Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

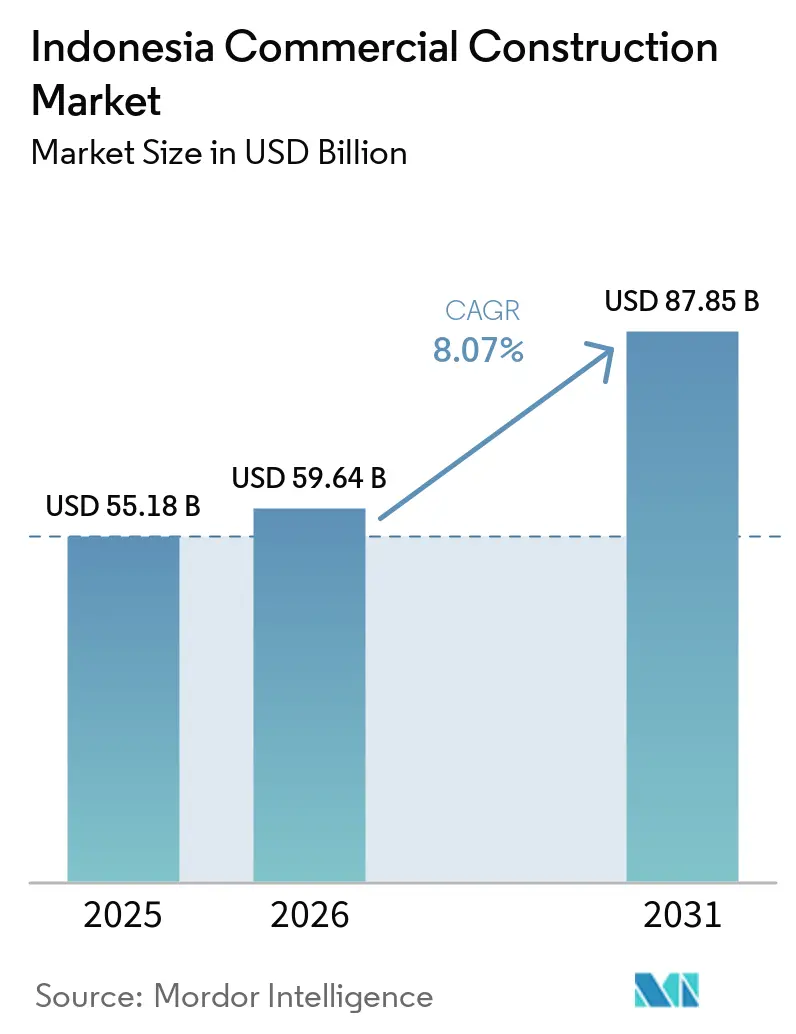

| Base Year Market Size (2025) | USD 55.18 Billion |

| Market Size (2026) | USD 59.64 Billion |

| Market Size (2031) | USD 87.85 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Commercial Construction Market Analysis by Mordor Intelligence

The Indonesia Commercial Construction Market size was valued at USD 55.18 billion in 2025 and estimated to grow from USD 59.64 billion in 2026 to reach USD 87.85 billion by 2031, at a CAGR of 8.07% during the forecast period (2026-2031). Rapid urban migration, steady economic growth, and the Vision 2045 agenda keep demand high for offices, malls, hotels, data centers, and logistics hubs. Government stimulus through the National Strategic Projects, public-private partnership (KPBU) mechanisms, and a more transparent permitting regime has intensified project pipelines. Private developers are capitalizing on the rising middle-class consumer base, while foreign contractors bring advanced engineering and green-building know-how that elevate quality standards. Supply-chain re-routing and e-commerce expansion are tilting fresh capital toward modern logistics assets, data infrastructure, and transit-oriented mixed-use nodes, creating multi-cycle growth prospects for the Indonesia Commercial Construction market.

Key Report Takeaways

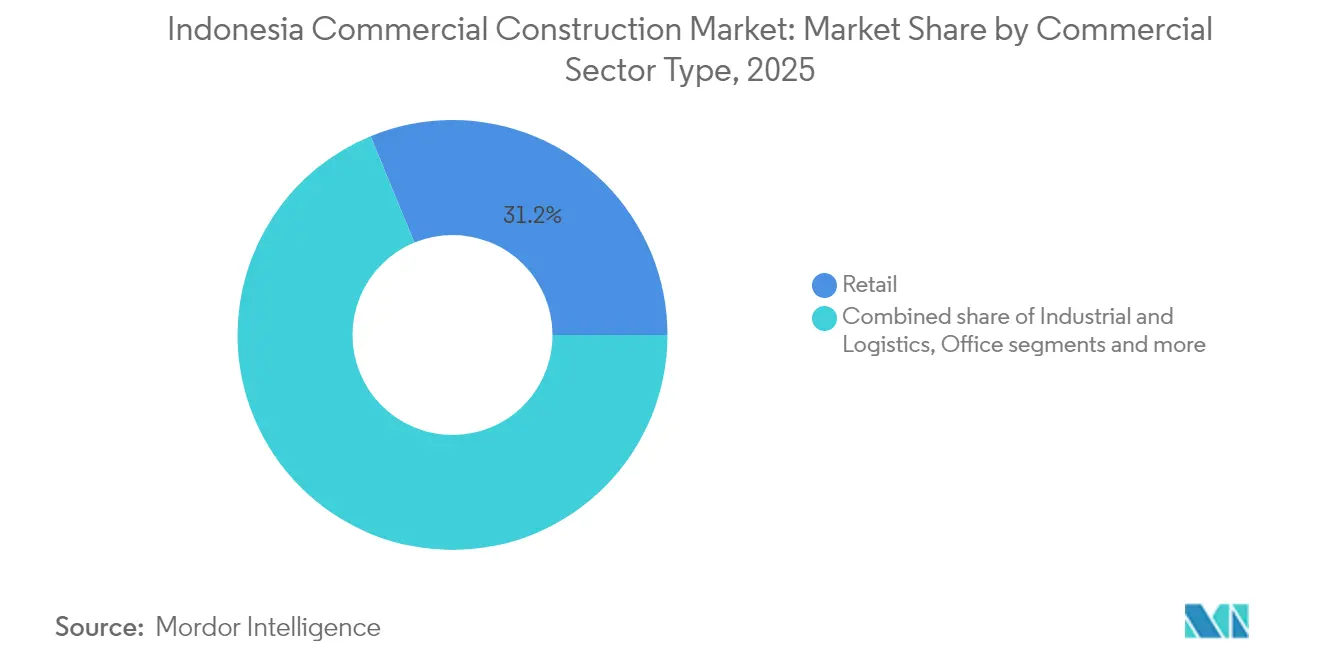

- By commercial sector type, retail captured 31.22% of Indonesia Commercial Construction market share in 2025; industrial & logistics is projected to grow at 8.93% CAGR through 2031.

- By construction type, new construction commanded a 72.85% share of the Indonesia Commercial Construction market size in 2025, while renovation registers the fastest 8.73% CAGR to 2031.

- By investment source, private capital held 65.15% of the Indonesia Commercial Construction market size in 2025; public investment shows a higher 8.49% CAGR over the forecast window.

- By region, DKI Jakarta led with 39.55% Indonesia Commercial Construction market share in 2025, whereas East Java records the quickest 9.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Commercial Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail chain expansion plans driving mall and lifestyle center construction in major cities | +1.2% | DKI Jakarta, West Java, East Java | Medium term (2-4 years) |

| Corporate demand for Grade-A office space supporting developments in Jakarta and tier-2 cities | +0.9% | DKI Jakarta, West Java core cities | Short term (≤ 2 years) |

| Integrated mixed-use projects gaining traction under city-led development frameworks | +0.8% | National, with concentration in Jakarta, Surabaya, Bandung | Medium term (2-4 years) |

| Transit-oriented developments (TODs) emerging near new rail and toll road corridors | +0.7% | DKI Jakarta, West Java, East Java | Long term (≥ 4 years) |

| Tourism sector recovery fueling hotel, resort, and supporting retail construction | +0.6% | Bali, Jakarta, emerging tourist destinations | Short term (≤ 2 years) |

| Increased foreign participation boosting investments in commercial and high-rise assets | +0.5% | National, with focus on Jakarta and tier-1 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Retail chain expansion plans drive urban commercial development

Indonesia's retail sector is witnessing robust growth, fueled by increasing disposable incomes and changing consumer preferences. Modern retail groups are accelerating new mall and lifestyle-center rollouts to capture rising disposable incomes and evolving consumer habits. Retail sales climbed to USD 46.34 billion in 2022 and are forecast to hit USD 71.89 billion by 2031, and developers respond by clustering retail, entertainment, and F&B at high-footfall nodes. Projects such as the USD 2.56 billion PIK 2 township in North Jakarta integrate shops, theme parks, and waterfront promenades in one destination, signaling a pivot toward experiential formats. As land prices inside the capital climb, chains increasingly target satellite cities where plots are larger and zoning is flexible. This steady pipeline sustains demand for architects, MEP consultants, and fit-out specialists across the Indonesia Commercial Construction market[1]Directorate General for National Export Development, “Indonesia Retail Sales Outlook 2022-2031,” Ministry of Trade, djpen.kemendag.go.id .

Corporate demand for Grade-A office space supports premium developments

Corporate demand for Grade-A office spaces is driving premium developments in Jakarta's CBD. Prime office rents in Jakarta’s CBD ticked up 0.7% year-on-year in Q3 2024, the first meaningful rise since 2015, reflecting renewed occupier confidence jll.co.id. Despite a still-high 70% occupancy level across 9.3 million sqm, multinationals in tech, finance, and advanced manufacturing are locking in larger floorplates to accommodate back-to-office mandates. Flagship towers such as the 260-meter Sahid Sudirman Center illustrate the shift toward mixed-use vertical campuses that stack offices, retail, and hospitality. Foreign direct investment in manufacturing jumped 18.6% in 2024, linking production expansion with needs for regional headquarters and support services. These trends underpin stable take-up for green, flexible, and digitally enabled workspaces in the Indonesia Commercial Construction market.

Integrated mixed-use projects gain momentum under urban planning frameworks

By combining work, living, and leisure spaces, mixed-use complexes effectively address land shortages and alleviate traffic congestion. Mitsubishi Estate’s USD 332 million Two Sudirman twin-towers will add 150,000 sqm of strata and rental space upon 2028 completion, anchoring a broader district vision in Jakarta. Authorities have streamlined one-stop permit centers for such schemes, shortening approval cycles and enticing capital from Japan, South Korea, and Singapore. Diversified revenue streams from condos, offices, and retail lower risk exposure for developers, while tenants welcome the convenience of co-located amenities. Sustainability features—from low-E façades to smart energy grids—command rental premiums and future-proof assets in the Indonesia Commercial Construction market.

Transit-oriented developments transform urban connectivity corridors

Transit-oriented developments (TODs) are emerging as a transformative force in urban planning, reshaping connectivity corridors and fostering sustainable growth. Financed in part by a USD 1.678 billion loan from JICA, the 11.8 km MRT Jakarta Phase 2 line is giving rise to bustling commercial hubs at stations such as Kota and Mangga Dua. Under Governor Regulation 15/2020, the MRT operator has been appointed as the corridor manager, enabling a cohesive approach to land use, air rights, and public realm design. Developers are racing to acquire plots within a 400-meter radius, where increased foot traffic can boost retail turnover by 20-30%. Transit-oriented developments (TODs) not only shorten commuting times but also reduce CO₂ emissions, supporting the city’s ambition for net-zero emissions by 2030. Looking ahead, similar rail-centric districts in Bandung and Surabaya are poised to adopt this model, further expanding Indonesia's commercial construction market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High construction input costs putting pressure on commercial project margins | -1.4% | National, with acute impact in Jakarta and major cities | Short term (≤ 2 years) |

| Zoning and permit delays continuing to slow project approvals and groundbreakings | -0.8% | National, particularly affecting complex mixed-use projects | Medium term (2-4 years) |

| Financing limitations affecting speculative and mid-scale commercial developments | -0.6% | National, with greater impact on tier-2 cities | Medium term (2-4 years) |

| Excess office and retail supply in some urban markets dampening new launches | -0.4% | DKI Jakarta, select tier-1 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High construction input costs pressure project viability

In 2024, cement sales in Indonesia dipped by 0.9% year-on-year, totaling 64.9 million tons. Meanwhile, output saw a modest uptick of 1%. This scenario underscores the margin compression faced by producers grappling with tepid demand. Steel prices, influenced by energy market fluctuations, have been erratic. This volatility has led to a surge in structural frame budgets, escalating costs by as much as 15%. In response, developers are either pivoting to lighter modular designs or intensifying local sourcing efforts when possible. While there's a rising trend in adopting recycled aggregates and low-carbon cement, scaling these practices is essential to bridge existing cost disparities. Given the recent cost surges, many are adopting phased construction strategies. These align cash expenditures with milestones like pre-leases or pre-sales, a trend becoming prominent in Indonesia's commercial construction landscape.

Zoning and permit delays create project execution risks

Complex mixed-use and public-private projects must navigate overlapping jurisdictions, lengthening pre-construction periods by six to nine months. Regulation No. 7/2024 on sustainable business development adds new documents covering energy modeling and life-cycle analysis, increasing compliance workloads. High-profile schemes such as the Dhoho Airport and the Java sea-wall have demonstrated how land acquisition and environmental reviews can bottleneck timelines. Lenders now insist on greater contingency buffers to cover potential delays, raising financing costs. Streamlined digital portals and one-map policy rollouts are expected to ease friction gradually, but near-term hurdles persist for the Indonesia Commercial Construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commercial Sector Type: Industrial & Logistics takes the growth lead

Industrial & logistics assets delivered the fastest 8.93% CAGR forecast between 2026 and 2031, although retail retained a 31.22% Indonesia Commercial Construction market share in 2025. Supply-chain restructuring and e-commerce growth lowered logistics costs to 14.29% of GDP in 2023, down from 23.80% in 2018, catalyzing warehouse and inland-port demand. The New Priok expansion, tripling yearly capacity to 18 million TEU, underscores how port investments trigger adjacent industrial parks and cold-chain hubs. Major developers roll out multi-story fulfillment centers near Jakarta’s ring roads to minimize last-mile mileage. Occupiers favor buildings with 12-meter clear heights, 70 kN/sqm floor loading, and solar-ready roofs, a specification set that is becoming the new normal across the Indonesia Commercial Construction market.

In contrast, brick-and-mortar retail pivots toward lifestyle and entertainment offerings that keep dwell times high amid online shopping’s rise. Flagship schemes like PIK 2 blend retail with theme parks and waterfront promenades, buffering occupancy risk. Office demand shows nuanced recovery: anchor tenants consolidate older leases into green, tech-rich towers that meet WELL and LEED standards. Indonesia Data-center construction, exemplified by Telkom’s 51 MW Batam campus, enters the mainstream “others” bracket, leveraging Indonesia’s strategic bandwidth routes. Together, these shifts diversify revenue bases and attract institutional capital into the Indonesia Commercial Construction market.

By Construction Type: New builds dominate yet renovations gather pace

New construction controlled 72.85% of Indonesia Commercial Construction market share in 2025 as greenfield township, port, and airport schemes capture headline investments. The relocation of the national capital to Nusantara, tagged at USD 35 billion, epitomizes the preference for ground-up megaprojects. Developers enjoy design freedom, modern building codes, and scalable infrastructure grids in fresh sites, often integrating smart-city sensors from day one. Notably, government infrastructure targets of USD 34.9 billion for 2025-2029 reinforce this pipeline.

Renovation nonetheless expands at 8.73% CAGR through 2031, outpacing the new-build average as asset owners retrofit to ESG mandates. Jakarta’s class-B office towers add secondary glazing, VRV air-conditioning, and touchless lifts to lure tenants seeking healthier workspaces. Hospitality owners swap out outdated ballrooms for co-working lounges that lift revenue per available square meter. Higher technical complexity translates into richer margins for specialist contractors and building-services firms in the Indonesia Commercial Construction market.

By Investment Source: Private funding still largest, public outlays accelerate

Private investors accounted for 65.15% of Indonesia Commercial Construction market size in 2025, drawing on internal cash, syndicated bank debt, and REIT proceeds. Developers familiar with strata-title pre-sales funnel advance payments into construction progress, a model that supports liquidity yet carries execution risk. Public investment, although smaller, is projected to climb at 8.49% CAGR as the state channels grant funds and viability-gap subsidies through KPBU structures that crowd in private partners. Notable foreign pledges—USD 96 million from Russia’s Magnum, USD 51 million from China’s Delonix, and USD 9.6 million from Australia Independent School—illustrate early successes but also the ongoing challenge of scaling overseas interest to the USD 3.13 billion that Nusantara alone seeks.

Blended finance solutions such as green bonds and sharia-compliant project sukuk emerge as alternative taps, aligning with growing ESG investor appetites. State-owned banks offer discounted credit lines tied to resource-efficient designs, sharpening incentives for sustainable build choices across the Indonesia Commercial Construction market.

Geography Analysis

DKI Jakarta anchors Indonesia’s commercial real-estate cycle with a 39.55% share in 2025, underpinned by resilient occupier demand in finance, technology, and healthcare. The region’s USD 1.678 billion MRT Phase 2 line fosters new retail strips and high-rise clusters around Kota, Mangga Besar, and Ancol Barat stations, lifting land values by up to 15% over the past 12 months. Prime office landlords achieved the first rental uptick since 2015, while integrated projects such as Two Sudirman’s twin towers illustrate sustained foreign confidence. The government’s gradual shift to Nusantara eases concerns of an immediate tenant exodus, allowing Jakarta developers to pace new launches while ramping up renovations of older towers into net-zero assets.

East Java records the fastest 9.31% CAGR as logistics corridors multiply and manufacturing payrolls expand. The privately financed Dhoho Kediri Airport brings passenger and cargo throughput to previously land-locked hinterlands, enabling resort, warehouse, and agro-export facilities. Surabaya’s port upgrades tie into Pelindo’s national strategy, cutting dwell times and making the province a preferred e-commerce fulfillment base. Cement producers in Gresik benefit from proximity to limestone quarries and new power plants, anchoring construction material supply chains that feed growth across the Indonesia Commercial Construction market.

West Java leverages proximity to Greater Jakarta and enjoys fresh infrastructure such as the Ciawi-Sukabumi Toll Road. Industrial estates in Bekasi and Karawang capture spill-over demand from auto, electronics, and EV battery assembly, supported by a deepening skilled-labor pool. Tourist-centric provinces like Bali resume hotel and retail builds on top of the USD 20 billion urban subway plan that will reshape Denpasar’s mobility grid. Collectively, these geographic nodes diversify the demand base, reduce Jakarta dependence, and expand the overall canvas of the Indonesia Commercial Construction market.

Competitive Landscape

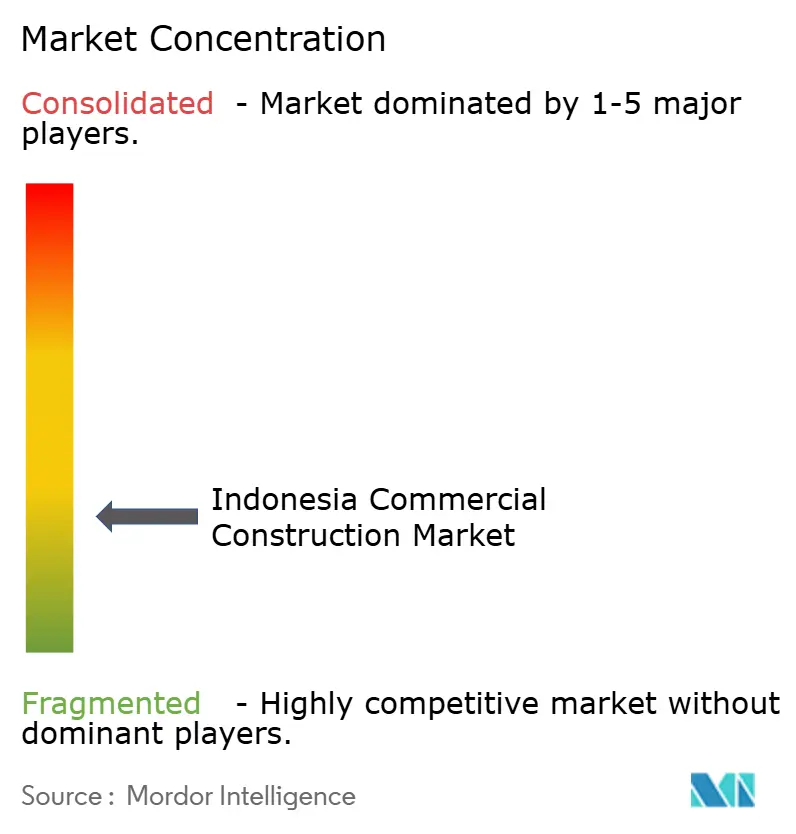

The Indonesia commercial construction market is moderately fragmented. State-owned giants such as PT Wijaya Karya, PT PP, and PT Adhi Karya leverage long-standing government ties to secure headline infrastructure jobs, yet they increasingly partner with Japanese EPC leaders that bring high-rise seismic technologies and timely execution. Wijaya Karya booked USD 804 million in revenue during Q3 2024 while slashing trade payables by 50%, showing a disciplined balance-sheet tightening that positions it for sizeable airport and port terminals. The firm’s USD 349 million contract for Hang Nadim Terminal 2 showcases its edge in aviation builds[3]PT Wijaya Karya, “Q3 2024 Financial and Operational Results,” WIKA Investor Relations, wika.co.id.

Foreign contractors expand footprints via joint ventures: Shimizu and Obayashi co-develop precast factories outside Jakarta, while Chinese groups target steel-intensive industrial parks. These alliances quicken construction cycles and introduce digital-twin monitoring. Local mid-caps such as Total Bangun Persada excel in fit-out and data-center builds, where high MEP complexity yields premium margins. Sustainability credentials have become a differentiator; players offering LEED and EDGE compliance win corporate mandates, adding a new skills race inside the Indonesia Commercial Construction market.

Financial maneuvering is equally strategic. To de-leverage, Wijaya Karya is divesting USD 449 million worth of toll-road stakes, freeing capital for high-margin design-build-finance packages. Developers tap REITs on the Singapore exchange to recycle stabilized mall assets, funneling proceeds into fresh landbanking. Meanwhile, new-format firms such as NeutraDC focus solely on hyperscale data parks, aligning with digital-sovereignty policy and carving niche competitive positions. The market’s evolution points toward growing specialization, alliance-driven scale, and ESG-led qualification hurdles that shape future rivalry.

Indonesia Commercial Construction Industry Leaders

PT PP(Persero) Tbk

PT Wijaya Karya Tbk

PT Total Bangun Persada Tbk

PT Nusa Raya Cipta Tbk

PT Adhi Karya Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: President Joko Widodo inaugurated PT Freeport Indonesia’s copper smelter in Gresik SEZ, the world’s largest single-line copper facility with 1.7 million tons annual capacity and potential state revenue of USD 5.13 billion.

- February 2025: PT Telkom Indonesia began construction of a 51 MW hyperscale data center in Batam through its NeutraDC arm, strengthening national digital-sovereignty goals.

- January 2025: PLN launched a USD 4.4 billion generation-and-grid expansion program designed to support Indonesia’s 8% economic-growth target.

- January 2025: President Prabowo earmarked IDR 48.8 trillion (USD 3.13 billion) through 2029 for Nusantara capital-city development, while Malaysia’s Citadel Group committed an additional IDR 6.5 trillion for housing and office blocks.

Indonesia Commercial Construction Market Report Scope

A complete background analysis of the Indonesia Commercial Construction market, which includes an assessment of the economy, market overview, market size estimation for key segments, and emerging trends in the market, market dynamics, and key company profiles are covered in the report.

Indonesia Commercial Construction Market is segmented by type (offices, retail, hospitality, institutional, and others). The report offers market size and forecast for Indonesia Commercial Construction Market in value (USD) for all the above segments.

By Commercial Sector Type

| Office |

| Retail |

| Industrial and Logistics |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Investment Source

| Public |

| Private |

By Region

| DKI Jakarta |

| West Java (Jawa Barat) |

| East Java (Jawa Timur) |

| Rest of Indonesia |

| By Commercial Sector Type | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| By Construction Type | New Construction |

| Renovation | |

| By Investment Source | Public |

| Private | |

| By Region | DKI Jakarta |

| West Java (Jawa Barat) | |

| East Java (Jawa Timur) | |

| Rest of Indonesia |

Key Questions Answered in the Report

What is the current size of the Indonesia Commercial Construction market?

The market was valued at USD 55.18 billion in 2025, is estimated at USD 59.64 billion in 2026, and is forecast to hit USD 87.85 billion by 2031.

Which segment is growing the fastest within Indonesia’s commercial construction?

Industrial & logistics is expanding at a 8.93% CAGR, outpacing all other sector types thanks to e-commerce and supply-chain investments.

How large is Jakarta’s share in the national commercial construction landscape?

DKI Jakarta accounted for 39.55% of Indonesia Commercial Construction market share in 2025, reflecting its role as the nation’s commercial hub.

What role does the KPBU scheme play in project financing?

KPBU structures let the government share risk with private investors, boosting public infrastructure spending while attracting foreign capital into commercial projects.

Why are mixed-use developments gaining popularity in Indonesia?

They optimize scarce urban land, blend multiple revenue streams, and align with transit-oriented planning that local governments actively promote.

Which risk factors could slow market growth over the next two years?

High material costs, permit delays, and excess space in some office and retail submarkets pose near-term headwinds, though policy reforms aim to ease these pressures.

Page last updated on: