United Kingdom NOR Flash Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

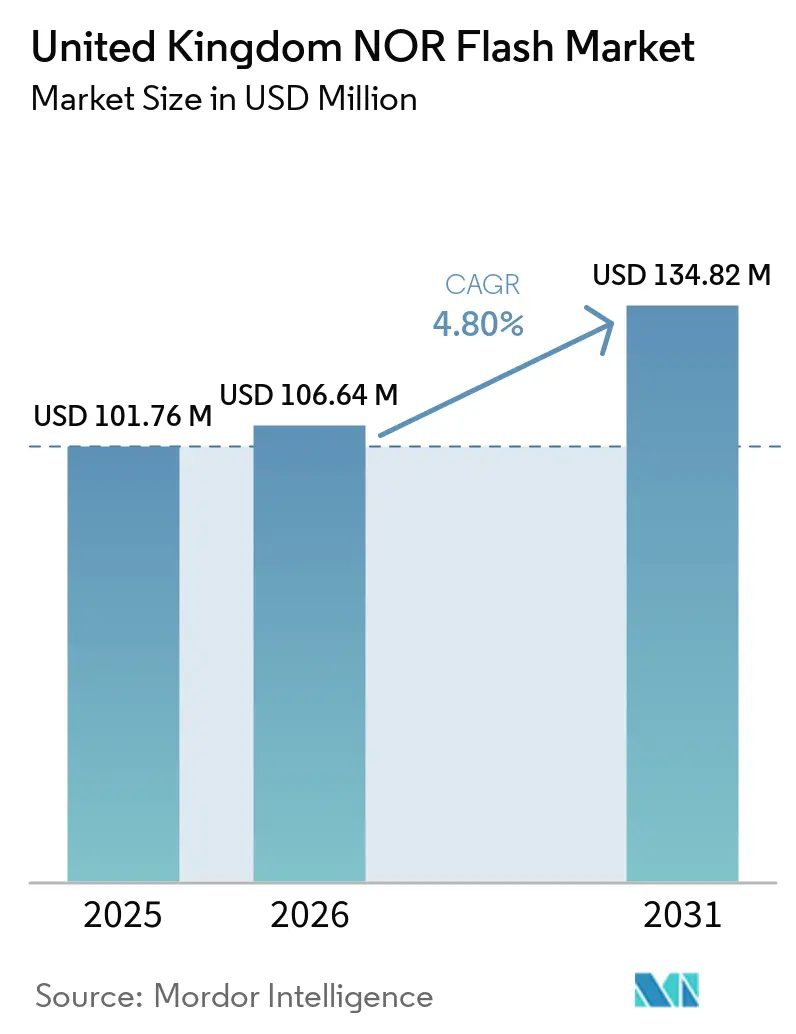

| Base Year Market Size (2025) | USD 101.76 Million |

| Market Size (2026) | USD 106.64 Million |

| Market Size (2031) | USD 134.82 Million |

| Growth Rate (2026 - 2031) | 4.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom NOR Flash Market Analysis by Mordor Intelligence

The United Kingdom NOR Flash market size is expected to increase from USD 106.64 million in 2026 to USD 134.82 million by 2031, growing at a CAGR of 4.8% over 2026-2031. Steady headline growth hides a rapid shift toward higher-bandwidth serial parts that serve automotive automation, 5G-plus telecom gear, and smart-meter roll-outs. Domestic design activity receives policy backing through the GBP 1 billion (USD 1.28 billion) Semiconductor Strategy, though United Kingdom NOR Flash market participants still depend on offshore sub-65 nm foundries for volume supply. Interface migration from quad SPI toward octal and xSPI, density migration into the 128 Mb band, and the rapid uptake of sub-1.8 V parts together reshape demand, while lead times of up to 24 weeks sustain seller pricing power. Key structural forces reinforce the medium-term outlook. Automotive applications delivered 29.7% of 2025 revenue and will advance at 7.7% through 2031 as zonal architectures add up to 15 NOR sockets per premium electric vehicle. Telecom operators have ring-fenced GBP 700 million (USD 889 million) to accelerate 5G-plus roll-outs and base-station upgrades, locking in a multi-year pipeline for instant-boot code storage. The mandatory smart-meter program, already past two-thirds coverage, guarantees tens of millions of 8-16 Mb devices, while defense programs such as Skynet 6 and Tempest drive long-tail demand for radiation-hardened parts. Supply risk remains the standout restraint as the country runs only legacy fabs and must navigate Brexit-induced certification friction that bloats inventory.

Key Report Takeaways

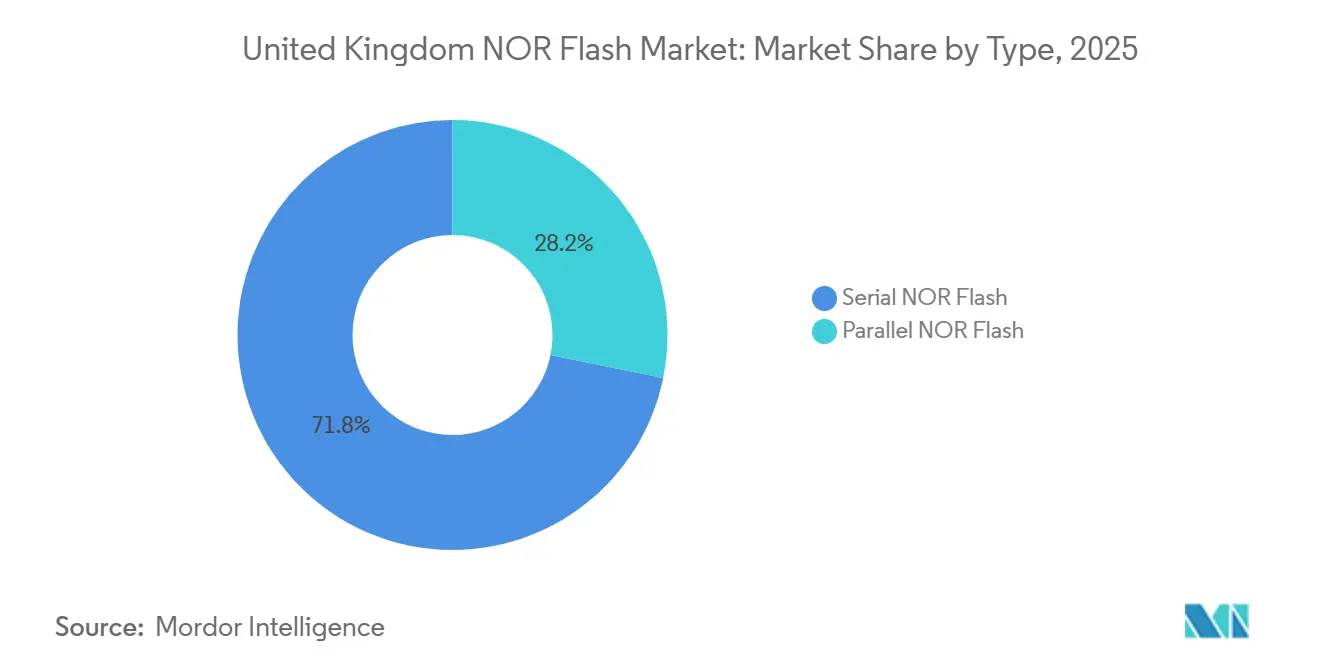

- By type, serial architectures held 71.8% of the United Kingdom NOR Flash market share in 2025 and are on course for a 7.5% CAGR through 2031 as octal and xSPI parts displace parallel devices.

- By interface, quad SPI delivered 43.2% of 2025 revenue, but octal and xSPI variants represent the fastest trajectory at 9.7% through 2031, meeting automotive and edge-AI bandwidth budgets.

- By density, the 16 Megabit and Less (More than 8 Mb) tier captured 21.1% of the 2025 value, while the 128 Megabit and Less (More than 64 Mb) band is projected to expand at 7.3% as firmware images and neural-network weights grow.

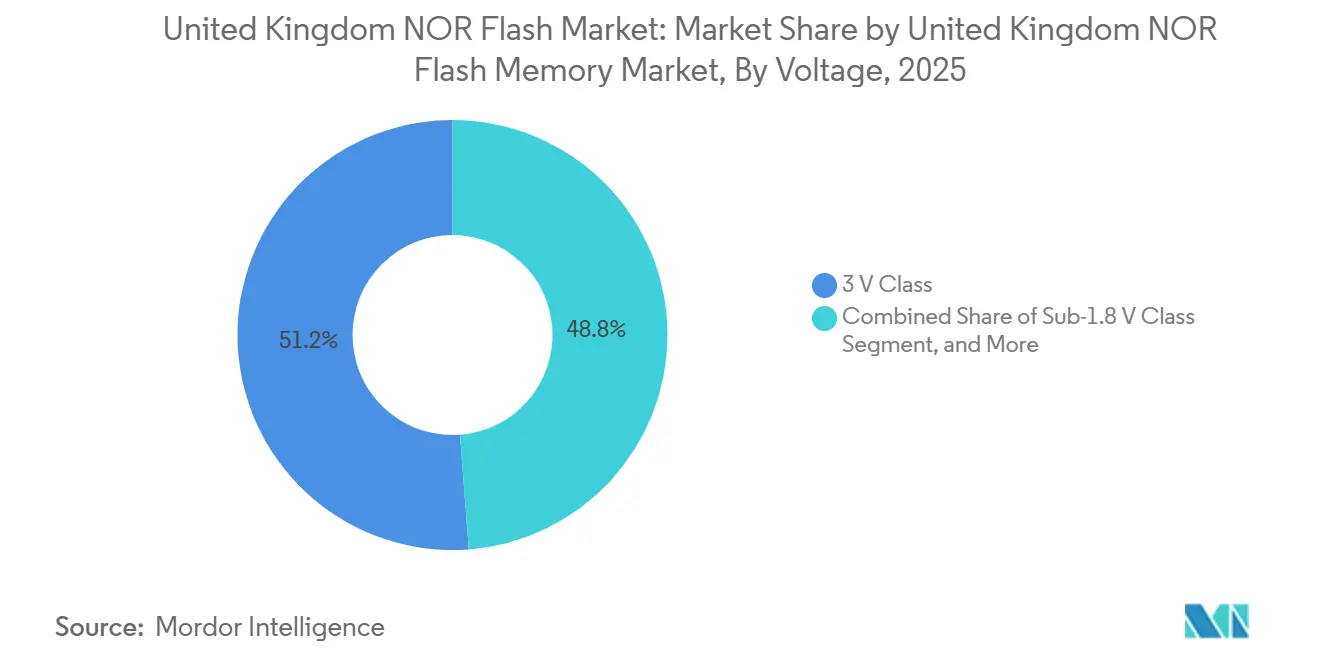

- By voltage, 3 V-class devices commanded 51.2% in 2025, yet sub-1.8 V parts post an 8.8% CAGR to 2031, tracking the migration to low-power microcontrollers.

- By end-user, automotive applications led with 29.7% revenue in 2025 and will keep a 7.7% growth clip, far above the overall United Kingdom NOR Flash market.

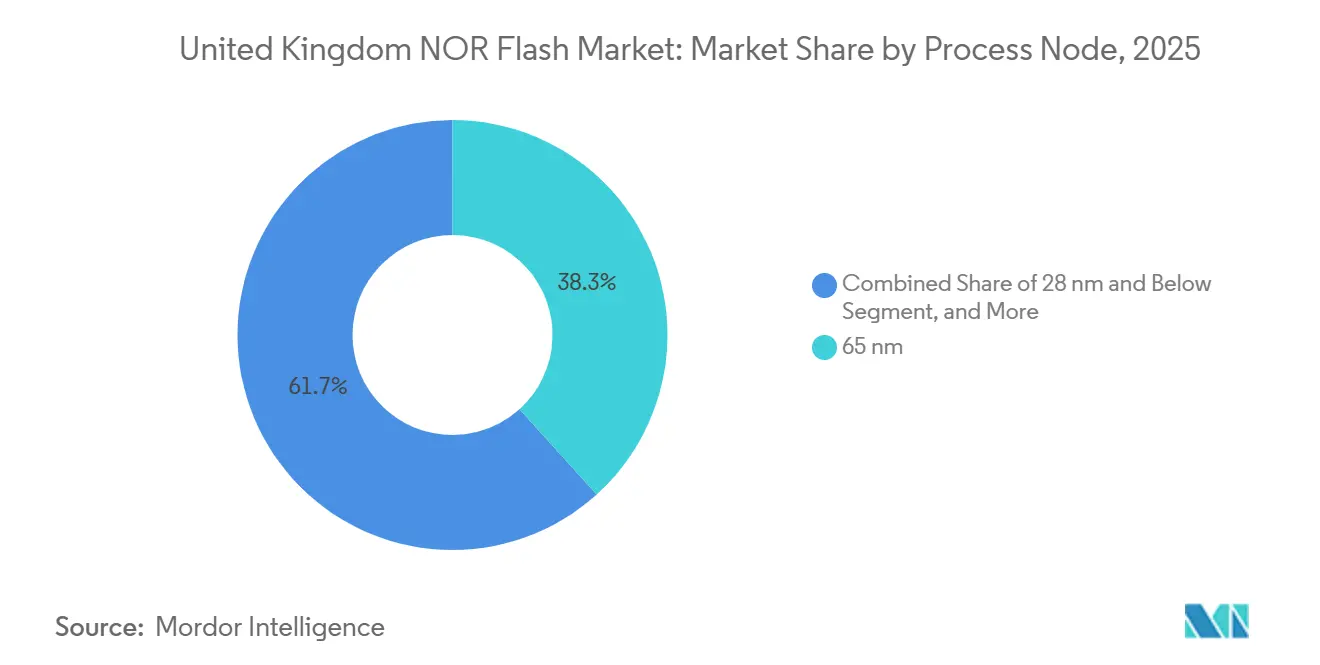

- By process technology node, 65 nm supplied 38.3% of 2025 revenue, but the 28 nm-and-below cohort shows an 8.4% advance as embedded-flash MCUs internalize code storage.

- By packaging type, BGA / FBGA led with 40.8% revenue in 2025 and while the WLCSP / CSP keep a 6.7% growth clip, far above the overall United Kingdom NOR Flash market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United kingdom holds a defined position within a broader international distribution. The nor flash market share data by Mordor Intelligence maps that allocation across all contributing countries and regions, globally.

United Kingdom NOR Flash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of ADAS and EV Platforms by UK OEMs Requiring Instant-Boot | +1.5% | National, automotive hubs | Long term (≥ 4 years) |

| 5G Infrastructure Roll-Out Accelerating Demand for High-Reliability Code Storage in Telecom Gear | +1.2% | National, urban clusters | Medium term (2-4 years) |

| Expansion of Smart Metering and IoT Deployments Under UK Net-Zero Mandate | +0.9% | National, utilities | Medium term (2-4 years) |

| Shift Toward Octal/xSPI Architectures in Edge-AI Modules Manufactured in the UK | +0.8% | National, industrial sites | Short term (≤ 2 years) |

| Semiconductor Design Tax Incentives (UK Semiconductor Strategy 2023) Boosting Local Prototyping | +0.6% | National, semiconductor R&D clusters | Medium term (2-4 years) |

| Defense Modernisation Programmes (Tempest, Skynet 6) Increasing Secure NOR Flash Uptake | +0.5% | National, aerospace and defense corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of ADAS and EV Platforms by UK OEMs Requiring Instant-Boot

Automotive designs now embrace zonal controllers, digital clusters, and ADAS stacks that run safety-critical code from execute-in-place memory. Infineon’s ASIL-D qualified SEMPER line and Winbond’s W35T octal family headline the approved device roster, enabling 400 MB/s read bandwidth within -40 °C to +125 °C envelopes.[1]Infineon Technologies, “SEMPER NOR Flash Family Achieves ASIL-D Certification,” infineon.com Jaguar Land Rover’s mid-2026 production halt over missing flash parts underlined supply fragility, prompting OEMs to dual-source and raise buffer stock. Zone-based EV platforms can host 10-15 discrete NOR sockets, more than triple legacy counts, making automotive the single largest growth lever for the United Kingdom NOR Flash market.

5G Infrastructure Roll-Out Accelerating Demand for High-Reliability Code Storage in Telecom Gear

Virgin Media O2’s GBP 700 million (USD 889 million) upgrade budget with Ericsson and Nokia, and Vodafone-Three’s 99% SA coverage pledge create a multi-year base-station build-out pipeline. Each radio unit embeds 64-256 Mb NOR for boot code and patch storage that survives harsh outdoor duty cycles. Regulatory backlogs around 6,200 pending tower approvals delay installations but extend procurement visibility, benefiting code-storage suppliers serving the United Kingdom NOR Flash market.

Expansion of Smart Metering and IoT Deployments Under UK Net-Zero Mandate

Smart-meter install counts hit 41 million by December 2025 and must reach 100% by 2030, sustaining a 350,000-unit monthly run rate.[2]Ofgem, “Smart Meter Statistics: December 2025,” ofgem.gov.uk Second-generation meters rely on dual-bank 8-16 Mb serial NOR to host secure bootloaders and LTE-M upgrade images. A 2026 policy imposes a 90-day fix window for non-operating meters, driving utilities to adopt over-the-air update flows that need fail-safe memory. Industrial IoT gateways and building-automation sensors mirror these requirements, widening the addressable United Kingdom NOR Flash market.

Shift Toward Octal/xSPI Architectures in Edge-AI Modules Manufactured in the UK

Edge inference accelerators and domain controllers increasingly call for 200 MB/s-plus read streams. JEDEC xSPI 2.0 compliant parts from Infineon and GigaDevice meet the need, halving latency versus quad SPI and unlocking concurrent erase-read operations.[3]GigaDevice Semiconductor, “GD25NX Series xSPI NOR Flash Launch,” gigadevice.com Domestic design houses in Cambridge and Bristol already prototype xSPI boards for autonomous mobile robots, reinforcing early-cycle demand inside the United Kingdom NOR Flash market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Domestic Wafer-Fab Capacity Leading to Supply-Chain Vulnerability | -1.3% | National, with dependency on European and Asian foundries | Medium term (2-4 years) |

| Rising Competitiveness of Low-Cost eMMC and High-Density NAND Solutions | -0.9% | National, with pressure in consumer electronics and data-logging applications | Short term (≤ 2 years) |

| High Photolithography Tooling Costs at ≤28 nm Nodes | -0.5% | Global, affecting UK-based design houses and fabless companies | Long term (≥ 4 years) |

| Brexit-Induced Regulatory Complexity for Cross-Border Semiconductor Trade | -0.7% | National, with friction at UK-EU border | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Wafer-Fab Capacity Leading to Supply-Chain Vulnerability

About 25 fabs in the UK continue to operate with geometries exceeding 180 nm, leading buyers to rely on imports for every advanced NOR part. The lack of domestic production capacity for advanced NOR Flash components has created a significant dependency on external suppliers. Offshore bottlenecks have further exacerbated the situation, with lead times for automotive-grade parts extending to 24 weeks in 2026. This has forced OEMs to maintain a safety stock for four months to mitigate supply chain disruptions. Meanwhile, an upgrade in Newport, costing GBP 250 million (USD 320 million), is focusing on SiC power instead of memory production. Consequently, the NOR Flash market in the UK remains structurally exposed to external shocks.

Rising Competitiveness of Low-Cost eMMC and High-Density NAND Solutions

Embedded MMC now delivers 400 MB/s and up to 256 GB, offering a cost-effective alternative to NOR in applications like infotainment and data-logging due to its lower cost per gigabyte. The introduction of next-generation UFS technology, which achieves speeds of up to 4,640 MB/s, is further diminishing NOR’s market share in scenarios where execute-in-place functionality is not critical. In response, NOR suppliers are introducing secure-boot NOR products exceeding 512 Mb and power-efficient 1.2 V parts to address specific market needs. However, despite these advancements, the significant price gap between NOR and its alternatives continues to pose challenges. This price disparity is particularly impacting segments of the United Kingdom NOR Flash market, where cost sensitivity is a key factor. As a result, NOR suppliers face increasing pressure to innovate and remain competitive in this evolving landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serial Architectures Dominate on Pin-Count Efficiency

In 2025, serial devices claimed a dominant 71.8% share of the United Kingdom's NOR Flash market. This dominance is attributed to the efficiency of quad and octal buses, which have significantly reduced PCB area while maintaining first-byte latency. Parallel NOR continues to play a critical role in avionics and defense applications due to its deterministic sub-10 ns access. However, its market share is projected to decline as serial bandwidth reaches 400 MB/s, offering a competitive alternative. Additionally, advancements in packaging, particularly the transition to WLCSP, are further embedding serial NOR in emerging applications. These include wearables and IoT nodes, where compact and efficient designs are increasingly prioritized.[4]Macronix International, “Macronix Restarts NT$22 Billion Capex for NOR Flash Expansion,” macronix.com

These trends are further bolstered by secondary effects that amplify the advantages of serial technology. Automotive designers are leveraging board savings by routing single-ended serial lines through compact harnesses, which simplifies design and reduces costs. At the same time, industrial OEMs are favoring serial NOR due to its lower component count, which proves advantageous during EMC compliance testing. These preferences are driving the adoption of serial technology in new designs across multiple industries. As a result, the United Kingdom's NOR Flash market is increasingly leaning towards high-speed SPI ecosystems. This shift underscores the growing importance of serial NOR in meeting the demands of modern applications.

By Interface: Octal and xSPI Surge on Bandwidth Demands

In 2025, Quad SPI accounted for 43.2% of the revenue, while octal and xSPI interfaces are projected to grow at a rate of 9.7% through 2031. This growth is primarily driven by the increasing demand from ADAS domain controllers, which require read streams exceeding 200 MB/s to function efficiently. Octal devices offer significant advantages, including a 40% reduction in random-access latency compared to quad counterparts, making them a preferred choice for advanced applications. Additionally, these devices support simultaneous bank operations, a critical feature for enabling seamless over-the-air updates. Despite these benefits, the adoption of octal and xSPI interfaces has been slower due to their dependence on microcontroller refresh cycles. However, Tier-1 automotive suppliers are already validating xSPI memory stacks, targeting their integration into 2027 launch programs.

Legacy single and dual SPI components continue to play a role in cost-sensitive sectors, such as consumer electronics and utility meters, where affordability is a key consideration. These components contribute to market volume but offer limited potential for value growth due to their outdated technology. The transition to octal interfaces is being accelerated by software toolchains that abstract differences in bus width, simplifying the migration process for manufacturers. As a result, octal interfaces are expected to become the default boot path in next-generation designs, particularly in the UK NOR Flash market. This shift reflects the growing need for higher performance and reliability in modern applications, which legacy SPI components cannot adequately address. The adoption of octal technology is poised to redefine the market landscape, ensuring compatibility with evolving design requirements.

By Density: Mid-Range Tiers Lead, High-Density Segments Accelerate

In 2025, the 16-Megabit-and-Less (More than 8 Mb) band accounted for 21.1% of spending, driven by the increasing demand for embedded controllers in industrial and smart-energy meters. These controllers are critical for enabling efficient operations and energy management in these applications. However, the growth trajectory is shifting towards the 128 Megabit and Less (More than 64 Mb) tier, which is projected to grow at a rate of 7.3% during the same period. This growth is primarily attributed to the rising adoption of EV gateways, which require larger firmware and AI weight caches to support advanced functionalities. Macronix's ArmorBoot components, ranging from 512 Mb to 2 GB, are playing a pivotal role by providing secure-boot solutions for cybersecurity-regulated assets. This development is pushing NOR Flash into application spaces that were previously dominated by NAND technology.

Low-end 2 Mb and smaller densities continue to find applications in power-management ICs, where their compact size and efficiency are advantageous. However, the economics of shrinking die sizes are gradually making these smaller geometries less viable for suppliers, leading to a reduction in their production. On the other hand, advancements at the higher end of the spectrum are opening new opportunities. The introduction of stacked 3D NOR technology is enabling the development of single-chip 4 Gb devices. These devices are well-suited for infotainment systems and edge-AI workloads, which demand high performance and reliability. This technological progress is significantly expanding the growth potential of the NOR Flash market in the United Kingdom, positioning it to meet the evolving demands of advanced applications.

By Voltage: Sub-1.8 V Class Gains on Power Budgets

In 2025, three-volt components held a dominant 51.2% share, reflecting the established industrial base and its widespread adoption across various applications. This dominance highlights the continued reliance on legacy systems and the compatibility of three-volt parts with existing infrastructure. However, devices operating below 1.8 volts are projected to grow at a robust rate of 8.8% through 2031. This growth is primarily driven by the increasing demand for battery-powered IoT devices and wearable technologies, which require lower power consumption. Additionally, dual-voltage designs, such as the GigaDevice GD25NX, are gaining traction as they allow developers to utilize a shared MCU core rail. By eliminating the need for an LDO, these designs help save board space and improve overall system efficiency.

Switching to lower voltages proves advantageous for energy efficiency and device longevity. Reducing voltage by half can significantly cut dynamic energy consumption to a quarter, enabling designers to extend the operational life of devices without requiring larger batteries. This shift is particularly relevant as energy efficiency becomes a critical factor in modern electronics. As microcontroller manufacturers solidify their focus on 1.2-volt roadmaps, the adoption of sub-1.8-volt NOR flash memory is expected to accelerate. This technology is poised to underpin the next wave of energy-efficient endpoints, particularly in the United Kingdom's NOR Flash market. The combination of lower power consumption and enhanced performance positions sub-1.8-volt NOR flash as a key enabler for the future of low-energy devices.

By End-User Application: Automotive Leads Growth, Industrial Anchors Volume

In 2025, the automotive sector accounted for 29.7% of revenue and is projected to grow at 7.7%, driven by advancements in zonal controllers, sensor-fusion units, and secure gateways. These technologies are enhancing vehicle safety, connectivity, and efficiency, contributing to the sector's expansion. The industrial and energy sectors remain key contributors, supported by mandatory smart meter adoption and programmable logic upgrades in factories, which improve operational efficiency. The communication sector benefits from 5G densification, enabling faster and more reliable connectivity. However, the consumer electronics sector faces margin pressures despite steady supply throughput, primarily due to competition from NAND alternatives, which offer cost-effective storage solutions.

Medical, aerospace, and defense sectors maintain niche yet premium markets, driven by specialized requirements and long-term contracts. These sectors rely on radiation tolerance and 15-year supply agreements, ensuring consistent demand and high average selling prices (ASPs). The medical sector benefits from advancements in imaging and diagnostic equipment, while aerospace and defense focus on mission-critical applications. These factors sustain profitability and reinforce the margin profile for vendors in the UK NOR Flash market, specifically. The combination of technological innovation and long-term partnerships positions these sectors as high-value contributors to the market.

By Process Technology Node: Advanced Nodes Gain on Density and Performance

In 2025, the 65 nm node accounted for 38.3% of total revenue, primarily driven by the economic yields from the 256 Mb class serial NOR. This node has proven to be a cost-effective solution for delivering reliable performance in the NOR Flash market. The transition towards 28 nm embedded flash is accelerating as UMC and SST have validated its capabilities, including 12.5 ns read times and a 100k-cycle endurance on SuperFlash Gen 4. These advancements are meeting the growing demand for faster and more durable memory solutions. In the United Kingdom NOR Flash market, the high costs associated with extreme-ultraviolet tooling are restricting new foundry entrants. This limitation is tightening supply and extending lead times, but it also ensures that higher-density parts command premium pricing, benefiting existing players in the market.

Above 90 nm lines remain operational, catering to radiation-hardened variants and fulfilling defense-related commitments. This demonstrates the dual-track approach to process adoption within the industry. Cutting-edge technologies are being utilized to meet the increasing demand for higher bandwidth and performance. At the same time, mature processes like the 90 nm node are being retained for applications requiring longevity and reliability. This balance allows manufacturers to address diverse market needs effectively. The continued use of older nodes highlights their importance in specialized applications, ensuring that both innovation and legacy processes coexist within the NOR Flash market.

By Packaging Type: BGA Leads, WLCSP Gains on Miniaturization

In 2025, BGA and FBGA formats commanded a 40.8% market share, primarily due to their vibration-resilient solder joints, which are highly valued in automotive and industrial sectors. These formats are particularly suited for applications requiring durability under harsh conditions, making them a preferred choice in these industries. Meanwhile, WLCSP shipment units are projected to grow at a rate of 6.7%, driven by the increasing demand for sub-0.6 mm Z-height in compact devices like fitness trackers and hearables. The trend toward miniaturization aligns with the growing wearables design community in Cambridge, which is fostering innovation in this space. This development is significantly boosting the miniature segment of the United Kingdom's NOR Flash market.[5]Renesas Electronics, “AT25SL128A 21-Ball WLCSP Datasheet,” renesas.com The convergence of these factors underscores the evolving dynamics of the semiconductor packaging market in the region.

Traditional SOIC and QFN formats continue to play a vital role in serving through-hole repairable boards, particularly in utility applications where reliability and ease of repair are critical. These formats remain relevant for specific use cases despite the ongoing shift toward miniaturization in consumer devices. However, as consumer electronics increasingly demand smaller and more efficient components, wafer-level packages are expected to gain a larger incremental share in the market. This shift reflects the growing preference for advanced packaging solutions that cater to the shrinking form factors of modern devices. The transition highlights the industry's focus on innovation to meet the evolving needs of end-users while maintaining compatibility with legacy systems where necessary.

Geography Analysis

England, supported by the West Midlands auto cluster and telecom deployments centered in London, dominates the demand for NOR Flash in the United Kingdom. Automotive leaders Jaguar Land Rover, Nissan Sunderland, and LEVC Coventry are driving this growth by expanding their electric vehicle production lines, which significantly increases the number of devices required per vehicle. This automotive pull has positioned England as a key player in the market. Additionally, Scotland strengthens its presence in the aerospace and defense sectors through Skynet ground stations and Tempest R&D initiatives, which generate demand for specialized, radiation-hardened Flash memory to meet stringent industry requirements.

Wales, while hosting a significant SiC expansion in Newport, remains primarily a memory-import zone, with limited local production capabilities. Northern Ireland, on the other hand, is gradually adopting smart meters and IoT gateways across its industrial estates, albeit at a slower pace compared to other regions. A common challenge across all regions is the reliance on offshore fabrication facilities, which has been further complicated by Brexit. The introduction of dual certification requirements has increased logistics costs, prompting distributors, particularly around London Heathrow's semiconductor hub, to maintain larger inventory buffers to mitigate supply chain disruptions.

Metropolitan councils' moratoria on 5G tower installations have slowed the drawdown of units, but this has extended the purchasing window for high-reliability memory products. Concurrently, the nationwide transition from 2G and 3G networks to LTE-M modules has created a demand for upgrades that embed serial NOR Flash. This transition ensures that all regions actively participate in the replacement cycle, which is a critical factor sustaining the United Kingdom's NOR Flash market. These developments highlight the dynamic interplay of regional factors and technological advancements shaping the market's trajectory.

Mordor Intelligence delivers a comprehensive view of the nor flash market across all major regions such as Europe and Asia, alongside country-level analysis for France, Italy, China, India, Japan, South Korea, and Germany, each offering a view of the local market realities.

Competitive Landscape

Five global suppliers dominate the competition in the United Kingdom's NOR Flash market. Winbond, with a 27% global share, led the 2025 serial segment and is bolstering its capacity through a USD 1.35 billion expansion. However, this capacity increase is projected to ease shortages only by mid-2027. GigaDevice, leveraging rapid octal roll-outs, secured the second position with a 23% market share. Macronix, holding 16%, is doubling down on 3D NOR technology to advance to 4 Gb devices. Infineon, with its SEMPER brand recognized for its functional safety pedigree, rounds out the top tier of suppliers in this competitive market.

The UK NOR Flash market is moderately fragmented. Smaller players, such as Puya and Elite Semiconductor, are focusing on cost-sensitive markets but face challenges due to the lack of automotive certifications. This limitation restricts their access to the most profitable accounts in the industry. To remain competitive, these companies are prioritizing strategic initiatives, including ASIL-D qualification, xSPI enablement, and secure-boot IP integration. Additionally, they are targeting defense programs with radiation-hard variants and addressing the growing demand for net-zero IoT nodes with dual-voltage low-power components. These efforts aim to carve out a niche in a market dominated by larger players.

Despite tight supply conditions, price discipline remains a key characteristic of the market. The ongoing supply constraints have created sell-out conditions over the past two years, putting pressure on manufacturers and suppliers. However, the capex cycle projected for 2026 to 2028 offers a glimmer of hope for incremental easing of these conditions. This anticipated easing is expected to gradually balance supply and demand, providing some relief to the market. Until then, the industry continues to navigate challenges while preparing for future growth opportunities.

United Kingdom NOR Flash Industry Leaders

Infineon Technologies AG (Cypress)

Micron Technology Inc.

Winbond Electronics Corp.

Macronix International Co. Ltd.

GigaDevice Semiconductor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: National Semiconductor Infrastructure Initiative released GBP 6.6 million (USD 8.4 million) across 12 design and prototyping projects.

- February 2026: Winbond unveiled a USD 1.35 billion capacity expansion aimed at serial NOR and specialty DRAM lines.

- February 2026: Macronix restarted NTD 22 billion (USD 704 million) capex to accelerate 3D NOR mass production.

- January 2026: UMC and SST secured AG1 automotive grade for 28 nm SuperFlash Gen 4 embedded flash.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom NOR flash memory market as revenue generated within the country from new NOR-architecture non-volatile memory chips, whether discrete packages or die embedded in microcontrollers, that enable execute-in-place code storage across consumer, communication, industrial, and automotive electronics. Values are reported in USD at factory-gate equivalence.

Demand for NAND flash, DRAM, SRAM, or other storage technologies remains outside this assessment.

Segmentation Overview

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit and Less (More than 2 Mb)

- 8 Megabit and Less (More than 4 Mb)

- 16 Megabit and Less (More than 8 Mb)

- 32 Megabit and Less (More than 16 Mb)

- 64 Megabit and Less (More than 32 Mb)

- 128 Megabit and Less (More than 64 Mb)

- 256 Megabit and Less (More than 128 Mb)

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Sub-1.8 V Class (1.2 V, 2.5 V, 5 V)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial and Energy

- Other Applications

- By Process Technology Node (Value)

- 90 nm and Above

- 65 nm

- 55 nm

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed UK-based component distributors, European wafer-fab managers, and engineering leads at Tier 1 automotive electronics suppliers. They then surveyed embedded-systems designers across London, Cambridge, and Midlands clusters. These conversations clarified real-world density preferences, demand seasonality, and ASP variance that secondary sources could not reveal.

Desk Research

We began with United Kingdom import-export codes from HMRC, shipment data collated in Volza, and production benchmarks released by the World Semiconductor Trade Statistics program. These hard numbers were blended with device tear-down surveys from IFixit, technology roadmaps published by the UK National Semiconductor Strategy, and patent volumes mined through Questel to map density and node migrations.

Annual reports filed by key memory vendors, audited statements in D&B Hoovers, and press coverage aggregated via Dow Jones Factiva provided average selling prices, capacity expansions, and channel mix insights that desk sources alone rarely align on. The references listed are illustrative; our analysts reviewed many additional open and paid datasets to cross-check every metric.

Market-Sizing & Forecasting

A top-down reconstruction built from HMRC trade values, UK fab output, and commodity ASP trajectories sets the initial 2024 base. Results are corroborated with selective bottom-up checks, sampled distributor sell-thru, board-level bill-of-materials audits, and limited supplier roll-ups to adjust totals where channel leakage appears. Key variables inside the model include: 5G base-station roll-out counts, new-car production and average NOR per vehicle ECU, annual shipments of smart meters, average node migration-driven die size shrink, and price elasticity when densities shift from 32 Mbit to 64 Mbit. A multivariate regression projecting these drivers under three macro scenarios extends the forecast to 2030. Where granular bottom-up inputs are patchy, bridge factors, such as MCU attach-rate trends, align segment splits with the verified top-line.

Data Validation & Update Cycle

Before sign-off, separate analyst pairs run variance checks against WSTS Europe totals, monitor sudden ASP swings, and rerun sensitivity tests. The report refreshes yearly, and an interim update is triggered if trade data or regulatory action moves quarterly volumes by more than five percent.

Why Our United Kingdom NOR Flash Baseline Commands Confidence

Published estimates often diverge because each firm chooses its own geographic boundary, product mix, and forecast cadence.

Key gap drivers here include whether embedded die inside MCUs are counted, if serial sub-types alone are reported, currency year selections, and how frequently average selling prices are refreshed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 101.76 M (2025) | Mordor Intelligence | - |

| USD 302.4 M (2024) | Regional Consultancy A | Includes only serial devices yet applies global ASPs and counts contract manufacturing shipped to UK OEMs abroad |

| USD 568 M (2021, Europe) | Trade Journal B | Uses broader regional scope and historic year, inflating comparison base |

| USD 800 M (2023, Europe) | Global Consultancy C | Combines NOR with small-density NAND and reports continental total rather than country view |

Taken together, the spread shows how scope choices and price assumptions, not fundamental demand, explain most variance. By anchoring values to verified UK customs data, recent vendor ASP disclosures, and device-level density demand, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can retrace and regularly update.

Key Questions Answered in the Report

What is the current size of the United Kingdom NOR Flash market?

The United Kingdom NOR Flash market size stands at USD 106.64 million in 2026 and is forecast to reach USD 134.82 million by 2031, according to Mordor Intelligence.

Which segment is growing fastest within United Kingdom NOR Flash demand?

Octal and xSPI serial interfaces are the fastest, advancing at a 9.7% CAGR as automotive and edge-AI systems require over 200 MB/s code-read bandwidth.

Why does automotive dominate United Kingdom NOR Flash growth?

Zonal architectures, digital cockpits and ADAS platforms multiply NOR sockets per vehicle, pushing automotive revenue to a projected 7.7% CAGR through 2031.

How will domestic policy affect supply security?

The GBP 1 billion (USD 1.28 billion) Semiconductor Strategy funds design IP and prototypes but does not yet add sub-65 nm wafer capacity, so offshore dependency will continue in the medium term.

Are low-power voltage classes taking over?

Yes, sub-1.8 V devices show the fastest uptake at 8.8% as IoT and wearable designers switch to 1.2 V-1.8 V MCUs to extend battery life.

What technologies threaten NOR Flash in the UK?

High-density eMMC and UFS deliver lower cost per gigabyte and faster sequential reads, eroding NOR's role in data-logging and infotainment where execute-in-place is not a must-have.

Page last updated on: