NOR Flash For Consumer Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

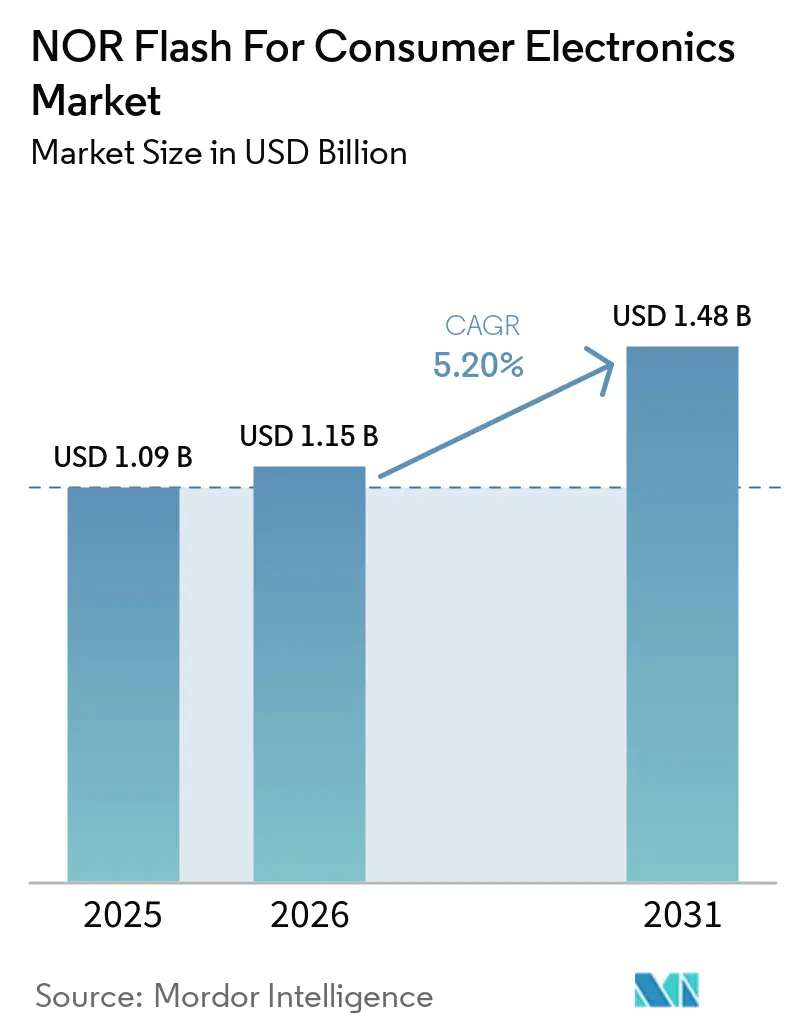

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

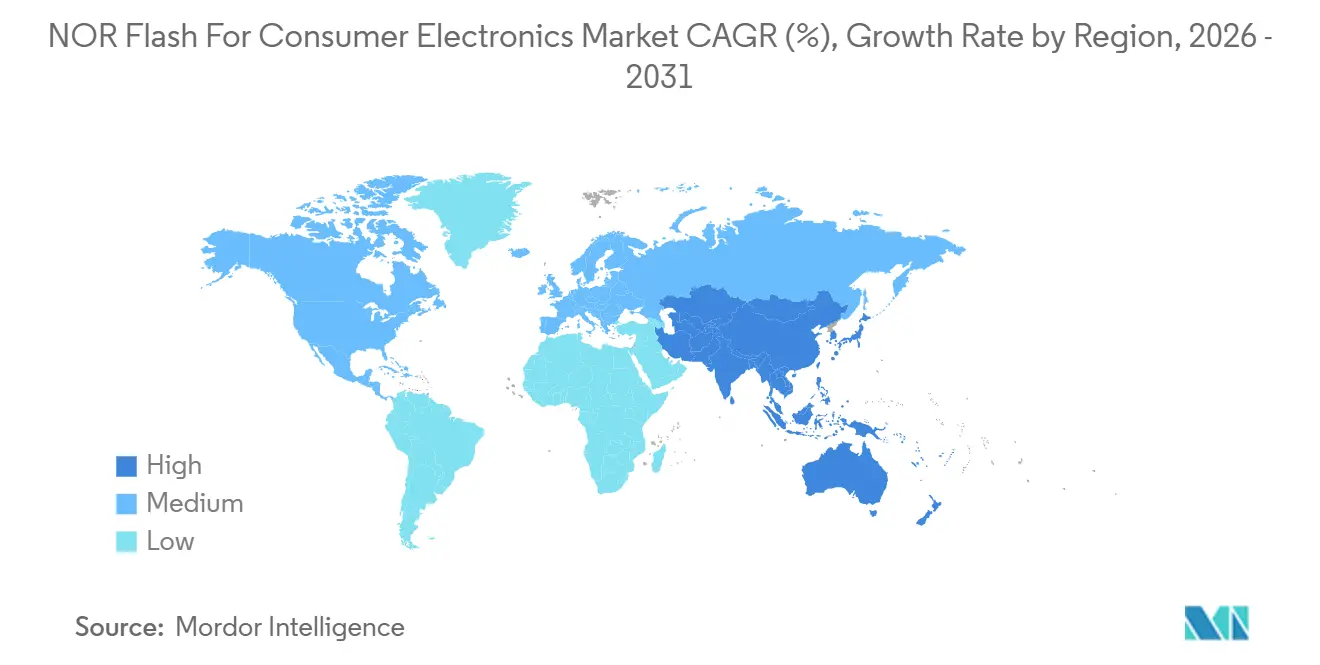

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

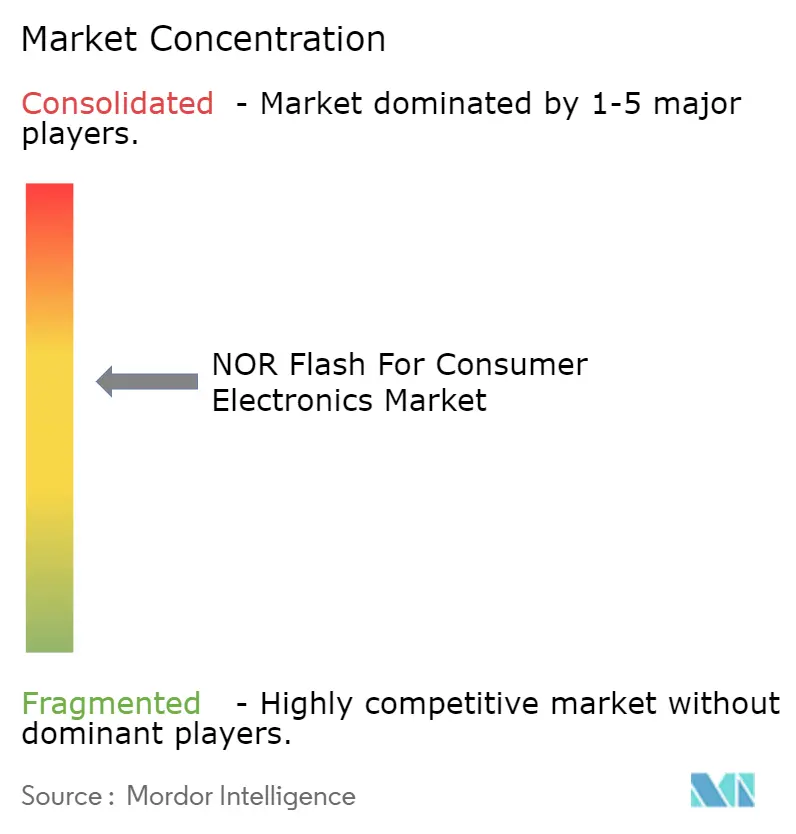

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

NOR Flash For Consumer Electronics Market Analysis by Mordor Intelligence

The NOR Flash For Consumer Electronics Market size is expected to increase from USD 1.09 billion in 2025 to USD 1.15 billion in 2026 and reach USD 1.48 billion by 2031, growing at a CAGR of 5.20% over 2026-2031. In terms of shipment volume, the market was valued at 6.03 billion units in 2025 and is expected to grow from 6.51 billion units in 2026 to 9.06 billion units by 2031, at a CAGR of 7.04% during the forecast period (2026-2031). Growth in the NOR flash for consumer electronics market is tied to a steady rise in always-on devices that need execute-in-place firmware storage, especially in smart home hardware, connected displays, gaming systems, and wearable products. Secure-boot requirements and broader over-the-air update architectures are also pushing device makers to use more reliable code storage across televisions, consoles, and other connected consumer platforms. China’s effort to build local supply at 55 nm and 40 nm nodes is changing procurement behavior, narrowing the historical gap between domestic and foreign suppliers in mid-density products. At the same time, buyers are placing more value on interface speed, lower standby power, and smaller packages, which is shifting design wins toward serial NOR, Octal, and xSPI, and wafer-level package formats. Competition remains moderate rather than fragmented, because a small group of established memory vendors still sets the pace on process migration, secure firmware features, and capacity expansion for the most active device categories.

Key Report Takeaways

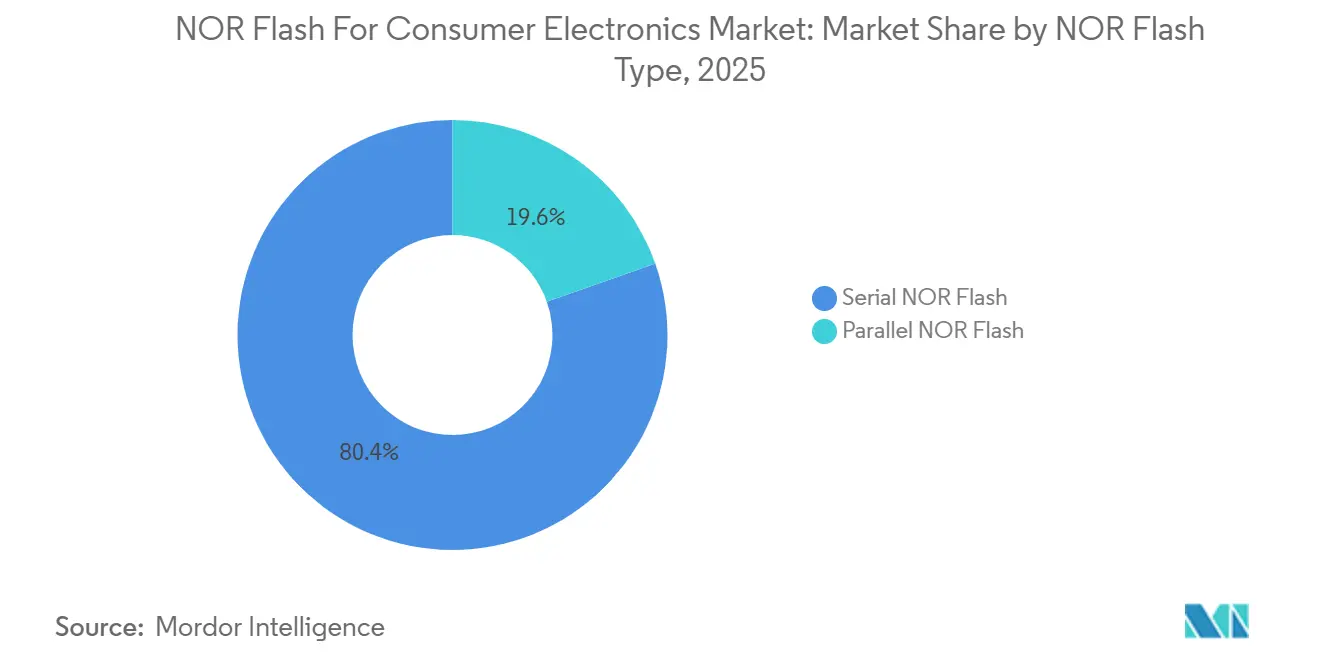

- By NOR flash type, serial NOR held 80.4% share of the NOR flash for consumer electronics market in 2025, while serial NOR also recorded the fastest projected CAGR at 6.7% through 2031.

- By interface, Quad SPI led with a 42.3% share of the NOR flash for the consumer electronics market in 2025, while Octal and xSPI are forecast to expand at a 6.9% CAGR through 2031.

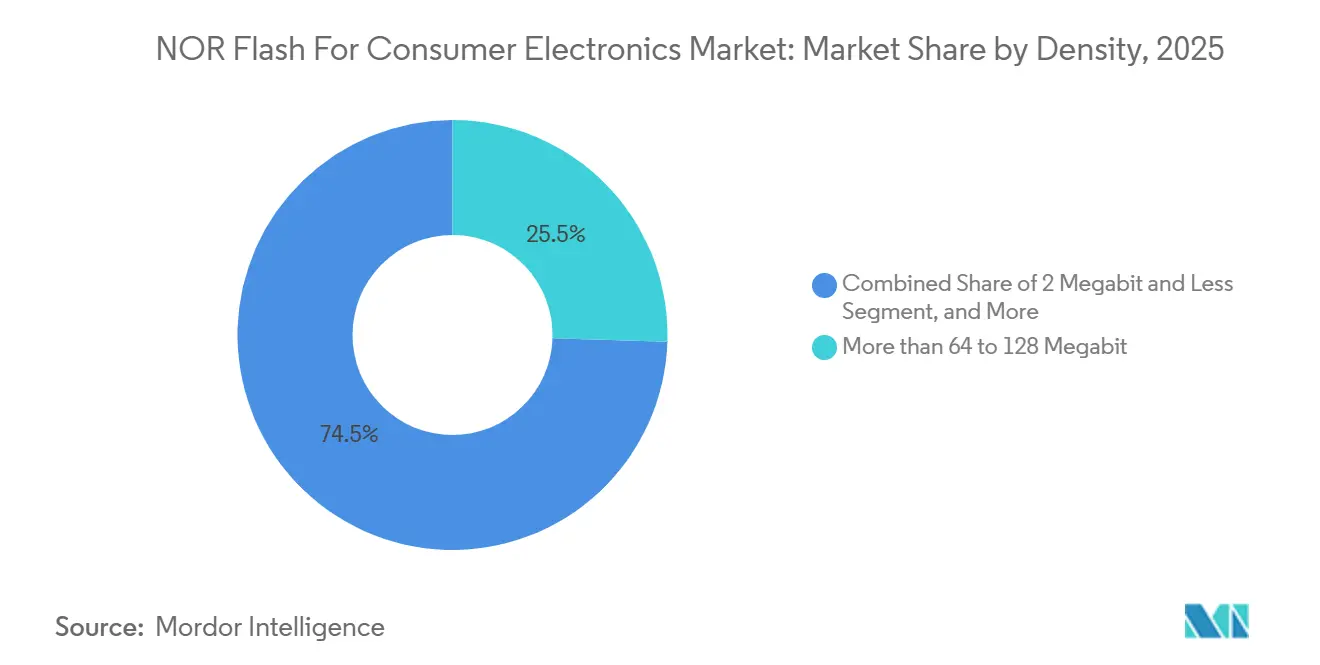

- By density, the more than 64 to 128 megabit tier accounted for 25.5% share of the NOR flash market for consumer electronics in 2025, while the more than 128 to 256 megabit tier is advancing at a 7.1% CAGR through 2031.

- By voltage, the 3 V class captured 46.1% share of the NOR flash market for the consumer electronics in 2025, while the 1.8 V class is projected to grow at a 7.3% CAGR through 2031.

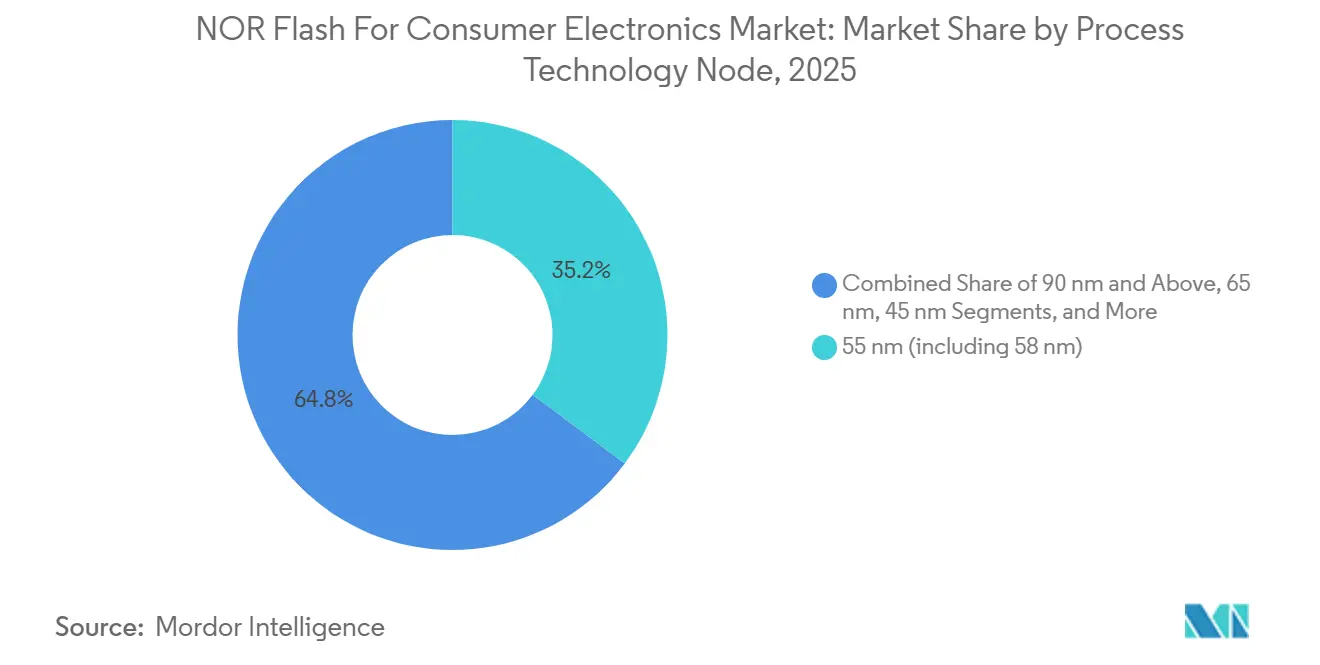

- By process technology node, the 55 nm node, including 58 nm variants, held 35.2% share of the NOR flash for consumer electronics market in 2025, while the 28 nm and below segment is projected to grow at a 7.7% CAGR through 2031.

- By packaging type, WLCSP/CSP accounted for 37.6% share of the NOR flash market for the consumer electronics in 2025 and also registered the fastest projected CAGR at 7.9% through 2031.

- By geography, Asia-Pacific held 52.8% share of the NOR flash for consumer market electronics in 2025 and is expected to post the fastest regional CAGR at 7.2% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global NOR Flash For Consumer Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Edge-AI IoT Appliances Adopting XiP Architecture Favoring High-Density Serial NOR | +1.4% | APAC core, China, Taiwan, Japan, with spill-over to North America and Europe | Medium term (2-4 years) |

| Proliferation of Voice-First Smart-Home Hubs Requiring Instant-On Firmware | +1.2% | North America, Europe, APAC | Short term (≤ 2 years) |

| Secure-Boot and OTA-Update Mandates in Connected TVs and Gaming Consoles | +1.0% | Global, with stronger compliance pressure in the EU | Short term (≤ 2 years) |

| China's 55 nm and 40 nm Localization Push Boosting Mid-Density NOR for Smartphones | +0.8% | China, with spill-over across APAC | Medium term (2-4 years) |

| Quad and Octal SPI Interfaces Enabling 4K Camera and Drone Fast-Boot Architectures | +0.6% | APAC core, China, Japan, South Korea | Medium term (2-4 years) |

| Ultra-Low-Power Wearables Driving Sub-45 nm Demand | +0.5% | Global, with early intensity in APAC and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Edge-AI IoT Appliances Adopting XiP Architecture Favor High-Density Serial NOR

The NOR flash market for consumer electronics is benefiting from a broader base of edge-AI appliances, such as smart displays, ambient computing hubs, and connected home cameras, that require code storage with fast boot performance. These products are moving toward in-place execution of memory because firmware and inference-related functions need to remain accessible without excessive RAM overhead, which makes high-density serial NOR more attractive in the design cycle. The product direction also favors suppliers that can combine higher densities with low-voltage operation and compact footprints for miniaturized consumer hardware. GigaDevice expanded its GD25UF 1.2 V ultra-low-power SPI NOR flash family in March 2026 to cover 8 Mb to 256 Mb densities and positioned the series for AI computing, wearables, hearables, and ASIC-based platforms. That kind of product expansion supports the view that the NOR flash for the consumer electronics market is shifting toward denser serial devices with better power efficiency rather than basic code-storage parts with limited performance headroom.

Proliferation of Voice-First Smart-Home Hubs Requiring Instant-On Firmware

The NOR flash for the consumer electronics market is also supported by voice-first smart-home devices that need local firmware to stay available for near-instant response after wake events. Smart speakers, display hubs, AI doorbells, and smart plugs depend on code storage that can support fast start-up without the longer load sequence associated with other memory types. This demand pattern matters because many brands now manage several assistant ecosystems on related hardware platforms, which raises the amount of firmware support each design must carry. Winbond identified smart home as a key growth area in its investor materials and stated that its F45 nm process improved die-size efficiency for TWS and IoT applications compared with the older F58 nm generation.[1]Winbond Electronics Corporation, “2H24 Investor Conference Presentation,” Winbond Investor Relations, winbond.com Winbond also reported that consumer electronics represented 29% of its 2025 application mix, showing that these device categories remain commercially important to the NOR flash for consumer electronics market and to the leading supplier base.

Secure-Boot and OTA-Update Mandates in Connected TVs and Gaming Consoles

The NOR flash market for consumer electronics is getting a further boost from security and update requirements in connected televisions and gaming systems. The European Union Cyber Resilience Act entered into force in December 2024, with vulnerability and incident reporting obligations starting in September 2026 and broader security-by-design requirements becoming effective in December 2027, which increases the focus on firmware integrity and device-level software governance.[2]European Commission, “Regulation (EU) 2024/2847,” EUR-Lex, eur-lex.europa.eu These rules support the use of dedicated code storage for secure boot chains and authenticated update flows, especially when device makers need a controlled, persistent location for firmware images. Macronix introduced ArmorBoot MX76 in August 2025 as a secure-boot NOR flash product with authentication protection, data integrity verification, SPI connectivity, 3 V and 1.8 V options, and capacities up to 1 GB.[3]Macronix International Co. Ltd., “Macronix Introduces Cutting-Edge Secure-Boot NOR Flash Memory - ArmorBoot MX76,” Macronix News, mxic.com.tw As update files grow with ongoing security patches and feature additions, the NOR flash for the consumer electronics market is likely to see a steady rise in minimum density needs even when end-device shipment growth is less dramatic.

China's 55 nm and 40 nm Localization Push Supporting Mid-Density NOR for Smartphones

The NOR flash market for consumer electronics in Asia-Pacific is being reshaped by China’s push to localize more memory content for smartphones and connected consumer devices. Chinese OEMs are placing greater weight on domestic sourcing as part of supply chain risk management, especially in mid-density products that fit mainstream handset and smart-device requirements. GigaDevice stated in its 2025 annual report that it achieved mass production of 45 nm SPI NOR flash in 2025 and now covers 13 capacity options from 512 Kb to 2 Gb across 5 voltage types and more than 20 product series. The same annual report showed 2025 revenue of CNY 9.203 billion (USD 1.28 billion) at the 2025 IRS average rate cited in the draft, indicating stronger scale during a period when domestic consumer electronics demand remained active. As more local suppliers build credible portfolios at 55 nm, 45 nm, and adjacent nodes, the NOR flash for the consumer electronics market is becoming more competitive in the mid-density range that supports mainstream smartphones, smart-home hubs, and connected audio products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Premium Versus NAND Above 256 Mb Limiting High-Resolution Camera Adoption | -1.3% | Global | Short term (≤ 2 years) |

| ASP Compression From Rising Chinese Capacity Pressuring Vendor Margins | -0.9% | APAC core, with spill-over to global markets | Medium term (2-4 years) |

| Scaling Ceilings Beyond 45 nm Steering OEMs Toward MRAM and ReRAM Alternatives | -0.6% | North America, EU, Japan | Long term (≥ 4 years) |

| Foundry Concentration in Taiwan Exposing Consumer-Device Supply Risk | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Premium Versus NAND Above 256 Mb Limiting High-Resolution Camera Adoption

The NOR flash for the consumer electronics market still faces a practical density limit in applications where code storage needs move well beyond 256 Mb. High-resolution camera modules in smartphones, action cameras, and home surveillance products can quickly push memory requirements into a range where NAND remains more cost-effective for larger payloads. That cost gap reduces NOR usage in imaging-heavy device designs even when fast boot characteristics still matter at system level. Macronix stated in its 2024 annual report that its 3D NOR development is intended to improve cost and density positioning, and the company discussed sampling in the second half of 2026 with mass production targeted for 2027. Until such products reach broader commercial use, the NOR flash for the consumer electronics market is likely to remain strongest in low to mid-density code storage rather than in the highest-capacity imaging-related memory needs.

ASP Compression From Rising Chinese Capacity Pressuring Vendor Margins

The NOR flash for the consumer electronics market is also dealing with pricing pressure as more Chinese capacity enters the mid-density range. This issue matters most in product bands where technical differentiation is narrower, and buyers can switch suppliers more easily on standard serial configurations. Vendors with older cost structures or limited exposure to premium applications face greater pressure when price becomes the main procurement filter. Winbond’s investor presentation noted softer NOR flash ASP conditions through mid-2025, while its 2025 results later showed that capacity for 2026 and 2027 was fully booked and that the company approved NTD 42.1 billion (USD 1.30 billion) in 2026 capital expenditure to expand Taichung flash capacity from around 50,000 to 57,000 to 58,000 monthly wafer starts. The result is a market where demand remains healthy, but margin protection increasingly depends on node migration, secure features, package flexibility, and customer relationships rather than on simple volume presence in the NOR flash for the consumer electronics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By NOR Flash Type: Serial NOR Shapes the Mainstream Design Base

Serial NOR commanded 80.4% of the 2025 NOR flash for the consumer electronics market share and is also the fastest-growing type segment, with a projected 6.7% CAGR through 2031. This lead reflects how completely consumer platform design has moved away from parallel memory controllers in current SoC roadmaps. Serial configurations use fewer traces, fit better into tighter board layouts, and align more closely with the low-voltage operating conditions now common in smart speakers, wearables, streaming devices, and connected home products. These traits keep serial NOR at the center of the NOR flash market for consumer electronics, as brands seek smaller, lower-power, and easier-to-qualify memory solutions for high-volume products.

Winbond’s 2025 annual results showed that flash memory accounted for 35% of the company's revenue, consistent with the large role of serial NOR in its portfolio and the weight of code-storage products in consumer electronics demand. The category is also helped by stronger adoption in AI-capable household devices, where firmware is expanding as voice, vision, and local processing features are added. Parallel NOR still serves older set-top boxes, fixed-function appliances, and simple remote-control designs where redesign costs are hard to justify. Even so, that installed base is gradually shrinking because newer silicon generations do not prioritize parallel memory support, which limits the long-term room for legacy formats in the NOR flash for consumer electronics market. The direction of travel remains clear, with serial products carrying both the volume base and the forward product roadmap for most modern consumer device designs.

By Interface: Quad SPI Holds the Core While Octal and xSPI Raise Performance

Quad SPI accounted for 42.3% of the 2025 NOR flash market share in consumer electronics and remained the standard interface for a broad range of mid-range devices. It serves smartphones, smart TVs, gaming accessories, and streaming hardware that require higher throughput than single- or dual-SPI can provide without moving to the higher cost and tighter design requirements of full Octal support. The wide controller compatibility of Quad SPI reduces integration risk for OEMs and helps shorten qualification cycles in products with large annual volumes. This keeps Quad SPI firmly positioned as the workhorse interface across the NOR flash for the consumer electronics market.

At the performance end, Octal and xSPI are forecast to grow at a 6.9% CAGR through 2031 as devices demand faster boot times and higher execution speeds for advanced firmware. GigaDevice launched the GD25NX series in November 2025 with a dual-voltage design, 200 MHz Octal SPI support, throughput up to 400 MB/s, and a stated 30% faster program speed than conventional 1.8 V Octal devices.[4]GigaDevice Semiconductor Inc., “GigaDevice Launches GD25NX Series xSPI NOR Flash with Dual-Voltage Design,” GigaDevice News, gigadevice.com The product also eliminated the need for an external boost circuit in thin wearable platforms by pairing a 1.8 V core with 1.2 V I/O, which is important in space-limited devices. Single and dual SPI still matter in simpler IoT nodes and basic appliances, but the growth path in the NOR flash for consumer electronics market is moving toward interfaces that support more demanding firmware loads and richer device responsiveness. As the product mix shifts toward AI-enabled and display-heavy platforms, Octal and xSPI should take a larger share of new premium design wins.

By Density: Mid-Range Devices Lead While Higher Capacities Gain From Update Growth

The more than 64 to 128 megabit segment accounted for 25.5% of the 2025 consumer NOR flash market, making it the most widely adopted density tier. It aligns with firmware needs for voice-assistant SoCs, smart TV boot code, active noise cancellation in hearables, and gaming accessory controllers. These applications require adequate code headroom without higher-cost density bands. This segment serves the broadest range of active product designs, balancing storage capacity, cost, and packaging flexibility.

The more than 128 to 256 megabit segment is the fastest-growing density band, with a projected 7.1% CAGR through 2031. Growth stems from increasing OTA updates and expanding software features. Winbond’s Taichung expansion targets 57,000–58,000 monthly wafer starts by late 2026 for higher-capacity products, while Macronix’s ArmorBoot MX76 series offers up to 1 GB capacities for secure firmware storage. Lower-density segments, more than 16 to 32 megabit NOR and below, support simple sensors, low-cost Bluetooth devices, and entry-level connected appliances. However, the growth center of the consumer NOR flash market is shifting upward as software stacks grow heavier. This trend is expected to continue, as security patches and feature additions accumulate over a product’s lifecycle.

By Voltage: 3 V Retains the Base While 1.8 V Gains From Portable Electronics

The 3 V class held 46.1% of the 2025 market and still anchors a large installed base across routers, gaming accessories, and other consumer systems built around 3.3 V I/O environments. Its lead comes from broad compatibility with existing microcontrollers, better fit with many mature device architectures, and easier integration in designs that are not aggressively optimized for ultra-low standby current. This keeps the 3 V segment important in the NOR flash market for consumer electronics, especially where redesign cycles are longer, and component risk is managed conservatively. Wide-voltage products also serve brands that want a single qualified hardware platform across multiple product tiers.

The 1.8 V class is the fastest-growing voltage segment and is projected to expand at a 7.3% CAGR through 2031 as wearables, hearables, and low-power IoT hardware scale further. GigaDevice said its expanded GD25UF family operates at 1.14 V to 1.26 V and cuts read power consumption by 50% to 70% compared with 1.8 V flash in target applications. Winbond also stated in its 2024 annual report that it entered mass production of a 1.2 V NOR flash product and received customer certifications for low-power wearable and IoT applications. These developments show that the NOR flash for the consumer electronics market is moving beyond standard low-voltage operation toward even lower-power configurations where board space, current draw, and thermal constraints all matter. The result is a stronger role for low-voltage memory in portable products that remain active for long periods on small batteries.

By Process Technology Node: 55 nm Keeps Scale While 28 nm and Below Expands Faster

The 55 nm node, including 58 nm variants, held 35.2% of the 2025 market and remained the most practical process choice for mainstream consumer device programs. It supports a large set of smartphones, media players, connected audio devices, and smart-home hubs where cost, reliability, and available supply matter as much as absolute die shrink. In the NOR flash market for consumer electronics, this node continues to offer a balance between mature manufacturing economics and competitive density for mid-range products. It also fits well with product families that need broad voltage coverage and long lifecycle support.

Winbond has highlighted its 58 nm-based products as durable options for IoT and connected applications, while GigaDevice stated that its 45 nm serial NOR reached mass production in 2025 and improved density relative to the earlier 55 nm generation. The 28 nm and below segment is projected to grow at a 7.7% CAGR through 2031, reflecting rising demand for compact AI-edge devices, advanced wearables, and other products that require greater density within smaller die footprints. Microchip and UMC announced the immediate commercial availability of 28 nm SuperFlash Gen 4 embedded NOR in January 2026, indicating that advanced embedded NOR has entered a more production-ready stage. Older 90 nm and above nodes still serve cost-sensitive controllers and white-goods overlap applications, but the more advanced end of the NOR flash for consumer electronics market is increasingly defined by tighter process geometry. That shift is especially visible in premium wearables and AI-capable devices where every square millimeter of silicon and board space matters.

By Packaging Type: WLCSP and CSP Match the Fastest Device Categories

WLCSP/CSP accounted for 37.6% of the NOR flash for the consumer electronics market size in 2025 and also posted the fastest projected CAGR at 7.9% through 2031. This dual position matters because it shows that the largest package format is also the one most closely aligned with the fastest-rising device classes. TWS earphones, smartwatches, slim smartphones, and fitness bands all reward smaller z-heights and tighter board integration, giving wafer-level and chip-scale packaging a clear advantage. That makes WLCSP/CSP one of the strongest structural beneficiaries inside the NOR flash for the consumer electronics market.

Winbond stated that its F45 nm WLCSP process enabled TWS opportunities that were difficult to address at the older F58 nm node due to die-size limits. GigaDevice launched the GD25NX series with both TFBGA24 and WLCSP options, enabling OEMs to qualify a single die across multiple form-factor tiers and use the same basic memory platform across different product designs. QFN and SOIC remain important for routers, controllers, and set-top hardware where thickness constraints are less severe, while BGA and FBGA support higher-density use in media processors and connected TV modules. Even so, packaging growth in the NOR flash for consumer electronics market is clearly tied to smaller and lighter devices, which keeps WLCSP/CSP in the leading position for both volume and growth. The packaging mix is therefore shifting in the same direction as the broader device mix, toward compact mobile and wearable electronics.

Geography Analysis

Asia-Pacific accounted for 52.8% of NOR flash market share in the consumer electronics market in 2025 and is also the fastest-growing regional block, with a 7.2% CAGR through 2031. China remains the main anchor because it combines the largest consumer electronics assembly base with a growing domestic memory supply position in smartphones, TWS devices, smart speakers, and smart-home hardware. Taiwan adds major wafer capacity and design depth, and Winbond said its Taichung site is moving toward 57,000 to 58,000 monthly wafer starts by late 2026 to support flash demand. Japan supports the region through premium electronics design and low-power memory know-how, while Renesas has highlighted serial NOR solutions with sleep current as low as 0.2 µA in its memory portfolio materials. South Korea remains important in flagship smartphones and connected display products, where higher-throughput interfaces and denser firmware storage are more common.

North America and Europe formed the second-largest demand cluster in the NOR flash for consumer electronics market, driven by premium device demand, gaming ecosystems, smart-home hardware, and connected home security products. The United States remains the largest single-country market in this group because of strong smart-speaker penetration, console refresh cycles, and connected-home platform upgrades. Europe has a stronger regulatory impact on memory content because firmware integrity and secure update capabilities carry greater weight in connected device design and documentation. The EU Cyber Resilience Act is central to that shift because it brings a more formal security framework to products that rely on managed firmware behavior.

South America, the Middle East, and Africa remained smaller in absolute demand, but they continue to add volume in affordable smartphones, value-tier streaming products, and connected appliances. Brazil stands out in South America because domestic electronics incentives support local manufacturing and assembly, providing a stable demand base for mid-range serial NOR products. Saudi Arabia and the United Arab Emirates are strengthening connected-device use through smart-city and digital infrastructure programs that support secure consumer gateways and home systems. Across Africa, demand tracks smartphone adoption and import assembly patterns, which favor established suppliers offering reliable mid-density parts with long lifecycle support. These regions do not yet set the technology pace for NOR flash in the consumer electronics market, but they do expand the addressable customer base for standard-serial products at mainstream density and voltage points.

Competitive Landscape

The NOR flash for the consumer electronics market is moderately concentrated, with a limited number of suppliers holding strong positions across serial NOR, secure firmware products, and low-power device applications. Winbond remains the clearest scale leader in the field, while Macronix, GigaDevice, Infineon, Microchip, and Renesas each compete from different strengths, such as security, embedded flash, low-power design, or regional customer reach. This structure means competition is active, but it is not open-ended, because new entrants still face barriers in process control, customer qualification, and packaging support. In practical terms, the NOR flash for the consumer electronics market rewards suppliers that can deliver dependable supply, strong application support, and a visible node roadmap rather than only low headline pricing.

Winbond said in February 2026 that it remained the worldwide number-one NOR flash supplier, and it also reported that 2026 and 2027 production capacity was fully booked, which signals firm customer commitments across the forward order book. Macronix has taken a different but equally important path by pairing secure-boot product development with long-range 3D NOR work aimed at closing the density and cost gap in larger-capacity use cases. GigaDevice has pushed product breadth through 45 nm mass production and new low-voltage and xSPI launches that target AI computing, wearables, and high-throughput consumer designs. These moves show that the main strategic levers in the NOR flash for consumer electronics market are capacity timing, node migration, and product specialization rather than broad-based price competition alone.

Another competitive theme is technology substitution at the high-performance edge of the NOR flash for consumer electronics market. Everspin launched the UNISYST MRAM family in March 2026 and positioned it as a NOR flash replacement for embedded systems at densities from 128 Mb to 2 Gb, with read bandwidth up to 400 MB/s and much faster write performance. That does not create an immediate mass shift in consumer products, because qualification timelines in electronics hardware remain long, but it does show where future substitution pressure could emerge. The most defensible positions will likely stay with vendors that combine secure storage features, low-power operation, compact packaging, and supply reliability in one portfolio. For that reason, the NOR flash for consumer electronics market is likely to remain controlled by a focused group of technically credible suppliers rather than swing toward extreme fragmentation.

NOR Flash For Consumer Electronics Industry Leaders

Winbond Electronics Corporation

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

Micron Technology Inc.

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Everspin Technologies launched the UNISYST MRAM family targeting NOR flash replacement in embedded systems at densities from 128 Mb to 2 Gb, offering read bandwidth up to 400 MB/s and write bandwidth approximately 400 times faster than NOR flash, engineering samples are scheduled for Q4 2026, presenting a medium-term displacement risk for high-performance consumer edge-AI applications.

- March 2026: GigaDevice announced the expansion of its GD25UF series 1.2V ultra-low power SPI NOR flash from 8 Mb to 256 Mb density coverage, targeting wearables, hearables, AI ASIC platforms, and medical devices with power consumption 50-70% lower than 1.8V flash and operating voltage between 1.14V and 1.26V.

- February 2026: Winbond Electronics announced full-year 2025 consolidated revenue of NTD 89.406 billion (USD 2.76 billion), a 9.55% increase year-on-year, reconfirmed its number-one global NOR flash supplier position, disclosed 2026 and 2027 production capacity as fully booked, and the board approved a record NTD 42.1 billion (USD 1.30 billion), capital expenditure plan for 2026 to expand Taichung flash capacity from approximately 50,000 to 57,000-58,000 monthly wafer starts.

- January 2026: Microchip Technology (SST) and UMC announced the commercial release of 28 nm SuperFlash Gen 4 embedded NOR flash with full automotive grade 1 certification on UMC's 28HPC+ foundry process platform, enabling volume consumer-adjacent and automotive design starts at the industry's most advanced embedded NOR flash node.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the consumer-electronics NOR flash memory market as the yearly revenue derived from newly manufactured serial and parallel NOR chips that finally sit inside smartphones, tablets, digital cameras, smart TVs, wearables, and smart-home devices where quick byte-level code execution is critical. According to Mordor Intelligence, we count only original component sales that move straight to device makers or their EMS partners, and we remove reseller mark-ups.

Scope Exclusion: Shipments bound for automotive, industrial, communication, or defense hardware and every NAND or emerging non-volatile memory lie outside this assessment.

Segmentation Overview

- By NOR Flash Type (Value And Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal And xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65-3.6 V)

- ≤1.2 V Class

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (Incl. 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Geography (Value And Volume)

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest Of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- Taiwan

- India

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Turkey

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interviewed NOR design engineers, EMS buyers, and firmware architects across Asia-Pacific, North America, and Europe. Their insights refined attach-rate, average density, and interface-mix assumptions that desk work could only approximate.

Desk Research

Our team first pulled volume signals from MIIT handset output, IDC wearable trackers, and UN Comtrade tariff codes 854232 and 854233. Price corridors were shaped through Form 10-K revenue splits, JEDEC and SIA statistical notes, plus proprietary looks on D&B Hoovers and Dow Jones Factiva that link vendor revenue to regional flow. The sources cited are illustrative; many other public and subscription materials were reviewed to cross-check and clarify findings.

Market-Sizing & Forecasting

Our top-down model converts yearly output of each device group into a NOR-addressable pool by applying penetration and density coefficients drawn from interviews and teardown logs. Supplier roll-ups, channel checks, and sampled average selling prices validate totals. Core variables such as global smartphone shipments, smartwatch volumes, the SPI to xSPI transition, die-shrink curves, and average NOR density per device feed a multivariate regression that carries the forecast through 2030, while scenario analysis cushions demand shocks.

Data Validation & Update Cycle

We run variance scans against customs data and vendor disclosures, conduct multi-step peer reviews, and sign off only after anomalies clear. Reports refresh once a year, with interim updates triggered when quarterly shipments swing beyond five percent or when a material technology inflection occurs.

Why Mordor's NOR Flash For Consumer Electronics Baseline Commands Reliability

We know published estimates often diverge because some firms bundle extra end-users, lock exchange rates, or lean solely on supplier revenue. Mordor's disciplined segmentation, annual refresh, and dual-source verification anchor a balanced baseline that users can trace back to clear device counts.

These contrasts show how our tighter scope, constant validation, and timely refresh give clients a dependable reference for strategy and planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.09 B | Mordor Intelligence | - |

| USD 5.27 B | Regional Consultancy A | Combines automotive and industrial demand, mixes NAND revenue, minimal primary checks |

| USD 2.85 B | Global Consultancy B | Uses manufacturer revenue only, 2023 FX rates, refreshes every two years |

These contrasts show how our tighter scope, constant validation, and timely refresh give clients a dependable reference for strategy and planning.

Key Questions Answered in the Report

What is driving demand for NOR flash in consumer electronics through 2031?

Demand is being supported by always-on connected devices, secure-boot requirements, OTA updates, and rising use of serial NOR in edge-AI products. The market is projected to reach USD 1.48 billion by 2031 at a 5.2% CAGR.

Which product type leads the current landscape?

Serial NOR led with 80.4% share in 2025 and is also the fastest-growing type segment, reflecting its fit with modern low-power SoC architectures and compact device layouts.

Which interface is growing fastest in this space?

Octal and xSPI is the fastest-growing interface segment with a 6.9% CAGR through 2031, driven by higher-throughput needs in wearables, AI devices, and display-heavy platforms.

Why is Asia-Pacific ahead of other regions?

Asia-Pacific held 52.8% share in 2025 and is growing at 7.2% CAGR because it combines consumer electronics assembly scale in China and Southeast Asia with wafer and design strength in Taiwan, Japan, and South Korea.

What is the main constraint on wider NOR flash adoption?

The main limit is the cost disadvantage above 256 Mb, where larger-capacity use cases such as high-resolution camera modules often shift toward NAND-based alternatives.

Which packaging format is benefiting most from device miniaturization?

WLCSP/CSP led with 37.6% share in 2025 and is also the fastest-growing packaging type at 7.9% CAGR, supported by TWS earphones, smartwatches, and other thin portable devices.

Page last updated on: