Europe NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

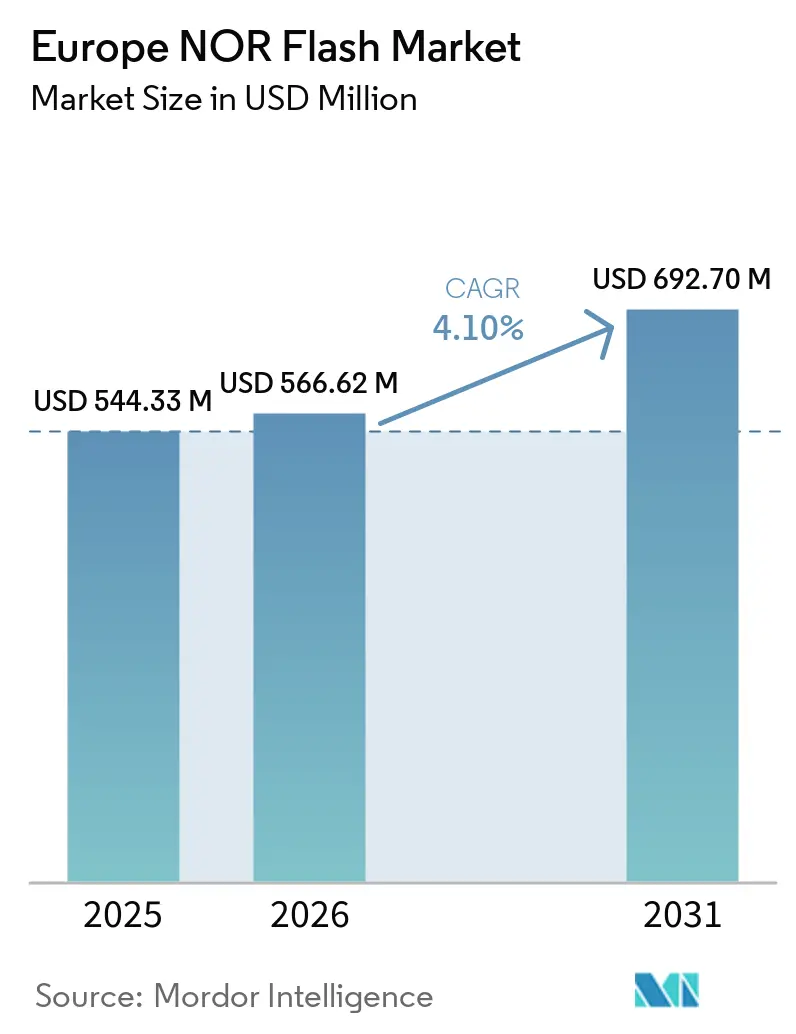

| Base Year Market Size (2025) | USD 544.33 Million |

| Market Size (2026) | USD 566.62 Million |

| Market Size (2031) | USD 692.70 Million |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe NOR Flash Market Analysis by Mordor Intelligence

The Europe NOR Flash Market size is projected to expand from USD 544.33 million in 2025 and USD 566.62 million in 2026 to USD 692.70 million by 2031, registering a CAGR of 4.10% between 2026 to 2031. In terms of shipment volume, the market was valued at 1.60 billion units in 2025 and is expected to grow from 1.7 billion units in 2026 to 2.13 billion units by 2031, at a CAGR of 4.89% during the forecast period (2026-2031). The Europe NOR Flash Memory market is moving beyond its older role as a stable code-storage category and is becoming a more strategic component layer for software-defined vehicles, edge-AI systems, and high-reliability industrial controllers. Demand is being shaped by European automakers shifting toward zonal and domain-controller architectures, where higher-bandwidth NOR with authenticated boot capability meets system needs that commodity NAND does not. The regional supply picture is also becoming more supportive as European policy and fab investments improve visibility around specialty-node availability for automotive and industrial memory programs. Competitive pressure remains active because established suppliers still lead premium sockets, while newer entrants are narrowing qualification gaps in the mid-density range and creating pricing pressure in selected tiers. The main restraints remain focused on photomask tightness at mature nodes and on low-density substitution risk from 1.8 V NAND in cost-sensitive consumer IoT applications, which can limit volume growth in lower-margin categories.

Key Report Takeaways

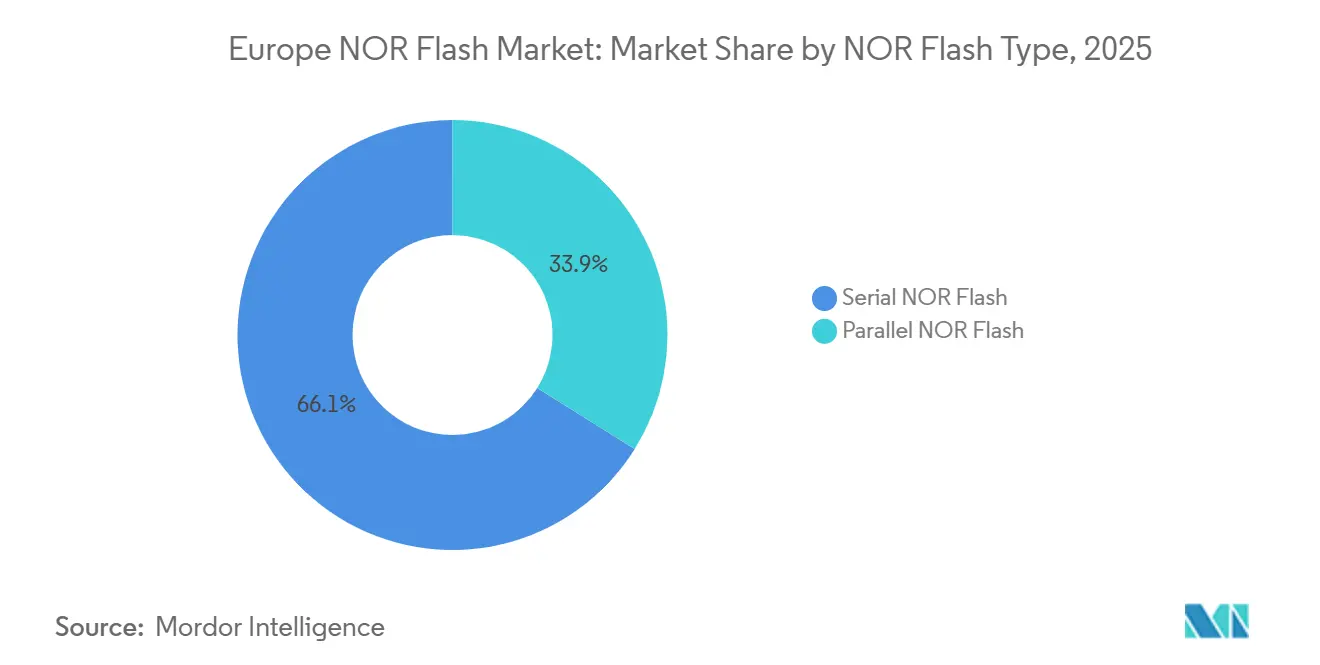

- By NOR flash type, serial NOR Flash led the Europe NOR Flash market with a 66.1% share in 2025 and is projected to register a CAGR of 5.7% through 2031.

- By interface, Quad SPI held 49.7% share of the Europe NOR flash market in 2025, while Octal and xSPI are forecast to grow at 5.9% through 2031.

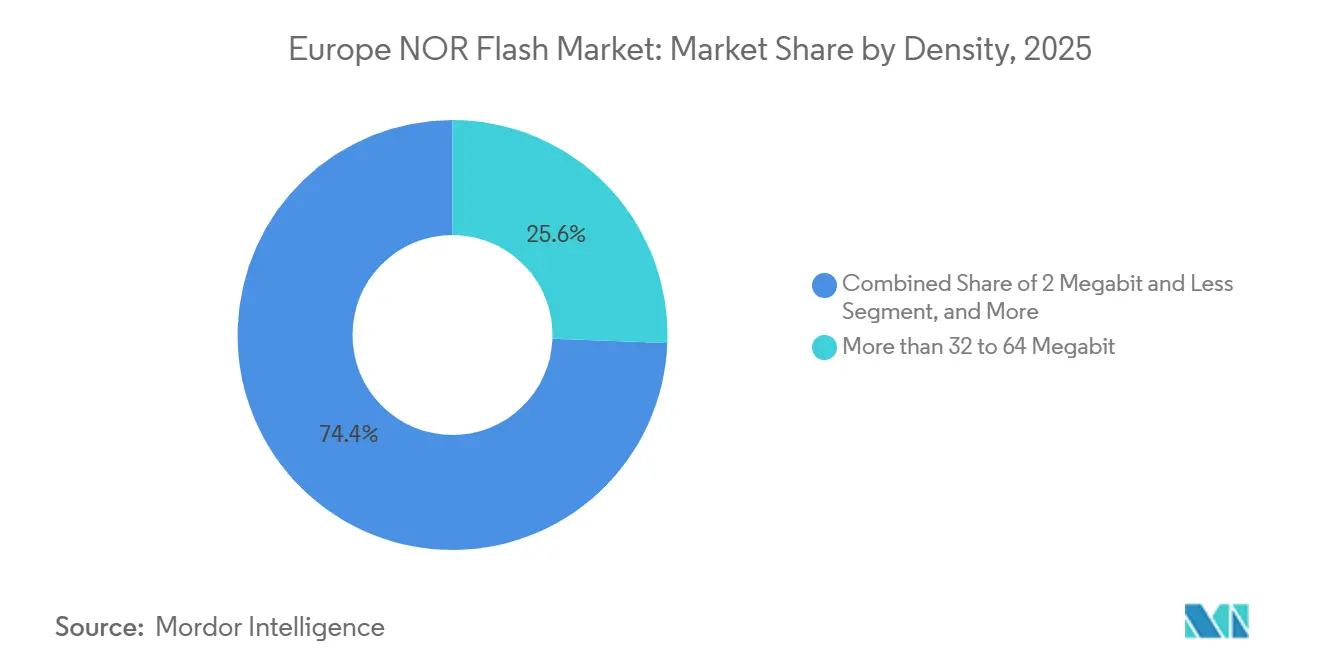

- By density, the more than 32 to 64 megabit band held 25.6% share of the Europe NOR Flash memory market in 2025, while the more than 128 to 256 megabit band is projected to expand at a 6.1% CAGR through 2031.

- By voltage, the 1.8 V class held 42.3% share of the Europe NOR Flash market in 2025, while the 1.2 V class is projected to grow at a 6.3% CAGR through 2031.

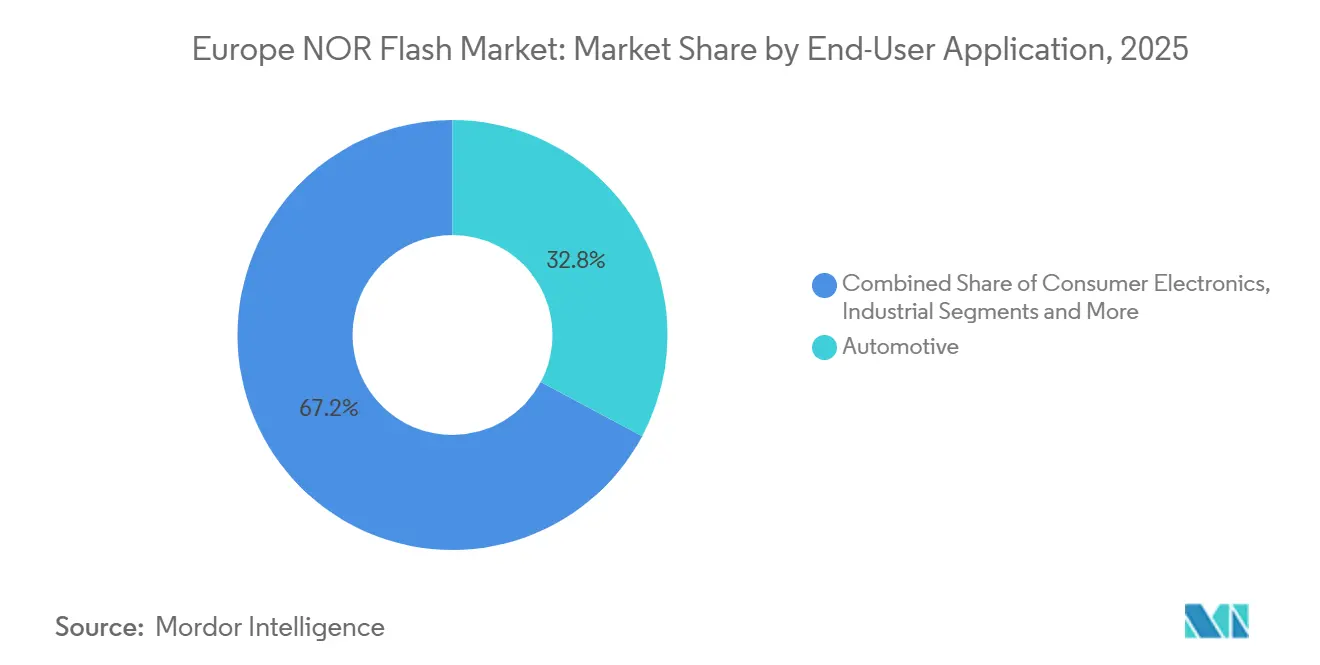

- By end-user application, automotive accounted for 32.8% of the Europe NOR Flash market in 2025 and is also the fastest-growing application, with a 5.6% CAGR through 2031.

- By process technology node, 28 nm and below held 39.9% share of the Europe NOR Flash market in 2025 and is projected to grow at a 6.2% CAGR through 2031.

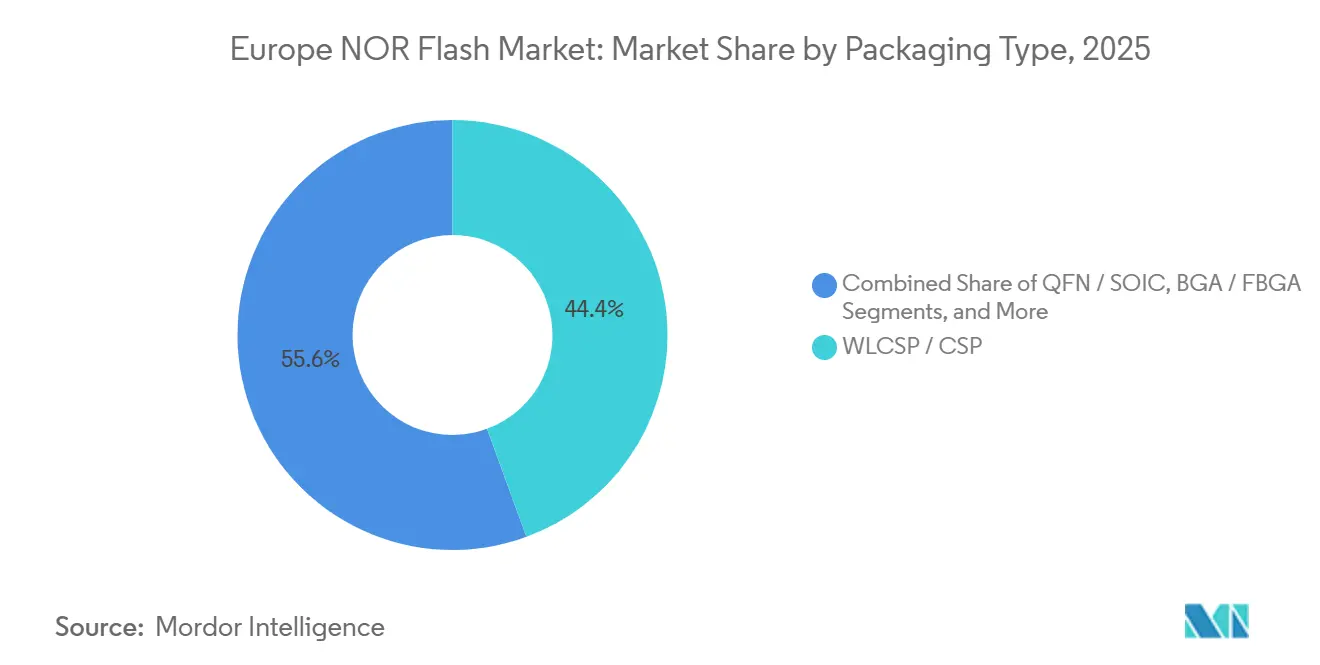

- By packaging type, WLCSP and CSP held 44.4% share of the Europe NOR Flash market in 2025 and are projected to grow at a 5.9% CAGR through 2031.

- By geography, Germany held 37.2% share of the Europe NOR Flash market in 2025, while Italy is projected to grow at a 5.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global nor flash market size report represents that cumulative total.

Europe NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift To OTA Firmware Updates In European EVs Boosting High-Density SPI NOR Demand | +1.2% | Germany, France, UK, core EV manufacturing hubs, spill-over to Italy and Nordics | Medium term (2-4 years) |

| Automotive OEM-Mandated Flash Quality Targets Driving Design-Ins In Germany And Nordics | +0.9% | Germany, primary, Sweden, Finland, and Netherlands | Short term (≤ 2 years) |

| EU Data-Centric Edge-AI Roll-Outs Elevating Serial NOR Adoption In Industrial PLCs | +0.7% | Germany, Industrie 4.0 corridors, France, and Italy | Medium term (2-4 years) |

| EU Chips Act Funding For 28 Nm And 45 Nm NOR Lines In Dresden | +0.5% | Germany, Silicon Saxony, secondary gains across EU27 | Long term (≥ 4 years) |

| Telecom Open-RAN Deployments In UK And France Requiring Low-Latency Boot Code Storage | +0.4% | UK and France, spill-over to Germany via Vodafone Open RAN rollout | Medium term (2-4 years) |

| Medical-Grade Wearables Regulation Accelerating Secure NOR Integration | +0.3% | EU27, strongest pull in Germany, France, and Italy medical device clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift To OTA Firmware Updates In European EVs Boosting High-Density SPI NOR Demand

UN Regulation No. 156 made a software update management system mandatory for all new vehicles sold in the European Union from July 2024, pushing Tier-1 suppliers toward dual-bank NOR designs that can update one bank while the other keeps the live code running.[1]European Union, “UN Regulation No. 156 - Uniform Provisions Concerning the Approval of Vehicles with Regards to Software Update and Software Updates Management System,” EUR-Lex, eur-lex.europa.eu That requirement increases the minimum flash allocation per ECU because rollback images must remain available, thereby directly increasing density demand in the European NOR Flash Memory market. It also supports better pricing for automotive-grade parts because OTA-ready NOR with integrated security features sells at a premium to standard code-storage devices. Infineon’s SEMPER X1 was introduced as an LPDDR Flash product aimed at next-generation automotive electronic and electrical architectures where fast access and real-time execution matter.[2]Infineon Technologies AG, “German Government Issues Final Funding Approval for New Infineon Fab in Dresden,” Infineon Technologies AG, infineon.com As European premium OEMs continue to standardize software-defined vehicle platforms, this shift keeps high-density SPI NOR in a favorable position across the forecast period.

Automotive OEM-Mandated Flash Quality Targets Driving Design-Ins In Germany And Nordics

German Tier-1 suppliers and Nordic automotive electronics manufacturers continue to treat ASIL-D functional safety as a practical entry requirement for new ADAS and gateway ECU programs, which raises the qualification bar in the Europe NOR Flash Memory market. GigaDevice’s GD25/55 automotive-grade SPI NOR family received ISO 26262 ASIL D certification in December 2024, opening access to qualification activities previously reserved for more established suppliers. Macronix also expanded its automotive-grade options in January 2025 by extending ASIL D compliance across both OctaFlash and Quad SPI variants in its MXSMIO family.[3]Macronix International Co. Ltd., “Macronix Flash Memory Family Includes Highest Level of Automotive Safety,” Macronix Newsroom, macronix.com Once an additional supplier reaches ASIL-D readiness, procurement teams gain greater negotiating power over socket pricing, even when incumbent vendors retain the design win. AEC-Q100 Grade 1 thermal and reliability screening adds another barrier, helping protect premium automotive sockets from low-capability entrants.

EU Data-Centric Edge-AI Roll-Outs Elevating Serial NOR Adoption In Industrial PLCs

European factory automation programs are placing more AI inference at the controller level, which increases demand for persistent and low-latency code storage in industrial systems across the Europe NOR Flash market. Macronix said in March 2025 that its OctaFlash MX25UW1G45G had been validated on STMicroelectronics’ STM32N6 AI-accelerated MCU platform for uses that include industrial automation, smart factory systems, and medical imaging. This matters because edge-AI controllers need frequent code and model updates without the erase-management burden that NAND brings at lower densities. That operating profile favors serial NOR, especially Octal and xSPI variants, in PLC refresh cycles tied to predictive maintenance and real-time anomaly detection. The result is a steadier industrial demand base that supports growth even when some consumer-oriented memory categories remain under substitution pressure.

EU Chips Act Funding For 28 Nm And 45 Nm NOR Lines In Dresden

The European Commission approved EUR 920 million (approximately USD 994 million) in German state aid in February 2025 to support Infineon’s semiconductor manufacturing project in Dresden in line with the objectives of the European Chips Act.[4]European Commission, “Commission Approves EUR 920 Million German State Aid Measure To Support Infineon in Setting Up a New Semiconductor Manufacturing Facility,” European Commission Press Corner, europa.eu Infineon then received final German government funding approval in May 2025 and said production at the Smart Power Fab is targeted to start in 2026, alongside its own EUR 5 billion (approximately USD 5.4 billion) investment commitment. These projects do not create a pure NOR-only capacity wave in the near term, but they improve supply assurance around the specialty nodes that matter most for advanced automotive-grade NOR. This supports dual-sourcing confidence for European OEMs seeking lower dependence on Far East sole-supplier exposure. Over time, that supply security improves the operating environment for the European NOR Flash Memory market, especially in high-reliability automotive and industrial programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fab-Level Yield Losses On 28 Nm Floating-Gate Nodes Elevating ASP Volatility | -0.8% | Global supply chain, direct ASP impact on Germany and France automotive procurement | Short term (≤ 2 years) |

| Rising 1.8 V NAND Substitutes Below 256 Mb In Consumer IoT Nodes | -0.6% | EU-wide consumer IoT, strongest impact in the UK and the rest of Europe, consumer electronics clusters | Medium term (2-4 years) |

| Tight Allocation Of Specialty Photomasks In Europe Hindering Parallel NOR Expansion | -0.4% | Silicon Saxony and the European foundry ecosystem | Medium term (2-4 years) |

| Post-Brexit Customs Delays Impacting Lead-Times For UK Automotive Tier-1s | -0.2% | UK, specifically the Midlands and North-West automotive corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fab-Level Yield Losses On 28 Nm Floating-Gate Nodes Elevating ASP Volatility

Advanced floating-gate integration at 28 nm continues to face charge-loss and cell-coupling challenges, which can widen erase thresholds and reduce effective output in higher-density NOR products. When yield tightens, suppliers usually prioritize premium automotive grades first, leaving industrial and communications customers with less procurement and pricing flexibility. In the Europe NOR Flash Memory market, that pattern matters because automotive buyers in Germany and France already operate under strict qualification rules that limit easy substitution. AEC-Q100 and JEDEC reliability screening add additional filtering steps, meaning baseline wafer volumes do not directly translate into saleable automotive die. The practical result is more volatile pricing and longer planning cycles for buyers who need qualified NOR at advanced specialty nodes.

Rising 1.8 V NAND Substitutes Below 256 Mb In Consumer IoT Nodes

Serial NAND at 1.8 V continues to pressure NOR below the 256 Mb threshold in cost-sensitive consumer IoT designs, where cost per megabit often outweighs random-read advantages. KIOXIA has published a technology brief that positions 1 Gb 1.8 V SLC NAND as a lower-cost alternative to NOR in applications where the software stack can tolerate managed storage complexity.[5]KIOXIA, “NOR to NAND Technology Brief,” KIOXIA Americas, americas.kioxia.com The substitution risk is highest in smart home devices, simple wearables, and entry-level connected appliances, where bill-of-materials pressure is high. It is less damaging in safety-critical or ultra-lean embedded systems because NAND still requires file-system and controller overhead that many simple RTOS designs do not carry. Even so, this remains a clear restraint on the lower end of the Europe NOR Flash market, where product differentiation is weaker, and price sensitivity is higher.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By NOR Flash Type: Serial NOR Flash Strengthens Its Lead Through Design Simplicity And Broader Qualification Support

Serial NOR Flash held 66.1% of the Europe NOR Flash market share in 2025, which reflected a long-running shift away from the wider bus structure used in parallel devices. The segment kept that lead because serial parts reduce pin count, lower PCB routing complexity, and fit more easily into compact automotive ECUs and industrial controllers. In many new programs, those system-level benefits matter as much as component cost because board area, power routing, and package integration are becoming stricter design priorities. The European NOR Flash market has therefore favored serial parts not only for mainstream MCU-based systems, but also for newer controller designs that need better bandwidth without a large physical footprint. Winbond’s Octal NOR portfolio shows how far serial architectures have advanced, with the company highlighting continuous read throughput up to 400 MB/s on xSPI-enabled products.

Parallel NOR Flash still has value in selected avionics, defense communications, and long-life industrial PLC programs, where legacy timing behavior and redesign risk are more important than pin efficiency. Those uses are narrower, but they remain commercially relevant because customers in such programs often prefer platform continuity over architectural change. Functional safety rules such as ISO 26262 apply across both product types, yet serial NOR has benefited from a wider flow of recent certification investments and product launches from active suppliers. That wider ecosystem matters because procurement teams in automotive and industrial systems increasingly favor parts with stronger tool support, broader interface compatibility, and longer forward roadmaps. As a result, the European NOR Flash Memory market continues to consolidate around serial solutions for new designs, while parallel NOR serves more of a maintenance and continuity role in specialized deployments.

By Interface: Quad SPI Holds The Installed Base While Octal And xSPI Push The Next Performance Step

Quad SPI accounted for 49.7% of the Europe NOR Flash market in 2025, underscoring its deep embeddedness in current MCU and SoC ecosystems. Its lead comes from mature driver support, broad chipset compatibility, and a long history of qualification across automotive and industrial systems. That installed base still matters because many OEMs prefer interface continuity when redesign costs are high, and code migration budgets are tight. Infineon’s SEMPER NOR product range continues to support these mainstream embedded requirements across automotive and industrial platforms that prioritize validated operation over aggressive interface change. For much of the European NOR Flash market, Quad SPI remains the default choice when bandwidth demands stay within current execute-in-place limits.

The balance is shifting toward higher-performance systems because domain controllers, AI-enabled edge nodes, and advanced communications hardware are pushing beyond traditional Quad SPI throughput ceilings. Octal and xSPI therefore represent the fastest-growing interface class, with the market forecast indicating 5.9% CAGR through 2031. Macronix demonstrated this direction in March 2025, when it said its OctaFlash products were selected for STMicroelectronics’ STM32N6 platform and could support 200 MHz DDR mode for 400 MB/s throughput. JEDEC xSPI standardization also reduces supplier lock-in concerns, making Octal migration easier for OEMs planning the next board generation. The result is a market mix where Quad SPI maintains its broad installed base, while Octal and xSPI capture a rising share of higher-bandwidth applications in the European NOR Flash Memory market.

By Density: Mid-Range Devices Keep The Largest Base While 256 Mb To 128 Mb Gains The Fastest

The more than 32 to 64 megabit NOR segment accounted for 25.6% of the Europe NOR Flash Memory market in 2025, making it the largest density tier by revenue. It reflects the needs of single-ECU automotive electronics, industrial sensor-fusion nodes, and telecom customer-premises equipment that require firmware storage without the higher cost of density bands. This segment remains durable as many embedded programs still fit within this range. The 256 Megabit and Less (greater than 128MB) NOR tier is forecast to grow at a 6.1% CAGR through 2031, driven by rising system complexity. In Europe, this shift aligns with zonal and domain-controller designs, consolidating code bases previously spread across smaller ECUs.

Smaller-density segments, more than 4 to 8 megabit, more than 2 to 4 megabit, and 2 megabit and less NOR, retain a stable installed base in legacy industrial controllers and simple sensor platforms. Demand remains steady as customers prioritize design continuity over performance upgrades. Supplier roadmaps are extending upward for new low-power applications, as seen in GigaDevice’s March 2026 expansion of its GD25UF ultra-low-power SPI NOR series from 8 Mb to 256 Mb. This supports AI computing platforms, medical wearables, and edge-AI systems needing larger low-power storage while retaining NOR flash characteristics. The European NOR Flash Memory market remains anchored in mid-range densities, with growth accelerating in upper-middle tiers due to increasing software complexity.

By Voltage: The 1.8 V Class Holds The Core Base While 1.2 V Becomes The Main Growth Layer

The 1.8 V class led voltage segmentation, with a 42.3% share in 2025, confirming its long-standing role in automotive ECUs and industrial safety controllers. This dominance comes from decades of platform standardization around 1.8 V supply rails, especially in embedded systems where reliability and qualification history carry more weight than aggressive redesign. Wide-voltage products also remain relevant because they enable engineers to bridge legacy 3 V environments and newer low-power SoC platforms without major architectural changes. In the European NOR Flash Memory market, that flexibility supports continued use in industrial refresh cycles where equipment fleets are upgraded in stages rather than replaced at once. The installed base, therefore, remains centered on 1.8 V, even as new low-power design priorities shift attention elsewhere.

The 1.2 V class is the fastest-growing voltage segment, with a 6.3% CAGR through 2031, because it aligns well with newer SoC input and output architectures that demand lower power and less board overhead. GigaDevice highlighted this direction in March 2025, introducing its GD25NE series with a 1.8 V core and 1.2 V I/O, claiming faster read performance and lower power consumption for compact embedded designs. That matters for wearables, medical diagnostics, and edge AI accelerator cards, where power budgets and space are both tight. The 3 V class still keeps legacy volumes in industrial and communications equipment with long refresh cycles, but it is not where the European NOR Flash Memory market is finding its strongest new design momentum. As a result, 1.8 V remains the anchor tier, while 1.2 V is emerging as the strategic growth layer for next-generation embedded platforms.

By End-User Application: Automotive Keeps The Largest Base And Also Sets The Fastest Pace

Automotive applications accounted for 32.8% share of the Europe NOR Flash Memory market in 2025 and are projected to advance at a 5.6% CAGR through 2031, which is a strong combination of scale and momentum. That pattern signals that the segment is still building lead rather than flattening, because each new vehicle platform carries more code, more secure boot requirements, and tighter functional safety rules. Software-defined features such as autonomous parking, battery management, zonal control, and advanced infotainment are all increasing flash content per vehicle, even when regional auto production is uneven. In the European NOR Flash market, this keeps automotive demand tied to architectural content growth rather than only unit output. It also strengthens the premium mix because higher-density, more highly qualified parts are gaining share within the automotive basket.

Industrial applications remain the second major support layer because Europe’s factory base continues to refresh PLCs and edge-control systems as part of digitalization and predictive maintenance programs. Communication applications are also important, especially when Open RAN and virtualized network hardware require dependable, low-latency boot-code storage for radio and distributed unit systems. Samsung said in April 2025 that it had validated a new chipset with Vodafone as part of broader AI-native and Open RAN network progress in Europe, which supports continued infrastructure activity related to secure, fast-boot memory. Consumer electronics remain the most exposed area because NAND substitution is more practical at lower densities, while medical and other applications are gaining structural support from EU device regulation and registration requirements. This creates an application mix where automotive leads the European NOR Flash market, industrial provides resilience, communications adds targeted upside, and medical demand builds a steadier long-cycle floor.

By Process Technology Node: 28 Nm And Below Leads On Both Scale And Growth

The 28 nm and below tier held 39.9% of the Europe NOR Flash Memory market share in 2025 and is projected to expand at a 6.2% CAGR through 2031. This dual lead reflects the node’s fit for advanced automotive NOR, where density, endurance, retention, and safety margins must coexist in a qualified process. Infineon’s SEMPER product materials continue to emphasize long retention, high endurance, and automotive-grade reliability, which helps explain why leading-edge NOR nodes are not being displaced in premium use cases. In the European NOR Flash Memory market, this is especially important for higher-density automotive applications, where software stacks and safety validation are both rising. Advanced nodes, therefore, remain a central part of value creation even when other memory categories compete more aggressively for wafer allocation.

Older nodes such as 90 nm and above, 65 nm, and 55 nm, including 58 nm, still serve a clear purpose in long-life industrial, defense, and communications equipment. Customers in those programs often avoid node migration because redesign, validation, and field support costs can exceed the benefits of moving to a smaller process. Winbond’s technical materials show how a well-optimized 58 nm platform can still deliver high-performance code-storage products suited to newer interfaces and compact form factors. The 45 nm node is also receiving more attention as European capacity planning under Chips Act-backed projects improves confidence in specialty manufacturing continuity. The result is a split structure in the Europe NOR Flash Memory market where 28 nm and below drives premium growth, while older nodes remain commercially durable in long-cycle embedded programs.

By Packaging Type: WLCSP And CSP Win Where Space, Signal Integrity, And Integration Matter Most

WLCSP and CSP packaging held a 44.4% share in 2025 and are projected to grow at a 5.9% CAGR through 2031, giving this packaging class the strongest combined position. That lead comes from the overlap between automotive electronics and medical wearables, where designers need very small footprints, low parasitic effects, and high integration efficiency. The Europe NOR Flash Memory market has steadily favored these package types because modern boards are more space-constrained and higher-speed interfaces are less tolerant of packaging-related signal penalties. GigaDevice’s WLCSP portfolio spans a broad density range and targets wearables and IoT devices that benefit from extremely thin and compact memory packaging. That packaging direction aligns well with system-in-package trends that are spreading across advanced embedded designs.

QFN and SOIC packages still maintain a large installed base in industrial and legacy communications systems, where board space is less restrictive, and field rework remains important. BGA and FBGA formats serve higher-density applications that require more I/O capability and tighter package routing for faster interfaces. The Others category, including known good die options, is also gaining relevance in specialized module assembly and multi-chip integration work. In the Europe NOR Flash Memory market, this means packaging is no longer a secondary selection issue because it now shapes form factor, thermal behavior, signal quality, and integration cost at the system level. WLCSP and CSP therefore remain the lead package family not only because they are smaller, but because they fit the broader design direction of automotive, medical, and advanced edge electronics.

Geography Analysis

Germany held a 37.2% share of the Europe NOR Flash Memory market in 2025, keeping it well ahead of every other country in the regional mix. This leadership stems from the concentration of premium automotive OEMs and Tier-1 electronics suppliers that use higher-density, higher-reliability NOR across ADAS, infotainment, and controller domains. Germany also benefits from its move toward more centralized vehicle architectures, where fewer controllers carry larger software images and therefore need stronger boot memory performance. Infineon said in May 2025 that its Dresden Smart Power Fab had received final funding approval and was targeting a 2026 production start, which strengthens Germany’s role as a strategic supply point for specialty semiconductor demand.

The United Kingdom and France remain the next most important country markets, although their demand profile is more mixed than Germany’s automotive-heavy pattern. In both countries, communications infrastructure activities related to Open RAN and virtualized radio networks create NOR demand that differs from that of vehicle electronics and is more closely tied to secure boot and low-latency code storage. France also benefits from medical technology and aerospace-linked electronics activity, where memory reliability and system integrity requirements remain high. The United Kingdom continues to face some logistics friction in supply planning because lead times can be affected when parts move through continental Europe or Asian production routes before entering local automotive and industrial programs. Even so, the Europe NOR Flash market continues to rely on both countries as important volume centers outside Germany because they combine communications, industrial, and selected automotive demand.

Italy is the fastest-growing country in the region with 5.4% CAGR through 2031, which reflects the expansion of automotive Tier-1 work in the Po Valley and a stronger medical electronics base around Bologna, Modena, and Milan. Its demand profile is well aligned with mid-range density NOR used in infotainment, instrument clusters, and embedded control modules, which places it in a favorable part of the regional mix. The rest of Europe adds further breadth through Scandinavian automotive and communications electronics, Polish manufacturing exports, and rising activity in Romania’s automotive electronics base. Medical device compliance under Regulation (EU) 2017/745, with EUDAMED-related obligations in force from May 2026, is also supporting secure NOR adoption across several regional manufacturing clusters.

Coverage of the nor flash market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia, alongside detailed country-level intelligence for France, Italy, United Kingdom, Germany, China, India, Japan, and South Korea, each shaped by local operating conditions.

Competitive Landscape

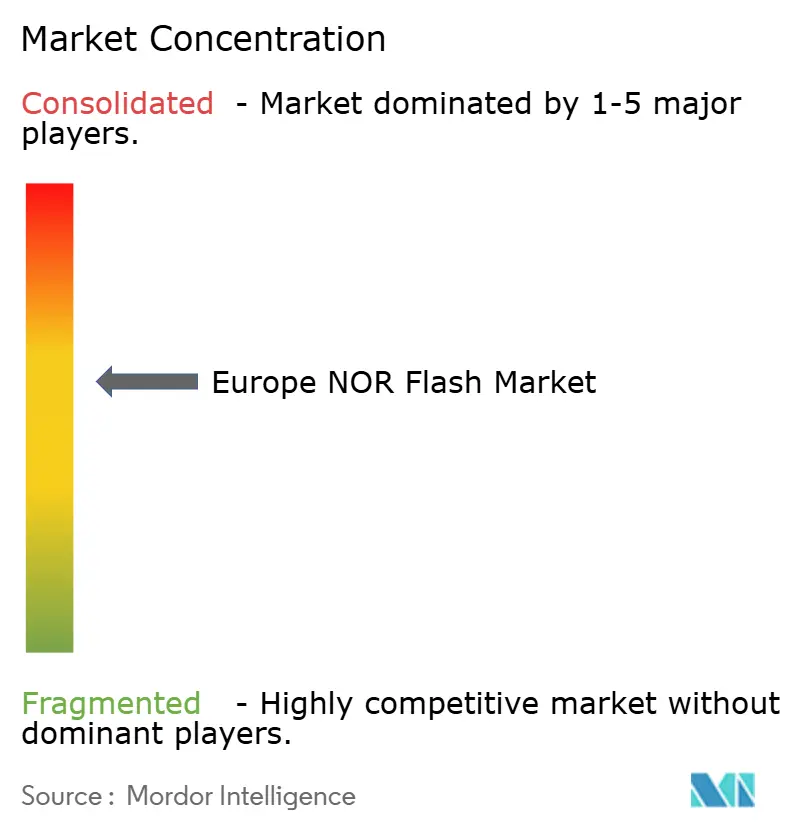

The European NOR Flash Memory market remains moderately concentrated, with Infineon Technologies AG, Winbond Electronics Corp., Macronix International Co., GigaDevice Semiconductor Inc., and Integrated Silicon Solution Inc. forming the core competitive group. The leading suppliers still control most premium automotive and industrial sockets because those programs reward depth of safety certification, lifecycle assurance, and interface roadmaps more than simple price competition. Even so, competition is becoming more active in the mid-density tier as newer entrants improve automotive readiness and push harder on pricing. This keeps the European NOR Flash Memory market competitive without fully fragmenting it.

Infineon’s position is reinforced by its automotive focus, its long-lifecycle support model, and its expanding Dresden manufacturing presence, all of which fit European OEM procurement priorities. Winbond competes on interface and throughput, particularly in Octal NOR, where its product line supports high-speed code storage use cases with strong read performance. Macronix has differentiated itself through secure-boot and memory security features, including the August 2025 launch of ArmorBoot MX76, which combined PUF-based authentication, data integrity verification, rollback prevention, and SPI NOR in one device. GigaDevice has moved aggressively in low-voltage and automotive-ready NOR, using product launches and qualification work to widen its addressable space in Europe. These company moves show that the competitive contest is increasingly being shaped by certification, security architecture, low-power operation, and roadmap depth rather than by density alone.

White-space opportunities remain visible in secure low-voltage NOR for medical wearables, in long-lifecycle supply-assured devices for rail and defense systems, and in memory that can support hardware-rooted cybersecurity requirements under European electronics regulation. Winbond’s technical discussion around the EU Radio Equipment Directive underscores how cybersecurity rules are making secure storage behavior more important in connected devices. This favors suppliers that can combine functional safety, secure boot, and long-term supply assurance in a single product family. As a result, the Europe NOR Flash market is competitive in pricing at the mid-range, but differentiation in the premium tier is still driven by quality, qualification depth, packaging, and embedded security capability.

Europe NOR Flash Industry Leaders

Infineon Technologies AG

Micron Technology Inc.

Winbond Electronics Corp.

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GigaDevice announced the expansion of its GD25UF series 1.2 V ultra-low-power SPI NOR Flash from 8 Mb to 256 Mb at Embedded World 2026 in Nuremberg, Germany, targeting AI computing platforms, medical wearables, edge AI, and automotive electronics. The broader density range positions GigaDevice to address a wider share of Europe’s low-power IoT and wearable NOR sockets.

- November 2025: GigaDevice launched the GD25NX series xSPI NOR Flash, featuring a 1.8 V core and 1.2 V I/O dual-voltage design that connects directly to 1.2 V SoCs without an external booster circuit, available in 64 Mb and 128 Mb densities in TFBGA24 and WLCSP packages. The GD25NX directly competes in the high-growth edge-AI and automotive wearables socket.

- October 2025: GlobalFoundries announced a EUR 1.1 billion (USD 1.19 billion) SPRINT capacity expansion at its Dresden, Germany site under European Chips Act co-funding, targeting production capacity of more than 1 million wafers per year by end-2028 with first new tool installations planned for the second half of 2026.

- August 2025: Macronix introduced the ArmorBoot MX76, a secure-boot NOR Flash combining PUF-based authentication, data integrity verification, monotonic rollback-prevention counters, and SPI interface in a single device supporting capacities up to 1 Gb. The product targets automotive, AI IoT, and medical applications demanding hardware root-of-trust at the memory layer.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

In this study, we define the Europe NOR flash memory market as all standalone serial and parallel NOR devices with densities above 512 Kb that are shipped to equipment manufacturers in automotive, industrial, consumer electronics, and telecom applications.

Scope Exclusion: Embedded flash blocks residing inside microcontrollers or system-on-chips are excluded to avoid double counting.

Segmentation Overview

- By Type (Value and Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Others - 1.2 V Class (Sub-1.8 V, 2.5 V, 5 V)

- By End-User Application (Value and Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-User Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (Including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Country

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

To verify desk findings, we interviewed application engineers, franchised memory distributors, and purchasing leads in Germany, the United Kingdom, France, and Italy. Their views on shipment discounts, automotive-grade premiums, and buffer stock practices helped us fine-tune assumptions and close information gaps.

Desk Research

Mordor analysts first mapped the landscape using open sources such as Eurostat import code HS 854232, World Semiconductor Trade Statistics regional sales, and the German Motor Transport Authority's electronics tables; these datasets reveal unit inflow, density shifts, and price erosion across Western and Central Europe. We then added insight from IEEE Xplore papers on xSPI adoption, patent trends captured on Questel, and financial splits from D&B Hoovers and Dow Jones Factiva to frame supplier exposure.

We also reviewed company filings, trade press interviews, SEMI's fab capacity tracker, and key association briefs, which together clarified supply swings and demand pockets. The references listed are illustrative only; many additional sources were consulted for data collection, cross-checks, and clarification.

Market-Sizing & Forecasting

We start with a top-down reconstruction that aligns Eurostat import value and WSTS regional sales with net OEM consumption after channel markdown factors. The output is tested against a sampled bottom-up roll that multiplies distributor volume disclosures by blended selling prices. Key model levers include yearly light vehicle production, industrial robot installs, the serial to parallel mix shift, and process node driven cost decline. A multivariate regression supported by ARIMA smoothing projects the market through 2030, while missing density data points are bridged with moving averages of adjacent brackets.

Data Validation & Update Cycle

Model outputs pass variance checks, scenario stress tests, and a two-level analyst review before sign-off. We refresh each study every twelve months, and analysts issue interim updates when events such as fab outages or major design wins materially alter demand.

Why Mordor's Europe NOR Flash Baseline Is Dependable

Published values often differ because firms vary device scope, pricing sources, and refresh cadence.

Some publishers merge embedded code storage or even NAND into one flash figure; others rely on list prices without distributor discounts, and a few project demand using aggressive automotive unit curves. Mordor keeps a narrowly defined standalone NOR lens, updates annually, and grounds every assumption in live distributor inputs, which tempers extremes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.37 B (2025) | Mordor Intelligence | |

| USD 3.38 B (2025) | Regional Consultancy A | Includes embedded MCU flash and omits channel discounts |

| USD 3.90 B (2025) | Industry Association B | Combines NAND with NOR and uses list price ASPs |

Once scope and pricing filters align, we believe Mordor's figure offers a balanced, transparent baseline that decision makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the 2026 size of Europe NOR Flash market?

The Europe NOR Flash market stands at USD 566.6 million in 2026 and is projected to reach USD 692.7 million by 2031 at a 4.1% CAGR.

Which end-user group leads regional demand?

Automotive is the leading end-user application, with 32.8% share in 2025, and it is also the fastest-growing application at 5.6% CAGR through 2031.

Why is serial NOR more widely used than parallel NOR in Europe?

Serial NOR led with 66.1% share in 2025 because it reduces pin count, lowers PCB complexity, and fits current MCU and controller ecosystems more easily than parallel NOR.

Which interface is growing fastest in new designs?

Quad SPI still held the largest share in 2025 at 49.7%, but Octal and xSPI are growing faster at 5.9% CAGR as software-heavy controllers need more bandwidth.

Which country offers the strongest growth outlook in the region?

Germany remained the largest country market with 37.2% share in 2025, while Italy is forecast to grow the fastest at a 5.4% CAGR through 2031.

What is the main risk for low-density applications?

The biggest pressure on lower-density use cases comes from 1.8 V NAND substitution below 256 Mb in consumer IoT designs where cost per megabit is the main selection factor.

Page last updated on: