Rhinoplasty Implants Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

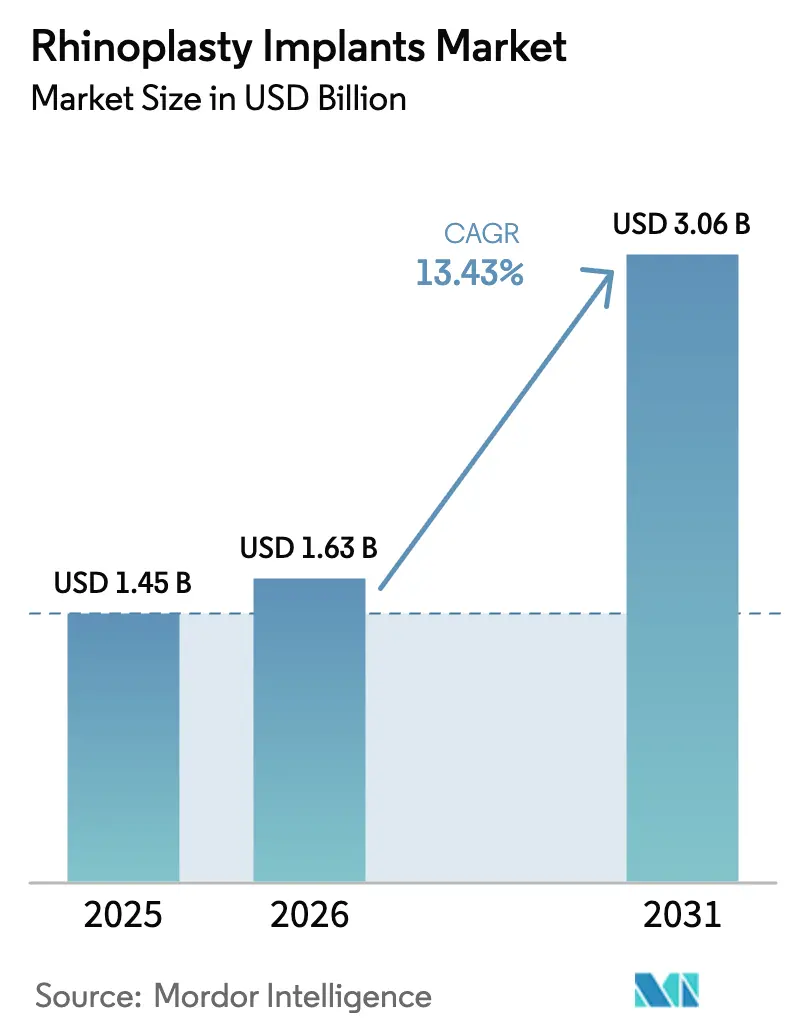

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 3.06 Billion |

| Growth Rate (2026 - 2031) | 13.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rhinoplasty Implants Market Analysis by Mordor Intelligence

Rhinoplasty Implants Market size in 2026 is estimated at USD 1.63 billion, growing from 2025 value of USD 1.45 billion with projections showing USD 3.06 billion, growing at 13.43% CAGR over 2026-2031.

Growth is tied to rising cosmetic volumes, especially a 2% year-over-year jump in United States procedures in 2024, and to rapid adoption of 3D-printed, patient-specific devices that shorten operating time and cut revision risk. Demand in Asia-Pacific is accelerating on the back of medical tourism and higher disposable income, while bioresorbable scaffolds promise to reduce long-term complications and reshape supplier portfolios. Parallel investment in imaging software, ultrasonic bone-sculpting tools, and streamlined ASC workflows is widening the technology gap between high-volume centers and smaller clinics. Regulatory delays in the European Union and tariff pressures in North America have pushed manufacturers toward dual sourcing and near-shoring, but these hurdles are also filtering out low-quality competitors, leaving established players with room to expand premium lines.

Key Report Takeaways

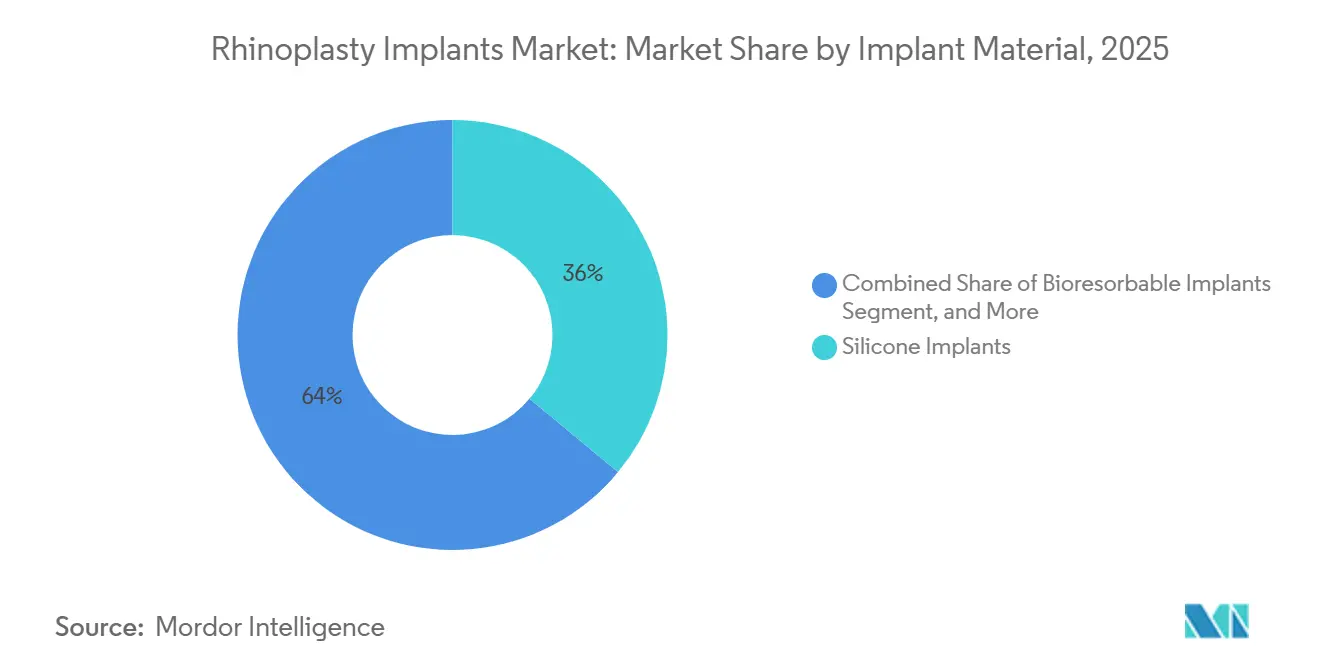

- By implant material, silicone implants captured 36.01% of the rhinoplasty implants market share in 2025, whereas bioresorbable implants are forecast to post the fastest 14.45% CAGR through 2031.

- By procedure type, augmentation rhinoplasty led procedure volumes with a 41.93% share in 2025; revision rhinoplasty is projected to record the highest 15.87% CAGR to 2031.

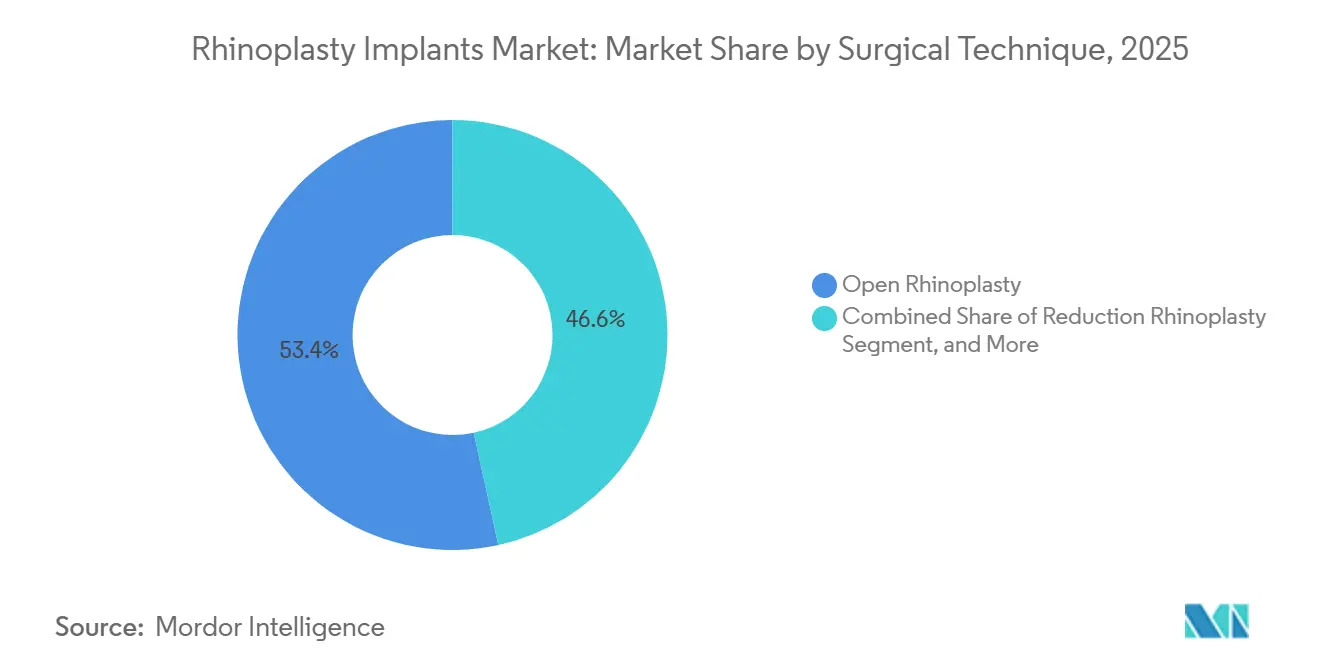

- By surgical technique, open rhinoplasty accounted for 53.42% of surgical technique revenue in 2025, while preservation techniques are set to expand at a 19.76% CAGR over the same period.

- By end user, hospitals commanded 61.63% of end-user revenue in 2025; ambulatory surgical centers are anticipated to register a 16.86% CAGR through 2031.

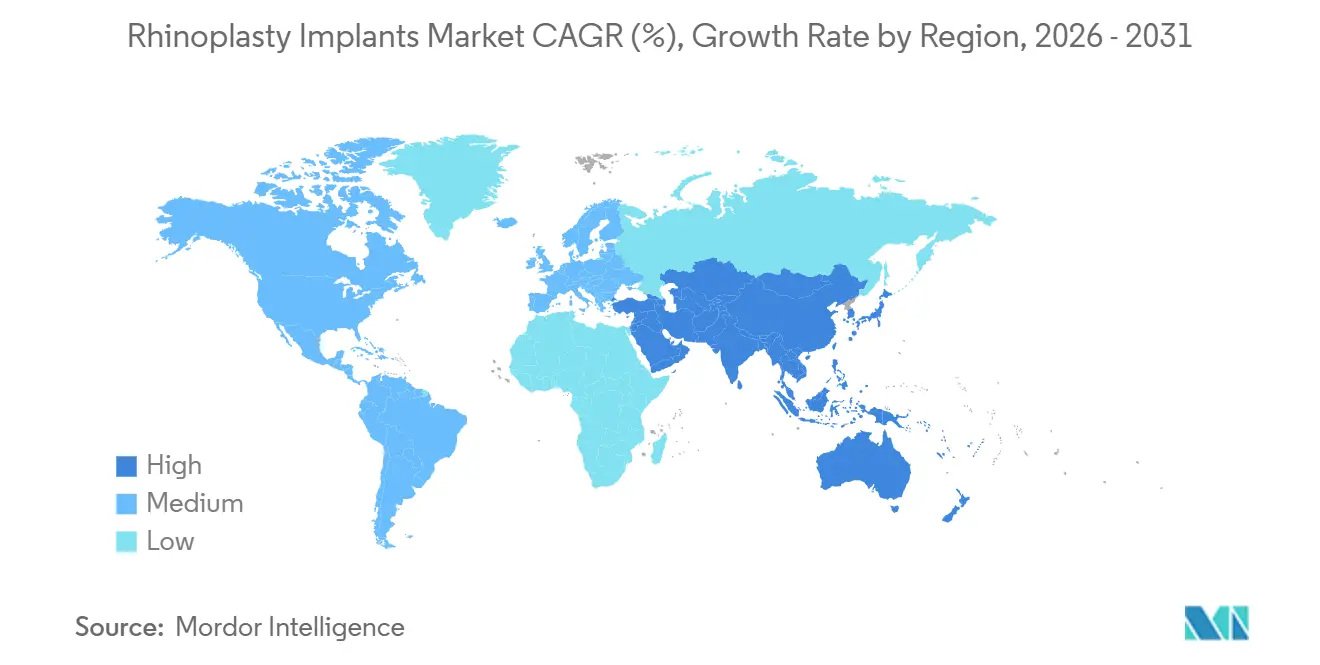

- By geography, North America accounted for 36.29% of global sales in 2024; Asia-Pacific is expected to deliver the fastest CAGR of 20.94% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rhinoplasty Implants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Cosmetic Rhinoplasty Demand | +3.2% | Global, with peak intensity in North America, South Korea, Brazil | Medium term (2-4 years) |

| Technological Advances in 3D Imaging & Patient-Specific Implants | +2.8% | North America & EU core, spill-over to APAC tier-1 cities | Long term (≥ 4 years) |

| Growing Nasal Trauma & Congenital Deformity Cases | +2.1% | Global, elevated in MEA conflict zones, South Asia road-trauma hotspots | Short term (≤ 2 years) |

| Rise of Minimally-Invasive Preservation Techniques | +2.5% | North America & EU early adopters, gradual APAC diffusion | Medium term (2-4 years) |

| Emergence of Bioabsorbable & 3D-Printed Implants | +1.9% | North America & EU regulatory-compliant markets, limited APAC penetration | Long term (≥ 4 years) |

| Near-Shoring to Offset 2025-26 Device Tariffs | +1.0% | North America (US, Canada, Mexico), partial EU benefit | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Cosmetic Rhinoplasty Demand

Social media exposure and normalized discussion of facial surgery are driving a steady increase in adult rhinoplasty volumes. United States procedures rose to 48,423 in 2024, with notable growth among patients aged 40 and older.[1]American Society of Plastic Surgeons, “Americans Spent More Than USD 28 Billion on Cosmetic Plastic Surgery in 2024,” plasticsurgery.org Medical tourism corridors in Indonesia and South Korea report double-digit growth as international patients seek lower prices without compromising implant quality. Competitive pricing in Southeast Asia averages USD 7,500 per case, about half the typical U.S. fee, creating fresh demand for premium yet affordable silicone and ePTFE implants. Manufacturers are reacting with tiered product lines that balance cost and brand equity. The uptick in older demographics also favors implants with proven safety records, reinforcing silicone’s current lead.

Technological Advances in 3D Imaging and Patient-Specific Implants

Routine use of CT scans and CAD software is moving the specialty toward precision engineering. Surgeons can order implants made of porous polyethylene or silicone that replicate individual anatomy, reducing trial-and-error and shortening anesthesia time.[2]JAMA Facial Plastic Surgery, “3D-Printed Patient-Specific Implants in Rhinoplasty: A Systematic Review,” jamanetwork.com A 2024 review found dorsal symmetry scores 18% higher when 3D-printed guides were used compared with freehand shaping. Capital costs exceed USD 500,000 for scanners, printers, and software, so uptake is highest in academic hospitals and top-tier ASCs. These facilities can command premium pricing, opening a profitability gap over clinics that rely on commodity implants. In response, large suppliers are partnering with bioprinting firms to scale patient-specific production and secure long-term contracts with high-volume centers.

Growing Nasal Trauma and Congenital Deformity Cases

Traffic accidents, interpersonal violence, and congenital anomalies continue to fuel reconstructive demand. Nasal fractures account for 40% of facial bone injuries, and a subset needs implant-based repair when autologous cartilage is inadequate. Conflict-affected regions in North Africa and the Middle East report rising trauma admissions, while South Asia sees elevated injury rates tied to rapid motorization. Reconstructive patients are less price-sensitive than elective cosmetic clients, supporting steady sales even during economic downturns. Hospitals favor porous polyethylene or titanium for these complex cases, giving manufacturers diversified revenue streams that offset cyclical cosmetic demand.

Rise of Minimally Invasive Preservation Techniques

Preservation rhinoplasty maintains the native dorsal vault, reducing postoperative swelling and enabling faster recovery. A 2025 study showed mean healing times shortened by nine days compared with traditional osteotomies. Adoption depends on high-resolution imaging and ultrasonic bone-sculpting tools, driving capital spending of USD 30,000-50,000 per unit. Younger surgeons trained in the last decade favor the technique, making it a key selling point for silicone implants with pre-contoured dorsal shapes. Early adopters are concentrated in North America and Western Europe, but spillover into tier-one Asian cities is expected as training fellowships expand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure & Implant Costs | -2.3% | Global, most acute in price-sensitive APAC and Latin America markets | Medium term (2-4 years) |

| Post-Operative Complication & Litigation Risk | -1.8% | North America & EU high-litigation environments, moderate APAC exposure | Short term (≤ 2 years) |

| Diverging Global Regulatory Pathways | -1.2% | Global, peak friction at US-EU-China regulatory interfaces | Long term (≥ 4 years) |

| Non-Surgical Fillers & Threads Cannibalizing Volumes | -2.0% | North America, EU, South Korea early-adopter markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure and Implant Costs

Total cosmetic rhinoplasty fees range from USD 7,500 in Southeast Asia to USD 15,000 in the United States, limiting access for middle-income households. Premium, patient-specific implants can add USD 2,500 to baseline costs, while reimbursement for hybrid functional-cosmetic procedures remains inconsistent. Latin American and South Asian consumers face a four-to-six-fold gap in disposable income compared with North America, curbing uptake despite strong interest. Price compression in commodity silicone segments squeezes margins and deters R&D spending. Manufacturers are deploying dual-tier portfolios to protect profitability, but encounter resistance from surgeons who prioritize proven materials over new, higher-priced options.

Non-Surgical Fillers and Threads Cannibalizing Volumes

Hyaluronic-acid fillers and PDO threads cost USD 800-2,000 and involve minimal downtime, appealing to younger users seeking subtle changes. A 2024 Chinese study reported a 92% satisfaction rate one year after non-surgical rhinoplasty, with mainly transient side effects.[3]Aesthetic Surgery Journal, “Non-Surgical Rhinoplasty: A Retrospective Study of 2,088 Cases,” academic.oup.com These alternatives captured 15-20% of cosmetic nasal-contouring demand in 2025, rising to 28% in South Korea. Although effects fade within 18 months, repeat treatments create a steady income stream for dermatologists, delaying some patients’ move to surgical solutions. Implant vendors counter by underscoring permanence and structural support, but face longer decision cycles and must invest more in patient education.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Implant Material: Silicone Dominance Meets Bioresorbable Disruption

Silicone accounted for 36.01% of the rhinoplasty implants market in 2025, reflecting low unit cost, decades of clinical data, and straightforward intraoperative handling. A 30-year longitudinal review confirmed shorter insertion time and comparable complication rates compared with autologous grafts. The rhinoplasty implants market size for silicone is expected to grow steadily, even as newer options emerge. However, bioresorbable implants are forecast to expand at a 14.45% CAGR, buoyed by surgeon interest in eliminating permanent foreign materials. Early clinical data show extrusion rates below 5%, almost half that reported for silicone.

ePTFE occupies a middle ground, offering tissue-integration benefits but commanding USD 800-1,200 per unit, limiting uptake to revision or high-end cosmetic practices. Porous polyethylene meets reconstructive needs through vascular ingrowth, though shaping challenges and infection risk limit its wider use. Titanium and cadaveric cartilage form a small specialty segment used when rigid structural support outweighs cost concerns. As younger surgeons gravitate toward 3D-printed and bioresorbable solutions, silicone suppliers are launching textured surfaces and hybrid designs to maintain loyalty. This interplay of familiarity and innovation keeps competition active across all material categories.

By Procedure Type: Augmentation Leads, Revision Surges

Augmentation rhinoplasty accounted for 41.93% of the market in 2025, driven by demand in East Asian markets, where higher nasal bridges are considered desirable. Implant costs are moderate, and surgical time is shorter than in reduction cases, sustaining volume. The rhinoplasty implants market size for augmentation is projected to continue rising, though at a slower pace, as the segment matures. Revision procedures, meanwhile, are projected to grow at a 15.87% CAGR, reflecting 10-15% dissatisfaction or complication rates after primary surgery. These cases are resource-intensive and yield higher surgeon fees, creating a premium niche.

Reduction rhinoplasty grows modestly as fillers address minor dorsal humps without osteotomies. Reconstructive procedures remain stable, supported by insurance coverage for trauma and congenital defects. Secondary interventions often require advanced implants such as patient-specific porous polyethylene or bioresorbable struts, giving device makers an opportunity to cross-sell imaging and planning software. The revision boom underscores the need for implants with precise geometries and proven long-term safety.

By Surgical Technique: Preservation Methods Gain Momentum

Open rhinoplasty accounted for 53.42% of revenue in 2025, favored for complex cases that need direct visualization. Surgeons value its versatility, and patients accept minor external scars that usually fade within months. The rhinoplasty implants market share linked to open procedures remains high, yet preservation approaches are rising at a 19.76% CAGR. Evidence shows reduced edema and a shorter recovery by 9 days compared with traditional osteotomies.

Closed rhinoplasty, performed through endonasal incisions, is suitable for straightforward cosmetic adjustments, offering a 15-20-minute shorter operative time. Diffusion of preservation techniques is fastest among recently trained surgeons in North America and Western Europe, while Asia-Pacific and Latin America still rely heavily on open methods. Equipment costs and learning curves limit adoption in smaller centers, creating a two-speed market where premium implants serve preservation specialists and lower-priced options cater to traditional practitioners.

By End User: ASCs Challenge Hospital Dominance

Hospitals captured 61.63% of revenue in 2025, thanks to complex reconstructive workloads, comprehensive accreditation, and integrated intensive-care support. Academic centers introduce fellows to the latest implants, reinforcing brand familiarity. In contrast, ambulatory surgical centers are projected to grow at a 16.86% CAGR, benefiting from costs 30-40% lower than hospital settings and faster case turnover. The rhinoplasty implants market size tied to ASCs is poised for rapid expansion as payers steer elective cases toward lower-cost venues.

ENT and plastic-surgery clinics form a hybrid segment for minor revisions under local anesthesia. Their fragmented purchasing favors suppliers that offer small-lot shipments and flexible inventory. The shift toward outpatient settings is forcing manufacturers to develop compact, sterile packaging and just-in-time logistics. While ASC accreditation can vary, payer incentives and patient convenience continue to reinforce the migration away from hospitals.

Geography Analysis

North America accounted for 36.29% of global sales in 2024, driven by high per-capita spending, a well-established cosmetic culture, and favorable reimbursement for reconstructive cases. United States volume reached 48,423 procedures in 2024, though primary growth is leveling off while non-surgical alternatives are drawing some demand. Canada and Mexico post faster gains thanks to medical tourism and near-shoring, which lower lead times. Strict FDA pathways safeguard product quality but lengthen approval timelines, reinforcing the advantage of established brands.

Europe shows a patchwork of regulatory and market conditions. Germany, the United Kingdom, France, Italy, and Spain account for a significant portion of regional demand, but the Medical Device Regulation has added 12-18 months to approval cycles and raised compliance costs by 25%. Brexit compounds complexity with separate UKCA marking. Despite hurdles, Europe pioneers preservation rhinoplasty and bioresorbable scaffolds in academic centers, positioning the region as a technology incubator.

Asia-Pacific is forecast for the fastest 20.94% CAGR through 2031, propelled by China’s medical aesthetics boom from RMB 311.5 billion in 2023 to a forecast RMB 1.3 trillion in 2030. South Korea attracts 22% of its medical tourists from China, maintaining premium pricing. India’s procedures cost one-third as much as the U.S. and benefit from streamlined visa policies. Indonesia’s 21% growth in procedures in 2024 underscores tourism’s role in redistributing volume. Japan and Australia grow more slowly but serve as early adopters of 3D-printed and bioresorbable implants.

The Middle East and Africa combine affluent elective demand in the GCC with reconstructive needs in conflict zones. South Africa offers Western-trained surgeons at lower price points, drawing regional patients. South America leverages Brazil’s long cosmetic history and Argentina’s currency advantage, with both markets favoring silicone for cost but gradually adopting preservation techniques in urban centers. Currency fluctuations and import duties remain key variables that manufacturers must monitor closely.

Competitive Landscape

The rhinoplasty implants industry remains moderately fragmented. Each is investing in 3D-printing partnerships and bioresorbable R&D to sustain share. Integra’s 2024 acquisition of a bioprinting platform underscores this pivot, with the goal of commercializing patient-specific cartilage scaffolds by 2026.

Vertical integration is spreading as firms purchase sterilization and packaging assets to shield against tariff and logistics shocks. W.L. Gore retains a defensible moat through its ePTFE patents, securing loyalty among revision specialists. Regional challengers, especially Wanhe Plastic Materials, leverage lower labor costs to sell discounted silicone implants in Asia-Pacific, compelling incumbents to compete on service quality rather than price.

White-space opportunities include ASC-optimized kits that bundle implants with single-use instruments. Suppliers able to guarantee three-week delivery windows to U.S. centers gain an edge under just-in-time inventory models. Strategic distribution agreements in Brazil and South Korea illustrate geographic tailoring: Zimmer Biomet’s 2025 partnership with a South Korean distributor aims to deepen penetration among preservation-trained surgeons.

Rhinoplasty Implants Industry Leaders

W. L. Gore & Associates

Establishment Labs

B. Braun Melsungen AG

GC Aesthetics plc

Integra LifeSciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Shoulder Innovations partnered with Interventional Systems to introduce a micro-robotic platform that improves precision in facial and shoulder surgery.

- November 2025: W&H Medical launched an FDA-cleared Piezo & Drill Combination Console designed for rhinoplasty and craniofacial procedures.

- June 2025: Lyra Therapeutics announced positive Phase 3 ENLIGHTEN 2 data for LYR-210 in chronic rhinosinusitis, supporting adjunctive applications in nasal surgery.

- April 2024: Integra LifeSciences acquired a bioprinting technology platform for USD 85 million to accelerate the commercial rollout of patient-specific nasal scaffolds.

Global Rhinoplasty Implants Market Report Scope

The Rhinoplasty Implants Market refers to the global industry focused on the development, production, and distribution of implants used in surgical and non-surgical rhinoplasty procedures, primarily for aesthetic enhancement or functional nasal reconstruction. It encompasses products, technologies, and services that support nasal reshaping, augmentation, and correction.

The Rhinoplasty Implants Market Report is Segmented by Implant Material (Silicone, ePTFE, Porous Polyethylene, Bioresorbable, Others), Procedure Type (Augmentation, Reduction, Revision, Other), Surgical Technique (Open, Closed, Preservation), End User (Hospitals, ASCs, Clinics), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

| Silicone Implants |

| ePTFE (Gore-Tex) Implants |

| Porous Polyethylene Implants |

| Bioresorbable Implants |

| Others (Titanium Implants, Cadaveric / Allograft Cartilage, etc.) |

| Augmentation Rhinoplasty |

| Reduction Rhinoplasty |

| Revision / Secondary Rhinoplasty |

| Other Procedure Types (Reconstructive, Filler / Non-Surgical Implants, etc.) |

| Open Rhinoplasty |

| Closed Rhinoplasty |

| Preservation / Minimal-Invasive |

| Hospitals |

| Ambulatory Surgical Centers |

| ENT & Plastic-Surgery Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Implant Material | Silicone Implants | |

| ePTFE (Gore-Tex) Implants | ||

| Porous Polyethylene Implants | ||

| Bioresorbable Implants | ||

| Others (Titanium Implants, Cadaveric / Allograft Cartilage, etc.) | ||

| By Procedure Type | Augmentation Rhinoplasty | |

| Reduction Rhinoplasty | ||

| Revision / Secondary Rhinoplasty | ||

| Other Procedure Types (Reconstructive, Filler / Non-Surgical Implants, etc.) | ||

| By Surgical Technique | Open Rhinoplasty | |

| Closed Rhinoplasty | ||

| Preservation / Minimal-Invasive | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| ENT & Plastic-Surgery Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the rhinoplasty implants market in 2026?

The rhinoplasty implants market size reached USD 1.63 billion in 2026.

What is the expected CAGR through 2031?

The market is forecast to expand at a 13.43% CAGR between 2026 and 2031.

Which implant material is growing the fastest?

Bioresorbable implants are projected for a 14.45% CAGR thanks to lower long-term complication risk.

Why are ambulatory surgical centers important for suppliers?

ASCs offer 30-40% lower procedure costs and are forecast for a 16.86% CAGR, creating demand for streamlined, pre-sterilized implant kits.

Which region will post the quickest growth?

Asia-Pacific is expected to achieve a 20.94% CAGR through 2031, led by China, South Korea, and Indonesia.

Page last updated on: