Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

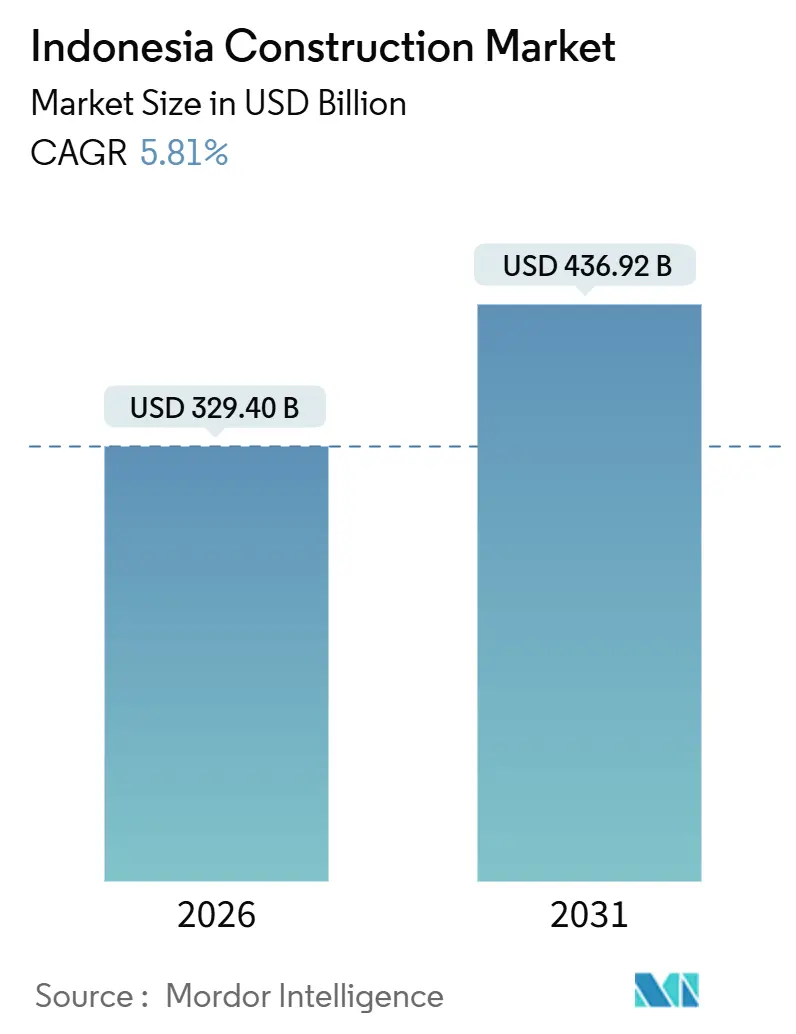

| Market Size (2026) | USD 329.40 Billion |

| Market Size (2031) | USD 436.92 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Construction Market Analysis by Mordor Intelligence

The Indonesia construction market size is estimated at USD 329.4 billion in 2026 and is expected to reach USD 436.92 billion by 2031 at a CAGR of 5.81% during the forecast period (2026 - 2031). Growth is transitioning from state-led megaprojects toward selective PPP-backed assets as state-owned contractors work through multi-year restructurings and tighter balance sheets. Infrastructure remains the largest revenue stream, but commercial activity is set to expand faster as hyperscale data centers and industrial estates move from commitment to execution. Within the construction industry in Indonesia, geographic rebalancing is visible, with Java still dominant while nickel-driven industrial clusters in Sulawesi and ongoing IKN-linked enabling works in Kalimantan tilt the medium-term project mix eastward. Construction methods are evolving as modular and precast pilots scale, yet conventional on-site building sustains its large base due to contractor familiarity and upfront cost sensitivity.

Key Report Takeaways

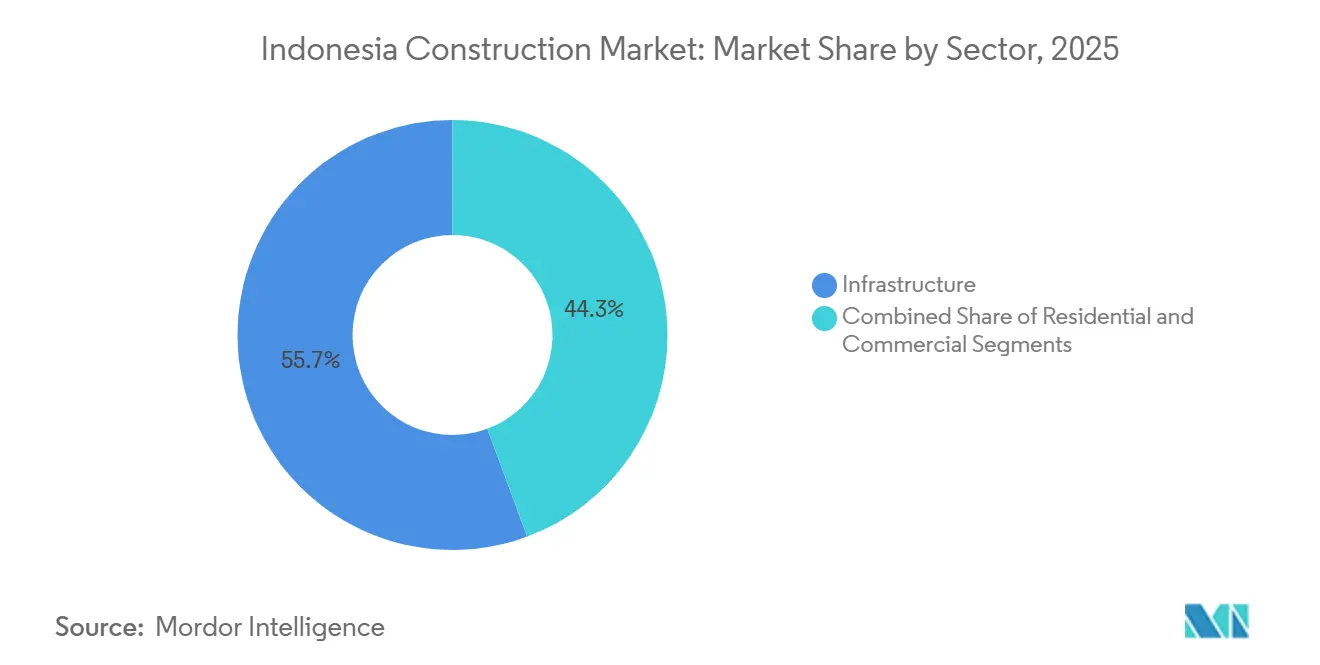

- By sector, infrastructure led with a 55.66% revenue share in 2025, while commercial is projected to record a 6.48% CAGR through 2031.

- By construction type, new construction accounted for 79.12% in 2025, while renovation is projected to grow at a 6.37% CAGR through 2031.

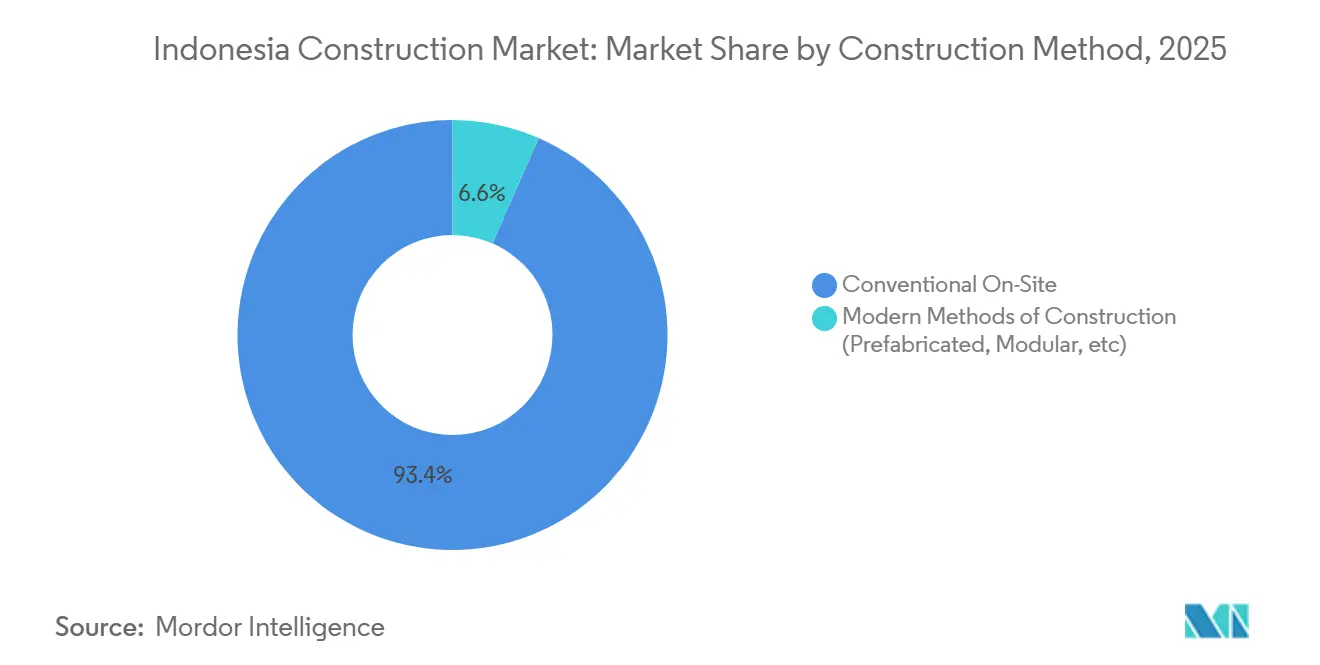

- By construction method, conventional on-site work held 93.44% in 2025, while modern methods are projected to expand at a 7.07% CAGR through 2031.

- By investment source, public investment held a 64.33% share in 2025 while private investment is projected to grow at a 6.33% CAGR through 2031, ahead of public’s 5.33%.

- By geography, Java accounted for 63.11% in 2025, while Sulawesi is projected to post a 6.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government megaproject pipeline | +1.5% | East Kalimantan, Sumatra, Java | Medium term (2-4 years) |

| Mining-based downstream investments | +1.2% | Central and Southeast Sulawesi, North Maluku | Long term (≥ 4 years) |

| Residential housing backlog and mortgage stimulus | +0.9% | National, major metros | Short term (≤ 2 years) |

| Data-centre and hyperscale cloud build-outs | +0.8% | Greater Jakarta, selected metros | Short term (≤ 2 years) |

| Foreign capital and PPP inflows for industrial estates | +0.7% | Sulawesi, Kalimantan, West Java | Medium term (2-4 years) |

| Green-building incentives and carbon-neutral mandates | +0.4% | National urban centres | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Megaproject Pipeline

Government Megaproject Pipeline Drives Selective Momentum. Multi-year national programs continue to shape workload visibility, with Jakarta MRT Phase 2A progressing and additional packages executed to extend urban transit capacity. Toll road expansion stays active through staged delivery and asset recycling by core state developers as operational corridors add maintenance and upgrade scopes. Budget priorities are rotating toward irrigation, water, and maintenance, which supports steady civil volumes even as direct greenfield toll-road funding recedes in favor of PPP structures. The IKN program continues to anchor enabling works, utilities, and access roads that support contractor backlogs and material flows into East Kalimantan. Together, these initiatives sustain near to medium-term activity while nudging developers to refine risk allocation, preconstruction planning, and financial structuring.[1]https://www.ina.go.id/

Mining-Based Downstream Investments

Processing hubs in Central and Southeast Sulawesi and North Maluku expand civil and industrial work as smelters, refineries, and balance-of-plant facilities proliferate. New hydrometallurgical lines and ancillary plants require heavy-duty foundations, roads, housing, and utilities, which deepen contractor engagement beyond core EPC scopes. Power and water linkages for these complexes are scaling through long-term power purchase agreements with the national utility, reinforcing grid and captive generation investments. Successive commissioning milestones at leading projects underpin a multi-year capex cycle and stable job creation tied to battery-value-chain localization. As the regulatory environment emphasizes higher-value processing, capital formation, and construction intensity are expected to remain firm in compliant zones.

Residential Housing Backlog and Mortgage Stimulus

Government housing programs add demand for affordable units, with subsidized mortgages and fee assistance mechanisms designed to improve access and shorten time-to-close. Lending channels remain concentrated among leading banks, which stabilizes underwriting standards and project screening for developers serving the mass-housing pipeline. Modular housing pilots by industrial partners demonstrate lead-time compression and cost visibility, which can complement subsidy-led demand if scale barriers and certification steps are addressed. Localized building codes and green standards are converging with national frameworks, which support clearer specifications for mid-market housing and public stock upgrades. Taken together, policy support and private pilots point to steady low to mid-income housing activity, with productivity gains likely to spread through prefabrication and standardized components.

Datacenter and Hyperscale Cloud Buildouts

Hyperscale capacity under construction in Greater Jakarta signals fast-growing demand for AI-ready workloads and low-latency connectivity for cloud services. Princeton Digital Group is delivering a 120 MW campus with phased completion, which anchors a cluster of high-spec builds requiring robust power, cooling, and security. EDGNEX Data Centers by DAMAC announced a 500 MW AI-focused facility designed for high-density racks and stringent efficiency targets. Domestic EPCs and specialist contractors are moving up the capability curve on data-center projects, which is improving cost control and value engineering adoption. Given sustained platform commitments, these projects are set to support sustained civil, MEP, and fit-out demand and stimulate adjacent utility investments.[2]https://www.damacgroup.com/en-gb/

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SOE debt overhang and funding tightness | -0.8% | National, concentrated in Java | Short term (≤ 2 years) |

| Land-acquisition bureaucracy and permitting delays | -0.6% | National, severe in selected sites | Medium term (2-4 years) |

| Skill-certification gap across the labour force | -0.4% | National, major project clusters | Long term (≥ 4 years) |

| Volatile cement and specialty-material supply chains | -0.3% | Java, Kalimantan, Sulawesi | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

SOE Debt Overhang and Funding Tightness

Large state contractors continue to deleverage after multi-year losses, which pressures working-capital availability and bid discipline. Waskita Karya reported continued losses into 2025 and prolonged trading suspensions, reinforcing the need for careful project selection and stronger payment assurance. Wijaya Karya disclosed improved gearing metrics following restructuring gains, though bond defaults and trading halts signal tighter access to capital. These funding constraints can slow mobilization schedules, compress margins on fixed-price contracts, and elevate counterparty risk for subcontractors and suppliers. Consolidation efforts and governance reforms aim to reduce unhealthy competition and stabilize pricing, yet execution will take time to filter through tenders and contract terms.[3]https://www.waskita.co.id/

Land-Acquisition Bureaucracy and Permitting Delays

Systematic land registration has advanced but remains incomplete, with data-quality gaps and uncertificated parcels complicating due diligence and right-of-way. Overlapping approvals across spatial conformity, forest-use, environmental assessments, and power licensing extend preconstruction timelines for linear and energy projects. Digital licensing through the OSS framework improves transparency but relies on local spatial plans and interagency synchronization to function as intended. For flagship sites, unresolved land matters can delay mobilization and force resequencing of packages, with knock-on effects on budgets and completion dates. Addressing these gaps requires tighter central regional coordination, clearer authority lines, and reliable cadastral data that integrates with permitting systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Commercial Outpaces Infrastructure on Data-Centre Surge

Infrastructure commanded 55.66% of Indonesia's construction market share in 2025, supported by the steady delivery of toll-road segments and ongoing progress on urban rail extensions. Commercial is positioned as the fastest-growing sector with a projected 6.48% CAGR through 2031 as large-scale digital infrastructure and industrial estates convert capital commitments into shovel-ready projects. Data-center investment is a key catalyst, with Princeton Digital Group building a 120 MW campus in Greater Jakarta and EDGNEX by DAMAC planning a 500 MW AI-focused facility to address demand for high-density computing. In parallel, downstream battery materials projects channel industrial construction into estates that integrate power, transport access, and utilities with staged commissioning plans.

Across the medium term, indonesia infrastructure will continue to anchor civil workloads, while commercial will capture more greenfield and fit-out activity linked to digitalization and export-oriented manufacturing. The pipeline of transit, water, and road renewals helps smooth volumes and supports local contractor ecosystems across Java and selected non-Java corridors. Commercial developers and EPC partners are bidding more actively on hyperscale packages and on high-spec industrial jobs as local capability improves, which strengthens competition and project delivery options. As permitting efficiency and grid capacity improve, the commercial growth vector should remain above the sector average while infrastructure retains its foundational base.

By Construction Type: Renovation Gains on Aging Asset Retrofits

New construction held 79.12% of the market in 2025, reflecting the weight of national programs and large industrial estates undergoing first-phase buildouts. Renovation is projected to grow at a 6.37% CAGR through 2031, supported by the need to extend asset life, comply with evolving energy standards, and retrofit systems for higher efficiency across public and private buildings. Toll-road concessions are increasing spending on overlays, bridge works, and drainage upgrades as traffic intensifies and climate resilience becomes a planning priority. Airports, ports, and public buildings are opting for expansion and refurbishment strategies that minimize service disruption and leverage existing footprints rather than new greenfield relocations.

Energy policy is reinforcing retrofit demand through a programmatic focus on decarbonizing supply and demand, with grid upgrades and efficiency mandates creating design scopes for HVAC, facades, and controls. As financing frameworks recognize lifecycle performance, projects that incorporate measurable efficiency gains and greener materials are better positioned to access supportive capital. The Indonesian construction market will see more tender packages structured around performance outcomes that reward durability and energy savings over the lowest upfront price. Over time, renovation volumes should expand beyond metro cores into secondary cities as standards, funding channels, and contractor capabilities align.

By Construction Method: Modern Methods Inch Forward on Pilot Momentum

Conventional on-site construction accounted for 93.44% of the market in 2025 due to entrenched practices, lower perceived first costs, and the prevalence of labor-intensive workflows. Modern Methods of Construction are projected to grow at a 7.07% CAGR through 2031 as precast, modular, and panelized systems move from pilots to early portfolios in housing, social infrastructure, and selected industrial builds. WIKA Beton’s manufacturing base and financial stability provide a platform to scale precast solutions as contractors seek time savings and predictable quality in repetitive elements. Modular home pilots by Saint-Gobain Indonesia and partners show one-month build times and integrated energy features, demonstrating potential fit for mid-market housing and disaster-resilient deployments.

Standardization and certification will shape the pace of adoption, with green-industry standards and BIM mandates supporting coordinated design, manufacturing, and installation. The Indonesia construction industry is also adopting digital workflows on public projects, which helps de-risk modular coordination and installation sequencing. As cost curves improve and domestic component supply deepens, modern methods should gain share in programmatic asset classes such as schools, clinics, and worker housing. In the near term, conventional delivery will remain dominant while hybrid approaches leverage precast and panelized subsystems to improve speed and quality.

By Investment Source: Private Capital Crowds Into Greenfield Data Centres

Public investment held a 64.33% share in 2025, reflecting legacy commitments to national projects and steady funding for roads, water, and public buildings. Private investment is projected to grow at a 6.33% CAGR through 2031, faster than the public’s 5.33%, as foreign equity flows into data centers, energy infrastructure, and industrial estates with clearer offtake paths and stable regulation. Dedicated infrastructure financiers and guarantees play a catalytic role for PPPs, broadening investor participation in transport and utilities. Hyperscale announcements from Princeton Digital Group and EDGNEX by DAMAC highlight the type of private-led greenfield platforms that are scaling in the current cycle.

Sovereign co-investment vehicles continue to develop asset pipelines and recycle capital into new projects, which supports a more sustainable financing ecosystem. Policy frameworks that enable 100% foreign ownership in priority infrastructure reduce friction for strategic sponsors and improve deal flow for high-impact assets. The Indonesia construction industry benefits when risk-sharing mechanisms, such as availability payments and revenue guarantees, align with investor expectations and public-service outcomes. Over the forecast period, private-led projects should expand their share of new starts while public capex anchors maintain and upgrade the national stock of infrastructure.

Geography Analysis

Regional performance shows a split between Java’s scale and Sulawesi’s pace, with Java accounting for 63.11% in 2025 and Sulawesi projected to deliver a 6.49% CAGR through 2031. Java’s urban and peri-urban corridors concentrate metro rail, road renewals, and commercial fit-outs as large developers and PPP consortia scale projects that rely on dense demand catchments. Within the construction industry in Indonesia, growth remains steady as asset classes like data centers and logistics hubs seek proximity to load centers and backbone networks, while modernizing public assets expands maintenance scopes.

Sulawesi and North Maluku stand out for industrial construction anchored in downstream metals, where multi-plant complexes require sustained civil, MEP, and integration work. Power connectivity through long-term agreements supports phased commissioning and stable site operations, which spreads construction demand across enabling utilities and worker housing. As compliance expectations for environmental and safety standards rise, project sponsors that invest early in sustainable design and community engagement are better able to secure permits and financing. This dynamic underpins Sulawesi’s position as the fastest-growing geography within the Indonesia construction market over the forecast period.

Kalimantan’s IKN-linked works, including roads, utilities, and site preparation, provide continuity for civil contractors and material suppliers as packages are sequenced for delivery. Sumatra advances corridor development through toll-road segments and water projects, which maintain robust workloads across provinces with rising industrial and agricultural output. Bali and Nusa Tenggara maintain tourism and airport refurbishment activity, with project selection sensitive to service reliability and environmental considerations. As logistics efficiency improves through targeted infrastructure, more non-Java provinces should attract high-spec investment that diversifies the Indonesia construction market beyond traditional hubs.

Competitive Landscape

Competitive intensity spans state-owned leaders, diversified private groups, and specialized EPCs, with market share influenced by access to capital, execution capabilities, and risk appetite. State-owned enterprises maintain strong positions in national projects while deleveraging efforts and governance reforms reshape bidding discipline and partnership models. Private players are increasing their presence in commercial and industrial builds, supported by hyperscale and downstream investments that favor fast-track delivery and cost transparency.

Strategically, sponsors and contractors are aligning around bankability and risk-sharing, using guarantees and blended finance to reach financial close on PPPs and large estates. Asset recycling through sovereign co-investors helps recycle capital into new projects while offering institutional investors exposure to stable cash flows. In data centers, domestic firms are capturing a larger share of EPC scopes historically dominated by international specialists, which is narrowing cost differentials and accelerating knowledge transfer.

Operationally, engineering and digital tools are spreading across public and private projects as BIM mandates and green standards push standardization and lifecycle optimization. Precast and modular platforms from industrial producers enable faster cycles on repetitive assets, with a runway for uptake as standards, training, and supply chains mature. Firms with credible ESG positioning and reliable supply partnerships are better placed to win high-spec tenders in energy, digital, and industrial sectors that demand strict compliance and long-term performance.

Indonesia Construction Industry Leaders

PT Hutama Karya (Persero)

PT Wijaya Karya (Persero) Tbk

PT Pembangunan Perumahan (Persero) Tbk

PT Adhi Karya (Persero) Tbk

PT Waskita Karya (Persero) Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: EDGNEX Data Centers by DAMAC announced a USD 2.3 billion, 500 MW AI-focused data center in Jakarta, with first-phase operations targeted for December 2026 and a PUE target of 1.32.

- September 2025: PT Wijaya Karya Beton Tbk posted 9M 2025 revenues of USD 161.5 million and net income of USD 0.09 million, reflecting macro pressures on precast demand.

- September 2025: PT Sanurhasta Mitra Tbk reported completion of strategic infrastructure projects by the Ministry of Public Works and Housing during 2024 in super-priority tourism zones.

- June 2025: Princeton Digital Group broke ground on JG1, a USD 1 billion, 120 MW hyperscale data-center campus in Greater Jakarta, with first-phase operations targeted for December 2026.

Indonesia Construction Market Report Scope

Construction includes any on-site physical work that involves erecting a structure, cladding, external finish, formwork, fixtures, installing services, and unloading equipment, supplies, etc. A complete background analysis of the Indonesian construction market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The Indonesian construction market is segmented by sector (commercial, residential, industrial, infrastructure (transportation) construction, and energy and utilities construction). The report offers market size and forecasts for all the above segments in value (USD).

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Others |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Java | |

| Sumatra | ||

| Kalimantan | ||

| Sulawesi | ||

| Others | ||

Key Questions Answered in the Report

What is the Indonesia construction market size and growth outlook to 2031?

The Indonesia construction market size is USD 329.4 billion in 2026, and it is forecast to reach USD 436.92 billion by 2031 at a 5.81% CAGR.

Which segment leads the Indonesia construction market and which grows fastest?

Infrastructure leads with a 55.66% share in 2025, while commercial is projected to be the fastest-growing segment with a 6.48% CAGR through 2031.

Which regions are most important for growth within Indonesia?

Java accounts for 63.11% in 2025, while Sulawesi is projected to grow fastest at a 6.49% CAGR given industrial parks and downstream metals projects.

What themes are driving private investment in Indonesia construction?

Hyperscale data centers and downstream battery-materials estates are attracting foreign capital and sponsors, supported by PPP guarantees and enabling regulation.

How quickly will modern construction methods scale in Indonesia?

Modern Methods of Construction are projected to expand at a 7.07% CAGR through 2031, with uptake led by precast and modular pilots from industrial producers and housing partners.

What are the key risks to watch for project delivery?

SOE deleveraging, land-acquisition and permitting complexity, skill-certification gaps, and imported specialty-material exposure can extend timelines and weigh on margins if not mitigated.

Page last updated on: