High-flow Nasal Cannula Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

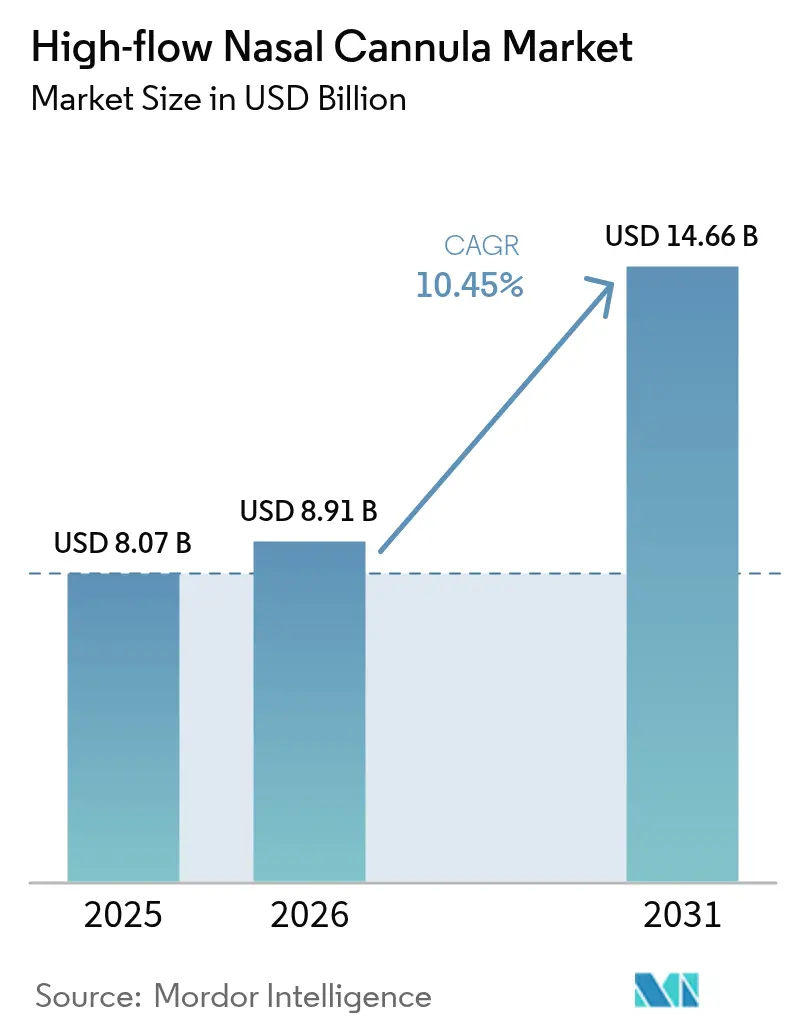

| Market Size (2026) | USD 8.91 Billion |

| Market Size (2031) | USD 14.66 Billion |

| Growth Rate (2026 - 2031) | 10.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-flow Nasal Cannula Market Analysis by Mordor Intelligence

The high-flow nasal cannula market size was valued at USD 8.07 billion in 2025 and estimated to grow from USD 8.91 billion in 2026 to reach USD 14.66 billion by 2031, at a CAGR of 10.45% during the forecast period (2026-2031). Growth is propelled by the widening adoption of heated, humidified high-flow oxygen therapy that reduces intubation rates, shortens hospital stays, and improves patient comfort. Expanding clinical evidence in chronic obstructive pulmonary disease (COPD), bronchiolitis, and peri-operative care is broadening the high-flow nasal cannula market across hospital, emergency, and home-care environments. Increasing prevalence of respiratory illnesses—COPD affects 200 million people and caused 3.2 million deaths in 2024—continues to push demand firsnet.org. Rapid device innovation in integrated flow monitoring, coupled with tele-respiratory platforms, strengthens the value proposition for providers while lowering total cost of care. At the same time, infection-control learning from recent pandemics accelerates preference for non-invasive gas delivery systems that minimize aerosol dispersion.

Key Report Takeaways

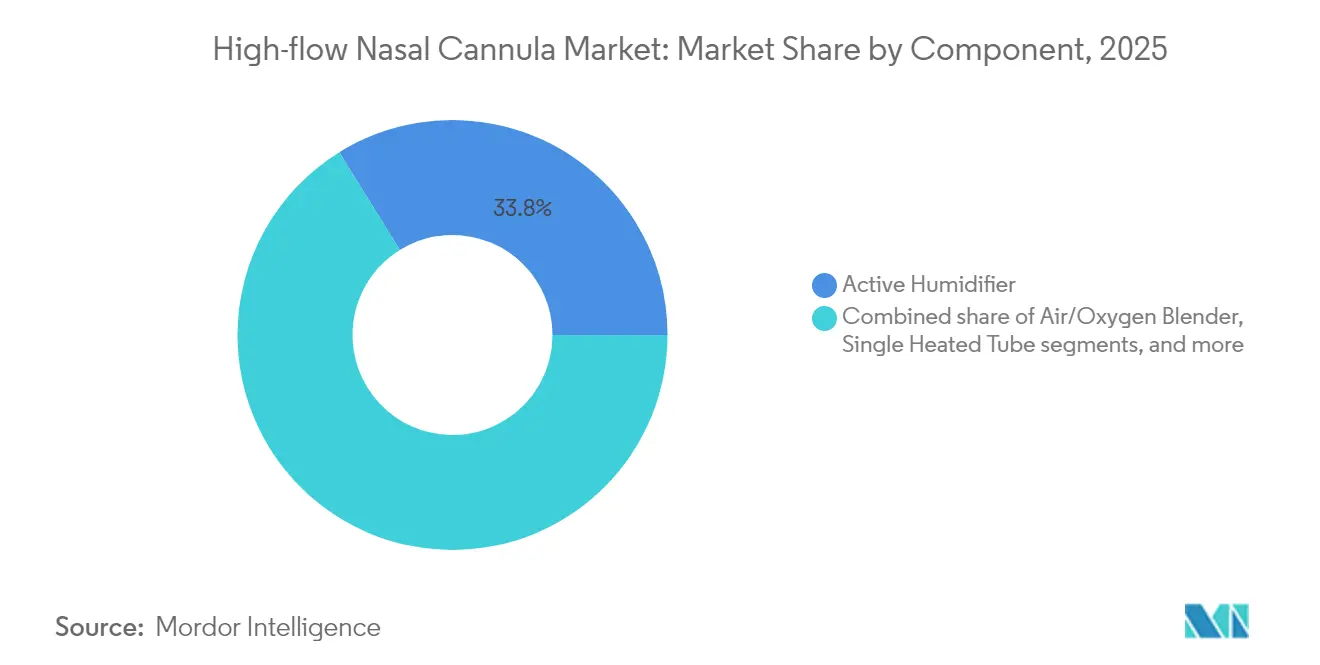

- By component, active humidifiers led with 33.82% of the high-flow nasal cannula market share in 2025, whereas nasal cannula components are forecast to advance at a 13.33% CAGR through 2031.

- By end-user, hospitals & intensive care units held 47.30% revenue share in 2025; Home-care Settings exhibit the fastest projected CAGR at 12.57% between 2026-2031.

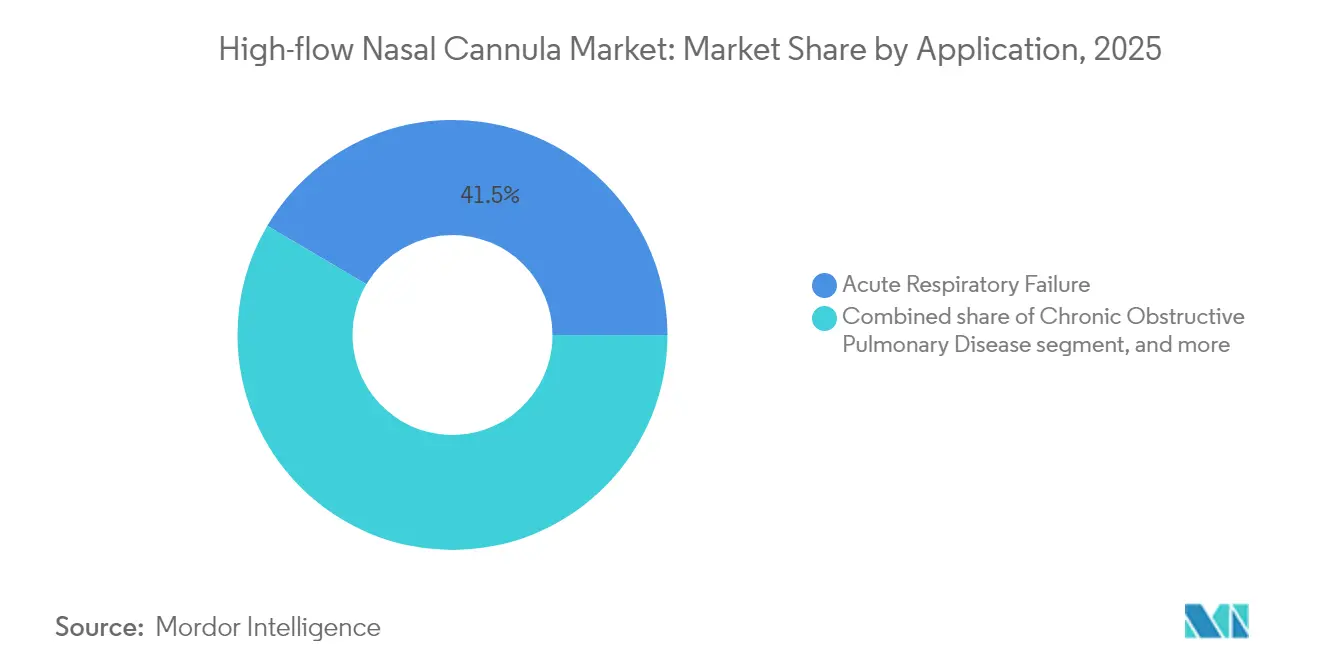

- By application, acute respiratory failure accounted for a 41.52% slice of the high-flow nasal cannula market size in 2025, while COPD applications are anticipated to grow at 11.23% CAGR to 2031.

- By patient age group, adults (18-64 yrs) comprised 58.40% of the high-flow nasal cannula market share in 2025; the geriatric segment is poised for a 10.21% CAGR from 2026-2031.

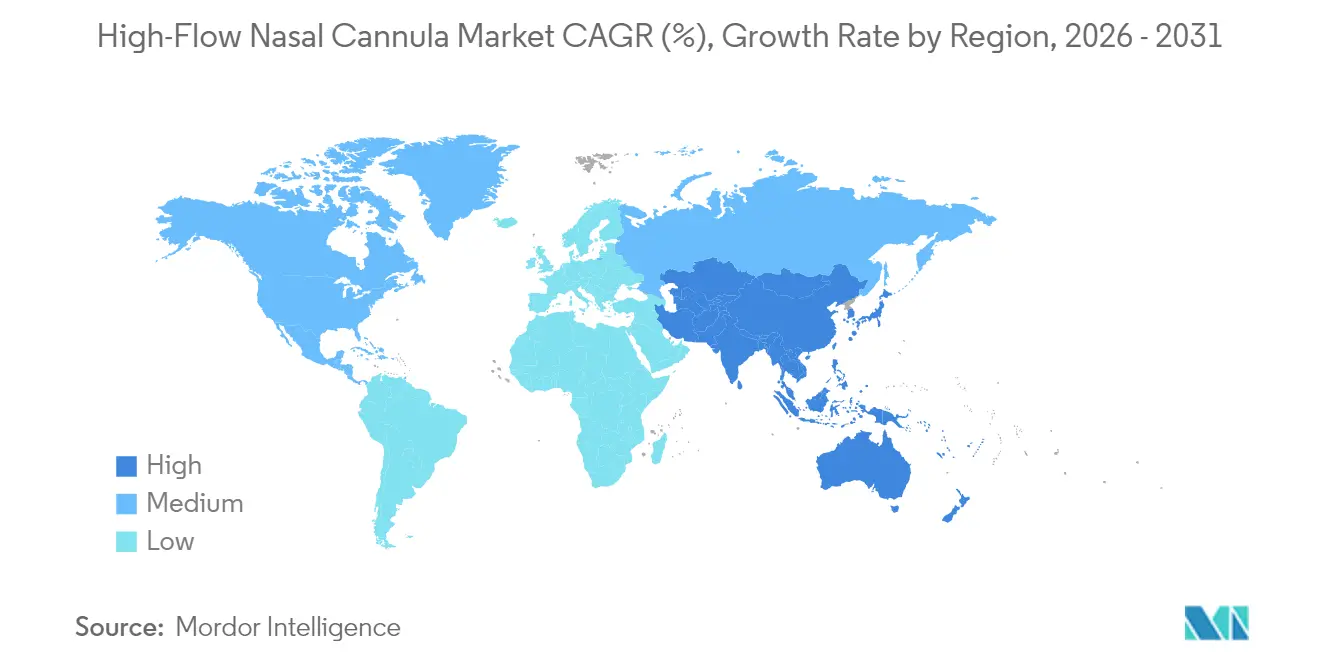

- By geography, North America commanded 37.45% of global revenue in 2025; Asia Pacific is predicted to register an 10.86% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-flow Nasal Cannula Market Trends and Insights

Driver Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global prevalence of acute & chronic respiratory diseases | +2.0% | Global | Long term (≥ 4 years) |

| Technological advancements in heated humidification & integrated flow monitoring | +2.0% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Expanding applications of HFNC beyond ICU into emergency & peri-operative settings | +1.0% | North America, Europe | Short term (≤ 2 years) |

| Growing adoption of home-based oxygen therapy & tele-respiratory care | +3.0% | North America, Asia Pacific | Long term (≥ 4 years) |

| Favorable reimbursement & clinical guidelines supporting non-invasive oxygenation | +1.0% | North America, Europe | Medium term (2-4 years) |

| Increase in pre-term birth rates necessitating neonatal HFNC | +1.0% | Asia Pacific, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Acute & Chronic Respiratory Diseases

The burden of COPD, which affected 200 million people and caused 3.2 million deaths in 2024, is pushing clinicians to escalate beyond conventional oxygen delivery methods[1]Forum of International Respiratory Societies, “The Global Impact of Respiratory Disease 2024,” firsnet.org. Asthma cases exceeded 350 million worldwide, while seasonal influenza remained the most detected pathogen in northern hemisphere surveillance. These epidemiological pressures have elevated demand for high-flow therapy that lowers readmissions and improves health-related quality-of-life scores, positioning the high-flow nasal cannula market as an essential pillar of modern respiratory care.

Technological Advancements in Heated Humidification & Integrated Flow Monitoring

Bench studies comparing leading devices showed that AIRVO 2, bellavista 1000, and HUMID-BH delivered closer to nominal dew-point at 37 °C, enhancing mucosal protection and secretion clearance[2]Frontiers in Medicine, “Comparative Bench Evaluation of Four High-Flow Nasal Cannula Systems,” frontiersin.org. Computational fluid-dynamics modeling confirmed that optimized cannula geometry supports near-100% relative humidity in the nasopharynx, limiting airway obstruction. These innovations allow real-time titration of flow and FiO₂, extend therapy beyond ICU walls, and differentiate offerings within the high-flow nasal cannula market.

Expanding Applications of HFNC Beyond ICU into Emergency & Peri-operative Settings

A 1,000-patient randomized trial in sedated gastrointestinal endoscopy reduced hypoxia from 21.2% to 2.0% using HFNC, eliminating severe events. In emergency rooms, HFNC improves comfort and shows a downward trend in admission rates versus conventional oxygen. Peri-operatively, interim NOTACS data suggest lower pulmonary complications and shorter stays after cardiac surgery. Such evidence widens addressable demand, bolstering the high-flow nasal cannula market.

Growing Adoption of Home-based Oxygen Therapy & Tele-respiratory Care

Home HFNC in severe COPD patients cut exacerbations by 1.40 events and avoided 0.96 hospital admissions annually. Integration with cloud dashboards enables clinicians to adjust flow remotely, aligning with value-based care incentives. Early discharge protocols for preterm infants on domiciliary HFNC demonstrate extended reach into pediatric long-term support. Collectively, these developments open a lucrative frontier for the high-flow nasal cannula market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & operating costs versus conventional oxygen delivery | -2.0% | Low-resource regions | Medium term (2-4 years) |

| Limited skilled personnel & training gaps in developing regions | -1.0% | Asia Pacific, Africa, South America | Long term (≥ 4 years) |

| Infection-control & aerosol-generation concerns during pandemics | -1.0% | Global | Short term (≤ 2 years) |

| Competitive pressure from alternative non-invasive ventilation (CPAP/BiPAP) | -1.0% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Costs Versus Conventional Oxygen Delivery

Initial HFNC system investment can be 3–5 times the price of standard oxygen, and disposable circuits add recurring expenses. Cost-utility analysis in pediatric bronchiolitis showed CPAP costing USD 17,574 versus USD 29,421 for HFNC while yielding marginally higher QALYs. Budget constraints and infrastructure gaps, such as erratic power supply, slow uptake in developing economies and temper the high-flow nasal cannula market trajectory.

Limited Skilled Personnel & Training Gaps in Developing Regions

Surveys reveal wide variability in flow-rate selection and weaning strategies across facilities. A pediatric quality-improvement project that standardized weaning cut mean therapy duration by 16 hours and length of stay by 24 hours. Shortages of respiratory therapists and structured education programs in many middle-income countries restrict optimal HFNC implementation, placing drag on the high-flow nasal cannula market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Active Humidifiers Lead Market Share

Active Humidifiers captured 33.82% of component revenue in 2025 thanks to their critical role in delivering gas at body-temperature humidity that protects mucosa. The high-flow nasal cannula market size for Active Humidifiers is set to rise at a steady 9.03% CAGR through 2031 as next-generation units embed algorithm-based dew-point control. Air/Oxygen Blenders follow, driven by demand for precise FiO₂ titration compatible with electronic health-record integration. Nasal Cannula components will pace the segment with a 13.33% CAGR, reflecting design improvements that reduce pressure ulcers and support pediatric sizing. Manufacturers increasingly lock these components into proprietary ecosystems, reinforcing stickiness within the high-flow nasal cannula market.

Design refinements stem from computational fluid-dynamics work demonstrating smoother gas distribution and reduced interface shear. Single Heated Tubes gain traction as they minimize condensation, which can trigger alarms and therapy interruptions. Integrative product strategies that combine humidifier, blender, circuit, and cannula under a single brand umbrella are helping major vendors defend pricing and margins within the high-flow nasal cannula market.

By End-user: Home-care Settings Emerge as Growth Frontier

Hospitals & Intensive Care Units commanded 47.30% of global revenue in 2025 as HFNC became standard in escalation algorithms from nasal prongs to ventilation. Meta-analysis of 10,230 patients confirmed a relative risk of 0.85 for subsequent invasive ventilation versus conventional oxygen, reinforcing hospital demand. Long-term Care Centers are adding HFNC to manage chronic hypoxemia in elderly residents, aided by portable trolley-mounted units.

Home-care Settings are projected to expand at a 12.57% CAGR, the fastest across end-users, buoyed by evidence of fewer COPD readmissions and advances in tele-respiratory dashboards. The high-flow nasal cannula market size for domiciliary use is expected to climb from USD 1.1 billion in 2025 to USD 2.23 billion by 2031. Pediatric retrospective data reveal low complication rates in children discharged on HFNC for upper-airway obstruction and CO₂ clearance. Emerging payor models that reimburse remote monitoring further stimulate adoption, diversifying revenue streams in the high-flow nasal cannula market.

By Application: COPD Management Drives Growth Momentum

Acute Respiratory Failure retained the largest application share at 41.52% in 2025. A MIMIC-IV study showed HFNC cutting 28-day sepsis mortality to 18.6% from 31.2% under standard care, underscoring clinical benefit. Acute Heart Failure represents a smaller but growing niche where mask-intolerant patients benefit from open-label oxygen delivery.

COPD use cases are rising fastest at an 11.23% CAGR, backed by randomized data indicating lower treatment failure compared with NIV and superior comfort. The 2025 GOLD report formally recommends HFNC for certain COPD phenotypes, providing guideline momentum. These endorsements are expected to lift the high-flow nasal cannula market share of COPD applications to 24.85% by 2031. Post-extubation, procedural sedation, and palliative indications collectively broaden the revenue base.

By Patient Age Group: Geriatric Segment Shows Highest Growth Potential

Adults aged 18-64 years generated 58.40% of 2025 sales as clinicians embraced HFNC for sepsis, trauma, and post-operative care. Trials show that HFNC during exercise reduces work of breathing and could support rehabilitation programs. Neonatal & Pediatric therapy remains sizable due to bronchiolitis admissions tripling over the last decade.

The Geriatric cohort is projected to grow at 10.21% CAGR, fastest of all age groups, since comfort issues limit mask tolerance in older adults. Systematic reviews reveal improved dyspnea scores and fewer therapy discontinuations in fibrotic interstitial lung disease when HFNC is used over NIV. The high-flow nasal cannula market size for geriatric patients is forecast to double between 2026 and 2031 as home-care programs expand and tele-supervision mitigates staffing constraints.

Geography Analysis

North America led with 37.45% revenue share in 2025, buoyed by advanced reimbursement and 25 million diagnosed asthma cases in the United States. High-flow therapy migrated from ICUs to general wards, as bronchiolitis support successes drove a 4.8-fold rise in pediatric HFNC utilization between 2013 and 2022. The high-flow nasal cannula market size for home-care in the region is on track to exceed USD 1.58 billion by 2031 amid insurer acceptance of tele-respiratory bundles.

Asia Pacific is set for the fastest 10.86% CAGR, propelled by rising respiratory disease incidence, infrastructure investment, and localization by global vendors. WHO’s 2024 compendium highlighted low-cost solutions such as PremieBreathe aimed at neonatal wards in low-resource hospitals. Government programs in China and India that subsidize non-invasive ventilation equipment will likely spur wider adoption in secondary-tier facilities.

Europe continues to adopt HFNC across Western health systems where robust clinical trials validate outcomes. Eastern European uptake is growing thanks to EU funding for respiratory care modernization. The Middle East & Africa and South America remain nascent yet promising; targeted clinician-training initiatives and modular HFNC systems suited to erratic electricity supply are expected to accelerate the high-flow nasal cannula market over the forecast horizon.

Competitive Landscape

The high-flow nasal cannula market shows moderate concentration. Fisher & Paykel Healthcare leads with the Optiflow platform and reported double-digit home-care growth in FY 2025. Teleflex leverages its broad anesthesia and respiratory portfolio to bundle HFNC with airway management tools. ResMed capitalizes on cloud connectivity know-how to integrate flow data into its AirView ecosystem for remote patient monitoring.

Bench humidity tests revealed measurable performance gaps between product families, shaping brand preference among clinicians. ICU Medical (Smiths Medical) plans to tie HFNC hardware into its infusion and vital-sign monitoring network, enabling unified clinical dashboards. Niche entrants focus on portable battery-operated units for outpatient transport and low-resource wards, using polymer additive manufacturing to cut cost and speed customization. As home-based therapy rises, consumer-grade aesthetics and smartphone apps are poised to turn patient experience into a competitive differentiator within the high-flow nasal cannula market

Several vendors are now piloting artificial-intelligence algorithms that auto-titrate flow and FiO₂ based on continuous vital-sign feeds, aiming to turn software accuracy into a core differentiator. Subscription models that bundle disposables with cloud analytics are gaining traction, generating predictable service revenue for manufacturers. Partnerships with hospital-at-home providers are accelerating the roll-out of compact, battery-ready HFNC carts that can be managed remotely by respiratory therapists. These moves intensify competitive pressure on price while elevating the importance of digital ecosystem strength across the high-flow nasal cannula market.

High-flow Nasal Cannula Industry Leaders

Fisher & Paykel Healthcare Limited

Teleflex Incorporated

Vapotherm Inc.

Masimo Corp. (TNI medical AG)

ResMed Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The American Thoracic Society International Conference featured multiple sessions on high-flow oxygen systems and non-invasive ventilation, highlighting the latest clinical trial data and emerging trends in respiratory health that will influence HFNC market development

- January 2025: Beyond Air, Inc. announced that its LungFit PH device received market authorization from the Australian Therapeutic Goods Administration (TGA) as a Class IIb medical device, expanding the company's global commercial footprint for respiratory support technologies

- January 2025: The Global Initiative for Chronic Obstructive Lung Disease (GOLD) released its 2025 report, which includes updated recommendations for oxygen therapy and ventilatory support in COPD management, providing clinical validation for HFNC applications in this patient population

- August 2024: The World Health Organization published its Compendium of Innovative Health Technologies for Low-resource Settings, highlighting the importance of adapting HFNC technology for use in developing regions to address global respiratory health challenges

- May 2024: A multicentre, randomised controlled trial published in BMJ demonstrated that HFNC oxygenation significantly reduced hypoxia incidence from 21.2% to 2.0% during sedated gastrointestinal endoscopy in obese patients, expanding the evidence base for HFNC use in procedural settings

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the high-flow nasal cannula (HFNC) market as the global sales value of integrated systems that combine an air-oxygen blender, heated humidifier, single heated circuit, and wide-bore nasal interface capable of delivering up to 60 L/min of warmed, humidified gas to neonate, pediatric, and adult patients. According to Mordor Intelligence, the market is valued at USD 8.07 billion in 2025 and is tracked across 17 major countries for every product, patient-age group, and care setting.

Scope exclusion: low-flow nasal cannulas and standalone oxygen blenders are outside this definition.

Segmentation Overview

- By Component

- Air/Oxygen Blender

- Active Humidifier

- Single Heated Tube

- Nasal Cannula

- Other Consumables

- By End-user

- Hospitals & Intensive Care Units

- Long-term Care Centers

- Home-care Settings

- Other End-users

- By Application

- Acute Respiratory Failure

- Chronic Obstructive Pulmonary Disease

- Acute Heart Failure

- Other Applications

- By Patient Age Group

- Neonatal & Pediatric (0-17 yrs)

- Adult (18-64 yrs)

- Geriatric (65 yrs +)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Respiratory therapists, ICU directors, biomedical engineers, and supply-chain managers were interviewed across North America, Europe, Asia-Pacific, and key emerging economies. Their insights helped us verify average selling prices, replacement cycles, patient-level utilization, and near-term regulatory triggers, closing gaps left by secondary sources.

Desk Research

We began with structured scans of public data sets such as WHO respiratory-disease burden, FDA 510(k) device clearances, Eurostat hospital-bed statistics, and national customs records for HS code 901920. Company filings and investor decks enriched price and margin signals, while tier-1 journals (for example, Critical Care), American Thoracic Society briefs, and regional procurement portals clarified clinical adoption patterns. Paid repositories, Dow Jones Factiva for deal flow and D&B Hoovers for supplier revenues, added historical context. This list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down model starts with acute-care and neonatal ICU bed counts, COPD and ARDS admission volumes, and guideline-based HFNC penetration rates; outputs are cross-checked through bottom-up roll-ups of publicly reported unit shipments and sampled ASPs. Core variables include average treatment hours per patient, annual device replacement ratios, reimbursement tariff changes, neonatal pre-term birth rates, and COVID-era baseline shifts. Multivariate regression with an ARIMA overlay projects each driver to 2030, and scenario analysis adjusts for oxygen-therapy protocol revisions. Any bottom-up gaps are bridged using channel-check ranges agreed in analyst workshops.

Data Validation & Update Cycle

Model outputs pass three-tier anomaly checks, peer review, and a senior analyst sign-off. Reports refresh annually, with rapid updates triggered by product recalls, reimbursement revisions, or pandemic-level events. Before client delivery, an analyst re-runs the model on the latest inputs.

Why Our High-flow Nasal Cannula Baseline Earns Trust

Published estimates often diverge because firms select different device mixes, assumption years, and refresh cadences.

Key gap drivers include inclusion of low-flow sets, varying disposal-consumable treatment, currency conversion points, and undisclosed ASP inflation methods. Mordor's consistent scope, annual refresh, and dual-path validation minimize these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.07 B (2025) | Mordor Intelligence | - |

| USD 9.06 B (2025) | Global Consultancy A | Bundles ancillary disposables; uses supplier list price without regional discounts |

| USD 8.21 B (2025) | Industry Association B | Excludes home-care usage; applies 2024 exchange rates across period |

| USD 7.30 B (2024) | Trade Journal C | Treats low-flow and high-flow devices together and assumes flat ASPs |

The comparison shows that once scope alignment and realistic price progressions are applied, Mordor's figure sits squarely between optimistic supplier-centric totals and conservative device-only counts, offering decision-makers a balanced, transparent baseline they can trace to verifiable inputs.

Key Questions Answered in the Report

How big is the high-flow nasal cannula market in 2026?

The high-flow nasal cannula market size is USD 8.91 billion in 2026 and is projected to reach USD 14.66 billion by 2031 at a 10.45% CAGR.

Which component segment is growing fastest?

Nasal Cannula components are forecast to register the highest 13.33% CAGR from 2026-2031 as new ergonomic designs improve patient adherence.

Why is home-care adoption accelerating?

Clinical evidence shows home HFNC cuts COPD exacerbations and hospital stays, and payors now reimburse remote monitoring, spurring 12.57% CAGR growth in this end-user segment.

Which region offers the greatest near-term expansion opportunities?

Asia Pacific is expected to record an 10.86% CAGR through 2031 thanks to rising respiratory disease prevalence, healthcare investment, and localized low-cost devices.

What is the main restraint to wider HFNC use in developing markets?

High capital cost versus standard oxygen delivery, combined with shortages of trained respiratory personnel, remains the chief barrier to adoption in resource-limited settings.

Who are the leading companies in the high-flow nasal cannula industry?

Fisher & Paykel Healthcare, Teleflex, and ResMed are the current market leaders, together holding around 47.0% of 2024 global revenue and driving innovation in connected care features.

Page last updated on: