India NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

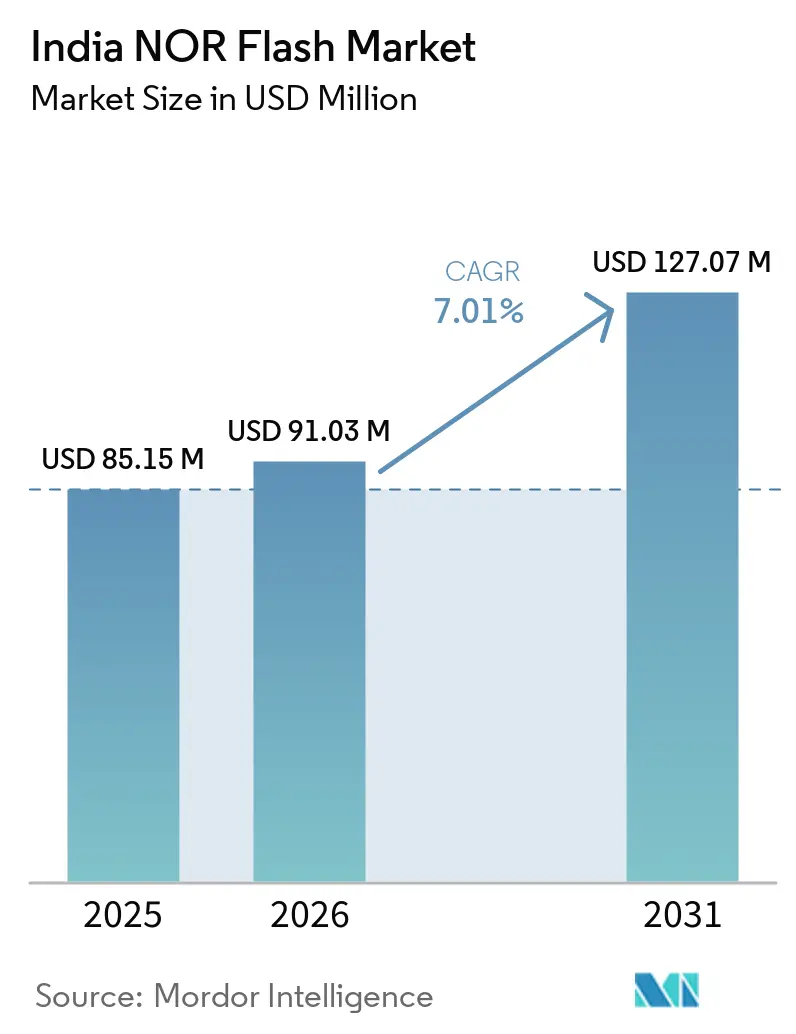

| Base Year Market Size (2025) | USD 85.15 Million |

| Market Size (2026) | USD 91.03 Million |

| Market Size (2031) | USD 127.07 Million |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India NOR Flash Market Analysis by Mordor Intelligence

The India NOR Flash market size is expected to increase from USD 85.15 million in 2025 to USD 91.03 million in 2026 and reach USD 127.07 million by 2031, growing at a CAGR of 6.9% over 2026-2031. Strong fiscal incentives, fast-rising electronics output, and new secure-boot mandates are driving demand even as buyers contend with high import duties and offshore wafer dependence. Production Linked Incentive (PLI) reimbursements and India Semiconductor Mission 2.0 cash subsidies reduce effective capital costs for electronics manufacturing services firms, allowing them to shift more procurement to domestic lines instead of importing pre-integrated modules. Secure-boot rules introduced by the Bureau of Indian Standards compel original equipment makers to embed dedicated code-storage memory, a niche where serial NOR excels because it provides execute-in-place capability at low pin counts. Automotive advanced driver-assistance systems are another catalyst, as tier-1 suppliers now require ISO 26262-qualified Octal or xSPI NOR devices that reach 400 MB/s read bandwidth to enable fast over-the-air firmware updates. Simultaneously, smartphone output under Make in India surged to USD 75 billion in fiscal 2026, expanding the base of devices that use 4-32 Mbit NOR dies for boot firmware.

Key Report Takeaways

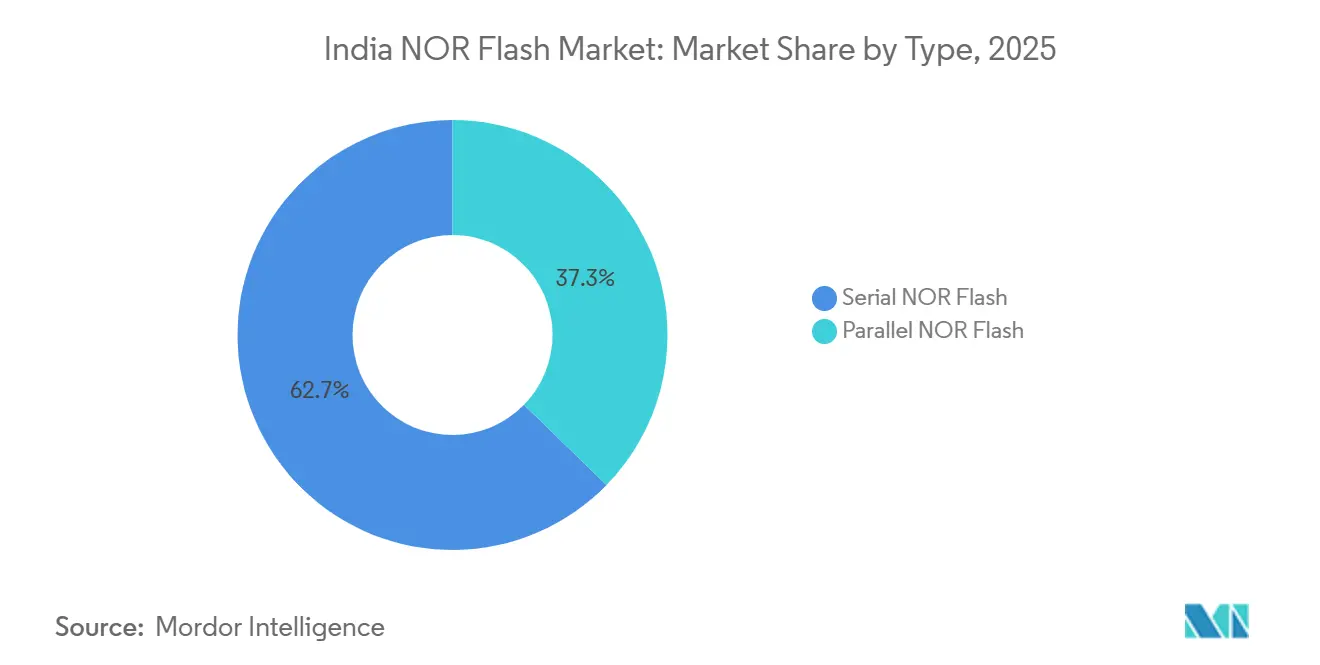

- By type, serial architectures led with 62.7% revenue share of the India NOR Flash market in 2025, and the segment is projected to expand at an 8.2% CAGR through 2031.

- By interface, Quad SPI dominated with 47.6% share of the India NOR Flash market in 2025, while Octal and xSPI variants are forecast to climb at a 9.8% CAGR to 2031.

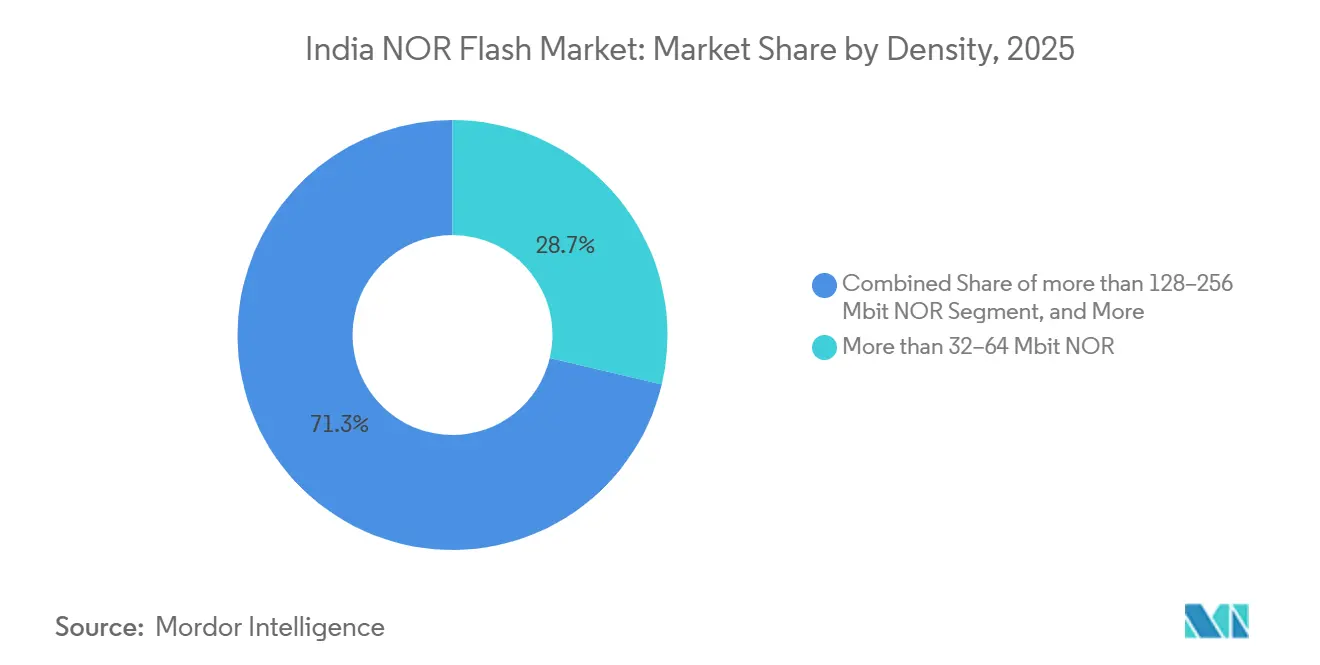

- By density, the 32-64 Mbit bin captured 28.7% of the India NOR Flash market share in 2025, whereas the 128-256 Mbit range is expected to grow at 12.4% through 2031.

- By voltage, 3 V devices held 54.8% share of the India NOR Flash market in 2025, but 1.8 V parts are advancing fastest with a 12.8% CAGR over 2026-2031.

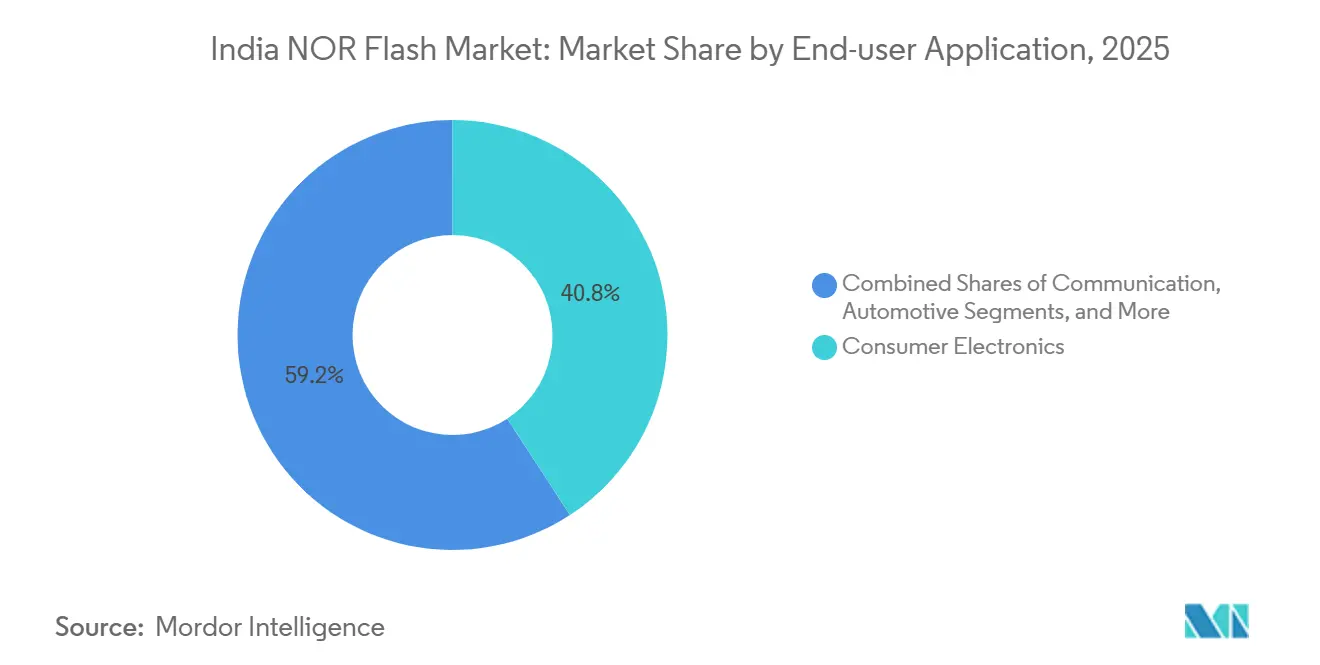

- By end-user application, consumer electronics accounted for 40.8% of the India NOR Flash market in 2025, yet automotive is set to grow at a 9.3% CAGR through 2031.

- By process technology node, 65 nm technology led with 36.9% share of the India NOR Flash market in 2025, and sub-28 nm nodes are projected to record a 7.6% CAGR through 2031.

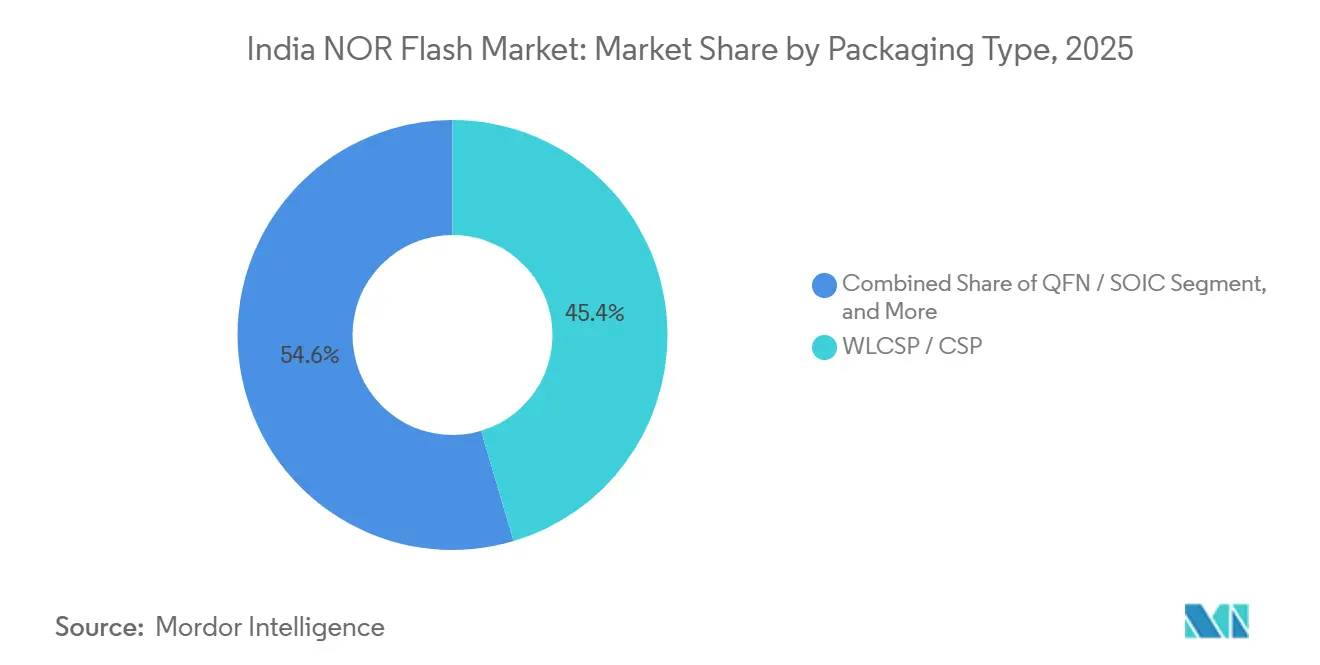

- By pakaging type, WLCSP / CSP led with 45.5% share of the India NOR Flash market in 2025, and is projected to record a 8.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India operates as part of an interconnected international environment rather than as a self-contained country level unit. The nor flash market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

India NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government PLI and semiconductor subsidies | +1.8% | National, strongest in Gujarat and Odisha | Medium term (2-4 years) |

| Secure-boot standards for IoT devices | +1.2% | National, early in smart meters and POS | Short term (≤ 2 years) |

| Domestic automotive ADAS ECU expansion | +1.5% | Chennai, Pune, Manesar | Medium term (2-4 years) |

| Smartphone production under Make in India | +1.0% | Noida, Chennai, Bengaluru | Short term (≤ 2 years) |

| Octal NOR adoption in aerospace and defense | +0.6% | Bengaluru, Hyderabad | Long term (≥ 4 years) |

| Edge-AI chips needing on-device code storage | +0.9% | Industrial hubs nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government PLI and Semiconductor Subsidies Lower Capital Barriers

India Semiconductor Mission 2.0 earmarked INR 1,000 crore (USD 120 million) for new assembly-test-mark-pack sites, while the Electronics Component Manufacturing Scheme approved 22 projects worth INR 41,863 crore (USD 5.02 billion) in January 2026, unlocking private coinvestment and reducing payback hurdles for local EMS companies.[1]Press Information Bureau, “Cabinet Approves India Semiconductor Mission 2.0,” pib.gov.in Micron’s USD 2.75 billion ATMP plant in Sanand signals confidence in foreign direct investment and encourages the formation of an ecosystem around Gujarat.

Secure-Boot Mandates Accelerate Serial NOR Demand

The Bureau of Indian Standards now requires cryptographic signature checks for consumer IoT firmware, pushing OEMs to add dedicated non-volatile code storage that can execute in place.[2]Micron Technology, “Sanand ATMP Facility,” micron.comMacronix answered with its ArmorBoot MX76 family up to 1 GB that supports dual 3.0 V and 1.8 V rails for secure-boot smart-meter designs.[3]Bureau of Indian Standards, “IoT Secure Boot Requirements,” bis.gov.in Early compliance efforts in smart-meter and payment-terminal rollouts ensure sustained design-in activity through 2027.

Automotive ADAS Electronics Need Functional-Safety NOR Flash

ADAS control units require ISO 26262-certified memory to ensure functional safety in automotive applications. Winbond’s W35T Octal NOR, built on a 58 nm process, delivers a high data transfer rate of 400 MB/s over xSPI and complies with ASIL-D standards, making it suitable for critical automotive systems. Similarly, Infineon’s Semper line, utilizing 45 nm MirrorBit technology, offers comparable bandwidth and reliability for ADAS systems. The increasing localization of ADAS module production in regions like Chennai and Pune is driving the demand for NOR Flash memory. This trend is boosting the NOR Flash content per vehicle, aligning with the growing adoption of advanced driver-assistance systems in the automotive sector.

Make in India Smartphone Output Sustains High-Volume Consumption

Smartphone manufacturing value reached USD 75 billion in fiscal 2026, with exports of USD 30 billion. The increasing demand for smartphones has driven the integration of 4-32 Mbit NOR Flash memory in every handset, primarily for boot and radio firmware. This growth is supported by advancements in memory technology, such as GigaDevice’s dual-supply SPI series, which significantly reduces active power consumption. These innovations cater to battery-sensitive subsystems, enhancing energy efficiency and performance. Additionally, the rise in smartphone exports highlights the growing global competitiveness of the sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| No domestic sub-55 nm NOR wafer fabs | -0.9% | Nationwide | Long term (≥ 4 years) |

| High import duties vs South-East Asian hubs | -0.6% | Nationwide | Short term (≤ 2 years) |

| Discrete NOR displaced by multi-chip packages | -0.8% | Smartphones, wearables | Medium term (2-4 years) |

| Supply uncertainty from China-Taiwan geopolitical risk | -0.7% | Automotive, industrial | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Advanced Domestic Fabs Constrains Supply Security

Ten semiconductor ventures cleared under ISM phases are primarily focused on 28 nm logic or compound semiconductors, rather than embedded non-volatile memory. As a result, all sub-55 nm NOR wafers are currently sourced from Taiwan and China, creating a dependency on these regions. This reliance poses a risk, especially during periods of supply chain disruptions or geopolitical tensions. Additionally, a 70% spike in DRAM spot prices during the first quarter of 2026 highlighted how foundry lines often shift priorities during market crunches. Such shifts further exacerbate the challenges for NOR production, leading to extended lead times and constrained supply. This dynamic underscores the vulnerability of the NOR supply chain in the current semiconductor landscape.

Import Tariffs Inflate Memory Costs

While the 2026 Union Budget removed duties on gallium and rare-earth inputs, packaged memory ICs continue to face tariffs that are 8-12 percentage points higher than those in ASEAN countries. This disparity in tariffs places smaller EMS firms at a disadvantage, as they lack the scale to negotiate rebates or absorb additional costs. Consequently, these firms struggle to remain price competitive in export tenders, particularly in markets where cost sensitivity is high. The higher tariffs also discourage domestic manufacturing of memory ICs, further impacting the supply chain. This situation underscores the need for policy adjustments to enhance the global competitiveness of Indian EMS firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serial NOR Dominates Mobile-Driven Market

Serial devices held 62.7% share in 2025 and are projected to outgrow the overall India NOR Flash market. These devices offer significant advantages by reducing board area and pin counts compared to parallel parts. This efficiency is particularly valued in applications such as consumer IoT, automotive control units, and industrial PLCs. The compact design and enhanced functionality of serial products make them a preferred choice for modern applications, driving their adoption across various industries.

Parallel NOR, on the other hand, continues to find use in legacy telecom and avionics backplanes that require 16-bit buses. However, vendors are increasingly positioning Octal serial parts as drop-in upgrades for these systems. Octal serial parts match the 400 MB/s throughput of parallel NOR while significantly reducing the footprint. Companies like Winbond, Macronix, and GigaDevice expanded their Octal portfolios during 2025-2026, providing designers with a seamless migration path to serial technology without compromising on bandwidth.

By Interface: Octal and xSPI Climb as Bandwidth Need Grows

Quad SPI generated 47.6% of interface revenue in 2025. However, Octal and xSPI interfaces are witnessing the fastest growth, driven by JEDEC xSPI 2.0 certification and the increasing demand for high-speed reads of 300-400 MB/s in automotive applications. These advancements are enabling manufacturers to meet the growing need for faster and more efficient memory solutions. The adoption of Octal and xSPI is further supported by their ability to deliver enhanced performance while maintaining compatibility with existing systems.

Leading vendors, such as Infineon with its Semper series and GigaDevice with the GD25LX256E, are integrating xSPI interfaces with features like functional safety and low power consumption. These innovations cater to the evolving requirements of industries like automotive and industrial automation. Meanwhile, Single and Dual SPI interfaces continue to hold relevance in ultra-cost-sensitive applications, such as wearables and sensors, where firmware size remains minimal, and cost efficiency is a priority.

By Density: 128-256 Mbit Segment Accelerates on Edge AI

Mid-range 32-64 Mbit devices continued to dominate in 2025, accounting for 28.7% of the market share. These devices remain a preferred choice due to their balance of cost and performance, catering to a wide range of applications. However, the demand for higher-capacity devices is steadily increasing, driven by advancements in technology and the growing need for efficient data storage solutions. AI co-processors, such as Mindgrove’s V2600, are a key driver of this trend as they require larger model weights to function effectively.

In the defense sector, avionics systems are increasingly procuring radiation-tolerant parts with capacities of 256 Mbit or more. These components are sourced through contracts with Bharat Electronics, addressing the specific needs of high-reliability applications. While this segment represents a low-volume niche, it remains highly profitable due to the premium pricing of specialized components. The demand for such devices is expected to grow as defense systems continue to evolve and require more advanced memory solutions.

By Voltage: 1.8 V Class Wins Designs Aimed at Battery Devices

3V families dominate replacement sales in industrial and automotive sectors, but 1.8 V variants are growing at nearly twice the rate. This rapid growth is driven by the increasing demand for energy-efficient solutions, as designers prioritize reducing standby power consumption. The shift towards 1.8 V variants underscores the industry's commitment to sustainability and innovation, addressing the evolving needs of modern applications. As energy efficiency becomes a critical factor, the adoption of lower voltage variants is expected to continue rising across various markets.

To support this transition, GigaDevice has introduced a dual-supply line that offers significant flexibility to handset manufacturers. This solution enables manufacturers to adopt 1.8 V variants without the need to redesign existing boards that still support 3 V rails. By facilitating seamless integration, GigaDevice helps manufacturers achieve energy efficiency while maintaining compatibility with current infrastructure. This approach not only reduces costs but also accelerates the adoption of advanced, energy-saving technologies in the market.

By End-User Application: Automotive Growth Outstrips Electronics Volume Leader

Consumer electronics accounted for 40.8% of revenue in 2025, driven by strong demand across various devices. However, growth in this segment has slowed to mid-single digits due to the higher base effect. Despite this, the sector remains a significant contributor to the overall market, supported by continuous advancements in technology and increasing consumer adoption of smart devices. The demand for memory components in consumer electronics is expected to remain steady, fueled by the proliferation of IoT devices and wearables.

Automotive demand is projected to grow at a 9.3% CAGR, primarily driven by the adoption of Advanced Driver Assistance Systems (ADAS) and the increasing average memory density per vehicle. This growth reflects the automotive sector's transition towards smarter and more connected vehicles. Meanwhile, industrial automation and communication infrastructure maintain steady replacement cycles, ensuring consistent demand. Additionally, the defense and aerospace sectors, though smaller in scale, contribute high-margin orders for radiation-hardened components, catering to specialized applications.

By Process Node: Sub-28 nm Share Edges Up Despite Offshore Dependence

65 nm wafers accounted for 36.9% of the total output in 2025. However, the adoption of 28 nm and finer nodes is increasing, driven by advancements in edge AI and ADAS technologies. These finer nodes are critical for supporting the growing demand for high-performance and energy-efficient applications across various industries. The shift towards advanced nodes highlights the industry's focus on innovation and the need to meet evolving technological requirements.

Despite this progress, domestic buyers remain dependent on Taiwanese and Chinese foundries for the production of 28 nm and finer nodes. This reliance introduces significant geopolitical and logistical risks, which could impact supply chain stability. The dependence underscores the importance of diversifying supply sources and investing in local manufacturing capabilities to mitigate potential disruptions and ensure long-term resilience in the semiconductor industry.

By Packaging Type: Wafer-Level CSP Surges in Handsets and Wearables

Wafer-level chip-scale packaging (WLCSP) and chip-scale packaging (CSP) accounted for 45.4% of the market share in 2025, driven by the demand for reduced Z-height in smartphones. Ball grid array (BGA) and fine-pitch ball grid array (FBGA) packaging are primarily utilized in high-pin-count automotive infotainment modules, while quad flat no-lead (QFN) and small outline integrated circuit (SOIC) packaging dominate legacy industrial boards. The increasing adoption of advanced packaging technologies is expected to drive growth in these segments during the forecast period.

In response to market demand, Macronix and GigaDevice expanded their WLCSP offerings for new Octal parts during 2025-2026. This expansion aligns with the growing need for compact, efficient packaging solutions across the automotive and industrial sectors. The advancements in packaging technologies are anticipated to enhance performance and reliability, further driving their adoption across multiple industries.

Geography Analysis

Production clusters in Noida, Chennai, and Bengaluru form the backbone of the India NOR Flash market. Gujarat’s Dholera SEZ gained prominence after Micron established its USD 2.75 billion ATMP line in February 2026, which has attracted several ancillary test houses and boosted the region's industrial ecosystem. Tamil Nadu’s automotive corridor drives demand for functional-safety NOR, catering to the growing requirements of the automotive sector. Meanwhile, Karnataka’s aerospace hub focuses on radiation-hardened memory for satellite payloads, aligning with the increasing demand for advanced aerospace technologies. Additionally, Odisha entered the market in April 2026 with plans for a 3D packaging plant, expanding back-end capacity beyond Gujarat and diversifying the country’s manufacturing footprint.

Northern industrial belts maintain consistent demand for 16-64 Mbit parts, particularly in PLCs and optical-network terminals, which are critical for industrial automation and communication networks. However, elevated tariffs continue to hinder export competitiveness when compared to countries like Thailand and Vietnam, which benefit from lower production costs. Despite this challenge, PLI reimbursements have provided partial relief to manufacturers, encouraging continued investment in the region. The reliance on Taiwanese foundries remains a significant concern, as it exposes the supply chain to geopolitical risks and potential disruptions. This dependency highlights the urgent need for diversification and the development of domestic manufacturing capabilities to strengthen the supply chain.

Strategic risk assessments indicate a 9% probability of a Taiwan blockade by mid-2027, which could significantly impact the supply chain and disrupt global markets. Such a scenario underscores the fragility of the current ecosystem and the importance of developing alternative sources to mitigate risks. Investments in domestic manufacturing infrastructure and partnerships with other global players are critical to reducing reliance on a single region. These measures could enhance the resilience of the India NOR Flash market, ensuring sustained growth and stability in the coming years. Proactive steps in this direction will also help the industry adapt to evolving global dynamics and maintain its competitive edge.

The nor flash market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe and Asia, along with detailed country-level analysis for South Korea, China, Italy, Germany, Mexico, France, and United States.

Competitive Landscape

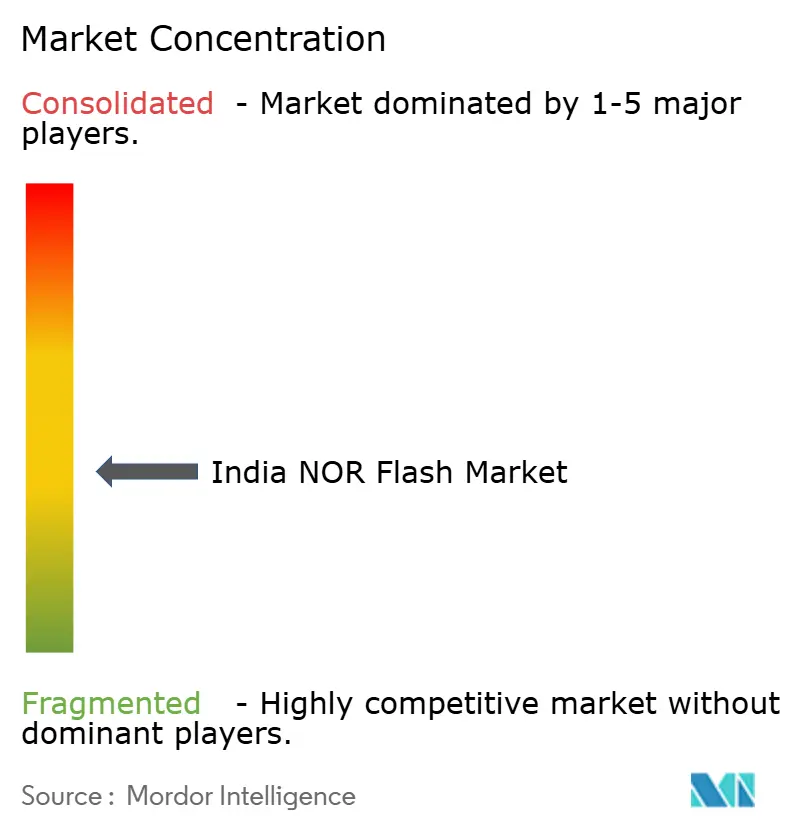

The supplier base in the India NOR Flash market is moderately fragmented. Key players such as Winbond, Macronix, and GigaDevice dominate serial shipments into the country, while Infineon and Micron primarily cater to automotive and industrial channels. Domestic fabless companies like Mindgrove and Netrasemi rely on Taiwan Semiconductor Manufacturing Company for 12 nm and 28 nm tapeouts, integrating NOR Flash blocks into edge-AI SoCs. Price competition is most intense in the consumer electronics segment, where large OEMs dual-source components to reduce bills of material by up to 20%. In contrast, automotive, defense, and aerospace sectors pay 20-30% premiums for ASIL-D or radiation-tolerant grades, which helps vendors maintain healthy margins.

Emerging opportunities in the market include radiation-hardened NOR for satellite avionics and secure-boot devices that support multi-vendor cryptographic roots of trust. Macronix’s ArmorBoot MX76 is well-positioned in this space, offering densities of up to 1 Gb along with dual-supply flexibility. Smaller Chinese suppliers, such as XTX and Longsys, compete aggressively on pricing in the industrial IoT segment. However, their inability to meet automotive certifications limits their market share. These gaps present significant potential for established players to expand their footprint in high-reliability applications.

Despite the competitive landscape, the demand for specialized NOR Flash solutions continues to grow. Segments like automotive and aerospace are driving the need for advanced memory solutions with enhanced safety and reliability features. Meanwhile, consumer electronics remain a price-sensitive market, pushing suppliers to innovate while maintaining cost efficiency. As the market evolves, strategic investments in R&D and partnerships with global foundries will be critical for suppliers to address emerging requirements and sustain growth in the coming years.

India NOR Flash Industry Leaders

Micron Technology Inc.

Winbond Electronics Corp.

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Bharat Electronics received Rs 6,795 crore (USD 815 million) in avionics and electronic warfare orders, boosting demand for radiation-hardened NOR Flash.

- April 2026: Odisha launched a 3D packaging unit, aiming to boost its domestic ATMP capacity.

- March 2026: Bharat Electronics and SASMOS HET agreed to co-develop defense sub-systems that integrate serial NOR for secure boot.

- February 2026: Micron inaugurated a USD 2.75 billion ATMP plant in Sanand, Gujarat.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the India NOR flash memory market as the annual revenue earned from brand-new serial and parallel NOR flash integrated circuits that are designed into consumer electronics, communication gear, automobiles, and industrial controllers. Only chips that are shipped into India or produced domestically and then sold to first-fit board assemblers are counted; aftermarket resales are outside scope.

Scope exclusion: devices based on NAND flash, DRAM, removable cards, and second-hand components are excluded.

Segmentation Overview

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Mbit and Less NOR

- More than 2-4 Mbit NOR

- More than 4-8 Mbit NOR

- More than 8-16 Mbit NOR

- More than16-32 Mbit NOR

- More than 32-64 Mbit NOR

- More than 64-128 Mbit NOR

- More than 128-256 Mbit NOR

- Greater than 256 Mbit NOR

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Others -1.2 V Class and Similar

- By End-user Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-user Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (incl. 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed memory controllers' design leads, contract manufacturers in Noida and Bengaluru, distributors that serve Tier-1 handset OEMs, and procurement heads at automotive ECU makers. Conversations across western, northern, and southern clusters validated density preferences, average selling prices, and forecast adoption of Octal SPI parts, filling gaps that desk work left.

Desk Research

We began with ministry datasets and tariff books (DGFT schedule 854232) that track byte-addressable memory imports, then reviewed Directorate General of Commercial Intelligence & Statistics shipment values, and the MeitY production-linked-incentive filings that disclose local output. Public trade association dashboards from the India Cellular & Electronics Association and SIAM helped us gauge handset and vehicle controller demand. Wider context was drawn from semiconductor outlook notes issued by the Semiconductor Industry Association, patent activity retrieved via Questel, and company 10-K filings. These examples illustrate the tier-one, non-paywalled and paid databases we tapped; many additional sources informed granular checks.

Market-Sizing & Forecasting

A top-down reconstruction that aligns import plus domestic production values with average device price points produced the 2025 baseline. Results were cross-checked through bottom-up supplier roll-ups for five leading vendors, giving us confidence to adjust for grey-market leakage. Key variables include handset PCB shipments, small-cell base-station roll-outs, density mix shifts toward ≥256 Mbit parts, automotive ECU counts, and the rupee-denominated ASP contraction curve. A multivariate regression blended with an ARIMA overlay projects each driver to 2030; scenario analysis tests currency and policy shocks before the model is frozen. Where supplier disclosures were incomplete, calibrated ratios from primary interviews bridged gaps.

Data Validation & Update Cycle

Every model pass is stress-tested against WSTS memory indices and monthly customs tallies. Senior reviewers rerun anomaly filters, and any variance above three percentage points triggers re-contact of domain experts. Reports refresh once a year, with interim patches after material events such as policy tweaks or fabs coming online.

Why Mordor's India NOR Flash Baseline Commands Confidence

Published numbers often differ because researchers pick dissimilar geographies, broader memory mixes, or optimistic price trajectories. Our disciplined scoping and annual refresh cadence temper those swings.

Key gap drivers include competitor studies that merge NAND and NOR, rely on extrapolated global ratios without import reconciliation, or apply single-point ASP declines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 85.15 million (2025) | Mordor Intelligence | - |

| USD 35 billion; Asia-Pacific flash memory (2024) | Regional Consultancy A | Combines NAND & NOR across 14 countries; no customs validation |

| USD 4.2 billion; global NOR flash (2022) | Trade Journal B | Global scope, older year, relies on vendor press releases without density split |

Taken together, the comparison shows that Mordor's narrowly defined, India-only baseline, grounded in traceable shipment data and cross-examined with industry interviews, offers decision-makers a balanced figure they can reliably build plans upon.

Key Questions Answered in the Report

What is the current India NOR Flash market size and projected growth?

The market stood at USD 91.03 million in 2026 and is projected to reach USD 127.07 million by 2031, expanding at a 6.9% CAGR according to Mordor Intelligence.

Which application segment is growing fastest?

Automotive electronics is the fastest-growing segment with a forecast 9.3% CAGR through 2031, propelled by local ADAS ECU production.

How are secure-boot mandates influencing product design?

Bureau of Indian Standards rules force IoT and smart-meter OEMs to adopt dedicated NOR Flash that supports cryptographic authentication, boosting demand for secure-boot families such as ArmorBoot MX76.

Why are Octal and xSPI interfaces gaining share?

Octal and xSPI meet 300-400 MB/s bandwidth targets needed for over-the-air firmware updates in ADAS and industrial edge AI, encouraging designers to shift away from Quad SPI.

What supply-chain risks do Indian buyers face?

India lacks sub-55 nm NOR fabs, so buyers rely on Taiwanese and Chinese foundries, exposing them to tariff costs and geopolitical disruptions.

Page last updated on: