North America Scaffolding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.08 Billion |

| Market Size (2026) | USD 7.34 Billion |

| Market Size (2031) | USD 9.93 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

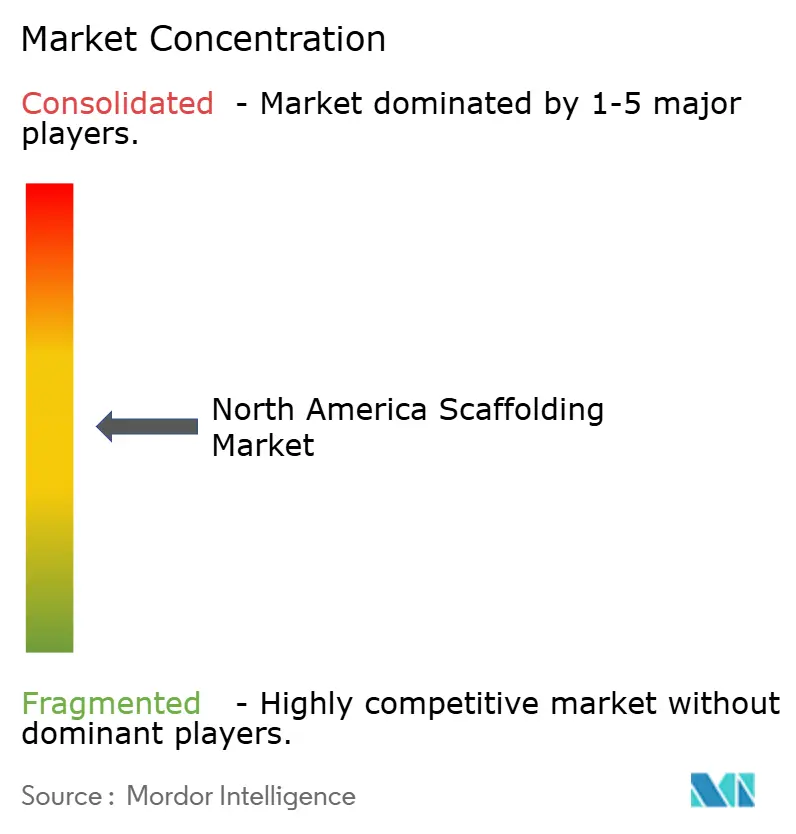

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Scaffolding Market Analysis by Mordor Intelligence

The North America Scaffolding Market size is expected to grow from USD 7.08 billion in 2025 to USD 7.34 billion in 2026 and is forecast to reach USD 9.93 billion by 2031 at 6.23% CAGR over 2026-2031.

The North America scaffolding market is supported by an aging stock of bridges, industrial plants, commercial facades, and utility assets that require repeated access work rather than one-time installation. Public construction spending continues to support visible project pipelines for scaffolding contractors and rental operators across the region. Demand also stays firm because commercial construction, energy retrofits, and industrial turnaround work continue to require fixed access systems where aerial platforms are less practical. The North America scaffolding market also benefits from the shift toward rental fleets and modular systems, as contractors try to control capital needs, shorten erection time, and work around labor shortages. Competition remains moderate because large integrated providers can offer broad service coverage, while regional firms still hold advantages in local response times and site relationships.

Key Report Takeaways

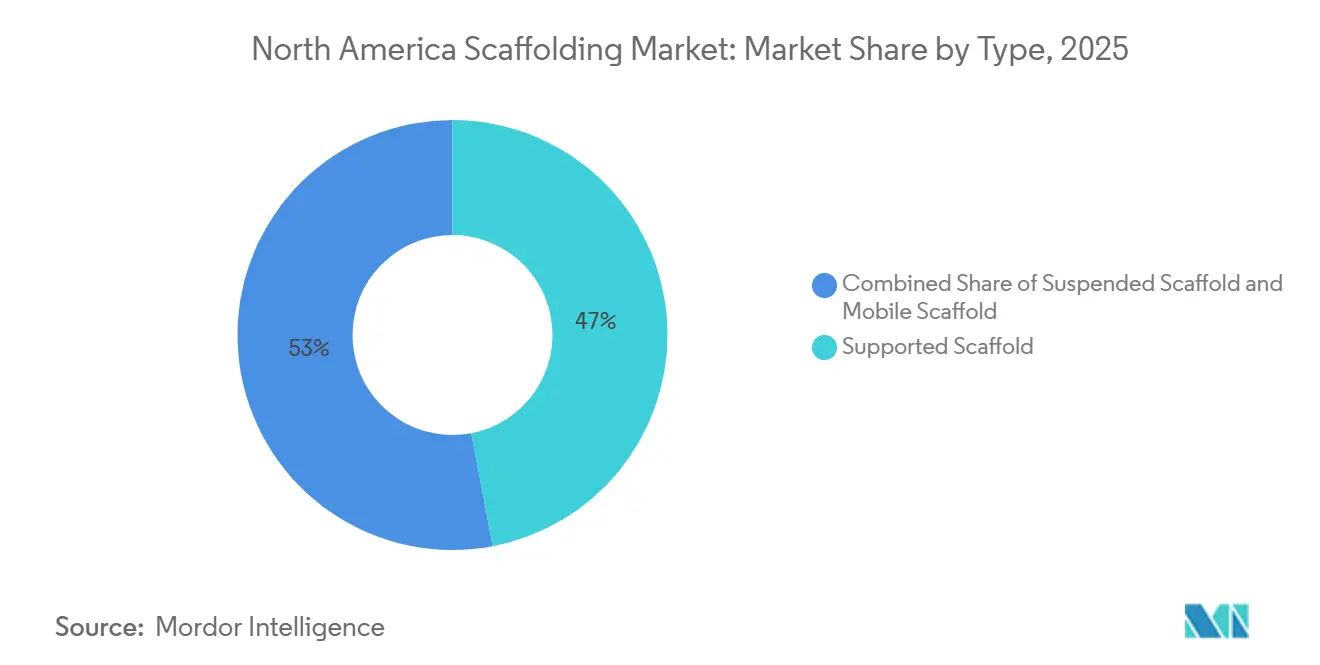

- By type, supported scaffold held a 47% revenue share in 2025, while suspended scaffolding is forecast to expand at a 6.70% CAGR through 2031.

- By system, frame / H-frame systems led with a 32% share in 2025, while modular / ringlock systems are projected to grow at a 7.20% CAGR through 2031.

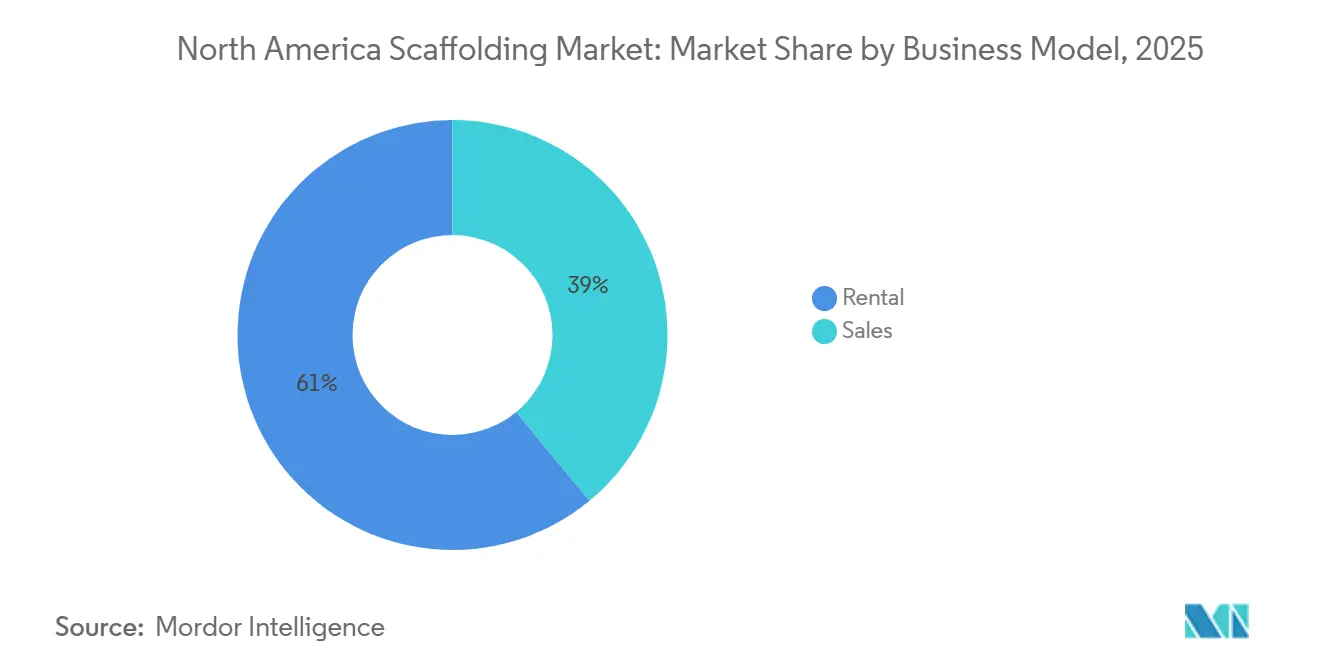

- By business model, rental accounted for 61% of the market in 2025 and also recorded the highest projected CAGR at 6.90% through 2031.

- By material type, steel captured a 58% share in 2025, while aluminum is expected to advance at a 7.50% CAGR through 2031.

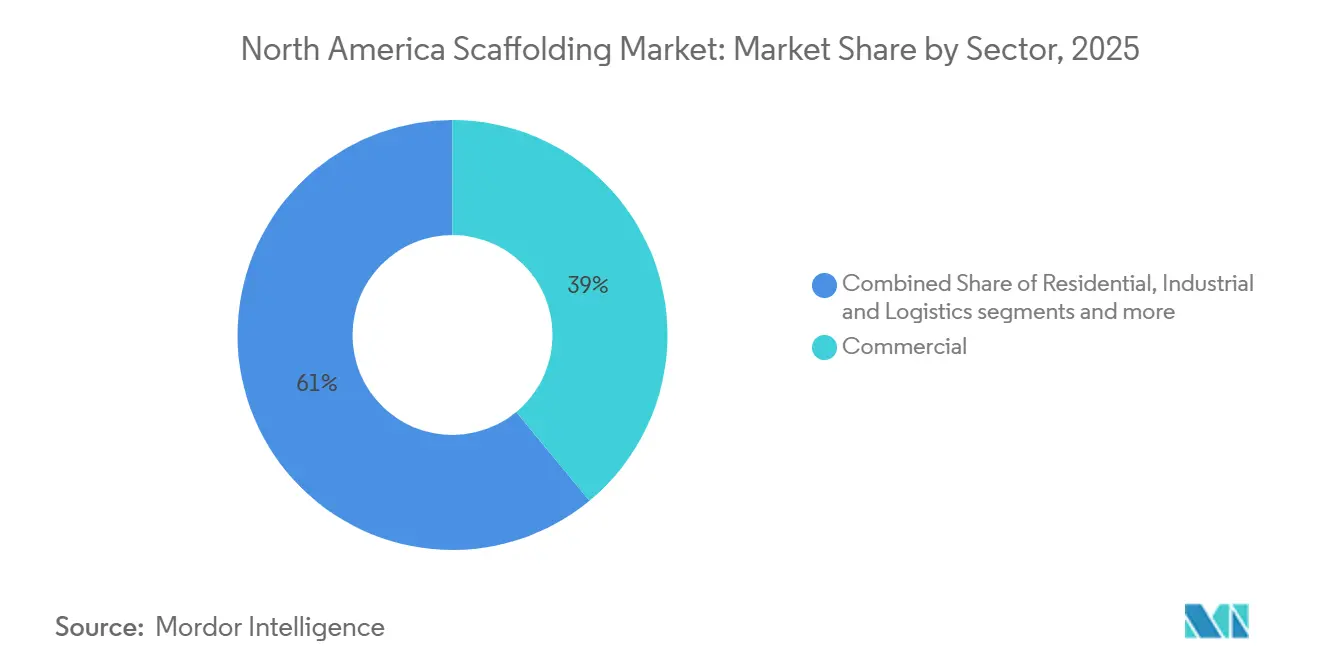

- By sector, the commercial sector accounted for 39% share of the North America scaffolding market size in 2025, while the infrastructure sector is forecast to grow at a 7.10% CAGR through 2031.

- By country, the United States held 70% of the North America scaffolding market share in 2025, while Mexico is projected to record the fastest growth at a 6.80% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Scaffolding Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Renewal and Retrofit Activity Drives Scaffolding Demand | +1.4% | The United States and Canada primarily, with additional gains in Mexico | Medium term (2-4 years) |

| Rental Model Preference Enhances Cost Efficiency and Flexibility | +0.9% | Regional | Short term (≤ 2 years) |

| OSHA Safety Compliance Requirements Support Scaffolding Adoption | +0.8% | The United States primarily, with spillover effects in Canada | Short term (≤ 2 years) |

| Modular and Quick-Assembly Systems Accelerate Market Adoption | +0.7% | Regional, strongest in major construction and energy corridors | Medium term (2-4 years) |

| Wind, Energy, and Industrial Maintenance Projects Increase Access Equipment Demand | +0.6% | United States Gulf Coast, Atlantic offshore corridor, and renewable hubs | Long term (≥ 4 years) |

| Growth in Data Center Construction Expands Scaffolding Requirements | +0.5% | The United States primarily, Canada secondarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Renewal and Retrofit Activity Drives Scaffolding Demand

Infrastructure renewal remains the strongest demand base for the North America scaffolding market because repair and rehabilitation work is continuous across transport, utility, and industrial assets. Public highway construction spending reflects a large and visible pipeline for access work on bridges, elevated roads, and related structures[1]U.S. Census Bureau, “Construction Spending, April 2026,” U.S. Census Bureau, census.gov. Retrofit activity also tends to use more scaffolding per job than new construction because crews must work around existing structures, tighter access points, and partial occupancy conditions. This pattern is also relevant in Canada, where transit projects, municipal bridge programs, and facility upgrades keep demand steady across major provinces. The result is a demand floor for the North America scaffolding market that is less exposed to short-term swings in private construction cycles.

Rental Model Preference Enhances Cost Efficiency and Flexibility

Rental remains central to the North America scaffolding market because contractors prefer to treat access equipment as a project cost rather than a long-term owned asset. Rental continues to lead the market because it offers a combination of financial flexibility and operational efficiency across a wide range of project durations. International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP) make rental more attractive for many firms that want to limit capital intensity and keep fleet maintenance off their balance sheet. The model also allows rental providers to spread the costs of transport, storage, inspection, and replacement across multiple projects simultaneously. As a result, the North America scaffolding market continues to favor operators with large fleets, high utilization, and service packages that include inspection records and reliable delivery.

OSHA Safety Compliance Requirements Support Scaffolding Adoption

The North America scaffolding market gains support from strict safety regulations, as regulated projects favor engineered systems over improvised access methods. Occupational Safety and Health Administration (OSHA) standards require load capacity, design, and fall protection rules that push buyers toward certified solutions[2]Occupational Safety and Health Administration, “1926 Subpart L, Scaffolds,” U.S. Department of Labor, osha.gov. The high level of enforcement activity keeps scaffolding among the most closely monitored areas in construction. This raises the value of documentation, inspection records, and trained erection practices for rental providers and contractors serving public and commercial projects. Canada follows a similar direction through standards-based compliance, which supports the broader shift toward formal system scaffolding in the North America scaffolding market.

Modular and Quick-Assembly Systems Accelerate Market Adoption

Modular systems are expanding faster than the overall North America scaffolding market because they reduce erection time and lower dependence on scarce skilled labor. Modular / ringlock systems are forecast to grow at a 7.2% CAGR through 2031, reflecting rising use on projects with complex geometry and tighter schedules. These systems are gaining traction in data centers, semiconductor facilities, industrial turnarounds, and major civil works because crews can configure them quickly without extensive field modification. Suppliers are aligning their product mix with this shift in project requirements[3]Doka Canada, “Doka Canada Expands Portfolio with the Introduction of Ringlock Modular Scaffolding,” Doka Canada, doka.com. The North America scaffolding market is therefore moving toward systems that combine speed, repeatability, and easier compliance on demanding sites.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Scaffolding Labor Shortages Constrain Project Execution | -0.7% | Regional, with the strongest pressure in industrial and renewable corridors | Short term (≤ 2 years) |

| High Capital and Maintenance Costs Increase Fleet Ownership Burden | -0.4% | Regional, with stronger pressure on mid-sized rental operators | Medium term (2-4 years) |

| Freight, Storage, and Site Logistics Complexity Raises Operating Costs | -0.3% | Regional, especially in dense urban and remote project locations | Short term (≤ 2 years) |

| Exposure to Construction Cycle Volatility Impacts Market Demand | -0.3% | Regional, especially among firms with heavy commercial real estate exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Scaffolding Labor Shortages Constrain Project Execution

Labor availability is the most immediate operating constraint in the North America scaffolding market because access to work depends on trained crews and careful site execution. The construction sector continues to need a large number of additional workers to maintain a balance between labor supply and expected demand. Many firms report project delays caused by worker shortages, which directly affect scaffold erection and dismantling and project timing. For scaffolding contractors, this problem affects mobilization speed and the ability to serve multiple jobs simultaneously. It also reinforces the move toward modular systems and rental partners that can reduce labor intensity inside the North America scaffolding market.

High Capital and Maintenance Costs Increase Fleet Ownership Burden

High fleet ownership costs remain a restraint on the North America scaffolding market, especially for firms that cannot spread maintenance and replacement costs across a broad rental base. Scaffolding components are subject to recurring inspection, repair, and retirement requirements in regulated environments. Steel-based fleets are especially exposed to repair and replacement cycles in corrosive or high-use settings, while transport and storage add another layer of fixed cost. This creates a structural advantage for larger operators, allowing them to centralize procurement, rotate inventory, and achieve better utilization across regions. Over time, that cost gap supports consolidation and makes scale more important in the North America scaffolding market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Supported Systems Anchor the Market, Suspended Scaffold Gains Momentum

Supported scaffold held 47% of the North America scaffolding market share in 2025, making it the core system for construction, maintenance, and retrofit work across the region. Its lead came from broad job-site fit, ease of deployment on standard projects, and the load-bearing performance needed in many industrial and commercial settings. Contractors also rely on supported systems because they work across new construction and rehabilitation scopes with fewer access limitations than specialized alternatives. In the North America scaffolding industry, this gives supported scaffold a broad installed base across urban construction, infrastructure repair, and plant maintenance. The segment also benefits from the rental model because large fleets of standardized components are easier to rotate between projects and regions.

Suspended scaffolding is forecast to grow at a 6.7% CAGR through 2031, which puts it ahead of supported systems in growth terms. That faster pace reflects rising demand in facade restoration, bridge soffit access, dam inspection, and other vertical or underside applications where supported systems are less practical. Older glass curtain wall buildings and urban towers now require ongoing access for maintenance and repair, which expands the use case for suspended equipment. Mobile scaffolding plays a role in fit-out work and light maintenance, but supported and suspended systems shape the main direction of the North America scaffolding market. The contrast between supported scaffold scale and suspended scaffold growth shows how demand is shifting toward harder-to-reach assets and more specialized access work.

By System: Frame / H-Frame Scaffolding Holds Scale, Modular / Ringlock Improves Project Economics

Frame / H-frame systems accounted for 32% of the market by system type in 2025, making them the largest system category in the North America scaffolding market. Their position reflects wide use in residential buildings, standard commercial facades, and lighter-duty jobs where familiarity and ready availability matter more than design flexibility. These systems remain attractive because crews know them well, and many contractors can source them quickly through local rental networks. In the North America scaffolding industry, that familiarity supports steady repeat demand on routine projects with simpler shapes and lower customization needs. Tube / coupler systems also remain relevant on industrial sites where crews need custom layouts around fixed equipment and process lines.

Modular / ringlock systems are projected to grow at a 7.2% CAGR through 2031, making them the fastest-growing system type. Their appeal lies in faster assembly, greater adaptability to complex layouts, and a stronger fit for data centers, semiconductor plants, and long-duration civil works. Cuplock remains a useful middle ground because it offers faster setup than tube-and-coupler while still supporting larger project volumes. Suppliers are investing in this category because it aligns with tighter schedules and labor constraints. The system mix in the North America scaffolding market is therefore moving from standard configuration toward higher-productivity formats that save time and reduce skilled labor pressure.

By Business Model: Rental Dominance Reflects Structural Cost Logic

Rental accounted for 61% of the North America scaffolding market in 2025 and is also the fastest-growing business model through 2031, with a 6.9% CAGR. That combination is important because it suggests the business model is strengthening, not just defending its installed base. Contractors continue to prefer rental when projects vary in duration, component type, and delivery timing, since owned fleets can sit idle between jobs or require repair before the next mobilization. The model also helps customers avoid the storage, inspection, and replacement burdens that can quickly escalate under safety and quality rules. In the North America scaffolding market, rental operators with deep fleets can shift assets between commercial, infrastructure, and industrial jobs more efficiently than firms that rely solely on ownership.

Sales still matter for industrial clients that use the same configurations repeatedly and want direct control over on-site assets. Those buyers are more common in long-cycle maintenance programs, captive plant environments, and specialized industrial settings where access systems are used continuously. Even so, the direction of the North America scaffolding market remains clear, as more customers prefer service packages over equipment alone. Rental providers can combine delivery, layout support, inspection records, and fleet replacement into a single relationship, thereby raising switching costs and supporting repeat business. This keeps rental at the center of competitive strategy across the region.

By Material Type: Steel Holds the Largest Share, While Aluminum Gains Momentum

Steel accounted for 58% of the market by material type in 2025, making it the largest segment in the North America scaffolding market. Its lead reflects higher load capacity, lower upfront unit cost, and strong fit with heavy industrial, petrochemical, and high-rise applications. Steel also benefits from contractor familiarity and a long history of use in demanding work environments where structural strength is the main priority. That makes it the default option across many plant maintenance jobs and larger supported scaffold installations. Timber or plywood and plastic or fiberglass remain smaller niches, mainly serving temporary, budget-sensitive, or specialty electrical and corrosive settings.

Aluminum is forecast to grow at a 7.5% CAGR through 2031, making it the fastest-growing material segment. The growth story is tied to lower weight, easier handling, and reduced labor hours during erection and dismantling. Aluminum is also better suited for renovation work, commercial interiors, and coastal or humid environments where corrosion management is a constant concern. These factors help explain why the North America scaffolding market is gradually shifting part of its material mix toward lighter systems, especially where transport speed and crew productivity matter. Steel will keep its scale advantage, but aluminum is gaining ground where project economics depend on lower handling effort and faster turnaround.

By Sector: Commercial Scale Supports Market Weight, Infrastructure Drives the Growth Curve

Commercial construction accounted for a 39% share of the North America scaffolding market in 2025, making it the largest end-use sector in the regional demand mix. Office renovation, retail redevelopment, hospitality upgrades, mixed-use projects, and institutional building work all support this scale. The segment also includes a growing set of large technical facilities, especially data center builds, which require structured access solutions through multi-stage installation programs. This gives commercial work broad volume across cities and secondary metros, even when individual project starts move unevenly. In the North America scaffolding market, commercial activity therefore remains the main source of day-to-day demand.

Infrastructure is projected to grow at a 7.1% CAGR through 2031, which makes it the fastest-growing sector. Bridge rehabilitation, transit expansion, highway upgrades, and energy grid work create long-duration projects that use scaffolding across multiple phases instead of short installation windows. Public construction spending remains high, which supports this stronger growth path. For contractors and rental providers, infrastructure jobs also tend to be longer, more complex, and less exposed to short-term commercial hesitation. That makes infrastructure the most attractive growth lane within the North America scaffolding market over the forecast period.

Geography Analysis

The United States held 70% of the North America scaffolding market share in 2025, making it the clear regional anchor by value. This lead rests on the scale of construction activity, the maturity of the rental network, and the weight of compliance-led demand across public and private projects. Public construction spending supports multi-year work on roads, bridges, and related structures. The country also has a large industrial maintenance corridor across the Gulf Coast, where refineries, petrochemical plants, and power facilities require recurring access services. In the North America scaffolding market, this gives the United States the broadest base of both routine and specialized demand.

Canada contributes a meaningful share of the North America scaffolding market through transit construction, municipal infrastructure rehabilitation, energy projects, and commercial high-rise development. Urban construction in cities such as Toronto and Vancouver supports demand for systems that fit tighter sites and taller structures. Modular formats are well aligned with this setting, and suppliers are responding by expanding engineered system offerings in the country. Canada also benefits from a standards-based approach to safety and execution, which favors formal system scaffolding over improvised solutions.

Mexico is forecast to post the fastest geographic expansion at a 6.8% CAGR, making it the fastest-growing country in the North America scaffolding market over the forecast period. The country is attracting more suppliers seeking exposure to industrial growth and a wider regional customer base. Project activity is also creating room for international firms that can combine system design with on-site technical support. The regional picture in the North America scaffolding market is therefore led by the United States scale, supported by Canadian stability, and accelerated by faster growth in Mexico.

Competitive Landscape

The North America scaffolding market is moderately concentrated, with large integrated providers competing alongside regional specialists and niche industrial access firms. BrandSafway, Sunbelt Rentals, Inc., The Brock Group, Altrad, and PERI are among the names with broad visibility across major project categories in the region. Scale matters because customers increasingly want one provider that can support scaffolding, access planning, temporary works coordination, and compliance documentation. At the same time, regional specialists remain relevant because response speed, local labor availability, and customer familiarity still influence contract awards. This keeps the North America scaffolding market competitive without making it highly fragmented.

Strategic moves by larger players show how competition is evolving. BrandSafway launched the Spider SC1000 Voyager battery-powered traction hoist in January 2026 to improve vertical transport on power-constrained sites, such as bridges, dams, wind farms, power plants, and refineries. In June 2025, BrandSafway also secured a multi-phase access solutions contract for the renovation of Warren Towers at Boston University, which shows the value of bundled access services on long-duration building projects. These moves matter because the North America scaffolding market increasingly rewards providers that combine product depth with project execution capability.

Acquisition activity also shows that companies are building broader service positions rather than relying on a single product line. Altrad completed the acquisition of Stork’s United Kingdom business in February 2025, following its acquisition of Beerenberg in November 2024, expanding its reach in offshore and industrial services. The North America scaffolding market is therefore moving toward a model in which scale, technical breadth, and solution-led service are more valuable than simple equipment supply alone. Regional players can still compete well, but the middle of the market faces the strongest pressure.

North America Scaffolding Industry Leaders

BrandSafway

Sunbelt Rentals, Inc.

The Brock Group

Layher Holding GmbH and Co. KG

PERI SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AT-PAC (Atlantic Pacific Equipment), a company of Umdasch Industrial Solutions and a subsidiary of Doka/Umdasch Group, opened a new branch in Auburndale, Florida, on May 4, 2026, strategically located between Tampa and Orlando to expand service coverage across the Southeast United States. The facility extends AT-PAC's Ringlock system supply, engineering capabilities, and its Hi-Vis digital scaffolding management tool to scaffolding contractors, asset owners, and engineering, procurement, and construction (EPC) firms across Florida's growing industrial and commercial project base.

- April 2026: Solid Platforms Inc. and the Eastern Atlantic States Regional Council of Carpenters (EASRCC) jointly opened the Spilock scaffold manufacturing facility in Johnstown, Pennsylvania, a labor-management partnership built around domestic fabrication of scaffold components from American-made steel. The facility currently employs over 30 union workers, with plans to more than double headcount within the year.

- February 2026: The Naval Sea Systems Command (NAVSEA) issued a sole-source contract notice to Excel Modular Scaffold and Leasing Corporation for modular scaffolding systems and leasing services at Portsmouth Naval Shipyard in San Diego, California, designating the company as the exclusive United States manufacturer and distributor of its proprietary scaffold system.

North America Scaffolding Market Report Scope

The North America Scaffolding Market is Segmented by Type (Supported, Suspended, and Mobile), System (Tube & Coupler, and More), Business Model (Sales and Rental), Material (Timber / Plywood, Steel, Aluminum, Plastic / Fibreglass, and Others), Sector (Residential, Commercial, Industrial & Logistics, and Infrastructure), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Supported Scaffold |

| Suspended Scaffold |

| Mobile Scaffold |

| Tube & Coupler |

| Cuplock |

| Modular / Ringlock |

| Frame / H-Frame |

| Sales |

| Rental |

| Timber / Plywood |

| Steel |

| Aluminum |

| Plastic / Fibreglass |

| Others |

| Residential |

| Commercial |

| Industrial & Logistics |

| Infrastructure |

| United States |

| Canada |

| Mexico |

| By Type | Supported Scaffold |

| Suspended Scaffold | |

| Mobile Scaffold | |

| By System | Tube & Coupler |

| Cuplock | |

| Modular / Ringlock | |

| Frame / H-Frame | |

| By Business Model | Sales |

| Rental | |

| By Material Type | Timber / Plywood |

| Steel | |

| Aluminum | |

| Plastic / Fibreglass | |

| Others | |

| By Sector | Residential |

| Commercial | |

| Industrial & Logistics | |

| Infrastructure | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the 2031 outlook for scaffolding demand in North America?

The North America scaffolding market is projected to reach USD 9.93 billion by 2031, up from USD 7.34 billion in 2026, at a 6.23% CAGR.

Which country leads regional demand?

The United States leads the region with a 70% share in 2025, driven by its large construction base, strong industrial maintenance demand, and a mature rental ecosystem.

Which business model is strongest in this space?

Rental is the leading model with a 61% share in 2025 and the fastest-growing, with a 6.9% CAGR through 2031.

Why are modular systems gaining traction across projects?

Modular / ringlock systems are growing at a 7.2% CAGR because they reduce erection time, improve flexibility on complex sites, and help contractors manage labor shortages.

Which end-use segment offers the best growth opportunity?

Infrastructure offers the strongest growth outlook, with a 7.1% CAGR through 2031, because long-duration bridge, highway, transit, and grid work require repeated access solutions.

What is the biggest operational challenge for scaffolding providers?

The labor shortage remains the main challenge because it slows project execution, limits crew availability, and increases pressure to adopt faster, less labor-intensive systems.

Page last updated on: