Indonesia Scaffolding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

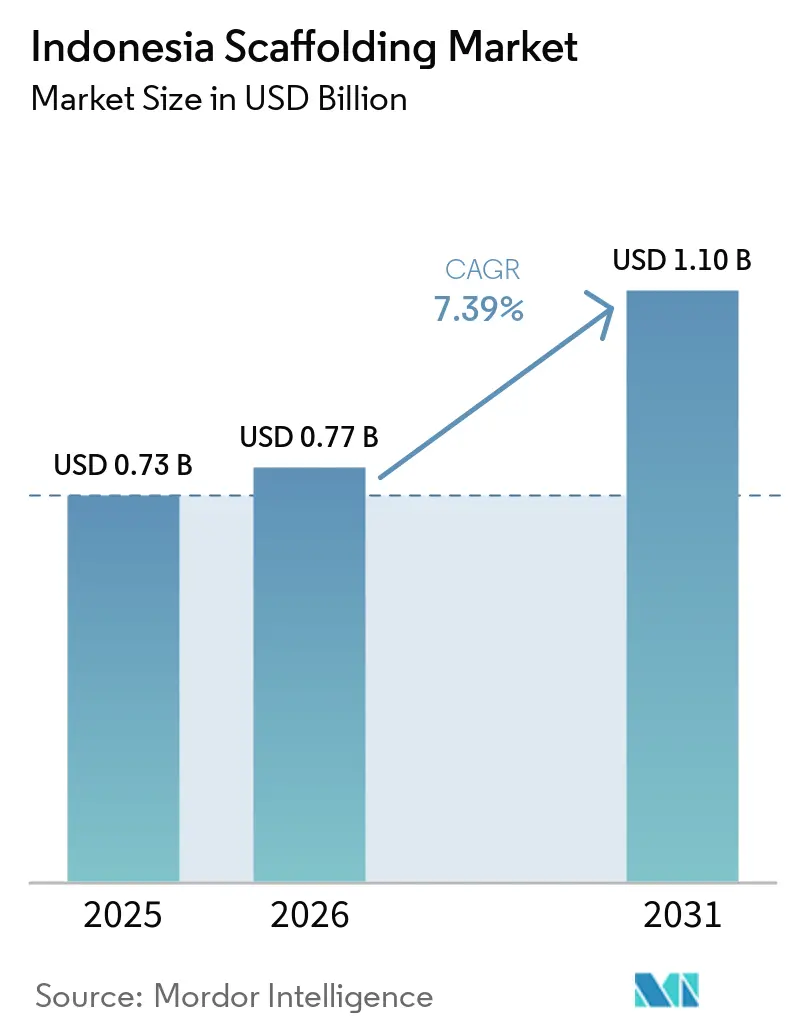

| Base Year Market Size (2025) | USD 0.73 Billion |

| Market Size (2026) | USD 0.77 Billion |

| Market Size (2031) | USD 1.10 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Scaffolding Market Analysis by Mordor Intelligence

The Indonesia Scaffolding Market size is projected to be USD 0.73 billion in 2025, USD 0.77 billion in 2026, and reach USD 1.10 billion by 2031, growing at a CAGR of 7.39% from 2026 to 2031.

The Indonesia scaffolding market is supported by a broad infrastructure pipeline under the national medium-term development plan, which keeps demand visible across transport, energy, and public works. Non-budget construction activities under National Strategic Projects and public-private partnership structures keep project execution active across several provinces, supporting recurring equipment demand over multiple project cycles. Construction value added in Indonesia strengthened, reinforcing the operating base for the Indonesia scaffolding market and supporting sustained demand across construction activities. Demand also benefits from tighter safety expectations, more complex industrial projects, and contractor preference for specialist access solutions rather than carrying idle equipment between jobs. The Indonesia scaffolding market remains fragmented, and competitive strength increasingly depends on certified systems, fleet depth, and the ability to deliver projects across Java and the outer islands with reliable on-site support.

Key Report Takeaways

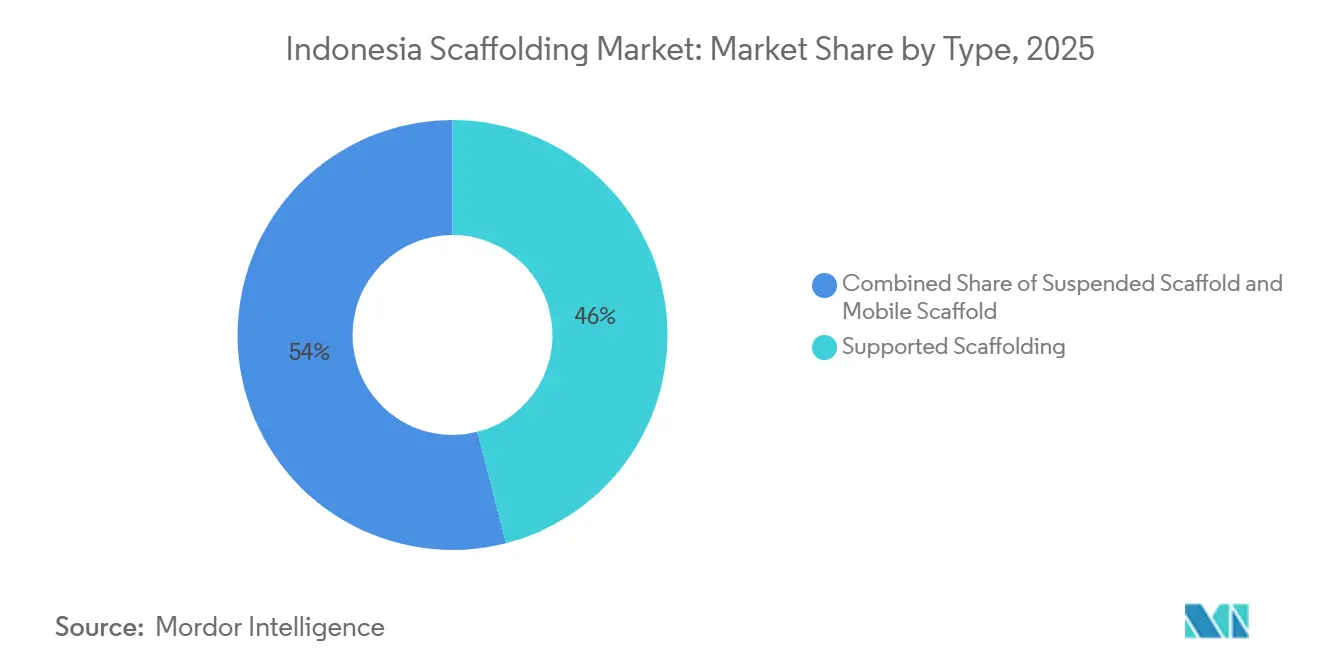

- By type, supported scaffolding led with a 46% revenue share in 2025, while suspended scaffolding is forecast to expand at a 7.70% CAGR through 2031.

- By system, modular / ringlock held 39% of the Indonesia scaffolding market share in 2025 and also recorded the highest projected CAGR at 8.35% through 2031.

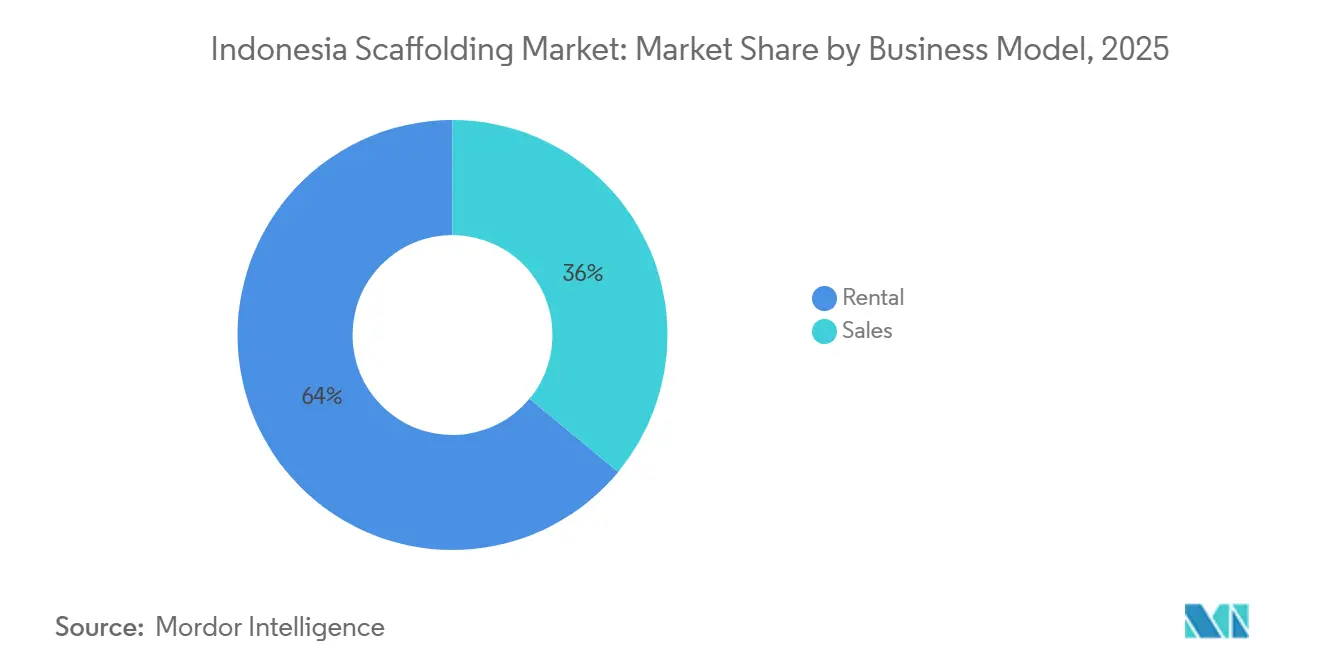

- By business model, rental accounted for 64% of the Indonesia scaffolding market size in 2025 and is advancing at a 7.90% CAGR through 2031.

- By material type, steel commanded a 68% share of the Indonesia scaffolding market size in 2025, while aluminum is projected to grow fastest at an 8.20% CAGR through 2031.

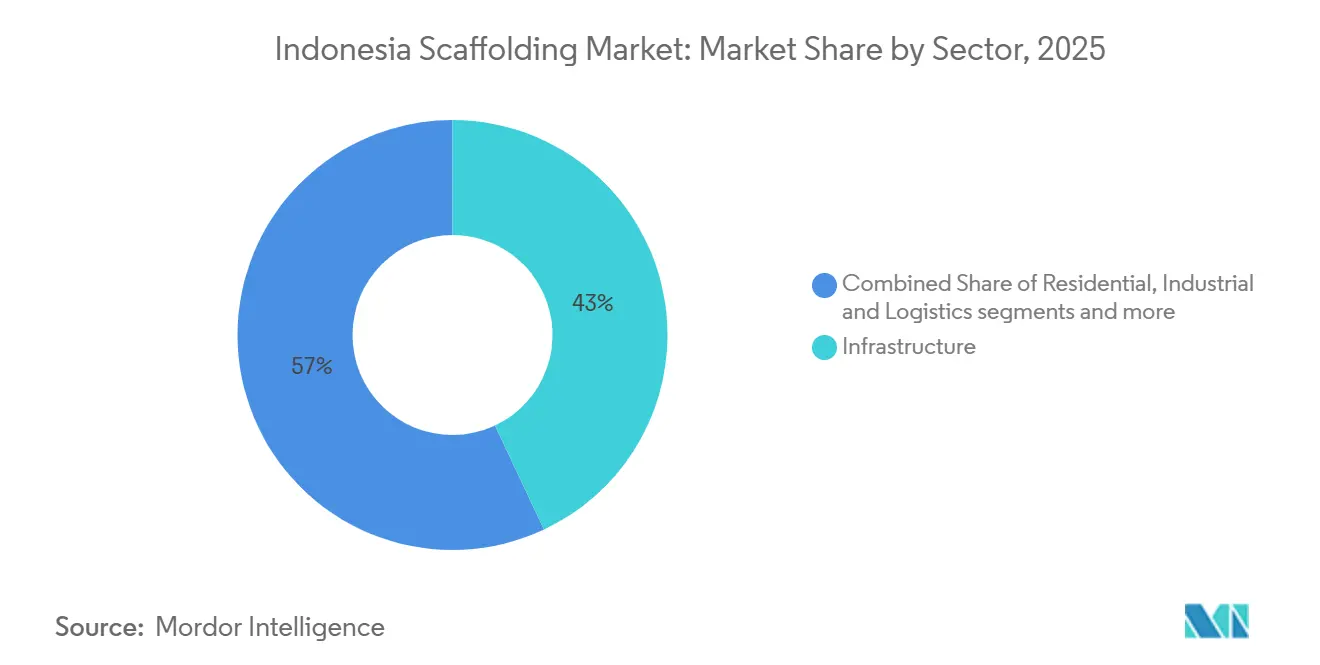

- By sector, infrastructure captured 43% of revenue in 2025 and is forecast to expand at an 8.45% CAGR to 2031.

- By geography, Java held 62% of the Indonesia scaffolding market share in 2025, while Kalimantan recorded the highest projected CAGR at 8.10% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Scaffolding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Development Across Industrial Corridors Drives Scaffolding Demand | +2.2% | Java, Kalimantan, Sulawesi | Medium term (2-4 years) |

| Refinery, Petrochemical, and Power Plant Maintenance Supports Scaffolding Utilization | +1.3% | Java, Sumatra | Short term (≤ 2 years) |

| Rental Preference Among Contractors and SMEs Expands Market Adoption | +1.0% | National, strongest in Java and Kalimantan | Medium term (2-4 years) |

| Shift Toward Modular and Ringlock Systems Enhances Project Efficiency | +0.8% | Java, Kalimantan, Sulawesi | Medium term (2-4 years) |

| Construction Growth in Tier 2 and Tier 3 Cities Increases Scaffolding Requirements | +0.6% | Secondary cities in Java and urban centers in Sulawesi | Long term (≥ 4 years) |

| Rising Safety Compliance Expectations Encourage Use of Standardized Systems | +0.5% | National, strongest in Java and Sumatra industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Development Across Industrial Corridors Drives Scaffolding Demand

The Indonesia scaffolding market is seeing stronger demand from industrial corridor construction than from one-off building activity. Large-scale development in Central and West Java keeps access equipment in use across groundworks, structures, utilities, and plant fit-out over extended timelines[1]Liputan6 Editorial Team, “KEK Kendal Kantongi Komitmen Investasi Rp 189 Triliun di Triwulan I 2026,” Liputan6, liputan6.com. The Kendal Special Economic Zone reported IDR 189.16 trillion (USD 10.51 billion) in investment commitments from 139 businesses by Q1 2026, suggesting a long build cycle rather than a short burst of activity. Batang also moved ahead with dryport construction in June 2026, adding another layer of civil and logistics-related work that supports demand for access equipment[2]IDN Times Editorial Team, “KEK Industropolis Batang Bangun Dryport Berbasis Rel,” IDN Times, idntimes.com. The same pattern is broadening beyond Java, as Special Economic Zones reached a total investment of IDR 335 trillion (USD 18.61 billion) by the end of 2025, indicating that Indonesia's scaffolding market is tied to a broader industrial expansion path.

Refinery, Petrochemical, and Power Plant Maintenance Supports Scaffolding Utilization

The Indonesia scaffolding market benefits from maintenance work, as refinery and petrochemical turnarounds cannot be postponed for long without incurring operational risk. Chandra Asri began scheduled maintenance at its Cilegon petrochemical complex in January 2026 across the Naphtha Cracker, Polymer Plant, Butadiene, and Methyl Tertiary-Butyl Ether (MTBE) units, creating immediate equipment demand during defined maintenance windows[3]Chandra Asri Group, “To Ensure Long Term Reliability Chandra Asri Group's Petrochemical Plants Undergo Scheduled Maintenance,” Chandra Asri, chandra-asri.com. PT Kilang Pertamina Internasional also appointed ABL Group in January 2026 for asset integrity work at the 348,000-barrel-per-day Cilacap refinery complex, including verification of more than 85,000 assets. In July 2025, PT Wijaya Karya completed the restoration of four 29,000 cubic meter gasoline tanks at Balongan under a contract worth IDR 279.3 billion (USD 15.5 million), demonstrating that even one refinery site can carry a meaningful scaffolding workload. This maintenance layer provides the Indonesia scaffolding market with a steadier revenue base, as it continues even when parts of the new-build cycle slow.

Rental Preference Among Contractors and SMEs Expands Market Adoption

The Indonesia scaffolding market is strongly shaped by a contractor base that prefers access to equipment over ownership. More than 65 million small and medium enterprises (SMEs) operate in Indonesia, and the segment contributes over 60% of the national gross domestic product, supporting a business environment where capital preservation matters. For many contractors, buying a fleet ties up cash, requires storage, and creates idle periods between projects, while rental keeps site costs closer to real work schedules. That preference is not limited to smaller builders, as industrial clients also use rental-plus-service arrangements during turnaround periods when specialized equipment is needed for short but intense work windows. As a result, the Indonesia scaffolding market continues to favor providers that can supply equipment, mobilization, and support in a single package rather than only selling frames and components.

Shift Toward Modular and Ringlock Systems Enhances Project Efficiency

The Indonesia scaffolding market is gradually moving toward modular / ringlock systems as project requirements become more demanding. Modular / ringlock systems already lead the systems category in both scale and growth, indicating that contractors are shifting to faster, more standardized configurations. This shift matters because industrial and infrastructure sites need repeatable assembly quality, documented load ratings, and easier on-site safety reviews. Certified modular systems also help crews work around complex shapes and multi-level structures with less site improvisation than older loose-component setups. Over time, that change should improve project speed and help formal suppliers in the Indonesia scaffolding market differentiate themselves from informal operators.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages Constrain Safe Erection and Dismantling Activities | -1.2% | National, most acute in Kalimantan, Sulawesi, and Papua | Long term (≥ 4 years) |

| Import Dependence for High-Specification Components Increases Cost Exposure | -0.8% | National, strongest for premium aluminum and modular systems | Medium term (2-4 years) |

| Price Sensitivity and Informal Competition Pressure Market Profitability | -0.7% | National, strongest in Java | Short term (≤ 2 years) |

| High Logistics and Inter-Island Distribution Costs Raise Operating Expenses | -0.5% | Sulawesi, Maluku, Papua, and parts of Kalimantan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages Constrain Safe Erection and Dismantling Activities

The Indonesia scaffolding market faces a clear labor constraint, as safe erection still depends on a limited pool of qualified workers. A national study published in April 2026 showed that only 6% of Indonesia’s 8.14 million construction workers held valid competency certifications, and 30,000 workers could lose their certifications by 2027 due to nonrenewal. That shortfall matters because formal scaffolding work is supposed to be carried out by trained personnel, especially when systems are modified or dismantled on active sites. The risk is higher outside the main urban centers, where new project growth is strong but certified labor is harder to secure. This gap restrains the Indonesia scaffolding market not because demand is weak, but because safe delivery is harder to scale at the same pace as project starts.

Import Dependence for High-Specification Components Increases Cost Exposure

The Indonesia scaffolding market also remains exposed to imported inputs for premium aluminum systems and precision modular components. That dependence raises landed costs when exchange rates move against buyers and makes procurement more sensitive to shipping delays and supply disruptions. Domestic fabrication has strengthened the local supply base for standard steel products, but it has not fully addressed the reliance on specialized upstream materials and components. The effect is strongest in higher-specification projects, where contractors cannot easily switch to lower-grade substitutes without affecting safety or performance. This keeps margin pressure in place across the Indonesia scaffolding market, especially for rental providers that need to renew fleets while keeping prices competitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Supported Scaffolding Holds the Core Position While Suspended Systems Gain From Urban Vertical Work

Supported scaffolding accounted for 46% of the Indonesia scaffolding market in 2025, making it the largest segment by a clear margin. Its lead comes from the fact that most active projects still involve ground-based or mid-rise work where stable, load-bearing access structures are required for concrete, facade, and finishing activities. The segment accommodates the broadest range of site conditions, making it the default choice for contractors working on residential, commercial, and infrastructure projects. That breadth is important because the Indonesia scaffolding market still depends on project volume from mainstream construction activity, rather than from specialized industrial sites. Supported systems also benefit from a familiar labor base, and that matters in a country where workforce certification gaps continue to affect installation quality on some sites.

Suspended scaffolding is the fastest-growing type and is projected to expand at a 7.7% CAGR through 2031. That growth reflects the larger stock of completed towers, commercial assets, and industrial structures that need facade access and periodic maintenance, especially in dense urban areas on Java. The type also becomes more relevant as government and mixed-use developments build taller structures that require access after core construction is complete. Mobile scaffolding remains smaller, but it serves interior fit-out, electrical works, and maintenance tasks where crews need fast repositioning inside buildings. Taken together, type demand in the Indonesia scaffolding industry shows a practical split, with supported systems driving everyday volume and suspended systems gaining ground as height and maintenance frequency increase.

By System: Modular / Ringlock Systems Hold the Largest Share and Continue to Expand Rapidly

Modular / ringlock scaffolding accounted for 39% of the Indonesia scaffolding market in 2025, making it the largest systems segment. The segment also posted the fastest projected growth at 8.35% through 2031, which means the technology leader is still taking share rather than merely defending it. That pattern points to a real change in contractor preference inside the Indonesia scaffolding market, especially on sites where assembly speed and consistent load performance matter. Standardized components help reduce setup variation and simplify documentation for contractors seeking cleaner safety records on regulated projects. This is one reason the systems category has become a key area of competition for suppliers serving industrial plants, public works, and larger private developments.

Legacy systems still play a role in the Indonesia scaffolding industry because they can be useful for irregular structures and for jobs where cost control matters more than speed. Tube-and-coupler solutions remain relevant for retrofit work or for layouts that do not fit standard modules well. Cuplock systems hold a middle ground where repetitive slab and facade work is common. Frame and H-frame scaffolding stays visible on lower-rise residential and light commercial projects because it is familiar and relatively easy to deploy. Even so, the overall direction of the Indonesia scaffolding market points toward more modular adoption as project complexity rises and formal contractors seek more predictable site performance.

By Business Model: Rental Dominates Because Capital Efficiency Matters Across Contractor Types

Rental accounted for 64% of revenue in 2025, making it the largest business model in the Indonesia scaffolding market. This structure is closely tied to contractor economics because ownership requires working capital, storage space, repair capability, and steady utilization across project cycles. In contrast, rental lets contractors match equipment use to active work and avoid carrying idle stock when one job ends before another begins. That advantage is especially strong in a market where small and medium enterprises account for a very large share of the business base and already contribute over 60% of the national gross domestic product. The size of this customer base means that the Indonesia scaffolding market continues to favor service-driven providers that can mobilize equipment quickly and support repeat short- to medium-duration jobs.

Rental is also the fastest-growing business model, with a projected CAGR of 7.9% through 2031. The strength of that outlook reflects recurring maintenance needs in petrochemical and refinery sites, where clients often prefer to bring in specialist fleets only when shutdown work is scheduled. Sales still hold a meaningful place among larger industrial users, engineering, procurement, and construction contractors, and entities that manage recurring plant work with more control over internal logistics. Those buyers value ownership when equipment can be reused across large sites and over long maintenance calendars. Even so, the center of gravity in the Indonesia scaffolding market remains with rental, which keeps fleet scale, asset turnover, and service reliability at the center of competitive strategy.

By Material Type: Steel Keeps the Lead While Aluminum Expands in Higher Efficiency Use Cases

Steel held 68% of the material segment in 2025, making it the clear leader in the Indonesia scaffolding market. It remains dominant because it is familiar, widely available through local supply channels, and well-suited to heavy civil and industrial work where load capacity is critical. Steel also aligns with the cost expectations of a broad contractor base, which matters in a market where price pressure from informal operators remains part of day-to-day competition. That combination keeps steel firmly in place across mainstream construction categories, especially where standard access needs are more important than lower weight. In practical terms, steel still defines the base demand profile for the Indonesia scaffolding market.

Aluminum is the fastest-growing material, with an 8.2% CAGR projected through 2031. The growth case is tied to easier handling and lower setup effort, which can reduce labor needs on maintenance-intensive projects where equipment is moved often. That makes aluminum more attractive in refinery, petrochemical, and facility service work where fast assembly and repeated changeovers matter. Timber and plywood continue to appear in informal or rural settings, but their role is narrowing as formal project specifications move toward compliant industrial systems. Plastic / fiberglass remain niche materials for specific environments where corrosion or electrical sensitivity alter access requirements. The result is a two-speed material mix in the Indonesia scaffolding market, with steel preserving volume leadership and aluminum widening its role in specialized work.

By Sector: Infrastructure Sets the Pace for Both Current Scale and Future Growth

Infrastructure accounted for 43% of the Indonesia scaffolding market in 2025, making it the largest sector by revenue. The segment stands out because public works, transport assets, and energy projects tend to run over long schedules and require access structures at multiple construction stages. The national pipeline includes ongoing work tied to the new capital city, broader transport links, and utility development, which keeps demand visible across multiple regions. Infrastructure is also the fastest-growing sector, with an 8.45% CAGR projected through 2031, making it the largest part of the Indonesia scaffolding market and the one expanding most quickly. That combination gives suppliers a strong reason to allocate fleets and technical resources to civil works and government-linked projects.

The new capital city pipeline is one of the clearest examples of this trend. Legislative and judicial complex construction progressed in 2025 and 2026, and the 2026 state budget included IDR 6 trillion (USD 333.3 million) for continued development. Residential activity still contributes a meaningful base, supported by housing demand and township expansion. Logistics, retail, and data-related building needs in Java also support commercial work. Industrial and logistics construction adds value through concentrated high-ticket projects. Still, infrastructure remains the strongest strategic anchor for the Indonesia scaffolding market because it combines scale, visibility, and multi-year continuity.

Geography Analysis

Java accounted for 62% of revenue in 2025, giving it the largest regional share in the Indonesia scaffolding market. The island leads because it concentrates industrial output, commercial construction, refinery maintenance, and government-linked project activity in a single broad operating area. Java also hosts several major industrial zones, including Kendal and Batang, where investment and logistics infrastructure continue to expand. Batang began dry port construction in June 2026, adding another multi-year project stream tied to industrial logistics development. Java also benefits from a steady maintenance layer, as Chandra Asri’s January 2026 turnaround at Cilegon and Pertamina-related activity at Cilacap both sustained site access demand beyond new-build work.

Kalimantan is the fastest-growing geography in the Indonesia scaffolding market, with an 8.1% CAGR projected through 2031. The main reason is the development of Nusantara in East Kalimantan, which has created a long-term pipeline for public buildings, housing, and supporting infrastructure. Construction of the legislative and judicial complexes is underway in 2026, and the planned completion timeline stretches into 2027, which gives suppliers a clearer demand horizon than in many short-cycle private projects. Around 2,000 civil servants were already present in Nusantara by March 2026, indicating the project is advancing from concept to operational reality. This gives Kalimantan a rare position in the Indonesia scaffolding market because it combines government spending, industrial expansion, and a multi-year construction schedule within a single geography.

Sumatra plays a steady secondary role through refinery, palm oil, and pulp-related assets, helping keep demand more stable than in purely speculative construction areas. Sulawesi and the rest of Indonesia still account for a smaller share. Still, they represent the broadening edge of the Indonesia scaffolding market as mineral processing zones and Special Economic Zones attract more investment. That broadening is promising, but inter-island transport costs continue to limit suppliers' margins when moving bulky equipment into eastern regions. Companies that build regional distribution capabilities or work with local logistics partners should be better positioned to capture growth as activity spreads beyond Java and Kalimantan.

Competitive Landscape

The Indonesia scaffolding market remains fragmented, with international suppliers and numerous domestic companies competing on equipment quality, rental availability, service support, and contractor relationships. Organized operators typically compete through certified systems, fleet reliability, engineering support, and the ability to serve industrial and infrastructure projects with consistent execution. Regional firms, meanwhile, often benefit from closer customer relationships, faster mobilization, and greater pricing flexibility within their operating areas. As a result, competition varies across project types, with technical capability playing a larger role in regulated and high-value projects. At the same time, proximity and cost competitiveness remain important in routine construction work. No single supplier holds a dominant position, and competition remains broadly distributed across national and regional participants.

International companies continue to strengthen their industrial service capabilities through acquisitions and service expansion strategies. For example, ALTRAD's acquisition of Stork's United Kingdom business in February 2025 expanded its industrial services platform and reinforced its ability to support maintenance-intensive sectors. Such developments are relevant because industrial clients increasingly seek integrated solutions that combine access systems with maintenance and project support services. This trend is gradually increasing the importance of service capabilities alongside equipment supply.

Domestic companies continue to play a central role in the industry through manufacturing capacity, local presence, and established contractor networks. PT Beton Perkasa Wijaksana operates a large fabrication facility in Cikupa and maintains 12 marketing offices nationwide, demonstrating how local suppliers compete through broad market coverage and operational reach. Other regional participants leverage local market knowledge and customer relationships, particularly in provinces where national networks remain less developed. Opportunities remain significant in industrial and infrastructure projects outside the main Java corridor, where logistics, service responsiveness, and local presence can be as important as brand recognition. Consequently, the market continues to favor companies that can combine certified systems, competitive pricing, and dependable project support across diverse geographic regions.

Indonesia Scaffolding Industry Leaders

PT Beton Perkasa Wijaksana

PERI Indonesia

Altrad Sparrows Indonesia

PT. Teras Teknik Perdana

PT. Kashiwabara Engineering Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: KEK Industropolis Batang commenced construction of a 30-hectare rail-based dry port with an initial annual capacity of 600,000-650,000 TEUs, planned to expand to 1 million TEUs as the surrounding industrial zone develops. The multi-phase project is expected to support sustained scaffolding demand during construction.

- June 2026: PT Aceh Global Steel (ISG Group) and PT Pembangunan Aceh (PEMA) signed an agreement to build a light steel manufacturing plant in the Aceh Industrial Zone, Aceh Besar. The project, targeted for completion by the end of 2026, will support industrial construction activity and increase demand for scaffolding during plant development.

- January 2026: PT Chandra Asri Pacific commenced a scheduled turnaround maintenance program at its Cilegon petrochemical complex, covering the Naphtha Cracker, Polymer, Butadiene, Methyl Tertiary-Butyl Ether (MTBE), and Butene-1 plants across two maintenance phases of approximately 26 and 41 days. The program is expected to sustain scaffolding demand at one of Banten's largest industrial facilities.

Indonesia Scaffolding Market Report Scope

The Indonesia Scaffolding Market Report is Segmented by Type (Supported, Suspended, and Mobile), System (Tube & Coupler, Cuplock, and More), Business Model (Sales and Rental), Material (Timber / Plywood, Steel, Aluminum, and More), by Sector (Residential, Commercial, Industrial & Logistics, and Infrastructure), and by Geography (Java, Sumatra, Kalimantan, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Supported Scaffold |

| Suspended Scaffold |

| Mobile Scaffold |

| Tube & Coupler |

| Cuplock |

| Modular / Ringlock |

| Frame / H-Frame |

| Sales |

| Rental |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Rest of Indonesia |

| By Type | Supported Scaffold |

| Suspended Scaffold | |

| Mobile Scaffold | |

| By System | Tube & Coupler |

| Cuplock | |

| Modular / Ringlock | |

| Frame / H-Frame | |

| By Business Model | Sales |

| Rental | |

| By Material Type | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By Geography | Java |

| Sumatra | |

| Kalimantan | |

| Sulawesi | |

| Rest of Indonesia |

Key Questions Answered in the Report

What is the expected value of Indonesia's scaffolding demand by 2031?

The Indonesia scaffolding market is forecast to reach USD 1.10 billion by 2031 from USD 0.77 billion in 2026, with a 7.39% CAGR over 2026 to 2031.

Which sector drives the largest share of revenue?

Infrastructure led with 43% of revenue in 2025 and is also the fastest-growing sector, with an 8.45% CAGR through 2031.

Why does rental remain the dominant business model in Indonesia?

Rental held 64% of revenue in 2025 because many contractors prefer lower upfront cost, less storage burden, and better capital efficiency across uneven project cycles.

Which system category is gaining the strongest traction?

Modular / Ringlock systems led with a 39% share in 2025 and are projected to grow at 8.35% through 2031, as contractors value faster assembly and more standardized performance.

Which region offers the strongest growth outlook?

Kalimantan is the fastest-growing geography, with an 8.1% CAGR through 2031, largely due to the multi-year Nusantara capital city development pipeline.

Page last updated on: