues Limit Adherence Despite Clinical Efficacy

Hypertonic saline shows stronger symptom relief and endoscopic improvements in clinical studies after endoscopic sinus surgery, although it also exhibits higher local irritation and more minor side effects than isotonic saline. The risk-benefit balance encourages surgeons to match solution tonicity to clinical goals, while providing counseling to reduce discontinuation due to discomfort. Real-world data show many patients report initial unpleasantness, although technique refinement leads the majority to continue past the first attempts, which suggests user education can reclaim a portion of those at risk of early dropout. Antiseptic solutions such as povidone-iodine may transiently increase nasal discomfort relative to saline yet have not shown serious safety signals in large trials, which supports careful patient selection and counseling on expected sensations. Budesonide irrigation maintains a favorable safety profile in pooled analyses, although user-dependent mixing and head-position variability can limit outcomes without hands-on coaching.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Squeeze Bottles Maintain Volume Leadership While Electric Systems Raise Performance Expectations

Squeeze bottles captured a 20.16% share in 2025, reflecting affordability, wide retail availability, and clinician familiarity in starter kits. Buyers value simple ergonomics and universal compatibility with premixed saline packets or home-mixed isotonic blends, which keeps entry barriers low for new users across the nasal irrigation market. Self-prepared isotonic solutions remain common for everyday hygiene, and premixed sachets reduce mixing errors in households that want predictable pH and tonicity. Manual bottle design has focused on grip, valve reliability, and one-handed operation to reduce learning curves for first-time users who may be apprehensive about discomfort. Specialty products like compressor-assisted nasal showers occupy a niche in European pharmacies where durable medical equipment is popular with ENT prescribers and outpatient clinics.

Electric and pulsatile systems are forecast to grow at a 21.19% CAGR through 2031 as they segment the user base with more personalization, pressure control, and integrated hygiene features. Flagship models advertise pulsation at 1,200 cycles per minute, variable speeds, and rinse-plus-suction flows designed to limit cross-pass contamination and reduce perceived effort. Designs now incorporate antimicrobial housings and self-clean cycles to reinforce confidence around contamination and cleaning routines, which addresses a central restraint. Safety innovation includes pressure-release valves that cap output to levels set to minimize epistaxis and barotrauma risk, answering one of the most cited tolerability concerns. Cordless, foldable, and IPX-rated devices expand usage into travel and work settings, which increases monthly active use days and supports replenishment cadence for saline packets.

By Technology: Manual Scale Persists, While Electric Gains from Batteries and Pressure Modulation

Manual technology held a 65.23% share in 2025, reflecting low device cost, near-universal saline compatibility, and broad placement across retail pharmacies and physician offices. Manual systems remain popular in early adoption because the learning curve is short, the price point is low, and results are visible, particularly during peak allergy seasons. As clinicians coach on temperature and head position, many users resolve early discomfort and continue use through pollen surges and cold seasons. Bottles increasingly feature removable, dishwasher-safe parts, which reduces routine cleaning barriers that can lead to drop-off in week two of new use.

Electric and battery-powered systems are projected to expand at a 20.15% CAGR through 2031, driven by lithium-polymer batteries, USB-C common charging, and microprocessor-controlled pressure profiles. Modern devices advertise multiple intensity levels for varied anatomy and sensitivity, alongside attached reservoirs that balance volume with portability. Rinse-and-suction functionality provides a differentiated experience that reduces time per session for busy users who still want thorough clearance. Pressure caps as low as 7 kPa aim to protect the middle ear and fragile mucosa, which underscores a safety-first approach in the emerging premium tier of the nasal irrigation industry. As these capabilities filter into mid-tier prices, the nasal irrigation market will see continued mix-shift toward electric platforms in both developed and fast-growing regions.

By Solution Type: Isotonic Leads, Hypertonic Serves Select Use Cases, Medicated Formulas Accelerate

Isotonic saline accounted for a 45.18% share in 2025, providing daily hygiene with low irritation and near-universal physician endorsement. Premixed sachets help users avoid common mixing errors and maintain pH balance, which improves comfort and adherence. Families and pregnant patients favor isotonic for routine hygiene due to gentleness, and pharmacists often recommend it for first-time users who are learning technique. Clinics also initiate isotonic irrigation in pre- and postoperative settings as a baseline before transitioning to adjunct protocols.

Hypertonic saline outperforms isotonic on specific clinical metrics after surgery, including symptom scores and endoscopic findings, while incurring higher local irritation and minor side effects. Surgeons guide usage windows for hypertonic to manage edema and mucus, and they counsel on expected transient discomfort that often resolves with correct temperature and head position[2]Adriano D. Lima et al., “Hypertonic Saline After FESS,” Brazilian Journal of Otorhinolaryngology, scienceopen.com.

Additive-enhanced solutions lead segment growth at a 20.69% CAGR, driven by xylitol, hypochlorous acid, povidone-iodine, and budesonide admixtures that convert lavage into a targeted therapy. Budesonide irrigation improves disease outcomes with a favorable safety profile in pooled studies, which increases clinician comfort with steroid admixtures in chronic care.

By Indication: Allergic Rhinitis Anchors Value While Chronic Rhinosinusitis Leads Growth

Allergic rhinitis held a 44.90% share in 2025 on the strength of broad prevalence and clear seasonal triggers that prompt retail and home purchases in the nasal irrigation market. Symptom flares in spring and fall increase daily irrigations per user, which supports recurring saline replenishment and reinforces long-term hygiene habits. Pharmacist coaching and clinic instructions address solution temperature and pH to limit stinging and epistaxis, which in turn reduces discontinuations during the first two weeks. As users gain familiarity, many maintain lower-frequency routines beyond peak seasons, which strengthens the installed base supporting the nasal irrigation market.

Chronic rhinosinusitis is projected to expand at a 21.18% CAGR through 2031, supported by guideline-driven care that emphasizes high-volume irrigation after surgery and, in many cases, corticosteroid admixing. Budesonide irrigation improves Sino-Nasal Outcome Test results without systemic steroid effects in pooled data, which underpins adoption in clinic-driven care plans. CRS patients show higher device-ownership rates and longer continuous usage after FESS, which elevates their lifetime value and supports premium device tiers. Clinics commonly dispense devices at the point of care, which improves technique and adherence in the first weeks at home.

By End User: Homecare Leads and Expands as Hospitals and Clinics Sustain Protocol-Driven Demand

Homecare accounted for 40.14% of total revenue in 2025 and is also the fastest-growing end user at a 20.16% CAGR, as consumers normalize lavage as part of hygiene routines and as digital fulfillment improves replenishment. Early-week adherence can be very high with instructions and coaching, and subscription prompts can help preserve routines beyond the second week, which grows the active user base. Knowledge gaps documented in recent surveys continue to narrow through pharmacist consultations and how-to content in retail and online channels, which helps sustain comfort. Rinse-plus-suction, antimicrobial housings, and self-clean cycles speak directly to at-home contamination anxieties, which supports continued growth in the nasal irrigation market.

Hospitals and ENT clinics maintain a combined minority share with high-value usage driven by protocols and hands-on coaching. Hospitals initiate high-volume irrigation within 24 hours after FESS in many cases, which stabilizes early adherence and accelerates healing. Clinics train on technique, head position, and solution selection, which improves outcomes in chronic rhinosinusitis and seasonal allergy management. These care settings often dispense devices directly, which improves adoption and reduces setup errors that can lead to early discontinuation. Together they reinforce long-term usage that flows back into homecare, reinforcing the installed base of the nasal irrigation market.

By Distribution Channel: Retail Pharmacies Hold the Line While E-Commerce Scales

Retail pharmacies held a 47.10% share in 2025, supported by pharmacist guidance that addresses gaps in solution preparation, device cleaning, and pediatric use. Seasonal displays and starter kits convert foot traffic during peak allergy months and cold seasons into trial and repeat purchase. In-person coaching raises comfort for first-time users who are wary of discomfort, which reduces week-one discontinuations in the nasal irrigation market.

E-commerce is projected to grow at a 21.03% CAGR through 2031, driven by direct-to-consumer models, auto-ship refills, and educational content that de-risks technique. Company sites highlight device differentiators like rinse-plus-suction, antimicrobial housings, and rechargeable batteries, supported by manuals and videos that close knowledge gaps. Brand sites and retail marketplaces emphasize verified reviews and how-to clips that turn awareness into purchase without pharmacy visits. These channel strengths grow the reach of the nasal irrigation market among younger digital-native buyers who value convenience and control.

Geography Analysis

North America held a 38.17% share in 2025, underpinned by a large burden of allergic disease and widespread clinician and pharmacist engagement with irrigation across acute and chronic use. Routine post-FESS irrigation protocols are entrenched in specialty care, which sustains device and consumables demand across hospitals, clinics, and home transitions[3]Centers for Disease Control and Prevention, “How to Safely Rinse Sinuses,” Centers for Disease Control and Prevention, cdc.gov. The region supports higher adoption of powered devices relative to other geographies due to disposable income and access to clinical coaching, which favors premium features like pulsation and self-clean cycles. Water-safety guidance is prominent and now common in device leaflets and web pages, which shapes behavior and maintains focus on sterile or boiled-then-cooled water.

Asia-Pacific is projected to expand at a 20.14% CAGR through 2031 as urbanization and air-quality factors increase symptom burdens that point users to daily hygiene routines. As middle-class purchasing power rises, mid-tier powered irrigators assembled locally increase accessibility without sacrificing pressure controls or antimicrobial features. Pharmacy and online channels are both active in educating first-time users with how-to content and refill subscriptions, which supports habitual use after initial trials. Cultural hygiene practices in select markets create a receptive base for device adoption, and clinical training in ENT centers spreads best practices into community settings in the nasal irrigation market.

Europe maintains steady growth as ENT societies and hospital protocols standardize high-volume irrigation after surgery and in chronic care. Compressor-assisted nasal showers hold niche positions in parts of Western Europe through established pharmacy channels that favor durable equipment, while home-based squeeze bottles and emerging electric devices broaden consumer choice. Clinical literature in 2024 and 2025 supports solution selection by balancing efficacy and tolerability, which guides patient counseling and sustains adherence for the nasal irrigation market.

Competitive Landscape

The nasal irrigation market features a mix of long-standing consumer-health brands, specialty device makers, and regional private labels. Device platforms span manual squeeze bottles to premium pulsatile systems with rinse-plus-suction, antimicrobial housings, and self-clean modes. In 2026, companies emphasize pressure safety, portability, and user education through manuals and video content to improve adherence from week one to week two and beyond. Manufacturers also align product instructions with CDC guidance, which improves water-safety compliance and addresses contamination concerns.

Strategic moves in 2025-2026 highlight portfolio refinement and product innovation. Church & Dwight executed a recall of nasal and teething swabs due to potential microbial contamination to safeguard patient safety while emphasizing unaffected product lines, which reflects stringent quality oversight across related categories. The company also announced divestitures of select non-core businesses to sharpen focus and mitigate tariff exposure while continuing to grow key brands internationally. Meanwhile, RhinoSystems extended its consumable line with Daytime and Nighttime SaltPods with essential oils, which increases the attach rate of proprietary refills for powered systems.

Corporate social responsibility and consumer trust remain important in this category. In January 2025, NeilMed donated Sinus Rinse units to first responders fighting wildfires, which drew attention to nasal hygiene benefits in smoke exposure and reinforced brand recognition among frontline workers. RhinoSystems earned a baby-product award for its nasal aspirator, which showcased features such as gentle suction, rechargeable power, and anti-backflow protections that matter for pediatric safety. Across companies, user education, water safety, and ease-of-use improvements are core to competitive differentiation in the nasal irrigation market.

Nasal Irrigation Industry Leaders

Church & Dwight Co., Inc.

Flaem Nuova S.p.A.

Health Solutions Medical Products Corp. (SinuPulse)

NeilMed Pharmaceuticals, Inc.

RhinoSystems, Inc. (Navage)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: VMED proudly unveiled its Nasal Irrigation Device at WHX Dubai 2026, showcasing an innovative solution for respiratory health. This launch marks the beginning of VMED's global expansion into key markets, including the GCC (UAE, Saudi Arabia, Qatar, Kuwait, Bahrain, Oman), Africa (major healthcare markets across the continent), and Europe (Western and Eastern European countries). The device features clinically validated nasal irrigation technology, a user-friendly design for daily use, effective relief from sinus congestion and allergies, medical-grade materials safe for all ages, and a portable, travel-friendly build. Regular use of the device offers significant health benefits, such as clearing nasal passages, reducing allergy symptoms, and improving breathing and sleep quality.

- January 2025: NeilMed Pharmaceuticals announced unlimited complimentary Sinus Rinse product donations to first responders combating Los Angeles wildfires, partnering with fire departments and EMS organizations across California to alleviate nasal discomfort from smoke and airborne pollutants. The initiative extends NeilMed's history of supporting emergency personnel during 9/11 and prior California fires, reinforcing its #1 physician-recommended positioning cultivated over 25+ years.

Global Nasal Irrigation Market Report Scope

As per the scope of the report, nasal irrigation, a safe and effective practice, involves using a saline solution (saltwater) to clear mucus, allergens, irritants, and bacteria from the nasal passages. This low-risk method provides relief from congestion associated with colds, allergies, and sinus infections. Commonly used tools for this procedure include neti pots, squeeze bottles, and syringes, making it a practical solution for managing nasal health. The nasal irrigation market is segmented by product type, technology, solution type, indication, end user, distribution channel, and geography. By product type, the market is segmented as neti pots, squeeze bottles (positive‑pressure LVLP), syringes/bulb syringes, powered/pulsatile/electric systems, and nasal douches/showers (compressor‑assisted). By technology, the market is segmented as manual and electric/battery‑powered. By solution type, the market is segmented as isotonic saline, hypertonic saline, and additive‑enhanced (e.g., xylitol, povidone‑iodine, HOCl, corticosteroid admixture per Rx). By indication, the market is segmented as chronic rhinosinusitis (with/without polyps), allergic rhinitis, upper respiratory infection/cold & flu, and post‑operative ENT care (post‑FESS/septoplasty). By end user, the market is segmented as homecare, hospitals, and ENT/allergy clinics. By distribution channel, the market is segmented as retail pharmacies/drugstores, e‑commerce/direct‑to‑consumer, and hospital/clinic pharmacies & B2B. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle-East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Neti Pots |

| Squeeze Bottles (positive‑pressure LVLP) |

| Syringes/Bulb Syringes |

| Powered/Pulsatile/Electric Systems |

| Nasal Douches/Showers (compressor‑assisted) |

| Manual |

| Electric/Battery‑Powered |

| Isotonic Saline |

| Hypertonic Saline |

| Additive‑enhanced (e.g., xylitol, povidone‑iodine, HOCl, corticosteroid admixture per Rx) |

| Chronic Rhinosinusitis (with/without polyps) |

| Allergic Rhinitis |

| Upper Respiratory Infection/Cold & Flu |

| Post‑operative ENT Care (post‑FESS/septoplasty) |

| Homecare |

| Hospitals |

| ENT/Allergy Clinics |

| Retail Pharmacies/Drugstores |

| E‑commerce/Direct‑to‑Consumer |

| Hospital/Clinic Pharmacies & B2B |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Neti Pots | |

| Squeeze Bottles (positive‑pressure LVLP) | ||

| Syringes/Bulb Syringes | ||

| Powered/Pulsatile/Electric Systems | ||

| Nasal Douches/Showers (compressor‑assisted) | ||

| By Technology | Manual | |

| Electric/Battery‑Powered | ||

| By Solution Type | Isotonic Saline | |

| Hypertonic Saline | ||

| Additive‑enhanced (e.g., xylitol, povidone‑iodine, HOCl, corticosteroid admixture per Rx) | ||

| By Indication | Chronic Rhinosinusitis (with/without polyps) | |

| Allergic Rhinitis | ||

| Upper Respiratory Infection/Cold & Flu | ||

| Post‑operative ENT Care (post‑FESS/septoplasty) | ||

| By End User | Homecare | |

| Hospitals | ||

| ENT/Allergy Clinics | ||

| By Distribution Channel | Retail Pharmacies/Drugstores | |

| E‑commerce/Direct‑to‑Consumer | ||

| Hospital/Clinic Pharmacies & B2B | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the nasal irrigation market growth outlook to 2031?

The nasal irrigation market is projected to reach USD 1.14 billion by 2031 from USD 0.50 billion in 2026, registering an 18.17% CAGR over 2026-2031.

Which product types lead demand in the nasal irrigation market today?

Manual squeeze bottles lead with a 20.16% share in 2025 due to affordability and clinician familiarity, while powered or pulsatile systems are the fastest-growing on the back of pressure control and convenience features.

How do clinical guidelines affect the nasal irrigation market?

ENT protocols frequently initiate irrigation within 24 hours after endoscopic sinus surgery and pooled evidence supports budesonide irrigation benefits, which stabilizes device and consumable adoption.

Which regions are set to expand fastest in the nasal irrigation market?

Asia-Pacific is projected to post the fastest growth with a 20.14% CAGR, supported by rising disposable incomes, urbanization, and accessible mid-tier electric devices produced locally.

What are the main safety considerations for sinus rinsing in the nasal irrigation market?

CDC guidance requires distilled, sterile, or boiled-then-cooled water for safe sinus rinsing, and manufacturers increasingly reflect these rules in instructions and product design.

Which end user category is growing fastest in the nasal irrigation market?

Homecare is both the largest and fastest-growing end user, with a 40.14% share in 2025 and a 20.16% CAGR through 2031, supported by self-care preferences and refill subscriptions.

Page last updated on: