India Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

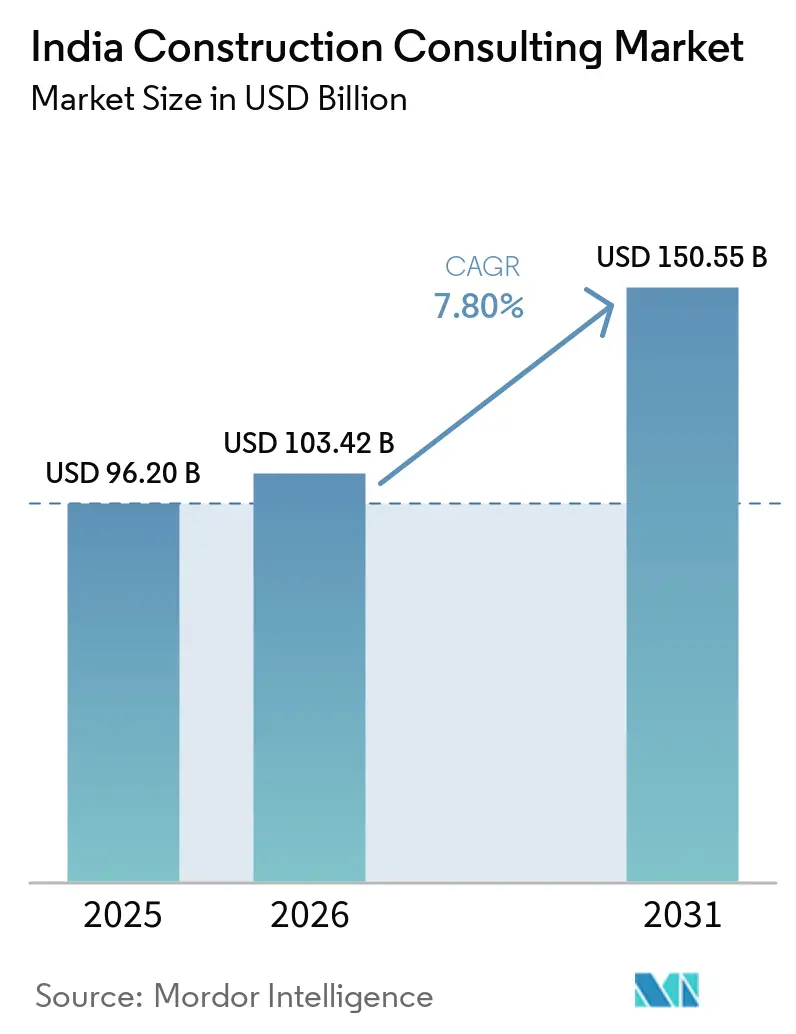

| Base Year Market Size (2025) | USD 96.20 Billion |

| Market Size (2026) | USD 103.42 Billion |

| Market Size (2031) | USD 150.55 Billion |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Construction Consulting Market Analysis by Mordor Intelligence

The India Construction Consulting Market size is expected to grow from USD 96.20 billion in 2025 to USD 103.42 billion in 2026 and is forecast to reach USD 150.55 billion by 2031 at 7.80% CAGR over 2026-2031.

Sustained public outlays under the USD 2,684.82 billion National Infrastructure Pipeline, rising private equity inflows of USD 2.4 billion during the first half of 2025, and the USD 19.5 billion Smart Cities Mission continue to amplify advisory demand. Building Information Modeling (BIM) mandates for federal works valued at over USD 1.19 billion are prompting consultants to expand their digital offerings. At the same time, program-based monitoring on the PAIMANA portal favors firms with real-time dashboarding skills. Semiconductor and data-center capital expenditure above USD 20 billion through 2030 is widening the scope for cleanroom, seismic, and power-redundancy advisory assignments. At the same time, volatile steel and cement prices, along with a shortage of certified cost engineers, are pressuring margins, making technology adoption and regional talent hubs decisive competitive factors for the India construction consulting market.

Key Report Takeaways

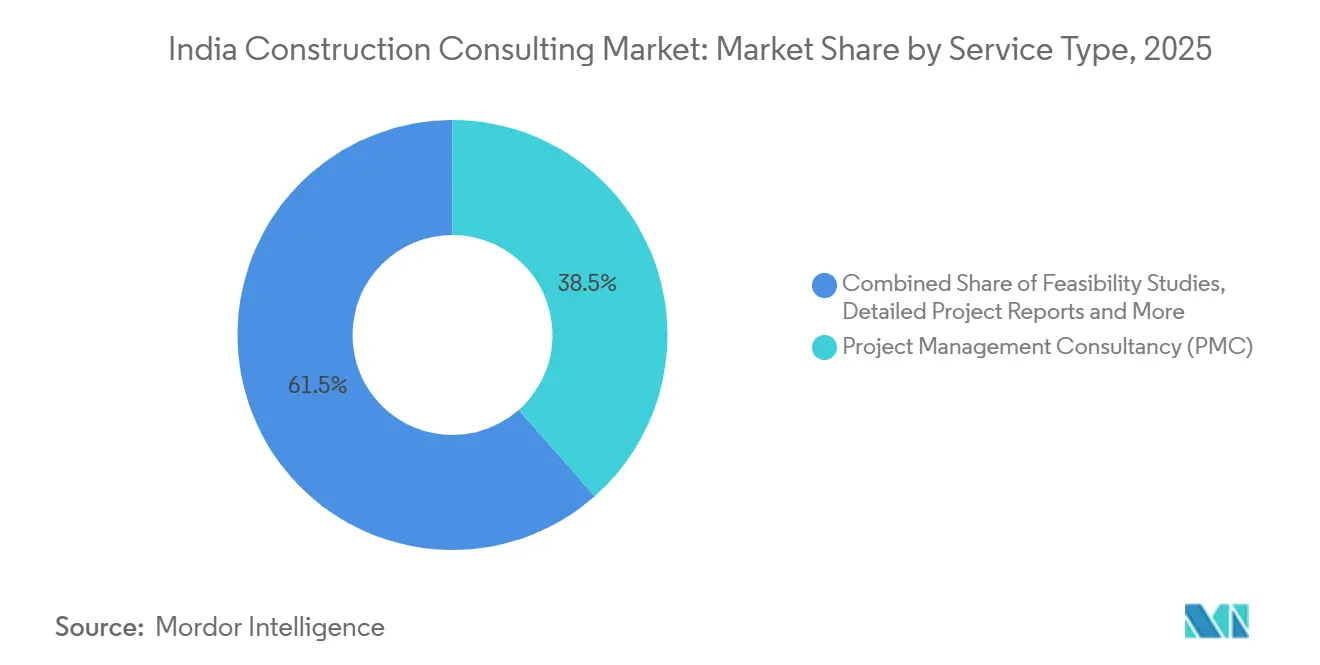

- By service type, Project Management Consultancy captured 38.5% of India's construction consulting market share in 2025; Master Planning is projected to grow at an 8.5% CAGR between 2026 and 2031.

- By sector, residential projects accounted for 37.5% of the India construction consulting market size in 2025, while infrastructure and civil consulting are forecast to advance at an 8.6% CAGR through 2031.

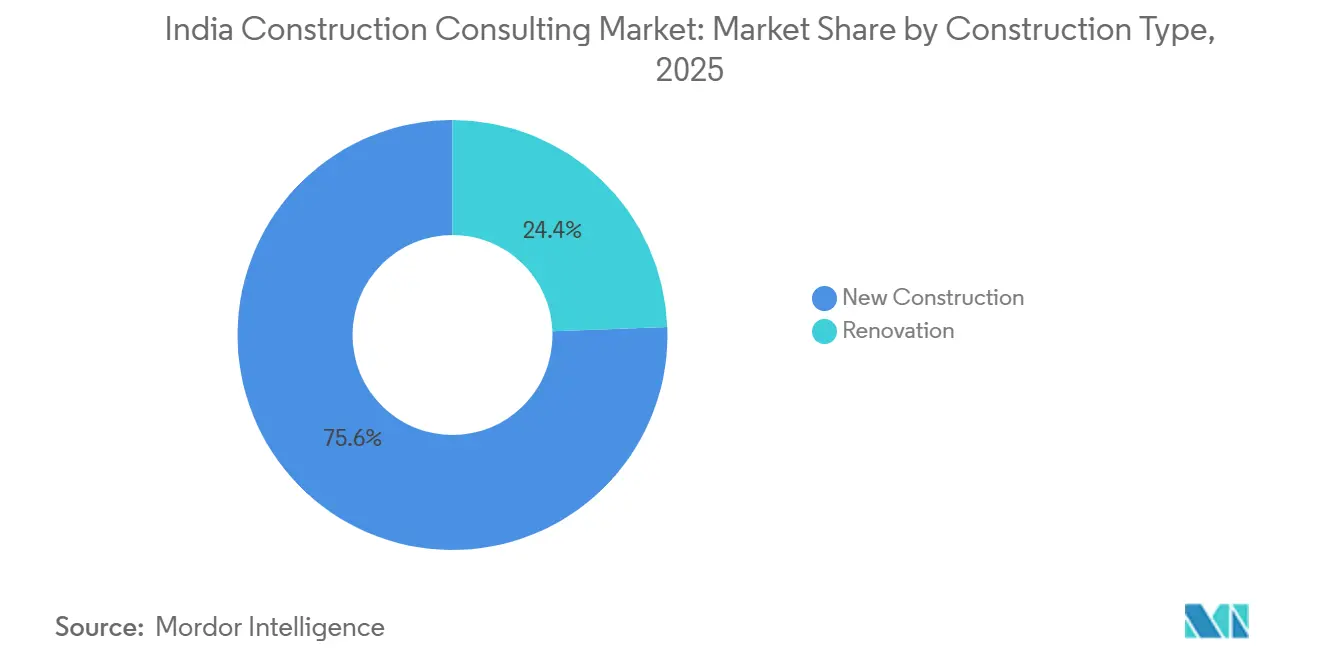

- By construction type, new builds made up 75.6% of the India construction consulting market in 2025; renovation assignments are set to expand at a 9.25% CAGR from 2026-2031.

- By investment source, private funding accounted for 60.5% of the India construction consulting market in 2025, yet publicly financed projects are on track for an 8.75% CAGR over the forecast horizon.

- By geography, the Mumbai Metropolitan Region held 18.58% of India construction consulting market share in 2025; the Rest of India cluster is expected to record a 9.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Infrastructure Pipeline and Smart Cities push | +2.1% | Nationwide, with early traction in Mumbai, Delhi NCR, Bengaluru, and Hyderabad | Medium term (2–4 years) |

| Real Estate Investment Trust and private equity inflows | +1.6% | Mumbai, Bengaluru, Delhi NCR, Hyderabad | Short term (≤2 years) |

| Semiconductor and data-center capital expenditure surge | +1.5% | Gujarat, Karnataka, Tamil Nadu, Telangana | Short term (≤2 years) |

| Digital construction mandates (BIM, Common Data Environment) | +1.3% | Tier-1 metros with spillover into Pune and Ahmedabad | Long term (≥4 years) |

| Environmental, Social, and Governance compliance demand | +1.2% | Commercial offices and industrial parks across India | Medium term (2–4 years) |

| Public-private partnership dispute-resolution reforms | +0.9% | Highways and metro corridors nationwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

National Infrastructure Pipeline and Smart Cities push.

Federal allocations worth USD 2,684.82 billion across 14,569 projects have changed consulting from episodic advice to continuous program management. The completion of 7,741 Smart Cities projects and the roll-out of 100 Integrated Command and Control Centers have embedded digital-twin workflows into municipal briefs. The PAIMANA dashboard tracks 1,392 projects valued at USD 418 billion and rewards advisors who deliver live, validated data to city officials. The 2026 Union Budget earmarked USD 36.5 billion for roads and USD 34.5 billion for railways, locking in multi-year deal flow for the India construction consulting market. These factors are concentrating opportunities among full-service firms able to combine engineering, digital, and quality-assurance credentials[1]Smart Cities Mission, “Progress Report 2025,” smartcities.gov.in .

Real Estate Investment Trust and private equity inflows

Private equity inflows rose 38% year-on-year to USD 2.4 billion during the first half of 2025. Brookfield’s USD 156.3 billion office acquisition and Blackstone’s USD 6 billion data-center pipeline show sustained institutional interest. REIT sponsors mandate third-party project controls, ESG reporting, and IGBC or GRIHA certifications, generating recurring assignments. Mindspace Business Parks alone committed USD 500 million to construction in FY 2026 while targeting 49% renewable energy use, compelling advisors to integrate green metrics from day one. Concentration of capital in Mumbai, Bengaluru, and Delhi NCR leaves secondary cities underserved, offering room for regional firms.

Semiconductor and data-center capital expenditure surge

Micron opened a USD 2.75 billion assembly and test plant in Gujarat in March 2026, and the India Semiconductor Mission 2.0 earmarked an additional USD 894 million. Blackstone, Google, and Adani together disclosed over USD 22 billion in data-center plans, each requiring Uptime Institute Tier III or IV certification, N+1 cooling, and seismic isolation. Such assignments pay 30-40% above standard commercial fees, yet only about 20 domestic consultancies have scalable cleanroom or hyperscale credentials. Concentrated capex is overloading regional capacity, letting global players deploy offshore design hubs to compress schedules[2]Ministry of Electronics and Information Technology, “Semiconductor Mission 2.0,” meity.gov.in .

Digital construction mandates (BIM, Common Data Environment)

The Central Public Works Department now requires BIM on public works above USD 1.19 billion, but enforcement outside metros remains uneven. National Highways Authority of India has added LiDAR, drones, and AI-enabled construction monitoring, cutting rework on pilot corridors by nearly one-quarter. Software licenses of USD 5,000-10,000 per seat and a talent pool of fewer than 15,000 certified BIM coordinators constrain rapid adoption. The March 2026 launch of Powerplay’s India-first AI workforce for construction shows how automation can reduce bill-of-quantities generation by 60%, nudging consultants toward higher-value analytics. Compliance with ISO 19650 information-management standards is now a prerequisite for many REIT-sponsored projects[3]Central Public Works Department, “BIM Circular 2024,” cpwd.gov.in .

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile input costs are squeezing fees | -0.8% | Nationwide, with sharper effects on steel-heavy works | Short term (≤2 years) |

| Talent scarcity in certified project management and cost engineers | -0.7% | National, with peaks in Pune, Ahmedabad, Kolkata | Long term (≥4 years) |

| Fragmented permitting inflates scope creep | -0.6% | Tier-2 and tier-3 cities | Medium term (2–4 years) |

| Artificial-intelligence design automation is commoditizing basic services | -0.5% | Digitally mature metros | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile input costs are squeezing fees.

Steel prices fell 15-20% during 2024-2025, pushing developers to renegotiate and cut consultant margins by roughly 250 basis points. Cement quotes varied by up to 10% quarter-on-quarter in southern states, prompting clients to demand routine value-engineering audits in the Indian construction consulting market. The National Highways Authority of India capped consultant fees at 2.5% of project cost in 2025, down from 3-3.5% earlier, a policy that multiple state agencies have copied. Payment lags extending to 120 days are forcing firms without strong working-capital lines to exit complex infrastructure assignments.

Talent scarcity in certified project management and cost engineers

India needs 60 million skilled construction workers by 2030, but only about 15,000 hold globally recognized Project Management Professional or Royal Institution of Chartered Surveyors credentials. Wages for certified profiles are rising 12-15% annually, and vacancy rates in second-tier cities exceed 20%. Firms rotate metro-based staff, adding travel costs that elevate bid prices. Global consultancies fill gaps via six-month expatriate secondments, but higher fee structures price them out of some public tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: PMC dominates as master planning accelerates.

Project Management Consultancy held 38.5% of India's construction consulting market share in 2025, underpinned by oversight on the 26,425 km Bharatmala highway program and nearly 1,800 km of metro lines. Master Planning and other strategy-led services are on course to register an 8.5% CAGR, reflecting demand for integrated land-use, utilities, and digital twin blueprints across semiconductor corridors and hyperscale data center parks. The India construction consulting market size tied to feasibility studies remains about one-quarter of revenue. Still, basic drafting and quantity surveying are now being automated, squeezing margins. Advisors scale advantage through ISO 19650-compliant Common Data Environment platforms that reduce rework by 20% and lift realization rates on multidisciplinary briefs. Firms without such digital depth are losing share or partnering with software houses to defend positions.

Second-tier cities still rely on AutoCAD deliverables, giving mono-discipline outfits a foothold, yet program-based contracting via the PAIMANA portal is moving national clients toward single-window consortia. AI-driven quantity take-off tools are freeing senior staff for higher-margin dispute-resolution and lender-engineer mandates. As public tenders now require USD 60-120 million in indemnity cover, only well-capitalized firms can afford the premium, leading to a steady rise in concentration in the Indian construction consulting market.

By Sector: Residential leads while infrastructure surges

Residential consulting accounted for 37.5% of the India construction consulting market in 2025, underpinned by affordable housing drives and rent-yield REIT platforms. Infrastructure and civil projects are projected to clock the fastest expansion at an 8.6% CAGR through 2031, fueled by USD 36.5 billion for roads and USD 34.5 billion for railways in Budget 2026. Transportation infrastructure remains the largest slice within this bucket, demanding corridor development plans, drone surveys, and AI-based quality control. Energy and utilities work, including solar and transmission corridors, is adding grid integration and battery storage feasibility to the scope. Commercial categories such as office, retail, and logistics account for roughly 30% of revenues, with hyperscale data centers as the star performer.

Data-center consulting pays margins of 30-40% above office work because of stringent Tier III/IV redundancy rules. REIT sponsors are dictating green metrics and stable rental yields, which oblige technical audits each quarter. Retail assignments face online-commerce headwinds yet pivot toward experiential malls that need entertainment and F&B layout choreography, a niche where design thinkers can shine inside the India construction consulting market.

By Construction Type: New builds dominate, renovation gains pace

New construction accounted for 75.6% of India's construction consulting market share in 2025, mirroring the country’s infrastructure deficit. Renovation services, however, are set to log a 9.25% CAGR to 2031 as commercial assets aged 15-20 years seek IGBC or GRIHA upgrades. Retrofit work commands 20% higher fees per square foot due to complexity in live buildings. Code updates under the 2024 Energy Conservation Building Code require envelope and HVAC overhauls that certified energy auditors must validate, lifting demand for specialist audits.

Major greenfield projects like Pune Metro Phase 2 and Hyderabad Metro Phase II ensure that new-build pipelines remain strong. Yet tightening urban plots, faster permit cycles for alterations, and green-bond incentives are encouraging owners to refurbish instead of raze. That balance lets consultants diversify cash flows within the India construction consulting market and hedge against cyclical slowdowns in new launches.

By Investment Source: Private funding leads, public spending accelerates.

Private capital accounted for 60.5% of the construction consulting market in India in 2025, yet publicly financed programs are forecast to grow faster at an 8.75% CAGR, supported by the National Monetization Pipeline worth USD 198.8 billion. Public agencies demand ISO 9001 quality systems and heavy indemnity cover, creating high entry barriers. The litigation-prone environment has, ironically, boosted independent-engineer workloads as parties seek to prevent disputes.

Private sponsors, mostly REITs and data-center developers, insist on quarterly ESG disclosures and value-engineering workshops, pushing consultants towards digital reporting dashboards. Payment security from escrow structures offsets tighter fee negotiations, helping balance sheets. Government invoices take up to 120 days to process, but supply multi-year visibility. Leading firms, therefore, juggle both pools to spread risk and maintain recurring revenue in the India construction consulting market.

Geography Analysis

Mumbai Metropolitan Region captured 18.58% of the India construction consulting market share in 2025, anchored by the USD 151.5 billion Coastal Road and the 33.5 km underground Metro Line 3, which required extensive utility relocation and tunnel advisory. Delhi NCR follows closely, driven by the 82.15 km Regional Rapid Transit System and the new Noida International Airport, now under construction and set to serve 12 million passengers annually from 2027. Bengaluru’s 73.75 km metro expansion and USD 154.8 billion Terminal 2 have turned the city into a metro-and-airport advisory hub. Yet, local scarcity of certified cost engineers inflates wages by 12-15% each year.

The Rest of India block is projected to register the fastest CAGR of 9.05% to 2031. Drivers include Pune Metro Phase 2, Hyderabad Metro Phase II, and Chennai Airport Terminal works, along with 6,376 km of highway awards spread over 24 states in FY 2026. Consultants operating here face fragmented permitting and fewer BIM mandates, so they blend local field offices with central digital hubs to cut lead times. Data-center and semiconductor investments cluster in Gujarat, Karnataka, Tamil Nadu, and Telangana, stretching available cleanroom design capacity and inviting global firms to step in.

Nationwide dispersion of projects under Smart Cities and Bharatmala is compelling advisors to staff regional centers for faster clearances. Tier-2 cities prize cost efficiency over digital sophistication, handing price-oriented contracts to smaller outfits while elite firms capture metro works rich in technology and ESG content. Upcoming airport privatizations worth USD 71.4 billion across 11 facilities add another layer of independent-engineer and lifecycle-due-diligence opportunities for the India construction consulting market.

Competitive Landscape

The India construction consulting market is moderately fragmented, with the ten largest firms - Larsen & Toubro, Tata Consulting Engineers, AECOM India, WSP India, Jacobs Engineering, RITES, Ircon International, Mott MacDonald, Ramboll, and Shapoorji Pallonji accounting for 40-45% of total revenue. International firms leverage global design hubs, BIM libraries, and ISO 19650-compliant platforms to secure mandates for multi-state highways, metros, and airports. Domestic players like RITES and Ircon rely on cost leadership, local expertise, and government empanelment to win public-sector projects. Mandatory professional indemnity coverage of USD 60-120 million per project and ISO 9001 requirements create barriers for new entrants, protecting incumbents.

Strategic initiatives focus on digital and advisory upgrades. L&T expanded its grid integration and nuclear capabilities by acquiring Sargent & Lundy’s Indian operations. At the same time, Tata Consulting Engineers launched an AI-enabled design optimization suite that reduced design cycles by up to 50%. WSP opened a global design hub in Hyderabad for 24/7 modeling support, and Jacobs introduced drone-based construction monitoring, achieving 20% rework savings in pilot projects. These efforts shift revenue toward higher-margin services such as master planning, risk analytics, and independent engineering, countering the commoditization of drafting and quantity surveying tasks.

Technology-driven challengers like Voyants Solutions and Builtattic use generative design and automated clash-detection tools to cut design fees by 40-50%, attracting cost-sensitive residential developers and data-center clients. However, their role in large public tenders is limited due to empanelment and indemnity requirements. Hyperscale data-center and semiconductor projects remain niche markets served by fewer than 20 consultancies capable of cleanroom HVAC, ultra-pure water systems, and seismic-isolation design, which allows premium pricing. The market sees intense price competition for routine PMC assignments, while specialized expertise commands higher margins, maintaining a moderately fragmented structure.

India Construction Consulting Industry Leaders

Larsen & Toubro (L&T-Sargent & Lundy / L&T Infra Engg)

Tata Consulting Engineers

AECOM India Pvt Ltd

WSP India

Shapoorji Pallonji Engineering & Construction

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Micron opened a USD 2.75 billion semiconductor assembly and test facility in Gujarat, unlocking demand for cleanroom advisory and ultra-pure water design.

- March 2026: Powerplay introduced an AI workforce for construction with 60% productivity gains in bill-of-quantities generation.

- February 2026: Adani Group announced USD 15.9 billion in airport investments over five years to reach 200 million passengers annually, spurring terminal expansion mandates.

- January 2026: Civil Aviation Ministry privatized 11 airports bundled for USD 71.4 billion, requiring lifecycle due diligence from empaneled consultants.

India Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design and Engineering Services |

| Master Planning and Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Mumbai Metropolitan Region |

| Delhi NCR |

| Pune |

| Bengaluru |

| Hyderabad |

| Chennai |

| Kolkata |

| Ahmedabad |

| Rest of India |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design and Engineering Services | ||

| Master Planning and Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Mumbai Metropolitan Region | |

| Delhi NCR | ||

| Pune | ||

| Bengaluru | ||

| Hyderabad | ||

| Chennai | ||

| Kolkata | ||

| Ahmedabad | ||

| Rest of India | ||

Key Questions Answered in the Report

How big will the India construction consulting market be by 2031?

It is projected to reach USD 150.55 billion by 2031, expanding at a 7.8% CAGR over 2026–2031.

Which service type currently dominates consulting demand?

Project Management Consultancy held 38.5% of India's construction consulting market share in 2025 and remains the core revenue stream.

Where are the fastest growth opportunities located?

Tier-2 and tier-3 regions outside the major metros are forecast to grow at a 9.05% CAGR as metro rail, airport, and data-center projects spread nationwide.

What impact do BIM mandates have on consultants?

Federal BIM requirements for projects over USD 1.19 billion are driving adoption of digital design tools, reducing rework by about 20% and increasing demand for certified coordinators.

How is private equity influencing the sector?

PE and REIT inflows of USD 2.4 billion in H1 2025 call for rigorous third-party oversight, boosting recurring fee income for advisors certified in ESG reporting.

Are AI tools a threat or an opportunity for consultants?

AI automates low-complexity drafting and quantity surveying, compressing fees while freeing capacity for higher-margin risk analytics and owner-representation roles within the industry.

Page last updated on: