Industrial NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

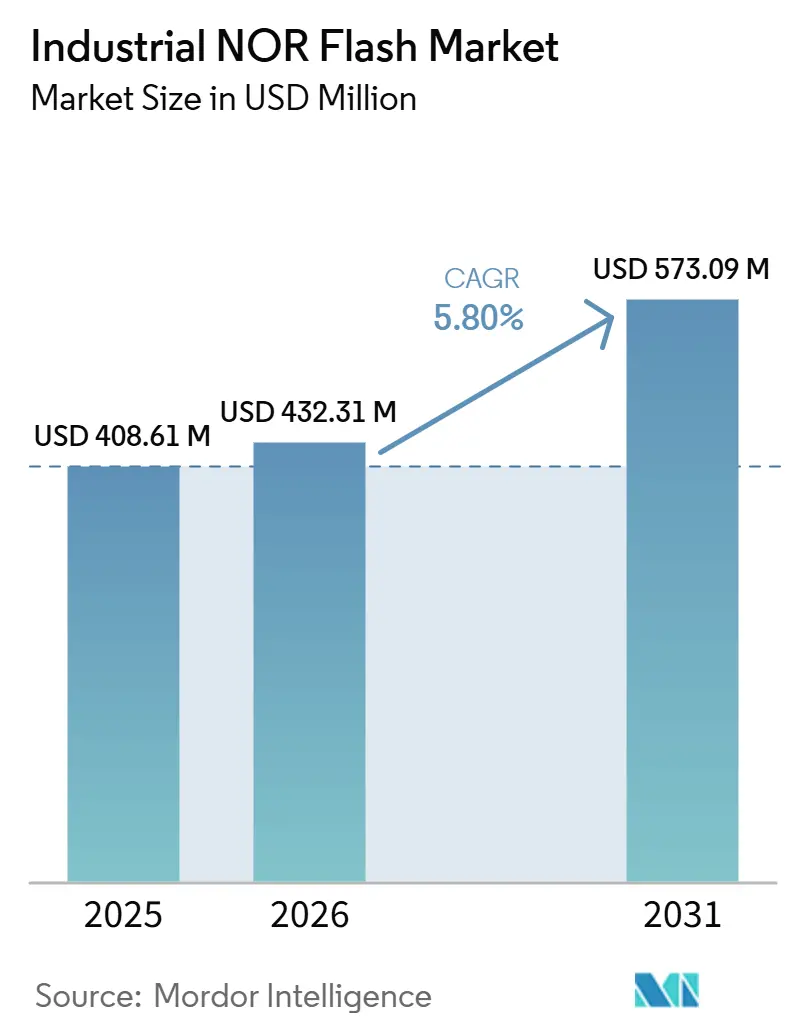

| Market Size (2026) | USD 432.31 Million |

| Market Size (2031) | USD 573.09 Million |

| Growth Rate (2026 - 2031) | 5.80% CAGR |

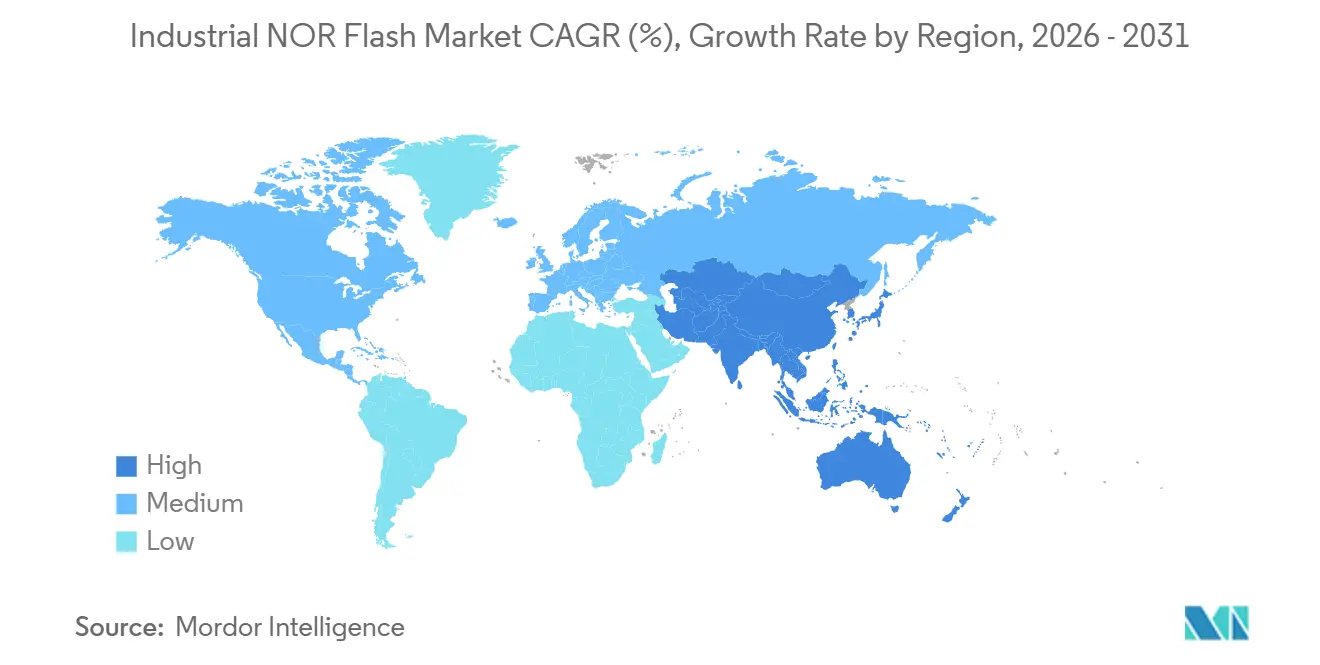

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

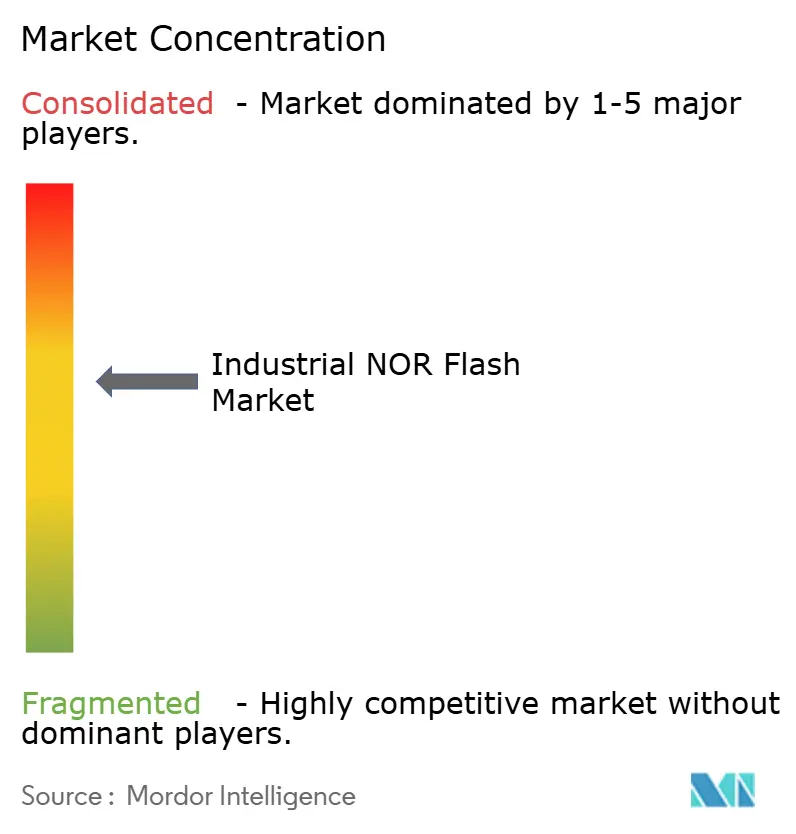

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial NOR Flash Market Analysis by Mordor Intelligence

The Industrial NOR Flash Market size is expected to increase from USD 408.61 million in 2025 to USD 432.31 million in 2026 and reach USD 573.09 million by 2031, growing at a CAGR of 5.80% over 2026-2031. In terms of shipment volume, the market was valued at 2.21 billion units in 2025 and is expected to grow from 2.40 billion units in 2026 to 3.47 billion units by 2031, at a CAGR of 7.85% during the forecast period (2026-2031). The industrial NOR flash market entered a distinct expansion phase in 2026 as AI server rack designs began using far more NOR flash content than earlier computing platforms. This demand pattern is shifting the market away from the older cycle that was shaped mainly by IoT and automotive sockets, and it is tightening supply across the density bands most used in AI server infrastructure. The industrial NOR flash market is also seeing a sharper split between premium products that compete on security, safety certification, bandwidth, and low-power performance, and commodity products that compete mostly on price. Taiwan-based IDMs are still investing heavily in capacity, but Chinese suppliers are expanding local production and adding pressure in standard density tiers. That mix is creating room for vendors that can pair supply reliability with secure-boot features, OTA-update support, xSPI compatibility, and specialized low-voltage offerings.

Key Report Takeaways

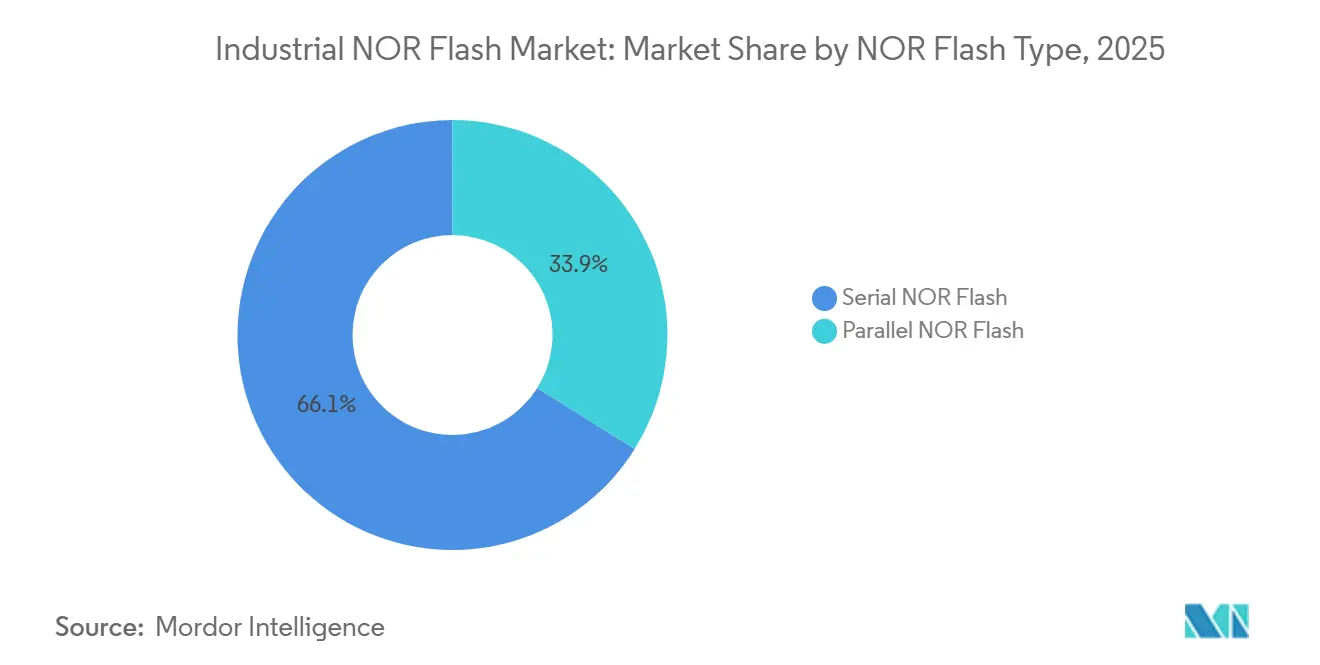

- By NOR flash type, serial NOR flash led the industrial NOR flash market with a 66.1% revenue share in 2025 and is projected to grow at a 6.7% CAGR through 2031.

- By interface, Quad SPI held 52.3% revenue share of the industrial NOR flash market in 2025, while Octal and xSPI are forecast to expand at a 6.9% CAGR through 2031.

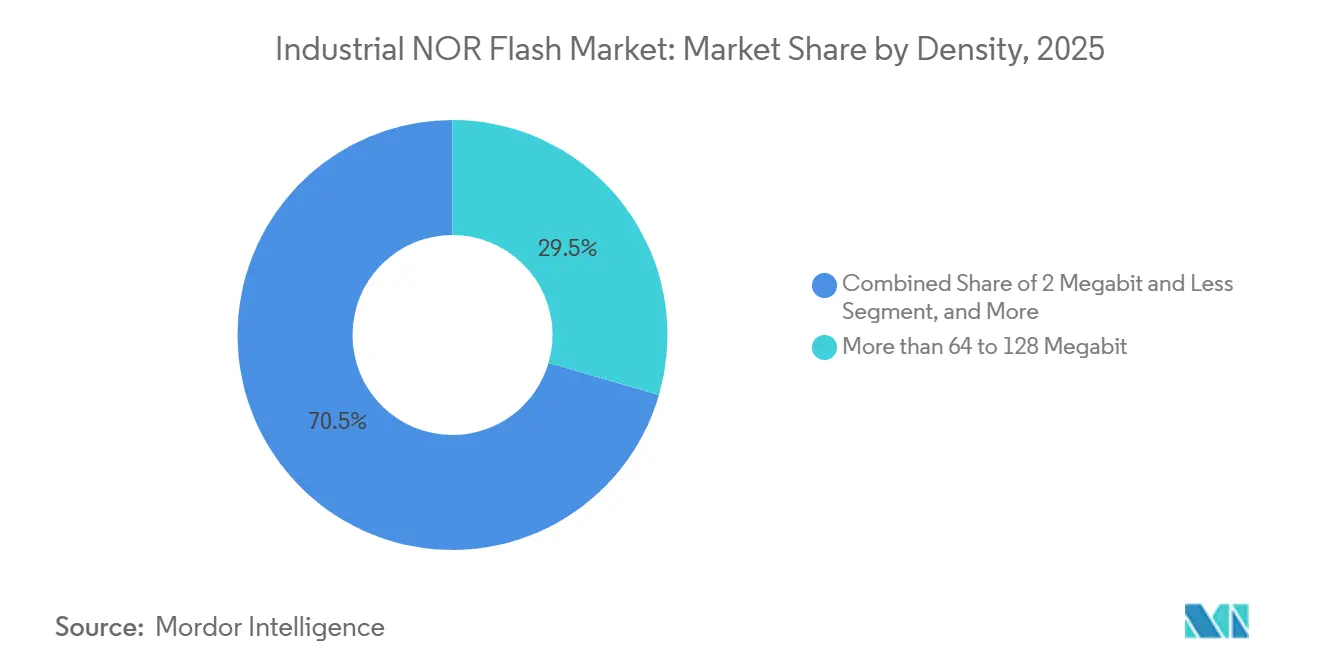

- By density, the more than 64 to 128 Megabit NOR band accounted for 29.5% of the revenue share of the industrial NOR flash market in 2025, while the more than 128 to 256 Megabit NOR band is advancing at a 7.1% CAGR through 2031.

- By voltage, the 1.8 V class held 44.9% revenue share of the industrial NOR flash market in 2025, while the ≤1.2 V and other specialty voltage segment is expected to grow at a 7.3% CAGR through 2031.

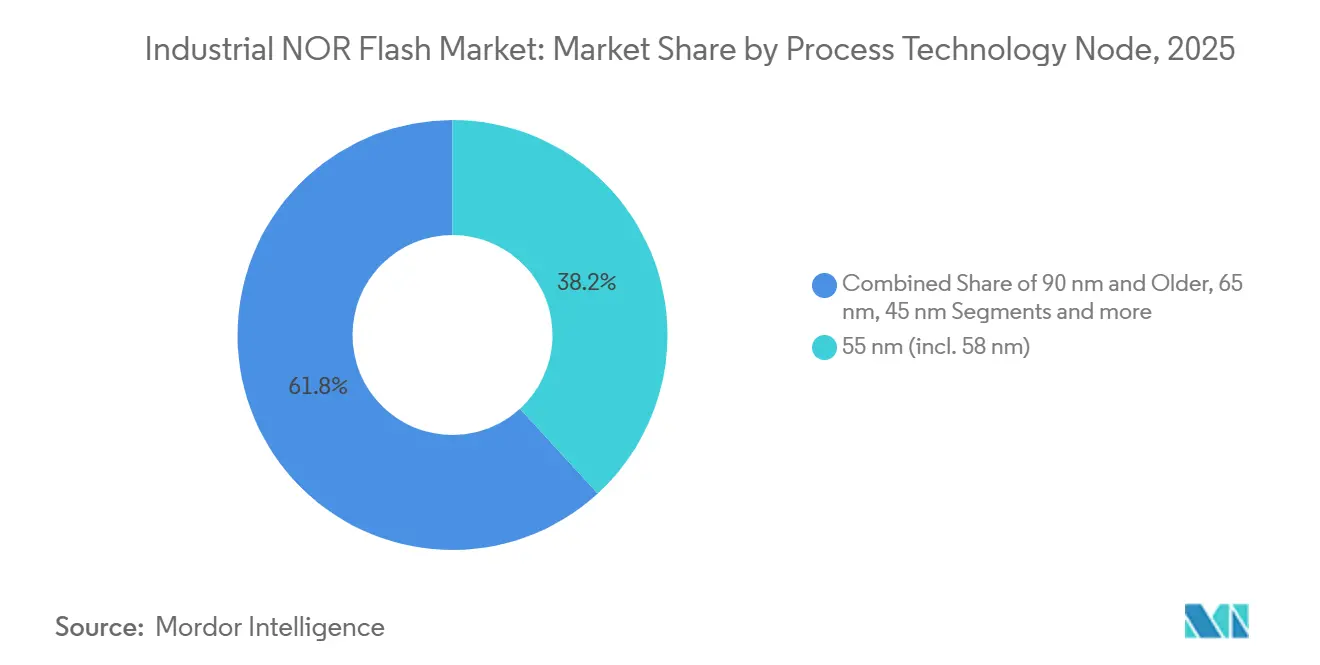

- By process technology node, the 55 nm node accounted for 38.2% revenue share of the industrial NOR flash market in 2025, while the 28 nm and below node is projected to grow at a 7.7% CAGR through 2031.

- By packaging type, QFN and SOIC captured 35.7% revenue share of the industrial NOR flash market in 2025, while WLCSP and CSP are forecast to expand at a 7.9% CAGR through 2031.

- By geography, Asia-Pacific accounted for 55.2% of global revenue in the industrial NOR flash market in 2025 and is expected to grow at a 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quad and Octal SPI Adoption For Fast-Boot IoT Edge Devices | +1.2% | Global, with concentration in China, Southeast Asia, and Germany's Industry 4.0 corridors | Short term (≤ 2 years) |

| China 55 Nm And 40 Nm Indigenous Process Push For NOR Self-Sufficiency | +0.9% | China primarily, with downstream pricing effects on APAC and European supply chains | Medium term (2-4 years) |

| Secure-Boot And OTA-Update Mandates In Industry 4.0 Factories | +0.8% | North America and EU, with early spill-over to APAC core manufacturing | Medium term (2-4 years) |

| Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices | +0.7% | North America and Europe, with growing APAC commercial space programs | Long term (≥ 4 years) |

| Low-Power 1.8 V Serial NOR For Wearable And Point-Of-Care Healthcare Electronics | +0.5% | Global, with concentration in North America, EU, and China | Medium term (2-4 years) |

| Real-Time Sensor Fusion In Autonomous Mobile Robots Driving Demand For 128-512 Mb NOR | +0.3% | Global, with concentration in North America, EU, Japan, South Korea, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Quad And Octal SPI Adoption Unlocking Higher Throughput at the IoT Edge

Quad SPI already supports a large installed base of code-storage sockets, and the move toward Octal SPI and xSPI is raising sustained read bandwidth to 400 MB/s for edge platforms that need faster boot and execution behavior.[1]JEDEC Solid State Technology Association, “xSPI Expanded Serial Peripheral Interface Standard JESD251,” JEDEC, jedec.org GigaDevice launched its GD25NX series in November 2025 with a 1.8 V core and 1.2 V I/O design, and the company said the product delivered 30% faster programming speed and 10% shorter erase time than conventional 1.8 V octal flash in 200 MHz double transfer rate mode. In the industrial NOR flash market, this shift matters because larger firmware images are making bandwidth a more visible design bottleneck than raw capacity in many AI edge nodes. Vendors that combine xSPI support with execute-in-place behavior are extending the role of NOR flash into applications that previously leaned on external SRAM to keep response times low. That is tightening platform qualification windows and giving an advantage to suppliers that already have certified high-speed portfolios in the industrial NOR flash market.

China 55 Nm And 40 Nm Indigenous Process Reshaping The Supply Equilibrium

China is reshaping the supply side of the industrial NOR flash market by expanding local production at 55 nm and 40 nm, with the goal of reducing dependence on Taiwan-based and U.S.-linked sources. Wuhan XMC had its IPO application accepted by the Shanghai STAR Market in September 2024, and the company offers foundry services for NOR flash at 40 nm and above.[2]China Securities Regulatory Commission, “XMC IPO Application Acceptance Notice,” China Securities Regulatory Commission, csrc.gov.cn GigaDevice and Puya are also broadening domestic supply options, which is increasing the strategic weight of local sourcing in standard and mid-density products. This build-out is not only replacing imports, but it is also creating a parallel pricing environment that is more aggressive in commodity tiers than in premium categories. The industrial NOR flash market is therefore becoming more clearly split between price-led domestic supply and qualification-led premium supply, where safety, security, and long design history still matter more than price alone.

Secure-Boot And OTA-Update Mandates Creating Compliance-Driven Demand Pull

Connected factories are using NOR flash in gateways, controllers, and edge compute nodes that now need verified firmware integrity and reliable over-the-air update capability as part of normal deployment requirements. The EU Cyber Resilience Act entered into force in October 2024, and full compliance for covered products is required by September 2026.[3]European Commission, “Regulation (EU) 2024/2847 Cyber Resilience Act,” Official Journal of the European Union, eur-lex.europa.eu That requirement is influencing product design outside Europe as well, because industrial system vendors in North America and Asia are aligning their architectures with the same expectations to preserve export access. Macronix introduced ArmorBoot MX76 in August 2025 as a single-device NOR flash platform that combines authentication, data integrity verification, secure update support, and OTA capability up to 1 GB. In the industrial NOR flash market, this shift is narrowing the usable supplier pool to vendors that can meet security hardening requirements without adding extra devices or more complex system integration.

Constellation-Scale LEO Satellites Creating A Durable Premium-ASP Pocket

Low Earth orbit satellite programs are creating a premium demand pocket in the industrial NOR flash market because these systems need non-volatile memory that can preserve boot code and mission-critical firmware in harsh radiation conditions. Infineon launched a 512 Mbit radiation-hardened-by-design QSPI NOR flash for space applications in November 2024, and the product was rated for 133 MHz operation with full QML qualification.[4]Infineon Technologies AG, “Infineon Unveils Industry's First Radiation-Hardened 512 Mbit NOR Flash for Space Applications,” Infineon, infineon.com That matters because large constellation programs can require hundreds or thousands of satellites, and each platform needs high-reliability memory content even when the launch cadence looks moderate. Qualification cycles are also long, and compliance with military or space-grade standards raises the entry barrier for new suppliers. This keeps premium pricing more resilient than in mainstream industrial sockets and gives the industrial NOR flash market a small but durable high-margin segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Premium Over NAND Above 256 Mb Limiting High-Density Consumer Adoption | -0.9% | Global, most acute in China and Southeast Asia consumer electronics hubs | Short term (≤ 2 years) |

| Scaling Ceilings Beyond 45 Nm Steering OEM Roadmaps Toward MRAM And ReRAM Substitutes | -0.8% | North America and EU premium automotive and industrial segments | Long term (≥ 4 years) |

| ASP Compression From Expanding Chinese Capacity Impacting Vendor Margins | -0.6% | Global, most acute for Taiwan IDMs in mid-density commercial tiers | Medium term (2-4 years) |

| Foundry Concentration In Taiwan Exposing Supply-Chain Disruption Risk | -0.5% | Global, with highest buyer exposure in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Premium Over NAND Constraining Adoption At The Density Ceiling

The industrial NOR flash market still faces a structural cost-per-bit disadvantage against NAND once density requirements exceed 256 Mb, which limits adoption in designs where storage economics matter more than fast random read access. The 2D NOR roadmap also remains difficult beyond 45 nm, and meaningful density scaling would require more advanced structures that are still far from broad-volume deployment. Macronix delayed its 3D NOR development program by about 2 years in 2026 to redirect resources toward supply-constrained mid-density NOR and eMMC products. That decision highlights the trade-off between long-term scaling investments and near-term revenue opportunities in segments that are already supply-constrained. The result is a dual-track industrial NOR flash market where 128-512 Mb products continue to grow in infrastructure, industrial, and automotive applications, but low-density consumer volumes are harder to expand when NAND alternatives are cheaper.

Scaling Ceilings Opening Architectural Entry Points For MRAM And ReRAM

Scaling limits in conventional 2D NOR are opening the door for MRAM and ReRAM in parts of the industrial NOR flash market where endurance, write speed, and advanced-node compatibility carry more weight. Everspin launched its UNISYST platform in March 2026 with xSPI compatibility, support for octal SPI, 200 MHz operation, 400 MB/s read bandwidth, and write endurance more than 400 times that of conventional NOR flash. Samsung also demonstrated 8 nm embedded MRAM with volume-production yields at ISSCC 2026, which raised the visibility of alternative memory paths for future automotive and industrial controllers. Even so, higher cost and a narrower range of available densities are keeping displacement limited to selected premium niches in the near term. That means coexistence should continue through much of the forecast period, but the industrial NOR flash market will face greater substitution pressure at the high-performance edge than in prior cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By NOR Flash Type: Serial NOR Drives Growth, Parallel Serves Long-Lifecycle Specialty Demand

Serial NOR flash held 66.1% of the industrial NOR flash market size in 2025 and is projected to grow at a 6.7% CAGR through 2031. Its lead reflects the preference of current IoT and automotive SoCs for low-pin-count serial interfaces that support execute-in-place without a dedicated memory bus. The industrial NOR flash market has moved steadily toward serial designs, as they better fit tighter board layouts and lower power budgets in new products. GigaDevice said its GD25NX xSPI NOR series achieved 400 MB/s throughput and reduced read power by up to 50% compared with conventional 1.8 V octal alternatives.

Parallel NOR flash is losing share, but it still retains a durable position in legacy programmable logic controllers, selected defense electronics, and some automotive safety modules. Those sockets often need synchronous parallel access and a wide bus width, and they also tend to stay in service for many years after initial qualification. That gives parallel products a stable revenue floor even as most new designs in the industrial NOR flash industry move to serial architectures. The overall pattern shows a market where serial dominates new demand, while parallel remains relevant in applications that value continuity and proven fit over redesign.

By Interface: Quad SPI Holds Mainstream Share, Octal And XSPI Lead The Next Design Cycle

Quad SPI accounted for 52.3% of the industrial NOR flash market share in 2025 because it offered the best balance between bandwidth, board simplicity, and controller compatibility. It remains the default choice across a wide installed base of industrial edge devices and microcontroller platforms. JEDEC standardization has supported this position by giving equipment makers a clear framework for serial flash interoperability. The SPI Single and Dual category still serves low-density and cost-sensitive sockets where legacy designs are not being refreshed quickly.

Octal and xSPI are the fastest-growing interface segments, with a 6.9% CAGR projected through 2031. That growth reflects demand from AI inference nodes and automotive domain controllers that need instant-on behavior and higher sustained read speed. In the industrial NOR flash market, vendors that embed ECC and CRC features into octal products are improving their chances in automotive safety programs where external support logic adds cost and design complexity. JEDEC xSPI protocol alignment is also becoming a practical gatekeeper for premium platform qualification. Vendors without a credible xSPI roadmap are likely to stay concentrated in standard sockets rather than the highest-margin part of the industrial NOR flash market.

By Density: Mid-High Density Anchors Revenue, High-Capacity Leads Structural Growth

The more than 64 to 128 Megabit NOR segment held 29.5% of the industrial NOR flash market size in 2025, making it the largest revenue band across all density categories. This segment fits well with many IoT gateways, automotive body electronics, and industrial control units that require firmware storage in the 4 MB–16 MB range. It also benefits from mature 55 nm process technology and a wide supplier base, which helps stabilize pricing and ensure consistent availability.

The more than 128 to 256 Megabit NOR segment is the fastest-growing band, projected to register a 7.1% CAGR through 2031. Growth is driven by larger firmware images in AI-capable edge devices, more complex AUTOSAR software stacks in next-generation automotive controllers, and increasing memory content per line card in AI networking switches and routers. Meanwhile, the Greater than 256 Megabit segment, though still smaller in unit volume, commands premium pricing in radiation-hardened, automotive-grade, and high-end AI server applications. Overall, the industrial NOR flash market is steadily shifting toward higher density per socket, even as socket growth in some applications moderates.

By Voltage: 1.8 V Class Leads Revenue, Sub-1.2 V Defines Next-Generation Platform Architecture

The 1.8 V class accounted for 44.9% of revenue in 2025 and remained the largest voltage segment in the industrial NOR flash market, as it is well-suited to wearables, IoT edge nodes, and automotive ADAS products. Lower operating voltage helps reduce current draw, and that matters in battery-powered or thermally constrained systems. The 3 V class still keeps a place in legacy industrial and automotive programs that value long qualification history. Wide-voltage devices also remain useful in ruggedized industrial and defense electronics where rail conditions are less tightly managed.

The ≤1.2 V and other specialty voltage segments are the fastest-growing parts of the industrial NOR flash market, with a 7.3% CAGR projected through 2031. GigaDevice expanded its GD25UF series to 8 Mb-256 Mb in March 2026, and the company said the portfolio delivered 50%-70% lower power consumption than conventional 1.8 V flash while reaching 80 MB/s in DTR Quad SPI mode. That product direction supports AI hearables, point-of-care medical devices, and edge processors that run at a core voltage of 1.2 V or lower. The ability to connect directly to SoC I/O without an external level shifter or booster circuit reduces BOM complexity and accelerates adoption in cost-sensitive volume designs.

By Process Technology Node: 55 Nm Commands Volume, 28 Nm And Below Defines The Performance Premium

The 55 nm node accounted for 38.2% revenue share in 2025, and it remained the workhorse process in the industrial NOR flash market because it combines maturity, high yield, and broad supply availability. It supports a large share of commercial volume across IoT, consumer, and mid-density industrial applications where cost is still the primary decision factor. Older nodes, such as 65 nm, 90 nm, and above, continue to serve long-lifecycle defense, infrastructure, and industrial programs that prioritize continuity and obsolescence management. That mix keeps 55 nm at the center of the present production base even as premium demand moves to finer geometries.

The 28 nm and below node is the fastest-growing process segment, with a 7.7% CAGR expected through 2031. This tier is most commonly used in automotive ASIL-D programs, dense AI server sockets, and space-grade devices, where bandwidth, form factor, and reliability justify the added process cost. The industrial NOR flash market is rewarding vendors that can combine fine-node manufacturing with integrated ECC, CRC, and other safety-critical features needed for premium designs. The 45 nm node remains an important bridge because it allows density gains without the full economic burden of 28 nm production, and it gives suppliers a practical path to extend portfolio depth before deeper node migration.

By Packaging Type: QFN And SOIC Anchor High-Volume Production, WLCSP Leads Miniaturization Wave

QFN and SOIC packages held 35.7% of revenue in 2025 and formed the largest packaging group in the industrial NOR flash market. Their lead reflects strong compatibility with mainstream industrial and automotive assembly flows, mature SMT handling, and efficient die-to-package area economics. BGA and FBGA packages serve denser networking and computing modules where board space and co-packaging considerations matter more. Other package formats, including ceramic options for defense and high-temperature uses, continue to provide a smaller but steady revenue base.

WLCSP and CSP are the fastest-growing packaging segments, with a 7.9% CAGR projected through 2031. GigaDevice said its GD25UF series has entered mass production across WLCSP, USON8, WSON8, and SOP8 packages, and the portfolio now spans 8 Mb to 256 Mb. That matters because the industrial NOR flash market is seeing stronger demand from wearables, optical modules, and compact IoT sensor nodes, where board real estate is under constant pressure. The packaging trend also supports smaller transceiver formats aligned with next-generation 800G and 1.6T standards, giving WLCSP and CSP a role beyond simple consumer miniaturization.

Geography Analysis

Asia-Pacific held 55.2% of the industrial NOR flash market share in 2025 and is projected to grow at a 7.2% CAGR through 2031, which keeps it firmly in the lead by both production scale and demand depth. China remains the largest domestic demand center in the region and is also the most active supply-side challenger, as local players expand 55 nm and 40 nm production for domestic self-sufficiency. Taiwan continues to anchor the IDM base in the industrial NOR flash market, and Winbond was reported to hold 23% of global NOR flash revenue while targeting a 30%-40% rise in NOR flash shipments in 2026. Macronix also restarted a TWD 22 billion (USD 699.1 million) investment plan to expand 12-inch factory output by 50% in 2026. Japan and South Korea add stable demand through automotive and industrial electronics, while India and Southeast Asia are becoming more important as electronics assembly expands under China-plus-one procurement strategies.

North America and Europe together form the second-largest demand block, and this part of the industrial NOR flash market is defined more by application value than by manufacturing scale. Demand is concentrated in automotive ADAS, defense, aerospace, and industrial automation, which supports higher average selling prices than standard consumer-driven memory segments. Infineon has reinforced this position with ASIL-D-aligned SEMPER NOR products and its 512 Mbit QML-qualified radiation-hardened NOR flash for space programs. Europe also benefits from a dense base of connected industrial equipment, and the Cyber Resilience Act is increasing procurement of secure NOR flash across the region's industrial device ecosystem.

The Rest of the World remains smaller, but it is still adding new demand in telecommunications infrastructure and industrial IoT deployments. Each 4G and 5G base station rollout creates an incremental need for NOR flash to store boot firmware and system configuration in network equipment. The Middle East is also becoming a meaningful secondary outlet for ruggedized industrial electronics tied to oil and gas automation and smart city programs. South America is more closely linked to electronics assembly and appliance manufacturing, so its growth tends to follow broader global demand shifts rather than define them within the industrial NOR flash market.

Competitive Landscape

The industrial NOR flash market is moderately concentrated, with Winbond, Macronix, GigaDevice, Infineon, and Micron controlling more than 55% of 2024 revenue. Competition is sharpening across 3 fronts, namely capacity investment, security integration, and leadership in low-voltage and high-speed interfaces. Winbond signaled a more aggressive supply stance by approving record 2026 capital expenditure of TWD 42.1 billion, equal to USD 1.33 billion, and by targeting a 30%-40% rise in NOR flash and NAND flash shipments. Macronix took a similar step by restarting a TWD 22 billion expansion plan for its 12-inch facility and by positioning ArmorBoot MX76 around secure boot, data integrity, and OTA update support. GigaDevice is pushing from another angle, with expanded 1.2 V products and xSPI-ready portfolios that target AI computing, wearables, hearables, and medical devices.

The white space in the industrial NOR flash market sits where ultra-low-power operation meets miniaturized packaging, especially in wearable medical and IoT endpoints. Chinese suppliers such as Zbit Semiconductor, Eon Silicon Solution, and XTX Technology are putting more pressure on commodity segments by qualifying alternative-source parts in common 8 Mb-64 Mb and 3 V categories. That strategy is eroding pricing power for larger IDMs that still depend on standard-density volume without enough feature differentiation. At the same time, secure flash, automotive certification, and high-speed interface support are giving premium suppliers a better defense against pure price competition.

Alternative memory suppliers are adding pressure, but they are not yet displacing the core volume base of the industrial NOR flash market. Everspin's UNISYST platform shows that xSPI-compatible MRAM is now targeting many of the same embedded code-storage applications that have long been served by NOR flash. JEDEC xSPI compliance is also acting as a practical screening tool for premium automotive and AI server programs, which means vendors without certified high-speed portfolios are losing access to the highest-value sockets. That dynamic should keep the industrial NOR flash market moderately concentrated, with continued fragmentation in commodity tiers and a smaller competitive field in premium categories where security, safety, and interoperability are becoming harder to separate.

Industrial NOR Flash Industry Leaders

Winbond Electronics Corporation

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

Puya Semiconductor (Shanghai) Co. Ltd.

Elite Semiconductor Microelectronics Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Winbond Electronics' board approved a capital expenditure budget of TWD 7.308 billion, USD 232 million, for production equipment and facility engineering, with investment commencing progressively from May 2026 to support ongoing NOR flash and DRAM capacity expansion at its Kaohsiung facility.

- March 2026: GigaDevice expanded its GD25UF 1.2V ultra-low-power NOR flash series from 8 to 256 Mb, delivering 50%-70% lower power consumption versus conventional 1.8 V flash, with full mass production across WLCSP, USON8, WSON8, and SOP8 packages, the series targets AI computing, wearables, hearables, and medical device applications.

- March 2026: Everspin Technologies launched the UNISYST unified MRAM platform as a direct xSPI-compatible alternative to serial NOR flash, offering 400 MB/s read bandwidth, write endurance more than 400 times higher than conventional NOR, AEC-Q100 Grade 1 qualification targeted, and engineering sample availability in Q4 2026.

- February 2026: Winbond Electronics announced record capital expenditure of TWD 42.1 billion, USD 1.33 billion, for 2026, nearly 8 times its 2025 outlay, targeting a 30%-40% year-on-year increase in NOR flash and NAND flash shipments and a doubling of DRAM capacity at its Kaohsiung facility by year-end.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the industrial NOR flash memory market as revenue generated from serial and parallel NOR devices that are designed, qualified, and marketed for factory automation, robotics, medical instrumentation, utilities, and other harsh-environment embedded systems where secure, byte-level code execution is vital.

Scope Exclusion: Consumer electronics, telecom handsets, and mainstream automotive infotainment sockets lie outside this industrial focus.

Segmentation Overview

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65-3.6 V)

- ≤1.2 V and Other Specialty Voltages

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (incl. 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Industrial Grade Packages

- By Geography (Value, Volume)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- Taiwan

- India

- South East Asia

- Rest of Asia-Pacific

- Rest of the World

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with component distributors in Asia, firmware engineers at PLC makers, and procurement managers from North American medical device firms. These conversations verified operating-temperature requirements, refreshed typical NOR content per board, and highlighted regional lead-time shifts that raw desk research could not reveal.

Desk Research

We collected baseline data from publicly available tier-1 sources such as the International Federation of Robotics, OECD industrial production indices, United States Census Bureau electronics trade tables, and WSTS semiconductor shipment statistics, which help us plot regional demand pools. Company 10-Ks, investor decks, and trade-association white papers on Industry 4.0 deployments supplied spend ratios and density splits. To fine-tune supplier shares and average selling prices, we tapped paid databases like D&B Hoovers for company financials and Questel for patent momentum around Quad and Octal SPI designs. The sources listed are illustrative; many additional publications were consulted for validation and clarification.

Market-Sizing & Forecasting

We start with a top-down construct that reconciles industrial electronics output, average NOR attach rates, and ASP trends, which are then cross-checked through sampled supplier roll-ups for sanity. Key variables like the installed base of industrial MCUs, new smart-factory capital outlay, secure-boot regulations, SPI bandwidth roadmaps, and foundry wafer pricing feed the model. Forecasts employ multivariate regression blended with scenario analysis to capture cycle swings in capital spending and macro demand. Gaps in bottom-up estimates are bridged using channel checks before the totals are finalized.

Data Validation & Update Cycle

Outputs pass variance checks against independent datasets, followed by a two-step peer review. We refresh figures each year and issue interim updates when material events, such as fab outages or major standard releases, move the market. A last-minute sweep ensures clients receive the latest view.

Why Mordor's Industrial NOR Flash Baseline Earns Trust

Published estimates often differ because study scope, density brackets, and refresh cadence vary.

Key gap drivers include a) broader inclusion of consumer and automotive demand, b) use of vendor shipment value without industrial filtering, and c) currency and ASP assumptions that lag contract pricing. Our disciplined segmentation and annual update cadence make our 2025 baseline the dependable reference for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 408.61 M (2025) | Mordor Intelligence | - |

| USD 5.27 B (2025) | Global Consultancy A | Combines consumer, telecom, and industrial volumes under one headline value |

| USD 3.25 B (2025) | Industry Association B | Counts automotive-grade NOR alongside industrial, inflating totals |

| USD 2.78 B (2025) | Trade Journal C | Relies on aggregated vendor revenue without density or end-market parsing |

In sum, our model ties every dollar to transparent variables, leverages on-ground intelligence, and updates promptly, so decision-makers can proceed with confidence.

Key Questions Answered in the Report

What is the current and forecast value of the industrial NOR flash space?

The industrial NOR flash market was valued at USD 408.61 million in 2025, reached USD 432.31 million in 2026, and is forecast to reach USD 573.09 million by 2031 at a 5.8% CAGR.

Why is AI server demand becoming important for industrial NOR flash?

AI server rack designs are using much higher NOR flash content than older computing platforms, which is shifting demand away from the earlier IoT and automotive-led cycle and tightening supply in the most relevant density tiers.

Which interface is expanding fastest in industrial NOR flash applications?

Octal and xSPI is the fastest-growing interface segment, with a projected 6.9% CAGR through 2031, driven by AI inference nodes and automotive domain controllers that need faster boot and higher read bandwidth.

Which density range is seeing the strongest growth?

The >128 Mb-?256 Mb density band is forecast to grow at a 7.1% CAGR through 2031 as firmware images expand in AI edge devices, automotive controllers, and networking hardware.

Which region leads global demand and supply?

Asia-Pacific leads with 55.2% of 2025 revenue and is forecast to grow at a 7.2% CAGR through 2031 because it combines the largest manufacturing base with strong domestic demand across China, Taiwan, Japan, and South Korea.

What are the main risks facing suppliers and buyers through 2031?

The biggest risks are the concentration of foundry capacity in Taiwan and China, cost disadvantages versus NAND at higher densities, and gradual substitution pressure from MRAM in premium automotive and industrial use cases.

Page last updated on: