Brazil Scaffolding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

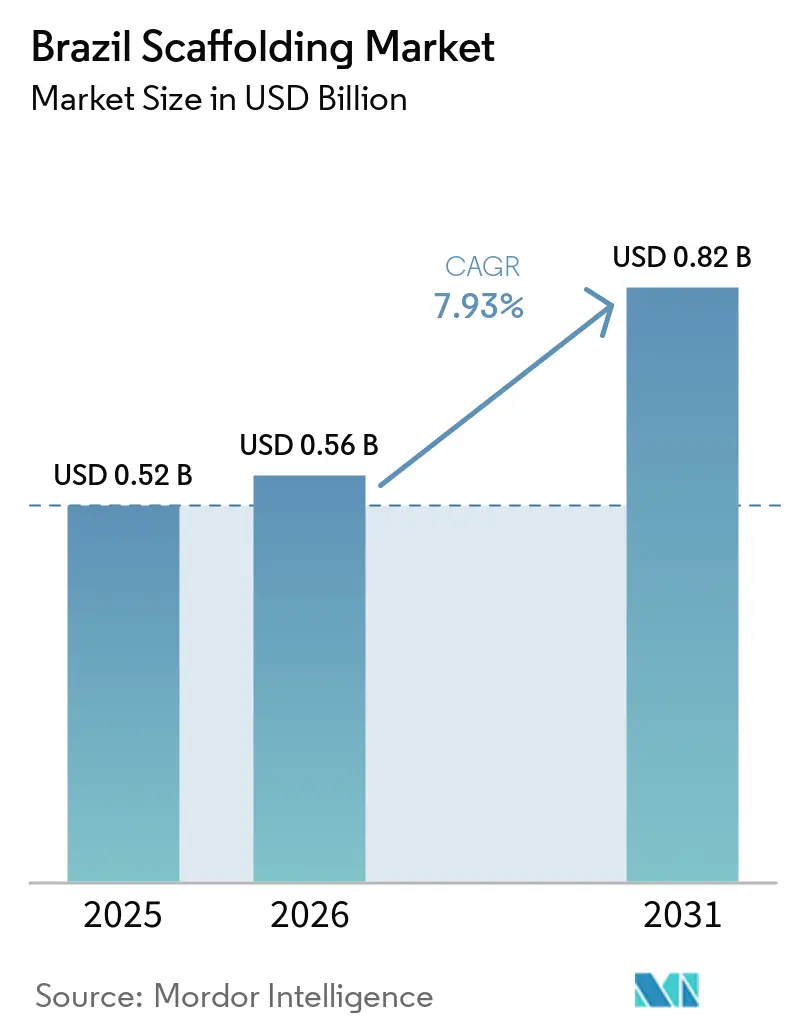

| Base Year Market Size (2025) | USD 0.52 Billion |

| Market Size (2026) | USD 0.56 Billion |

| Market Size (2031) | USD 0.82 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Scaffolding Market Analysis by Mordor Intelligence

The Brazil Scaffolding Market size was valued at USD 0.52 billion in 2025 and is estimated to grow from USD 0.56 billion in 2026 to reach USD 0.82 billion by 2031, at a CAGR of 7.93% during the forecast period (2026-2031).

The Brazil scaffolding market is supported by steady activity in public works, refinery maintenance, building renovation, and housing construction, which keeps demand for access equipment active across both new-build and maintenance work. Demand is also shifting toward higher-specification systems because large project owners now place greater weight on compliance, documentation, and engineered access layouts than in prior procurement cycles. Contractors are also leaning more heavily on flexible fleet access and faster installation methods as labor pressure and schedule discipline tighten across construction and industrial shutdown work. The market also has room for suppliers that can pair equipment with engineering support, inspection records, and site logistics, because these services increasingly shape vendor selection on larger jobs. Industrial maintenance activity also continues to support recurring scaffold demand across refining and other process assets, providing the market with a broader base than a construction-only cycle.

Key Report Takeaways

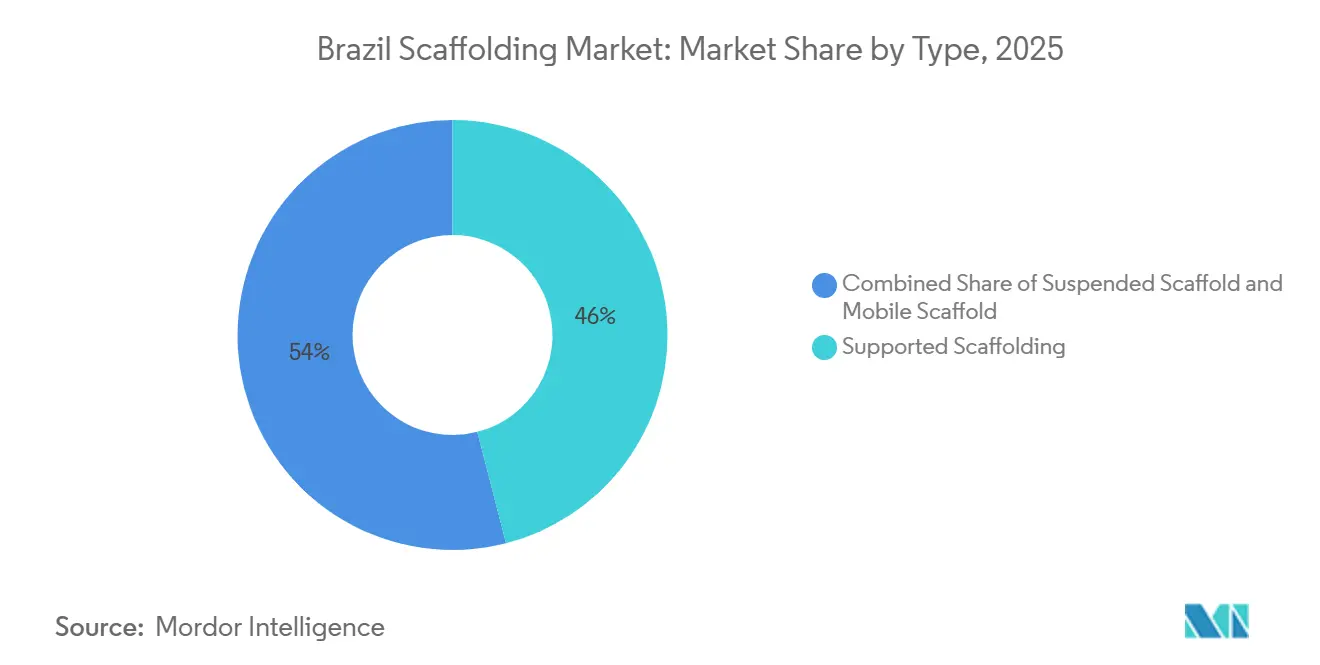

- By type, supported scaffolding led with a 46% revenue share in 2025, while suspended scaffolding is forecast to expand at an 8.80% CAGR through 2031.

- By system, the frame / H-frame held the largest share at 34% in 2025, while modular / ringlock recorded the highest projected CAGR at 8.60% through 2031.

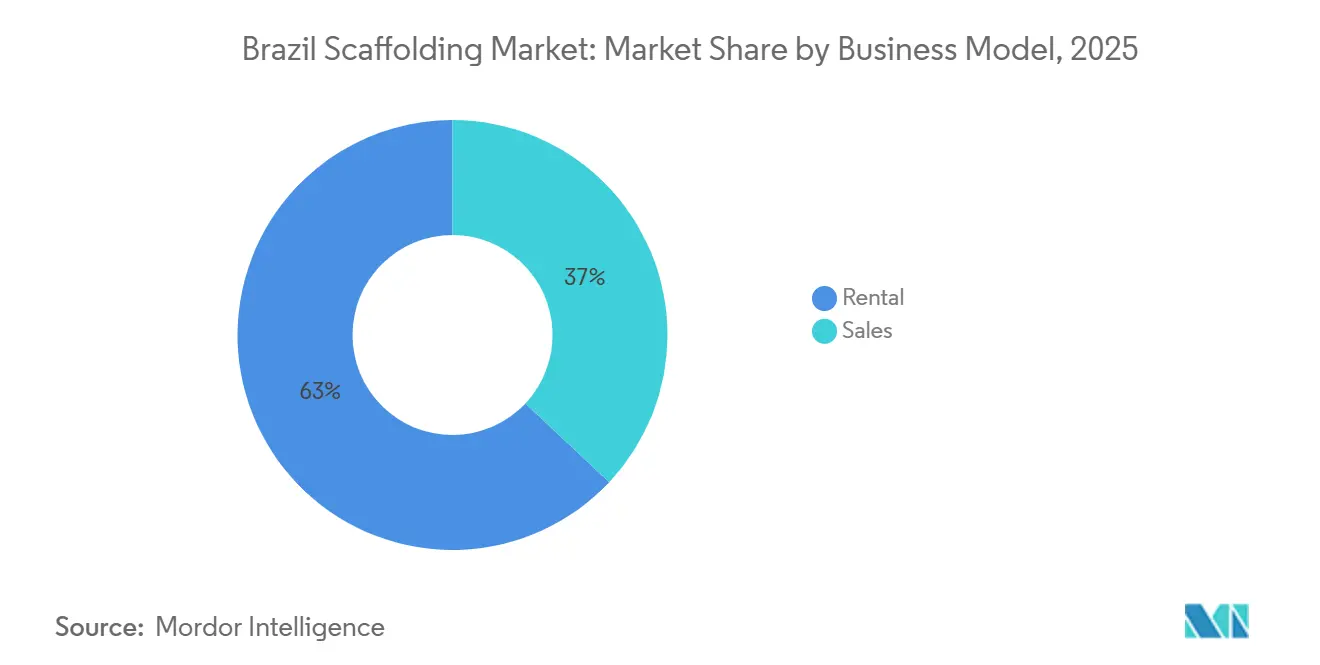

- By business model, rental held 63% of the Brazil scaffolding market share in 2025, and rental also recorded the highest projected CAGR at 8.90% through 2031.

- By material type, steel accounted for 57% of the Brazil scaffolding market size in 2025, while aluminum is advancing at a 9.10% CAGR through 2031.

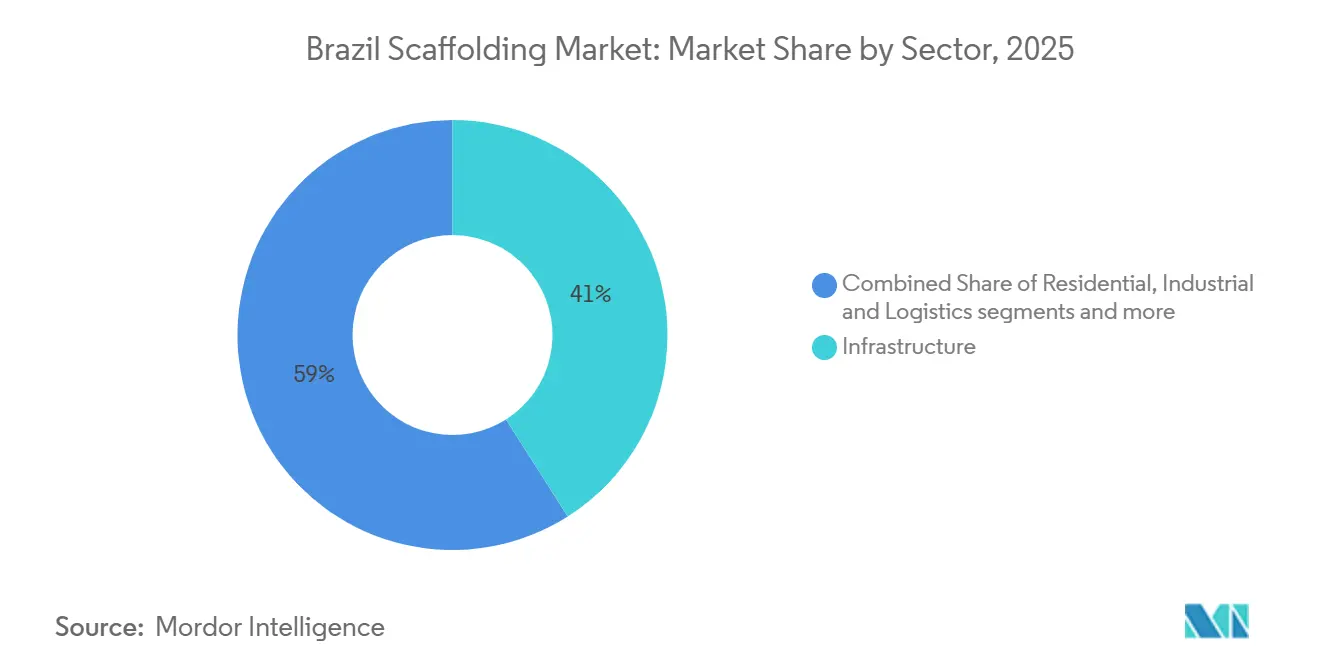

- By sector, infrastructure captured 41% of the Brazil scaffolding market revenue in 2025, and infrastructure is also forecast to post the highest CAGR at 9.20% through 2031.

- By geography, Southeast Brazil led with 39% of the Brazil scaffolding market revenue in 2025, while North Brazil is projected to grow the fastest at a 9.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Scaffolding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Infrastructure Renewal and Vertical Construction Growth Drive Scaffolding Demand | +2.2% | Southeast Brazil, Northeast Brazil | Medium term (2-4 years) |

| Oil and Gas Maintenance and Refinery Turnarounds Increase Scaffolding Utilization | +1.4% | Southeast Brazil, Northeast Brazil | Short term (≤ 2 years) |

| Industrial Plant Maintenance and Shutdown Cycles Support Market Growth | +1.2% | Southeast Brazil, South Brazil | Short term (≤ 2 years) |

| Rental Preference Among Contractors and SMEs Expands Scaffolding Adoption | +1.1% | National, concentrated in Southeast and Northeast Brazil | Medium term (2-4 years) |

| Shift Toward Modular and Safer Access Systems Enhances Market Penetration | +0.8% | National, with early adoption in São Paulo and Rio de Janeiro | Medium term (2-4 years) |

| Demand for Faster Assembly Solutions Improves Labor Efficiency on Job Sites | +0.5% | National, with early gains in Southeast and South Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Infrastructure Renewal and Vertical Construction Growth Drive Scaffolding Demand

Urban works and vertical construction continue to create a broad base of demand for the Brazil scaffolding market because both activities require repeated access at early, mid, and finishing stages. This matters because scaffold demand does not end after structural works; it continues through facade installation, painting, cladding, repairs, and later maintenance cycles. The Brazil scaffolding market also benefits when these projects overlap, since contractors then need more equipment on short notice and often value a reliable supply over the lowest purchase price. High-rise work in dense cities also increases the appeal of engineered systems that can work within tighter footprints and stricter safety rules. Public works and urban renewal, therefore, support steady equipment turnover, while vertical construction adds recurring use windows that extend well beyond the first mobilization.

Oil and Gas Maintenance and Refinery Turnarounds Increase Scaffolding Utilization

Oil and gas maintenance remains an important driver of the Brazil scaffolding market, as refinery and processing assets require safe temporary access for inspection, repair, and shutdown work. The recent maintenance intensity across major assets points to continued reliability work across the system and supports recurring demand for access solutions[1]Agência Brasil, “Petrobras Refineries Run Above 100% Capacity,” Agência Brasil, agenciabrasil.ebc.com.br. Large industrial owners also continue to plan multi-year maintenance programs, which improve visibility for scaffold suppliers serving heavy industrial clients[2]Petróleo Brasileiro S.A., “Petrobras Aprova Plano De Negócios 2026-2030,” Agência Petrobras, petrobras.com.br. For scaffold providers, this means demand is tied not only to large turnaround events but also to ongoing condition monitoring and planned interventions between major shutdowns. That pattern supports stronger utilization for companies that can provide engineered layouts, dependable mobilization, and compliance records for industrial clients.

Industrial Plant Maintenance and Shutdown Cycles Support Market Growth

Planned maintenance across chemicals, pulp and paper, food processing, energy, and other process industries provides the Brazil scaffolding market with a recurring demand layer that is less dependent on new project awards. These sites operate on maintenance calendars that require temporary access even when new construction activity slows, which helps stabilize scaffold demand over time. Cost discipline is also shaping behavior, because the National Construction Cost Index rose 5.92% in 2025, and labor costs increased 8.98% in the same period[3]Câmara Brasileira da Indústria da Construção, “Desempenho Da Construção Civil Em 2025 E Perspectivas Para 2026,” CBIC, cbic.org.br. As budgets tighten, plant owners place greater value on systems that reduce downtime, limit assembly hours, and shorten the total maintenance window. This favors suppliers that can plan access more precisely, move quickly between work fronts, and document compliance in a way that fits industrial audit expectations.

Rental Preference Among Contractors and SMEs Expands Scaffolding Adoption

The Brazil scaffolding market continues to see a clear preference for rental, as many contractors prefer flexibility over fixed ownership costs. That preference is especially visible when project pipelines are active but uneven, because rental helps firms match fleet use to project timing without locking up capital in large idle inventories. It also suits smaller contractors that need compliant equipment and supporting documentation but do not have the scale to maintain large in-house fleets. The Brazil scaffolding market benefits from this shift because rental providers often bundle engineering review, inspection support, and maintenance into their commercial offers, thereby enhancing service quality. Over time, that business model strengthens larger, organized operators and makes the market more service-led than product-led.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages Constrain Safe Erection and Dismantling Activities | -1.3% | National, most acute outside major labor hubs | Short term (≤ 2 years) to Medium term (2-4 years) |

| High Equipment Costs and Financing Constraints Limit Market Expansion | -1.0% | National, more severe for SME operators outside Southeast Brazil | Medium term (2-4 years) |

| Informal and Price-Sensitive Competition Intensifies Market Fragmentation | -0.7% | National, intensified in North and Northeast Brazil | Long term (≥ 4 years) |

| Logistics, Storage, and Site Handling Complexity Increases Operating Costs | -0.5% | National, most acute in North Brazil and remote sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages Constrain Safe Erection and Dismantling Activities

Labor availability remains a real limit on the Brazil scaffolding market because scaffold erection and dismantling require trained crews capable of working safely at height. This is not an area where contractors can easily replace missing workers with general labor, since the work depends on process discipline, safety training, and reliable supervision. Cost pressure is also rising, making inefficient crew use even harder for contractors and rental providers to absorb. When skilled labor is scarce, project managers tend to favor systems that reduce person-hours and simplify assembly steps. That shifts demand toward solutions that are faster to install, easier to inspect, and less dependent on large crews.

High Equipment Costs and Financing Constraints Limit Market Expansion

High equipment costs remain a restraint for the Brazil scaffolding market, as fleet growth requires sustained capital commitment in a business that is highly sensitive to utilization. This is more difficult for smaller firms, especially outside the main industrial and construction hubs, where demand can be less predictable and access to financing is weaker. The result is a two-speed market in which larger organized operators can add capacity and improve service coverage more easily than regional firms. That gap affects both ownership models and rental expansion, because inventory depth, transport capability, and maintenance readiness all depend on capital. Over time, financing pressure can slow capacity additions even when project demand is supportive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Supported Scaffolds Dominate, While Suspended Scaffolds Record the Fastest Growth

Supported scaffolding held a 46% share in 2025, maintaining its leading position because it suits a wide range of job types and remains familiar to contractors across building and civil works. Its broad use on residential, commercial, and infrastructure sites makes it the default option where ground support is practical, and the access layout does not require complex suspension. That wide applicability also supports repeat use across different project phases, from structural activity to finishing work and later repairs. In the Brazil scaffolding market, supported systems still benefit from straightforward installation logic and an established contractor comfort level that reduces training friction on common job sites. This combination of cost discipline, basic versatility, and broad user familiarity helps preserve the segment’s scale even as demand becomes more specialized.

Suspended scaffolding is forecast to grow at an 8.80% CAGR through 2031, reflecting the stronger pull from facade work, high-rise construction, and renovation in dense urban settings. Its growth is tied to job sites where supported systems are harder to deploy because street space is limited or building height makes ground-based access less efficient. The segment also benefits from ongoing maintenance of existing towers, since facade cleaning, repainting, and envelope repairs create repeated access demand after project completion. In that sense, suspended systems gain from both new construction and the aging of commercial and residential building stock. The Brazil scaffolding industry is therefore seeing a gradual shift in mix, with standard supported systems maintaining volume while suspended systems capture faster growth in more space-constrained urban environments.

By System: Frame Systems Dominate, While Modular / Ringlock Gains From Productivity and Control

Frame or H-frame systems accounted for a 34% share in 2025 and retained leadership because they are simple, familiar, and cost-effective for a large part of the installed base. Mid-tier contractors continue to use these systems widely on repetitive building work where procurement teams prioritize straightforward setup and dependable availability. Their strong position also reflects the practical reality that many users do not need the full design flexibility of more advanced modular systems for low- to medium-complexity jobs. In the Brazil scaffolding market, this keeps the frame or H-frame relevant across common residential and commercial tasks where repeatable geometry and lower upfront cost still carry weight. The system, therefore, remains the volume leader even as buyer expectations continue to evolve.

Modular / ringlock systems are forecast to grow at a 8.60% CAGR through 2031 because they offer higher productivity, greater adaptability, and a more engineered feel for complex jobs. These systems are better suited to clients who want faster assembly, better control over layout quality, and clearer alignment with compliance and documentation practices. That matters more as labor costs remain elevated and contractors seek ways to boost crew productivity on active sites. Modular systems also align with suppliers' commercial strategy to move away from commodity pricing and toward higher-value service packages. The Brazil scaffolding market is therefore balancing two realities, with the frame or H-frame preserving scale in mainstream work. At the same time, ringlock gains ground where speed, geometry control, and auditability matter more.

By Business Model: Rental Accounts for the Largest Share and Continues to Expand

Rental captured 63% of market revenue in 2025, underscoring contractors' strong preference for flexibility over fixed ownership in a market characterized by uneven project timing and tight capital discipline. Rental reduces the burden of carrying large inventories and lets contractors bring in equipment only when project schedules actually require it. It also gives users easier access to maintenance support, replacement components, and inspection readiness, which is valuable on sites where downtime carries a high penalty. In the Brazil scaffolding market, this structure supports faster commercial decisions because the buyer is often paying for availability and compliance support rather than only for metal inventory. That is one reason rental remains the clearest business model anchor across the current cycle.

Rental is also the fastest-growing business model, with an 8.90% CAGR projected through 2031, indicating the penetration cycle is still incomplete. This is unusual because large segments in equipment markets often slow once they become dominant, yet rental in this case continues to extend its advantage. The reason is that organized rental providers can bundle transport, engineered layouts, maintenance, and documentation into a single offer, thereby raising switching costs for customers once these services are embedded in procurement routines. The model also scales well in complex jobs where clients need responsiveness more than ownership. The Brazil scaffolding industry is therefore moving further toward service-led competition, with rental providers strengthening their edge through fleet depth, regional coverage, and stronger site support rather than solely through equipment availability.

By Material Type: Steel Maintains Leadership as Aluminum Gains Momentum

Steel accounted for 57% of revenue in 2025, making it the clear material leader because it remains widely available, structurally trusted, and suitable for a broad range of load requirements. Its position is also supported by long-standing contractor familiarity and by users' installed habits that have built site routines around steel-based configurations. That gives steel a durable role in the Brazil scaffolding market, especially in standard applications where durability and known performance matter more than weight savings. Timber, plywood, and specialty non-conductive materials remain present only in narrower use cases, so they do not change the broader material hierarchy. Steel, therefore, continues to anchor volume, especially where buyers focus on conventional performance and broad compatibility.

Aluminum is forecast to grow at a 9.10% CAGR through 2031, as its lower weight reduces assembly effort and enables faster on-site handling. This matters more in a labor-constrained environment because lighter systems can improve crew productivity, reduce fatigue, and shorten the time required to move between work fronts. Aluminum also holds appeal at coastal and high-humidity industrial sites where corrosion exposure increases the long-term cost of steel ownership. The higher initial acquisition cost still matters, but the broader cost picture is shifting in aluminum’s favor in selected applications. The Brazil scaffolding market is therefore not replacing steel at the core. Still, it is steadily widening aluminum use in jobs where portability, corrosion resistance, and labor efficiency change the total value equation.

By Sector: Infrastructure Accounts for the Largest Share and Fastest Growth

Infrastructure accounted for 41% of market revenue in 2025, making it the largest end-use sector, as large civil works and public assets require access equipment across multiple construction and maintenance stages. This segment benefits from the fact that scaffold demand in infrastructure is not limited to a single work package, since bridges, stations, utilities, and other assets need access at different points over long project timelines. It also tends to favor organized suppliers that can mobilize larger fleets, support engineering review, and manage documentation across multiple sites. In the Brazilian scaffolding market, infrastructure projects are especially important for companies seeking durable revenue visibility and stronger fleet utilization. The scale of the segment, therefore, reflects both the size of project pipelines and the repeated access needs built into public and utility works.

Infrastructure is also projected to grow at a 9.20% CAGR through 2031, making it the leading sector in both size and expansion. That pattern shows that public works, utility upgrades, and large civil contracts are still generating enough momentum to outpace the rest of the market. Residential activity continues to provide an important floor because housing work creates steady, recurring demand, but it does not carry the same combination of project scale and technical intensity. Commercial, industrial, and logistics work remains relevant because it supports higher-value jobs and maintenance activities, yet its pace tends to follow the timing of private investment. The Brazil scaffolding market, therefore, relies on infrastructure as its main growth engine. At the same time, other sectors provide balance and help keep fleet demand from becoming overly dependent on a single project class.

Geography Analysis

Southeast Brazil accounted for 39% of market revenue in 2025, maintaining its lead, as the region combines the country’s deepest base of vertical construction, industrial assets, and civil engineering work. The region also benefits from stronger logistics, a broader supplier base, and a concentration of organized contractors capable of handling larger, more technical projects. That makes the Brazil scaffolding market’s Southeast cluster the core operating zone, especially where clients require engineering support, documentation, and rapid fleet movement between sites. Refining and industrial maintenance activities also continue to strengthen the region’s role, as they add recurring scaffold demand beyond the normal building cycle. Large logistics hubs and stronger service infrastructure further support organized operators that want national scale with dependable execution.

South Brazil remains a solid secondary market because it has a stable industrial base and recurring maintenance demand from manufacturing and process facilities. Northeast Brazil is important for expansion because urban works and infrastructure deficits continue to create room for additional scaffold demand as project execution broadens beyond the traditional core states. Central-West Brazil adds activity through administrative construction, warehousing, and agro-industrial facilities, although it still depends heavily on execution capacity and supplier reach. Across these regions, the Brazil scaffolding market is shaped by a practical divide between areas with deep, organized supply and those with demand but thinner formal fleet coverage.

North Brazil is projected to grow at a 9% CAGR through 2031, making it the fastest-growing regional segment in the country. The growth outlook is tied to energy and resource-linked projects rather than to the same urban density drivers seen in the Southeast. This gives the region a different demand profile, with more dependence on infrastructure and utility work than on large-scale high-rise construction. At the same time, transport distance, site complexity, and limited skilled labor slow the pace at which awarded projects turn into executed scaffold contracts. This means the Brazil scaffolding market in the North has a stronger growth profile. Still, it also requires suppliers that can manage distance, transport, storage, and labor limitations more carefully than in the country’s core markets.

Competitive Landscape

The Brazil scaffolding market remains fragmented, with global specialists such as Layher, PERI, Altrad Group, and BrandSafway competing alongside a wide base of regional suppliers and local operators. Large players tend to focus on industrial and complex civil contracts where engineering support, compliance records, and service reliability carry more weight than the lowest unit price. Smaller operators remain relevant in residential and low-complexity work, where proximity and pricing can still decide contract awards. This split keeps the Brazil scaffolding market open to many participants, but it also creates clear differences between volume-driven local competition and higher-value organized competition. The result is a market structure in which formal operators try to move customers toward service quality. At the same time, informal and price-led firms keep pressure on margins in simpler work categories.

PERI illustrates one organized strategy, because its large logistics footprint in São Paulo supports fleet management, service readiness, and national execution capability. That kind of infrastructure matters because larger project clients increasingly expect reliable delivery, equipment traceability, and stronger technical support from vendors. Altrad has followed another route by expanding through acquisitions, including Beerenberg in November 2024 and Stork’s United Kingdom business in February 2025, which reinforces its broader industrial services platform. In January 2026, Altrad also confirmed plans to accelerate merger and acquisition activity in 2026 and 2027, which signals that global industrial services groups still see scale and service breadth as strategic advantages. These moves show that larger companies are using capability expansion, service integration, and geographic reach to improve their position in more technical contracts.

Competitive advantage is therefore shifting away from simple equipment supply and toward the ability to combine access systems with engineering, documentation, and dependable execution. That shift benefits companies that can support turnaround work, infrastructure schedules, and repeat industrial maintenance without exposing clients to compliance gaps. It also creates space for material and product differentiation, as companies such as ROHR position lightweight aluminum systems for users who value faster handling and lower labor intensity. The Brazil scaffolding market is likely to remain fragmented overall. Still, organized leaders should continue to gain ground on higher-value contracts where service depth and audit readiness matter more than price alone. This should widen the gap between local transactional competition and more structured competition centered on project support and compliance-led selling.

Brazil Scaffolding Industry Leaders

Layher

PERI

ULMA Construction

Altrad

BrandSafway

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Loxam SAS acquired a 50.3% controlling stake in Mills Locação, Serviços e Logística S.A. for USD 0.3 billion, with the total transaction value reaching USD 0.7 billion after the mandatory tender offer for the remaining shareholders. Mills, which began with scaffolding and shoring activities and later expanded into equipment rental, is Brazil’s largest rental company. It operates a fleet of nearly 16,000 units across steel and aluminum tubular structures, shoring, access equipment for civil construction, and reusable concrete forms. The deal gives Loxam a stronger position in Brazil and brings European rental and access expertise more directly into the country’s scaffolding space.

- May 2026: Petrobras signed contracts with SBM Offshore for 2 Floating Production Storage and Offloading units under the Sergipe Deepwater project using a Build, Operate, and Transfer model. The combined contract value stood at USD 7.8 billion, with SEAP II valued at USD 3.8 billion and SEAP I at USD 4 billion. The scale of these offshore units is expected to support steady scaffolding demand during structural assembly, topside installation, piping work, and later maintenance activity. This adds another long-duration project pipeline for scaffold deployment in Brazil’s oil and gas segment.

- April 2026: Delta Plus Group completed the acquisition of Athena's Consultoria e Informatica S/A, a Brazilian company focused on fall protection equipment, on April 16, 2026. Athenas generated annual revenue of USD 7.8 million and employs more than 100 people, with over 80 working in production. The acquisition strengthens Delta Plus’s presence in Brazil’s height-safety equipment market. It also reinforces the safety product requirements for scaffold assembly, use, and dismantling, including harnesses, lanyards, and fall-arrest systems, as required under NR-18 and NR-35.

Brazil Scaffolding Market Report Scope

The Brazil Scaffolding Market is Segmented by Type (Supported, Suspended, and Mobile Scaffold), System (Tube & Coupler, and More), Business Model (Sales, and Rental), Material Type (Timber / Plywood, Steel, Aluminum, and More), Sector (Residential, Commercial, Industrial & Logistics and More), and Geography (Southeast, South, Northeast, North, Central-West Brazil). The Market Forecasts are Provided in Terms of Value (USD).

| Supported Scaffold |

| Suspended Scaffold |

| Mobile Scaffold |

| Tube & Coupler |

| Cuplock |

| Modular / Ringlock |

| Frame / H-Frame |

| Sales |

| Rental |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| Southeast Brazil |

| South Brazil |

| Northeast Brazil |

| North Brazil |

| Central-West Brazil |

| By Type | Supported Scaffold |

| Suspended Scaffold | |

| Mobile Scaffold | |

| By System | Tube & Coupler |

| Cuplock | |

| Modular / Ringlock | |

| Frame / H-Frame | |

| By Business Model | Sales |

| Rental | |

| By Material Type | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By Geography | Southeast Brazil |

| South Brazil | |

| Northeast Brazil | |

| North Brazil | |

| Central-West Brazil |

Key Questions Answered in the Report

What is the current size of Brazil’s scaffolding business?

The Brazil scaffolding market stood at USD 0.52 billion in 2025, reached USD 0.56 billion in 2026, and is forecast to hit USD 0.82 billion by 2031, growing at a 7.93% CAGR over 2026 to 2031.

Which product type leads revenue in Brazil?

Supported scaffolding led the market in 2025 with a 46% share because it remains the most widely used format across residential, commercial, and civil projects.

Which scaffold system is growing the fastest in Brazil?

Modular / ringlock is the fastest-growing system, with an 8.6% CAGR through 2031, driven by stronger demand for productivity, layout control, and better compliance support.

Why is rental so important for scaffold suppliers in Brazil?

Rental accounted for 63% of revenue in 2025 and is also the fastest-growing business model, with an 8.9% CAGR, because contractors want flexibility, a lower ownership burden, and easier access to service support.

Which material has the strongest growth outlook?

Steel remained the leading material with a 57% share in 2025, but aluminum is forecast to grow at 9.1% CAGR through 2031 because it is lighter and can reduce handling and assembly effort.

Which region offers the strongest future expansion?

Southeast Brazil remained the largest region, with a 39% share in 2025, while North Brazil is projected to expand the fastest at a 9% CAGR through 2031, driven by energy and infrastructure activity.

Page last updated on: