Americas NOR Flash Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

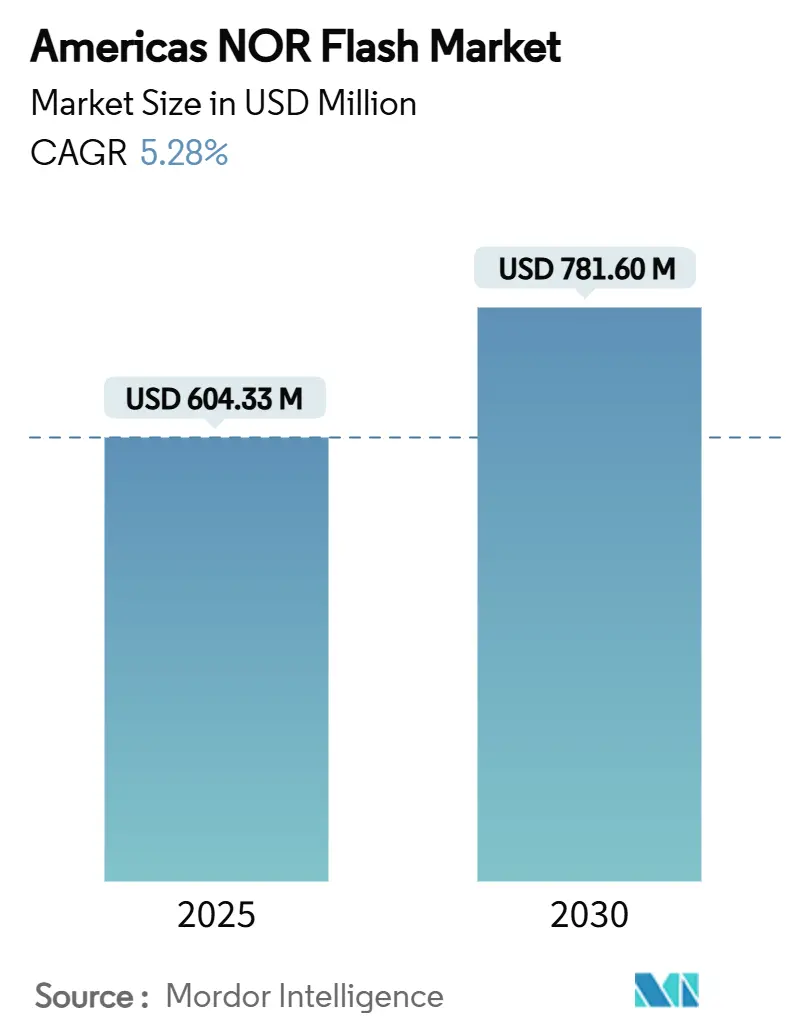

| Market Size (2025) | USD 604.33 Million |

| Market Size (2030) | USD 781.60 Million |

| Growth Rate (2025 - 2030) | 5.28% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Americas NOR Flash Market Analysis by Mordor Intelligence

The Americas NOR Flash market is valued at USD 604.33 million in 2025 and is on track to reach USD 781.60 million by 2030, advancing at a 5.28% CAGR. Growth rides on rising electronic content in vehicles, factory digitalization, and dense 5G roll-outs that require instant-boot code storage. Regional manufacturing incentives such as the U.S. CHIPS and Science Act and Mexico’s IMMEX program are shortening lead times and improving supply resilience. Device makers are also widening product lines with radiation-tolerant, ultra-low-power, and secure-boot variants, helping them target aerospace, battery-powered IoT, and software-defined vehicle platforms. Interface innovations such as Octal SPI and HyperBus further compress boot sequences, supporting execute-in-place execution across safety-critical endpoints in the Americas NOR Flash market.

Key Report Takeaways

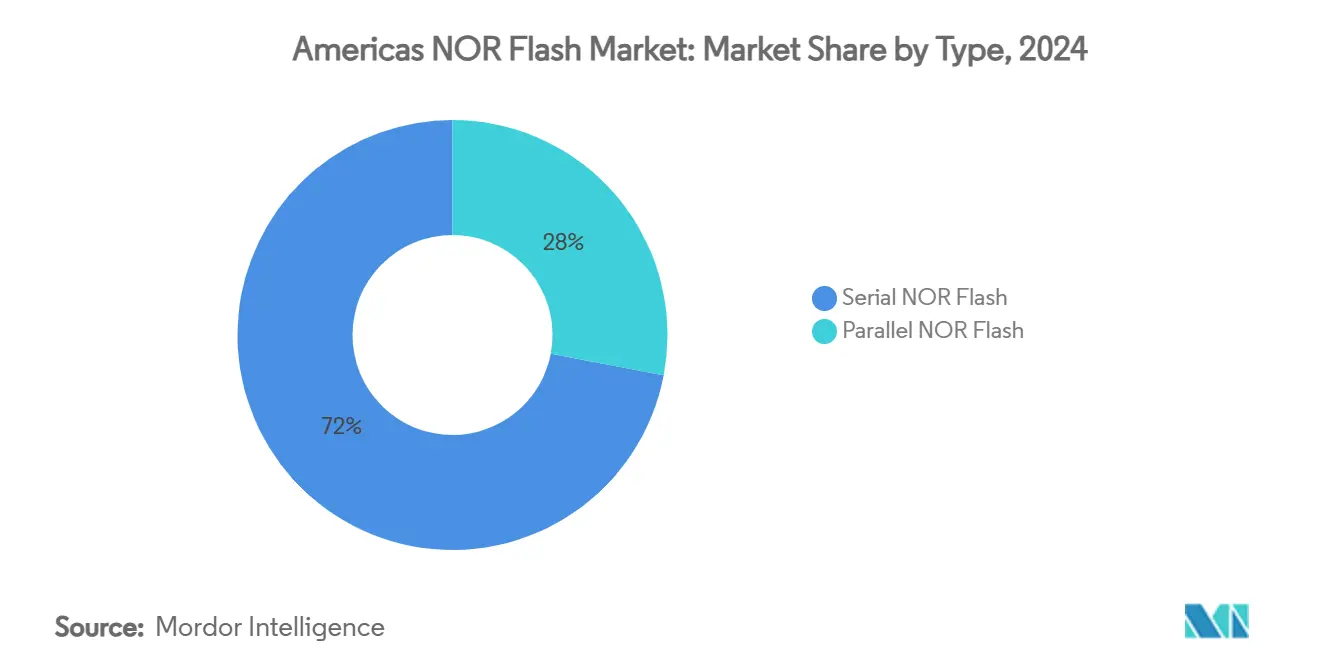

- By technology type, serial NOR held 68% of the Americas NOR Flash market share in 2024. Serial NOR is also projected to post the fastest 5.7% CAGR through 2030.

- By interface, Octal/OSPI devices generated 38% revenue in 2024; HyperBus/HX is set to grow at 5.4% CAGR over the same horizon.

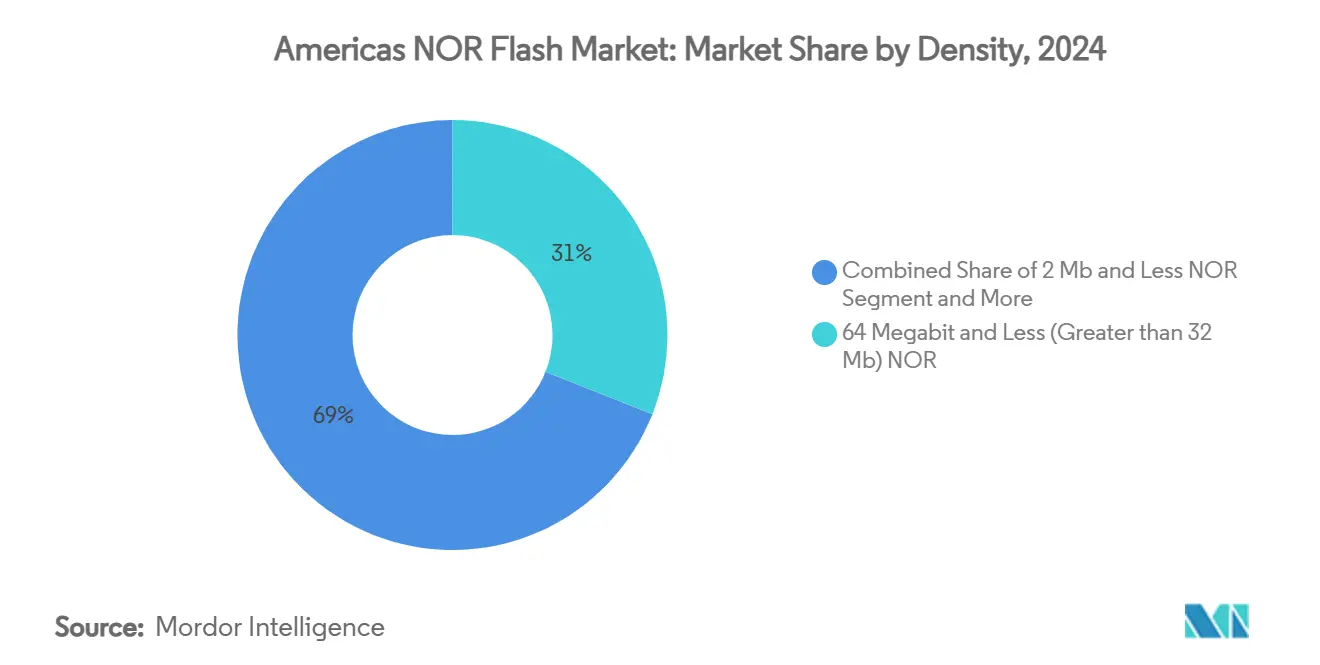

- By density, the 64 Mbit segment accounted for 31% of the Americas NOR Flash market size in 2024; the 256 Mbit band is forecast to expand at a 5.5% CAGR to 2030.

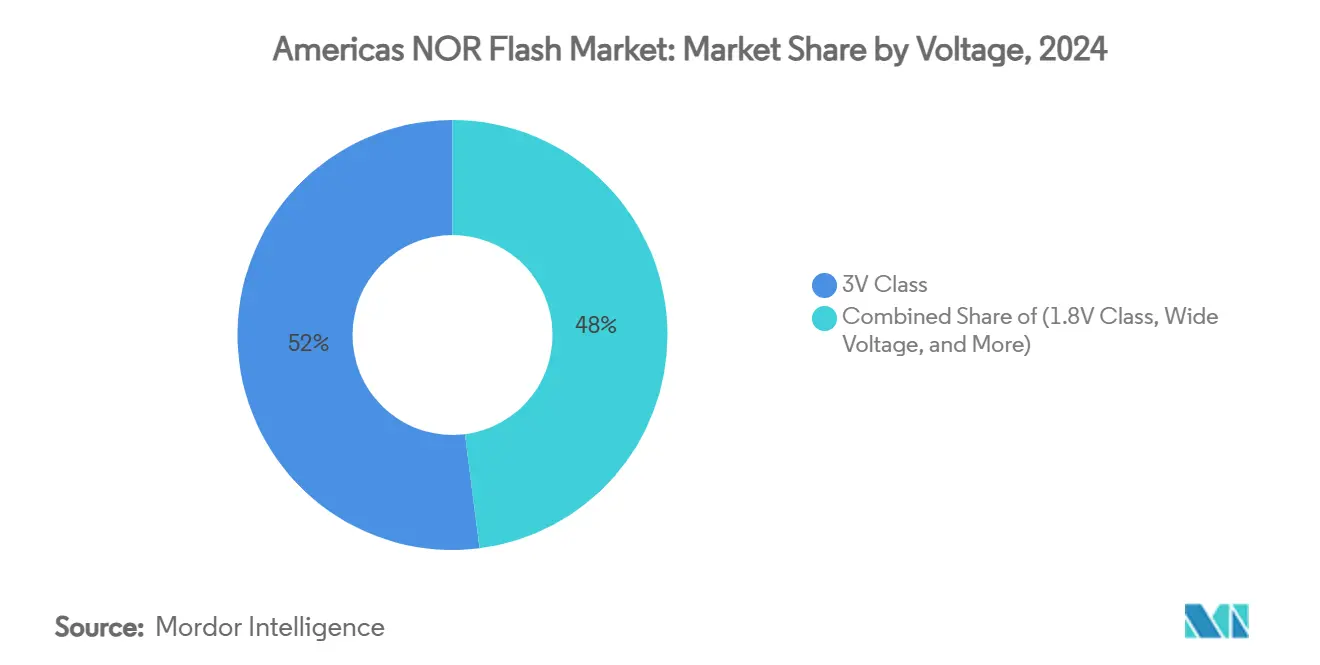

- By voltage, the 3 V class held 52% of the Americas NOR Flash market share in 2024, while 1.8 V devices are projected to expand at a 5.3% CAGR through 2030.

- By end-user application, consumer electronics led with 42% of the Americas NOR Flash market size in 2024, while automotive is advancing at a 5.8% CAGR through 2030.

- By process technology, the 65 nm node led with 38% of revenue in 2024, while 28 nm and below nodes are forecast to grow at a 5.5% CAGR to 2030.

- By packaging type, QFN/SOIC solutions captured 41% of the Americas NOR Flash market size in 2024, whereas WLCSP/CSP formats are set to post a 5.4% CAGR.

- By geography, the United States controlled 72% revenue in 2024; Mexico is forecast to achieve a 5.9% CAGR from 2025 to 2030.

- Infineon Technologies, Micron Technology, GigaDevice, Macronix, and Winbond together commanded about 60% of 2024 revenue.

Americas NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive-grade serial NOR demand in ADAS/IVI | +1.20% | United States, Mexico, Brazil | Medium term (2-4 years) |

| Proliferation of low-power IoT edge devices needing instant-boot firmware | +0.90% | United States, Canada | Medium term (2-4 years) |

| Migration of industrial automation PLCs from EEPROM to high-end NOR | +0.70% | United States, Mexico | Long term (≥ 4 years) |

| 5G small-cell roll-outs boosting SPI NOR usage in communication modules | +0.80% | United States, Canada, Brazil | Short term (≤ 2 years) |

| In-region wafer-fab incentives lowering cost base | +0.60% | United States, Canada, Mexico | Medium term (2-4 years) |

| Rise of aerospace and defense secure-boot requirements | +0.50% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Automotive-Grade Serial NOR Demand in ADAS/IVI

Automotive manufacturers across the Americas are increasing serial NOR content to store boot code and firmware for safety-critical driver-assistance and infotainment subsystems. ISO 26262 ASIL-D certification has become mandatory, and Infineon’s SEMPER family met this bar in May 2025, enabling engineers to shorten boot time by 30% while satisfying extended temperature specifications[1]Infineon Technologies AG. "Infineon SEMPER™ NOR Flash family achieves ASIL-D certification." May 8, 2025. . Average NOR Flash density per vehicle has climbed 30% since 2024 as Level 2+ features require more sensors and local processing. Tier-1 suppliers now favor quad and octal SPI interfaces to reach up to 400 MB/s, ensuring real-time operation during functional safety checks. Design cycles of 2-4 years lock in demand visibility, underpinning predictable volumes for vendors.

Proliferation of Low-Power IoT Edge Devices

Battery-powered smart-home sensors, wearable health trackers, and industrial condition-monitoring nodes require instant-boot firmware stored in non-volatile memory. GigaDevice's GD25NE dual-supply SPI NOR introduced in March 2025 halves read power draw relative to standard 1.8 V parts[2]CST Inc. "CST Inc,DDR5,DDR4,DDR3,DDR2,DDR,Nand,Nor,Flash,MCP ..." January 27, 2025. . Canadian manufacturers of wireless security sensors reported battery life gains from 18 to 30 months after adopting these devices. Material cost inflation in silicon wafers has been offset by smaller die sizes, keeping price points competitive. Rapid IoT product cycles spur steady replacement demand every one to two years, supporting recurring revenue for suppliers.

Migration from EEPROM to High-End NOR in Industrial Automation

Factories in the United States and Mexico are modernizing programmable logic controllers to support frequent over-the-air firmware updates, replacing legacy EEPROM with high-end NOR Flash. Cisco’s industrial networking guidelines stress secure, low-latency storage for code integrity[3]Cisco. “Networking and Security in Industrial Automation Environments - Cisco.” Accessed April 29, 2025. . A Mexican automotive parts plant achieved a 40% reduction in system initialization time after the switch, despite a 15% component cost premium. Extended lifecycle expectations—often more than 10 years—favor NOR’s endurance and long data retention. Conversion activity is anticipated to run throughout the decade, elevating long-term unit growth.

5G Small-Cell Roll-Outs Boosting SPI NOR Usage in Communication Modules

U.S., Canadian, and Brazilian telecom operators accelerated 5G densification in urban centers during 2024–2025, each small cell embedding multiple NOR Flash chips for firmware storage. A Brazilian carrier installed 10,000 units in 2024, lifting telecommunications NOR consumption significantly. Octal SPI and HyperBus parts help cut boot time below 0.5 s, an essential requirement for self-healing mesh networks. The surge is front-loaded into the next two years, offering near-term upside for vendors positioned with industrial-temperature-grade products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating photomask costs for sub-28 nm NOR nodes | -0.70% | United States | Medium term (2-4 years) |

| OEM qualification of Xilinx Zynq and eMMC substitutes | -0.50% | United States, Canada | Medium term (2-4 years) |

| Supply-chain cyclicality causing inventory write-downs | -0.30% | Americas | Short term (≤ 2 years) |

| Environmental regulations tightening lead-frame options | -0.20% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Photomask Costs for Advanced NOR Nodes

Moving below 28 nm raises photomask outlays beyond USD 5 million per set, prompting several U.S. fabs to delay node transitions. One manufacturer postponed a 22 nm migration after a 65% price spike, opting instead for process tweaks yielding a 15% die-size cut. While CHIPS-funded metrology initiatives may alleviate pressure, immediate cost hurdles restrain density and power-efficiency gains in the medium term.

Functional Substitutes Gaining OEM Qualification

Programmable SoCs such as Xilinx Zynq and integrated eMMC modules are being validated for roles historically filled by discrete NOR Flash. A Canadian industrial OEM eliminated three NOR devices by adopting a Zynq-based board, realizing bill-of-materials savings despite higher unit pricing. Execute-in-place workloads, however, still favor NOR, limiting substitution to select high-integration designs through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serial NOR Extends Dominance as Parallel Retains Mission-Critical Niche

In the Americas NOR Flash market, serial devices held about 72% revenue. Serial NOR attracts IoT, consumer electronics, and automotive platforms thanks to low pin count, reduced PCB area, and lower standby current. GigaDevice leveraged this demand to secure a significant share and focuses on further enhancing it by increasing its R&D spending. A U.S. portable diagnostic equipment maker moved from parallel to serial NOR, trimming system power by 40% while preserving medical-grade reliability.

Parallel NOR retained its foothold in 2024 and is projected to grow at a 3.6% CAGR to 2030, significantly less than serial NOR's growth. Aerospace and defense programs value its faster random access and radiation resilience. Infineon’s radiation-hardened 512 Mbit QSPI NOR, qualified in November 2024, underscores continued innovation in this space[4]Infineon Technologies AG. "Infineon’s Radiation-Hardened NOR Flash Achieves QML Qualification." Power Systems Design, January 1, 2025. . A defense integrator selected parallel NOR for a new military radio, absorbing a 25% cost premium to guarantee mission uptime during extreme temperature swings.

By Interface: OSPI Gains Scale While HyperBus Targets Peak Bandwidth

Octal SPI captured 38% of 2024 revenue as designers exploit up to 400 MB/s throughput for safety-critical boot code. Winbond’s W77T Secure Flash, launched in January 2025, meets ISO 26262 ASIL-D Ready status and delivers 200 MHz DDR performance on the xSPI bus. A Mexico-based ADAS supplier cut cold-start times to 0.4 s using OSPI, critical for autonomous functions that must initialize before vehicle motion.

HyperBus/HX remains a premium tier, but is expanding at 5.4% CAGR through 2030, propelled by AI-enhanced perception systems. Infineon’s SEMPER line supports 400 MB/s using 45 nm MIRRORBIT technology. A California autonomous-vehicle start-up standardized HyperBus NOR for next-gen sensor fusion, accepting a 12% packaging-material cost rise in exchange for deterministic latency.

By Density: 64 Mbit Holds the Center While 256 Mbit Accelerates

The 64 Mbit tier accounted for 31% of the Americas NOR Flash market size in 2024 as appliance, industrial, and mid-range IoT devices balance cost against firmware footprint. A Brazilian smart-appliance producer standardized on this density to host user-interface assets within aggressive bill-of-materials limits.

Richer code bases in automotive infotainment and industrial analytics are pushing 256 Mbit NOR toward 5.5% CAGR. Macronix’s 3D NOR roadmap tackles planar scaling barriers, promising higher capacity without cost spikes. A U.S. infotainment supplier moved from 128 Mbit to 256 Mbit, investing 15% more per chip to enable immersive graphics and over-the-air features.

By End-User Application: Consumer Electronics Leads as Automotive Surge Continues

Consumer electronics generated 42% of 2024 revenue as smartphones, tablets, and smart TVs require execute-in-place code that can boot in milliseconds. A Brazilian TV brand adopted quad SPI NOR for 2025 sets, slicing boot time by 35% even as component costs rose 10% due to supply constraints. Enhanced user experience offsets the price hike.

Automotive revenue is growing at 5.8% CAGR through 2030 as electronic content per vehicle escalates. GigaDevice’s ASIL-D certified GD25/55 series underpins safe over-the-air updates. A U.S. tier-1 supplier integrated the device to comply with tightening software lifecycle requirements. Industrial automation remains robust as PLC vendors transition from EEPROM, while 5G infrastructure and aerospace programs supply high-margin specialty demand.

By Voltage: 3 V Class Dominates While 1.8 V Accelerates

The 3 V class generated an equal of 52% revenue in 2024. Designers favor its noise immunity and compatibility with legacy regulators in factory controllers and body electronics. A U.S. PLC maker continues sourcing 3 V parts to avoid power-architecture redesign and requalification costs that can exceed USD 1 million per product line.

Americas NOR Flash market size for 1.8 V devices is smaller today, yet growing at a 5.5% CAGR. Wearables, smart meters, and portable medical sensors need lower voltage to stretch battery life. GigaDevice’s dual-supply SPI NOR enables 1.8 V operation without reworking host processors, easing adoption. Wide-range 1.65–3.6 V parts address fluctuating supply rails in automotive cold-crank events, while nascent 1.2 V variants target energy-harvesting IoT tags.

By Process Technology Node: 65 nm Leads While Advanced Nodes Accelerate

Mainstream 65 nm production delivered 38% of 2024 revenue for the Americas NOR Flash market. The node offers mature yields and proven reliability needed for 10-year lifecycles in body control modules. An automotive tier-1 supplier standardized on 65 nm for new door modules, balancing cost and assurance of supply through 2035.

28 nm and below nodes, though only limited market share today, are advancing at a 5.5% CAGR. ADAS processors and space avionics require higher densities and lower active power, which smaller geometries deliver. Infineon’s radiation-hardened NOR produced on an advanced node supports QML-V goals, confirming premium demand. 90 nm parts persist in legacy meter and set-top boxes, while 55 nm and 45 nm nodes bridge the cost and performance gaps for industrial drives.

By Packaging Type: QFN/SOIC Leads While WLCSP/CSP Gains Momentum

QFN/SOIC packages represented 41% of 2024 revenue, aided by robust solder joints and straightforward pick-and-place flows. A Canadian industrial manufacturer unified its BOM around QFN to simplify line qualification and extended-temperature reliability tests. Infineon’s SEMPER portfolio leverages these formats across 16- to 24-pin counts, aligning with bulk reflow processes.

Americas NOR Flash market size for WLCSP/CSP devices is smaller but climbing at a 5.4% CAGR. Smartphones, smartwatches, and insulin pumps demand footprint savings of up to 70%. Although assembly yield targets are tighter, the area reduction justifies a 12% cost premium in volume. BGA/FBGA remains vital for high-I/O automotive processors that need thermal slug designs, while niche ceramic or hermetic packages serve extreme aerospace temperatures.

Geography Analysis

The United States remains a key contributor to America's NOR Flash market with about 72% revenue share. Federal incentives of USD 39 billion are catalyzing more than USD 200 billion in new semiconductor projects, including Micron’s USD 50 billion fabs. A new NOR production line in Arizona cut domestic lead times by 40%, supporting U.S. automakers developing Level 2+ driver-assistance.

Mexico accounted for a smaller share, however, is poised for a 5.9% CAGR to 2030. IMMEX incentives encourage nearshoring, and Guadalajara’s electronics hub expanded NOR consumption by 65% year-on-year to supply infotainment dashboards for North American assembly plants. Parallel NOR retains relevance in border aerospace facilities owing to ITAR-compliant production lines.

Brazil's growth in the studied market is propelled by telecom densification. A São Paulo carrier installed 5,000 new 5G small cells, boosting NOR demand by about 28% within communications gear. Federal R&D tax credits help offset customs duties on imported tool sets.

The studied market in Canada is also anticipated to grow owing to stable demand in mining automation and smart-home OEM clusters in Ontario. The federal CHIPS program aims to scale wafer capacity, and a materials supplier opened a photolithography chemicals plant to service regional fabs.

The Rest-of-South-America segment also shows notable growth prospects as countries like Chile and Colombia modernize telecom networks and encourage IoT agriculture pilots. Cross-border knowledge transfer from Mexico’s maquiladora ecosystem is expected to shorten learning curves for local contract manufacturers.

Competitive Landscape

The five largest vendors—Infineon, Micron, GigaDevice, Macronix, and Winbond—held about 60% of 2024 revenue, indicating moderate concentration. Infineon reinforced its edge by certifying SEMPER NOR to ASIL-D in May 2025. It also bought Marvell’s Automotive Ethernet unit for USD 2.5 billion in April 2025 to integrate networking with memory and microcontrollers, raising projected revenue significantly by 2025.

Micron secured USD 6.1 billion in federal funding, unlocking dual-state fabs that will raise advanced-memory output and shorten domestic lead times. Process co-optimization with equipment suppliers aims to cut die cost by 15% by 2027, bolstering its position against Asian incumbents.

GigaDevice’s focus on ultra-low-power architecture helped it seize over 15% of America's NOR Flash market share in 2024. The GD25NE family halved read power, capturing design wins in Canadian smart-security sensors. Management targets notable growth by 2025 through sustained 10% R&D expenditure.

Macronix bets on 3D NOR to sidestep planar scaling challenges. Proof-of-concept samples demonstrated vertical stacking without sacrificing random-access speed, attracting interest from infotainment device makers seeking denser footprints.

Winbond leverages TrustME® secure-flash credentials to service automotive users needing post-quantum cryptography support. January 2025 shipments validated mass-production readiness under ASIL-D.

Niche entrants such as Alliance and Everspin address legacy asynchronous interfaces and MRAM overlays, respectively, offering specialized paths around mainstream competition. The CHIPS Act’s domestic-content requirements may favor U.S. fabs such as GlobalFoundries, which can supply wafers without export-license complexities, broadening choices for defense contractors.

Americas NOR Flash Industry Leaders

-

Infineon Technologies AG

-

Micron Technology Inc.

-

GigaDevice Semiconductor Inc.

-

Macronix International Co. Ltd.

-

Winbond Electronics Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infineon SEMPER NOR Flash family achieved ISO 26262 ASIL-D certification, enabling deployment in safety-critical automotive systems.

- April 2025: Micron secured USD 6.1 billion in CHIPS funding to support USD 50 billion fab investments in Idaho and New York.

- April 2025: Infineon bought Marvell’s Automotive Ethernet business for USD 2.5 billion to enhance software-defined vehicle solutions.

- February 2025: SkyWater agreed to acquire Infineon’s Austin 200 mm fab, boosting U.S. capacity for 130 nm–65 nm nodes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Americas NOR flash memory market as the annual value of stand-alone serial and parallel NOR devices shipped into finished equipment across North, Central, and South America. This includes code-storage chips for automotive electronics, industrial controllers, consumer gadgets, telecom gear, and aerospace systems, reported in USD revenue at the manufacturer-to-OEM level.

Scope exclusion: NAND flash, embedded eFlash inside MCUs, and foundry service revenue are outside the study.

Segmentation Overview

-

By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

-

By Interface (Value)

- Standard SPI

- QSPI

- Octal/OSPI

- HyperBus/HX

-

By Density (Value)

- 2 Megabit And Less NOR

- 4 Megabit And Less-NOR (greater than 2mb) NOR

- 8 Megabit And Less (greater than 4mb) NOR

- 16 Megabit And Less (greater than 8mb) NOR

- 32 Megabit And Less (greater than 16mb) NOR

- 64 Megabit And Less (greater than 32mb) NOR

- 128 Megabit and Less (greater than 64MB) NOR

- 256 Megabit and Less (greater than 128MB) NOR

- Greater than 256 Megabit

-

By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others - 1.2V Class (and similar sub-1.8V) (2.5V, 5V, etc.)

-

By End-user Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other Applications

-

By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

-

By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Others

-

By Country (Value, Volume)

- United States

- Canada

- Mexico

- Brazil

- Rest of Americas

Detailed Research Methodology and Data Validation

Primary Research

Mordor Intelligence experts interview chip makers, contract assemblers, automotive Tier-1 design leads, and distribution channel managers across the United States, Mexico, and Brazil. Dialogs validate ASP corridors, density mix shifts, and attach-rate assumptions, and they flag disruptive policy moves like CHIPS Act incentives.

Desk Research

Our analysts scan tier-1 public sources such as United States International Trade Commission trade logs, UN Comtrade shipment codes, Canada Innovation, Brazil ANATEL device approvals, and industry association briefs from JEDEC and SEMI. Financial filings, investor decks, and reputable press updates enrich pricing and capacity checks. Paid databases, including D&B Hoovers for supplier financials and WSTS for regional semiconductor billings, supply structured time series. The sources cited here are illustrative; many additional references informed the dataset.

Market-Sizing & Forecasting

A top-down reconstruction starts with WSTS revenue for serial and parallel NOR lines, adjusted by Americas import-export flows and by in-house fab output disclosed during earnings calls. These are then split by end use through penetration-rate based demand pools. Select bottom-up supplier roll-ups and channel checks temper the totals. Key levers tracked include automotive ECU NOR content per vehicle, 1.8 V serial share in 5G CPE shipments, industrial robot installations, average selling price erosion, wafer capacity utilization, and exchange-rate swings. Multivariate regression, trained on the above drivers, projects values through 2030, while scenario analysis handles policy or supply shocks.

Data Validation & Update Cycle

Outputs pass variance tests versus customs data and WSTS billings before a second-analyst review. A fresh validation round precedes every annual refresh, and we trigger interim updates if trade sanctions, fab outages, or policy grants materially shift forecasts.

Why Mordor's Americas NOR Flash Baseline Commands Reliability

Published estimates often diverge because firms pick dissimilar regions, bundle extra memory types, or refresh models on different cadences.

Key gap drivers include scope (some studies report global totals or only North America), inclusion of NAND or embedded flash, reliance on production value rather than end-use demand, and currency conversion cut-offs. Our disciplined region definition, driver-level variables, and yearly refresh make the baseline replicable and decision-ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 604.33 million (2025) | Mordor Intelligence | - |

| USD 1.9 billion (2022) | Regional Consultancy A | Counts all North America chip shipments and mixes bare-die sales with packaged parts, with no end-use split |

| USD 656.4 million (2021) | Trade Journal B | Uses older base year and omits Latin American demand, while applying static ASPs |

| USD 5.27 billion (2025) | Global Consultancy C | Global scope that bundles parallel NOR and broader embedded memory segments |

These comparisons show that once region, device type, and pricing logic are aligned, Mordor's figure sits at the credible midpoint, giving clients a transparent, defensible starting point for strategy and budgeting.

Key Questions Answered in the Report

What is the projected value of the Americas NOR Flash market in 2030?

The market is forecast to reach USD 781.60 million by 2030 based on a 5.28% CAGR.

Why is serial NOR preferred over parallel NOR in many designs?

Serial NOR uses fewer pins, lowers standby current, and reduces board area, making it well-suited to IoT, consumer, and automotive electronics.

How are government incentives affecting NOR Flash manufacturing?

Programs such as the U.S. CHIPS Act reduce fabrication costs and shorten supply chains, encouraging new domestic capacity that improves lead times.

What distinguishes SLC from MLC NOR Flash?

SLC stores one bit per cell, providing higher endurance and faster access, while MLC stores multiple bits per cell, offering greater density at lower cost but reduced write cycles.

Page last updated on: