Indonesia Formwork Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

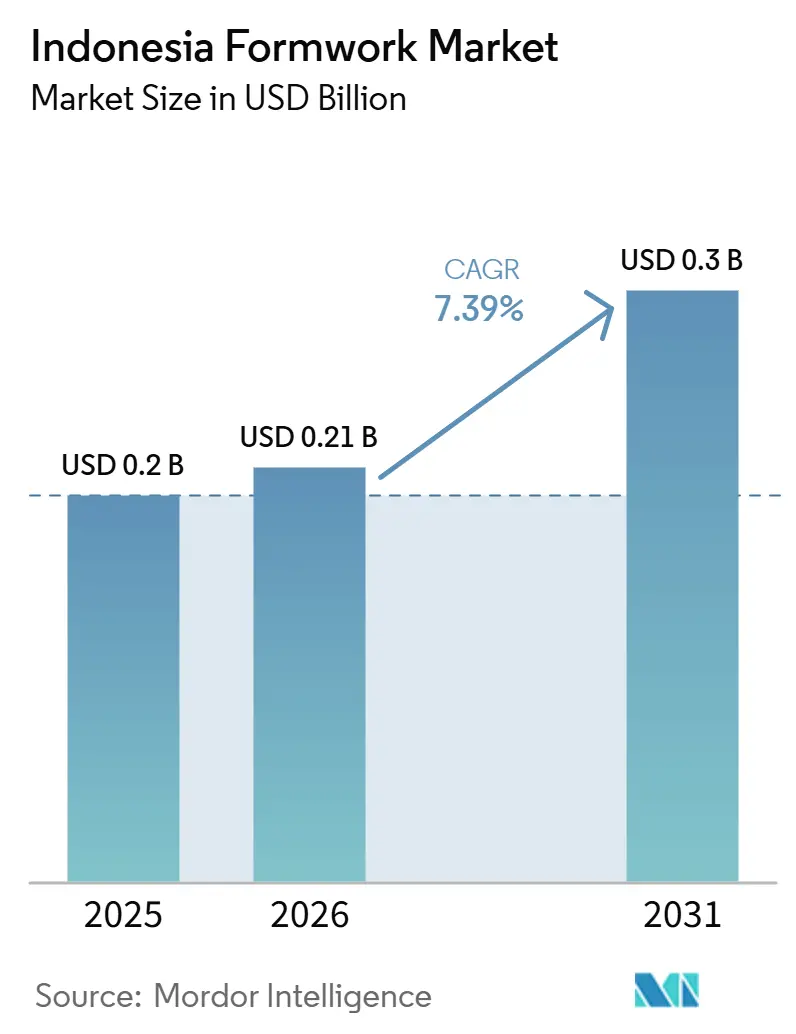

| Base Year Market Size (2025) | USD 0.2 Billion |

| Market Size (2026) | USD 0.21 Billion |

| Market Size (2031) | USD 0.3 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Formwork Market Analysis by Mordor Intelligence

The Indonesia Formwork Market size is expected to grow from USD 0.2 billion in 2025 to USD 0.21 billion in 2026 and is forecast to reach USD 0.3 billion by 2031 at 7.39% CAGR over 2026-2031.

The Indonesia formwork market is expanding because contractors are changing how they procure, finance, and deploy concrete shaping systems across a broader construction pipeline, rather than because of a single isolated demand pocket. Public infrastructure spending remains a major support, with the Ministry of Public Works finalizing a 2026 budget of IDR 118.5 trillion (USD 7.3 billion). Road connectivity receives the largest allocation at IDR 45.62 trillion (USD 2.8 billion). At the same time, the broader 2025 to 2029 infrastructure plan still leaves a large funding gap that will keep private and Public-Private Partnership (PPP) execution active. Productivity pressure is also pushing the Indonesia formwork market toward reusable and engineered systems, as only 5.96% of Indonesia’s 8.14 million construction workers hold formal competency certificates, limiting safe deployment capacity and raising the value of systems that reduce labor intensity on site. The shift toward Building Information Modeling (BIM)-based project planning is raising the importance of engineering support in supplier selection, since the Ministry of Public Works is moving toward wider BIM use on large projects by 2029, and contractors that integrate formwork planning earlier can shorten pour cycles and reduce coordination errors. Demand is also broadening into specialized applications tied to Jakarta Mass Rapid Transit (MRT) Phase 2A, the Nusantara Capital program, and the government’s target to complete 5,000 suspension bridges by the end of 2026, creating room for suppliers with deep rental capacity, logistics control, and project-specific engineering capability.

Key Report Takeaways

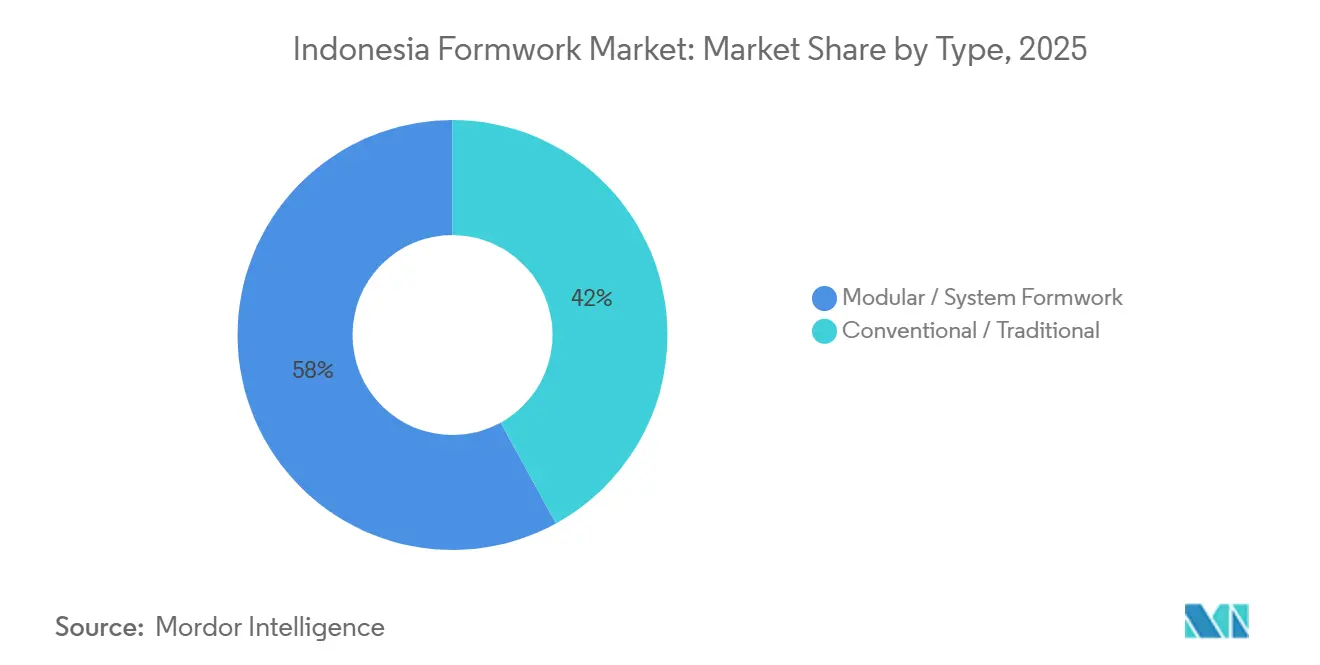

- By type, modular / system formwork held a 58% share of demand in 2025 and is forecast to expand at the fastest CAGR of 8.50% through 2031.

- By configuration, static formwork held 46% of the Indonesia formwork market share in 2025, while climbing formwork is forecast to expand at an 8.54% CAGR through 2031.

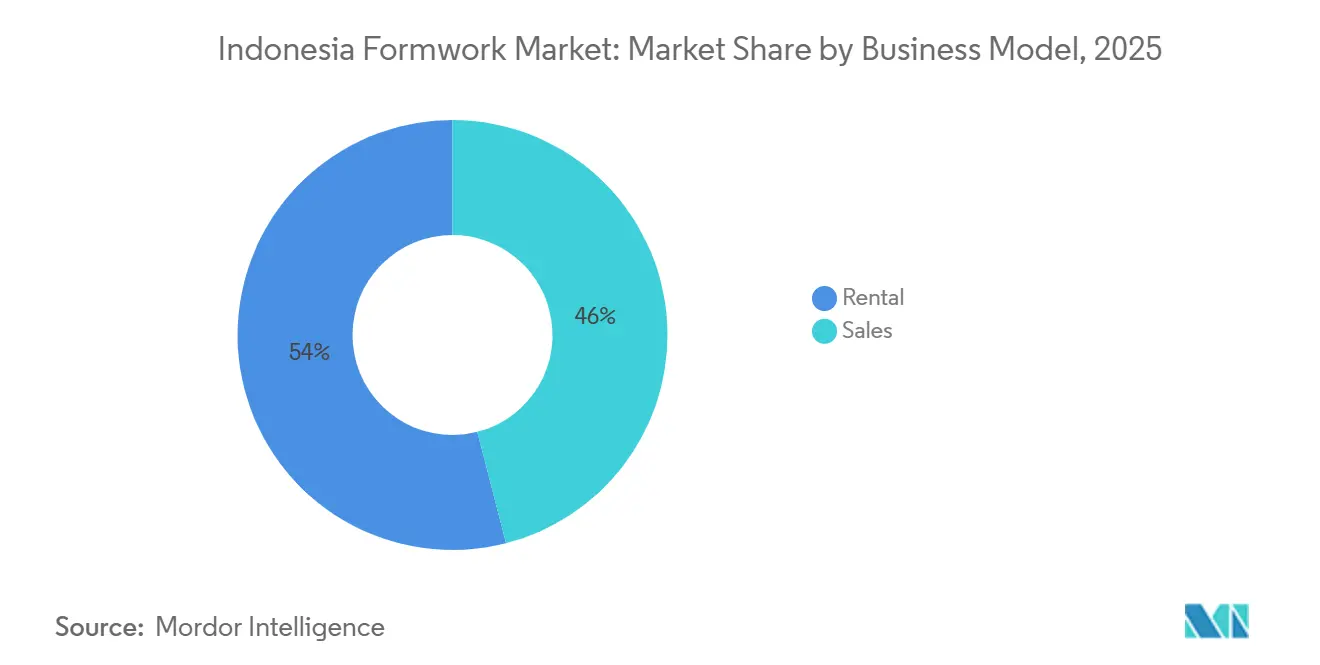

- By business model, rental held 54% of the Indonesia formwork market share in 2025 and recorded the highest projected CAGR at 9.30% through 2031.

- By sector, infrastructure accounted for 39% of the Indonesia formwork market size in 2025 and is advancing at a 9.10% CAGR through 2031.

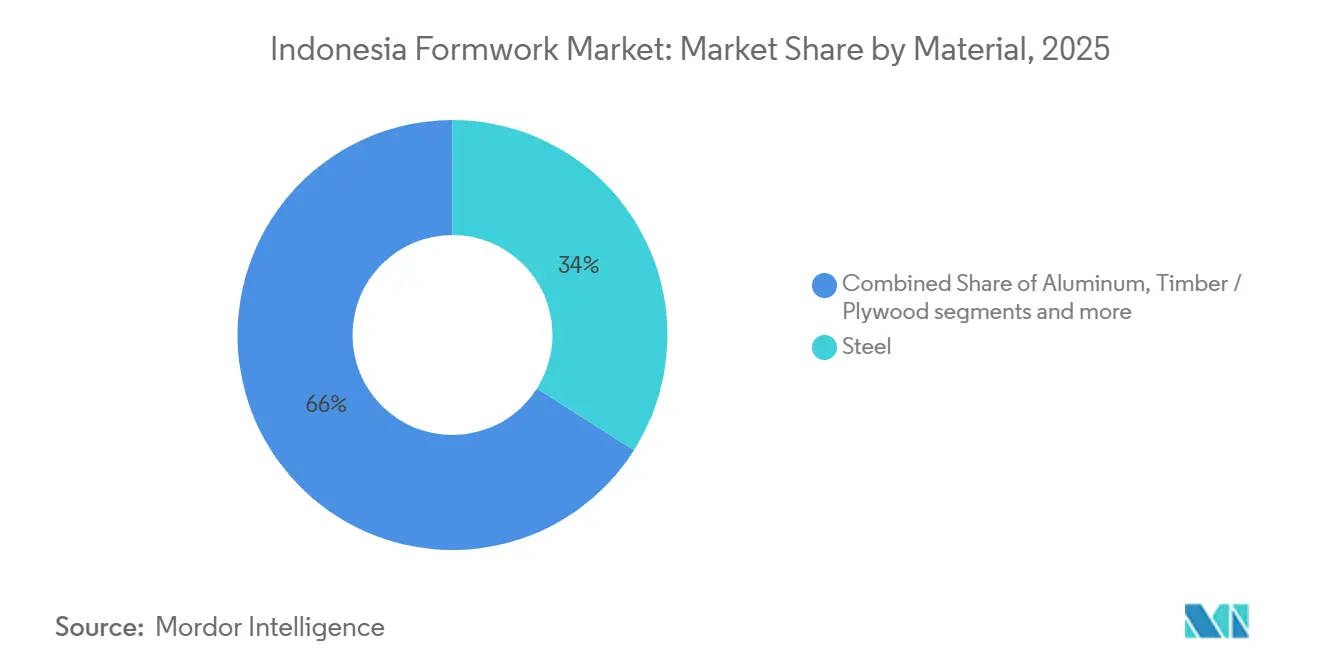

- By material, steel captured 34% of demand in 2025, while aluminum is forecast to expand at a 9.68% CAGR through 2031.

- By city, Jakarta accounted for 38% of demand in 2025 and is projected to grow at an 8.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Formwork Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-Backed Demand From Transport and Urban Projects | +2.0% | Java core including Jakarta, Surabaya, and Bandung, with spillover to Kalimantan through IKN | Medium term (2-4 years) |

| Shift Toward Modular and System Formwork | +1.4% | National, with concentration in Jakarta and satellite cities | Long term (≥ 4 years) |

| Rising Adoption of Rental-Based Procurement | +1.1% | National, with early gains in Jakarta, Surabaya, and Medan | Medium term (2-4 years) |

| Specialized Formwork Need For Tunnels, Bridges, and Transit Corridors | +0.9% | National, including Kalimantan, Java, and Sumatra | Medium term (2-4 years) |

| Demand From High-Rise Residential Construction | +0.7% | Greater Jakarta, Surabaya, and Bandung | Short term (≤ 2 years) |

| Labor Productivity Pressure and Skilled Worker Shortages | +0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Backed Demand from Transport and Urban Projects

The Indonesia formwork market is supported by a public works pipeline that remains large enough to sustain demand across roads, transit, bridges, and water-related assets. The Ministry of Public Works finalized a 2026 budget of IDR 118.5 trillion (USD 7.3 billion). It allocated IDR 45.62 trillion (USD 2.8 billion) to road connectivity alone, providing contractors with a clear order flow for civil concrete works[1]Ministry of Public Works Indonesia, “2026 Budget Allocation for Infrastructure Development,” VOI, voi.id. Indonesia’s infrastructure requirements for 2025 to 2029 were estimated at IDR 1,905.3 trillion (USD 119.1 billion), and the state budget covers only 35.63% of that amount, so private and PPP execution still matter for the construction calendar. That funding structure benefits suppliers that can keep fleets deployed across sequential project phases, because multi-package contracts reduce idle time and reward delivery continuity. In the Indonesian formwork market, this means large rental operators can defend accounts more easily than smaller local firms when project owners want a single supplier to support multiple pours and work fronts. The demand base is also less concentrated than before, as transport and urban works are progressing simultaneously across Java and selected outer-island locations.

Shift Toward Modular and System Formwork

The Indonesia formwork market is moving toward modular and system solutions because the total project cost is becoming more important than line-item material cost. Modular / system formwork held 58% of demand in 2025, and the reuse economics are becoming easier for mid-tier contractors to justify for repetitive structures. Reusable formwork panels can typically achieve 50 to 200 reuse cycles, while sawn timber often remains below 10 pours, significantly improving lifecycle economics well before very large tower projects. PERI Indonesia’s 2025 references at the JKT09 Data Center in Karawang and the Bank Indonesia complex in West Java show that system penetration now extends beyond traditional high-rise use cases into industrial and institutional work. A 2025 study published by Universitas Warmadewa also found that aluminum formwork delivered faster cycle times and lower labor costs per pour than conventional methods on repetitive beam, slab, and column structures. Government support for wider BIM adoption by 2029 further strengthens this trend, as digital formwork planning shortens coordination cycles and embeds engineering capability into the commercial offer.

Rising Adoption of Rental-Based Procurement

The Indonesian formwork market is also being reshaped by a clear shift toward rental, especially when contractor liquidity is tight, and project cash conversion remains uneven. International suppliers such as PERI, Doka, and Kumkang Kind support that shift by bundling engineering layouts, delivery coordination, and site assistance with equipment access. Local operators remain relevant on price, turnaround speed, and local relationships, especially in Greater Jakarta and Central Java, but their narrower fleet depth limits participation in large multi-phase projects. The difference becomes more visible outside major metros because outer-island mobilization often cannot wait for the procurement and assembly of owned equipment. In the Indonesia formwork market, rental is therefore functioning as both a financing response and an execution response, which is why growth is not limited to one contractor class or one province.

Specialized Formwork Need For Tunnels, Bridges, and Transit Corridors

The Indonesia formwork market is gaining support from projects that need specialized systems for underground works, bridge structures, and large transport corridors. Jakarta MRT Phase 2A reached 60.8% completion in May 2026, and the CP202 package advanced to 65.61%, which keeps demand active for tunnel walls, underground station boxes, shafts, and other precision concrete structures that require engineered formwork systems. PT Wijaya Karya is also using sliding formwork on the Multi Utility Tunnel of the IKN Judicial Complex Road in Nusantara, where construction progress has reached 19.35% against a planned 18.29%, demonstrating that specialized formwork can accelerate execution on technically demanding infrastructure. The government’s target to complete 5,000 suspension bridges by the end of 2026 is creating additional demand for bridge pier and abutment formwork across remote locations, where logistics strength matters as much as engineering capability. These projects are expanding the role of suppliers who can provide climbing, sliding, and tunnel-oriented systems beyond standard wall-and-slab solutions. In the Indonesia formwork market, this is raising the value of technical support, fleet readiness, and project-specific design capability in public infrastructure contracts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Requirement For Advanced Formwork Systems | -0.8% | National, most acute in tier-2 cities and outer islands | Long term (≥ 4 years) |

| Raw Material Price Volatility in Steel, Aluminum, and Timber | -0.7% | Global impact, with direct pass-through to Indonesia’s import-dependent production | Short term (≤ 2 years) |

| Logistics and Handling Complexity Outside Major Demand Centers | -0.4% | Outer islands including Sulawesi, Kalimantan, Papua, and secondary parts of Sumatra | Medium term (2-4 years) |

| Uneven Contractor Awareness and Training Gaps | -0.3% | National, with added pressure in tier-2 cities and island provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Requirement For Advanced Formwork Systems

The Indonesia formwork market still faces a meaningful barrier from the upfront cost of advanced climbing, hydraulic self-climbing, and tunnel-oriented systems. Many mid-tier contractors can see the lifecycle benefits of reusable systems, but the initial mobilization cost remains difficult to absorb when project cash collection is delayed. Access to financing is also limited because equipment lending often requires signed contracts, creating a qualification gap for contractors bidding on more technical projects. Compliance adds another layer, since suppliers increasingly need to meet SNI (Standar Nasional Indonesia)-related expectations for structural products in regulated project categories. Rental helps reduce the burden for standard applications, but it does not fully solve the economics of specialized carriers and hydraulic systems that can remain idle between sequential pours. In the Indonesia formwork market, this keeps adoption highest among firms with stronger balance sheets, established project pipelines, or support from international supplier networks.

Raw Material Price Volatility in Steel, Aluminum, and Timber

The Indonesia formwork market is also exposed to raw material price swings, especially in steel-heavy rental fleets and fabricated panel systems. Indonesia’s wholesale price index for steel sheets and plates reached 99.98 in April 2026 after a December 2025 low of 96.99, which signaled rising input pressure for operators locked into fixed-price contracts. SNI-related enforcement for zinc-coated and aluminum-zinc-coated steel products, effective from May 2026, further tightened supply conditions, even though it did not stabilize raw material pricing. Aluminum supply is increasing, with Indonesia’s primary aluminum output projected to reach 1.6 million tonnes in 2026. Still, the added volume does not automatically lower the cost of the alloy-specific extrusions used in structural formwork panels. Timber-based systems are not insulated either, because cost-sensitive projects still compare panel alternatives against timber and plywood availability on a rolling basis. This creates a margin environment in which price discipline matters as much as fleet utilization, especially for suppliers competing in the rental and fabricated steel segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Modular Systems Redefine Cost Competitiveness Across Project Scales

Modular / system formwork held 58% of the Indonesia formwork market share in 2025, which reflected widening adoption among both large contractors and mid-tier firms. The leading position was supported by tighter delivery schedules on public projects, where repeatable wall and slab cycles favor reusable systems over timber-heavy setups. Conventional / traditional formwork still served low-rise housing, small commercial work, and many outer-island projects, where crew familiarity and low upfront costs remained practical advantages. The 2025 Universitas Warmadewa study reinforced that direction, showing that aluminum formwork reduced labor costs and improved cycle times for repetitive beam, slab, and column work compared with conventional methods [2]Universitas Warmadewa, “Comparative Analysis of Cost and Time for Beam, Slab, and Column Formwork Using Conventional and Aluminum Formwork Methods,” Journal of Infrastructure Planning and Engineering, ejournal.warmadewa.ac.id. PERI Indonesia’s deployments across the Two Sudirman Tower, the JKT09 Data Center in Karawang, and the Terminal Kalibaru project in North Jakarta also demonstrated that a single modular platform can serve residential, industrial, and marine applications simultaneously.

The Indonesia formwork industry is likely to continue shifting toward modular systems as compliance and planning practices move in the same direction. The Ministry of Public Works is advancing broader BIM adoption throughout the current decade, making detailed formwork planning part of the preparation and review of larger projects. Contractors who include formwork layouts in tender-stage planning can reduce coordination errors before concrete placement begins, thereby supporting shorter cycle times. Conventional systems are not expected to disappear, as they still align with the cost profile of smaller sites and areas where logistics remain difficult. Even so, the value mix in the Indonesia formwork market is likely to move further toward modular and system products through 2031 as more projects prioritize repeatability, schedule control, and engineering support.

By Configuration: Climbing Formwork Enters Infrastructure Standard Practice

Static formwork accounted for 46% of demand in 2025, making it the leading configuration for applications such as slabs, flatwork, foundations, and single-repetition pours. Its large base came from the fact that many projects still did not need repositioning systems or vertical climbing solutions to meet schedule and cost targets. Climbing formwork is the fastest-growing configuration with an 8.54% CAGR through 2031, driven by two different project streams in the Indonesia formwork market. One stream comes from high-rise residential and commercial towers in Jakarta. In contrast, the other comes from shaft-heavy public works such as Mass Rapid Transit (MRT) stations, tunnels, spillways, and utility corridors. The MRT Phase 2A package is the clearest current example, because underground stations require dimensional control and working-at-depth capabilities that standard flat-form systems cannot provide.

Slipform and tunnel systems remain smaller in volume, but they occupy positions that are difficult to replace once the project method has been set. Continuous-pour structures such as silos, selected tunnel elements, and utility corridors depend on those methods to avoid interruptions and rework. WIKA’s use of sliding formwork at the IKN Multi Utility Tunnel in May 2026 provided a visible public-sector reference. It demonstrated that specialized systems deliver schedule benefits on technically demanding sites. That matters for the Indonesia formwork market because public references often influence future specification choices more than product catalog claims. As tunnel, transit, and high-rise infrastructure projects move forward, climbing and specialized configurations are likely to take a larger share of higher-value work even if static formwork remains the largest by installed volume.

By Business Model: Rental Penetration Deepens as Balance Sheets Tighten

Rental held 54% of the Indonesia formwork market size in 2025 and is forecast to grow at a 9.30% CAGR through 2031, making it the strongest business model. The leading position reflects working capital pressure across contractors operating under milestone-based payment systems and unable to keep large owned fleets active at all times. In practice, rental does more than lower upfront spending because it also gives users access to engineering design, delivery planning, and on-site support. That bundled structure has helped international suppliers such as PERI, Doka, and Kumkang Kind build stickier client relationships than bare-equipment providers can usually achieve. Local operators such as Indosteger, PT Cokrosoemitro Wirast Utama, and PT Tangga Mas Jaya Makmur remain competitive where delivery speed, local knowledge, and pricing matter most, especially around Greater Jakarta and Central Java.

The Indonesia formwork market is also showing a geographic difference within the rental model. Rental demand is growing quickly in outer-island and infrastructure zones, not only in Jakarta, because equipment procurement and mobilization windows are often too short for ownership to be practical. That makes rental the default execution choice in some projects rather than a purely financial choice. Lianggong Formwork’s delivery of H20 timber beam and cantilever climbing formwork for the BNI project in 2025 showed how overseas suppliers are also moving into the rental-adjacent space by combining certified products with more localized project support. As rental penetration deepens, supplier differentiation in the Indonesia formwork market will continue to rely on fleet continuity, engineering depth, and responsiveness rather than equipment access alone. That dynamic favors firms that can support both standard slabs and more technical climbing or tunnel-related packages within one commercial relationship.

By Sector: Infrastructure Commands Volumes, Data Centers Raise Specification Standards

Infrastructure accounted for 39% of the Indonesia formwork market in 2025 and is projected to expand at a 9.1% CAGR through 2031, making it both the largest and fastest-growing sector. The segment is supported by a steady pipeline of roads, bridges, dams, and transit projects that sustain demand for concrete structures across multiple construction cycles. Continued government investment through the 2026 public works budget and the 2025-2029 infrastructure development program is expected to maintain project activity, supported by both public funding and private-sector participation. Residential construction remained the second-largest sector, driven by repetitive wall, core, and slab applications in urban housing projects. Commercial demand is also evolving as data center construction requires higher floor load capacity, tighter dimensional tolerances, and greater precision in concrete placement than in conventional commercial buildings.

The Indonesia formwork market is expanding beyond its traditional reliance on public infrastructure and residential construction. PERI Indonesia's involvement in the JKT09 Data Center in Karawang demonstrates that engineered formwork systems are increasingly being adopted in digital infrastructure alongside institutional and port-related developments. Industrial and logistics projects are also becoming more demanding as multinational manufacturers require higher construction quality for factories, battery plants, warehouses, and assembly facilities. This trend is increasing demand for certified, repeatable, and engineering-led formwork solutions, even though project volumes remain lower than in infrastructure. As a result, the Indonesia formwork market is gradually shifting toward project segments where precision, construction efficiency, and technical support have become more important than upfront equipment cost.

By Material: Steel Holds the Volume, Aluminum Captures the Faster Growth

Steel accounted for 34% of demand in 2025, making it the largest material category in the Indonesia formwork market. Its leadership is supported by widespread local fabrication capability, proven structural performance, and lower procurement costs than aluminum for comparable panel sizes. Timber / plywood continues to serve small residential projects, remote locations, and highly cost-sensitive applications, although its role is gradually declining where repeated reuse and higher productivity are priorities. Aluminum is projected to record the fastest CAGR of 9.68% through 2031, driven by repetitive floor plates and housing projects where higher reuse cycles, faster construction, and lower labor requirements offset the higher initial investment.

Competitive dynamics within the material segment are also evolving. Kumkang Kind operates in Jakarta and supports the Indonesian market with engineering expertise backed by nearly 2.1 million m² of annual aluminum formwork manufacturing capacity across its Korean and Malaysian facilities. Doka's acquisition of MFE further strengthened its position in monolithic aluminum formwork across Southeast Asia, improving its ability to serve Indonesia's growing residential and affordable housing projects. Despite aluminum's faster growth, steel is expected to remain the preferred material for many civil, industrial, and general building applications because of its cost advantages and suitability for a broad range of project requirements. As a result, the Indonesia formwork market is likely to maintain a dual-material structure, with steel providing the largest volume base. At the same time, aluminum captures a growing share of high-repetition, productivity-focused, and value-added construction projects.

Geography Analysis

Jakarta held 38% of the Indonesian formwork market share in 2025 and is projected to grow at an 8.20% CAGR through 2031, keeping it as the country’s largest city-level demand center. The city combines underground MRT works, high-rise residential construction, commercial towers, data centers, and marine infrastructure, so suppliers are serving several distinct formwork applications simultaneously. Jakarta MRT Phase 2A continues to support tunnel and station box demand. At the same time, projects such as Two Sudirman Tower and Terminal Kalibaru show that premium systems are also active in above-ground commercial and port structures[3]PERI Indonesia, “Projects,” PERI Indonesia Official Website, peri.id. This makes Jakarta the clearest reference market in the Indonesian formwork market for suppliers seeking visibility across both standard and specialized applications.

Surabaya remains East Java’s main construction hub, and its demand is tied to industrial estates, urban housing, and commercial buildings that support logistics across eastern Indonesia. Bandung is becoming more important as city expansion, tourism-linked projects, and surrounding transport works expand the market for retaining walls, abutments, and slabs. While Medan anchors demand in Sumatra, the 2026 Inpres allocation of IDR 34.33 trillion (USD 2.1 billion) for irrigation, local roads, and school infrastructure should support broader regional civil works this year. These cities do not yet match Jakarta in depth. Still, they matter because they extend the Indonesia formwork market beyond one metro and create repeat demand for rental, fabricated steel, and modular systems. Their local supplier bases are also thinner than Jakarta’s, which gives firms with reliable logistics and engineering support a better chance to build share through project continuity.

The rest of Indonesia covers the market’s most underserved but strategically important demand areas, including Kalimantan, Sulawesi, Papua, Bali, and secondary cities across Sumatra. Nusantara Capital development in East Kalimantan is creating engineering-intensive requirements for government buildings, judicial infrastructure, and utility tunnels, and much of that capability still has to be mobilized from outside the immediate area. The target to complete 5,000 suspension bridges by the end of 2026 directs demand toward remote geographies where logistics can be a bigger constraint than technical specification. Bali also introduces a different demand pattern through large hospitality and mixed-use projects, as shown by PERI Indonesia’s DUO deployment at the Grand Outlet Bali project, suggesting that higher-specification systems are spreading into island-based commercial construction as well.

Competitive Landscape

The Indonesia formwork market remains moderately fragmented, with PERI SE and Doka holding the strongest international positions through engineering expertise, project execution experience, and well-established rental capabilities. Their competitive advantage extends beyond product offerings, as project-specific engineering, site supervision, and technical advisory services have become increasingly important on large and complex projects. Korean suppliers such as Kumkang Kind and KMF occupy a strong mid-tier position, particularly in aluminum formwork and civil engineering applications, while offering a more cost-competitive alternative to leading European brands. Local companies, including Indosteger, ALCA Metals, PT Cokrosoemitro Wirast Utama, and PT Tangga Mas Jaya Makmur, continue to maintain meaningful positions in conventional formwork and scaffolding-linked rental, where pricing, delivery speed, and long-standing contractor relationships remain key competitive factors.

Competitive pressure is also increasing from Chinese manufacturers, with Lianggong emerging as a notable challenger. The company established an Indonesian subsidiary, obtained SNI certification in 2025, and supplied H20 timber beam and cantilever climbing formwork for the BNI project, strengthening its presence in certified and cost-sensitive project segments. PERI has responded by expanding its service-led approach rather than competing primarily on price, while its training programs at the OASIS Central Sudirman project since August 2024 demonstrate how customer support has become an important element of client retention. Doka's acquisition of MFE has also reinforced its aluminum formwork capabilities across Southeast Asia, positioning the company to benefit from Indonesia's growing residential and affordable housing construction. These developments indicate that competition is increasingly driven by engineering capability, certification, technical support, and integrated project services rather than equipment supply alone.

The greatest competitive opportunities remain in engineering-led project support and outer-island market coverage. Suppliers that can provide Building Information Modeling (BIM)-compatible formwork layouts, pour-sequence optimization, and dependable fleet availability are better positioned to secure repeat business. At the same time, many regions outside Indonesia's major metropolitan areas remain underserved, where logistics capability, workforce training, and on-site technical support often influence contract awards as much as equipment pricing. As a result, the Indonesia formwork market is expected to remain moderately fragmented, with competition centered on technical capability, service quality, and regional execution strength rather than market dominance by a few suppliers.

Indonesia Formwork Industry Leaders

PERI SE

Doka GmbH

ULMA Construction

Acrow Formwork and Construction Services Ltd.

Alsina Formwork

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: PT Wijaya Karya (WIKA) deployed sliding formwork technology on the Multi Utility Tunnel at the Nusantara Capital's Judicial Complex Road project, achieving construction progress of 19.35% against a planned 18.29%, demonstrating improved execution efficiency on a major public infrastructure project.

- May 2026: Jakarta MRT Phase 2A reached 60.8% overall completion, while the CP202 package covering Harmoni, Sawah Besar, and Mangga Besar stations advanced to 65.61%. The project is expected to sustain demand for formwork systems as tunnel and underground station construction continues through 2026.

- December 2025: The Indonesian Ministry of Public Works finalized its 2026 budget at IDR 118.5 trillion (USD 7.3 billion), with road connectivity receiving the largest allocation of IDR 45.62 trillion (USD 2.8 billion), supporting continued demand for formwork across transport infrastructure projects.

Indonesia Formwork Market Report Scope

The Indonesia Formwork Market Report is Segmented by Type (Conventional /Traditional and Modular / System Formwork), Configuration (Static, Climbing, Slipform, and More), Business Model (Sales and Rental), Sector (Residential, Commercial, and More), Material (Timber / Plywood, Steel, Aluminum, Plastic/Fiberglass and More), and City (Jakarta, Surabaya, Bandung, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional / Traditional |

| Modular / System Formwork |

| Static |

| Climbing |

| Slipform |

| Tunnel |

| Sales |

| Rental |

| Residential |

| Commercial |

| Industrial and Logistics |

| Infrastructure |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fiberglass |

| Other Materials |

| Jakarta |

| Surabaya |

| Bandung |

| Medan |

| Rest of Indonesia |

| By Type | Conventional / Traditional |

| Modular / System Formwork | |

| By Configuration | Static |

| Climbing | |

| Slipform | |

| Tunnel | |

| By Business Model | Sales |

| Rental | |

| By Sector | Residential |

| Commercial | |

| Industrial and Logistics | |

| Infrastructure | |

| By Material | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fiberglass | |

| Other Materials | |

| By City | Jakarta |

| Surabaya | |

| Bandung | |

| Medan | |

| Rest of Indonesia |

Key Questions Answered in the Report

What is the current size and outlook for formwork demand in Indonesia?

The Indonesia formwork market stands at USD 0.21 billion in 2026 and is forecast to reach USD 0.30 billion by 2031 at a 7.39% CAGR.

Which product type currently leads demand in Indonesia?

Modular / system formwork led with 58% of demand in 2025, showing that reusable engineered systems are now the main product base for larger and more repetitive projects.

Why is rental growing faster than direct sales?

Rental held 54% of demand in 2025 and is growing at 9.30% CAGR because contractors want lower upfront spending, faster mobilization, and bundled engineering support.

Which end-use sector creates the largest volume opportunity?

Infrastructure is the largest sector with 39% of demand in 2025, and it is also the fastest-growing at 9.10% CAGR through 2031 because of roads, transit, bridges, and utility works.

Page last updated on: