Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 101.22 Billion |

| Market Size (2026) | USD 106.89 Billion |

| Market Size (2031) | USD 140.4 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Infrastructure Market Analysis by Mordor Intelligence

The Indonesia infrastructure market size is expected to grow from USD 101.22 billion in 2025 to USD 106.89 billion in 2026 and is forecast to reach USD 140.4 billion by 2031 at 5.6% CAGR over 2026-2031. Robust population growth, rapid urbanization, and the National Medium-Term Development Plan (RPJMN 2025-2029) combine to keep project pipelines full, even as the state trims discretionary budgets to protect fiscal targets. Fresh equity from the Indonesia Investment Authority (INA), worth USD 10.3 billion in managed assets, signals deeper private participation, while new green-bond channels make renewable and climate-resilient projects bankable. Transportation remains the single-largest contributor to civil-works value because toll-road build-outs directly cut logistics costs that are still above regional peers. Digital-economy ambitions add an emerging layer: hyperscale data-center construction and fiber-optic corridors now account for a growing share of EPC contracts, creating a diversified demand profile[1]Kementerian Pekerjaan Umum dan Perumahan Rakyat, “Rencana Kerja 2025,” pupr.go.id.

Key Report Takeaways

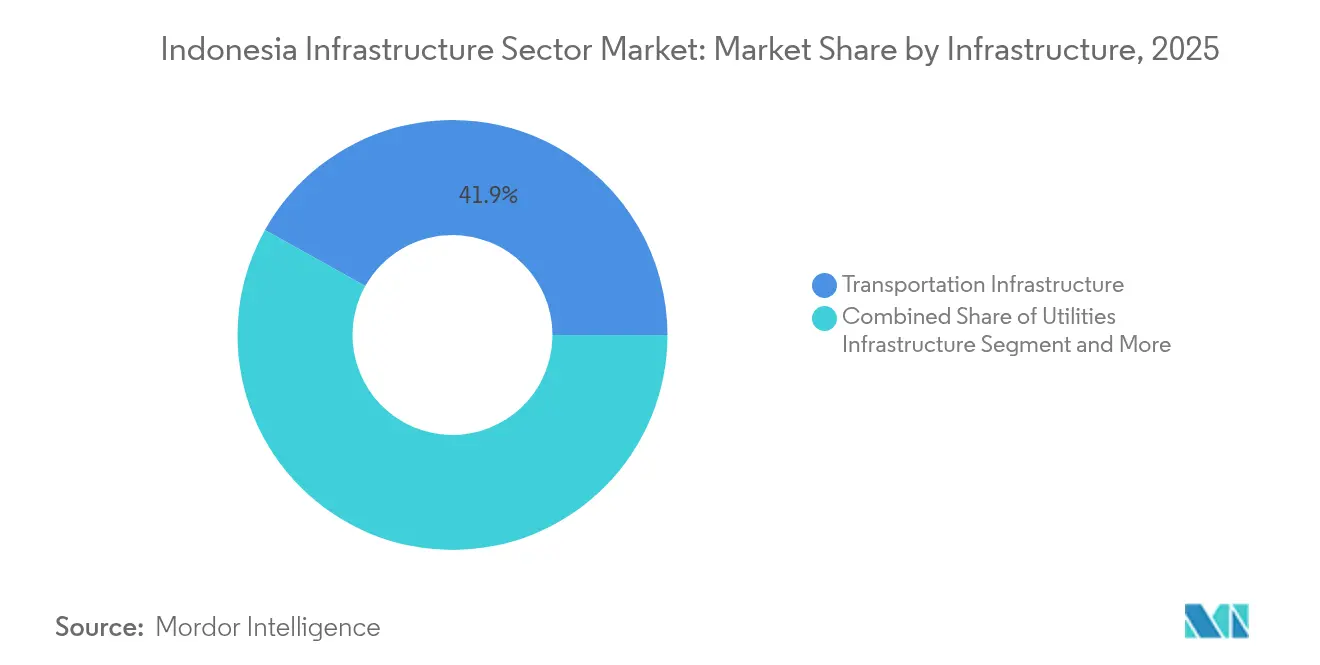

- By infrastructure type, transportation led with 41.87% Indonesia infrastructure market share in 2025, transportation is projected to post the fastest 6.88% CAGR through 2031.

- By construction type, new builds held 77.35% share of the Indonesia infrastructure market size in 2025, renovation is advancing at a 6.62% CAGR to 2031.

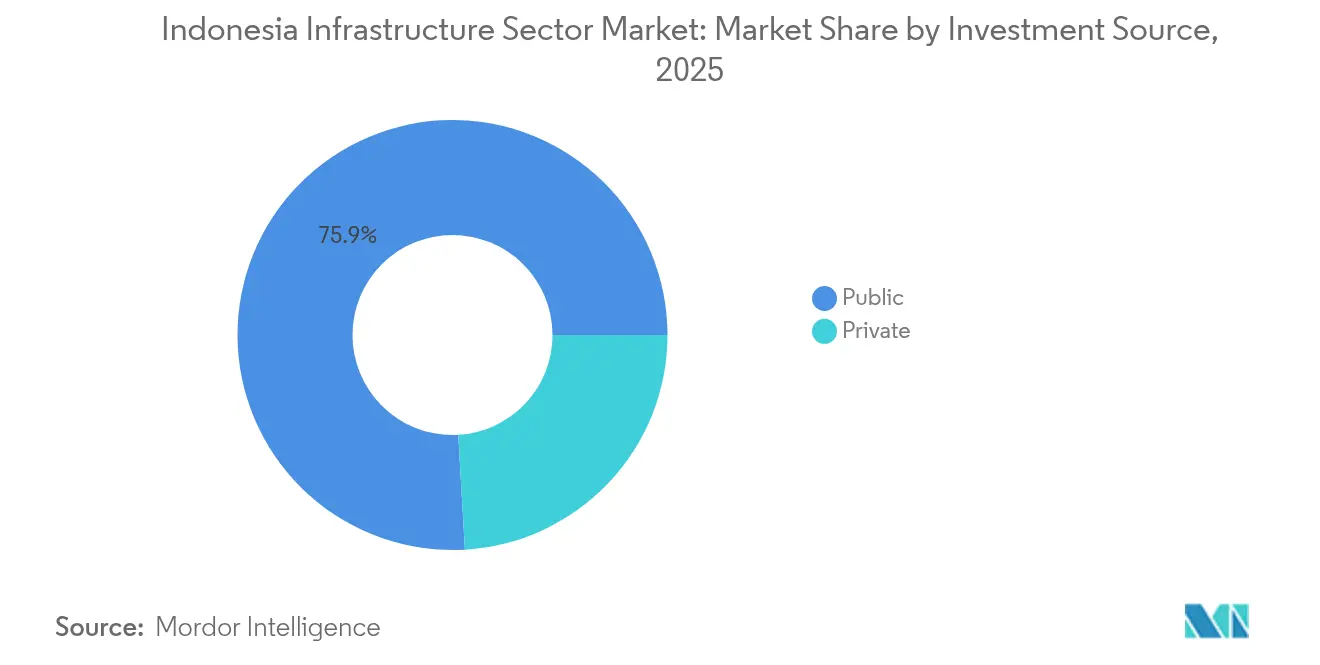

- By investment source, the public sector commanded 75.92% of spending in 2025, while private capital is set to expand at 7.45% CAGR through 2031.

- By geography, Java held 57.96% share of the Indonesia infrastructure market size in 2025, Kalimantan is advancing at a 6.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Medium-Term Development Plan (RPJMN 2025-2029) | +1.2% | National; most funds flow to Java, Kalimantan | Long term (≥ 4 years) |

| Relocation of the new capital (Nusantara) | +1.1% | Kalimantan focus with regional spill-overs | Long term (≥ 4 years) |

| Sovereign wealth fund (INA) catalyzing PPP pipelines | +0.9% | Nationwide; early allocations in Java & Sumatra | Medium term (2-4 years) |

| Growing urbanization and middle-class expansion | +0.8% | Java core; spill-over to Sumatra, Sulawesi | Medium term (2-4 years) |

| Surge in data-center and fiber backbone build-outs | +0.6% | Java and Batam hubs; tier-two cities next | Short term (≤ 2 years) |

| Green-bond financed renewable and climate-resilient assets | +0.4% | Geothermal-rich regions; coastal zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Medium-Term Development Plan (RPJMN 2025-2029)

The RPJMN commits USD 25.8 billion in 2025 for roads, mass transit, and energy transition assets, making infrastructure the policy centerpiece for escaping the middle-income trap. A pipeline of 210 strategic projects already enjoys presidential regulation backing, which reduces approval risk and standardizes PPP templates across ministries. Execution credibility is high because 153 legacy projects worth USD 67.1 billion reached completion between 2016-2023, demonstrating a functioning delivery apparatus. The plan explicitly targets logistics-cost reduction below 10% of GDP, a metric closely watched by manufacturing investors. By embedding climate resilience and digital connectivity targets, RPJMN provides visibility that encourages multidecade private capital commitments.

Relocation of the New Capital (Nusantara)

The USD 29 billion first-phase build of Nusantara turns Kalimantan into the largest construction site in Southeast Asia, sparking ancillary demand in ports, airports, and water systems. More than 61.7% of state-funded packages were physically complete by December 2024, a key confidence signal for institutional investors eyeing later-stage parcels. Design parameters call for carbon neutrality by 2045 and fully digital public services, positioning the city as a demonstration hub for smart, sustainable infrastructure. Foreign pledges reached USD 97 million by late 2024, with Russian, Chinese, and Australian participants, and are expected to accelerate once core civil works de-risk remaining phases. Spill-over effects already include road upgrades linking mineral-rich South Sulawesi to new logistics channels, underscoring the project’s national multiplier.

Sovereign Wealth Fund (INA) Catalyzing PPP Pipelines

INA grew from a USD 5 billion seed vehicle in 2021 to USD 10.3 billion in assets by 2024, proving institutional depths that global investors require before committing to greenfield risk. Its USD 2.7 billion toll-road platform attracted capital from APG and Abu Dhabi Investment Authority, mitigating currency and regulatory risks for pension funds that had previously stayed away. INA’s co-investment model now extends to a USD 1.2 billion technology-infrastructure program with Granite Asia that targets edge data centers and smart-city utilities. By standardizing due-diligence templates and offering minority equity structures, INA shortens deal timelines and lowers financing costs. The result is a robust PPP deal flow that plugs fiscal gaps without diluting sovereign oversight.

Growing Urbanization and Middle-Class Expansion

Urbanization hit 57.3% in 2024 and metropolitan areas generated 60% of national GDP, stretching transport, water, and social infrastructure beyond design capacity. Middle-income households, projected to total 141 million by 2030, demand higher-quality amenities such as mass rapid transit and smart-grid electrification. Greater Jakarta’s 34 million residents already drive daily mobility requirements that underpinned the launch of LRT Jabodebek and expansion of MRT Jakarta Phase 2. Passenger-car ownership growth sustains toll-road traffic, evidenced by the network’s expansion to 2,816 km after adding 217.8 km in 2023. Rising urban tax receipts give local governments more headroom for blended-finance projects, completing a feedback loop that channels consumer prosperity into long-term infrastructure demand[2]World Bank, “Indonesia Urbanization Review,” worldbank.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fiscal-deficit-driven cap-ex ceilings | -0.7% | Nationwide, hardest on secondary projects | Short term (≤ 2 years) |

| Protracted land-acquisition and permitting cycles | -0.5% | Mainly Java; emerging in peri-urban corridors | Medium term (2-4 years) |

| Climate-change-related cost escalations (flooding, sea-level) | -0.4% | Java core, coastal areas of Sumatra and Sulawesi | Long term (≥ 4 years) |

| Fragmented SME contractor ecosystem & low BIM adoption | -0.3% | National, with concentration in outer islands and rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fiscal-Deficit-Driven Cap-Ex Ceilings

The Ministry of Public Works budget plunged 73% to USD 1.9 billion for 2025 after a presidential efficiency mandate, forcing ministries to shelve new physical projects unless co-financed via PPPs. Although the deficit rule underpins macro stability, it shifts risk-sharing toward private investors who demand higher returns, raising project-level costs. State-owned builders now prioritize return-guaranteed toll roads over socially oriented works such as irrigation channels. The Nusantara build illustrates the tension: only 12.1% of allocated funds were spent by May 2024, compelling aggressive outreach to foreign partners. In the near term, financing scarcity may delay non-strategic assets, but it also accelerates market discipline that rewards efficient, well-structured projects.

Protracted Land-Acquisition and Permitting Cycles

Law No. 2/2012 standardized land procurement, yet inconsistent local implementation leaves 15% of owners unsatisfied with compensation, extending timelines by an average of two to three years. In Java, where land values soared up to 500% over a decade, negotiation stalemates frequently require court settlement, stalling high-profile roads and railways. Indirect costs mount quickly: contractors estimate overruns at 15-20% when access roads or utilities must be redesigned around disputed parcels. Attempts to streamline permits through a one-stop OSS system trimmed paperwork but did little to synchronize land and environmental clearances, creating new administrative chokepoints. Until procedural alignment reaches district levels, acquisition lag will remain a structural drag on the Indonesia infrastructure market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Transportation Extends the Connectivity Revolution

Transportation captured 41.87% of the 2025 project value within the Indonesia infrastructure market, reflecting its centrality to cost-of-goods reduction and regional integration. New corridors such as the 1,065.5 km Trans-Java network and the Lampung-Aceh Trans-Sumatra line shorten travel times and underpin commodity supply chains. The Jakarta–Surabaya high-speed rail feasibility stage indicates future passenger rail spending once financial close is reached. Simultaneously, 25 airports have been built or upgraded since 2015, facilitating tourism and e-commerce air-cargo flows, while the maritime “Tol Laut” program enhances port-to-port reliability across 115 ports. The Indonesia infrastructure market size for transportation projects will expand at a 6.88% CAGR through 2031 as public-sector concessional loans dovetail with private toll-road equity, positioning the segment for both volume and margin growth.

Growth potential extends beyond highways. State rail operator PT Kereta Api Indonesia now bundles station commercial rights with track upgrades, creating blended revenue streams attractive to pension funds. In aviation, Dhoho Kediri, the first unsolicited airport PPP at USD 567.7 million, sets a precedent for greenfield deals, while digital air-traffic-management systems enter procurement to raise throughput. Port operators, led by Pelindo, pursue dredging and crane automation to meet 24/7 shipping standards, and investors eye bond-financed refrigerated-container yards that link fisheries to export gateways. Together, these initiatives diversify construction orders and deepen skill requirements, reinforcing transportation’s role as the flagship of the Indonesia infrastructure market.

By Construction Type: New Builds Dominate but Renovation Gains Traction

New construction accounted for 77.35% of Indonesia infrastructure market share in 2025, underscoring the nation’s basic-facility deficit after decades of underinvestment. Greenfield megaprojects such as the Nusantara government precinct, edge data-center campuses, and multi-GW geothermal plants anchor the forward pipeline. Engineering firms deploy Building Information Modeling to compress design cycles, though adoption costs limit penetration among small subcontractors. Crucially, the push for net-zero public buildings generates demand for advanced materials and modular construction methods, opening niches for specialty suppliers.

Renovation is forecast to post a 6.62% CAGR, propelled by aging 1980s–1990s assets that require seismic retrofits and digital upgrades. Java’s dense urban fabric drives most of this spend as traffic volumes strain older bridges and tunnels. Regulation now mandates BIM for public buildings above 2,000 m², prompting owners to integrate predictive-maintenance sensors during retrofits. Financial vehicles such as energy-performance contracts help municipalities fund efficiency upgrades without upfront cash, inviting ESCOs into the Indonesia infrastructure market. As climate change intensifies rainfall and heat stress, retrofit scope increasingly includes green roofs, permeable pavements, and drainage expansions, blending civil works with environmental engineering.

By Investment Source: Private Capital Accelerates within a Public Framework

Public funds still underwrote 75.92% of 2025 disbursements, but private investment into the Indonesia infrastructure market is projected to grow 7.45% annually to 2031 as PPP structures mature. INA’s toll-road and digital-infrastructure platforms validate syndicated-equity models, while multilaterals de-risk geothermal and waste-to-energy plants through political-risk insurance. Ministerial Regulation No. 7/2023 codified 75:25 debt-to-equity norms, providing lenders with clarity on leverage ceilings. Domestic pension funds, capped at 45% infrastructure allocation, enter brownfield refinancing deals to match long-dated liabilities.

Foreign direct investment momentum is evident. The U.S. International Development Finance Corporation put USD 126 million into the Ijen geothermal field, and Nvidia teamed with Indosat for a USD 200 million AI center, signaling convergence of tech and infrastructure capital. Even mining infrastructure benefits: CIMIC’s USD 99.4 million (AUD 154 million) Pomalaa contract packages environmental offset works into EPC scope, meeting global nickel-supply ESG standards. Combined, these trends shift balance sheets away from fiscal dominance, embedding market discipline without sacrificing national-interest oversight.

Geography Analysis

Java retained 57.96% of 2025 spending thanks to dense population and the completed Trans-Java toll-road spine, which now links key industrial clusters in eight hours rather than 14. Mass-transit extensions to South Tangerang and the JORR 2 ring road unlock urban development tracts, while Jakarta’s proposed USD 10.5 billion sea wall awaits presidential sign-off amid rising flood risk. Mature assets now tilt toward capacity upgrades, such as 5G-ready fiber corridors and smart-traffic management. Private developers partner with local governments for transport-oriented complexes, broadening revenue beyond pure civil works.

Sumatra positions itself as the next logistics corridor. Completion of the 2,749 km Trans-Sumatra network draws bulk-commodity firms seeking lower shipping costs, while West Sumatra’s 83 MW geothermal expansion confirms renewable-energy potential. INA’s equity stake underwrites toll segments, and the Asian Development Bank finances connector roads to feeder ports, stitching the island into the national value chain. Secondary cities like Pekanbaru launch waste-to-energy tenders, offering EPC opportunities in urban services.

Kalimantan posts the fastest 6.42% CAGR through 2031, anchored by Nusantara and mining infrastructure upgrades. Port dredging and runway extensions precede the capital’s 2024-2029 construction schedule, ensuring materials flow without bottlenecks. Australian and Japanese firms sign MOUs for water-treatment plants sized for a projected population of 2 million. Simultaneously, South Sulawesi’s nickel corridor benefits from rail and power additions that enable downstream smelting. The region thus shifts from a resource frontier to an integrated industrial-urban ecosystem, providing a diversified workload for contractors.

Regulatory Landscape

Indonesia's construction and infrastructure delivery is regulated primarily by the Ministry of Public Works through the Directorate General of Construction Development (Direktorat Jenderal Bina Konstruksi), under the framework of Law No. 2 of 2017 on Construction Services (as amended). Risk-based business licensing under Government Regulation No. 28 of 2025 has tightened compliance expectations for contractors and consultants, including mandatory standards for business activities and relevant product or service standards.

For public works procurement, Presidential Regulation No. 46 of 2025 (amending the government procurement framework) anchors tendering and contractor selection for state-funded projects. Licensing and professional credentials are increasingly enforced through national digital systems, with business licensing via the Online Single Submission (OSS) system and construction-services data compliance via SIJKT (Sistem Informasi Jasa Konstruksi Terintegrasi). Business Entity Certificates (SBU) and professional certifications (SKK) are registered and monitored through Ministry of Public Works portals, raising the importance of audit-ready documentation for both domestic and foreign participants.

Value Chain Analysis

Indonesia's infrastructure value chain begins with project origination and budgeting, led by central ministries, local governments, and priority programs such as RPJMN 2025-2029 and Nusantara/IKN. Feasibility, design, and permitting follow, typically driven by AEC firms and state-linked delivery agencies, with financing then shaping procurement. Public disbursements are complemented by PPP platforms, including INA-backed vehicles, alongside project-level de-risking in select energy and logistics assets, before packages move into EPC and specialist subcontracting across civil works, MEP, and digital infrastructure.

Upstream supply relies on domestic material producers and equipment channels, but performance is constrained by logistics and coordination gaps across ports, roads, and multi-tier subcontracting. Local content obligations, including requirements under Presidential Regulation No. 12 of 2021 for government-funded construction with a minimum combined LCR and Company Benefit Weight threshold, and the Ministry of Public Works 2025-2029 supply-chain management road map are pushing contractors to qualify local inputs and standardize procurement. Cement illustrates the scale and imbalance, with around 121.6 million tons of production capacity in 2025 versus roughly 70 million tons of domestic demand, while construction input costs in mid-2025 were cited as about 40% higher than in February 2020. This gap reinforces the need for tighter planning, bundled contracting, and digital controls to limit cost overruns and schedule slippage.

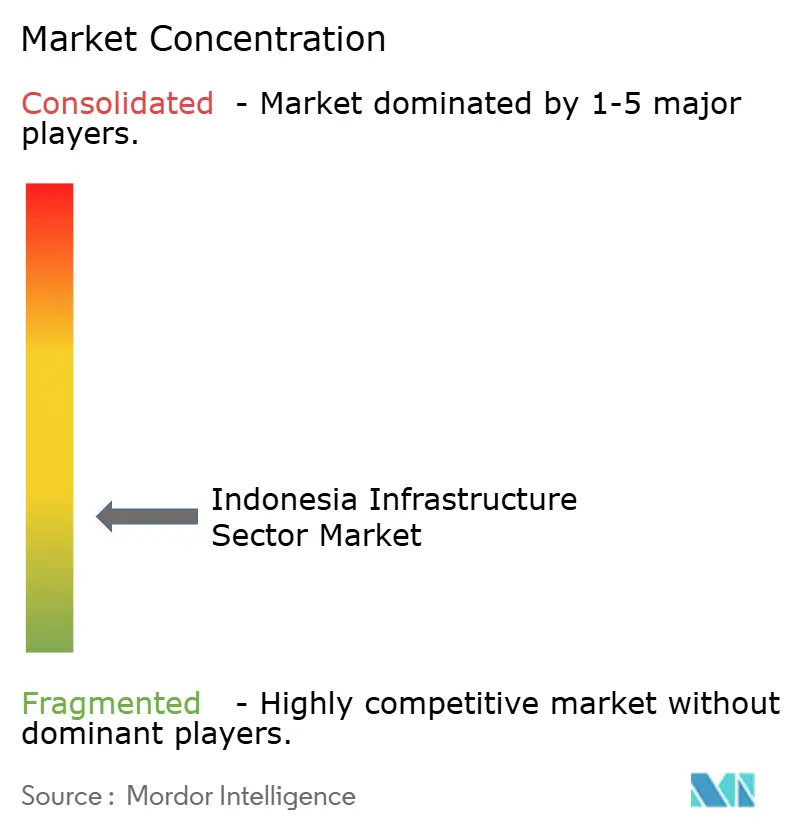

Competitive Landscape

The Indonesia Infrastructure Market is fragmented. State-owned giants dominate headline projects, giving the market a moderate concentration. PT Hutama Karya leads strategic toll-road builds, while PT Wijaya Karya captured a USD 5.5 billion Terminal 2 contract at Hang Nadim Airport, reinforcing SOE dominance in aviation assets. Private firms gain share in segments requiring specialized skills data centers, hospital PPPs, and modular housing where speed and technology matter more than balance-sheet size.

Strategic alliances with foreign EPCs reshape competition. Korea Investment-Sinar Mas injects design automation into hyperscale builds, and CIMIC Group’s mining packages import Australian safety standards. These tie-ups transfer know-how to local subsidiaries, raising the industry’s average technical baseline. Digital adoption emerges as a competitive wedge: companies using BIM-to-field integration report 10-15% schedule savings, giving them an edge in bid evaluations that now score lifecycle cost.

Financing capability distinguishes winners from runners-up. SOEs capitalize on government guarantees but face leverage caps, encouraging divestment of mature assets to pension funds. Private contractors, meanwhile, bundle design-build-finance offers to shorten procurement cycles for cash-strapped municipalities. ESG credentials become a threshold rather than a bonus as lenders screen carbon footprints, forcing late adopters into costly retrofits just to stay in contention.

Indonesia Infrastructure Industry Leaders

PT Nusantara Infrastructure Tbk

PT Adhi Karya (Persero) Tbk

PT Brantas Abipraya (Persero)

PT Hutama Karya (Persero)

PT Indonesia Pondasi Raya Tbk

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Private co-investment and standardized PPP execution remain key whitespace areas as fiscal discipline shifts more projects toward blended finance. INA's role as a catalyst, with USD 10.3 billion in managed assets by 2024, including a USD 2.7 billion toll-road platform and a USD 1.2 billion technology-infrastructure program with Granite Asia, supports repeatable equity syndication. This is particularly relevant for toll roads, digital corridors, and brownfield refinancing that can be packaged for long-duration capital.

Delivery digitization also opens opportunities in productivity-led contracting. Kementerian PUPR's BIM Roadmap (2024 onward) and BIM requirements embedded into public-sector processes via the SIDLACOM lifecycle approach expand demand for BIM-capable designers, contractors, and software-enabled construction management, especially for complex, multi-interface projects such as Nusantara/IKN. Connectivity programs provide near-term volume visibility: the Gending-Besuki section (49.7 km) of the Probolinggo-Situbondo-Banyuwangi (Prosiwangi) Toll Road reached 100% construction completion in April 2026 and moved into operational feasibility assessments, while the Balikpapan-IKN toll road segments are targeted for completion by December 2026. Together, these milestones support opportunities in commissioning, O&M readiness, and adjacent utilities and logistics facilities.

Recent Industry Developments

- July 2026: PT Jasa Marga (Persero) Tbk communicated that the Gending-Besuki section of the Probolinggo-Situbondo-Banyuwangi (Prosiwangi) Toll Road, which reached 100% construction completion in April 2026, entered functional and operational feasibility assessments. This moves activity from heavy civil works into commissioning, readiness, and traffic-opening milestones, and it also pulls demand for supporting services such as tolling systems and maintenance preparation.

- October 2025: PT Bogor Serpong Infra Selaras (BSIS), a consortium including PT Jasa Marga (Persero) Tbk and PT Adhi Karya (Persero) Tbk, signed the toll-road concession agreement for the 32.03 km Serpong-Bogor toll road project (Rp12.35 trillion). The award expands the invest-build-operate pipeline around Greater Jakarta and reinforces the use of consortium structures to mobilize capital and execution capacity for urban connectivity corridors.

- November 2024: A consortium including PT JGC Indonesia and PT Meindo Elang Indah signed a USD 3.5 billion EPCI contract for BP Berau's Tangguh Ubadari CCUS project in West Papua. The contract supports high-value engineering and construction scope in a technically demanding segment, strengthening local execution capability in large-scale energy infrastructure packages with tighter standards on process safety and integrated delivery.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Indonesia infrastructure sector market is defined as the annual value of infrastructure works delivered in Indonesia across major build and upgrade activities, captured in USD terms for a consistent year-on-year view.

Scope exclusions: This sizing excludes routine, non-project operating expenses and small ad hoc repairs that are not tracked as structured infrastructure programs.

Segmentation Overview

- By Infrastructure

- Transportation Infrastructure

- Utilities Infrastructure

- Social Infrastructure

- Extraction Infrastructure

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By Geography

- Java

- Sumatra

- Kalimantan

- Sulawesi

- Rest of Indonesia

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the investable pipeline and the delivery capacity that typically turns plans into executed value. We relied on public budget and planning documents, along with project and procurement disclosures, to understand timing, funding mix, and the types of assets being built.

Sources referenced included, for example, national statistics and economic releases, Ministry of Finance budget publications, the national development planning framework (including RPJMN documents), central bank macro indicators, and tender and PPP announcements published by official bodies. Company annual reports, investor presentations, and reputable press were also used to cross-check project starts and completion signals. A paid subscription covering company financials and a contracts and tenders database was used selectively to reduce missed coverage on large projects. These sources are illustrative only, and many other public references were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what gets executed versus what is only announced, which is a common gap in infrastructure tracking. We spoke with a mix of owners, EPC and contractors, and financing and advisory participants across Indonesia, and we used those conversations to pressure-test cost progression, delivery timelines, and funding availability across key regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 20% | |

| Mid tier: 50% | Functional/Unit leaders: 37% | |

| Smaller Players: 21% | Managers: 43% |

Market-Sizing & Forecasting

Our model starts with a top-down build that reconstructs annual infrastructure value from Indonesia-specific investment signals, including public budget allocations, RPJMN-linked project pipelines, PPP award activity, and observed execution tempo in major corridors. Once the demand pool is shaped, the outputs are corroborated with selective bottom-up checks, such as sampled project ticket sizes multiplied by expected award counts, and contractor capacity and utilization discussions gathered through channel checks.

A few inputs that materially move the model include the split between new construction and renovation, public versus private funding share, timing of large transport works, utilities expansion pace, and inflation in construction inputs that affects realized project value in USD terms. For forecasting, scenario analysis was applied around funding availability and award-to-execution lags. The selected scenario was aligned to expert consensus gathered in interviews so the trajectory stays practical when project timing shifts.

Data Validation & Update Cycle

Validation is done through multiple passes so that outliers do not quietly flow into the final totals. Analysts compare the modeled market level against independent signals such as budget realization patterns, major project awards, and macro capacity constraints, and then unusual jumps are reviewed and adjusted with documented reasons.

Before sign-off, assumptions are re-checked across segments and years, and follow-up outreach is triggered when a change in policy, funding, or delivery pace can materially alter the outlook. Reports are refreshed annually, with interim updates when a major event changes the pipeline, and a final pre-delivery review is completed to ensure the latest public releases are reflected.

Mordor Intelligence's Indonesia Infrastructure Sector Market Size Compared With Other Published Estimates

Published market sizes for Indonesia infrastructure often do not match, even when they use similar labels, because the boundaries and counting rules are not the same. Differences typically come from what is treated as infrastructure value, which year is used as the starting point, and how pipeline timing is converted into annual executed value.

Budget realization signals, PPP award disclosures, and project execution pacing checks are the evidence anchors that keep Mordor Intelligence's estimate tied to delivered infrastructure value in 2025, rather than broader construction activity that may include adjacent spending. In this market, gaps also come from whether social and manufacturing infrastructure are included, how renovation and maintenance are treated, and whether USD conversion uses a consistent year-average rate or a mixed timing approach.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 101.22 B (2025) | |

| Industry Publication A | USD 95.78 B (2024) | Uses a prior-year snapshot and high-level investment discussion, with limited visibility on execution lags, which can undercount years where awards convert into delivered value later. |

| Global Consultancy B | USD 233.76 B (2023) | Applies a broader infrastructure definition that can fold in maintenance and adjacent construction value, and the older base year combined with faster growth assumptions can inflate the comparable market level. |

The spread across figures is mainly explained by scope boundaries and timing conversion from plans into annual delivered value, followed by base-year choice and currency handling. By keeping the counting rules explicit and linking each year to observable funding and execution signals, the final number stays traceable and easier to replicate when assumptions need to be refreshed.

Key Questions Answered in the Report

What is the forecast value of the Indonesia infrastructure market by 2031?

The market is projected to reach USD 140.4 billion by 2031 as planned projects under RPJMN and private PPPs move into execution.

Which segment holds the biggest share in Indonesian civil-works spending?

Transportation commands 41.87% of 2025 spending, led by toll-road and mass-transit build-outs.

Why is private capital expected to rise in Indonesian infrastructure?

Fiscal caps limit pure public funding, while standardized PPP regulations and INA co-investment platforms lower entry barriers for private investors.

Which region will grow the fastest through 2031?

Kalimantan leads with a 6.42% CAGR because of the new capital city and associated mining-logistics upgrades.

How are green bonds influencing Indonesian projects?

Sovereign and corporate green-bond issuance exceeds USD 3 billion, channeling funds into geothermal, mass transit, and flood-control assets while meeting investor ESG criteria.

Page last updated on: