Germany NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

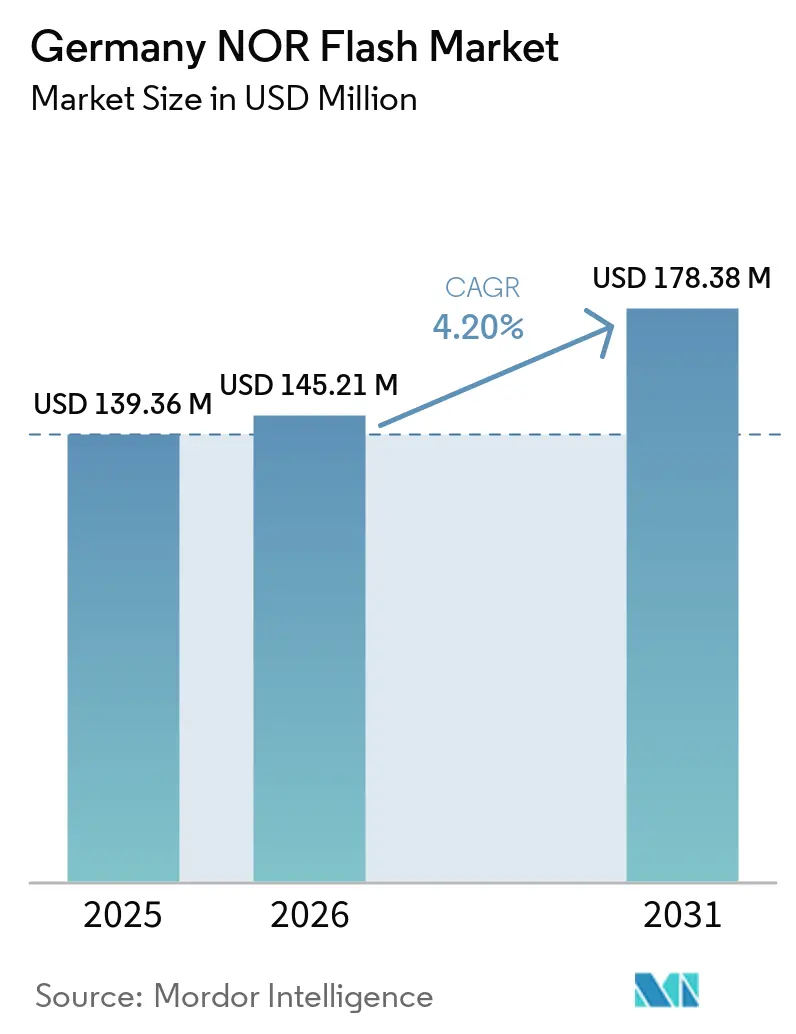

| Base Year Market Size (2025) | USD 139.36 Million |

| Market Size (2026) | USD 145.21 Million |

| Market Size (2031) | USD 178.38 Million |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany NOR Flash Market Analysis by Mordor Intelligence

The Germany NOR Flash Market size is expected to increase from USD 139.36 million in 2025 to USD 145.21 million in 2026 and reach USD 178.38 million by 2031, growing at a CAGR of 4.20% over 2026-2031. In terms of shipment volume, the market was valued at 642.17 million units in 2025 and is expected to grow from 680.46 million units in 2026 to 855 million units by 2031, at a CAGR of 4.67% during the forecast period (2026-2031). The German NOR flash memory market is driven more by automotive electronics, industrial automation, and demand for safety-critical firmware than by high-volume consumer electronics shipments. Demand remains tied to long product qualification cycles, strict reliability expectations, and the need for secure boot and fast code execution in connected systems. Policy support for domestic semiconductor capability is also making local manufacturing and design presence more important in supplier selection. Competitive positioning, therefore, depends not only on density and pricing but also on qualification status, longevity commitments, and the ability to support German OEM and Tier-1 design programs. Opportunities remain strongest in the automotive domain control, factory edge devices, and specialized high-value use cases where performance, certification, and supply assurance matter more than lowest-cost memory.

Key Report Takeaways

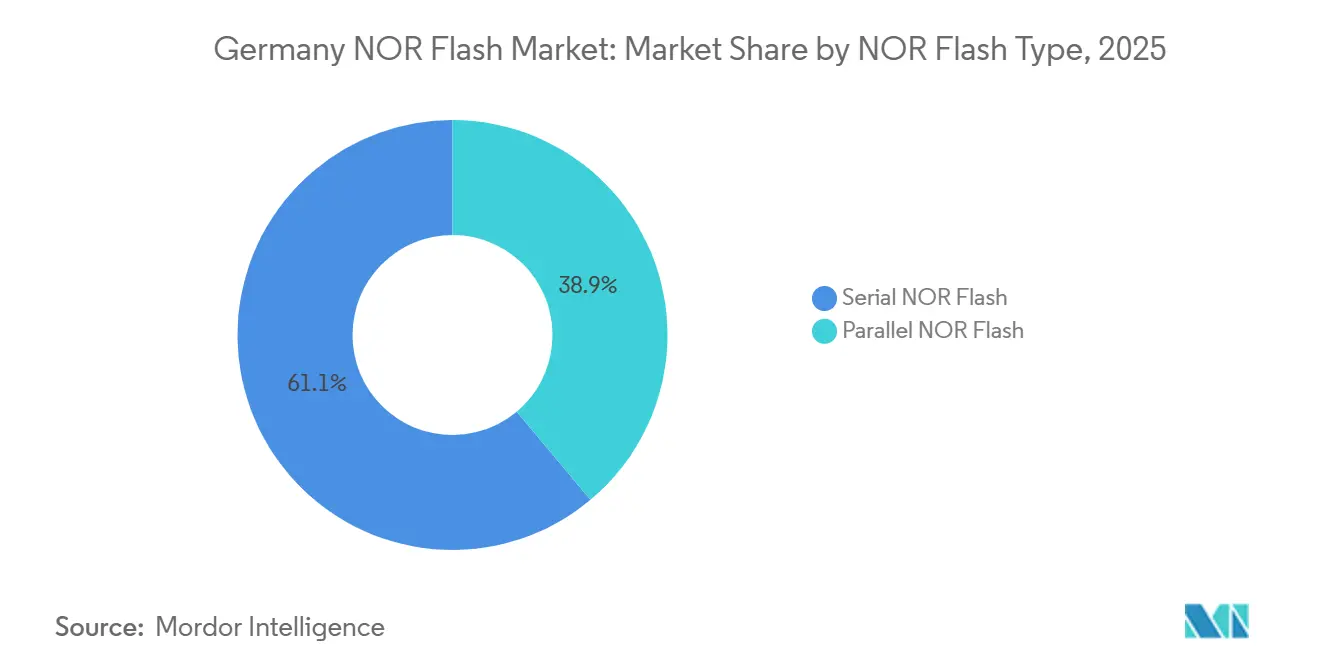

- By NOR flash type, serial NOR flash led with a 61.1% revenue share of the German NOR flash market in 2025, while serial NOR flash is projected to grow at a 5.2% CAGR through 2031.

- By interface, quad SPI held the largest revenue share at 50.4% of the German NOR flash market in 2025, while octal and xSPI recorded the highest projected CAGR at 5.6% through 2031.

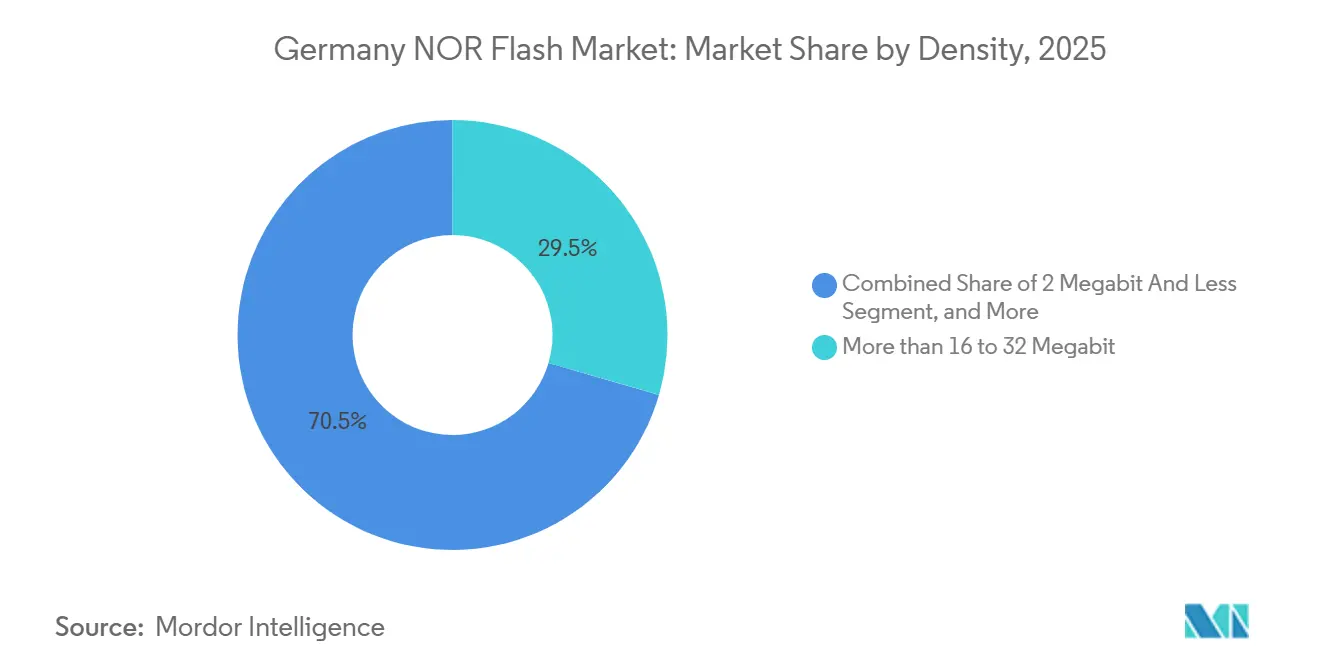

- By density, the 32 Mb tier captured a 29.5% revenue share of the German NOR flash market in 2025, while the 128 Mb tier is forecast to expand at a 5.7% CAGR through 2031.

- By voltage, the 1.8 V class held a 46.6% share of the German NOR flash market in 2025, while the 1.2 V class is expected to grow at a 5.1% CAGR through 2031.

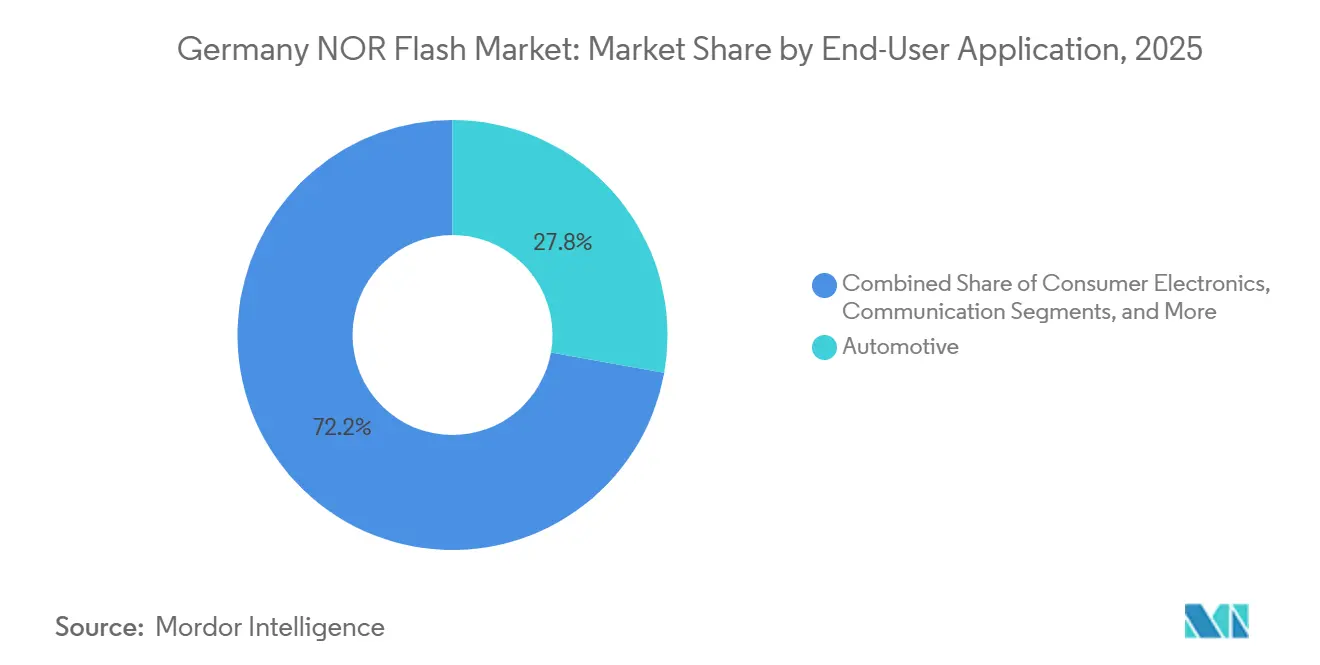

- By end-user application, automotive accounted for a 27.8% share of the German NOR flash market in 2025 and also recorded the highest projected CAGR at 6.2% through 2031.

- By process technology node, 55 nm accounted for 39.7% share of the German NOR flash market in 2025, while 28 nm and below is expected to advance at a 5.9% CAGR through 2031.

- By packaging type, QFN/SOIC held the largest share at 35.3% of the German NOR flash market in 2025, while WLCSP/CSP is forecast to grow at a 5.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide nor flash market outlook captures this forward trajectory.

Germany NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Firmware-Intensive ADAS and Domain Controllers Accelerating Automotive-Grade NOR Demand | +1.5% | Germany, concentrated in Bavaria, Baden-Württemberg, and Lower Saxony automotive corridors | Medium term (2-4 years) |

| Quad and Octal SPI Adoption for Fast-Boot IoT Edge Devices Across German Manufacturing Hubs | +0.8% | Germany, concentrated in North Rhine-Westphalia, Baden-Württemberg, and Bavaria manufacturing clusters | Short term (≤ 2 years) |

| Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices | +0.5% | Germany, with spill-over to broader European space industry suppliers | Long term (≥ 4 years) |

| Bundesregierung Mikroelektronik Funding Driving 55 nm and 40 nm On-Shore Production for NOR Self-Sufficiency | +0.4% | Germany, concentrated in Dresden, Munich, and Regensburg semiconductor clusters | Long term (≥ 4 years) |

| Secure Boot and OTA-Update Mandates in Industrie 4.0 Factories | +0.3% | Germany, with early gains in Stuttgart, Munich, and Hamburg industrial zones | Short term (≤ 2 years) |

| Low-Power 1.8 V Serial NOR Enabling Wearable and Point-of-Care Healthcare Electronics | +0.2% | Germany, with DACH spill-over | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Firmware-Intensive ADAS And Domain Controllers Accelerating Automotive-Grade NOR Demand

Germany’s OEM and Tier-1 base is moving from distributed electronic control units toward domain- and zonal-architecture approaches, and that shift increases the amount of external code storage used on each vehicle platform. The Germany NOR flash memory market benefits from this transition because fast boot, execute-in-place operation, and dependable firmware storage remain central to safety-critical automotive systems. Infineon positions its automotive memory portfolio directly into ADAS and autonomous domain controller designs, where rapid startup and dependable firmware access are required before wider system initialization.[1]Infineon Technologies AG, “Domain Controller For ADAS And Autonomous Driving,” Infineon Technologies AG, infineon.com This design pattern narrows the pool of qualified suppliers, helping certified vendors defend pricing even when broader memory pricing softens. As German vehicle architectures consolidate compute functions, firmware density continues to rise within each controller, which supports a structurally firmer demand base for automotive-grade NOR parts.

Quad And Octal SPI Adoption For Fast-Boot IoT Edge Devices Across German Manufacturing Hubs

Germany’s factory automation base is adopting faster serial interfaces because boot delays translate directly into production interruptions in sensor networks, gateways, and programmable controllers. The German NOR flash memory market is gaining from this shift as standard SPI and dual I/O devices give way to higher-bandwidth quad SPI and octal solutions in industrial edge equipment. Winbond’s W35T octal NOR supports 400 MB/s continuous read throughput at 200 MHz DDR and is positioned for industrial factory automation and IoT systems that need instant-on behavior.[2]Winbond Electronics Corporation, “W35T Octal NOR Flash Product Brief,” Winbond Electronics Corporation, winbond.com GigaDevice also moved this transition forward with its GD25NX xSPI line, which combined a 1.8 V core and 1.2 V I/O design to reduce the external power circuitry requirements in constrained edge nodes. As German machine builders push for redundant boot-code storage and lower downtime risk, octal and xSPI adoption is moving from a niche upgrade to a practical system requirement.

Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

Germany’s growing role in European space programs adds a small-volume but high-value source of demand for specialized non-volatile memory. The German NOR flash memory market benefits from this, as radiation-tolerant boot storage and FPGA configuration memory are required in satellite platforms where failure tolerance is limited. Infineon highlighted a radiation-tolerant memory portfolio for low-earth-orbit missions, reinforcing Germany’s place in the supply chain for space-grade memory products. Micron also launched a space-qualified portfolio in 2025, showing that this niche is large enough to draw broader supplier investment rather than remain a one-vendor corner of the memory business.[3]Micron Technology, Inc., “Micron Launches Space-Qualified Portfolio To Power Mission-Critical Data For Aerospace Innovation,” Nasdaq Press Release, nasdaq.com LEO constellation expansion, therefore, adds incremental demand that complements automotive and industrial growth rather than competing with it.

Bundesregierung Mikroelektronik Funding Driving 55 Nm And 40 Nm On-Shore Production For NOR Self-Sufficiency

Federal policy is now giving domestic semiconductor capability a stronger operational role in supplier positioning and investment planning. The German NOR flash memory market stands to benefit, as the German government’s microelectronics strategy aims to expand design capability, accelerate lab-to-fab transfer, and improve investment support across the semiconductor chain.[4]Bundesministerium für Forschung, Technologie und Raumfahrt, “Weichenstellung Für Deutschlands Technologische Zukunft - Bundeskabinett Beschließt Mikroelektronik-Strategie,” BMFTR, bmftr.bund.de Germany also committed a minimum of EUR 18 billion, which was USD 20.3 billion using the IRS 2025 average rate, under the Hightech Agenda Deutschland through 2029 to reinforce the country’s microelectronics position. The European Commission’s approval of Infineon’s Dresden expansion added further weight, with EUR 3.4 billion (USD 3.8 billion) in planned capacity expansion and EUR 920 million (USD 1 billion) in state subsidies tied to automotive-relevant node capacity.[5]Bundesministerium für Wirtschaft und Energie, “Europäische Kommission Genehmigt Weiteres Deutsches Chips-Act-Projekt: Infineon Baut Seine Chip-Produktion In Dresden Aus,” BMWE, bundeswirtschaftsministerium.de This policy framework supports suppliers with German manufacturing, engineering, and customer support footprints, thereby reducing the perceived risk associated with offshore-only sourcing models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Premium Over NAND Above 256 Mb Limiting High-Density Consumer Adoption | -0.8% | Germany is concentrated in consumer electronics and communication segments, with a broader European spill-over | Short term (≤ 2 years) |

| Scaling Ceilings Beyond 45 nm Steering German OEM Roadmaps Toward MRAM and ReRAM Substitutes | -0.5% | Germany, concentrated in automotive and industrial Tier-1 design centers in Munich, Stuttgart, and Hamburg | Long term (≥ 4 years) |

| Foundry Concentration in Taiwan Exposes Supply-Chain Disruption Risk for German Tier-1s | -0.3% | Germany's automotive supply chain, with broader DACH and European industrial exposure | Medium term (2-4 years) |

| ASP Compression from Expanding Chinese Capacity Impacting Vendor Margins in Europe | -0.2% | Germany is concentrated in consumer and low-density communication segments through channel pricing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By NOR Flash Type: Serial NOR Architecture Extends Its Lead Over Parallel Flash

Serial NOR flash held 61.1% of revenue in 2025, and that lead shows how strongly German OEMs prefer low pin-count memory for compact control units and industrial edge designs. In the German NOR flash memory market, serial NOR flash is also expected to grow at a 5.2% CAGR through 2031, which keeps it ahead of overall market growth. This strength comes from compatibility with smaller board layouts, lower power draw, and easier integration into automotive and industrial control modules. Parallel NOR flash still matters in older telecommunications and industrial systems that were built around parallel-bus MCU architectures and are rarely redesigned during long operating lives.

The German NOR flash memory industry is still influenced by installed-base replacement cycles, and that helps sustain parallel demand in legacy equipment even as new programs move elsewhere. Winbond and GigaDevice have both pushed the serial category forward through octal and xSPI variants that raise read bandwidth without changing the basic serial architecture path. That internal migration from standard serial interfaces to faster serial interfaces gives serial NOR an extra layer of momentum beyond its installed base. It also means suppliers must manage node capacity carefully because the same mature process nodes are increasingly used across other automotive and power semiconductor products.

By Interface: Quad SPI Dominance Is Transitioning As Octal And XSPI Gains Momentum

Quad SPI accounted for 50.4% of interface revenue in 2025, reflecting its broad compatibility with the MCU and SoC families widely used by German Tier-1 suppliers. The fastest interface growth comes from octal and xSPI, projected to grow at a 5.6% CAGR through 2031 as controller bandwidth needs continue to rise. In the German NOR flash memory market, this change is tied to multi-domain vehicle controllers and industrial edge devices that need faster code loading without a full memory architecture change. JEDEC xSPI compliance also reduces migration risk by helping suppliers and OEMs move toward 8-line devices with a familiar development path.

The German NOR flash memory industry is therefore shifting inside the serial category rather than abandoning it. Infineon’s SEMPER X1 LPDDR flash shows how far that path can go, with bandwidth designed for next-generation software-defined vehicle architectures that require rapid data access and minimal downtime. Macronix has also aligned with this direction through its xSPI-oriented memory family and automotive safety positioning, indicating broad vendor agreement on the interface roadmap. The practical outcome is that quad SPI remains the current volume standard, while octal and xSPI increasingly define where new design wins are heading.

By Density: 32 Mb Leads Today, But 128 Mb Outpaces On Momentum

The 16-32 megabit tier accounted for 29.5% of revenue in 2025, making it the largest density bracket in the German NOR flash memory market. That position reflects its fit with body control modules, powertrain controllers, and industrial edge gateways, where firmware images still sit comfortably within that range. The 128 megabit tier is projected to grow at a 5.7% CAGR through 2031 as domain controllers, digital cockpit systems, and more capable factory gateways combine software loads that were once spread across separate modules. This density shift follows the broader rise in code volume, secure update staging, and feature-rich embedded systems.

The 256 megabit and above categories are also gaining traction in systems where execute-in-place performance and certification standards matter more than raw cost efficiency. Lower-density tiers continue to serve long-life industrial instrumentation and simpler IoT endpoints, making them commercially relevant even if growth is modest. The German NOR flash memory market for the 32 megabit tier remains important because it accounts for a large share of current automotive and industrial production programs. At the same time, larger densities are becoming more practical as connected devices require more room for secure firmware images, update staging, and longer software support windows.

By Voltage: 1.8 V Class Leads, But 1.2 V Class Is The Fastest-Growing Frontier

The 1.8 V class held a 46.6% share in 2025, giving it the largest position within voltage segmentation in the German NOR flash memory market. That lead reflects its strong fit with low-power automotive, IoT, and embedded control designs where reliable serial NOR performance matters but board power budgets remain tight. Wide-voltage parts still serve mixed-rail board environments, and 3 V devices keep a place in established industrial systems with older power architectures. The fastest growth is coming from the 1.2 V class, which is forecast to expand at a 5.1% CAGR through 2031 as designers reduce power draw and remove extra voltage support circuitry.

GigaDevice reinforced this direction at Embedded World 2026 by extending its GD25UF family from 8 Mb to 256 Mb, widening the addressable set of low-voltage storage applications. The company had already shown the same design logic in 2025 with dual-power supply NOR meant for 1.2 V SoC environments. That matters for healthcare wearables and point-of-care devices where battery life, board size, and component count directly affect product performance. As more connected medical and edge devices move to lower-voltage logic, 1.2 V NOR becomes a more practical option rather than a narrow specialty choice.

By End-User Application: Automotive Dominates Value And Leads Growth

Automotive accounted for 27.8% of revenue in 2025 and is the fastest-growing end-user segment, with a 6.2% CAGR through 2031. This means automotive combines current scale and future momentum in the German NOR flash memory market, which is unusual and reflects the software expansion occurring in modern vehicles. German Tier-1 suppliers need memory parts that meet automotive qualification, long retention, endurance, and functional safety requirements, while maintaining a high barrier to entry. Industrial is the second-largest demand base, supported by PLCs, gateways, robotics, and secure connected equipment across manufacturing clusters.

Healthcare electronics remains smaller in absolute terms, but it is becoming increasingly strategically important because compact connected devices require low-voltage firmware storage with dependable startup behavior. Other end uses, including defense, network infrastructure, and space systems, have lower volumes but higher selling prices due to extended lifecycles and specialized performance requirements. The German NOR flash memory market share held by automotive at 27.8% in 2025 shows how central vehicle electronics has become to overall demand. Infineon’s domain controller positioning and Winbond’s industrial and automotive memory offerings both reflect how suppliers are aligning their product roadmaps with these higher-value embedded applications.

By Process Technology Node: 55 Nm Anchors Automotive Volume While Sub-28 Nm Defines The Growth Frontier

The 55 nm node accounted for 39.7% of process technology revenue in 2025, giving it the largest position in the German NOR flash memory market. Its lead reflects the maturity of this node for automotive qualification, where proven reliability often matters more than aggressive scaling. At the same time, 28 nm and below is projected to grow at a 5.9% CAGR through 2031 as Europe builds more advanced specialty process capacity and advanced embedded memory options become more practical. Older nodes, such as 65 nm and 90 nm, still matter in communication infrastructure, defense systems, and long-life industrial designs, where requalification costs remain high.

The segment is therefore split between a durable mature-node base and a smaller but faster advanced-node frontier. Germany’s policy push for stronger semiconductor capability supports both ends of that structure by backing local manufacturing and R&D programs. Infineon’s and TSMC’s work on advanced embedded RRAM shows why sub-45 nm memory scaling is becoming more selective and more dependent on proprietary technology paths. That leaves 55 nm well entrenched in current automotive production, even as advanced nodes gather strategic importance for future platforms.

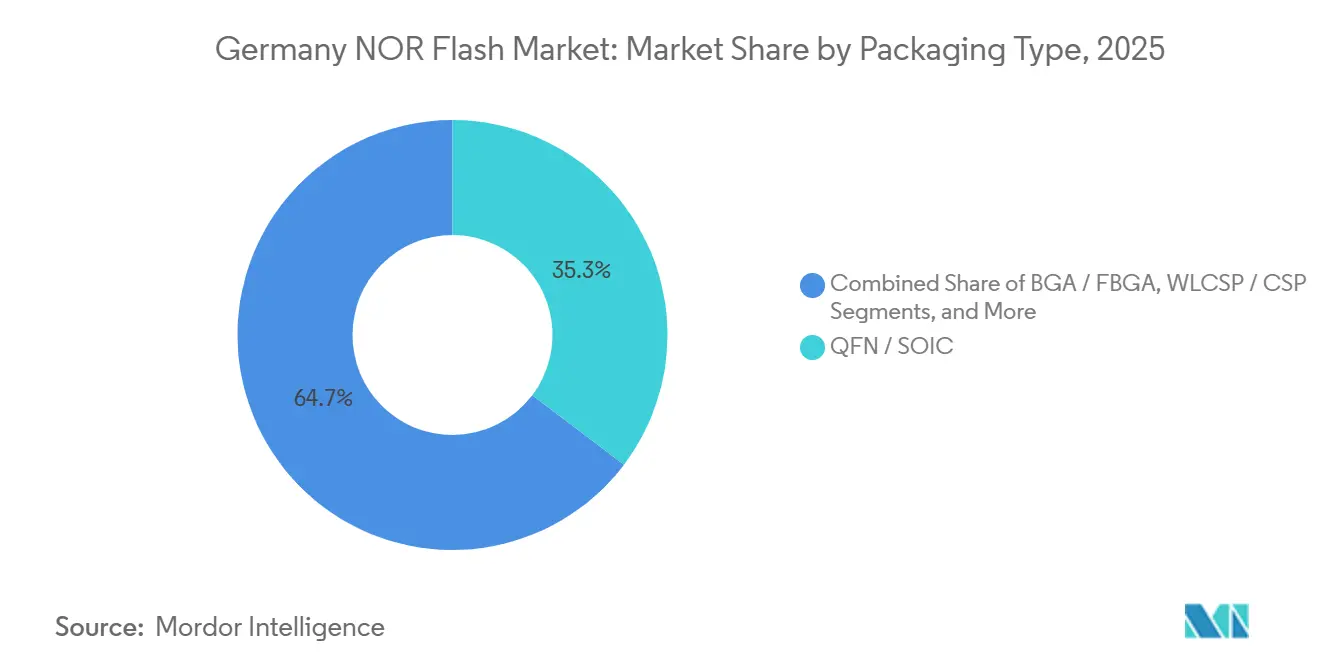

By Packaging Type: QFN/SOIC Leads, WLCSP/CSP Is The Fastest-Growing Format

QFN/SOIC held the largest packaging share at 35.3% in 2025, showing that thermal robustness, assembly familiarity, and reworkability still matter in automotive and industrial electronics. In the German NOR flash memory market, WLCSP/CSP is the fastest-growing packaging format, with a 5.8% CAGR through 2031, driven by miniaturization as a design rule in wearables, sensor modules, and compact automotive electronics. BGA/FBGA is also gaining ground in higher-density systems where pin count and signal integrity matter more. Other legacy package types continue to lose relevance as serial interfaces reduce line count and new layouts prioritize smaller footprints.

Infineon’s SEMPER Nano family illustrates why wafer-level packaging is becoming increasingly important in small-form-factor designs, especially when both low voltage and tight board area are required. Packaging choices are also shaped by EU material and compliance requirements, which make lead-free compatibility a baseline condition for commercial use. The German NOR flash memory market remains substantial, with attached QFN/SOIC sizes, because of its broad industrial and automotive installed base. Even so, WLCSP/CSP is increasingly where new compact-device programs are being won.

Geography Analysis

The German NOR flash memory market was valued at USD 139.4 million in 2025 and is projected to reach USD 178.4 million by 2031 at a 4.2% CAGR. This single-country profile is anchored by automotive electronics and industrial automation, which together create a demand mix that favors reliability, long product life, and firmware integrity. Germany’s automotive export base remained large at EUR 258 billion, which was USD 291.5 billion, in 2024, and that helps sustain a demanding domestic ecosystem for AEC-Q100 qualified memory components. The concentration of major engineering and manufacturing centers across Bavaria, Baden-Württemberg, Lower Saxony, and other industrial regions also shortens the path from design win to wider platform adoption. The German NOR flash memory market share tied to automotive and industrial programs is therefore supported by both the size of the domestic equipment base and the density of local engineering activity.

Industrial automation gives the market a second durable pillar beyond vehicle production. Siemens’ SIMATIC IOT2050 platform documentation shows the use of OSPI boot architecture, which confirms that higher-bandwidth serial NOR interfaces are already present in German-made industrial equipment. Fraunhofer IMS has also continued work on secure key memory and physically unclonable function technology for Industry 4.0 electronics, which aligns with the wider shift toward hardware-level security in connected factory devices. These factors keep demand stable even when short-cycle electronics spending weakens.

Germany also has a smaller but important role in space-related electronics and semiconductor sovereignty efforts. The federal push behind IPCEI Advanced Semiconductor Technologies strengthens the local case for advanced semiconductor R&D and manufacturing, and that supports a more resilient supply base for memory used in strategic applications. At the same time, Germany’s reliance on imported semiconductors from Taiwan keeps supply-chain resilience high on procurement agendas, which is why dual sourcing and European fabrication are gaining more weight in sourcing decisions. That combination of strong embedded demand and rising supply security focus continues to support the local outlook.

The nor flash market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe and Asia. This is complemented by country-specific insights for Italy, United Kingdom, Japan, India, South Korea, Mexico, and France, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

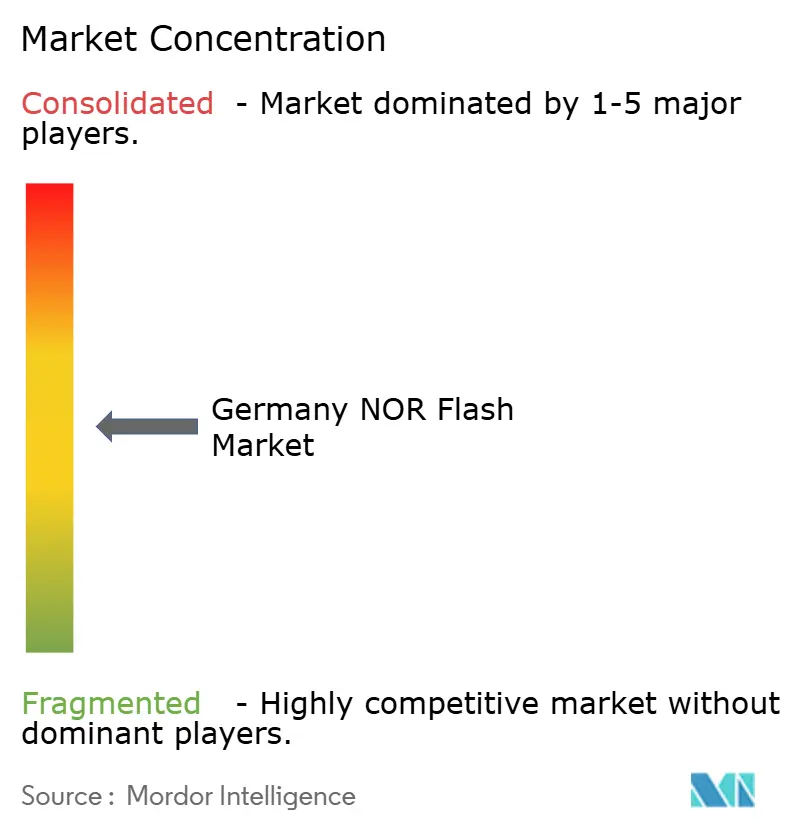

The German NOR flash memory market shows moderate concentration, with Infineon holding the strongest domestic strategic position through local manufacturing, automotive customer relationships, and a portfolio aligned with safety-critical code storage. Winbond remains an important competitor in mid-density automotive and industrial sockets, where pricing, longevity commitments, and qualified product availability help it stay relevant. Macronix competes through product breadth and automotive safety positioning, while GigaDevice has been especially active in product launches tied to low-voltage and xSPI use cases. Integrated Silicon Solution Inc. also remains part of the active supplier set across industrial and communications applications. At the lower-density end, Chinese suppliers such as GigaDevice, Puya, and Zbit are putting price pressure on European channels, even though the high-density automotive end remains far more selective.

Several strategic moves over 2025 and 2026 show how vendors are trying to widen their position in the German NOR flash memory market. Macronix expanded its MXSMIO memory family with ISO 26262 ASIL-D support in January 2026, which improved its ability to compete for automotive design wins that previously favored more established safety-qualified suppliers. GigaDevice widened its low-voltage roadmap in both 2025 and 2026, first with dual-power-supply SPI NOR and then with a broader 1.2 V density range aimed at AI, wearable, and edge applications. Winbond also differentiated through secure flash by integrating post-quantum cryptography into its TrustME line for code-storage applications. These moves show that differentiation is now built around safety, security, power efficiency, and interface speed rather than solely around density.

The competitive white space remains strongest in high-density automotive-grade, space-grade, and security-enhanced NOR products, where qualification and trust matter more than low-priced, high-volume supply. Infineon’s product positioning in the automotive domain, control, and high-bandwidth flash keeps it close to the center of these premium design cycles. Smaller suppliers such as Alliance Memory, AMIC Technology, and Etron Technology continue to serve longevity-sensitive replacement demand in older industrial and defense systems. That leaves the market competitive across broad embedded applications, but more concentrated where qualification, safety, and secure lifecycle support are harder to replicate.

Germany NOR Flash Industry Leaders

Winbond Electronics Corporation

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

Infineon Technologies AG

Micron Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GigaDevice announced the expansion of its GD25UF series 1.2 V ultra-low power SPI NOR Flash to a full density range of 8 Mb to 256 Mb at Embedded World 2026, Nuremberg, Germany. The expansion targets AI computing, wearable medical devices, and edge AI platforms, and the devices entered mass production immediately.

- January 2026: Macronix expanded its MXSMIO flash memory family to include ISO 26262 ASIL-D certification for automotive applications. The OctaFlash MX25/6 and QSPI MX25/66/U/L_G series are available in production, enabling Macronix to compete for automotive design wins in Germany previously dominated by Infineon’s SEMPER family.

- November 2025: GigaDevice launched the GD25NX series xSPI NOR Flash with a 1.8 V core and 1.2 V I/O design in 64 Mb and 128 Mb densities. The dual-voltage architecture eliminates the need for external boost circuitry for 1.2 V SoC applications, reducing system power consumption and BOM cost in IoT and wearable designs.

- October 2025: The German Federal Cabinet approved the Mikroelektronik-Strategie, establishing a national roadmap for semiconductor R&D, skilled workforce development, and manufacturing investment. The BMFTR committed to a minimum of EUR 18 billion (USD 20.3 billion) under the Hightech Agenda Deutschland and launched a national chip design competence center to accelerate "from lab to fab" transitions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the German NOR flash memory market as the invoiced value of newly manufactured serial and parallel NOR chips shipped to domestic OEM, ODM, and distributor channels across automotive, industrial, consumer, communication, and other end uses. Values are expressed in constant 2024 USD.

Scope exclusion: We exclude NOR blocks embedded inside system-on-chips or evaluation boards and any refurbished or gray-market inventory.

Segmentation Overview

- By Type (Value and Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Other Sub-1.8 V Classes (1.2 V, 2.5 V, 5 V)

- By End-User Application (Value and Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packages

Detailed Research Methodology and Data Validation

Primary Research

We interviewed purchasing heads at Tier-1 auto suppliers, EMS buyers, and memory distributors in Bavaria, Saxony, and NRW, and ran short surveys with IoT start-ups. Their feedback confirmed live ASP brackets, density roadmaps, and interface changeover dates that we fed into the model.

Desk Research

We began with tier-one public datasets such as Statistisches Bundesamt trade codes, KBA vehicle output, ACEA EV registrations, VDMA semiconductor machinery indices, and patent families mined through Questel, which together revealed unit flows, density shifts, and production ramp timing.

Our team then screened company filings, Infineon expansion releases, and trade press archived in Dow Jones Factiva and D&B Hoovers, aligning ASP commentary with shipment tallies.

The sources named illustrate, not exhaust, the wider set consulted during data collection.

Market-Sizing & Forecasting

We apply a top-down construct: domestic production, imports, and re-export volumes are reconstructed, adjusted for capacity utilization, and multiplied by verified ASP ranges; selective bottom-up rollups of vendor invoices validate totals. Key variables include EV assembly volume, Industrie 4.0 controller shipments, average code size per ECU, interface-mix shares, and density migration rates. A multivariate regression with ARIMA overlays produces the 2025-2030 outlook, and gaps are bridged with moving-average interpolation agreed upon during interviews.

Data Validation & Update Cycle

Before sign-off, Mordor analysts run variance dashboards against customs data and trade indices, re-contacting sources when deviations exceed two standard deviations. We refresh the model annually and issue interim updates for material fab or policy events.

Why Mordor's Germany NOR Flash Baseline Earns Trust

We acknowledge that published estimates often diverge because firms cherry-pick chip types, use different FX dates, or project densities with optimistic yield curves.

Mordor counts only traceable, freshly produced chips, applies monthly Bundesbank rates, and refreshes every twelve months, whereas other publishers fold in refurbished supply or broad flash categories, inflating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 139.36 M (2025) | Mordor Intelligence | - |

| USD 245.8 M (2024) | Regional Consultancy A | Serial NOR only, national sales up-scaled via smartphone penetration |

| USD 2.8 B (2025) | Industry Blog B | Groups all non-volatile codes under NOR customs headings |

| USD 5.78 B (2024) | Trade Journal C | Adds embedded NOR in SoCs and speculative fab output |

Overall, we believe Mordor's disciplined scope selection, transparent variables, and frequent refreshes deliver a balanced, repeatable baseline that decision makers can rely upon.

Key Questions Answered in the Report

What is the projected value of Germany's NOR flash memory demand by 2031?

It is projected to reach USD 178.4 million by 2031, rising from USD 139.4 million in 2025 at a 4.2% CAGR over 2026-2031.

Which end-user group is driving the strongest growth in Germany?

Automotive is the key growth engine. It held 27.8% of revenue in 2025 and is projected to expand at a 6.2% CAGR through 2031.

Why is serial NOR flash ahead of parallel NOR in Germany?

Serial NOR led with 61.1% share in 2025 because German OEMs favor low-pin-count, low-power memory that fits compact automotive and industrial designs.

Which interface is gaining the most momentum in new designs?

Octal and xSPI are growing the fastest at a 5.6% CAGR through 2031 as domain controllers and industrial edge devices need higher read bandwidth and faster boot performance.

What process node remains most important for current production?

The 55 nm node led with 39.7% of revenue in 2025 because it is deeply established in automotive-qualified NOR production and long validation cycles.

What are the main risks for suppliers through the forecast period?

The main risks are cost pressure versus NAND at higher densities, and longer-term substitution pressure from MRAM and ReRAM in advanced-node platforms.

Page last updated on: