China NOR Flash Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

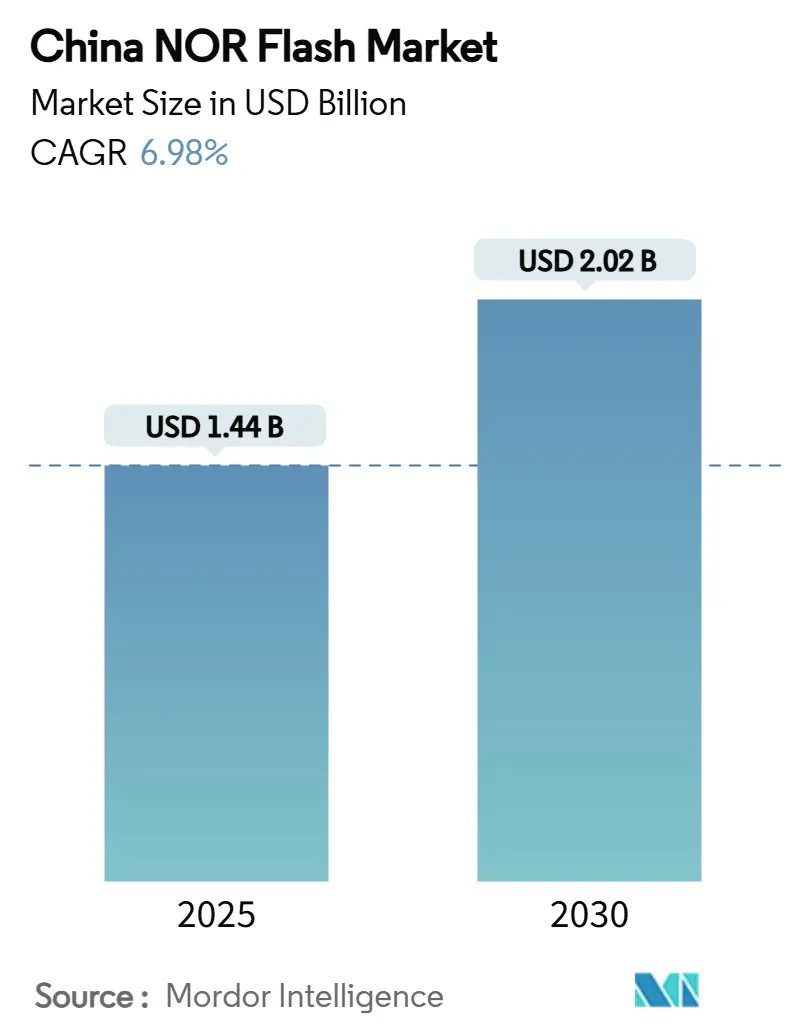

| Market Size (2025) | USD 1.44 Billion |

| Market Size (2030) | USD 2.02 Billion |

| Growth Rate (2025 - 2030) | 6.98% CAGR |

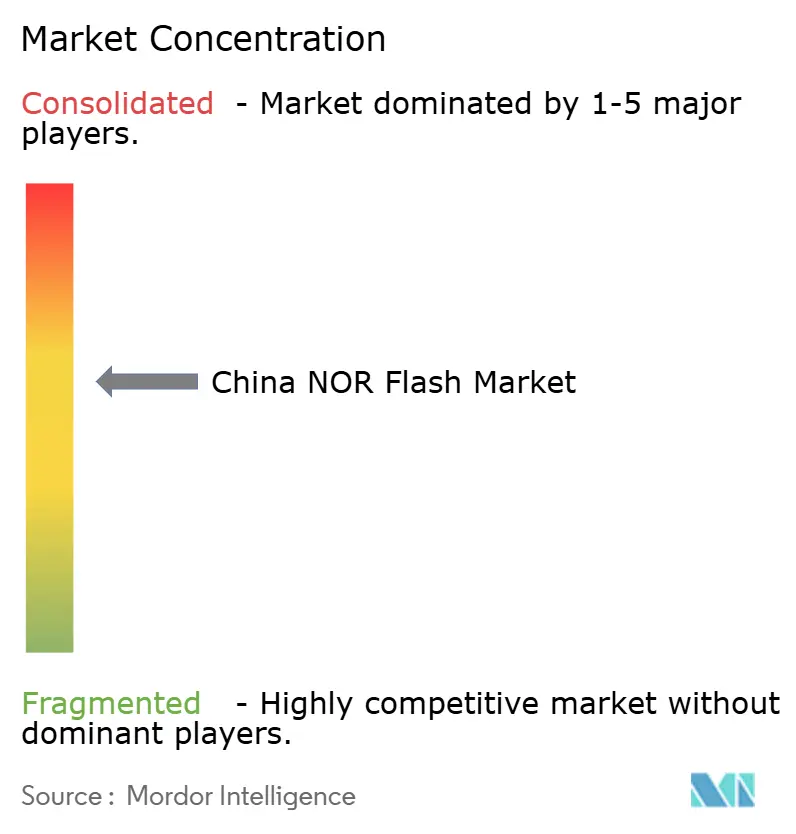

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China NOR Flash Market Analysis by Mordor Intelligence

Market Analysis

The China NOR Flash market size is expected to be worth USD 1.44 billion in 2025 and is projected to reach USD 2.02 billion by 2030, growing at a 6.98% CAGR during the forecast period. Growth stems from Beijing’s push for semiconductor self-sufficiency, the XinChuang procurement mandate, and mounting local demand in electric vehicles, industrial IoT, and premium consumer devices. Domestic suppliers are moving up the value curve by focusing on 55 nm and 65 nm process nodes that strike a balance between cost and performance, while hybrid serial-parallel products are closing the gap with higher-density alternatives. Regional manufacturing clusters in Guangdong, Jiangsu, and Anhui are accelerating time-to-market for automotive-grade parts that meet ISO 26262 safety targets. Meanwhile, smartphone, smart-EV, and industrial system OEMs continue to favour execute-in-place memories that boot quickly and maintain code integrity under harsh conditions, sustaining a resilient pipeline for the China NOR Flash market even when broader memory cycles soften.

Key Report Takeaways

- By product type, Serial NOR held 79.2% of the China NOR Flash market share in 2024. The Serial NOR Flash segment is also anticipated to witness the highest CAGR of 7.5%, while the Parallel NOR is forecast to expand at a 3.2% CAGR through 2030.

- By interface, SPI Single/Dual led with 45.1% revenue share in 2024; Quad SPI is projected to grow at a 7.1% CAGR to 2030.

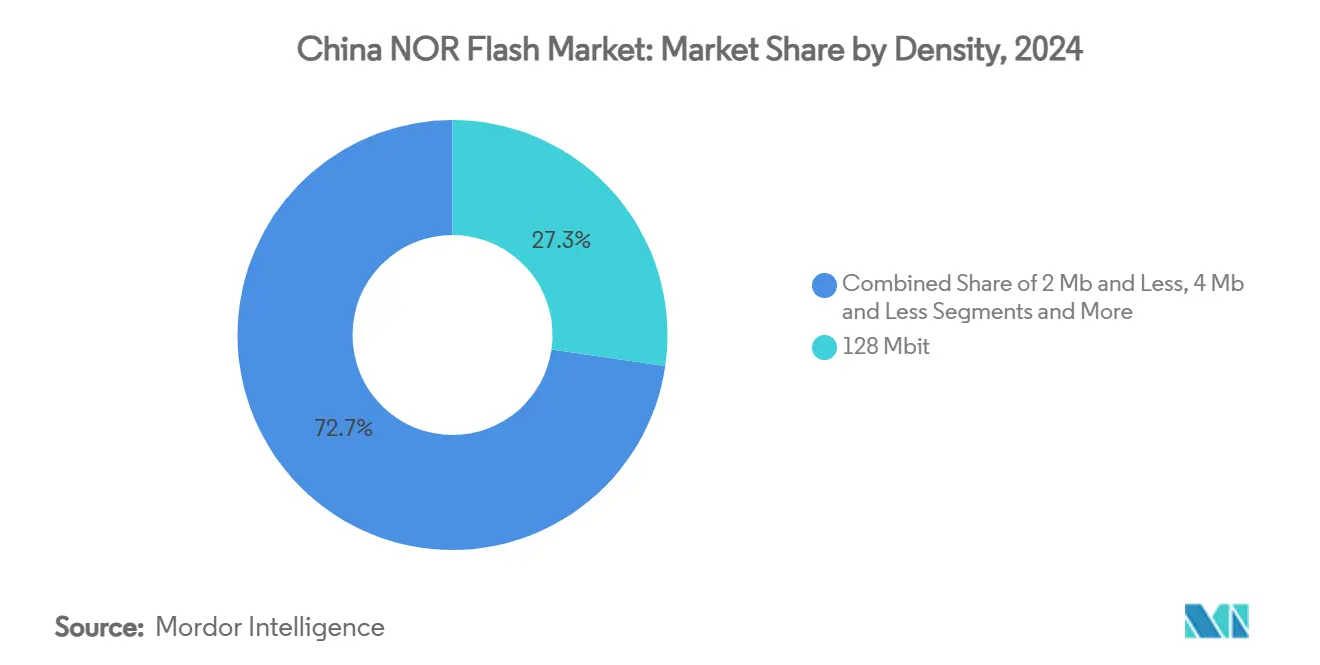

- By density, 128 Mbit devices accounted for 27.3% of the China NOR Flash market size in 2024; densities above 256 Mbit are expected to rise at a 7.3% CAGR.

- By voltage, 3 V class devices commanded a 53.2% share of the China NOR Flash market size in 2024 and are advancing at a 7.1% CAGR through 2030.

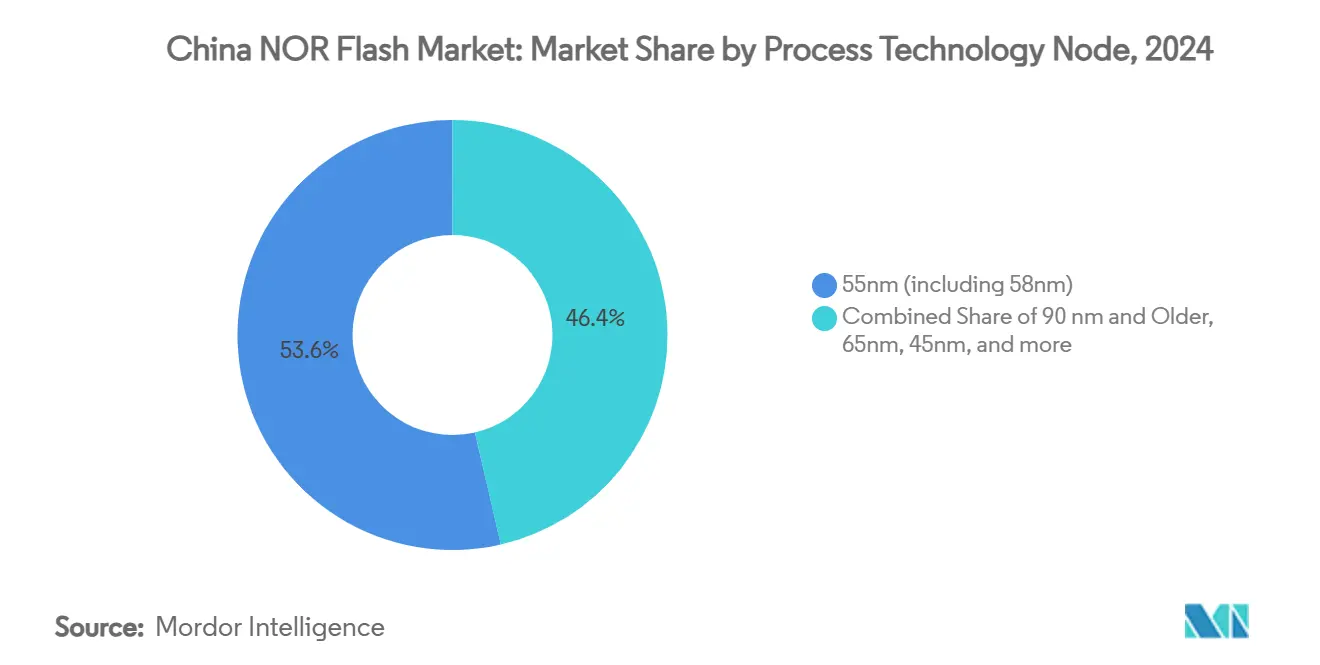

- By process node, 55 nm contributed 53.6% of 2024 revenue, whereas 65 nm nodes exhibit the fastest CAGR of 7.4% to 2030.

- By packaging, QFN/SOIC held 41.6% revenue share in 2024 and is poised to grow 7.2% annually.

- By end use, consumer electronics led with 47.9% revenue share in 2024; automotive applications are growing at 7.8% CAGR to 2030.

Future direction is shaped by developments occurring across multiple countries and regions, with China contributing to the overall trajectory. The outlook on worldwide nor flash market reflects how these are expected to evolve collectively.

China NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing digitalization and data-centric applications | +1.80% | National; Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| XinChuang program favouring China-made memory | +2.10% | National; government and SOEs | Long term (≥4 years) |

| Expansion of smart-EV hubs in Guangdong and Anhui | +1.40% | Guangdong, Anhui | Medium term (2-4 years) |

| Rapid OLED driver adoption requiring enhanced NOR | +0.90% | Coastal electronics zones | Short term (≤2 years) |

| Surging demand from domestic smartphone OEMs | +0.70% | Shenzhen, Dongguan, Beijing | Short term (≤2 years) |

| Evolution of smart vehicles | +1.20% | Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Digitalization and Emergence of Data-centric Applications

Industrial IoT rollouts, municipal smart-city projects, and AI-driven edge devices elevate NOR Flash from commodity status to mission-critical infrastructure. Secure-boot sequences and execute-in-place code storage underpin reliable field operations, making high-end serial parts indispensable for surveillance cameras, traffic controllers, and power-grid sensors. Robust government funding for digital-infrastructure pilots accelerates qualification cycles, shortening time-to-volume for domestic suppliers.[1]CSIS, "Semiconductor Supply Chain Constraints Report," csis.org Firmware integrity requirements further reinforce the appeal of NOR’s random access advantages over block-based alternatives. As application software footprints swell, OEMs migrate from 32 Mbit to 128 Mbit devices, maintaining single-chip designs without sacrificing boot speed. Continuous firmware-over-the-air updates in field equipment lock in a stable replacement demand, ensuring sustained expansion of the China NOR Flash market.

Government “XinChuang” Procurement Program Favouring China-made Memory

Mandatory localization for servers, PCs, and embedded modules across ministries catalyzes a structural uptick in domestic NOR shipments. Tier-one suppliers secure multiyear supply commitments, providing predictable fab loading that justifies process-node refinements. Higher-quality assurance targets embedded in the program elevate incoming inspection and reliability test benchmarks, narrowing historical performance gaps with foreign competitors. The procurement rules effectively ring-fence roughly one-third of total national demand, limiting import penetration and enabling domestic firms to allocate R&D toward differentiated, security-enhanced NOR portfolios. Budget certainty enables suppliers to negotiate longer material contracts, thereby stabilizing wafer input pricing despite cyclical swings in broader memory markets. XinChuang mandates domestic content in critical information systems, with compliance deadlines of 2026 for ministries and 2027 for state-owned firms. Memory is explicitly covered, carving out a protected segment equal to nearly one-third of total demand. Preferential contracts let GigaDevice and Puya ramp new 55 nm product families while improving quality standards to narrow performance gaps with foreign peers.[2]KIOXIA, "Serial NAND and Automotive Storage Solutions," kioxia.com

Expansion of Smart-EV Production Hubs in Guangdong Anhui Using Automotive-grade NOR

Large-scale EV clustering compresses development cycles between automakers and local memory houses. Automotive-qualified NOR devices with ISO 26262 ASIL D ratings now populate digital cockpits, battery-management units, and domain controllers, each demanding instant-on diagnostics during cold-start events. Local authorities subsidize reliability labs, enabling comprehensive temperature-cycling and electromagnetic-interference testing close to manufacturing lines. The clustering effect reduces logistics lead times and amplifies engineering collaboration, translating to faster product tweaks and higher design-win retention for domestic suppliers. As EV software stacks grow, memory content per vehicle climbs, further expanding the addressable slice of the China NOR Flash market.

Rapid Adoption of OLED Display Drivers Requiring Enhanced NOR for Code Storage

OLED driver ICs demand longer firmware blocks to orchestrate pixel-level color correction and power management, lifting baseline density requirements. Serial NOR remains preferred thanks to execute-in-place support, allowing SoCs to read code directly over quad-SPI without external DRAM buffers. High-end smartphone makers now fit 128 Mbit and 256 Mbit devices, up from 64 Mbit a generation ago, preserving slim form-factor budgets. This capacity creep masks unit price erosion, sustaining revenue momentum for suppliers. While some budget phones pivot to Serial NAND, premium display modules still prioritize boot-time consistency and low latent defects, keeping OLED demand tightly coupled to NOR technology in the China NOR Flash market.

OLED controllers need larger and faster code space for pixel-level algorithms, favouring high-bandwidth NOR with execute-in-place capability. Chinese smartphone makers are upsizing from 64 Mbit to 128 Mbit densities and adopting Quad SPI to cut boot latency. Device makers in Dongguan and Shenzhen are early adopters of Octal NOR variants delivering 400 MB/s read throughput.[3]STMicroelectronics, “OLED Display Driver Overview,” st.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of R&D and fabrication | -0.80% | National; major fab hubs | Long term (≥4 years) |

| Growing Substitution by high-speed SPI NAND in displays and wearables | -1.30% | Consumer electronics centers | Medium term (2–4 years) |

| Structural yield disadvantage due to tight design rules in 55nm / 45nm NOR nodes | -0.90% | Domestic advanced NOR bit-density programs | Medium term (2–4 years) |

| Export control choke-points on Etch + PVD toolsets for high-reliability automotive-grade NOR | -1.10% | Global toolmakers: the highest constraint in China's auto-grade NOR | Long term (3–5+ years) |

| Source: Mordor Intelligence | |||

High Cost of R&D and Fabrication

State-of-the-art photolithography tools, specialty etchers, and mask sets escalate capital intensity, limiting newcomers to mature-node lines. Export controls on EUV and key deposition gear oblige Chinese fabs to engineer workarounds, stretching development timetables. Depreciation loads compress gross margins, prompting selective capacity additions timed to peak demand seasons. Collaborative design frameworks between controller IC firms and NOR vendors attempt to squeeze extra bandwidth from legacy process nodes, yet physics-based scaling constraints persist. While government grants soften cash burn, fiscal prudence forces a paced roll-out of successive technology generations, tempering the growth arc of the China NOR Flash market.

Growing Substitution by High-speed SPI NAND in Displays and Wearables

Serial NAND narrows latency gaps by integrating page-buffer acceleration and compatible instruction sets, letting OEMs swap devices without major PCB revisions. Cost per bit advantages exceed 30% at densities beyond 512 Mbit, luring designers of smartwatches and budget smart TVs. Memory suppliers counter with hybrid QSPI NAND lines that mimic NOR read speeds while preserving NAND-style economics, blurring category boundaries. Yet, in path-critical code storage, such as automotive failsafe systems, the deterministic response of NOR remains non-negotiable. The net effect is a segmented substitution pattern that caps upside in price-sensitive niches of the China NOR Flash market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Serial Dominates While Parallel Gains Momentum

Serial NOR Flash devices held a commanding 79.2% of the China NOR Flash market share in 2024, anchored by SPI and QSPI interfaces that need only four to eight pins. In 2025, the segment continues to grow as embedded microcontrollers standardise on serial buses for boot code storage in consumer electronics. Across 2025-2030, Parallel NOR expands at a 3.2% CAGR, driven by demand for deterministic access in centralised automotive computers.

Developers increasingly blur the lines between serial and parallel by adopting Octal devices that reach 400 MB/s read speeds while preserving compact pinouts. GigaDevice’s GD25LX line shows how a serial package can rival legacy parallel bandwidth.[4]GigaDevice, “Annual Report 2024,” gigadevice.com Automotive brands piloting domain controller designs in Anhui value such products for fast over-the-air update cycles without adding board space.

By Interface: Quad SPI Adoption Accelerates Amid Performance Demands

SPI Single/Dual retained 45.1% revenue share in 2024 as the workhorse interface for cost-sensitive IoT nodes. The China NOR Flash market now sees OEM roadmaps shifting toward Quad SPI to cut boot times in digital cockpits and industrial HMIs. Quad SPI grows at 7.1% CAGR and could overtake Single/Dual by 2029 if adoption curves in smart-EV dashboards stay on track.

At the premium end, Octal and xSPI devices are entering telematics and AI accelerator cards that need sustained bandwidth beyond 200 MB/s. Winbond reports that its Octal interface supports up to 416 MHz equivalent transfers, doubling frame-buffer load speeds for high-resolution cluster displays. Though volumes remain small, these interfaces establish a migration path should performance ceilings of Quad SPI emerge.

By Density: Higher Capacities Capture Premium Segments

The 128 Mbit tier held 27.3% of 2024 sales, balancing code size and cost across mobile, IoT, and industrial use cases. The China NOR Flash market size above 256 Mbit is forecast to have a CAGR growth of 7.3% to 2030, driven by data-heavy ADAS and infotainment stacks in electric vehicles. Densities of 512 Mbit and 1 Gbit remain niche but accelerate fastest, benefiting from Alliance Memory and Infineon launches that marry high density with QSPI interfaces.

Mid-range 32 Mbit-64 Mbit parts stay relevant for communications and meter endpoints, though their share slips as firmware footprints expand. Sub-16 Mbit parts gradually retreat to legacy and ultra-low-cost gadgets. Security-enhanced NOR such as Winbond W77Q overlays AES-256 encryption and secure boot features on all densities, creating new premium sub-segments.

By Voltage: 3 V Class Dominates While Maintaining Growth Leadership

Devices rated for 3 V accounted for 53.2% of 2024. Automotive and industrial boards prefer 3 V for robust noise margins and compatibility with 5 V-tolerant GPIO. The China NOR Flash market share for 1.8 V parts covers wearables and mobile phones, where battery life trumps voltage headroom.

Suppliers introduce 1.2 V experimental lines to partner with new sub-threshold MCUs, yet such parts are still pilot-scale. Designers seeking one flash portfolio across multiple voltages gravitate toward wide-voltage options that span 1.65-3.6 V, simplifying qualification across product tiers. Winbond’s 3V automotive series illustrates why this voltage class remains the sweet spot for ISO 26262 systems.

By Process Technology Node: 55 nm Dominates While 65 nm Shows Surprising Growth

In 2024, 55 nm nodes supplied 53.6% of wafers because domestic fabs like SMIC achieved high yield and stable supply at that geometry. The China NOR Flash market is now seeing renewed interest in 65 nm, which records a 7.4% CAGR due to its proven reliability in harsh environments. TSMC publicised multiple automotive qualifications for its 65 nm embedded flash, reassuring Chinese module makers of long-term support.[5]Infineon Technologies AG, press release, May 8, 2025, infineon.com

Trade restrictions that curb access to advanced EUV tools make moving below 40 nm impractical. Consequently, domestic IDMs refine 55 nm and 65 nm cell architectures, adding stacked bit-line and charge-trapping designs to push density without shrinking lithography. These adaptations extend lifespan and write endurance, matching stringent vehicle lifetime requirements.

By Packaging Type: QFN/SOIC Packages Lead Through Versatility

QFN and SOIC combined controlled 41.6% of 2024 revenue and grew 7.2% annually, reflecting their balance of thermal handling, board real estate, and cost. The China NOR Flash market size for these packages aligns with trends in smart-EV and industrial controllers that operate at elevated temperatures. Micron’s 16-pin SOIC N25Q128A11ESE40F highlights why SOIC remains a standard for automotive ECU designs where pin-to-pin drop-in matters.[6]Micron Technology, “N25Q NOR Flash Data Sheet,” micron.com

BGA and WLCSP packages are adopted in premium phones and wearables, offering thinner profiles, though at a higher assembly cost. Flip-chip options are emerging for centralised compute modules that demand robust signal integrity at high read frequencies. Domestic OSATs invest in QFN automation lines to meet XinChuang qualification queues, ensuring capacity headroom for 2026-2027 compliance peaks.

By End-user Application: Consumer Electronics Leads, Automotive Accelerates

Consumer devices led with 47.9% of revenue in 2024, anchored by smartphones, tablets, and smart-home appliances. Domestic OEMs replace imported memory to secure logistics and cost, helped by serial devices that follow mature SPI protocols. The China NOR Flash market sees automotive grow 7.8% CAGR as EV makers integrate larger flashing footprints for firmware-over-the-air updates.

Network gear for 5G infrastructure remains another steady user, demanding high-reliability boot devices that resist bit-flip under continuous operation. Industrial IoT nodes in Shenzhen factories embed secure NOR to protect intellectual property and support remote update frameworks. Health-tech devices, security cameras, and emerging AIoT hubs in Xi’an add incremental volume, broadening the customer base for domestic suppliers.

Geography Analysis

Regional clustering defines demand patterns. Guangdong, Shanghai, and Jiangsu together account for the majority of shipments because they host consumer-electronics assembly lines and IC packaging houses. Local design centres in Shenzhen’s Bao’an district fast-track qualifications, allowing domestic fabs to win sockets inside OLED smartphones and smart-home gateways. Jiangsu’s Suzhou Park adds backend test capacity, reducing logistics cost for final module makers.

Anhui and Jiangsu lead automotive memory uptake. Hefei’s EV corridor hosts smart-EV start-ups and Tier-1 suppliers who require 256 Mbit/s to 1 Gbit/s NOR for domain controllers. Close proximity to GigaDevice’s Suzhou fab shortens DVT loops, encouraging joint reliability studies that align with ISO 26262. The China NOR Flash market size linked to these provinces is likely to grow significantly as EV builds multiply.

Beijing and major provincial capitals represent policy-driven demand through XinChuang mandates. Ministries, public utilities, and state-owned banks migrate to local IT stacks that standardise on China-produced NOR to secure firmware roots-of-trust. This steady pull helps balance cyclicality from consumer gadgets and creates predictable order books for domestic suppliers. Cross-provincial research and development nodes focusing on secure memory co-locate with these customers, accelerating feature roadmaps.

Analysis of the nor flash market by Mordor Intelligence spans multiple other regional evaluations across Europe and Asia, supported by country-level insights for Japan, South Korea, France, United Kingdom, Germany, Mexico, and United States, wherein local market conditions keep varying from one country to another.

Competitive Landscape

China’s NOR Flash Market arena blends moderate concentration with intensifying domestic ascendancy. GigaDevice remains among the top NOR Flash suppliers in China, leveraging a broad portfolio that ranges from 1.2 V miniaturized parts to 400 MB/s octal solutions. Winning ISO 26262 ASIL D accreditation for its GD25/55 line unlocks premium automotive engagements and signals process maturity on China-based lines.[7]Infineon Technologies AG, press release, May 8, 2025, infineon.com Macronix continues to lead the density-innovation race via 3D NOR prototypes that stack multiple cell planes, a maneuver aimed at bending cost-per-bit curves downward. Winbond retains the shipment crown by volume but pivots R&D toward secure-flash variants to defend margins in commoditizing consumer niches.

Domestic challengers such as Puya Semiconductor and Giantec sharpen focus on mid-density, cost-sensitive segments, courting IoT module makers constrained by bill-of-materials ceilings. Their fab-light models outsource wafer fabrication yet invest in controller-firmware co-design, differentiating on system-level performance rather than raw cell geometry. Foreign incumbents adopt dual tactics, e.g., Infineon, recently doubled down on automotive functional-safety credentials, while Alliance Memory expanded high-density offerings to serve embedded boards that outgrow 128 Mbit ceilings.

Strategic moves orbit around balancing density, performance, and compliance. Suppliers courting automotive demand allocate capital to extensive qualification labs and zero-defect initiatives, whereas those chasing IoT volumes emphasize power-down data-retention specifications and secure boot features. The resulting coexistence of premium and commodity tiers prevents single-player dominance, positioning the China NOR Flash market as a competitively vibrant but policy-shaped battleground.

China NOR Flash Industry Leaders

-

GigaDevice Semiconductor Inc.

-

Macronix International Co. Ltd

-

Winbond Electronics Corporation

-

Puya Semiconductor (Shanghai) Co., Ltd.

-

Giantec Semiconductor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Winbond noted 1Q25 NOR revenue down 10% QoQ yet up 5% YoY as bit shipments rose low-teens % YoY, flagging tighter SLC NAND supply that could swing demand back to NOR.

- January 2025: Infineon’s SEMPER family achieved ISO 26262 ASIL-D certification for automotive NOR, targeting ADAS and cockpit modules.

- April 2025: Alliance Memory unveiled 128 Mb-512 Mb serial NOR at Embedded World to serve industrial and medical embedded designs.

- December 2024: GigaDevice’s GD25/55 SPI NOR family received formal ASIL-D certification, supporting throughputs up to 400 MB/s and 20-year data retention.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the China NOR flash memory market as the yearly revenue generated by newly-manufactured serial and parallel NOR devices sold within mainland China, measured in USD and units, irrespective of package or process node. We focus on all densities up to and above 256 Mbit that are embedded in consumer electronics, communication gear, automobiles, industrial controllers, and other code-storage use cases.

Scope exclusions include parts shipped to overseas factories for re-export, legacy UV-EPROM replacements, and stacked die that combine NOR with MCU logic.

Segmentation Overview

-

By Product Type

- Serial NOR Flash

- Parallel NOR Flash

-

By Interface

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

-

By Density

- 2 Megabit and Less NOR

- 4 Megabit and Less-NOR (greater than 2mb) NOR

- 8 Megabit and Less (greater than 4mb) NOR

- 16 Megabit and Less (greater than 8mb) NOR

- 32 Megabit and Less (greater than 16mb) NOR

- 64 Megabit and Less (greater than 32mb) NOR

- 128 Megabit and Less (greater than 64MB) NOR

- 256 Megabit and Less (greater than 128MB) NOR

- Greater than 256 Megabit

-

By Voltage

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V – 3.6 V)

- Others - 1.2V Class (and similar sub-1.8V) (2.5V, 5V, etc.)

-

By End-user Application

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other Applications

-

By Process Technology Node

- 90 nm and Older

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

-

By Packaging Type

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed fabless designers, foundry managers, EMS buyers, and tier-one component distributors across Shenzhen, Shanghai, Nanjing, Taipei, and Detroit. The conversations clarified average contract prices, density mix shifts, automotive qualification timelines, and import substitution plans, enabling us to fill gaps left by desk work and to validate early model outputs.

Desk Research

We began by gathering macro and trade-level clues from tier-one public sources such as the Ministry of Industry and Information Technology, China Customs (GACC) shipment records, the China Association of Automobile Manufacturers, WSTS semiconductor statistics, and patent filings mined via Questel. Annual reports, 10-K filings, and investor decks from key suppliers complemented these datasets, while D&B Hoovers supplied private-company revenue splits that anchor supplier roll-ups.

Press releases, tender portals, and leading electronics trade magazines then helped us timestamp node migrations, ASP resets, and capacity ramp-ups. These references illustrate typical inputs only; many additional publicly available materials were reviewed to cross-check figures and definitions.

Market-Sizing & Forecasting

A top-down production and trade reconstruction created the initial demand pool. We layered import value, domestic wafer starts on relevant lines, and average selling price curves to establish the baseline. Select bottom-up checks, including sampled supplier revenues and distributor channel audits, were then applied to fine-tune totals.

Key model drivers include: 1) serial NOR attach rate per 5G small cell, 2) average NOR content per smart EV ECU, 3) wafer starts by node, 4) quarterly ASP compression, and 5) density migration toward higher capacities. Multivariate regression of these variables underpins the forecast; scenario analysis tests policy and pricing shocks, and gaps in bottom-up data are bridged using historic density mix benchmarks.

Data Validation & Update Cycle

Outputs pass three rounds of analyst review, variance screens against independent indicators, and re-checks with select interviewees. Reports refresh each year, while interim updates are triggered when policy shifts or fab outages alter supply, ensuring clients receive the latest view before delivery.

Why Mordor's China NOR Flash Baseline Is the Benchmark for Reliability

Published estimates often differ because each firm chooses its own geography, density range, and unit-to-revenue conversion.

Key gap drivers include competitors blending NAND or Asia-Pacific volumes into totals, using list-price rather than transaction-price ASPs, or projecting with fixed growth multipliers instead of live node-level inputs. Our annual refresh cadence and dual (top-down and bottom-up) reconciliation further narrow variance.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.44 B (2025, China) | Mordor Intelligence | - |

| USD 1.20 B (2023, Asia-Pacific) | Regional Consultancy A | Broader geography, pre-inflation ASPs, no node segmentation |

| USD 2.78 B (2025, Global) | Trade Journal B | Global scope, includes NOR used in stacked MCPs, forecast from linear trend |

These comparisons show that when geography, density, and real transaction prices are aligned, our balanced, transparent baseline remains the most dependable reference for strategic planning. Clients tell us the clarity of Mordor's variable-level logic lets them quickly trace and replicate every step, boosting confidence in investment and sourcing decisions.

Key Questions Answered in the Report

What is the current size of the China NOR Flash market?

The market is valued at USD 1.44 billion in 2025 and is projected to reach USD 2.02 billion by 2030.

How will the XinChuang initiative influence demand?

XinChuang mandates domestic components in government and state-owned systems, securing a protected demand pool estimated at one-third of total market volume through 2027.

Which interface is growing fastest in the China NOR Flash market?

Quad SPI is expanding at a 7.1% CAGR because it quadruples bandwidth over conventional SPI, essential for rapid boot in complex automotive and industrial systems.

What competitive strategies are local suppliers using against global incumbents?

Domestic companies focus on mature 55 nm/65 nm nodes for reliable supply, secure ISO 26262 certifications for automotive design wins, and release hybrid QSPI NAND products to counter cost pressure from Serial NAND substitutes.

Page last updated on: