China Scaffolding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

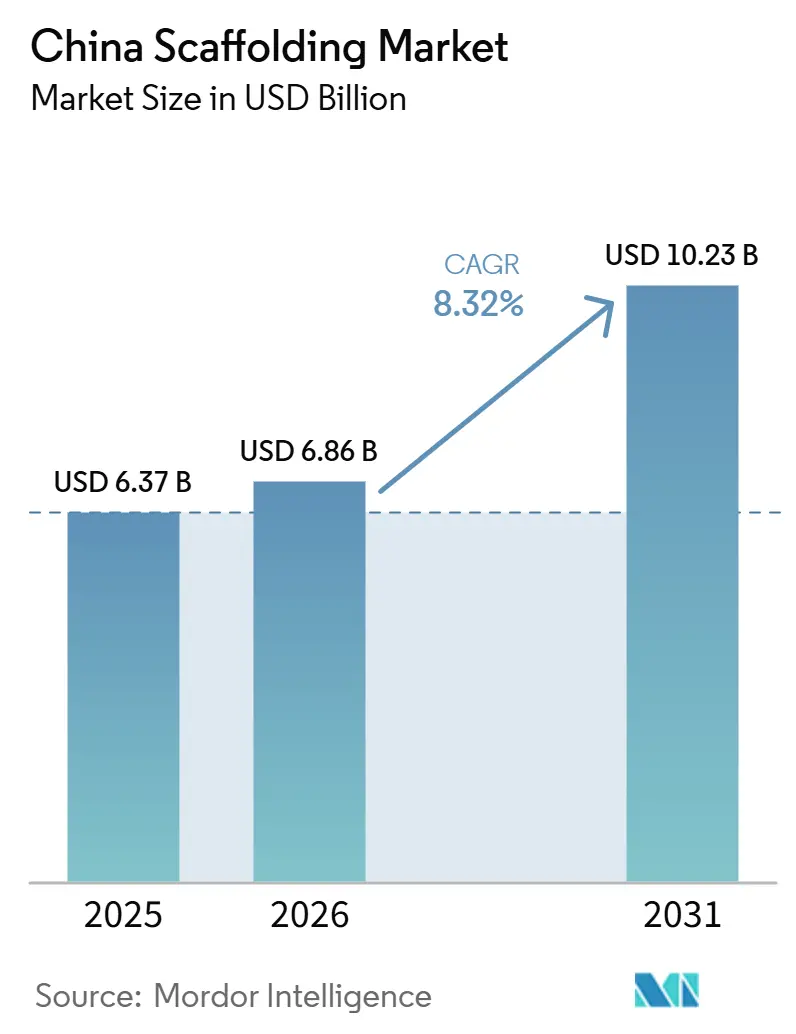

| Base Year Market Size (2025) | USD 6.37 Billion |

| Market Size (2026) | USD 6.86 Billion |

| Market Size (2031) | USD 10.23 Billion |

| Growth Rate (2026 - 2031) | 8.32% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Scaffolding Market Analysis by Mordor Intelligence

The China Scaffolding Market size was valued at USD 6.37 billion in 2025 and is estimated to grow from USD 6.86 billion in 2026 to reach USD 10.23 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031).

The China scaffolding market is supported by a stronger public works cycle, with infrastructure investment in China rising 8.9% year over year in the first quarter of 2026, well ahead of the broader fixed-asset growth trend. The policy backdrop is also favorable because the 15th Five-Year Plan directs major spending toward power grids, urban pipelines, industrial facilities, and transport corridors that require access systems over long construction periods. The China scaffolding market is also benefiting from a gradual shift toward modular systems that are easier to deploy under tighter safety rules and more complex site conditions. At the same time, the property downturn is still limiting part of the addressable demand base, since real estate development investment in China continued to fall in 2026 and kept residential construction under pressure. This leaves room for growth in the China scaffolding market through rental services, infrastructure-focused fleets, industrial project access, and premium engineering support, where local price competition is less intense.

Key Report Takeaways

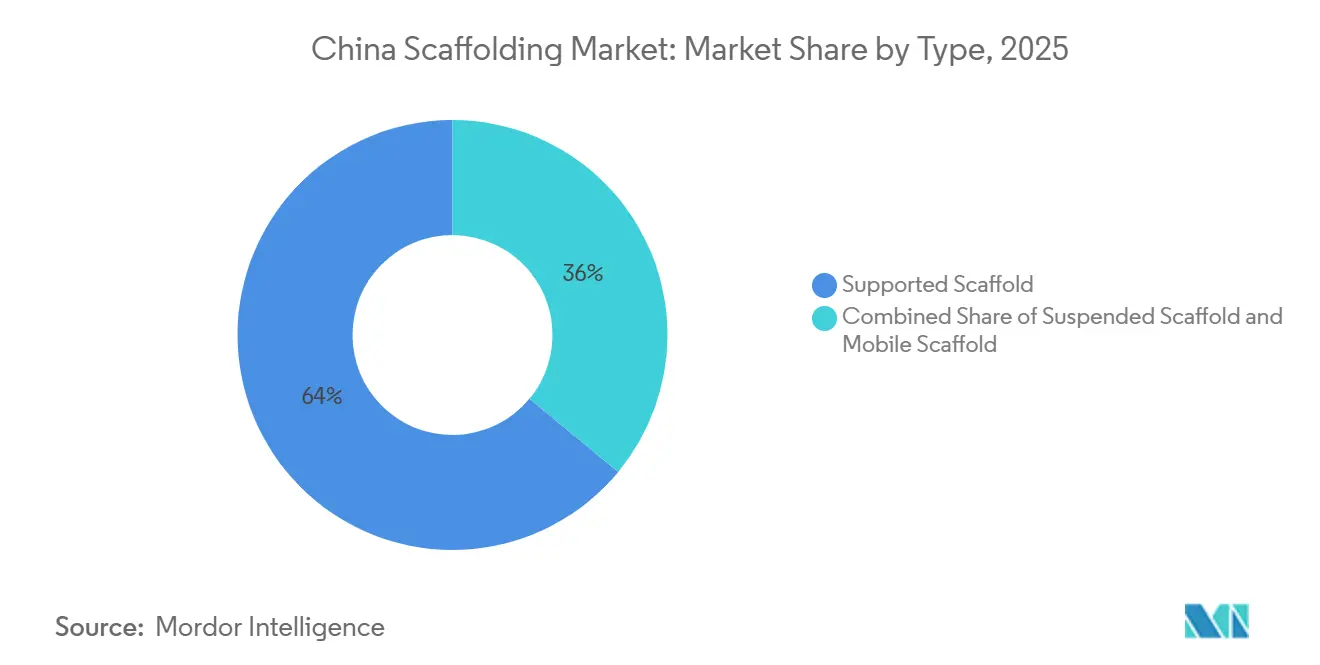

- By type, the supported scaffold held 64% of the China scaffolding market share in 2025, while the mobile scaffold is projected to grow at a 9.9% CAGR through 2031.

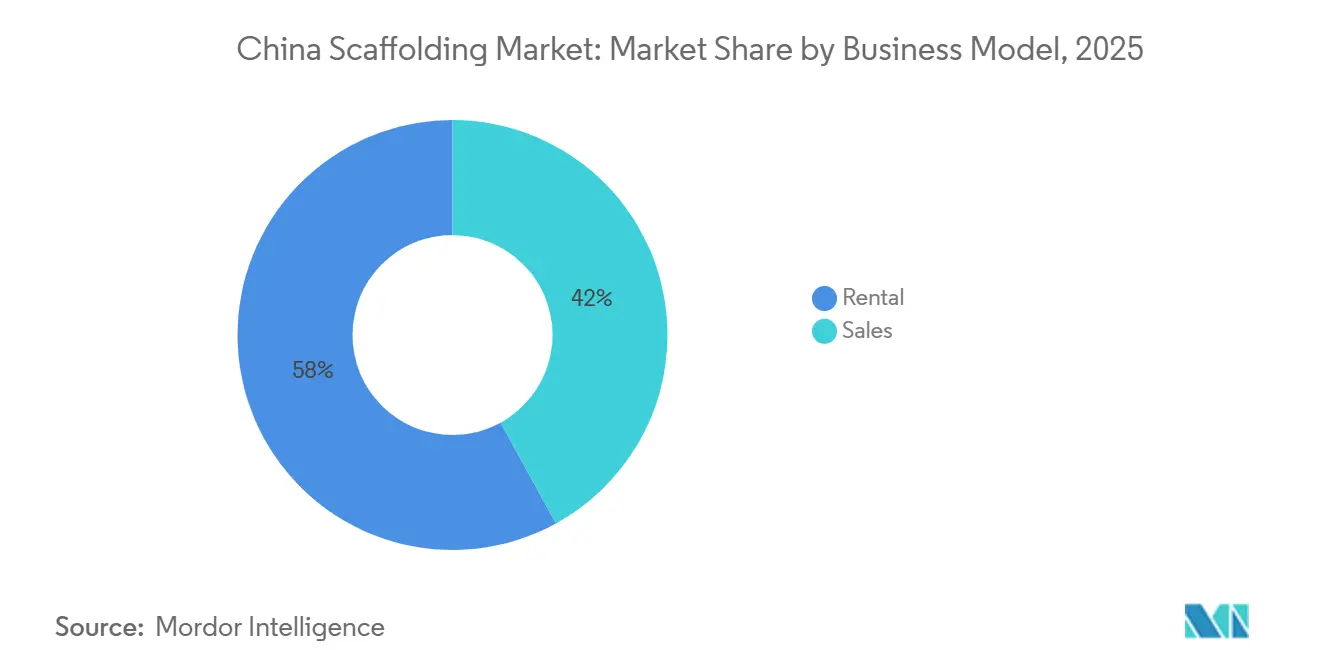

- By business model, rental held 58% of the China scaffolding market share in 2025 and is also forecast to grow at 9.3% CAGR through 2031.

- By material type, steel accounted for 69% of the China scaffolding market size in 2025, while aluminum is expected to expand at 9.8% CAGR through 2031.

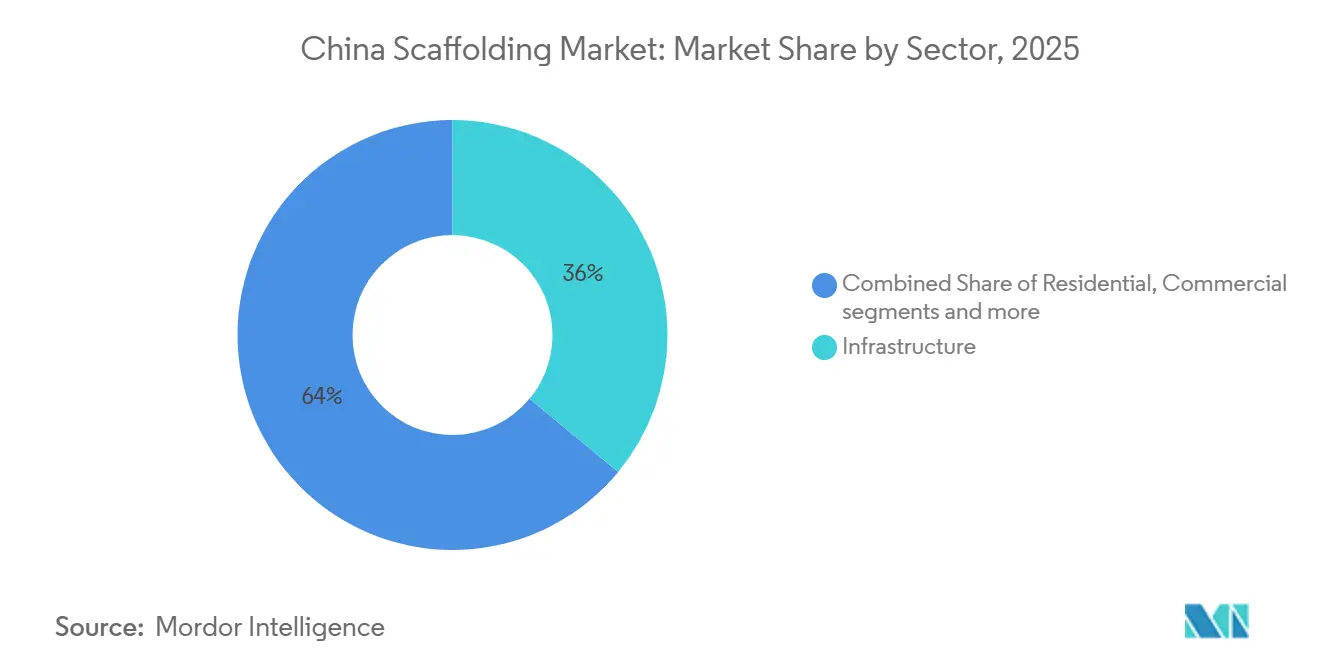

- By sector, infrastructure captured 36% share of the China scaffolding market size in 2025, while industrial and logistics is set to record the highest CAGR at 9.33% through 2031.

- By region, East China held 28% of the China scaffolding market share in 2025, while Southwest China is projected to grow fastest at 10.2% CAGR through 2031.

- By system, modular or ringlock accounted for 41% of the segment in 2025 and is also the fastest-growing system, with a 10.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Scaffolding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-Led Construction Spending Drives Scaffolding Demand | +2.5% | National, with stronger demand in East China, North China, and Southwest China | Long term (≥ 4 years) |

| Shift Toward Modular and Reusable Systems Supports Market Modernization | +1.8% | National, with earlier uptake in large coastal construction hubs | Medium term (2-4 years) |

| Rising Labor Costs and Workforce Shortages Accelerate System Scaffolding Adoption | +1.2% | National, with sharper pressure in major urban construction centers | Medium term (2-4 years) |

| Growth in Industrial and Energy Projects Increases Scaffolding Requirements | +1.0% | Southwest China, North China, Central China, and selected South China clusters | Long term (≥ 4 years) |

| Export-Oriented Manufacturing Base Supports Scaffolding Production and Demand | +0.8% | East China and South China manufacturing belts | Medium term (2-4 years) |

| Expansion of Transportation Infrastructure Projects Boosts Scaffolding Utilization | +0.7% | National, with notable intensity in East China and Southwest China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Construction Spending Drives Scaffolding Demand

The China scaffolding market is closely tied to the country’s public investment cycle, and 2026 shows a clear shift back toward infrastructure-led construction. China’s 2026 budget framework included USD 103.9 billion in central government investment, along with ultra-long-term treasury support and a large local government bond pipeline for public works and related projects[1]Ministry of Finance, “2026 Report on Budgets,” Ministry of Finance, npcobserver.com. Infrastructure investment rose 8.9% year over year in the first quarter of 2026, with particularly strong activity in civil aviation and waterway transport, both of which require large, recurring access needs from early civil works through fit-out and maintenance. The 15th Five-Year Plan also directs more spending toward power grids, urban pipelines, and industrial facilities, pushing demand away from short residential cycles and toward longer public programs. This gives the China scaffolding market a steadier project base and supports suppliers that can serve long-duration infrastructure projects with dependable fleet availability and engineering support.

Shift Toward Modular and Reusable Systems Supports Market Modernization

The China scaffolding market is moving toward modular, reusable systems because project owners want faster assembly, greater consistency, and fewer safety incidents on large sites. This shift is being reinforced by updated technical requirements under the Ministry of Housing and Urban-Rural Development framework for disk-lock scaffolding and by provincial safety specifications for suspended access systems[2]National Digital Library of Standards, “DB32/T 5173-2025 Safety Technical Standards for Cantilevered Steel Pipe Scaffolding in Construction,” National Digital Library of Standards, ndls.org.cn. These rules make it harder for older low-standard configurations to compete on regulated projects, especially where inspection, traceability, and structural performance matter more than upfront price. Contractors also prefer systems that can move across bridges, as well as for industrial, logistics, and commercial work, with less adjustment and less wasted time between phases. Over time, this supports a higher-quality fleet mix in the China scaffolding market and gives system-led suppliers an advantage over firms that still depend mainly on commodity tube-and-coupler offerings.

Rising Labor Costs and Workforce Shortages Accelerate System Scaffolding Adoption

China’s construction workforce shrank sharply between 2021 and 2025, even though the sector remained one of the country’s better-paying major industries. In 2025, the number of workers directly involved in construction fell further, which added pressure on project execution and labor availability. Skilled trade shortages in major cities are also pushing wages higher and making it harder for contractors to stay on schedule. As a result, contractors are moving toward scaffolding systems that can be erected faster and with fewer workers. This is strengthening demand for modular and aluminum systems, since they offer a practical way to reduce labor intensity and improve site productivity.

Growth in Industrial and Energy Projects Increases Scaffolding Requirements

Industrial and energy construction is becoming a stronger source of demand for the China scaffolding market as the country increases spending on grid upgrades, industrial capacity, and strategic facilities. In May 2026, China allocated USD 29.8 billion from ultra-long treasury bonds to 336 national strategy projects, many of which were tied to energy security, industrial capacity, and urban infrastructure. The same policy package highlighted long-range spending on power grid upgrades, which creates repeated demand for access systems at towers, substations, and related transmission works. Safety rules are also tightening in industrial settings, as the 2025 petrochemical steel scaffold standard raised expectations for inspection and technical compliance on refinery and chemical sites[3]Ministry of Industry and Information Technology, “SH/T 3555-2025 Technical Standard for Safety of Steel Scaffold in Petrochemical Industry,” Code of China, codeofchina.com. This keeps the China scaffolding market aligned with industrial maintenance and energy project demand, where technical requirements are higher and rental fleets need stronger certification discipline.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak Property-Led Construction Demand Limits Market Growth Opportunities | -1.5% | National, most visible in residential-heavy local markets | Long term (≥ 4 years) |

| Raw Material Price Volatility Pressures Manufacturer Margins | -1.0% | National, tied to steel and aluminum procurement cycles | Medium term (2-4 years) |

| Fragmented Lower-Tier Supplier Base Intensifies Market Competition | -0.8% | National, with stronger pricing pressure in core production clusters | Short term (≤ 2 years) |

| High Compliance Requirements Increase Operational and Certification Costs | -0.6% | National, with a greater burden in industrial and cross-provincial activity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Weak Property-Led Construction Demand Limits Market Growth Opportunities

The property downturn remains the clearest drag on the China scaffolding market, as residential construction once generated strong demand for facade, fit-out, and finishing. Real estate development investment in China fell 13.7% year over year in January through April 2026, and newly started floor space also declined sharply during the same period. This reduces order flow for suppliers that historically depended on apartment and mixed-use projects, especially in lower-tier markets with heavier exposure to housing starts. Infrastructure and industrial projects are offsetting part of this loss, but they do not always replace residential volume at the same speed or with the same margin structure. That is why the China scaffolding market still carries a property-linked headwind even with stronger public works spending in 2026.

Raw Material Price Volatility Pressures Manufacturer Margins

Steel and aluminum prices moved in opposite directions in 2025 and 2026, which created uneven cost pressure for manufacturers and rental companies with mixed fleets. Steel prices declined, lowering input costs for steel scaffolding but also reducing the scrap value of older steel assets. Aluminum prices, on the other hand, increased sharply, raising the cost of fleet upgrades and new equipment purchases. This has made the shift from steel to aluminum more expensive, even as demand for mobile and modular systems grows. As a result, margin pressure is increasing for companies trying to reposition their fleets toward faster-growing product categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Supported Scaffold Dominates While Mobile Systems Gain Ground

Supported scaffolding accounted for 64% of the China scaffolding market in 2025, reflecting the continued practicality of ground-supported access across bridges, industrial works, utilities, and large civil structures. This part of the China scaffolding market remains dominant because it handles heavy loads and adapts well to long-duration infrastructure projects where reliability matters more than frequent repositioning. It also benefits from the installed base of rental fleets that already carry large quantities of supported systems and can redeploy them across transport, energy, and general contracting work. Suspended scaffold keeps a smaller but steady role in facade access, maintenance, and projects where ground-based support is limited by site design or elevation.

Mobile scaffold is the fastest-growing type, with a forecast CAGR of 9.9% through 2031, and that growth reflects changing site priorities rather than a short-term spike. Contractors are using more mobile towers in interior fit-out, logistics buildings, and maintenance programs where crews need faster repositioning and less setup time between tasks. This pattern fits the wider construction mix as warehousing, industrial facilities, and service-oriented project work expand more quickly than the residential segment. Over the forecast period, mobile systems will still trail supported scaffold in total volume. Still, their role will continue to expand in projects where flexibility and quick movement matter more than maximum static load.

By System: Modular / Ringlock Consolidates its Leadership

Modular / ringlock accounted for 41% of the system segment in 2025, making it the leading system category in the China scaffolding market. Its position is strong because it can serve infrastructure, industrial, and commercial work without the same labor intensity or assembly variability seen in older configurations. Ringlock systems also align with the direction of the China scaffolding market, where customers increasingly want repeatable performance, faster deployment, and cleaner compliance with stricter technical rules. Tube & coupler remain relevant for irregular structures and certain legacy sites, while cuplock and frame systems remain useful for selected repetitive or lighter-duty tasks.

Modular / ringlock is also the fastest-growing system, with a forecast CAGR of 10.4% through 2031, reinforcing the view that this is a structural shift rather than a temporary preference. Contractors working on fast-track infrastructure and industrial sites value modular designs because they shorten erection time and reduce on-site complexity. The category also aligns well with the need for stronger safety performance and easier inspection. Over the next several years, ringlock should continue to pull share from older systems, though legacy configurations will remain in use where project conditions or budgets are narrower.

By Business Model: Rental is the Structural Winner

Rental accounted for 58% of the China scaffolding market in 2025, confirming that access equipment is increasingly treated as a service rather than a balance-sheet asset. This model works well because many contractors need equipment only for defined project phases and prefer to avoid capital tie-up, storage costs, transport complexity, and compliance administration. Rental also aligns with the current structure of the China scaffolding market, where project pipelines are uneven across sectors and fleet flexibility gives operators a better chance to shift equipment toward stronger regions and end uses. Larger rental firms can support customers with design help, delivery scheduling, site setup, inspection records, and replacement inventory, which makes them more valuable on complex jobs than a simple equipment sale.

The rental model is also expected to grow at a 9.3% CAGR through 2031, indicating it is not only the largest segment but also one of the most resilient. This growth is supported by public infrastructure, logistics construction, and industrial work, where fleets can remain active over long schedules without requiring customers to own equipment outright. The model is becoming stronger as customers look for operators that can pair supply with engineering advice, safety documentation, and better visibility into asset use. In the China scaffolding market, this points to a service-led structure where scale, compliance discipline, and utilization management matter as much as the physical equipment itself.

By Material Type: Steel Leads, but Aluminum Emerges as the Efficiency Lever

Steel accounted for 69% of the China scaffolding market in 2025, and that leadership reflects cost familiarity, broad fleet availability, and a strong fit with heavy civil and industrial work. Steel remains the backbone of the China scaffolding market because it better meets the load requirements of bridges, tunnels, power projects, and petrochemical sites than lighter alternatives in many use cases. It also benefits from entrenched contractor preference, as site teams across China are deeply familiar with steel systems in both rental and owned-equipment formats. In addition, much of the installed rental base is still steel-based, so replacement takes time even when end users show interest in lighter materials.

Aluminum is the fastest-growing material segment, with a forecast CAGR of 9.8% through 2031, because its lighter weight improves handling speed and reduces physical strain during setup and dismantling. This matters more as contractors focus on labor efficiency, especially on interior projects, repetitive floor work, and maintenance programs that require frequent movement. Even so, aluminum will expand unevenly across the China scaffolding market, because heavy infrastructure and some industrial settings still favor the load profile and lower acquisition cost of steel. The likely outcome is a more mixed material base, with aluminum gaining share in commercial, high-access, and service-intensive applications while steel stays stronger in the heaviest end uses.

By Sector: Infrastructure Anchors Demand While Industrial and Logistics Accelerate

Infrastructure accounted for 36% of the China scaffolding market in 2025, which made it the largest end-use sector by revenue. This reflects the simple fact that transport, energy, water, and utility programs now supply the broadest and most visible order base for access systems across China. Infrastructure projects suit the China scaffolding market because they require high volumes, long schedules, repeated maintenance access, and strong engineering coordination from the early structural phase onward. In this setting, infrastructure remains the stabilizing base of the China scaffolding market because it is less exposed to changes in private buyer sentiment than housing.

Industrial and logistics is the fastest-growing sector, with a forecast CAGR of 9.33% through 2031, and that growth reflects several demand streams moving together. New logistics centers, energy facilities, manufacturing parks, and warehouse-linked construction all require staged access from structural works through mechanical, electrical, and plumbing installation. This segment is also benefiting from the expansion of automated warehousing and supply-chain infrastructure in both coastal and inland markets. For the China scaffolding market, this means industrial and logistics demand is no longer a small adjacent niche, but a core growth engine with longer-term relevance.

Geography Analysis

East China accounted for 28% of the China scaffolding market in 2025, making it the largest regional market by revenue. This leadership comes from the depth of project activity across Shanghai, Jiangsu, and Zhejiang, where transport, industrial, logistics, and export-linked construction overlap in a concentrated area. The region also benefits from major infrastructure, logistics, and manufacturing projects that lengthen equipment deployment cycles. These projects require years of access support rather than short bursts of equipment delivery, which helps stabilize regional fleet use. East China, therefore, remains the operational center of the China scaffolding market because it combines scale, project diversity, and stronger demand for higher-value systems.

North China and South China form the second layer of regional demand, but their roles differ within the China scaffolding market. North China relies heavily on the supply side because it is tied to manufacturing capacity and industrial corridors that generate steady maintenance and construction needs. South China, by contrast, shows stronger demand for technically complex coastal and bay-area projects, including bridge and logistics-related work. China's scaffolding market thrives on the production prowess of one region and the premium project demands of another.

Southwest China is the fastest-growing region, with a forecast CAGR of 10.2% through 2031, and that momentum is tied to a large project pipeline across transport, industrial, and urban infrastructure. The region is benefiting from stronger capital deployment in the Chengdu-Chongqing economic zone and related inland development programs. Central China is also becoming more relevant as policy and industrial investment shift inland, although it still depends on equipment flows from stronger production regions. This leaves the China scaffolding market with a regional pattern where East China holds scale leadership, while Southwest China sets the pace for future growth.

Competitive Landscape

The China scaffolding market is fragmented with premium global specialists at the top, strong domestic specialists in the middle, and a wide base of smaller, price-led suppliers at the bottom. Doka and PERI maintain their strongest positions in technically demanding work, where engineering capability, safety assurance, and complex geometry matter more than simple equipment supply. In the China scaffolding market, this premium tier does not compete on price with the full domestic base. Still, it remains influential wherever technical risk is high and failure costs are severe. That keeps the market competitive unevenly, with quality-led competition at the top and price-led competition across much of the middle and lower end.

Domestic leaders are strengthening their position by combining local production economics with smarter manufacturing, broader channel reach, and selective overseas expansion. GETO New Materials is one example of a domestic player using smart manufacturing and international reach to build a stronger competitive position. State-owned enterprise contractors also shape the China scaffolding market because some maintain captive access and formwork capacity, which reduces the amount of premium work available to third-party providers. This pushes independent suppliers to differentiate through engineering services, compliance and quality, or rental responsiveness, rather than relying solely on commodity equipment volume.

Technology and compliance are becoming more important sources of competitive advantage in the China scaffolding market. Operators that can document inspections, track fleets, and support project planning digitally are better positioned to win industrial and infrastructure work under tighter standards. This raises the pressure on smaller firms that still compete mainly on spot pricing and low-standard inventory. Over time, the China scaffolding market is likely to see more consolidation in the mid-tier, not because competition disappears, but because the cost of meeting safety, documentation, and project-delivery expectations keeps rising. The result is a market where fragmentation remains high, yet sustainable advantage increasingly comes from scale, system quality, and dependable execution.

China Scaffolding Industry Leaders

Doka (China) Co., Ltd.

PERI China

Beijing Zulin Formwork & Scaffolding Co., Ltd.

Qingdao Alulite Formwork Scaffolding Co., Ltd.

KITSEN Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The Chong-Qi Yangtze River combined road-rail cable-stayed bridge achieved main bridge closure on June 9, 2026, marking a major milestone for one of China’s most technically complex bridge programs on the Shanghai-Nanjing-Chongqing high-speed rail corridor.

- April 2026: China allocated USD 29.8 billion in ultra-long special treasury bond funding to 336 national strategy projects across energy security, industrial capacity, and urban infrastructure, which supported near-term procurement activity across multiple construction categories.

- March 2026: The Haitai Yangtze River Tunnel passed the 50% construction milestone in its right-line shield section and remained on track for a 2028 opening, extending the visibility of tunnel-related access demand.

China Scaffolding Market Report Scope

The China Scaffolding Market Report is Segmented by Type (Supported, Suspended, and Mobile), System (Tube & Coupler, Cuplock, Modular / Ringlock, and More), Business Model (Sales and Rental), Material Type (Timber / Plywood, Steel, and More), Sector (Residential, Commercial, Industrial & Logistics and More), and Region (North, East, South, Central, Southwest China). The Market Forecasts are Provided in Terms of Value (USD).

| Supported Scaffold |

| Suspended Scaffold |

| Mobile Scaffold |

| Tube & Coupler |

| Cuplock |

| Modular / Ringlock |

| Frame / H-Frame |

| Sales |

| Rental |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| North China |

| East China |

| South China |

| Central China |

| Southwest China |

| By Type | Supported Scaffold |

| Suspended Scaffold | |

| Mobile Scaffold | |

| By System | Tube & Coupler |

| Cuplock | |

| Modular / Ringlock | |

| Frame / H-Frame | |

| By Business Model | Sales |

| Rental | |

| By Material Type | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By Region | North China |

| East China | |

| South China | |

| Central China | |

| Southwest China |

Key Questions Answered in the Report

What is the 2026 outlook for China scaffolding demand?

The China scaffolding market is estimated at USD 6.86 billion in 2026 and is projected to reach USD 10.23 billion by 2031.

What is driving growth in scaffolding demand across China?

Infrastructure construction, industrial projects, logistics facilities, and the shift toward modular systems are the main growth drivers.

Which segment leads by revenue in China?

Supported scaffold led by type with 64% share in 2025, steel led by material with 69%, rental led by business model with 58%, modular / ringlock led by system with 41%, and infrastructure led by sector with 36%.

Which segment is growing fastest through 2031?

Industrial & logistics is the fastest-growing sector at 9.33% CAGR, while mobile scaffold is the fastest-growing type at 9.9%, and Southwest China leads among regions at 10.2%.

Why is rental so important in scaffolding supply?

Rental helps contractors avoid ownership costs, improves fleet flexibility, and shifts compliance and service obligations to specialized providers. That is why rental already held 58% share in 2025.

What is the biggest risk to future expansion?

The main risk remains the property downturn, which continues to weigh on residential construction activity and limits demand.

Page last updated on: