Italy NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

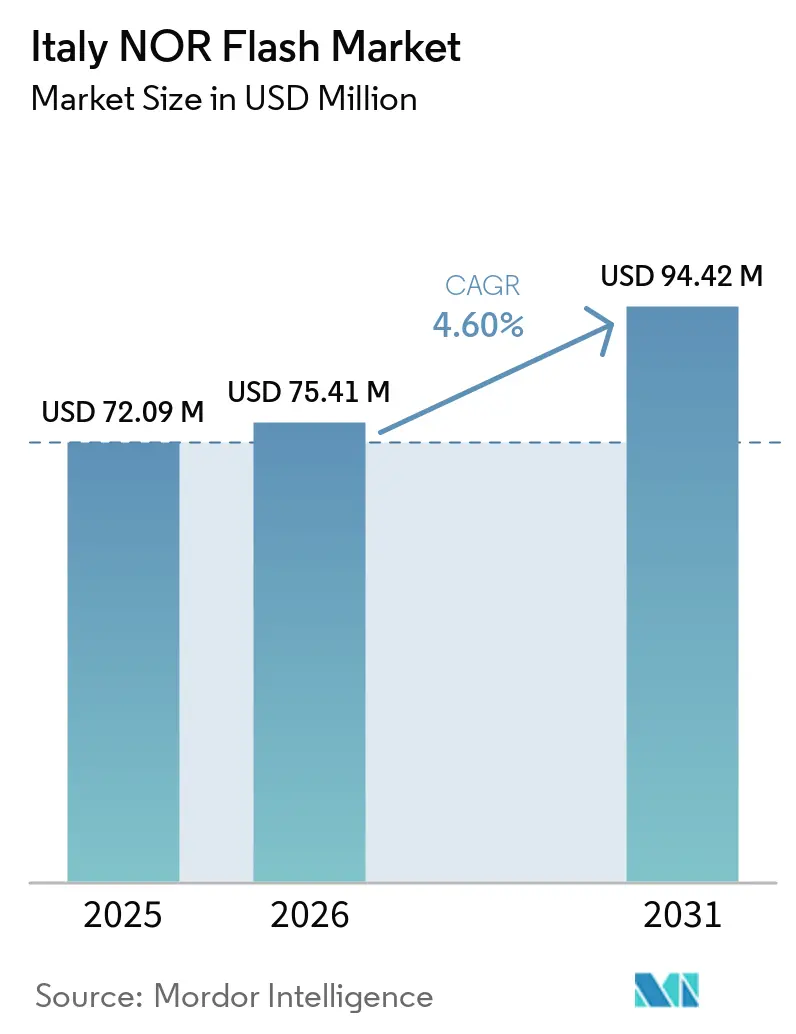

| Base Year Market Size (2025) | USD 72.09 Million |

| Market Size (2026) | USD 75.41 Million |

| Market Size (2031) | USD 94.42 Million |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

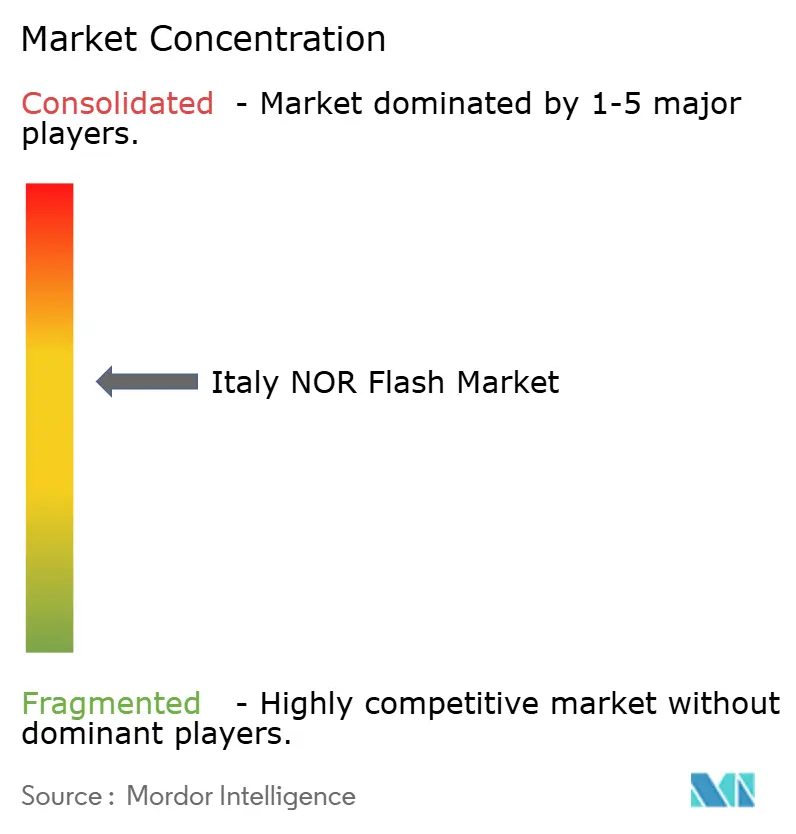

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy NOR Flash Market Analysis by Mordor Intelligence

The Italy NOR Flash market size is expected to increase from USD 72.09 million in 2025 to USD 75.41 million in 2026 and reach USD 94.42 million by 2031, growing at a CAGR of 4.60% over 2026-2031. Robust electronics demand from premium automotive platforms, utility smart-meter modernization, and government-backed factory-automation programs keep the growth curve stable even though the country lacks a domestic wafer-fabrication line. Automotive original-equipment manufacturers (OEMs) in Turin, Modena, and Bologna anchor the largest end-use cluster, while Lombardy and Veneto continue to absorb Serial NOR devices for energy-management gateways. Interface migration toward Octal and xSPI variants gains momentum as over-the-air (OTA) firmware updates become mandatory across vehicle types. Density needs also rise: ADAS controllers are moving from 128 Megabit to 256 Megabit nodes to host neural-network inference models and secure-boot partitions. At the same time, supplier consolidation remains moderate, with four brands accounting for roughly 60-65% of local revenue, maintaining pricing discipline while still leaving room for niche entrants.

Key Report Takeaways

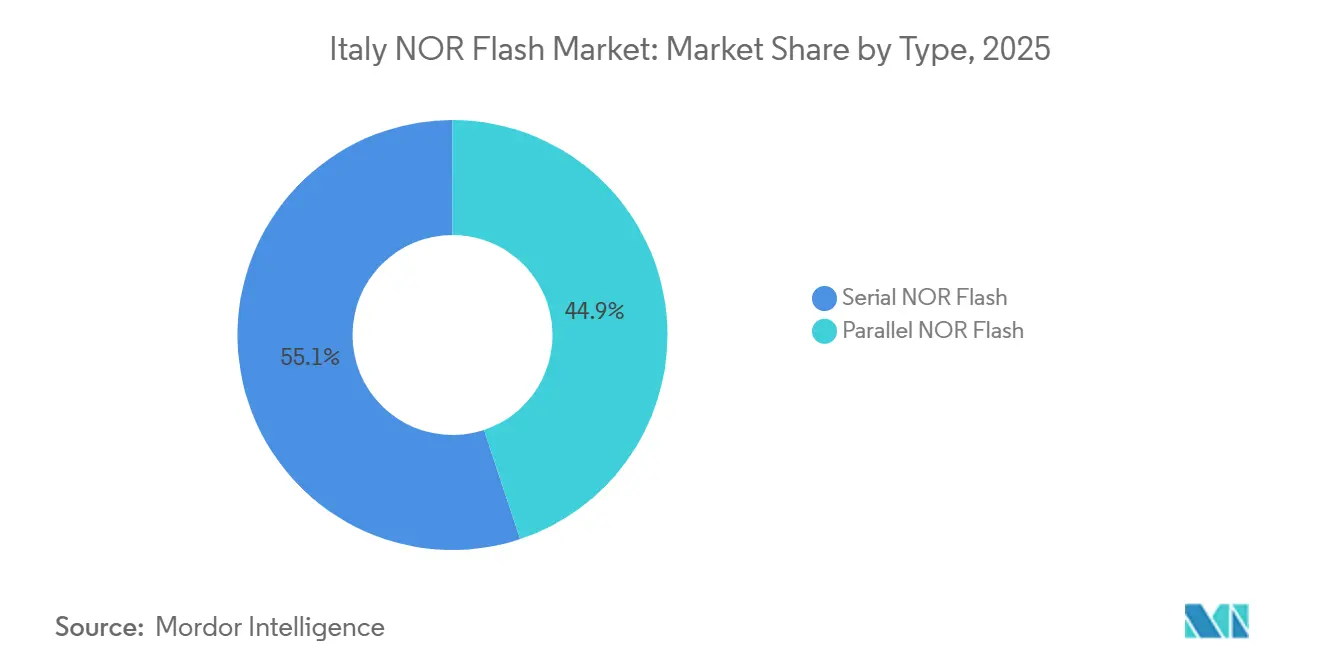

- By type, Serial NOR Flash held 55.10% of the 2025 revenue share in Italy NOR flash market, while Parallel NOR is on track for a 7.40% CAGR through 2031, the fastest growth among device formats.

- By interface, Quad SPI commanded 40.90% share of the Italy NOR flash market in 2025, whereas the Octal and xSPI category is forecast to expand at a 9.60% CAGR, the quickest among connectivity options.

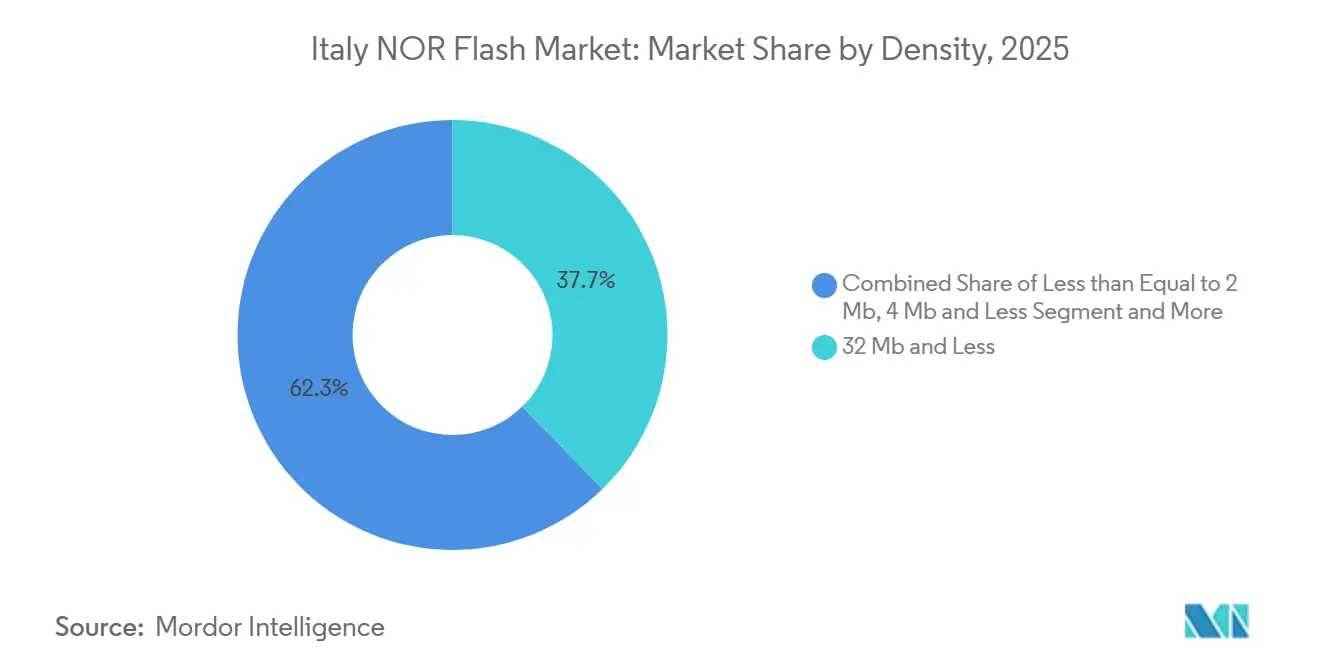

- By density, the 32-Megabit-and-smaller group led with 37.70% of volume of the Italy NOR flash market in 2025; however, the 256 Megabit class is projected to grow at 7.20% annually, the highest rate within this segmentation.

- By voltage, legacy 3 Volt designs dominated with 56.40% of 2025 shipments of the Italy NOR flash market, yet the 1.8 Volt class is poised for an 8.70% CAGR, marking the most rapid rise among voltage groups.

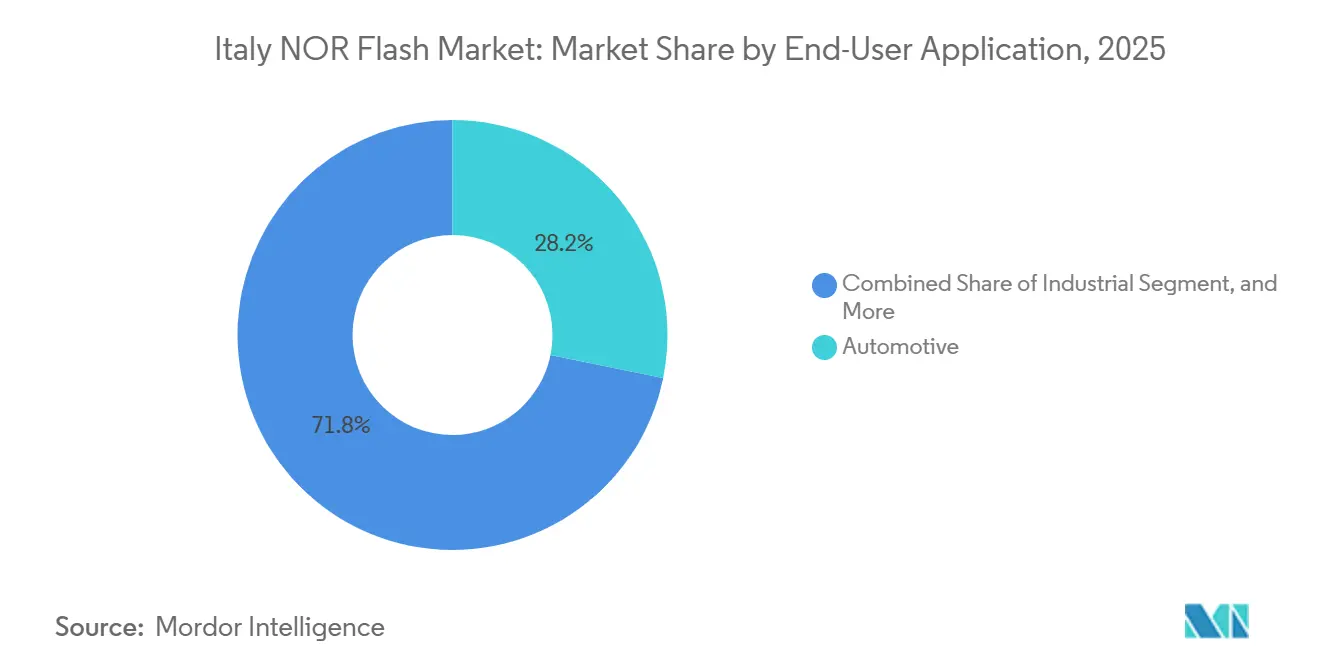

- By end-user application, automotive captured 28.20% share in 2025 of the Italy NOR flash market, but industrial deployments are forecast to log the strongest 7.60% CAGR during 2026-2031.

- By process node, 65-nanometer technology supplied 33.60% of 2025 units of the Italy NOR flash market, while 28-nanometer-and-smaller nodes are set for an 8.30% CAGR, the steepest climb among lithography options.

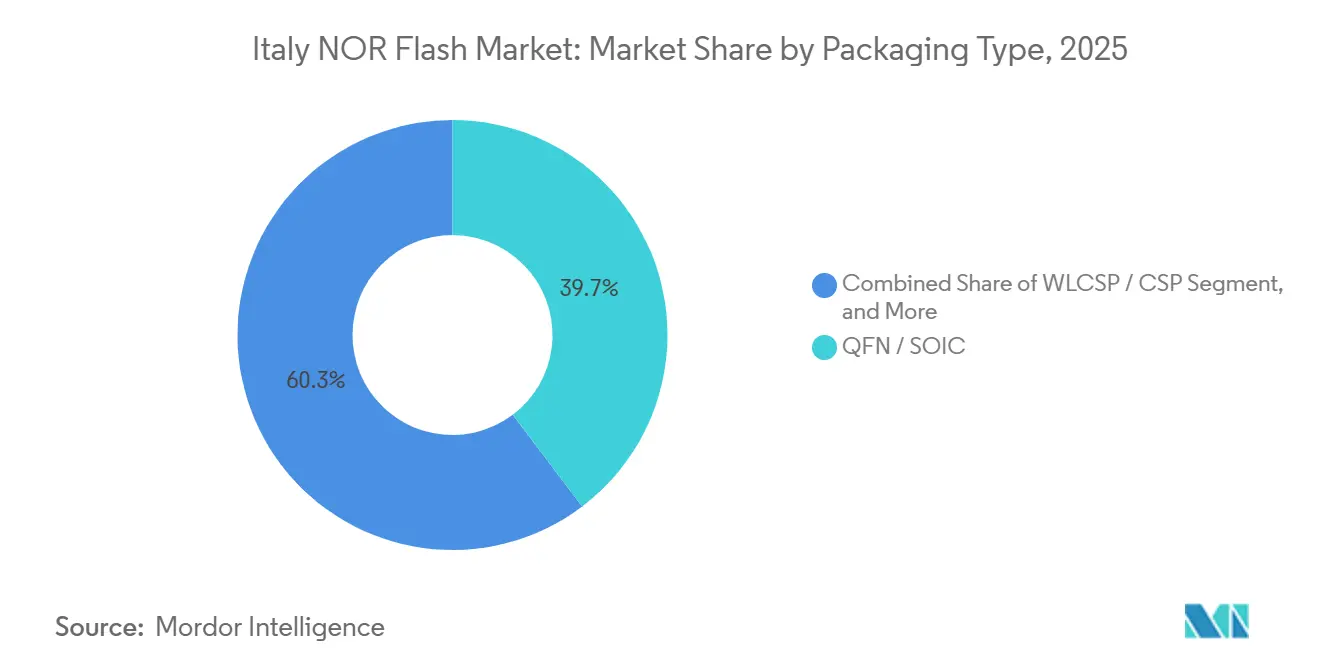

- By packaging type, Quad Flat No-lead and SOIC accounted for 39.70% of 2025 demand of the Italy NOR flash market, whereas Wafer-Level Chip-Scale Packages will advance at a 6.60% CAGR, the fastest among package styles.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Figures recorded within Italy feed into a worldwide estimate while studying the global industry. Mordor Intelligence's nor flash market size captures this aggregation.

Italy NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of ADAS and Autonomous Platforms in Italian Automotive OEMs | +1.8% | Turin, Modena, Bologna | Medium term (2-4 years) |

| Growing Deployment of Smart Energy Meters by Italian Utilities | +1.2% | National, especially Lombardy, Lazio, Emilia-Romagna | Medium term (2-4 years) |

| Government Incentives for Industrial IoT under Transizione 4.0 | +1.0% | Nationwide, strongest in Veneto, Lombardy, Emilia-Romagna | Short term (≤ 2 years) |

| Rising Demand for Secure OTA Updates in Connected Two-Wheelers | +0.6% | Bologna, Pontedera, Milan | Medium term (2-4 years) |

| Transition of Italian Broadcasting Infrastructure to DVB-T2 Firmware Upgrades | +0.3% | National | Short term (≤ 2 years) |

| Miniaturization Push in Italian Medical Device Start-Ups and Wearables | +0.2% | Milan, Bologna, Rome | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of ADAS and Autonomous Platforms in Italian Automotive OEMs

Stellantis joined the AI4I consortium in 2026, locking in co-development paths that embed NOR Flash into next-generation zonal controllers.[1]Stellantis, “Corporate Communications,” stellantis.com The group already demonstrated Level 3 capabilities in late 2025 and earmarked USD 10 billion in semiconductor sourcing to 2030, including 256 Megabit-plus devices for deterministic boot. Ferrari and Lamborghini follow similar roadmaps, integrating predictive maintenance stacks that also demand secure, instant-on storage. Parallel NOR Flash thus gains favor because its fixed-latency read path satisfies ISO 26262 ASIL-D worst-case execution targets. The shift to octal 200 MHz buses delivers 400 MB/s throughput, reducing OTA downtime from hours to minutes and enhancing dealer service economics.

Growing Deployment of Smart Energy Meters by Italian Utilities

Enel’s Open Meter II program, backed by a EUR 500 million (USD 540 million) European Investment Bank loan, targets 41 million endpoints with automotive-grade Serial NOR inside each meter.[2]Enel, “Strategic Plan 2026-2028,” enel.com A2A’s 1.3 million-unit rollout in Milan and Brescia follows the same architecture. Second-generation meters operate from −25 °C to +70 °C and require 100,000 program-erase cycles plus 20-year retention, specifications aligned with AEC-Q100 Grade 1 Flash. As the regulator ARERA pushes the remaining meters toward a 2027 deadline, demand concentrates in Lombardy, Lazio, and Emilia-Romagna. Suppliers able to certify wide-temperature, low-pin-count devices gain a durable advantage.

Government Incentives for Industrial IoT Under Transizione 4.0

The tax-credit pool of EUR 2.2 billion (USD 2.37 billion) expired in mid-2025, yet the 2026 budget replaced it with iperammortamento that lets firms deduct 120-130% of qualified hardware from taxable income. Edge gateways, PLCs, and sensor nodes specified by small and medium manufacturers now adopt 8-64 Megabit Serial NOR for boot and configuration storage. However, talent shortages in the Lecco mechatronics hub, vacancy rates hit 8.5%, and slow full utilization despite available capital.[3]National Industry 4.0, “Transizione 4.0 Tax Incentives,” transizione40.it Even so, uptake remains brisk because larger firms in Veneto and Lombardy can capture the depreciation benefit quickly.

Rising Demand for Secure OTA Updates in Connected Two-Wheelers

Ducati’s Desmo450 MX introduced predictive maintenance via the X-Link app in April 2026, forcing encrypted firmware storage inside 1.8 Volt NOR Flash to comply with the EU’s Data Act.[4]Ducati, “Desmo450 MX Connectivity Features,” ducati.com Piaggio, which controls 18% of Europe’s scooter segment, also migrated to hardware-based secure boot to satisfy UN R155 cybersecurity rules. Compared with 3 Volt parts, 1.8 Volt and emerging 1.2 Volt Flash cut energy draw by up to 70%, critical for motorcycles with limited alternator output. Suppliers integrating Physical Unclonable Functions inside the memory array position themselves for rapid design wins as two-wheeler OEMs scale OTA programs across model lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Front-End Fab Costs Versus Limited Domestic Wafer Capacity | -1.4% | National | Long term (≥ 4 years) |

| Stringent EU REACH and RoHS Compliance Raising Qualification Costs | -1.1% | EU-wide, acute for Italian automotive and industrial OEMs | Short term (≤ 2 years) |

| Skill Shortages in Embedded NOR Flash Design in Italian SMEs | -0.5% | Lombardy, Veneto, Emilia-Romagna | Medium term (2-4 years) |

| Euro Depreciation Volatility Affecting Memory Component Pricing | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Front-End Fab Costs Versus Limited Domestic Wafer Capacity

Italy depends on Asian foundries whose allocation rules favor higher-volume customers. European fabs sit at a 20-30% cost disadvantage, and the EU NanoIC pilot line remains focused on 5 nm nodes, not used for NOR Flash. The cancellation of Intel’s Magdeburg megafab further underscores regional fragility, while STMicroelectronics’ EUR 5 billion (USD 5.40 billion) SiC campus focuses on power devices rather than memory. Consequently, local integrators face longer lead times and higher purchasing costs, eroding competitiveness in export-oriented machinery.

Stringent EU REACH and RoHS Compliance Raising Qualification Costs

Comprehensive RoHS testing for one NOR Flash part can exceed USD 1,000, and failure penalties run to EUR 100,000 (USD 108,000), exposing small distributors to existential risk.[5]European Commission, “European Chips Act State-Aid Approvals,” digital-strategy.ec.europa.eu July 2026 marks the end of several key exemptions, forcing requalification of legacy automotive modules. Simultaneous AEC-Q100 and chemical compliance inflates time-to-market by up to nine months. Suppliers with centralized documentation portals and pre-certified portfolios enjoy a clear sales advantage, yet overall compliance burdens still dampen near-term demand elasticity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Parallel NOR Emerges for Safety-Critical Boot Paths

Parallel NOR accounted for a smaller share of the Italian NOR Flash market in 2025, yet its 7.40% CAGR underscores rising demand for advanced driver assistance systems. Automotive domain controllers cannot tolerate boot latency above 100 ms, so deterministic read performance takes precedence over pin-count savings. Infineon and Winbond both released AEC-Q100 Grade 1 Parallel devices that sustain instant-on operation at 150 °C junction temperatures. Serial NOR remains indispensable for compact telematics and wearables, but its market growth rate lags because safety-critical modules are moving to wider buses.

Parallel NOR also benefits from execute-in-place firmware execution, reducing cost by eliminating external DRAM in safety islands. As Stellantis consolidates 30-plus control units into zonal architectures, each node requires dual-redundant Parallel NOR banks for A/B firmware images. Conversely, the SKU diversity of Serial NOR ensures it will keep at least half of total unit shipments, covering industrial sensors and smart meters that value low cost per pin and streamlined PCB routing.

By Interface: Octal and xSPI Raise the Bandwidth Ceiling

Quad SPI owns the largest slice of the Italian NOR Flash market share, yet its 40.90% position is set to erode as Octal and xSPI climb at 9.60% CAGR. GigaDevice’s GD25NX line pushes 400 MB/s read speeds at 200 MHz, a fivefold leap over legacy Dual SPI. Italian OEMs adopt these parts to slash OTA update time and cellular data-plan costs. Stellantis benchmarks show a 2 GB firmware package downloading in under six minutes when hosted on xSPI Flash compared with 30 minutes on Quad SPI.

Standard and Dual SPI continue in set-top boxes and industrial controllers with annual code revisions. However, as UN R155 mandates secure update pipelines, the xSPI protocol’s 8-bit DDR signaling plus side-band pins for authentication become persuasive features. Microcontroller vendors such as Renesas now ship reference designs pairing automotive MCUs with on-board Octal Flash pre-loaded with secure-boot loaders, smoothing adoption across Tier 1 suppliers.

By Density: 256 Megabit Class Bridges Mainstream and High-End Needs

Italy NOR Flash market size data show 32 Megabit-and-smaller devices dominate volume, especially in smart meters and industrial gateways. Still, the 256 Megabit bracket advances 7.20% per year as ADAS stacks swell. Infineon’s Semper family offers 25-year data retention or 1 million cycle endurance on the same die, de-risking long field life. Tier 1 suppliers now dual-source 256 Megabit xSPI Flash for both infotainment and safety islands, reducing qualification overhead.

As data rates rise from 512 Megabits to 1 Gigabit, discussions intensify over the cost-per-bit between NOR and NAND. NOR technology continues to hold its ground due to its ability to meet the stringent requirements of random-read stability and execute-in-place functionalities, which are critical in ASIL-D environments. These features make NOR a reliable choice for applications where safety and performance cannot be compromised. Italian OEMs have strategically adopted a dual-storage approach, securing the primary boot process in NOR to ensure deterministic and reliable start-up. Meanwhile, they utilize NAND for storing bulk map data, capitalizing on its high-capacity storage capabilities. This combination allows manufacturers to balance performance, cost, and storage efficiency effectively.

By Voltage: 1.8 Volt Designs Align With Battery-Powered Platforms

Legacy 3 Volt parts ruled in 2025 thanks to entrenched automotive and smart-meter footprints. The 1.8 Volt class, however, heads toward an 8.70% CAGR as Piaggio, Ducati, and wearable start-ups converge on lower supply rails. GigaDevice’s GD25UF family cuts read power by half while staying within 1.14-1.26 volts for the I/O ring, eliminating external regulators in many designs. Italian industrial IoT nodes leveraging LoRaWAN and NB-IoT modems also benefit from longer battery life when firmware storage drops to sub-2 Volt operation.

Wide-voltage 1.65-3.6 Volt parts remain popular for modules that face brown-out events during engine crank. Developers appreciate one part number covering multiple rail options, simplifying BOM management. Over time, though, more OEMs will migrate to single-rail 1.8 Volt or 1.2 Volt boards to trim power-distribution losses in clustered electronic architectures.

By End-User Application: Industrial Surges Under Transizione 4.0 Incentives

Automotive unsurprisingly led the 2025 leaderboard with 28.20% of value, yet factory automation emerges as the growth engine through 2031. Tax-advantaged machinery purchases under Transizione 4.0 are driving significant upgrades in programmable logic controllers (PLCs), which increasingly incorporate 8-64 Megabit Serial NOR for secure boot and configuration retention. This trend is particularly evident in Veneto’s packaging-machinery firms and Lombardy’s textile-automation shops, both of which report double-digit growth in orders for panel PCs and gateways featuring advanced Flash technology. These developments highlight the growing demand for reliable and secure memory solutions in industrial automation. As factory automation continues to expand, it is expected to play a pivotal role in shaping the future of the NOR Flash market.

Smart-meter deployments are also contributing steady volume to the NOR Flash market, although their revenue impact is relatively smaller due to the lower average density of 4-16 megabits. These deployments are part of broader efforts to modernize energy infrastructure and improve efficiency. While the density requirements are modest, the consistent demand for smart meters ensures a stable revenue stream for NOR Flash manufacturers. Additionally, connected medical devices and aerospace avionics represent niche markets with specialized requirements. These applications demand extended temperature ranges and radiation-tolerant components, which command premium price points. Together, these segments help offset pricing pressures from the highly competitive consumer electronics sector.

By Process Technology Node: 28 Nanometer and Below Add Security Blocks

Italy’s demand pattern currently favors the 65 nm node, which remains dominant due to its established reliability and cost-effectiveness. However, advanced nodes such as 45 nm, 40 nm, and 28 nm are gaining traction as they incorporate embedded cryptographic engines and Physical Unclonable Functions, enabling OEMs to meet stringent UN R155 audit requirements. GigaDevice’s 55 nm platform has already achieved ISO 26262 ASIL-D certification for densities ranging from 64 Megabit to 2 Gigabit, providing Tier 1 suppliers with confidence in long-term supply stability. Macronix has further advanced the market with its 28 nm ArmorBoot devices, which integrate secure boot and secure update functionalities into a single die. These innovations are setting new benchmarks for security and performance in the NOR Flash market.

Despite advancements, older 90 nm flows continue to serve legacy applications, particularly in broadcast and factory installations, where design cycles can extend up to 15 years. However, the cost gap between 65 nm and 55 nm nodes has significantly narrowed, making the latter a more attractive option for higher densities without excessive die sizes. Advanced nodes are increasingly unlocking new capabilities, and the market is expected to shift towards sub-45 nm nodes as automotive customers complete their current five-year requalification cycles. This transition will likely drive further innovation and adoption of advanced NOR Flash technologies in Italy.

By Packaging Type: WLCSP Shrinks the Footprint for Wearables

Italian EMS providers, already equipped with reflow profiles and test sockets, continue to rely on Quad Flat No-lead and SOIC packages due to their established infrastructure. These packages remain essential in the market as they align with the existing manufacturing capabilities of these providers. On the other hand, shipments of WLCSP packages are experiencing a strong annual growth rate of 6.60%. This growth is fueled by increasing demand for compact and efficient solutions in applications such as miniature hearing aids, glucose monitors, and telematics tags for two-wheelers. GigaDevice has introduced 8 Megabit WLCSP units, which occupy less than 4 mm² on the board. This compact size is a critical factor for enabling advancements in true wireless earbuds and smart rings, where space constraints are a significant consideration.

Ball Grid Array packages have emerged as the preferred choice for domain controllers exceeding 256 Megabit, primarily due to their ability to address signal integrity and thermal management challenges. These packages are particularly suited for high-performance applications where reliability is paramount. In 2024, Silicon Box received approval for a EUR 3.2 billion (USD 3.46 billion) advanced-packaging facility in Novara, marking a significant investment in the region's semiconductor capabilities. This plant is expected to provide chip-scale services, which could play a crucial role in regionalizing supply chains. Although the facility is projected to ramp up operations after 2027, it holds the potential to reshape the advanced-packaging landscape in Europe. The development underscores the growing importance of localized supply chains in the semiconductor market.

Geography Analysis

Northern regions drive three-quarters of Italy's NOR Flash market demand, with Lombardy and Veneto leading the way due to their high consumption of devices for smart meters and industrial gateways. Automotive purchases are heavily concentrated in Turin, Modena, and Bologna, where companies like Stellantis, Ferrari, and Lamborghini are localizing ADAS development. Additionally, Emilia-Romagna’s mechatronics corridor is expanding the use of Serial NOR in robotics, particularly for motion-control boards. Lazio, while slightly behind, is gaining traction as Rome-based utilities accelerate meter exchanges mandated by ARERA. This regional demand highlights the diverse applications of NOR Flash across Italy.

Southern regions currently contribute modestly to the NOR Flash market but hold potential for growth. The anticipated operationalization of Silicon Box’s Novara facility and STMicroelectronics’ Catania expansions could significantly enhance packaging and test capacity in the region. Such developments are expected to shorten supply chains and mitigate the impact of Euro-USD currency fluctuations, which are projected to reach 1.24 by 2027. However, the lack of a domestic memory wafer-fab remains a critical challenge, exposing Italian integrators to extended ocean lead times and geopolitical risks in Asia. These factors underscore the need for strategic investments in the region.

Policymakers are increasingly viewing packaging investments as a temporary solution to address supply chain vulnerabilities. While these investments could provide immediate relief, the absence of mature-node fabs within Italy continues to hinder long-term growth prospects. Brussels is currently evaluating incentives to attract such fabs, which could help reduce dependency on imports and strengthen the local semiconductor ecosystem. In the meantime, regional initiatives like the Novara and Catania projects are expected to play a crucial role in stabilizing the market and supporting Italy’s growing demand for NOR Flash applications.

Mordor Intelligence evaluates the nor flash market across all key regional markets, including Europe and Asia, with deeper country-level insights covering Germany, France, South Korea, United States, China, India, and Japan.

Competitive Landscape

The Italian NOR Flash market is moderately concentrated. Four brands, including STMicroelectronics, Infineon, Winbond, and GigaDevice, collectively command roughly 60-65% of Italy's NOR Flash market revenue. STMicroelectronics leverages its Italian manufacturing roots to secure automotive sockets, even though the company outsources NOR fabrication. This strategic approach allows the company to maintain a strong foothold in the automotive sector. In 2026, GigaDevice expanded its distribution network through SEMITRON, which intensified price competition in the industrial sector. This move highlights the growing competitiveness within the market as companies strive to capture a larger share. Infineon and Winbond differentiate themselves with ISO 26262 ASIL-D and AEC-Q100 Grade 1 certifications, which are critical for securing Level 2+ ADAS contracts.

Macronix has successfully carved out a niche in the market with its ArmorBoot secure-flash line. This product integrates authentication logic within the same die, a feature that resonates strongly with SMEs lacking in-house cybersecurity expertise. By addressing a specific pain point for smaller enterprises, Macronix has positioned itself as a key player in this segment. The ArmorBoot line not only enhances security but also simplifies implementation for businesses with limited technical resources. This innovation underscores the importance of product differentiation in a competitive market. Macronix's strategy demonstrates how targeted solutions can open new opportunities in underserved areas.

Chinese competitors, such as Puya Semiconductor, continue to disrupt the market with aggressive pricing strategies. However, they face significant challenges in meeting qualification standards for safety-critical automotive modules. These barriers limit their ability to compete in high-stakes applications, such as automotive systems requiring stringent certifications. Meanwhile, no single supplier holds more than a 25% market share, which encourages buyers to adopt multi-vendor strategies. This approach helps purchasers mitigate allocation risks while enhancing their negotiation leverage. The fragmented market structure ensures that competition remains robust, benefiting buyers through diversified sourcing options.

Italy NOR Flash Industry Leaders

Infineon Technologies AG

Micron Technology Inc.

GigaDevice Semiconductor Inc.

Macronix International Co. Ltd

Winbond Electronics Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GigaDevice expanded GD25UF ultra-low-voltage SPI NOR family to 8-256 Megabit densities, trimming read power by up to 70% versus 1.8 Volt parts.

- March 2026: GlobalFoundries and Renesas deepened manufacturing partnership to secure FD-SOI and feature-rich CMOS capacity for embedded-flash MCUs.

- January 2026: Stellantis joined AI4I and Chips-IT initiatives, committing to USD 10 billion of semiconductor sourcing through 2030.

- December 2025: European Investment Bank approved EUR 1 billion (USD 1.08 billion) credit line for STMicroelectronics to accelerate Italian and French fab expansions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italy NOR flash memory market as the yearly revenue generated by newly manufactured serial and parallel NOR devices, across all densities, voltages, packages, and process nodes, shipped to Italian OEM and aftermarket channels for code-storage or execute-in-place uses within consumer, automotive, industrial, and connected-device electronics.

Scope Exclusion: Firmware services, NAND-based combo packages, and refurbished or gray-market chips lie outside this boundary.

Segmentation Overview

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit and Less NOR greater than 2 Mb

- 8 Megabit and Less NOR greater than 4 Mb

- 16 Megabit and Less NOR greater than 8 Mb

- 32 Megabit and Less NOR greater than 16 Mb

- 64 Megabit and Less NOR greater than 32 Mb

- 128 Megabit and Less NOR greater than 64 Mb

- 256 Megabit and Less NOR greater than 128 Mb

- Greater than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage 1.65 V - 3.6 V

- Other Voltage Classes 1.2 V 2.5 V 5 V

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other Applications

- By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm including 58 nm

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

Detailed Research Methodology and Data Validation

Primary Research

Our team spoke with Tier-1 automotive module designers in Turin, Lombardy-based set-top-box makers, and Italian distributors to verify density preferences, ASP corridors, and octal-SPI adoption. Follow-up calls with global NOR suppliers' supply-chain managers validated shipment seasonality and margin ranges.

Desk Research

We drew on Italy's ISTAT electronics trade tables, Eurostat's HS 854231 import codes, and customs manifests to anchor unit inflows, and then consulted European Semiconductor Industry Association white papers, Questel patent-family counts, and REACH/RoHS filings shaping device mixes. Company 10-Ks, investor decks, IEEE Electron Devices papers, plus revenue splits from D&B Hoovers and news flow on Dow Jones Factiva filled trend gaps. These sources are indicative; many additional public and subscription outlets aided data collection and triangulation.

Market-Sizing & Forecasting

A top-down build reconstructs domestic demand from local assembly plus net imports, then is tension-checked with selective bottom-up roll-ups of supplier shipments and channel audits. Key variables like ADAS ECU installs per car, DVB-T2 decoder refresh volumes, smart-meter roll-out quotas, EU Chips Act fab additions, and density-level ASP trends drive annual shifts. Multivariate regression and ARIMA overlays extend the view to 2030. Where small-lot industrial orders escape bottom-up capture, distributor mark-ups are applied to close gaps, after one-time bottom-up and top-down convergence.

Data Validation & Update Cycle

Outputs undergo variance scans versus five-year CAGR bands and peer ratios; any anomaly triggers senior analyst review and, if material, a rapid re-survey. We refresh models each year and issue interim updates when policy or fab-capacity shocks arise, ensuring clients receive the latest perspective before report delivery.

Why Mordor's Italy NOR Flash Baseline Earns Trust

Estimates differ because firms vary geographic cuts, device taxonomy, and refresh cadence; such choices push totals apart.

Typical gaps stem from: (1) some sources roll Italy into wider Europe, (2) others count only serial-SPI chips yet fold retrofit module revenue, (3) several extrapolate global ASP curves without Italian channel feedback, and (4) refreshes can be biennial, whereas Mordor analysts revisit drivers quarterly to mirror Transizione 4.0 incentives and local fab news.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 72.09 M (2025) | Mordor Intelligence | - |

| USD 200 M (2025) | Regional Consultancy A | Serial-only scope plus retrofit module sales inflate value |

| USD 5.27 B (2025) | Global Consultancy B | Worldwide revenue re-mapped to Italy and includes NAND substitutes |

The comparison shows that Mordor's disciplined country boundary, variable mix, and annual refresh deliver a balanced, transparent baseline that decision-makers can trace to clear inputs and reproducible steps.

Key Questions Answered in the Report

What is the current Italy NOR Flash market size and its projected value by 2031?

The market stands at USD 75.41 million in 2026 and is forecast to reach USD 94.42 million by 2031, reflecting a 4.60% CAGR over 2026-2031.

Which interface segment is expanding fastest in Italy?

Octal and xSPI NOR Flash shows the highest growth, projected at 9.60% CAGR through 2031 as automotive OEMs accelerate OTA-update bandwidth.

Why is Parallel NOR gaining traction despite lower 2025 share?

Safety-critical automotive controllers require deterministic boot times, and Parallel NOR meets ISO 26262 latency constraints better than Serial formats, driving a 7.40% CAGR.

How do Transizione 4.0 incentives influence industrial demand?

Enhanced depreciation rules let manufacturers write off up to 130% of qualified hardware, encouraging PLC and gateway upgrades that embed Serial NOR Flash.

Which voltage class is preferred for battery-powered two-wheelers?

1.8 Volt and emerging 1.2 Volt NOR Flash reduce energy draw by up to 70%, making them ideal for connected motorcycles and scooters pursuing UN R155 compliance.

What hampers domestic supply of NOR Flash in Italy?

High front-end fab costs and a lack of local memory wafer plants keep the country dependent on Asian foundries, lengthening lead times and exposing buyers to currency swings.

Page last updated on: