NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

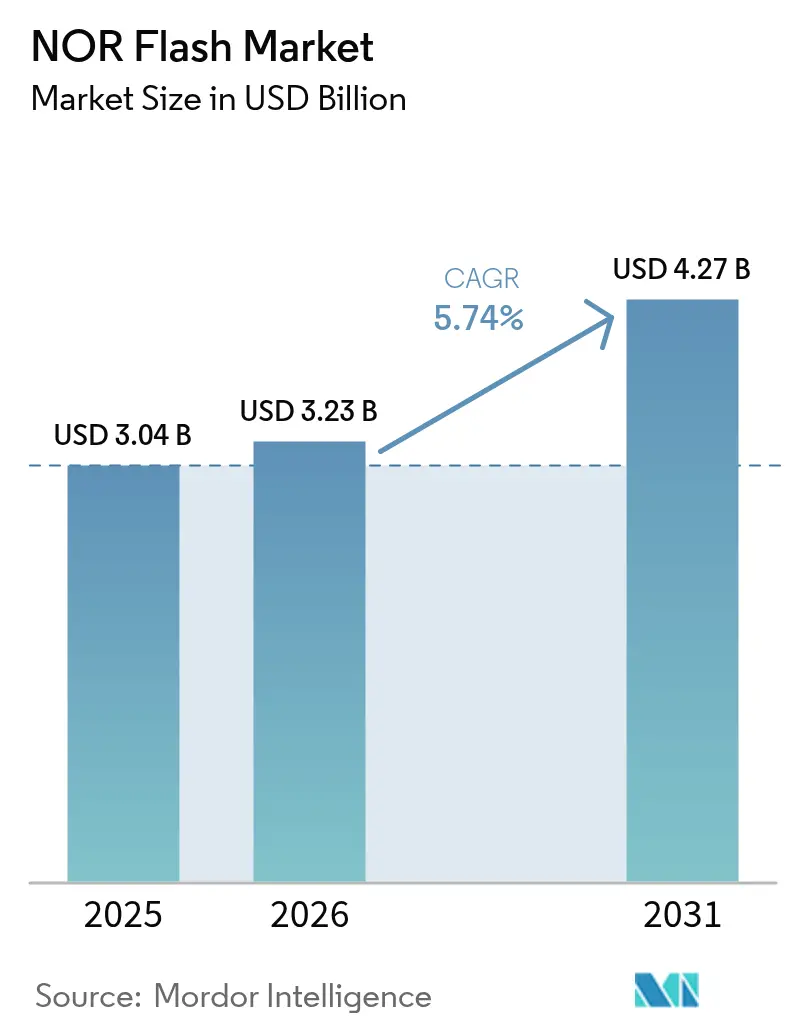

| Market Size (2026) | USD 3.23 Billion |

| Market Size (2031) | USD 4.27 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

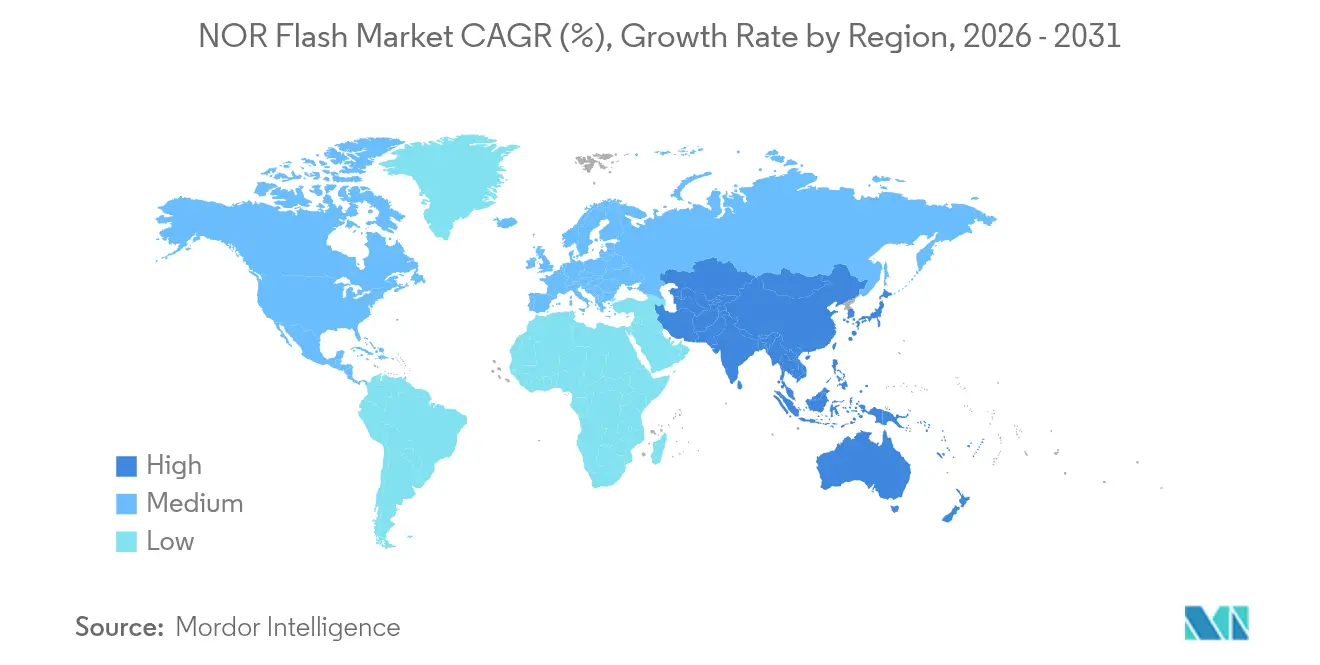

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

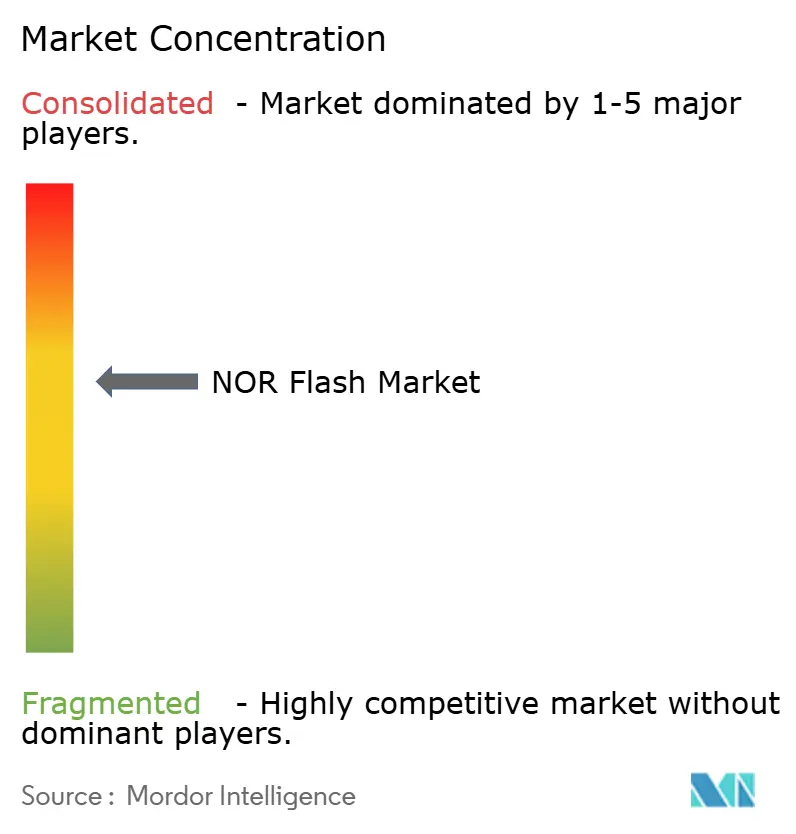

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

NOR Flash Market Analysis by Mordor Intelligence

The NOR Flash market size is projected to expand from USD 3.04 billion in 2025 and USD 3.23 billion in 2026 to USD 4.27 billion by 2031, registering a CAGR of 5.74% between 2026 to 2031. Steady demand from firmware-intensive automotive electronics, low-latency industrial IoT gateways and radiation-hardened satellite payloads continues to anchor revenue. Serial devices, valued for six-to-twelve-pin footprints, dominate design wins as engineers prioritize board-space efficiency. At the same time, Chinese 55 nanometer capacity additions are compressing average selling prices, encouraging incumbents to shift toward automotive-qualified, security-enhanced and radiation-tolerant variants. Interface migration from Quad to Octal SPI, density moves beyond 256 Megabit for over-the-air (OTA) update buffers and the growing use of sub-1.8 Volt parts in battery-powered wearables combine to broaden the addressable NOR Flash market across end-user sectors.

Key Report Takeaways

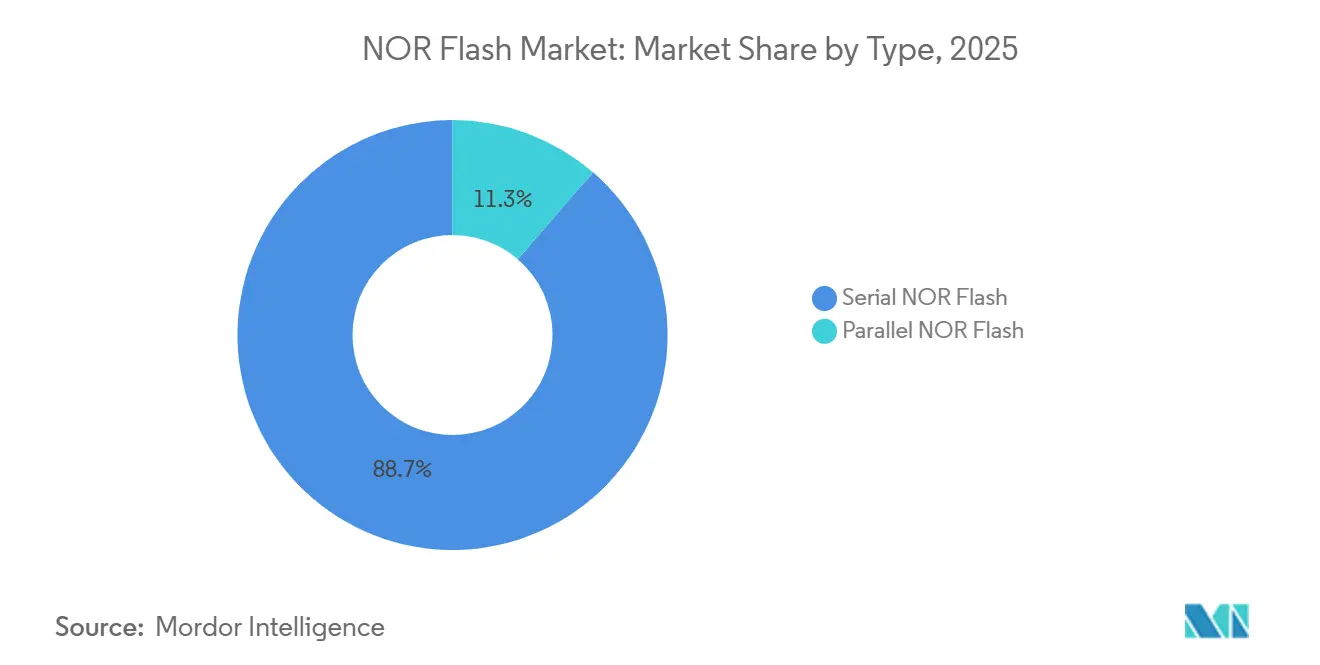

- By flash type, Serial NOR Flash led with 46.11% of the NOR Flash market share in 2025, while the segment is forecast to expand at a 6.12% CAGR through 2031.

- By interface, Quad SPI accounted for 38.57% of the market in 2025, whereas Octal/xSPI is projected to register the fastest growth at a 6.93% CAGR during 2026–2031.

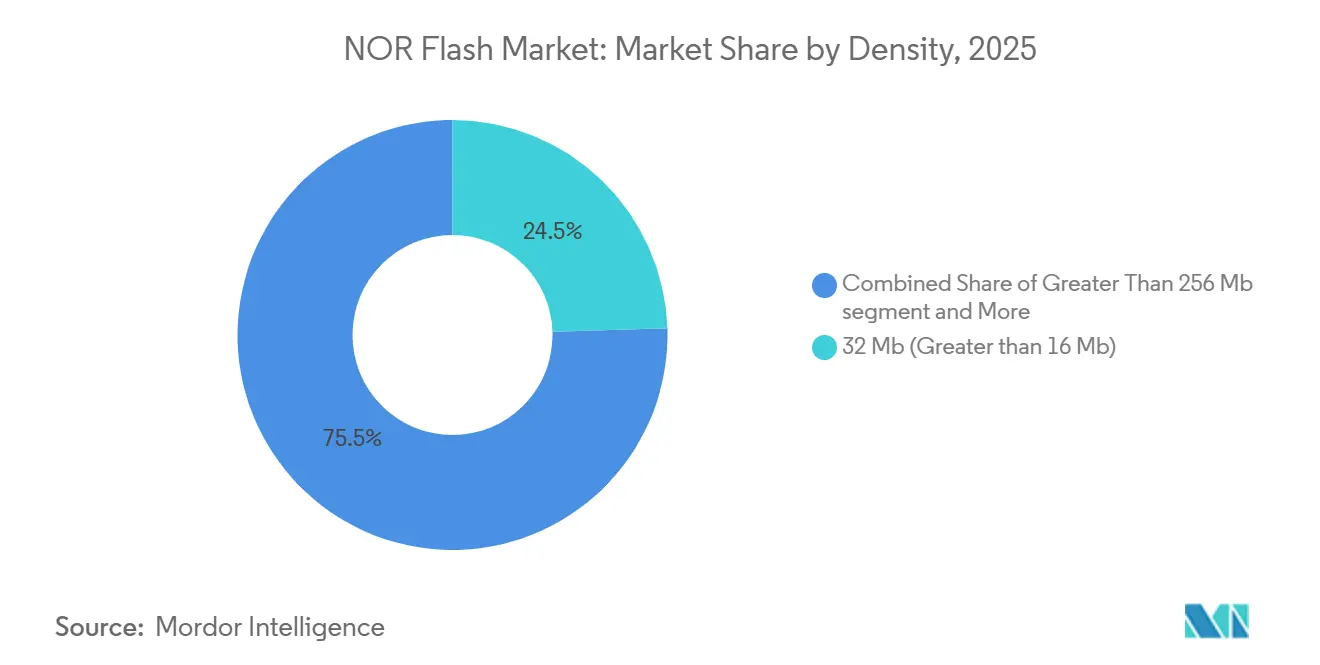

- By density, 32 Mb (>16 Mb) held 24.35% of the market share in 2025, while >256 Mb density devices are anticipated to grow at a 5.92% CAGR through 2031.

- By voltage, the 3V class dominated with 43.12% market share in 2025, while Sub-1.8V solutions are expected to witness a 6.27% CAGR over the forecast period.

- By end-user application, Automotive emerged as the leading segment with 29.79% share in 2025 and is projected to grow at a 6.55% CAGR through 2031.

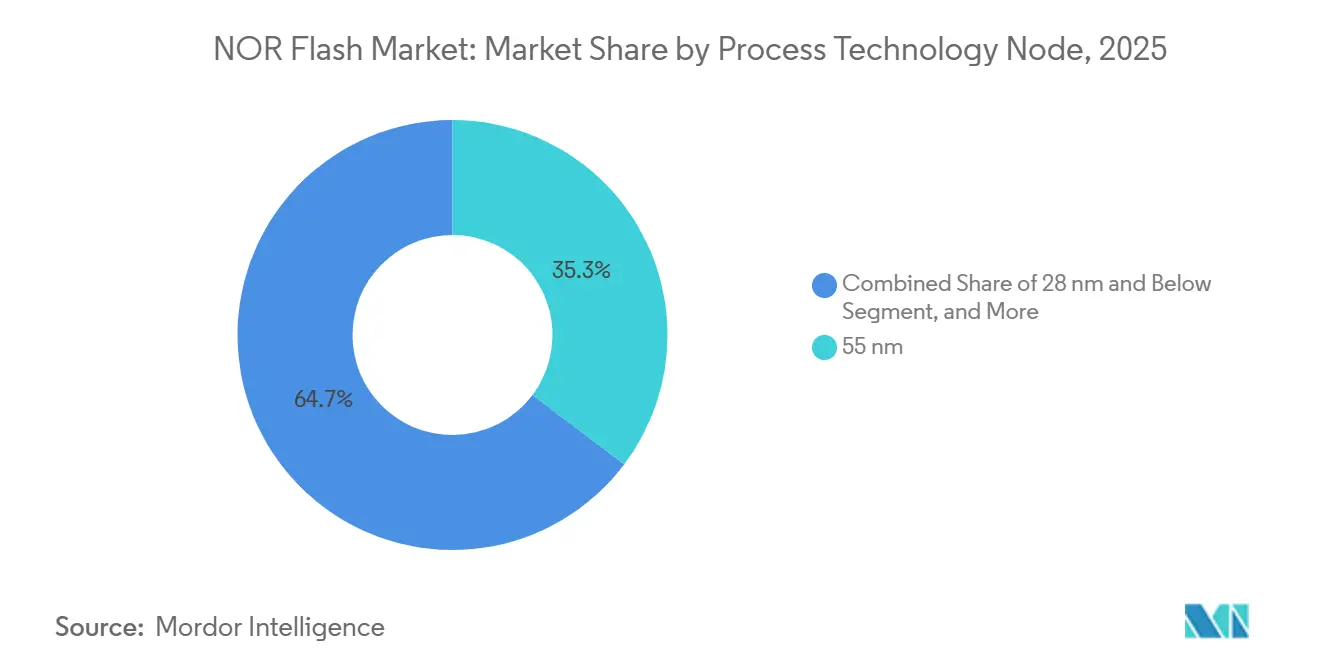

- By process node, 55 nm accounted for 35.26% of the market in 2025, whereas 28 nm and below technologies are forecast to expand at a 6.43% CAGR during 2026–2031.

- By packaging type, WLCSP/CSP held 33.93% of the market share in 2025 and is expected to register a robust 10.9% CAGR through 2031.

- By geography, Asia-Pacific dominated with 48.81% market share in 2025 and is projected to grow at the fastest rate of 15.3% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Firmware-Intensive ADAS and Domain Controllers Accelerating Automotive-Grade NOR Demand | +1.20% | Global, with concentration in Germany, Japan, South Korea, and United States | Medium term (2-4 years) |

| Quad and Octal SPI Adoption for Fast-Boot IoT Edge Devices Across Global Manufacturing Hubs | +0.90% | APAC core (China, Taiwan, Southeast Asia), spill-over to North America and Europe | Short term (≤ 2 years) |

| Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices | +0.70% | Global, led by United States and Europe launch operators | Long term (≥ 4 years) |

| China's 55 nm and 40 nm Indigenous Process Push for NOR Self-Sufficiency | +0.80% | China domestic, with export implications for APAC and emerging markets | Medium term (2-4 years) |

| Secure Boot and OTA Update Mandates in Industry 4.0 Factories | +0.60% | Europe (Germany, Netherlands), North America, APAC industrial corridors | Medium term (2-4 years) |

| Low-Power 1.8 V Serial NOR for Wearable and Point-of-Care Healthcare Electronics | +0.50% | Global, with early adoption in North America, Europe, and urban APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Firmware-Intensive ADAS Domain Controllers

Automakers are consolidating dozens of electronic control units into centralized domain controllers that boot complex neural-network firmware and calibration tables. Each controller now integrates multiple 32 Megabit or 64 Megabit serial NOR die to store safety-critical code paths. Infineon’s AURIX TC4x microcontrollers, sampling for Level 2+ autonomy, expose dual Quad SPI ports qualified to AEC-Q100 Grade 1, illustrating the trend.[1]Infineon Technologies, “AURIX TC4x Product Brief,” infineon.com Engineers also specify endurance above 100,000 program-erase cycles and 20-year data retention at 125 °C, reinforcing the pull for proven automotive process flows. As these requirements permeate mid-range vehicles, the NOR Flash market benefits from a 6.55% automotive CAGR and deeper content per car.

Quad and Octal SPI for Fast-Boot IoT Edge Devices

Smart meters, gateway controllers and edge-AI cameras increasingly mandate sub-100 millisecond boot times. Octal SPI NOR, offering sustained reads beyond 400 Mbps, enables real-time operating systems to launch without latency overhead. Winbond’s W77Q series delivers this throughput at 1.2 Volt supply, aligning with industrial uptime targets in China, Germany and the United States.[2]Winbond Electronics, “W77Q Octal SPI NOR Flash,” winbond.com The adoption wave supports the fastest interface growth rate at 6.93% CAGR and cements serial NOR as the default execute-in-place memory for latency-sensitive IoT nodes.

Constellation-Scale LEO Satellites

Low Earth orbit deployments from SpaceX, OneWeb and Project Kuiper each carry 10-20 radiation tolerant NOR die rated above 100 kilorads total ionizing dose. Micron’s MT25Q family, qualified to NASA EEE-INST-002, exemplifies parts engineered for single-event-upset immunity.[3]Micron Technology, “MT25Q Radiation-Tolerant NOR,” micron.com Annual unit demand will surpass 50 million by 2028, creating a protected, high-margin niche that adds 0.7 percentage points to overall CAGR and offers incumbents a buffer against commodity price compression.

China’s 55-40 nm Self-Sufficiency Push

Beijing’s semiconductor plan has triggered rapid NOR capacity ramps at Wuhan XMC, GigaDevice and Puya. Over 30,000 wafer starts per month at 55 nanometer were added between 2024 and 2025, targeting 4-128 Megabit serial densities. The influx lowered commodity average selling prices by up to 20%, reshaping the global cost curve.[4]Financial Times, “China Accelerates Chip Self-Sufficiency Plan,” ft.com While margin pressure persists, wider availability of mid-density parts expands the NOR Flash market footprint in local white goods and emerging-market smartphones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Premium over NAND Above 256 Mb Limiting High-Density Consumer Adoption | -0.60% | Global, with pronounced effect in price-sensitive consumer electronics markets | Short term (≤ 2 years) |

| Scaling Ceilings beyond 45 nm Steering OEM Road-Maps toward MRAM and ReRAM Substitutes | -0.40% | North America and Europe design centers, with gradual APAC adoption | Long term (≥ 4 years) |

| Foundry Concentration in Taiwan Exposing Supply-Chain Disruption Risk | -0.30% | Global, with acute sensitivity in automotive and industrial sectors | Medium term (2-4 years) |

| ASP Compression from Expanding Chinese Capacity Impacting Vendor Margins | -0.50% | Global, with margin pressure most severe for commodity-grade products | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cost Premium over NAND Above 256 Mb

At densities above 256 Megabit, NOR die cost two-to-three times more per gigabit than 3D NAND, a gap that widens as NAND scales to 200-layer stacks. Consumer device designers therefore combine a small NOR for boot code with large NAND for application firmware, limiting large density NOR penetration. The premium subtracts 0.6 percentage points from CAGR and confines high-density growth mainly to automotive and aerospace update buffers.

Scaling Ceilings Steering Shift to MRAM

NOR cell scaling stalls beyond 45 nanometers as charge-retention margins shrink. MRAM and ReRAM offer sub-20-nanometer scalability, 35-nanosecond latency, and endurance above 1 million cycles. Everspin’s 256 Mb ST-MRAM, now sampling, demonstrates a credible substitute path. Although price remains 3-5 times higher than NOR, anticipated volume ramps by 2029 pose a long-term substitution threat and clip the NOR Flash market growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flash Type: Serial Leadership Deepens

Serial NOR maintained 46.11% of NOR Flash market share in 2025 and is on track for a 6.12% CAGR to 2031. The pin-light topology reduces routing layers, lowers electromagnetic interference and fits within ultra-thin wearables. Parallel NOR, bound to 20-48 address-data lines, lingers in legacy PLCs and military avionics where deterministic access supersedes board size. Ongoing miniaturization, coupled with system-in-package adoption, will enlarge serial NOR’s share of the NOR Flash market.

Designers increasingly bundle serial NOR with microcontrollers inside compact QFN and WLCSP footprints to shorten trace length and improve signal integrity. Winbond’s W25Q series alone ships more than 1 billion units annually into consumer and networking equipment. Meanwhile, parallel NOR retains relevance where 16-bit bus bandwidth and established qualification heritage matter, notably in radiation-hardened satellite electronics.

By Interface: Octal and xSPI Momentum Builds

Quad SPI owned 38.57% of 2025 revenue thanks to broad microcontroller support, yet Octal and xSPI interfaces will post the briskest 6.93% CAGR. Octal doubles data lanes to eight, pushing sustained read throughput past 400 Mbps and slicing firmware boot from 150 milliseconds to under 50 milliseconds for 16 MB images. The xSPI standard, ratified by JEDEC in 2024, layers command queuing and inline ECC atop Octal, priming it for functional-safety automotive designs.

Basic SPI single and dual modes, still prevalent in cost-sensitive white goods, will cede share as edge-AI inference accelerators from Qualcomm and Hailo demand faster wake-up cycles. As a result, interface migration will reinforce serial NOR’s positioning in the NOR Flash market and elevate aggregate blended average selling prices despite unit-price erosion in older modes.

By Density: Middle-Cores Remain the Sweet Spot

The 32 Megabit tier captured 24.35% of 2025 revenue, balancing cost and capacity for body controllers and industrial gateways. Ultra-low cost 2-4 Megabit devices persist in RFID modules and smartcards, whereas densities above 256 Megabit will rise at 5.92% CAGR on the back of OTA staging and data-logging in electrified vehicles.

Nevertheless, the bulk of the NOR Flash market size will stay anchored between 8 Megabit and 64 Megabit where most embedded firmware falls. This mid-range cluster enjoys stable wafer cost at 55-65 nanometer nodes and fits single-die footprints compatible with WLCSP, aligning with compact system designs.

By Voltage: Sub-1.8 V Parts Gain Ground

Three-volt devices, aligned with 3.3 V logic, held 43.12% share in 2025. Yet sub-1.8 V serial NOR is expanding at 6.27% CAGR, favoured in coin-cell wearables and point-of-care diagnostics that target two-year battery life. Winbond’s 1.2 V W77Q cuts active read current below 5 mA at 50 MHz, extending charge cycles in continuous glucose monitors.

The 1.8 V class acts as a transitional step for industrial gateways moving from legacy 3.3 V buses toward low-power operation. Wide-voltage parts covering 1.65-3.6 V offer design flexibility in portable instruments that experience fluctuating battery rails.

By End-User Application: Automotive Drives Upside

Automotive held 29.79% of 2025 revenue and heads for a 6.55% CAGR to 2031, buoyed by ADAS domain controllers and battery-management systems that each embed multiple NOR die. Consumer electronics, at 26%, face slower momentum as smartphones migrate firmware to embedded NAND, though NOR retains secure-element and boot ROM niches.

Industrial automation, with deterministic latency needs, and communication equipment fuelled by 5G base stations ,together secure around 40% of the NOR Flash market. Aerospace, defense and medical segments, while small, command premium radiation-hardened or biocompatible devices, sustaining attractive margins for specialized vendors.

By Process Technology Node: Shrinks Move to 28 nm

The 55 nm node accounted for 35.26% of 2025 shipments, balancing cost and mature automotive qualification. Nodes at 28 nm and below will grow at 6.43% CAGR as OEMs seek standby currents under 50 µA and higher endurance. Chinese fabs are aggressively scaling 40 nm serial production, narrowing the cost delta versus 55 nm and accelerating migration for mid-density parts.

Older 90 nm and 130 nm lines survive in legacy industrial control units where redesign cost outweighs power gains. The gradual node progression underpins the NOR Flash market’s ability to improve power efficiency without the extreme ultraviolet lithography hurdles facing logic semiconductors.

By Packaging Type: WLCSP and CSP See Double-Digit Growth

WLCSP and CSP formats captured 33.93% share in 2025 and will surge at 10.9% CAGR through 2031, enabling under-0.6 mm package heights suited to hearables and smart rings. QFN and SOIC remain mainstays for automotive body modules that require robust solder joints and heat dissipation.

Ball-grid arrays serve high-pin-count domain controllers, while ceramic packages persist in space and defense where out-gassing and hermeticity drive selection. As consumer devices push for ever-thinner profiles, advanced packages will capture a larger share of the NOR Flash market.

Geography Analysis

Asia-Pacific generated 48.81% of 2025 revenue and is forecast to post a 15.3% CAGR to 2031. China’s self-reliance drive expanded domestic NOR wafer starts beyond 30,000 per month, trimming commodity pricing by up to 20%. Taiwan’s Winbond and Macronix continue to supply automotive-grade and radiation-tolerant parts worldwide, while Japan and South Korea add embedded NOR within application processors. Auto-electronics assembly growth in Thailand and Vietnam plus India’s incentive-backed test operations widen regional demand.

North America and Europe jointly delivered 38% of 2025 revenue, advancing at 4.8% CAGR. Design leadership in the United States, Germany and France couples with safety standards such as ISO 26262 and DO-254, favouring incumbents with deep qualification heritage. The United Kingdom and France stimulate radiation-hardened adoption for avionics and satellite missions, reinforcing a value-over-volume dynamic.

South America and Middle East and Africa together contributed 13% of revenue in 2025 and will rise at 3.9% CAGR. Brazil’s vehicle assembly and Gulf smart-city projects draw imports of mid-density serial NOR, yet limited local wafer fabrication tempers acceleration. As a result, these regions remain net importers, linking NOR demand closely to automotive production cycles and infrastructure digitalization projects.

Mordor Intelligence provides coverage of the nor flash market across other key regional markets, including Europe and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to France, India, Mexico, United States, China, Japan, Italy, and United Kingdom incorporating local coverage and market participation, as required.

Competitive Landscape

The NOR Flash market shows moderate concentration. Winbond and Macronix lead serial shipments from Taiwan, while Infineon, Micron and Renesas add depth through automotive and aerospace qualification portfolios. Chinese challengers GigaDevice, Puya and Wuhan XMC have lifted 55 nm output, forcing price discipline on commodity densities.

Incumbents reply by stacking differentiation layers such as AEC-Q100 Grade 1 compliance, hardware security modules and radiation-tolerant design kits. Winbond’s 2025 patent covering integrated security blocks in serial NOR underpins this pivot. Renesas bundles Quad SPI controllers into RH850 microcontrollers, offering system-level optimization that discrete vendors cannot match.

MRAM and ReRAM suppliers, led by Everspin and Panasonic, threaten NOR in high-performance embedded systems but remain uneconomical for mass deployment. Consequently, the top five manufacturers commanded about two-thirds of 2025 revenue, sustaining balanced rivalry without tipping into oligopoly.

NOR Flash Industry Leaders

Infineon Technologies AG

Micron Technology Inc.

GigaDevice Semiconductor Inc.

Macronix International Co. Ltd

Winbond Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infineon Technologies’ SEMPER™ NOR Flash family achieved ASIL-D certification under ISO 26262:2018, reinforcing its automotive credentials.

- April 2025: Macronix unveiled 3D NOR Flash technology with density scaling up to 8× over planar solutions and sampling slated for late 2026.

- March 2025: GigaDevice displayed ISO 26262-certified GD25/55 serial NOR flash families at Embedded World, delivering up to 2 Gb capacity at 400 MB/s data rate.

- March 2025: Winbond introduced the TrustME W77Q secure-flash series, integrating post-quantum LMS signatures for IoT devices.

- December 2024: GigaDevice’s GD25/55 automotive-grade SPI NOR family obtained ISO 26262 ASIL-D certification, covering capacities up to 2 GB.

Global NOR Flash Market Report Scope

The NOR Flash Market Report is Segmented by NOR Flash Type (Serial NOR Flash, Parallel NOR Flash), Interface (SPI Single/Dual, Quad SPI, Octal and xSPI), Density (2 Mb and Less, 4 Mb, 8 Mb, 16 Mb, 32 Mb, 64 Mb, 128 Mb, 256 Mb, Greater than 256 Mb), Voltage (3 V Class, 1.8 V Class, Wide-Voltage, Other Sub-1.8 V Classes), End-User Application (Consumer Electronics, Communication, Automotive, Industrial, Other End-User Applications), Process Technology Node (90 nm and Older, 65 nm, 55 nm, 45 nm, 28 nm and Below), Packaging Type (WLCSP/CSP, QFN/SOIC, BGA/FBGA, Other Packaging Types), and Geography (North America, Europe, Asia-Pacific, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Serial NOR Flash |

| Parallel NOR Flash |

| SPI Single / Dual |

| Quad SPI |

| Octal and xSPI |

| 2 Megabit And Less NOR |

| 4 Megabit And Less-NOR (greater than 2mb) NOR |

| 8 Megabit And Less (greater than 4mb) NOR |

| 16 Megabit And Less (greater than 8mb) NOR |

| 32 Megabit And Less (greater than 16mb) NOR |

| 64 Megabit And Less (greater than 32mb) NOR |

| 128 Megabit and Less (greater than 64MB) NOR |

| 256 Megabit and Less (greater than 128MB) NOR |

| Greater than 256 Megabit |

| 3 V Class |

| 1.8 V Class |

| Wide-Voltage (1.65 V - 3.6 V) |

| Others - 1.2V Class (and similar sub-1.8V) (2.5V, 5V, etc.) |

| Consumer Electronics |

| Communication |

| Automotive |

| Industrial |

| Other Applications |

| 90 nm and Older |

| 65 nm |

| 55 nm (including 58 nm) |

| 45 nm |

| 28 nm and Below |

| WLCSP / CSP |

| QFN / SOIC |

| BGA / FBGA |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Type | Serial NOR Flash | |

| Parallel NOR Flash | ||

| By Interface (Value) | SPI Single / Dual | |

| Quad SPI | ||

| Octal and xSPI | ||

| By Density (Value) | 2 Megabit And Less NOR | |

| 4 Megabit And Less-NOR (greater than 2mb) NOR | ||

| 8 Megabit And Less (greater than 4mb) NOR | ||

| 16 Megabit And Less (greater than 8mb) NOR | ||

| 32 Megabit And Less (greater than 16mb) NOR | ||

| 64 Megabit And Less (greater than 32mb) NOR | ||

| 128 Megabit and Less (greater than 64MB) NOR | ||

| 256 Megabit and Less (greater than 128MB) NOR | ||

| Greater than 256 Megabit | ||

| By Voltage (Value) | 3 V Class | |

| 1.8 V Class | ||

| Wide-Voltage (1.65 V - 3.6 V) | ||

| Others - 1.2V Class (and similar sub-1.8V) (2.5V, 5V, etc.) | ||

| By End-user Application | Consumer Electronics | |

| Communication | ||

| Automotive | ||

| Industrial | ||

| Other Applications | ||

| By Process Technology Node (Value) | 90 nm and Older | |

| 65 nm | ||

| 55 nm (including 58 nm) | ||

| 45 nm | ||

| 28 nm and Below | ||

| By Packaging Type | WLCSP / CSP | |

| QFN / SOIC | ||

| BGA / FBGA | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the forecast value of the NOR Flash market by 2031?

The NOR Flash market is projected to reach USD 4.27 billion by 2031 on a 5.74% CAGR.

Which end-user sector is growing fastest for NOR Flash devices?

Automotive electronics, driven by ADAS domain controllers and battery-management systems, is advancing at 6.55% CAGR through 2031.

Why are Octal and xSPI interfaces gaining traction?

They double read bandwidth over Quad SPI, enabling sub-100 millisecond boot times required by edge-AI and industrial IoT equipment.

How is Chinese capacity affecting NOR Flash pricing?

New 55 nm lines at Wuhan XMC and GigaDevice have lowered commodity segment average selling prices by up to 20% year-over-year.

What packaging trends are emerging for ultra-thin devices?

Wafer-level chip-scale and chip-scale packages below 0.6 mm thickness are growing at 10.9% CAGR, supporting hearables and smart rings.

Which memory technologies could displace NOR Flash after 2029?

MRAM and ReRAM offer sub-20 nm scalability and high endurance, positioning them as long-term alternatives once cost gaps narrow.

Page last updated on: