India Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

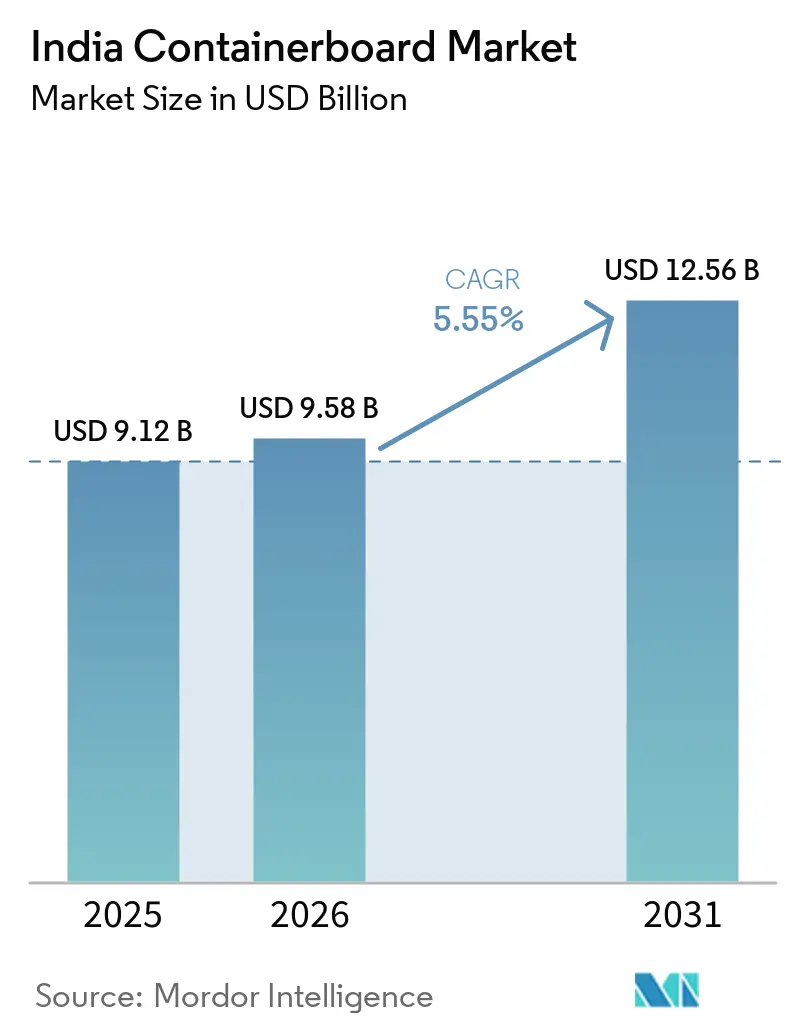

| Base Year Market Size (2025) | USD 9.12 Billion |

| Market Size (2026) | USD 9.58 Billion |

| Market Size (2031) | USD 12.56 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

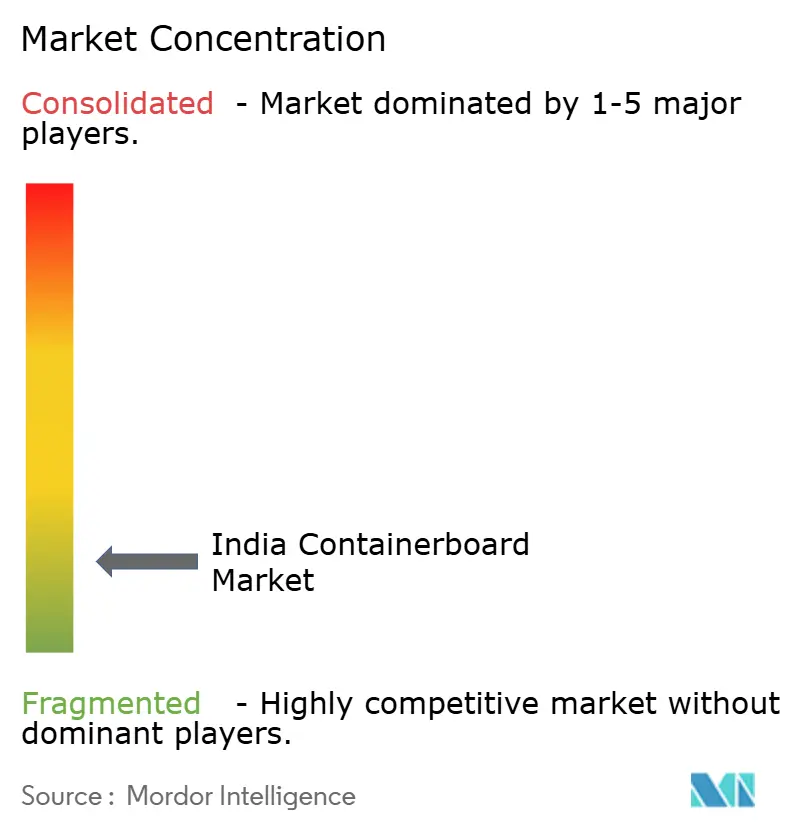

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Containerboard Market Analysis by Mordor Intelligence

The India containerboard market size is expected to increase from USD 9.12 billion in 2025 to USD 9.58 billion in 2026 and reach USD 12.56 billion by 2031, growing at a CAGR of 5.55% over 2026-2031. The Indian containerboard market is drawing support from e-commerce fulfillment growth, food processing expansion, and policy pressure against single-use plastic formats, which are widening consumption across everyday shipping and retail packaging needs. Express parcel volumes are expected to rise from 10 to 11 billion shipments in FY 2025 to 24 to 29 billion by FY 2030, which keeps corrugated secondary packaging at the center of the volume story. The India containerboard market also differs from many peer emerging economies because it combines fast-turn quick-commerce packaging demand with export-grade industrial corrugation, rather than relying mainly on retail-led movement. In the India containerboard market, import normalization and trade remedies could help restore margins for domestic producers, while tighter European waste shipment rules after 2027 could disrupt access to low-cost recovered fiber for mills that still depend on imported furnish. The production-linked investment pipeline is also raising the quality threshold for packaging, because new manufacturing and export capacity needs stronger and more uniform corrugated formats than older domestic retail channels required.

Key Report Takeaways

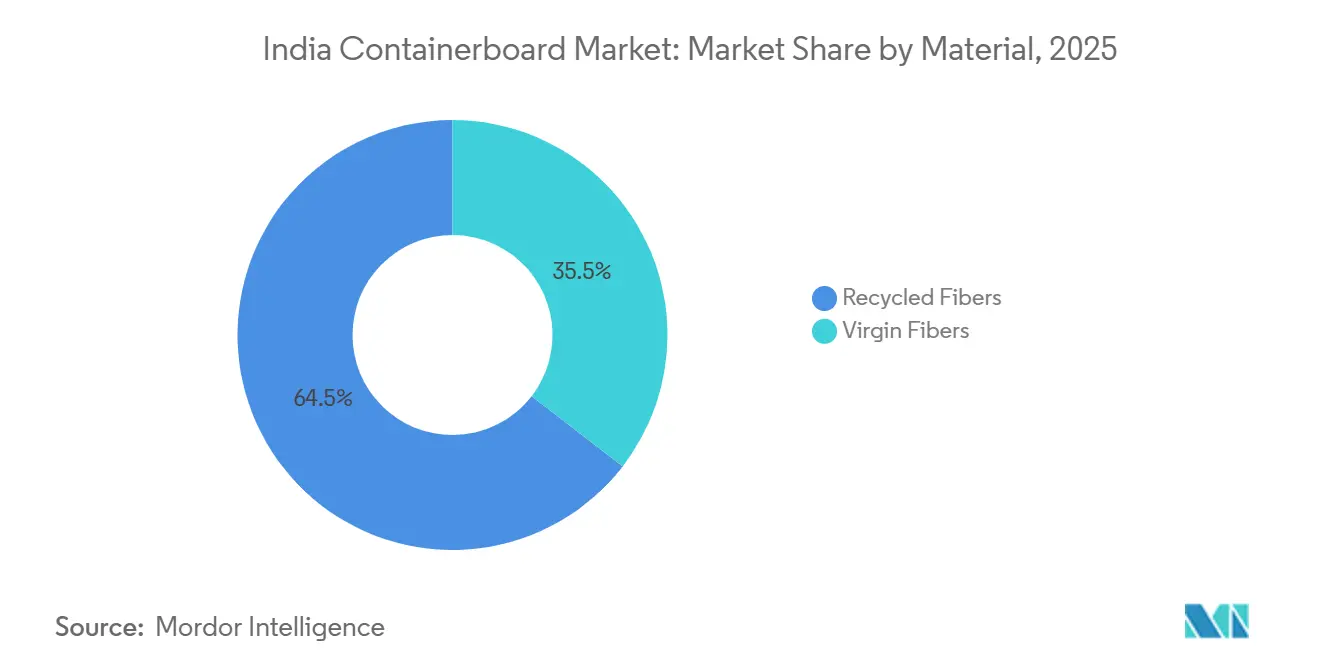

- By material, recycled fibers captured 64.53% of the India containerboard market share in 2025.

- By product type, the India containerboard market size for the kraftliners segment is forecast to advance at a 6.18% CAGR through 2031.

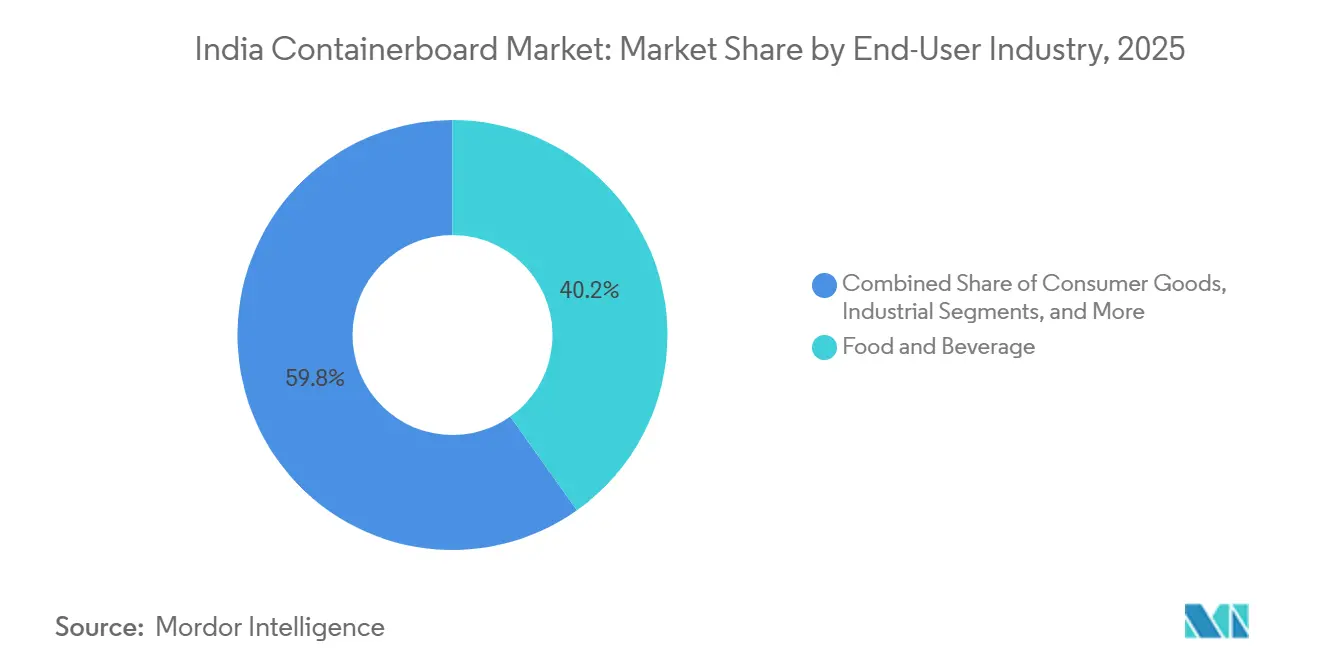

- By end-user industry, food and beverage captured 40.18% of the India containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce And Quick-Commerce Corrugated Demand | +1.4% | Pan-India, led by Tier-1 cities, with spillover to Tier-2 and Tier-3 by 2027-2028 | Short term (≤ 2 years) |

| Food And Beverage Packaging Premiumization | +1.1% | South India, West India, and national FMCG supply chains | Medium term (2-4 years) |

| Regulatory Push Toward Recyclable Fiber-Based Packaging | +0.9% | National, with early compliance gains in Maharashtra, Tamil Nadu, and Karnataka | Short term (≤ 2 years) |

| Manufacturing And Export Logistics Expansion | +0.7% | Gujarat, Maharashtra, Telangana, and Tamil Nadu industrial corridors | Medium term (2-4 years) |

| Lightweighting And Strength Engineering For Automated Corrugation | +0.5% | National, concentrated in automated corrugating hubs in West and South India | Medium term (2-4 years) |

| Premium Kraftliner Import Substitution | +0.4% | Gujarat, Uttar Pradesh, and Andhra Pradesh mill clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce And Quick-Commerce Corrugated Demand

India's quick-commerce sector reached USD 3.35 billion in gross merchandise value in 2024 and is projected to grow to USD 8.83 billion by 2028 at a 27.42% CAGR, which is reshaping packaging demand across urban fulfillment networks.[1]Manish Tiwari, Mohammad Alijah Hasan, and Vineet Tiwari, “Integrating Circular Economy Principles in Quick Commerce, Assessing Customer Satisfaction and Repurchase Behavior,” Asian and Pacific Economic Review, asparev.org Blinkit operated more than 1,500 dark stores across more than 100 cities in 2025, while Zepto and Swiggy Instamart had also scaled to dense dark-store networks, which widened the addressable base for short-cycle corrugated consumption. These networks do not just need more boxes; they need compact and right-sized corrugated packs that can withstand repeated lateral handling from picking to dispatch. That requirement is pushing buyers toward testliner and fluting grades that meet short-span compression and edge-crush needs with greater consistency, rather than relying only on burst-factor thresholds. Mills that still compete mainly on low-cost recycled output are under pressure to upgrade their specification control, because automated, fast-turn delivery systems are exposing weak formations and uneven compression performance more quickly than traditional retail channels did. This change is important for the India containerboard market because it is shifting demand toward technically dependable grades even within high-volume, price-sensitive packaging formats.

Food And Beverage Packaging Premiumization

India's food processing and beverage value chains are steadily tightening packaging specifications as organized retail, food safety requirements, and commitments to recyclable formats all move in the same direction. Brand owners such as Coca-Cola, PepsiCo, and Parle Agro have been aligning their packaging portfolios toward recyclable formats, thereby increasing the use of mono-material and fiber-based secondary packaging in organized distribution channels. Food processors are also reducing pack weights by moving liner grammages from 150 GSM toward 120 GSM while still trying to preserve compression performance through stronger fiber design and better board engineering. In April 2026, the Food Safety and Standards Authority of India issued a draft notification proposing paper, paperboard, cellulose, or other naturally derived materials for pan masala and tobacco packaging, extending the regulatory push for fiber-based formats into a category that had long relied on multi-layer plastic structures. That change matters because southern and western India already has high demand density for these product categories, so that any format migration can flow quickly into regional requirements for testliner and kraft grades. For the India containerboard market, this premiumization trend is raising the baseline expectation for print quality, compression consistency, and recyclability across food-linked corrugated packaging.

Regulatory Push Toward Recyclable Fiber-Based Packaging

The Ministry of Environment, Forest, and Climate Change notified the Plastic Waste Management Amendment Rules, 2026 on March 31, 2026, requiring 30% recycled content in rigid plastic packaging in FY 2025-26 and increasing that threshold to 60% by FY 2028-29. Paper packaging also entered a more formal compliance phase, as extended producer responsibility obligations took effect on April 1, 2026, requiring brand owners, importers, and e-commerce entities to register and meet recovery and recycling targets.[2]Akansha Pal, “What Changed in India's Plastic Waste Management Rules in 2026, EPR, Traceability, and Recycled Content Targets,” Pakka, pakka.com These changes raise the compliance burden for plastic-heavy formats while making traceable and recyclable fiber-based alternatives more attractive in procurement decisions. The effect is already visible in e-commerce packaging choices, where paper-based cushioning and corrugated alternatives are gaining ground as platforms try to simplify compliance and reduce scrutiny on plastic use. The Central Pollution Control Board's certificate-led framework also creates clearer demand signals for recycled-fiber grades, because buyers now have stronger reasons to seek documented recovery and recycling pathways. This regulatory pressure matters for the India containerboard market because it supports demand through compliance needs rather than solely through discretionary sustainability claims.

Manufacturing And Export Logistics Expansion

The production-linked incentive framework had approved 836 applications across 14 strategic sectors by December 2025, attracting more than INR 2.16 lakh crore (USD 24.8 billion) in cumulative investment, and food processing alone had drawn more than INR 9,200 crore (USD 1.1 billion). The Union Budget 2026-27 added a record INR 12.2 lakh crore (USD 140 billion) in capex allocation and included a dedicated INR 10,000 crore (USD 1.1 billion) container manufacturing initiative over five years, which strengthens the broader logistics and packaging base. These investments matter beyond simple box-volume growth, because export-linked electronics, pharmaceuticals, food processing, and automotive components all require corrugated packaging with higher burst strength, greater moisture resistance, and greater compression reliability. That creates a stronger domestic case for virgin-fiber or hybrid-furnish capacity, especially where imported higher-performance liner grades have filled quality gaps. The PLI-linked build-out in food processing is also lifting demand for cup stock, barrier-coated formats, and better-performing secondary packaging from mills that already serve organized manufacturing customers. For the India containerboard market, industrial scaling is steadily raising the technical floor for board quality, not just adding more volume to existing grade structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wastepaper And Imported Fiber Price Volatility | -1.2% | National, with acute exposure in North India and Gujarat mill clusters dependent on seaborne recovered fiber | Short term (≤ 2 years) |

| Power, Fuel, And Freight Cost Inflation | -0.9% | National, with heightened pressure on small mills in North India and East India where grid reliability is variable | Medium term (2-4 years) |

| Quality Variability In Domestic Recovered Fiber Streams | -0.5% | Pan-India, particularly impacting urban fringe and Tier-2 collection catchments | Long term (≥ 4 years) |

| Post-2027 EU Waste Shipment Regulation Exposure | -0.3% | National, with critical exposure for mills in West and East India reliant on European OCC supply | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wastepaper And Imported Fiber Price Volatility

India still relies on seaborne recovered fiber for a meaningful share of recycled-board furnish, and that dependence leaves many producers exposed to sudden cost swings in imported OCC and other feedstock streams. The risk is amplified by currency movement, because INR weakness can push landed costs higher even when dollar-denominated international fiber prices appear stable. This creates a widening gap between integrated players with captive pulp or plantation support and recycled-fiber mills that depend heavily on imported furnish and short procurement cycles. Smaller mills are especially vulnerable because they lack the financial flexibility to build inventory buffers when import conditions turn unfavorable, which can force abrupt production cuts or local price increases. The pressure also changes sourcing behavior, as mills seeking higher-purity recovered inputs compete more directly for premium grades rather than relying on mixed domestic scrap streams. For the India containerboard market, fiber volatility remains the most immediate profitability risk for producers that lack integration and scale.

Power, Fuel, And Freight Cost Inflation

Energy remains the second-largest cost variable in containerboard manufacturing after fiber, and mills continue to face pressure from power, fuel, and transportation costs. One mill disclosed fuel expenditure of INR 4,500 per tonne (USD 51.6 per tonne) and that level shows how quickly energy costs can eat into margin when selling prices soften. Freight costs add another layer of strain, because inland mills serving coastal or distant corrugator customers bear a logistics burden that directly affects price competitiveness. Smaller mills in regions with uneven grid reliability feel this more sharply, since they are less able to smooth disruptions through captive power or diversified sourcing. The inverted GST structure identified in 2025, where paperboard attracted 18% GST while corrugated boxes bore only 5%, also tied up working capital for converters and weakened liquidity across the domestic packaging chain. In the India containerboard market, this cost structure limits how fast producers and converters can invest in quality upgrades, even when demand remains healthy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material - Recycled Fiber Dominance With Rising Virgin-Grade Ambition

Recycled fibers accounted for 64.53% of the India containerboard market in 2025, reflecting the cost logic of a manufacturing base that still depends heavily on recovered fiber to remain competitive. India recycled 50% of used paper and boards, compared with 85% in developed economies, which shows that domestic recovery efficiency is still far below the level needed to fully support mill furnish needs. That gap affects both availability and quality, because weaker collection systems produce a more uneven domestic recovered-fiber stream and keep many mills dependent on imported OCC. Virgin fiber grades remained the smaller material segment, but they are projected to grow at a 6.02% CAGR through 2031, as brand premiumization and investment in import substitution support higher-performance kraftliner demand. The India containerboard market is therefore seeing a two-speed material transition, where recycled grades still dominate volume while virgin grades are becoming more attractive for applications that require higher compression strength, smoother surfaces, and greater consistency.

Virgin grades are also benefiting from trade action, as the Directorate General of Trade Remedies recommended anti-dumping duties of USD 152.27 per metric ton on Chinese virgin paperboard and USD 123.18 per metric ton on Chilean virgin paperboard, which could improve the economics for domestic mills if those measures hold. FSC certification and EPR compliance are becoming commercial entry requirements in the Indian containerboard industry, especially for FMCG and pharmaceutical exporters, who are now screening packaging suppliers more closely for traceability and sustainability credentials.[3]Akansha Pal, “What Changed in India's Plastic Waste Management Rules in 2026, EPR, Traceability, and Recycled Content Targets,” Pakka, pakka.com Paswara Papers illustrates the balancing act within the segment, as it has shifted from a 60:40 kraft-to-kraftliner mix toward a more liner-led output profile while prioritizing high-quality DSOCC imports from the United States over mixed-grade recovered fiber. That move shows how even mid-tier producers are separating commodity recycled output from higher-specification grades, and it also suggests that demand for premium imported recovered fiber can remain firm even if there is only a slow improvement in lower-grade domestic collection.

By Product Type - Testliners Hold Scale While Kraftliners Gain Momentum

Testliners held 44.11% of the India containerboard market share in 2025, reflecting their cost-efficient fit with the country's broad corrugated supply chain and strong availability across domestic mills. More than 140 mills produced testliner grades in India, which helped Fastmarkets launch dedicated monthly recycled containerboard price assessments for North India, West India, and South India in January 2026. That step matters because benchmarked price discovery usually emerges only when a segment has enough depth, repeatability, and regional differentiation to support transparent market references. Fluting also remains a large product class, but its path is becoming increasingly sensitive to lightweighting as higher-performing semi-chemical and engineered grades enable grammage reductions without the same loss in box performance. The India containerboard market still relies on testliners for volume stability, yet the value pool is gradually shifting toward boards that deliver tighter performance across faster, more automated packaging lines.

Kraftliners are projected to grow at a 6.18% CAGR through 2031, supported by e-commerce handling standards, premium retail presentation needs, and domestic efforts to displace imported higher-performance liners. The shift from burst-factor specifications toward SCT and ECT-based evaluation increasingly favors kraftliner in the Indian containerboard industry, because it runs more reliably on high-speed Flexo-Folder-Gluer lines at comparable grammage levels. Producer strategy is starting to reflect that change, as mills are investing in better stock preparation, headboxes, shoe presses, and process control to reduce caliper variability and improve strength retention across lighter basis weights. This means technology is no longer just an efficiency lever in product competition, because it is becoming central to whether a producer can reliably serve premium liner demand as buyer specifications tighten.

By End-User Industry - Food And Beverage Leads While Consumer Goods Expands Fastest

Food and beverage accounted for 40.18% of the Indian containerboard market in 2025, supported by cold-chain expansion, transit-packaging hygiene needs, and the steady scaling of organized food processing. Corrugated boxes accounted for 65% to 70% of logistics packaging in India's food supply chain, giving this end-user base a strong, recurring pull on liner and medium demand. Production-linked investment in food processing has reinforced that position, as new plants require repeatable, retail-ready packaging across domestic and export channels. Consumer goods are projected to grow at a 6.24% CAGR through 2031 as FMCG brands move away from multi-layer plastic secondary packs and quick-commerce platforms widen the number of small, corrugated-ready SKU formats moving through urban delivery systems. The India containerboard market is therefore finding one demand anchor in food-linked packaging stability and another in the faster format diversification that consumer goods continue to create.

Industrial applications remain a critical volume base because automotive components, engineering goods, and chemicals rely on high-stack-compression corrugated formats where liner performance cannot be compromised. The other end-user cluster, which includes pharmaceuticals and agriculture, is also gaining momentum in the Indian containerboard industry as export packaging rules, cold-chain formalization, and traceability requirements steadily raise minimum packaging standards. Paper-packaging EPR obligations that took effect in April 2026 add a compliance layer to procurement decisions in food, beverage, and consumer goods, making the move away from difficult-to-recycle plastic structures more structural than optional. That combination of baseline industrial need and rising regulatory discipline in branded goods is broadening the demand profile, rather than tying growth to a single buyer category.

Geography Analysis

Southern India remained one of the most important production zones in 2026, with integrated assets such as Tamil Nadu Newsprint and Papers Limited in Trichy, Seshasayee Paper and Boards in Erode and Tirunelveli, and Andhra Paper Limited in Rajahmundry shaping regional supply conditions. TNPL's packaging board unit produced 200,075 metric tonnes in FY 2026, its highest-ever board output since inception, demonstrating the scale advantage available to efficient southern mills. Seshasayee Paper began execution of its MDP-IV expansion project in February 2026, following earlier environmental clearance, with a 20% capacity increase from 2.55 lakh tonnes to 4 lakh tonnes over two years and an investment plan of INR 750 crore (USD 86.1 million) to INR 800 crore (USD 91.8 million). The south also benefits from biomass and renewable energy linkages, including bagasse-based energy at TNPL and wind-linked power at Seshasayee, which can soften the operating-cost burden relative to coal-dependent mills. The India containerboard market depends on this southern base not only for capacity but also for the lower-cost, better-quality output that regional FMCG buyers increasingly prefer.

Western India, led by Gujarat and Maharashtra, is the fastest-expanding production and conversion corridor because it combines port access to imported fiber with one of the country's densest converter clusters. JK Paper's Fort Songadh mill in Gujarat commissioned a 400 ADMT per day Valmet BCTMP line in late 2025, directly supporting its ambitions for lightweight coated board and premium liner. N R Agarwal Industries also received approval in February 2026 to increase the duplex board capacity at Vapi Unit I by 25% to 10,000 metric tonnes per month, without separate capital expenditure, underscoring how process optimization can unlock near-term capacity in the western corridor. Demand support in Maharashtra and Gujarat is relatively durable because it is tied to pharmaceuticals, electronics, FMCG, and export-linked manufacturing, rather than to only discretionary retail volume. Northern demand still matters in parallel, and mills in western Uttar Pradesh and nearby clusters serve a large consumer base where quick-commerce and e-commerce networks are extending deeper into Tier-2 cities.

Eastern India remains centered on Odisha and West Bengal, with Emami Paper Mills and other regional assets supporting converter demand in eastern FMCG and pharmaceutical packaging. Emami expanded its packaging board capacity from 132,000 to 180,000 tonnes per annum and upgraded its Balasore mill in 2025, thereby improving the region's ability to supply better multilayer-coated grades. ITC's Bhadrachalam mill in Telangana, with 10.7 lakh tonnes per year across four plants, continues to act as a pan-India supply anchor while the company also targets a 20% increase in value-added paperboard exports to the Middle East and Europe in 2026. The India containerboard market also gained a stronger northern manufacturing foothold when ITC completed the acquisition of Century Pulp and Paper at Lalkuan, Uttarakhand, on March 31, 2026, for INR 3,498 crore (USD 401.5 million), adding 4.8 lakh tonnes per annum of installed capacity and reducing a long-standing geographic gap in its network.

Competitive Landscape

The India containerboard market remains fragmented at the production end, with more than 140 mills producing testliner grades alone, while the wider paper mill base spans 850 to 900 units, of which only around 550 are operational. Yet consolidation is becoming more visible as buyer standards rise, especially in value-added packaging and converter-facing segments, where reliable board quality matters more than simple tonnage availability. The clearest divide is between vertically integrated producers such as ITC Limited, JK Paper Limited, and West Coast Paper Mills Limited and smaller recycled-fiber mills that remain more exposed to fiber costs, energy inflation, and uneven quality control.[4]West Coast Paper Mills Limited, “Annual Report 2024-25,” West Coast Paper Mills Limited, westcoastpaper.com Large integrated players benefit from captive pulp, agroforestry, renewable energy, and a wider distribution reach, which make them more resilient when imports undercut domestic pricing or when costs become volatile. The India containerboard market is therefore fragmented in terms of count, but increasingly polarized in terms of capability and financial resilience.

Strategic moves since late 2024 show how leading producers are extending their reach beyond base paper production. JK Paper acquired a 72% stake in Borkar Packaging Private Limited and completed the merger of Horizon Packs, Securipax Packaging, and JKPL Utility Packaging in December 2024, which strengthened its downstream position in corrugated conversion and folding-carton manufacturing. ITC used M&A to expand geographically and increase capacity through the Century Pulp and Paper acquisition, which gave it a northern footprint and additional installed capacity at a cyclical low point in the paperboards segment. The market also continues to present white space in domestic virgin kraftliner, barrier-coated testliner for food-contact secondary packaging, and lightweight fluting solutions that preserve ECT performance while lowering basis weight. Those areas are attractive because they sit where import substitution, regulatory compliance, and automation-led box performance needs overlap.

Technology adoption is becoming a sharper competitive tool because buyers increasingly specify caliper consistency, moisture control, and formation quality in addition to basic strength metrics. Producers are responding with upgrades such as size presses, better headboxes, advanced stock preparation systems, and drive-control improvements that help stabilize board quality on faster machines. Ruchira Papers commissioned its rebuilt Paper Machine-3 in December 2025, while other mid-tier players are also modernizing to expand their GSM range and improve quality consistency, indicating that competitive pressure is no longer confined to the largest integrated groups. The India containerboard market is also seeing compliance itself become a barrier, because FSC chain-of-custody expectations and EPR-linked registration requirements are narrowing access to higher-quality buyer relationships for mills and converters that remain informal or weak on traceability.

India Containerboard Industry Leaders

ITC Limited

JK Paper Limited

West Coast Paper Mills Limited

Tamil Nadu Newsprint and Papers Limited

Emami Paper Mills Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Khanna Paper Mills integrated Voith DuoFormerD technology at its facility, enhancing paper formation and productivity. The upgrade is expected to improve formation quality for recycled testliner grades destined for e-commerce corrugated applications and positions the company to compete on SCT performance metrics alongside larger integrated producers.

- April 2026: Tamil Nadu Newsprint and Papers Limited recorded its highest-ever paper and board production since inception in FY 2026, with board output reaching 200,075 metric tonnes. The company completed commissioning of its 100 TPD tissue paper machine ordered from ANDRITZ, representing a capital-intensive product diversification that partially insulates the business from containerboard margin cycles.

- March 2026: ITC Limited completed the acquisition of the Pulp and Paper Undertaking of Aditya Birla Real Estate Limited, Century Pulp and Paper, at Lalkuan, Uttarakhand, for INR 3,498 crore (USD 401.5 million). The acquired plant carries 4.8 lakh tonnes per annum of installed capacity, provides a northern India manufacturing presence, and is expected to be EPS-accretive in its first full year, with ITC targeting a 30% to 40% increase in EBITDA per tonne after 2 full operating years.

- February 2026: N R Agarwal Industries received Gujarat Pollution Control Board approval to increase duplex board production capacity by 25%, from 8,000 metric tonnes to 10,000 metric tonnes per month, at its Vapi Unit I, effective immediately and without separate capital expenditure. The company also began land acquisition for a INR 1,200 crore (USD 137.7 million) Unit VI project in December 2025, targeting an additional major capacity block.

India Containerboard Market Report Scope

The India Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The India Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast size of the India containerboard market?

The India containerboard market is valued at USD 9.58 billion in 2026 and is forecast to reach USD 12.56 billion by 2031, growing at a 5.55% CAGR over 2026-2031.

Which material segment leads India containerboard demand?

Recycled fibers lead demand with a 64.53% share in 2025, reflecting the cost structure of India's large recovered-fiber-based mill network.

Which product type is growing fastest in India containerboard?

Kraftliners are the fastest-growing product type, with a forecast CAGR of 6.18% through 2031 as packaging specifications become stricter in e-commerce and export logistics.

Which end-user group contributes the most volume?

Food and beverage leads with a 40.18% share in 2025, supported by organized food processing, cold-chain growth, and recurring logistics-packaging needs.

Why is quick-commerce important for containerboard producers in India?

Quick-commerce increases demand for compact and stronger corrugated packs because dark-store handling and rapid dispatch cycles require dependable compression performance.

What are the main risks for producers through 2031?

The biggest risks are imported fiber price volatility, energy and freight inflation, and possible pressure on recovered-fiber availability after tighter European waste shipment rules.

Page last updated on: