Industrial Agitators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.92 Billion |

| Market Size (2031) | USD 3.61 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Agitators Market Analysis by Mordor Intelligence

The industrial agitators market size is expected to grow from USD 2.80 billion in 2025 to USD 2.92 billion in 2026 and is forecast to reach USD 3.61 billion by 2031 at 4.33% CAGR over 2026-2031. The industrial agitators market is being supported by large capital programs across chemicals, pharmaceuticals, and water infrastructure, where agitation systems now need to meet stricter efficiency, hygiene, and containment requirements at the same time. Buyers are placing more weight on lifecycle cost than on initial purchase price, which is shifting demand toward variable-frequency-driven units with lower power use per unit of throughput. That change is altering how suppliers price, position, and service their portfolios, especially in applications where energy savings can be demonstrated at scale. The industrial agitators market is also being shaped by the electrification of process industries, as operators replace oversized fixed-speed equipment with electronically controlled systems that can respond better to changing batch conditions. Alloy cost pressure and the wider use of single-use bioprocess vessels in small-batch pharmaceutical manufacturing remain real constraints, but the industrial agitators market continues to gain support from retrofit demand and new slurry-mixing requirements tied to EV battery production.

Key Report Takeaways

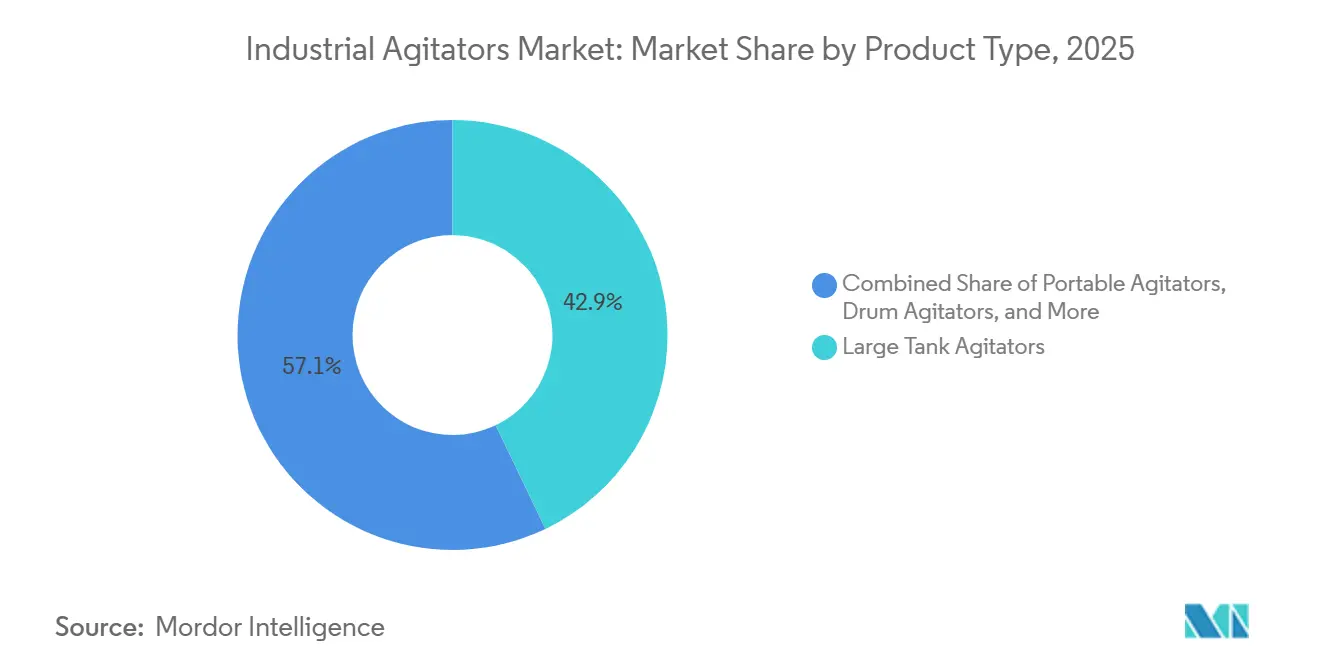

- By product type, large tank agitators held 42.89% of the industrial agitators market in 2025, while magnetic agitators are projected to grow at a 5.12% CAGR through 2031.

- By mounting configuration, top-mounted agitators held 72.32% of the industrial agitators market in 2025, while bottom-mounted designs are forecast to expand at a 4.91% CAGR through 2031.

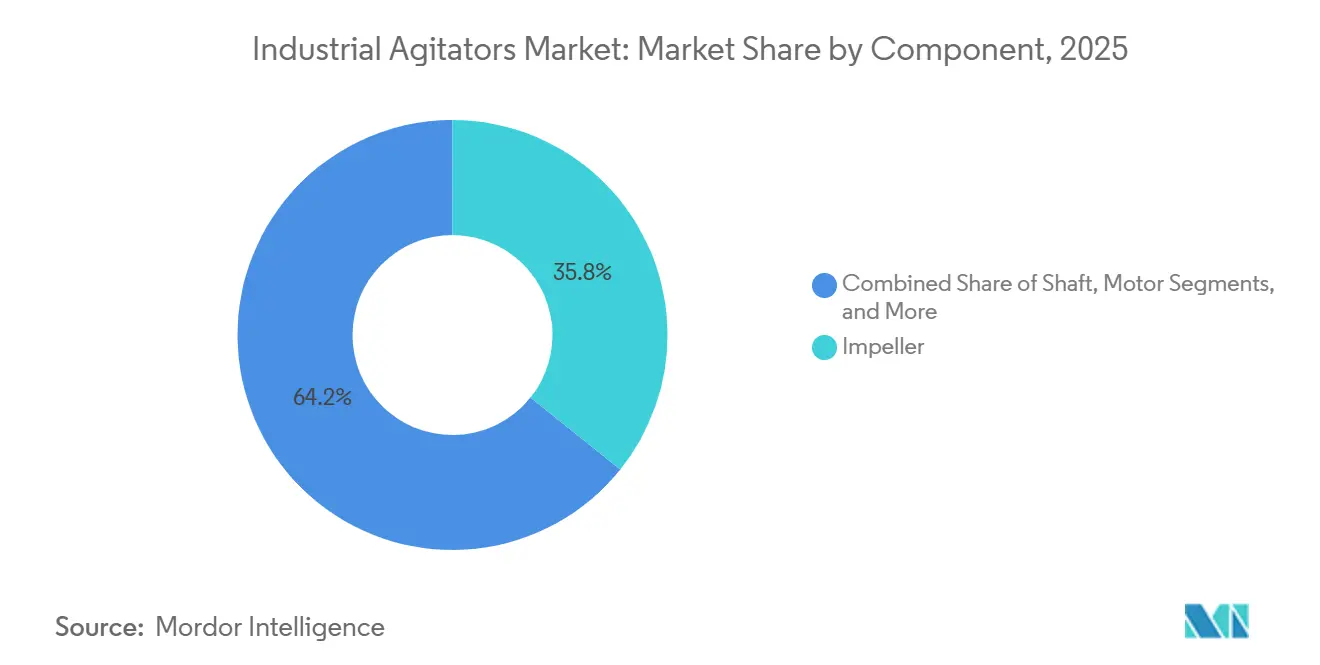

- By component, impellers accounted for 35.76% of the industrial agitators market in 2025, while seals and bearings are expected to grow at a 4.84% CAGR through 2031.

- By mixing flow pattern, axial flow represented 48.84% of the industrial agitators market in 2025, while tangential flow is set to advance at a 4.95% CAGR through 2031.

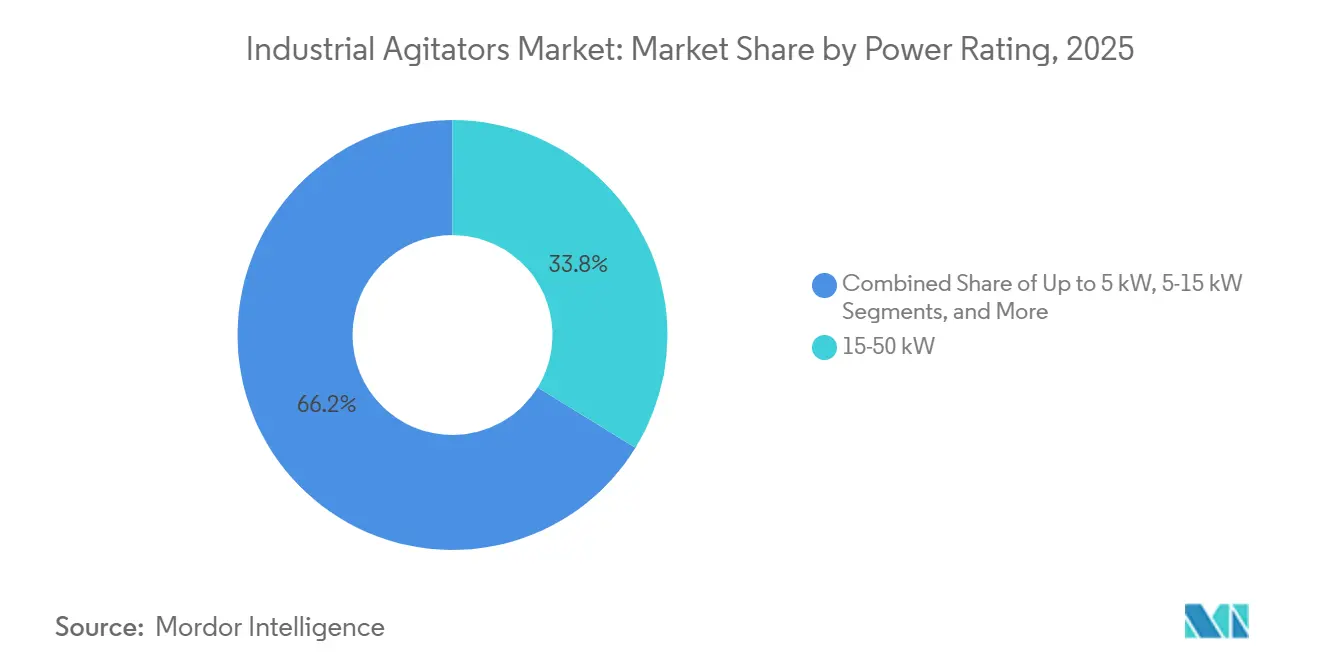

- By power rating, the 15-50 kW segment accounted for 33.78% of the industrial agitators market in 2025, while the up-to-5 kW segment is projected to grow at a 4.76% CAGR through 2031.

- By end-user industry, chemicals and petrochemicals held 30.33% of the industrial agitators market in 2025, while pharmaceuticals and biotechnology are forecast to grow at a 4.69% CAGR through 2031.

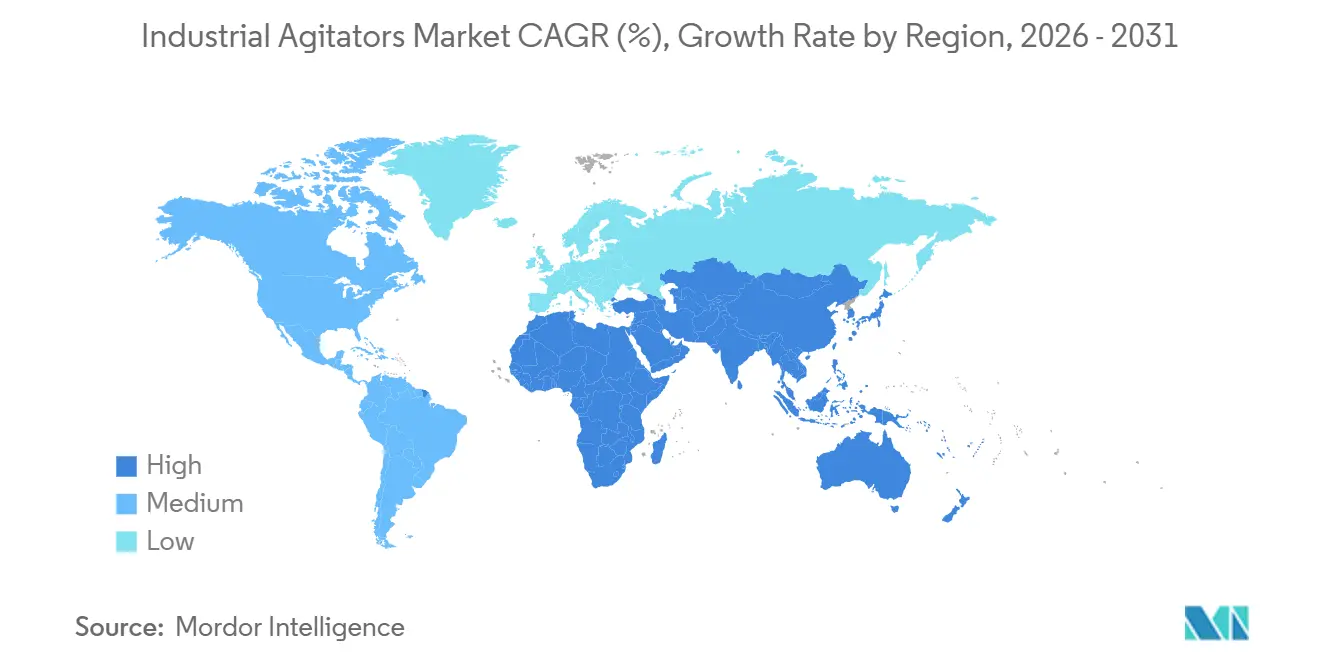

- By geography, Asia-Pacific held 38.54% of the industrial agitators market in 2025 and is also the fastest-growing regional segment with a 4.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Agitators Market Trends and Insights

Driver Imapct Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chemical and Petrochemical Capacity Additions | +1.0% | Global, concentrated in Asia-Pacific, the Middle East, and North America | Short term (≤ 2 years) to Medium term (2-4 years) |

| Wastewater Treatment Retrofit and Energy-Efficiency Spending | +0.8% | Global, strongest in North America, Europe, and APAC urban centers | Medium term (2-4 years) |

| Pharmaceutical and Bioprocess Capacity Expansion | +0.7% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) to Long term (≥ 4 years) |

| Food and Beverage Hygiene And Batch Consistency Requirements | +0.6% | Global, strongest in North America, Europe, and Southeast Asia | Short term (≤ 2 years) to Medium term (2-4 years) |

| EV Battery Slurry Mixing Line Investments | +0.3% | Asia-Pacific, with spillover to Europe and North America | Short term (≤ 2 years) |

| Shift Toward Magnetic-Drive Agitators in Zero-Leakage Duty | +0.2% | Global, strongest in North America, Europe, and Japan | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chemical and Petrochemical Capacity Additions Drive Agitator Procurement

Chemical and petrochemical capacity additions remain the strongest demand driver for the industrial agitators market because every new reactor train, polymerization vessel, and effluent tank needs a defined agitation solution. These projects often require large-tank, high-torque, or side-entry systems that are engineered around vessel size, fluid behavior, and process duty rather than drawn from a standard catalog. That raises equipment value and also extends engineering and delivery timelines compared with simpler mixing equipment. Procurement, therefore, moves early in the project cycle, and suppliers that enter during FEED or detailed design can secure specifications before final equipment awards. This pattern gives OEMs with local engineering support and process application depth a clear advantage in the industrial agitators market.

Wastewater Treatment Retrofit and Energy-Efficiency Spending Broaden the Installed Base

Wastewater treatment spending is expanding the industrial agitators market through retrofit activity as municipalities and industrial operators replace aging mixers to cut energy use and improve process stability. The driver is less about a wave of new plants and more about lowering operating costs while meeting tighter performance expectations in existing facilities. Xylem reported that the Clifton Sanitation District in Colorado cut energy consumption by more than 50% and eliminated 99% of settling issues after upgrading to adaptive mixers in oxidation ditch service.[1]Xylem, “Adaptive Mixers Eliminate 99% of Ditch Settling Problems for Clifton Sanitation District,” Water Plant Technology, waterplant.tech Retrofit demand is also widening through anaerobic digestion and biogas-to-power projects, where continuous-duty mixing is needed to keep sludge and slurry streams uniform. Operators are increasingly willing to pay more upfront when a supplier can document savings over a short payback period, which supports value growth in the industrial agitators market.

Pharmaceutical and Bioprocess Capacity Expansion Drives Specification Complexity

Pharmaceutical and bioprocess investment is raising the technical bar in the industrial agitators market because these facilities demand higher cleanliness, traceability, and containment than standard-duty applications. Johnson and Johnson announced a more than USD 1 billion investment in a next-generation cell therapy manufacturing facility in Pennsylvania, and AbbVie announced a USD 1.4 billion pharmaceutical manufacturing campus in Durham, North Carolina.[2]Johnson and Johnson, “Johnson and Johnson Expands U.S. Footprint With More Than USD 1 Billion Investment in Next Generation Cell Therapy Manufacturing Facility in Pennsylvania,” BioSpace, biospace.com Bora Biologics also completed a USD 30 million expansion in San Diego in January 2026, adding 500 L to 2,000 L single-use bioreactor capacity that still depends on specialized media and buffer preparation systems. FDA requirements under 21 CFR Part 211 continue to push equipment designs toward cleanable geometry, validated materials, and tighter containment expectations. Even so, wider use of single-use vessels creates a substitution risk at smaller batch sizes, which means growth in this part of the industrial agitators market is strong but not unlimited.

Food and Beverage Hygiene and Batch Consistency Requirements Elevate Engineering Standards

Food and beverage processors are treating agitator selection as a hygiene and product-quality decision, which is lifting the average specification level in the industrial agitators market. Traceability and contamination control now carry more weight in equipment selection because processors need cleaner designs and more consistent batch handling. FSMA requirements have reinforced the need for stronger preventive controls and better process discipline across food operations. Alfa Laval's EnSaLine launch in March 2026 directly addressed this need with a 3-A certified hygienic platform, FDA-compliant non-metallic parts, a fully flushable design, and CIP while running capability.[3]Alfa Laval, “New Agitator Platform From Alfa Laval, A Milestone Breakthrough in Effortless Mixing in Hygienic Production,” Alfa Laval, alfalaval.us The result is a two-speed industrial agitators market, where regulated exporters are moving to premium hygienic designs while price-sensitive domestic processors continue to buy simpler impeller-in-vessel systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Lifecycle Cost of Large Industrial Agitators | -0.5% | Global, most acute in emerging markets with constrained maintenance budgets | Medium term (2-4 years) to Long term (≥ 4 years) |

| Stainless Steel and Alloy Price Volatility | -0.4% | Global, with higher exposure in Europe and North America | Short term (≤ 2 years) |

| Single-Use Mixing Adoption in Small-Batch Bioprocessing | -0.2% | North America, Europe, and developed Asia-Pacific markets | Medium term (2-4 years) to Long term (≥ 4 years) |

| ATEX, Noise, and Mechanical Seal Compliance Complexity | -0.2% | Europe, North America, and global cGMP markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Lifecycle Cost of Large Industrial Agitators Constrains Capacity Adoption

Lifecycle cost remains a meaningful restraint on the industrial agitators market because maintenance, seal replacement, gearbox work, erosion, and downtime can exceed the initial purchase price over a long service period. This issue is most visible in price-sensitive markets where operators delay replacement even after equipment moves beyond its preferred engineering life. The burden is heavier in abrasive and high-solids duties such as mining, where wear on seals and impellers is faster and more expensive to manage. Even in developed markets, approvals can be harder to secure because total ownership cost is less visible than it is for simpler rotating equipment. Suppliers are responding with digital monitoring and predictive maintenance tools, but the industrial agitators market still faces adoption limits where end users do not yet have the data systems needed to prove lifecycle savings.

Stainless Steel and Alloy Price Volatility Pressures Margins and Project Timelines

Stainless steel and alloy volatility is constraining the industrial agitators market because wetted parts, shafts, and impellers in hygienic and corrosion-duty service depend heavily on nickel-bearing grades such as 316 and 316L. When surcharge levels rise, catalog equipment becomes harder to price without compressing supplier margins. Custom projects can pass part of the increase through escalation clauses, but standard units usually have less pricing flexibility. Buyers also tend to slow award decisions when raw material costs are unstable because they want more certainty on final equipment pricing and project budgets. This leaves the industrial agitators market exposed to shorter quoting windows, longer negotiations, and weaker contribution on high-volume standard-duty units.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Large-Tank Dominance Shaped by Chemical Process Architecture

Large tank agitators held 42.89% of the industrial agitators market share in 2025, reflecting their central role in chemical, petrochemical, and water-treatment vessels that need continuous-duty, high-torque mixing. These systems are usually engineered to vessel specification, which raises unit value and creates longer order-to-delivery cycles than standard catalog products. Portable agitators serve a different layer of demand in small-batch blending, industrial maintenance, and field-mixing work where ease of deployment and replacement frequency matter more than customization. Drum agitators also remain relevant in cosmetics, coatings, and specialty chemicals because users value fast turnover and simple handling across repeated short-cycle duties.

Magnetic agitators are the fastest-growing product type in the industrial agitators market, with a 5.12% CAGR projected through 2031 as pharmaceutical and specialty chemical operators move toward zero-leakage designs. Their appeal comes from better containment, lower seal-related failure risk, and stronger fit with cleanability requirements, even when the initial purchase cost is higher than for conventional units. Alfa Laval's EnSaLine B and EnSaLine S platforms, introduced in March 2026, were built around hygienic service, flushable design, and faster maintenance access. Other product types, including hybrid solutions used in continuous-flow specialty processes, remain narrower in volume but support the industrial agitators market by filling application gaps that standard impeller systems do not always address.

By Mounting Configuration: Top Entry Holds Scale While Bottom-Mounted Systems Gain Priority

Top-mounted configurations accounted for 72.32% share of the industrial agitators market size in 2025, supported by their very large installed base in chemicals, water treatment, and mining. Plants in these sectors often prefer top entry because tank access from above is straightforward, and maintenance can be managed with existing overhead lifting arrangements. Side-mounted systems remain important in crude oil blending and large storage tanks where vessel diameter and headroom make top entry less practical. This keeps the traditional mounting mix stable across bulk-process industries even as new hygienic facilities adopt different layouts.

Bottom-mounted agitators are forecast to grow at a 4.91% CAGR through 2031 in the industrial agitators market as biopharmaceutical and food processors favor closed-vessel processing, full drainability, and cleaner vessel tops. The change is structural because many new sterile and hygienic plants now specify these layouts early in process design rather than adding them later. Sulzer's Scaba STA launch in July 2025 showed that major suppliers are still improving the efficiency and hydraulic performance of top-entry units to defend mature share positions.[4]Sulzer, “Sulzer Launches Energy Efficient Scaba STA Vertical Agitator,” Impeller.net, impeller.net The industrial agitators market is therefore seeing a mounting mix that changes by end use and compliance need rather than through a full shift away from top-mounted equipment.

By Component: Efficiency Competition Centers on the Core Mixing Stack

Impellers represented 35.76% of revenue in 2025, making them the largest component segment because geometry and metallurgy shape process performance more than any other single element. In practice, impeller design determines circulation pattern, shear profile, solids suspension, gas dispersion, and power draw, so buyers treat it as the core value driver in the assembly. Axial-flow hydrofoils and radial-flow turbines remain the main formats for broad chemical and food processing duties. Competition is increasingly centered on proprietary designs that improve mixing efficiency without forcing major changes in vessel design or installed motor power.

Seals and bearings are forecast to expand at a 4.84% CAGR through 2031 in the industrial agitators market as replacement demand rises and containment expectations tighten in high-purity and hazardous service. Growth is also being supported by wider use of double mechanical and magnetic-drive arrangements in applications where leakage control matters more than upfront equipment cost. Motor selection is moving toward IE4 and IE5 efficiency classes in continuous-duty applications, while shaft design is becoming more optimized through digital engineering methods that reduce unnecessary overdesign. This makes the component stack a major source of performance differentiation in the industrial agitators market, not just a bill-of-materials decision.

By Mixing Flow Pattern: Axial Flow Leads While Tangential Flow Gains in Sensitive Processes

Axial flow held 48.84% of the market in 2025 because it remains the most efficient choice for bulk blending, solids suspension, and heat-transfer duty in large industrial vessels. That position is closely tied to chemical and water treatment applications where circulation and throughput matter more than localized shear. Radial flow still has a clear role in gas-liquid mass transfer, especially in fermentation and reaction systems where dispersion quality affects process outcomes. Multi-impeller shafts that combine axial and radial elements are becoming more common as operators handle taller vessels and more complex viscosity profiles.

Tangential flow is the fastest-growing pattern in the industrial agitators market, with a 4.95% CAGR expected through 2031 as fermentation, crystallization, and bioprocess systems prioritize lower shear and more controlled wall sweeping. These designs are valued because they reduce product stress and support more stable handling of sensitive formulations and crystal growth processes. EKATO highlighted this direction through its TORUSJET-based crystallization approach and its modular hydrogenation platform for API production. As higher-value process duty expands, the industrial agitators market is moving toward more application-specific flow selection and less reliance on legacy design habits.

By Power Rating: Mid-Range Units Stay Core While Lower-Power Systems Expand Faster

The 15-50 kW band held 33.78% of revenue in 2025, which reflects its fit with a broad range of chemical, water, and mid-scale pharmaceutical vessels. This range benefits from wide motor availability, familiar gearbox ratios, and established seal packages, which keep purchasing practical for common industrial duties. Above-50 kW systems remain essential in bulk chemicals, mining, and large treatment facilities where lifecycle energy use matters more than initial capital cost. The 5-15 kW band continues to serve drum agitators, portable units, and pilot-scale process work that tends to generate frequent replacement demand.

The up-to-5 kW segment is projected to grow at a 4.76% CAGR through 2031 in the industrial agitators market as laboratory-adjacent and small-batch applications expand. These smaller systems are well-suited to benchtop bioreactors, development vessels, and specialty ingredient lines where footprint and precision matter more than raw power. At the same time, improved impeller efficiency can allow operators to operate in a lower power band without losing process performance, moderating revenue growth in the middle of the range. Demand by power class in the industrial agitators market, therefore, reflects both true expansion and substitution toward more efficient system design.

By End-User Industry: Chemicals Anchor Volume While Pharma Lifts Value

Chemicals and petrochemicals accounted for 30.33% of revenue in 2025, making this the largest end-user group because agitation is embedded across reaction, blending, neutralization, and crystallization steps. The segment remains broad and resilient because equipment demand comes from both base chemicals and higher-value specialty chemistries. Water and wastewater treatment add a steady stream of replacement demand, while food and beverage upgrades are lifting specification quality toward more hygienic systems. Minerals and mining, paper and pulp, and energy and power continue to provide a dependable base for the industrial agitators market through high-torque and abrasion-resistant duties.

Pharmaceuticals and biotechnology are projected to expand at a 4.69% CAGR through 2031 in the industrial agitators market, supported by biologics, biosimilars, and vaccine capacity additions. Bora Biologics completed a USD 30 million expansion in January 2026, and the site now supports commercial-scale readiness with added single-use bioreactor capacity that still requires associated media and buffer handling systems. AbbVie and Johnson and Johnson also moved ahead with large U.S. manufacturing investments in 2026, which support demand for high-specification mixing and formulation systems. This end-user mix helps the industrial agitators industry preserve value in premium applications even while standard-duty classes remain more exposed to price competition.

Geography Analysis

Asia-Pacific held 38.54% of the industrial agitators market size in 2025 and is expected to expand at a 4.89% CAGR through 2031. The region combines the deepest pipeline of chemical, pharmaceutical, and water infrastructure additions, which keeps both standard-duty and engineered demand active. China and India remain central to this pattern because large process investments and expanding domestic manufacturing ecosystems support a broader procurement base. South Korea adds another premium layer through biologics expansion, where stainless and hybrid processing systems continue to be commissioned for higher-value output. WuXi Biologics announced structural completion and key equipment arrival at its Chengdu microbial commercial manufacturing site in April 2026, reinforcing China's position in bioprocess-related equipment demand.

North America and Europe together form the other major revenue center for the industrial agitators market, supported by pharmaceutical reshoring, wastewater retrofits, and food-grade equipment upgrades. In the United States, AbbVie, Johnson and Johnson, and Amgen all announced major manufacturing commitments that support GMP-compliant agitation demand across upstream, formulation, and utility systems. Europe is seeing a stronger replacement cycle in variable-frequency-driven units as processors focus on tighter control and lower energy draw in continuous-duty service. Germany remains the leading European value market because it brings together specialty chemicals, pharmaceuticals, and food processing in one concentrated industrial base.

South America, the Middle East, and Africa represent smaller but important growth pockets in the industrial agitators market. Saudi Arabia and the UAE are led by downstream petrochemicals and desalination, while Africa depends more on wastewater infrastructure and mining-related agitation duties. Brazil and Argentina support food processing and industrial chemicals, although currency pressure can delay project commitments and extend replacement cycles. As installed bases age across these regions, service, retrofits, and upgrade work are becoming a larger part of the industrial agitators market than greenfield demand alone.

Competitive Landscape

The industrial agitators market shows moderate consolidation at the global tier and clear fragmentation across regional and specialist suppliers. A small group of multinational OEMs, including ITT, Alfa Laval, Sulzer, and EKATO, compete mainly on application engineering depth, installed-base coverage, and aftermarket strength rather than on unit price alone. ITT's completion of its USD 4.775 billion acquisition of SPX FLOW in March 2026 was the most important ownership change in the sector and brought Lightnin, Philadelphia Mixing, Plenty, and Milton Roy Mixing into one process equipment umbrella. That combination gives the business a broader mixing portfolio, a larger service reach, and more room to spread research and development spending across brands. At the same time, many regional manufacturers and application specialists continue to win standard-duty orders by offering lower cost and faster delivery, which keeps the industrial agitators market from becoming tightly concentrated.

Alfa Laval is following an equipment-plus-service strategy in the industrial agitators market through its EnSaLine platform, which combines hygienic mixing with predictive maintenance support through the Clariot VX sensor. Sulzer is defending mature top-entry positions by upgrading hydraulic performance and efficiency in the Scaba STA line. EKATO continues to compete through process-specific expertise in crystallization, hydrogenation, gas-inducing mixing, and lithium-related applications. These moves show that the industrial agitators market is being shaped by technology fit, compliance capability, and lifecycle support rather than by simple catalog breadth.

Smaller specialists such as Dynamix Agitators and Sharpe Mixers still compete effectively because they can move faster and tailor equipment to narrow use cases without the same overhead structure as large OEMs. Another shift is emerging from battery manufacturing, where electrode slurry preparation requires high-viscosity mixing and a different qualification path from traditional process industries. Suppliers that can prove energy savings, containment performance, and faster service intervals are better placed to protect price and deepen aftermarket penetration. This keeps the industrial agitators market technically differentiated even while regional competition remains active in standard equipment categories.

Industrial Agitators Industry Leaders

SPX FLOW Inc.

Xylem Inc.

Alfa Laval AB

Sulzer Ltd.

EKATO Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AbbVie announced a USD 1.4 billion investment to build a 185-acre pharmaceutical manufacturing campus in Durham, North Carolina, integrating advanced manufacturing and AI-driven laboratory technologies for immunology, neuroscience, and oncology products, with construction beginning in 2026 and completion expected by the end of 2028. The facility will require substantial GMP-compliant agitation systems across formulation and upstream bioprocess operations, reinforcing the US as a primary market for pharmaceutical-grade agitators.

- April 2026: WuXi Biologics announced the structural completion and key equipment arrival at its microbial commercial manufacturing site in Chengdu, China, targeting GMP release for production by end-2026, with a 15,000 L fermenter capacity enabling up to 110 drug substance batches annually and long-term expansion potential up to 60,000 L. The facility also features China's first dual-chamber lyophilization line and a 10 million+ vial-per-year fill capacity, representing a major scaling event for high-precision bioprocess agitation demand.

- March 2026: Alfa Laval launched the EnSaLine agitator platform on March 17, 2026, introducing a hygienic mixing line for food, dairy, beverage, and pharmaceutical production that reduces energy consumption by up to 80% versus comparable technologies, with 3-A certification, FDA-compliant non-metallic parts, CIP-while-running capability, and a cartridge-based seal-and-bearing assembly serviceable in under 30 minutes by a single technician.

- March 2026: ITT Inc. completed the acquisition of SPX FLOW on March 2, 2026, for a total consideration of USD 4.775 billion funded through a combination of cash and equity, combining ITT's Industrial Process segment with SPX FLOW's Lightnin, Philadelphia Mixing Solutions, Plenty Mixers, and Milton Roy Mixing brands within the renamed Flow Technologies segment. The transaction materially concentrates ownership of 4 global agitator brands and is expected to accelerate shared research and development across the mixing portfolio.

Global Industrial Agitators Market Report Scope

The Industrial Agitators Market Report is Segmented by Product Type (Large Tank Agitators, Portable Agitators, Drum Agitators, Magnetic Agitators, and Other Product Types), Mounting Configuration (Top-Mounted, Side-Mounted, and Bottom-Mounted), Component (Impeller, Shaft, Motor, and Seals and Bearings), Mixing Flow Pattern (Axial Flow, Radial Flow, and Tangential Flow), Power Rating (Up to 5 kW, 5–15 kW, 15–50 kW, and Above 50 kW), End-Use Industry (Chemicals and Petrochemicals, Water and Wastewater Treatment, Food and Beverage, Pharmaceuticals and Biotechnology, Minerals and Mining, Paper and Pulp, Energy and Power, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Large Tank Agitators |

| Portable Agitators |

| Drum Agitators |

| Magnetic Agitators |

| Other Product Types |

| Top-Mounted |

| Side-Mounted |

| Bottom-Mounted |

| Impeller |

| Shaft |

| Motor |

| Seals and Bearings |

| Axial Flow |

| Radial Flow |

| Tangential Flow |

| Up to 5 kW |

| 5–15 kW |

| 15–50 kW |

| Above 50 kW |

| Chemicals and Petrochemicals |

| Water and Wastewater Treatment |

| Food and Beverage |

| Pharmaceuticals and Biotechnology |

| Minerals and Mining |

| Paper and Pulp |

| Energy and Power |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Large Tank Agitators | ||

| Portable Agitators | |||

| Drum Agitators | |||

| Magnetic Agitators | |||

| Other Product Types | |||

| By Mounting Configuration | Top-Mounted | ||

| Side-Mounted | |||

| Bottom-Mounted | |||

| By Component | Impeller | ||

| Shaft | |||

| Motor | |||

| Seals and Bearings | |||

| By Mixing Flow Pattern | Axial Flow | ||

| Radial Flow | |||

| Tangential Flow | |||

| By Power Rating | Up to 5 kW | ||

| 5–15 kW | |||

| 15–50 kW | |||

| Above 50 kW | |||

| By End-User Industry | Chemicals and Petrochemicals | ||

| Water and Wastewater Treatment | |||

| Food and Beverage | |||

| Pharmaceuticals and Biotechnology | |||

| Minerals and Mining | |||

| Paper and Pulp | |||

| Energy and Power | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and forecast for industrial agitators?

The industrial agitators market was USD 2.80 billion in 2025, is valued at USD 2.92 billion in 2026, and is forecast to reach USD 3.61 billion by 2031 at a 4.33% CAGR.

Which product type leads demand for industrial agitators?

Large tank agitators led with 42.89% share in 2025 because they are essential in chemical, petrochemical, and water-treatment vessels that require continuous-duty mixing.

Which region is growing fastest for industrial mixing equipment?

Asia-Pacific is the fastest-growing region with a 4.89% CAGR through 2031, supported by chemical, pharmaceutical, and water infrastructure additions.

Why are magnetic agitators gaining traction?

Magnetic agitators are projected to grow at a 5.12% CAGR because zero-leakage duty, containment, and hygienic process requirements are becoming more important in pharma and specialty chemicals.

Which end-user group is creating the strongest premium equipment demand?

Pharmaceuticals and biotechnology are expected to grow at a 4.69% CAGR through 2031, and that segment typically requires higher-specification, GMP-compliant mixing systems.

What is the main buying shift shaping supplier competition?

Buyers are moving from initial purchase price toward total lifecycle cost, which favors variable-frequency-driven systems, higher-efficiency designs, and stronger aftermarket support.

Page last updated on: