Indonesia Construction Consulting Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

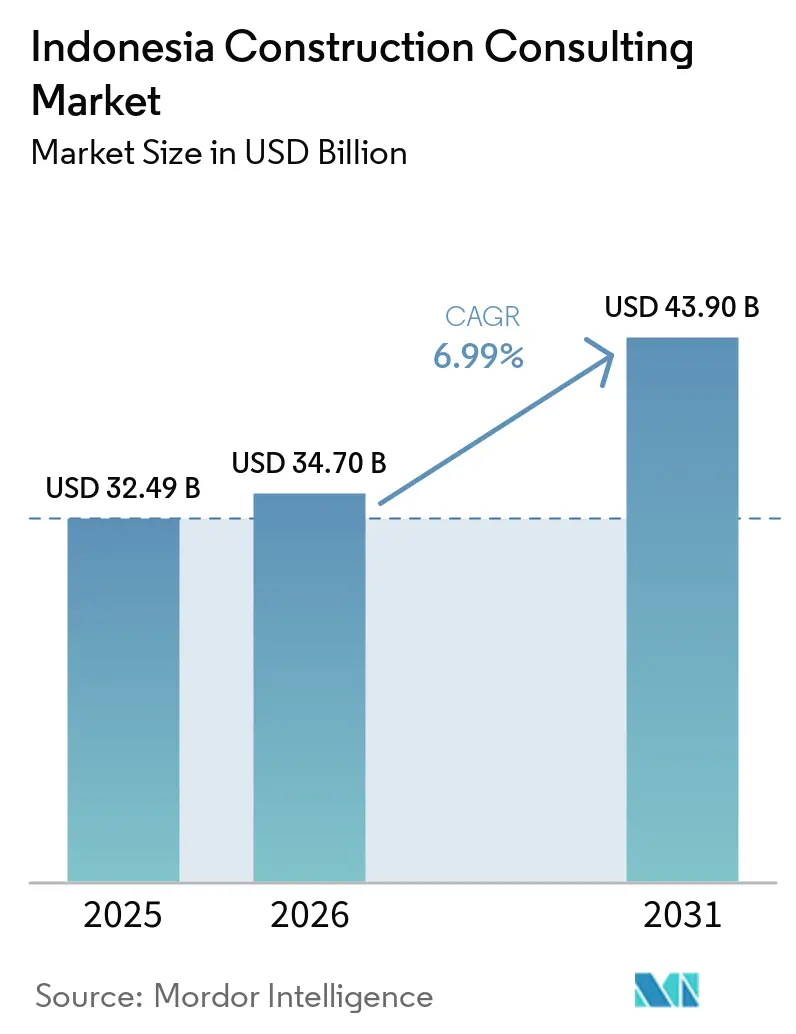

| Base Year Market Size (2025) | USD 32.49 Billion |

| Market Size (2026) | USD 34.70 Billion |

| Market Size (2031) | USD 43.90 Billion |

| Growth Rate (2025 - 2031) | 6.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Construction Consulting Market Analysis by Mordor Intelligence

The Indonesia Construction Consulting Market size was valued at USD 32.49 billion in 2025 and is estimated to grow from USD 34.70 billion in 2026 to reach USD 43.90 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031). Demand is being driven primarily by consulting-intensive activities rather than by construction volume alone. Every Nusantara package is being awarded with separate project management contracts, BIM coordination assignments, and stakeholder engagement scopes. Each of these layers contributes directly to the revenue pool of the Indonesia construction consulting market.

At the same time, more than 55 PPP schemes expected to be awarded between 2025 and 2029 require lender model audits, viability gap assessments, and risk allocation studies. As a result, advisory work begins well before physical construction starts, increasing the number of consulting hours required in the early stages of projects.

The digital-first mandate under SPBE also requires consultants to manage live dashboards that combine BIM 5D cost data with procurement progress. This is increasing software spending and demand for specialized talent, while also supporting billable rates that are 10% to 15% higher than those for traditional 2D-based work.

Finally, green building certifications are no longer optional services. EDGE and Greenship compliance requirements are now being included in employer specifications, creating a stable and recurring revenue stream for sustainability consultants within the Indonesia construction consulting market.

Key Report Takeaways

- Project management consultancy held 54.33% of Indonesia construction consulting market share in 2025, whereas design-and-engineering is projected to advance at 8.95% CAGR through 2031.

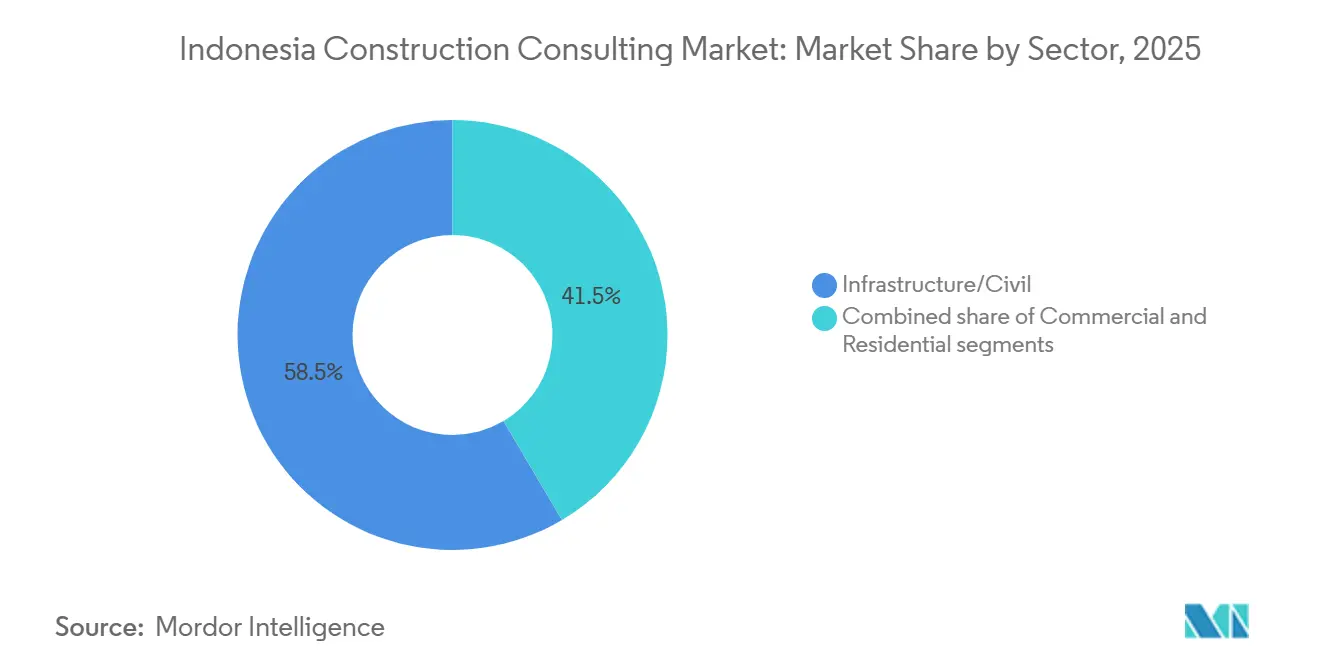

- Infrastructure captured 58.55% of the Indonesia construction consulting market size in 2025, while commercial work, led by hyperscale data-center campuses, is forecast to grow at 8.11% CAGR to 2031.

- New construction commanded 81.22% of 2025 activity, yet renovation is the fastest expanding construction type with a 9.37% CAGR for 2026-2031.

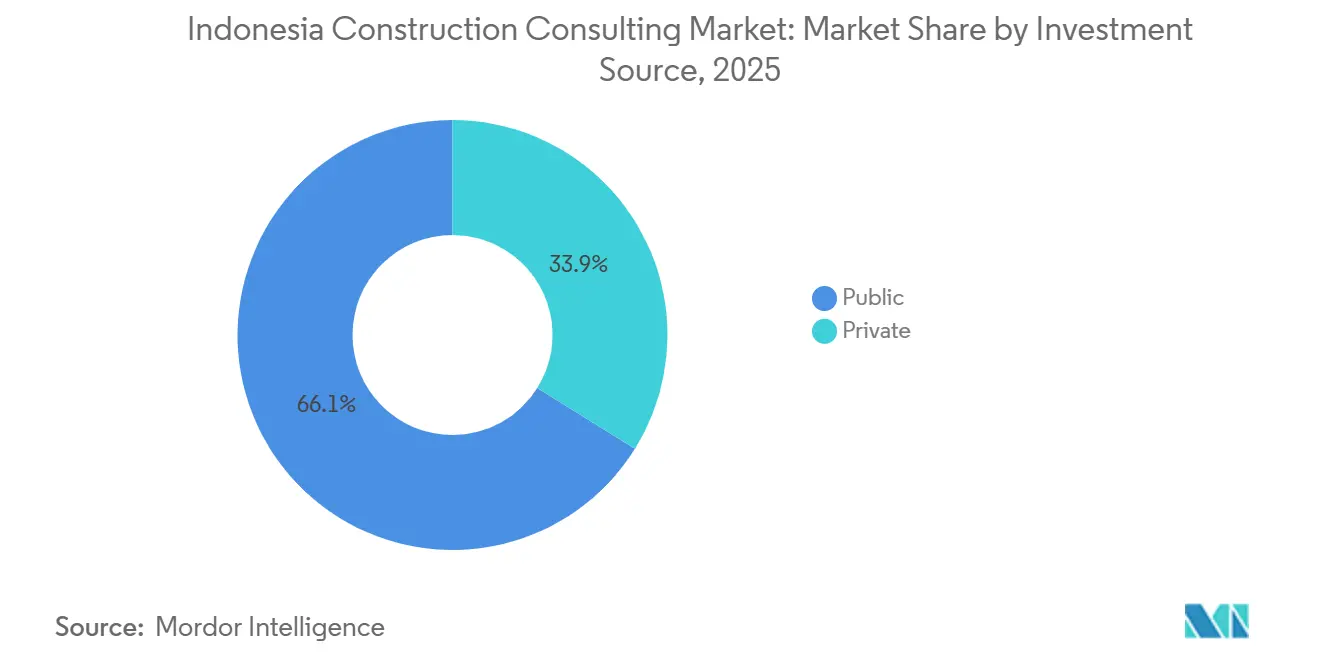

- Public spending contributed 66.12% of 2025 billings, but private funding is expected to expand at 8.32% CAGR on the back of green-building and data-center investment.

- Java generated 63.11% of 2025 revenue; Sulawesi is the highest-growth region, set to rise at 8.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nusantara new-capital megaproject fuelling multi-phase consulting demand | +1.8% | Kalimantan core, Java design hubs | Long term (≥ 4 years) |

| Building Information Modeling (BIM) and Sistem Pemerintahan Berbasis Elektronik (SPBE) digital-construction mandates | +1.5% | National, Java leads roll-out | Medium term (2-4 years) |

| Revamped Public-Private Partnership (PPP) framework with INA co-investment | +1.3% | Java, Sumatra toll roads, Sulawesi ports | Long term (≥ 4 years) |

| Mandatory AMDAL EIA & PROPER ESG ratings tightening pre-construction due-diligence | +1.2% | Nationwide, strongest on Java & Sumatra | Medium term (2-4 years) |

| Down-stream nickel-EV industrial parks in Sulawesi spurring specialised infrastructure advisory | +0.9% | Sulawesi & North Maluku clusters | Short term (≤ 2 years) |

| Uptake of EDGE/Greenship certifications | +0.7% | Jakarta, West Java, Banten, Bali | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nusantara new-capital megaproject fuelling multi-phase consulting demand

Parliament cleared over 20 Phase II packages across legislative and judicial zones, each valued between USD 760 million and USD 1.27 billion, with completion targeted by 2028. This pipeline guarantees a steady flow of feasibility, detailed design, and project-management contracts even if broader infrastructure budgets soften. The government’s mix of direct budget allocations and PPP tranches, USD 3.8 billion to USD 8.2 billion, calls for advisors able to structure risk-sharing agreements. A grant of USD 2.49 million from the U.S. Trade and Development Agency for smart-city studies signals that multilateral sponsors now bake digital-technology requirements into terms of reference, raising capability thresholds for local firms. Because roll-out runs through 2028, Nusantara acts as a counter-cyclical anchor that cushions the Indonesian construction consulting market against spending swings elsewhere[1]Petromindo Newsroom, “Indonesia infrastructure round-up February 2026,” petromindo.com.

Building Information Modeling (BIM) and Sistem Pemerintahan Berbasis Elektronik (SPBE) Digital Mandates

Since 2025, state buildings larger than 2,000 m² and complex infrastructure must use BIM, yet only about one engineer in twenty holds accredited training. Software subscriptions of roughly USD 3,000 per seat match a junior salary, deterring small players. The 2025 SPBE, Electronic-Based Government System regulation now obliges electronic dashboards for real-time cost and schedule tracking, making 4D and 5D integration a de facto requirement. Firms that embraced BIM report tangible savings; pipe waste on the Sepaku water network fell from 3.0% to 1.2%, while laggards risk exclusion from high-profile tenders. Absent a national subsidy, larger enterprises with in-house academies are widening the skills gap.

Public-Private Partnership (PPP) & Sovereign-Fund Co-Investment

Revisions to the KPBU framework call for USD 34–41 billion of projects between 2025-2029, spanning water, toll roads, and housing. The Indonesia Investment Authority (INA) now takes equity stakes and offers traffic-revenue guarantees, lowering risk premiums for private bidders. As a result, transaction advisers must combine financial modelling with technical diligence and ESG screening. Toll concessions such as the Palembang-Betung segment illustrate this hybrid approach, where state funds underwrite construction but O&M is auctioned to private operators. Expertise in viability-gap structuring and multi-lane free-flow tolling is increasingly prized.

Mandatory AMDAL EIA & PROPER ESG ratings tightening pre-construction due-diligence

Indonesia digitized its three-tier environmental review in 2025, speeding approvals but demanding deeper baseline data. PROPER ratings now cover almost 3,700 industrial sites; projects scoring poorly face financing obstacles, pushing developers to retain environmental consultants earlier. Regulators increasingly align green-building seals with PROPER scores, opening a niche for firms that package permitting, mitigation, and certification[2]Ministry of Environment and Forestry, “PROPER Program Update 2025,” menlhk.go.id. Investment in GIS, air-quality simulation, and social-impact surveys that used to be discretionary is becoming mandatory, expanding scope and billable hours for multidisciplinary teams. This regulatory convergence is a structural driver of sustainability consulting demand on major projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lowest-cost (Harga Terendah) tendering bias reducing value-added consulting scope | -1.1% | National, most acute at provincial and district-level procurement | Medium term (2-4 years) |

| Payment delays & State-Owned Enterprise (SOE) debt overhang squeezing consultant cash-flows | -1.6% | National, concentrated in Java (SOE headquarters), ripple effects to outer islands | Short term (≤ 2 years) |

| Shortage of certified BIM/PMP professionals constraining capacity | -0.8% | National, more acute in Sumatra, Kalimantan, Sulawesi where training infrastructure is limited | Long term (≥ 4 years) |

| Fragmented central-local approvals causing project slippages | -0.6% | National, worse in outer islands where central-local coordination is weaker | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lowest-cost (Harga Terendah) tendering bias reducing value-added consulting scope

Most public tenders still hinge on the lowest price, relegating technical quality to a pass-fail filter. This structure compresses fees, discourages investment in BIM or value engineering, and forces mid-sized domestic consultancies into a race to the bottom. Provincial agencies rarely deploy quality-based selection because evaluators lack the capacity to score technical proposals, further entrenching price-only awards. Larger state-owned and foreign firms cope by cross-subsidizing thin-margin studies with higher-margin supervision mandates, but smaller outfits are squeezed, limiting overall innovation in the Indonesia construction consulting market.

Payment delays & State-Owned Enterprise (SOE) debt overhang squeezing consultant cash-flows

Construction SOEs carry billions in short-term debt; one flagship contractor defaulted on USD 63 million in bonds in 2025 and is litigating over unpaid high-speed-rail invoices. Budget cuts halved the Public Works ministry’s outlays in 2025, stretching consultant payment cycles from 30 days to as long as four months. Smaller firms must bridge working-capital gaps at double-digit interest rates, eroding profitability. A state plan to merge loss-making builders in 2026 could eventually improve credit quality, but the transition period is likely to freeze bid invitations and prolong cash-flow pressure across the Indonesia construction consulting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Project-Management Anchors Revenue as High-Value Design Accelerates

Project management consultancy controlled 54.33% of 2025 revenue, reflecting Indonesia's construction consulting market size leadership in large toll-road and mass-transit programs. Design-and-engineering, however, is forecast to post the quickest expansion at 8.95% CAGR, buoyed by multi-disciplinary scope on Nusantara’s judicial and legislative compounds and by complex process-plant layouts in Sulawesi’s nickel-EV hubs. Master planning remains a small but strategic niche, especially for new industrial estates that require phasing and utility optimization.

BIM rules are redrawing the competitive map. Only three in ten firms now deliver full 3D-to-5D workflows, and they command premiums of up to 20% over 2D rivals. Foreign players leverage proprietary common-data environments and larger training budgets, while several domestic leaders have responded by launching in-house academies to certify staff and preserve share. As a result, the Indonesia construction consulting market size for high-end design is expanding faster than the overall sector value.

By Sector: Infrastructure Remains the Backbone as Commercial Projects Propel Future Upside

Infrastructure in Indonesia represented 58.55% of 2025 billings, anchored by roads, rail, and water schemes. Nevertheless, commercial assignments are expected to rise at an 8.11% CAGR, topping the sector growth chart. Hyperscale data centers, such as a USD 4.5 billion 500 MW campus outside Jakarta, need specialized MEP, seismic isolation, and liquid-cooling expertise, lifting average fee multipliers.

Office and retail refurbishments add a parallel revenue stream as 2 million m² of idle 2010s-era space seeks energy-efficient retrofits. Meanwhile, industrial logistics parks benefit from e-commerce tailwinds and regional supply-chain shifts. Within infrastructure, new mandates for climate-resilient drainage and multi-lane free-flow tolling expand the scope for advisory services beyond civil works. Collectively, these trends reinforce commercial momentum but keep infrastructure as the revenue anchor of the Indonesia construction consulting market.

By Construction Type: New Builds Dominate Today, Renovation Wave Accelerates Tomorrow

New builds accounted for 81.22% of 2025 turnover, mirroring the scale of Nusantara’s greenfield districts and Sulawesi smelter expansions. Renovation, however, is projected to clock a 9.37% CAGR through 2031, the fastest within this classification. Government slum-upgrade programs will renovate 400,000 units in 2026 alone, and landlords are retrofitting aging towers to secure EDGE or Greenship badges.

Renovation projects often entail structural assessments, laser scanning, and phased occupancy planning, which can lift hourly rates even if gross contract values are lower than for greenfields. The need to digitize legacy drawings into BIM adds an extra fee layer, supporting profitability for consultants specialized in as-built modeling.

By Investment Source: Public Funding Provides Stability while Private Capital Fuels Rapid Gains

Public outlays delivered 66.12% of revenue in 2025, but private capital is growing at 8.32% CAGR as green buildings, data hubs, and private industrial estates proliferate. Of 385 certified green assets logged by September 2025, two-thirds were privately financed, confirming that ESG goals are a private-sector priority. PPP restructuring, with sovereign-fund equity, viability-gap grants, and performance-based annuities, blurs the classic public-private line and enlarges advisory scope around financing strategy.

Private developers generally prefer quality-and-cost scoring, rewarding innovation, while many public bodies still select by lowest price. This bifurcated procurement culture encourages consultants to maintain diversified client books to balance margin and volume, shaping revenue resilience within the Indonesia construction consulting market.

Geography Analysis

Java generated 63.11% of 2025 consulting spend thanks to its concentration of ministries, SOE headquarters, and high-rise commercial real estate. Budget tightening and SOE debt, however, are tempering growth to mid-single digits. The island remains the focal point for green-building retrofits and for hyperscale data-center clusters that rely on robust fiber connectivity and ample power.

Sulawesi is the fastest-growing territory at an 8.46% CAGR, powered by the Morowali and North Maluku nickel-EV value chains. These complexes demand port dredging, high-voltage integration, and environmental remediation studies. Chinese EPC contractors dominate, spurring demand for bilingual consultants versed in both Indonesian and GB engineering codes.

Kalimantan’s consulting pipeline is anchored by Nusantara. Access toll roads have already cut Balikpapan capital travel times nearly in half, driving urban-planning and utilities design in buffer zones[3]IKN Authority, “Nusantara Progress Dashboard Q1 2026,” ikn.go.id. Spending will peak around 2027-2028 as government campuses enter detailed design and construction. Sumatra trails in growth but benefits from toll-road completions that lower logistics costs and improve project viability in secondary cities.

Competitive Landscape

International giants such as AECOM and Nippon Koei stand out for BIM maturity and global delivery systems, securing marquee projects like Jakarta MRT extensions and Indonesia’s first BIM-designed hydro plant. State-owned consultancies leverage framework agreements and historical ties to ministries, but their competitiveness is being diluted by restructuring and balance-sheet stress.

Domestic independents are responding through vertical integration. One long-established firm now operates geotechnical, construction management, and Japan joint-venture arms under one umbrella. Another rebranded its EPC unit in 2025 to chase design-build contracts across energy and infrastructure. Niche newcomers focus on claims, contract administration, and modular value engineering, unbundling traditional scopes into higher-margin advisory strips.

Technology leadership is the emerging wedge. Only 30% of market participants run full BIM processes, giving early adopters pricing power and access to digitally mandated tenders. Similarly, the capacity to deliver integrated ESG, energy modeling, and PROPER compliance is allowing specialist boutiques to capture premium work, particularly on commercial retrofits and PPP‐sponsored water projects.

Indonesia Construction Consulting Industry Leaders

AECOM Indonesia

Arcadis Indonesia

WSP Indonesia

Mott MacDonald Indonesia

Arup Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lippo Group broke ground on the USD 2.47 billion Meikarta affordable-housing complex, a 54-tower project that will need comprehensive master-planning and environmental services.

- February 2026: State contractor WIKA reported 86% completion on the Sepaku water-supply network, citing BIM-enabled material savings that cut pipe waste to 1.2%.

- July 2025: Nippon Koei secured a 25-month PMC mandate for Jakarta MRT East-West Line 1, expanding its 866-project Indonesian portfolio.

- April 2025: Rekayasa Engineering renamed its EPC arm Rekind E&C to target integrated design-build opportunities in energy and manufacturing.

Indonesia Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design & Engineering Services |

| Master Planning & Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Java |

| Sumatra |

| Kalimatam |

| Sulawesi |

| Others |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design & Engineering Services | ||

| Master Planning & Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Key Region | Java | |

| Sumatra | ||

| Kalimatam | ||

| Sulawesi | ||

| Others | ||

Key Questions Answered in the Report

What is the current value of the Indonesia construction consulting market?

The market stands at USD 34.7 billion in 2026 and is projected to reach USD 43.9 billion by 2031.

How fast is the sector expected to grow?

Industry revenue is forecast to rise at a 6.99% CAGR over the 2026-2031 period.

Which service type generates the most consulting revenue?

Project-management consultancy leads, accounting for 54.33% of 2025 billings.

Where is demand expanding the quickest geographically?

Sulawesi leads with an expected 8.46% CAGR through 2031, fueled by nickel-EV industrial parks.

What is driving the surge in sustainability consulting?

Stricter AMDAL and PROPER regulations, plus a growing pool of green-building certifications, are boosting demand for integrated environmental and ESG advisory.

Page last updated on: