Japan NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

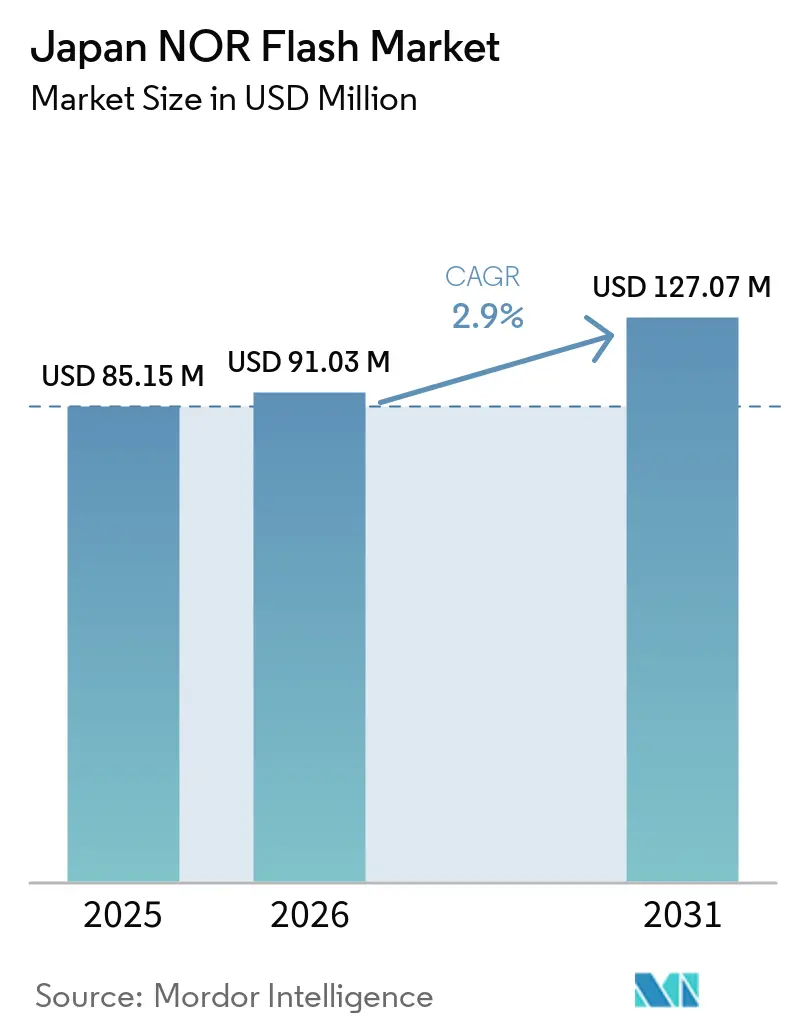

| Base Year Market Size (2025) | USD 85.15 Million |

| Market Size (2026) | USD 91.03 Million |

| Market Size (2031) | USD 127.07 Million |

| Growth Rate (2026 - 2031) | 2.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan NOR Flash Market Analysis by Mordor Intelligence

The Japan NOR Flash market size is expected to increase from USD 91.03 million in 2026 to reach USD 127.07 million by 2031, growing at a CAGR of 2.90% over 2026-2031. A measured expansion is being led by higher-density parts designed into advanced driver-assistance systems, zonal automotive architectures, Open RAN radio units, and edge-AI controllers. Vehicle electrification raises the firmware footprint per car, factories moving toward Society 5.0 need instant-on code storage, and display makers replacing LCD with OLED integrate larger timing-controller firmware. Government support is material: the Ministry of Economy, Trade and Industry (METI) has mapped JPY 9.4 trillion (USD 59 billion) in semiconductor subsidies, favoring suppliers that assemble or fabricate in Japan. At the same time, parallel NOR, Octal, and xSPI interfaces, and sub-1.8 V parts gain share as system designers chase boot-time and power advantages. Competitive intensity stays moderate: Infineon, Renesas, Winbond, and Macronix dominate automotive and industrial designs, while cost-driven niches invite Chinese challengers.

Key Report Takeaways

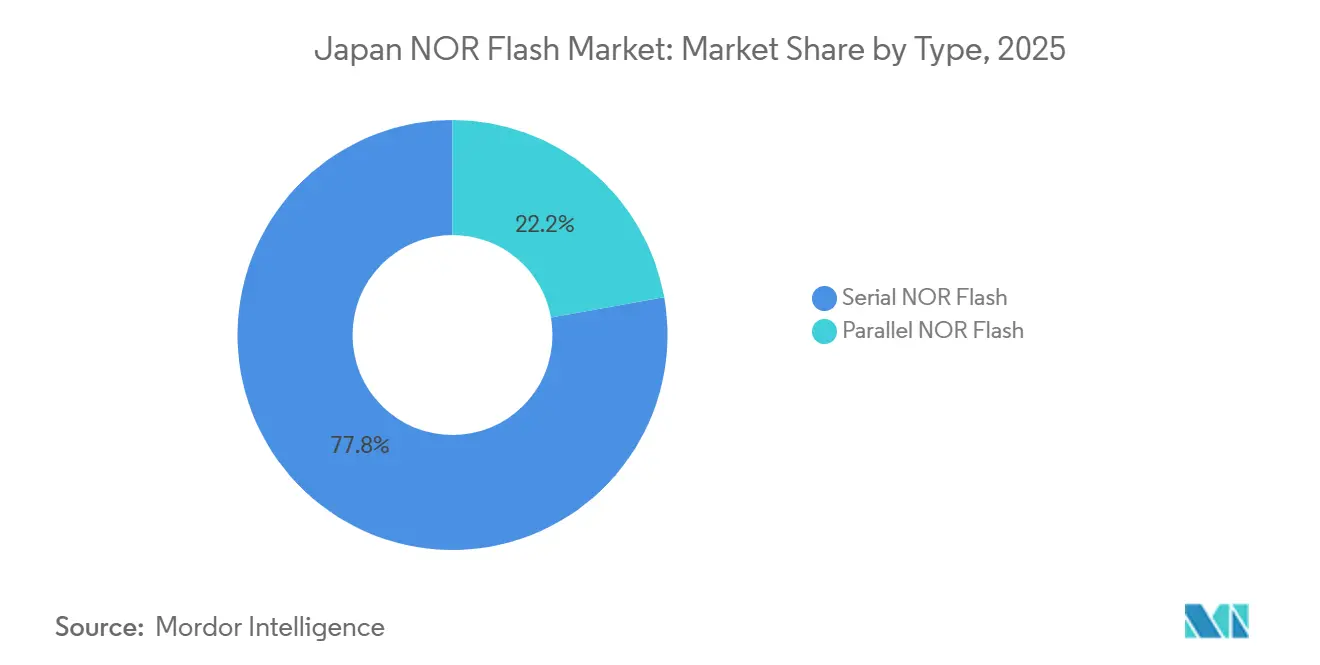

- By NOR flash type, serial NOR Flash led with 77.81% of the Japan NOR Flash market share in 2025, whereas parallel NOR is forecast to expand at a 3.26% CAGR through 2031.

- By interface, Quad SPI captured 49.12% revenue share of the Japan NOR Flash market in 2025, but Octal and xSPI are projected to grow at a 4.62% CAGR through 2031.

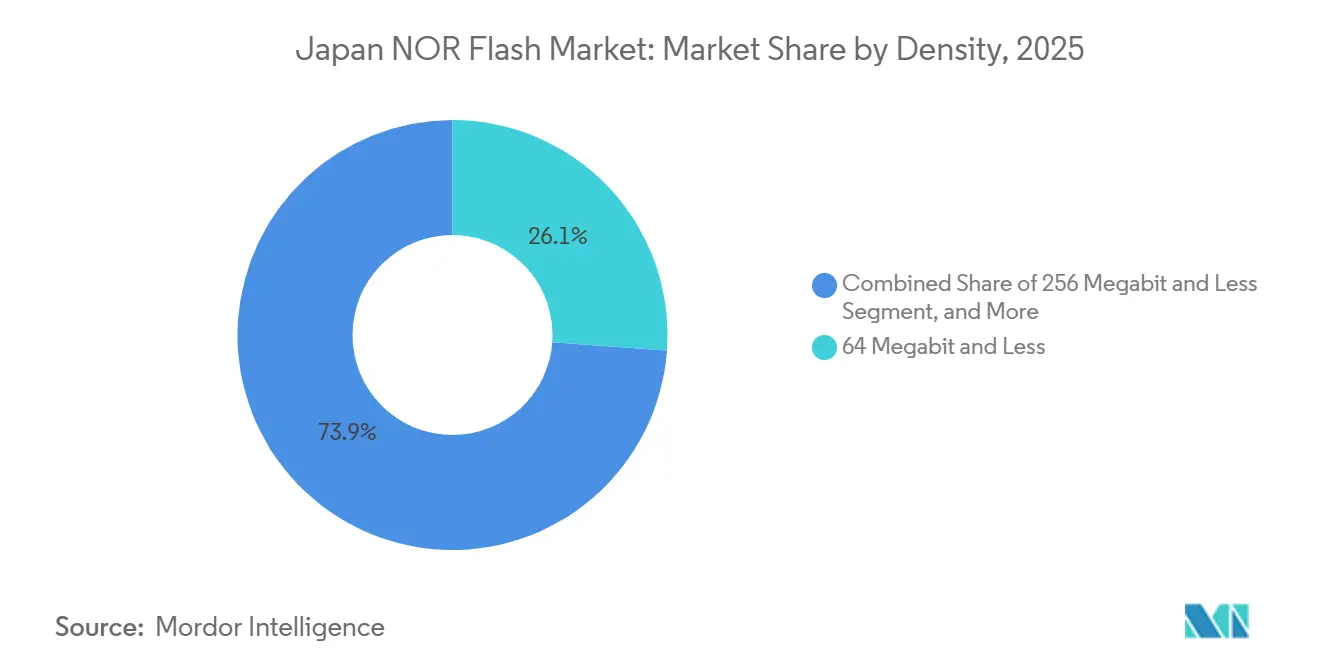

- By density, 64 Mb and less devices held 26.14% share of the Japan NOR Flash market size in 2025, while densities above 256 Mb are set to grow at a 5.93% CAGR to 2031.

- By voltage, the 3 V class dominated with 56.83% share of the Japan NOR Flash market in 2025, and the sub-1.8 V segment is projected to expand at a 4.36% CAGR through 2031.

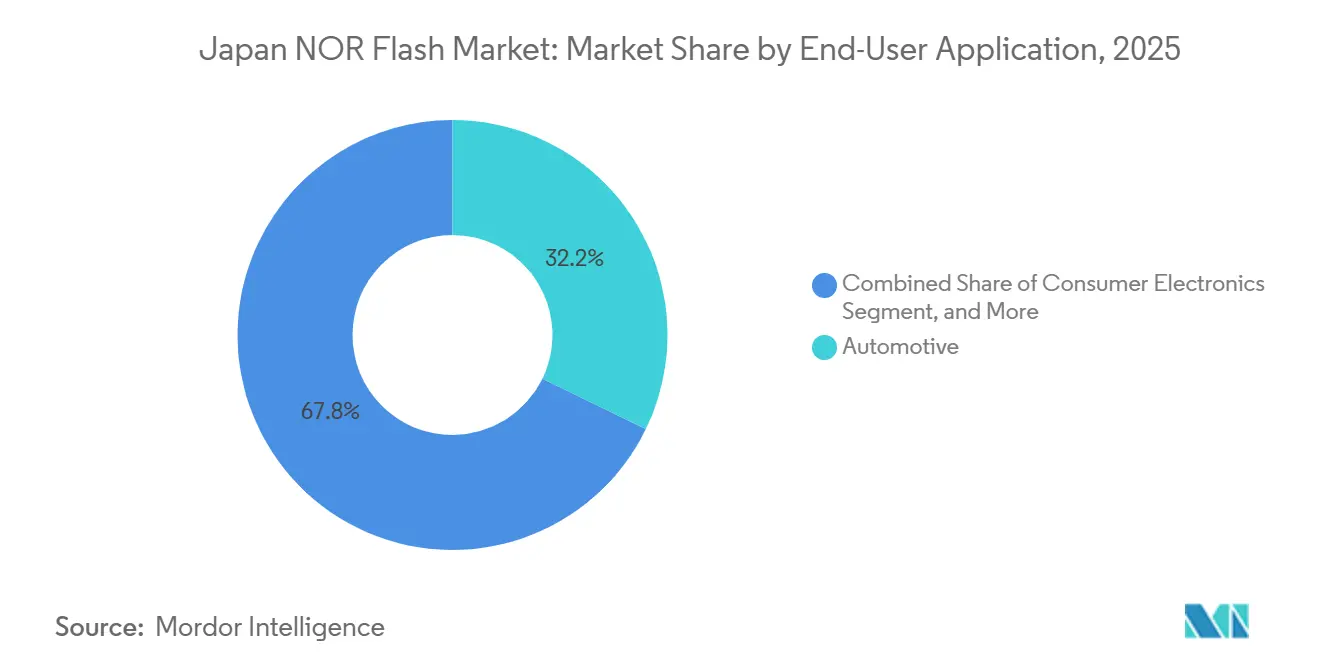

- By end-user application, automotive accounted for 32.22% of the Japan NOR Flash market size in 2025 and is advancing at a 5.85% CAGR through 2031.

- By process technology node, 55 nm accounted for 40.82% of the Japan NOR Flash market size in 2025, while 28 nm and Below is projected to grow at a CAGR of 6.22% in 2031.

- By packaging type, WLCSP / CSP accounted for 38.21% of the Japan NOR Flash market size in 2025, and is advancing at a 3.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

National developments in Japan connect differently with activity unfolding across other parts of the world. In the global nor flash market coverage, Mordor Intelligence integrates these into a single analytical framework.

Japan NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Embedded NOR Flash in Automotive ECUs Driven by Japan's ADAS and EV Growth | +1.20% | Aichi, Hiroshima, Kanagawa clusters | Medium term (2-4 years) |

| Demand for High-Reliability Memory in Industrial Automation Amid Society 5.0 Initiatives | +0.70% | Osaka, Nagoya, Tokyo metro | Long term (≥ 4 years) |

| Transition from LCD to OLED and MicroLED Panels Requiring Higher-Density NOR for Timing Controllers | +0.50% | Nationwide, export spillover | Medium term (2-4 years) |

| Expansion of 5G Base Stations and O-RAN Hardware Requiring Fast Boot-Code Storage | +0.40% | Urban centers, industrial corridors | Short term (≤ 2 years) |

| Localization of Semiconductor Supply Chain Under METI Resilience Programs | +0.30% | Nationwide | Long term (≥ 4 years) |

| Emergence of AI Edge Devices Demanding Instant-On Code Storage in Harsh Environments | +0.30% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Embedded NOR Flash in Automotive ECUs

Japanese vehicle makers are consolidating multiple control domains into zonal architectures that rely on high-density NOR Flash for sub-second boot times and firmware-over-the-air updates. Infineon’s ASIL-D-certified SEMPER family, GigaDevice’s GD25/55 line, and Macronix’s 400 MB/s Octal part all received automotive safety nods, giving tier-1 suppliers certified building blocks.[1]GigaDevice Semiconductor Inc., “GD25/55 NOR Flash Series Secures ASIL-D Certification,” gigadevice.com Growing electric-vehicle output and stricter ADAS mandates enlarge firmware images, so each car now embeds more NOR bits even as ECU counts decline. Subaru’s 2026 platform using Infineon AURIX microcontrollers exemplifies this shift, reinforcing the Japan NOR Flash market’s link to domestic auto production.[2]Macronix International Co., Ltd., “MXSMIO Octal NOR Flash Achieves ASIL-D Compliance,” macronix.com

Demand for High-Reliability Memory in Industrial Automation

Society 5.0 is driving factories toward cyber-physical convergence, with METI allocating JPY 29.5 billion (USD 0.19 billion) for edge-AI semiconductors designed to boot instantly and withstand extreme factory conditions.[3]Infineon Technologies AG, “SEMPER NOR Flash Family Achieves ASIL-D Certification,” infineon.com These advancements are critical as controllers operating on private 5G networks require deterministic start-up capabilities. NOR flash memory, with its execute-in-place feature, eliminates the latency associated with NAND shadowing, making it a preferred choice. To meet these demands, suppliers are qualifying products with wider temperature ranges and enhanced error-correction codes. This alignment of product roadmaps with Japanese automation clusters is fostering innovation and supporting the country's push toward advanced manufacturing.

Transition From LCD to OLED and MicroLED Panels

Display manufacturers transitioning to OLED and MicroLED technologies require larger calibration tables to be stored within timing controllers. As pixel densities increase, firmware sizes are exceeding 128 Mb, driving the demand for NOR Flash memory with capacities greater than 256 Mb. This trend is not confined to domestic markets, as many panels produced in Japan are exported to South Korea and China. The shift toward higher densities benefits suppliers utilizing 28 nm nodes, where the cost per bit is reduced. This development is expected to strengthen the long-term volume outlook for the Japan NOR Flash market, aligning with the growing demand for advanced display technologies.

Expansion of 5G Base Stations and O-RAN Hardware

NEC’s commercial vRAN plan aims to deploy 50,000 base stations by FY 2026, with each radio unit relying on NOR flash memory for secure boot processes. NTT DOCOMO’s open-interface blueprint emphasizes the need for sub-10-second start-up times, a requirement that Quad and Octal NOR flash can meet without the additional DRAM typically required when using NAND. This focus on rapid start-up and secure boot aligns with the densification of cell sites, which significantly increases the number of NOR-equipped boards in use. As a result, the demand for NOR flash memory is expected to rise, providing a near-term boost to the market. NEC and NTT DOCOMO’s initiatives are likely to set a precedent for other operators, further driving adoption and growth in the sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Migration to 28 nm and Below Nodes in Japan's High-Cost Fab Environment | -0.8% | Domestic fabs, supplier partners | Medium term (2-4 years) |

| Growing Adoption of SLC NAND as a Lower-Cost Substitute in Consumer Electronics | -0.5% | Nationwide, consumer export flows | Short term (≤ 2 years) |

| Limited Domestic Lithography Capacity Constraining High-Volume NOR Production | -0.3% | Advanced-node fabs | Long term (≥ 4 years) |

| Yen Volatility Inflating Imported Photoresist and Equipment Costs | -0.2% | Materials-dependent suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Migration to 28 nm and Below Nodes

Moving embedded NOR to advanced nodes reduces cost per bit but demands expensive tooling. SST and UMC’s 28 nm SuperFlash proves technical feasibility, yet most domestic lines still run 40-55 nm because Japan’s fab costs outpace Taiwan and China. Government funds target logic rather than mature NOR, so suppliers must either absorb lower margins or outsource, dampening the pace at which the Japan NOR Flash market accesses cost-efficient capacity.

Growing Adoption of SLC NAND as a Substitute

SLC NAND cells occupy roughly one-quarter the silicon area of NOR, so high-volume gadgets such as set-top boxes and wearables are switching where execute-in-place is unnecessary. Winbond and Lexar publications show comparable endurance to 55-nm NOR, widening the price gap at 1 Gb densities and curbing NOR’s share in cost-sensitive consumer devices.[4]Winbond Electronics Corporation, “Technical Article on Automotive Functional Safety,” winbond.com The substitution risk restrains the Japan NOR Flash industry’s upside beyond automotive and industrial niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serial Leadership, Parallel Persistence

In 2025, serial devices captured a commanding 77.81% share of Japan's NOR Flash market. Their dominance is attributed to their lower pin count and compact footprints, which make them highly suitable for space-constrained applications such as ECUs and IoT boards. These devices benefit from advancements like continued density scaling and the adoption of Octal/xSPI modes, enabling them to achieve throughput levels comparable to parallel NOR without increasing costs. This combination of performance and cost-efficiency has solidified their position as the preferred choice in the market. Furthermore, their ability to meet the evolving demands of modern applications ensures their sustained relevance. Consequently, serial devices are expected to maintain their leadership in Japan's NOR Flash market through 2031.

Meanwhile, parallel NOR continues to serve a loyal customer base in legacy industrial controllers and aerospace systems. These systems rely on microcontrollers specifically designed for 16- or 32-bit buses, making them incompatible with newer technologies without significant modifications. Transitioning these platforms would require extensive PCB redesigns and recertification processes, which are both time-consuming and costly. As a result, users often opt to retain these systems, ensuring the segment's continued presence in the market. Despite its niche status, parallel NOR is projected to achieve a respectable 3.26% growth rate, driven by its critical role in supporting legacy applications. This steady demand underscores its importance in specific industrial and aerospace use cases.

By Interface: High-Bandwidth Octal and xSPI Accelerate

Quad SPI, accounting for 49.12% of revenue, strikes a balance between cost and speed for mainstream designs. Its widespread adoption is driven by its ability to meet the performance requirements of various applications without significantly increasing costs. On the other hand, the Octal/xSPI segment is emerging as the fastest-growing player in Japan's NOR Flash market, boasting a 4.62% CAGR. This growth is attributed to its superior bandwidth capabilities, which exceed 400 MB/s. Such high bandwidth enables multi-core ADAS processors to achieve sub-second ignition readiness, a critical requirement for 2026 vehicle programs. The increasing demand for advanced automotive systems further fuels the adoption of Octal/xSPI interfaces.

Single and Dual SPI cater to price-sensitive wearables and smart-home sensors, which boot infrequently and handle modest data transmissions. These interfaces are particularly suited for applications where cost efficiency is a priority over high performance. Their simplicity and low power consumption make them ideal for devices with limited functionality and intermittent usage. Despite advancements in other interfaces, Single and Dual SPI will continue to thrive in scenarios where controlling the bill of materials takes precedence. Their persistence in the market highlights the ongoing demand for cost-effective solutions in specific use cases. As a result, they remain a vital part of the NOR Flash market ecosystem.

By Density: Firmware Bloat Drives High-Capacity Uptake

In 2025, devices with 64 Mb memory and below accounted for 26.14% of sales, primarily in body electronics and traditional factory nodes. These devices continue to play a significant role in applications where cost efficiency and basic functionality are prioritized. However, advancements in technology have led to increased memory requirements in certain applications. ADAS domain controllers, OLED timing-controllers, and Open RAN radios now demand dual images for failsafe updates, effectively doubling their memory needs. This shift has driven the adoption of higher memory densities, particularly those exceeding 256 Mb. These higher densities are expanding at a rate of 5.93%, significantly contributing to the growth of Japan's NOR Flash market, especially in premium product segments.

While lower memory ranges, like 2 Mb, still cater to ultra-low-cost tags and basic sensors, their applications are gradually evolving. The proliferation of edge-AI technologies is driving a need for more advanced capabilities even in cost-sensitive designs. As a result, these designs are expected to transition to 4 Mb memory to accommodate inference libraries and support AI-driven functionalities. This shift highlights the growing demand for higher memory capacities across various applications. Although the transition may take time, the trend underscores the increasing importance of memory in enabling smarter and more efficient devices. The evolution of these lower ranges reflects the broader technological advancements shaping the NOR Flash market.

By Voltage: Energy Efficiency Favors 1.8 V Class

The 3 V class dominated with 56.83% share in 2025, and the sub-1.8 V segment is projected to expand at a 4.36% CAGR through 2031. While the 3 V class continues to lead in traditional microcontroller ecosystems, every new 28 nm automotive SOC is now shipping with sub-1.2 V I/O. This transition is driving suppliers to adopt lower-voltage NOR technology, which significantly reduces standby current by half. The demand for these advanced NOR solutions is growing as automotive applications increasingly prioritize energy efficiency. In Japan, the market share for NOR Flash parts operating below 1.8 V is steadily increasing, aligning with the adoption of these chips. This growth is further supported by METI grants, which actively promote the development and use of energy-efficient semiconductors. These factors collectively highlight the ongoing shift towards lower-voltage solutions in the automotive sector.

Wide-voltage components, ranging from 1.65 to 3.6 V, remain a preferred choice in mixed-signal boards due to their versatility. These components are particularly advantageous in environments where peripherals operate across varying voltage ranges. By accommodating a broad spectrum of voltage requirements, they simplify the integration process and reduce the need for additional level-shifters. This capability makes them a practical solution for designers working on complex mixed-signal systems. Furthermore, their ability to support multiple voltage levels ensures compatibility with diverse applications. As a result, wide-voltage parts continue to hold a significant position in the semiconductor market.

By End-User Application: Automotive Outpaces Overall Market

In 2025, automotive applications accounted for 32.22% of the market value and are projected to grow at a rate of 5.85%, driving the expansion of the overall Japan NOR Flash market. This growth is attributed to the increasing adoption of consolidated domain architectures in vehicles. These architectures use fewer controllers but require each controller to store larger firmware files, leading to higher data storage needs. As a result, the trend of increasing bits per vehicle continues to rise. The automotive sector's demand for NOR Flash is further fueled by advancements in vehicle technology and the integration of more sophisticated electronic systems.

Communication infrastructure experiences a temporary boost from the Open RAN rollout, set to continue through 2026. This rollout is expected to enhance network flexibility and efficiency, driving short-term demand for NOR Flash in the sector. However, the consumer electronics sector remains stagnant, primarily due to the increasing substitution of NOR Flash with NAND technology. This shift impacts the growth potential of NOR Flash in consumer devices. On the other hand, industrial automation demonstrates resilience under the Society 5.0 capital expenditure initiatives. The sector's demand for high-reliability NOR Flash is particularly strong in robotics and vision systems, which require robust and dependable memory solutions to support advanced automation processes.

By Process Technology Node: 28 nm and Below Edges Forward

Production on 55 nm accounted for 40.82% of revenue in 2025 due to its established reliability in automotive applications. This node remains a preferred choice for applications requiring proven performance and durability. However, parts fabricated at 28 nm and below are witnessing the strongest growth, with a CAGR of 6.22%. These advanced nodes reduce the cost per bit and enable capacities exceeding 512 Mb, making them highly competitive. To meet growing demand, manufacturers are outsourcing production to cost-efficient foundries abroad. This trend is expected to continue until domestic production capacity is sufficiently scaled.

Legacy 90 nm production lines continue to cater to niche markets such as aerospace and medical applications. These sectors prioritize multi-decade life cycles and reliability over density, ensuring the survival of small production volumes. Aerospace applications often require components with extended operational lifespans, while medical devices demand high reliability for critical operations. Despite their limited scale, these legacy nodes remain essential for addressing specific market needs. As a result, they maintain relevance in industries where durability and long-term performance outweigh the need for higher densities.

By Packaging Type: Miniaturization Favors WLCSP/CSP

Wafer-level and chip-scale packaging accounted for 38.21% of the market share and are projected to grow at a rate of 3.91% during the forecast period. This growth is primarily driven by the increasing adoption of zonal controllers in the automotive sector, where reducing board footprints is a critical requirement. These packaging solutions offer compact designs and enhanced performance, making them ideal for advanced automotive applications. Additionally, their ability to support high-density integration aligns with the evolving needs of modern vehicles. As automakers continue to innovate, the demand for wafer-level and chip-scale packaging is expected to rise steadily.

QFN (Quad Flat No-lead) and SOIC (Small Outline Integrated Circuit) packaging remain highly favored in industrial applications due to their ease of inspection and rework. These features are particularly valued in environments where reliability and maintenance are crucial. On the other hand, BGA (Ball Grid Array) and FBGA (Fine-pitch Ball Grid Array) packaging are widely used in high-density automotive domain boards. Their superior thermal management capabilities make them indispensable for applications requiring efficient heat dissipation. As automotive systems become more complex, the relevance of BGA and FBGA packaging is expected to grow, ensuring optimal performance and durability.

Geography Analysis

In Japan, the automotive hubs of Aichi, Hiroshima, and Kanagawa dominate NOR Flash consumption, hosting a confluence of OEMs, tier-1 suppliers, and microcontroller vendors. These regions serve as critical centers for the automotive supply chain, where the demand for NOR Flash is driven by advanced automotive applications. Highlighting a push for localization, METI's subsidy map reveals a hefty JPY 9.4 trillion (USD 59 billion) commitment to bolster domestic semiconductor initiatives. This investment aligns with Japan's strategy to reduce reliance on foreign suppliers and strengthen its semiconductor ecosystem. The localization trend particularly benefits firms that conduct assembly or testing within Japan's borders, ensuring greater control over production and supply chain stability.

Hiroshima, not only a site for Micron's DRAM expansion, but is also home to photoresist suppliers catering to every global EUV fab, granting Japan a strategic edge in materials. This dual role positions Hiroshima as a key player in both memory production and semiconductor materials supply. However, Japan's lithography landscape is somewhat limited, which poses challenges for the domestic production of advanced NOR Flash. Canon's upcoming 2025 nanoimprint line focuses on advanced packaging, leaving embedded NORs underserved. Consequently, a significant portion of high-density NORs for Japanese automotive needs is still produced in Taiwan or China. This reliance on foreign production exposes Japan to risks such as yen fluctuations and export-control challenges, which could disrupt the supply chain.

After shipping disruptions in the Strait of Hormuz in April 2026, currency volatility led to a spike in imported resist prices, highlighting the ripple effects of global chokepoints on local component costs. These disruptions underscored the vulnerability of Japan's semiconductor supply chain to external factors. In response, policymakers established a JPY 150 billion (USD 0.94 billion) equity fund in FY 2026, aimed at fostering domestic production of low-power memories. This initiative reflects the government's recognition of the strategic importance of the NOR Flash market for national resilience. By investing in local production capabilities, Japan aims to mitigate risks associated with global supply chain dependencies and enhance its technological self-sufficiency.

Mordor Intelligence's coverage of the nor flash market extends across other regions including Europe and Asia, while country-specific intelligence is also available for China, India, United Kingdom, Mexico, France, United States, and Italy, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The Japan NOR Flash market competition is moderately fragmented. Infineon, Renesas, Winbond, and Macronix hold a dominant position in the Japan NOR Flash market, driven by early successes in automotive design and long-standing production commitments. These companies have solidified their market presence by consistently delivering products tailored to automotive requirements. Regular updates to their roadmaps, including advancements like higher densities and ASIL-D safety packages, ensure their competitiveness. Their ability to secure renewal contracts through 2031 underscores their strategic focus on long-term market engagement. Meanwhile, new Chinese entrants, despite offering competitive pricing and achieving automotive certifications, face hurdles such as building brand credibility, establishing local support infrastructure, and navigating extended validation processes, which slow their market entry.

Innovation in the Japan NOR Flash market is centered on advancements in interface technology and security enhancements. Macronix has launched its ArmorBoot technology, integrating root-of-trust engines to bolster security. Winbond has achieved ASIL-D compliance with its Octal components, meeting the rigorous safety standards of the automotive industry. Renesas streamlines procurement by combining NOR Flash with its microcontrollers, offering a more integrated and efficient solution. These technological advancements not only address current market needs but also reinforce the leadership position of these companies. By prioritizing innovation, they continue to maintain a competitive advantage in a rapidly evolving industry.

Smaller fabless companies, such as Integrated Silicon Solution, are capitalizing on niche opportunities within the market. These firms focus on segments where older densities or extended product availability take precedence over high capacity. Additionally, emerging opportunities in AI edge devices and Open RAN boards are reshaping the market landscape. These applications emphasize boot speed and adaptability over established relationships, creating new growth avenues. As these segments are less constrained by traditional market dynamics, they provide smaller players with opportunities to innovate and compete effectively. This diversification underscores the evolving nature of the NOR Flash market and highlights the potential for growth in untapped areas.

Japan NOR Flash Industry Leaders

Infineon Technologies AG

Winbond Electronics Corporation

Renesas Electronics Corporation

Macronix International Co., Ltd.

Micron Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: METI issued a manufacturing-base strengthening report outlining subsidy extensions for advanced semiconductor sites, reinforcing localization momentum.

- March 2026: Infineon and Subaru partnered to embed AURIX microcontrollers in next-generation EVs, increasing per-vehicle NOR content.

- February 2026: TSMC confirmed a 3 nm logic upgrade at Kumamoto, without embedded NOR plans, keeping local customers reliant on offshore supply.

- January 2026: Macronix gained ASIL-D compliance for its MXSMIO Octal NOR, enabling 400 MB/s boot for zonal automotive ECUs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Japan NOR flash memory market as manufacturer-level revenue from serial and parallel NOR flash integrated circuits that are fabricated or finally sold into devices assembled within Japan. These ICs serve code storage roles where rapid read latency, execute-in-place, and high endurance are critical across consumer gadgets, 5Gradios, automotive ECUs, and factory controllers.

Scope Exclusion: NAND flash, DRAM, phase-change or ReRAM devices, and downstream module or board-level assembling services are outside our numbers.

Segmentation Overview

- By NOR Flash Type (Value)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- 4 Megabit and Less (Greater than 2 Mb)

- 8 Megabit and Less (Greater than 4 Mb)

- 16 Megabit and Less (Greater than 8 Mb)

- 32 Megabit and Less (Greater than 16 Mb)

- 64 Megabit and Less (Greater than 32 Mb)

- 128 Megabit and Less (Greater than 64 Mb)

- 256 Megabit and Less (Greater than 128 Mb)

- Greater than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Sub-1.8 V Class (1.2 V and Similar)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication Infrastructure

- Automotive

- Industrial

- Other Applications

- By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

Detailed Research Methodology and Data Validation

Primary Research

To validate desk findings, we interviewed fabless chip designers in Yokohama, OSAT managers, Tier-1 ECU firmware architects, and procurement leads at G base-station OEMs across Kanto, Kansai, and Kyushu. Their insights on density migration toward 128-Mbit parts, SPI adoption in 5Gradios, and AEC-Q100 qualification hurdles refined usage ratios and price curves that desk sources could only hint at.

Desk Research

Analysts first compiled publicly available anchors such as METI's electronic parts production index, Japan Customs HS-8542 export files, JEITA shipment tallies, and WSTS unit splits, which help us translate wafer output to packaged die flow. Complementary context came from Bank of Japan price data, patent landscaping drawn through Questel, and financial disclosures in 10-Ks, Yuho filings, and investor decks of leading memory suppliers. Where visibility was limited, D&B Hoovers and Dow Jones Factiva fed us company-level revenue clues. This list is illustrative; numerous additional databases and press archives were tapped to cross-check figures and narratives.

Market-Sizing & Forecasting

Our model begins with a top-down reconstruction that scales domestic MCU, wireless and automotive production volumes by NOR penetration rates, then applies blended ASPs derived from customs and channel checks. Select bottom-up cross-tests, supplier roll-ups and sampled ASP × unit calculations flag gaps before adjustments. Key drivers modeled include: 1) 5Gbase-station roll-out pace, 2) EV and ADAS vehicle build counts, 3) average die density uplift, 4) yen-to-USD shifts affecting local ASPs, and 5) fab capacity additions at 55 nm and below. Forecasts rely on a multivariate regression layered over ARIMA trend extensions, with coefficient ranges validated through expert consensus interviews.

Data Validation & Update Cycle

Outputs undergo anomaly scans against independent metrics, peer review by a senior analyst panel, and finally a pre-publication refresh. Mordor Intelligence revisits each data set annually, triggering interim updates when major capacity ramps, policy moves, or price shocks emerge.

Why Mordor's Japan NOR Flash Baseline Earns Trust

Published values often differ because firms pick dissimilar product mixes, geographic cuts, and pricing paths. Our disciplined, Japan-only scope and annual refresh cadence limit those distortions.

Key gap drivers include others bundling NAND with NOR, reporting global revenues, or layering consultancy services into market value, whereas our figure captures pure NOR silicon shipped within Japan at factory gate pricing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 275.78 M (2025) | Mordor Intelligence | - |

| USD 3.07 B (2024) | Regional Consultancy A | Combines NAND and NOR for Japan, inflating total addressable market |

| USD 3.22 B (2025) | Global Consultancy B | Reports global NOR revenues, not country-specific view |

| USD 5.27 B (2025) | Industry Journal C | Adds customization services and applies optimistic price escalation |

Taken together, the comparison shows that when variables are tightly aligned to Japan-only silicon sales, Mordor's measured baseline offers decision-makers a balanced, reproducible starting point backed by transparent steps and continuous validation.

Key Questions Answered in the Report

What is the current Japan NOR Flash market size and how fast is it growing?

The Japan NOR Flash market size is projected at USD 91.03 million in 2026 and is forecast to reach USD 127.07 million by 2031 at a 2.90% CAGR, according to Mordor Intelligence.

Which end-user segment is expanding the quickest?

Automotive applications are growing the fastest at a 5.85% CAGR as electric vehicle production and ADAS penetration raise firmware storage per car.

Why are Octal and xSPI interfaces gaining share?

Next-generation automotive domain controllers and Open RAN radio units require over 400 MB/s read speeds for sub-second boot, making Octal and xSPI the preferred interfaces.

How is government policy influencing supply?

METI has pledged JPY 9.4 trillion (USD 59 billion) in semiconductor subsidies and created equity funds to localize memory production, favoring suppliers with Japanese fabs or assembly.

What technology node leads production today?

The 55 nm node holds the largest revenue share because of proven automotive reliability, but 28 nm and below parts are the fastest-growing as suppliers chase per-bit cost savings.

Which competitive factor most limits new entrants?

Automotive qualification cycles of five or more years and the need for local technical support make it difficult for new vendors to displace incumbent suppliers.

Page last updated on: