Benelux Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.5 Billion |

| Market Size (2026) | USD 2.57 Billion |

| Market Size (2031) | USD 2.95 Billion |

| Growth Rate (2026 - 2031) | 2.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benelux Containerboard Market Analysis by Mordor Intelligence

The Benelux containerboard market size is expected to grow from USD 2.50 billion in 2025 to USD 2.57 billion in 2026 and is forecast to reach USD 2.95 billion by 2031 at 2.79% CAGR over 2026-2031. The Benelux containerboard market is being supported by a faster shift away from single-use plastics in food service and grocery packaging as PPWR rules move into application from August 2026. Demand is also staying firm because Rotterdam and Antwerp-Bruges continue to anchor a large export and logistics base that depends on heavy-duty corrugated transit packaging. Strong paper and cardboard recovery in Belgium gives the region a healthier recovered fiber pool than many Western European peers, which helps recycled-grade mills manage supply risk. Competition remains moderately concentrated among large integrated European producers and regional converters, and capacity rationalization is still needed because operating rates have improved but are not yet at levels that typically restore full pricing power. Growth in the Benelux containerboard market is still being held back by OCC and energy cost swings and by lower board intensity per parcel over time, but e-commerce expansion and cardboard’s regulatory carve-out in transport packaging continue to support steady demand.

Key Report Takeaways

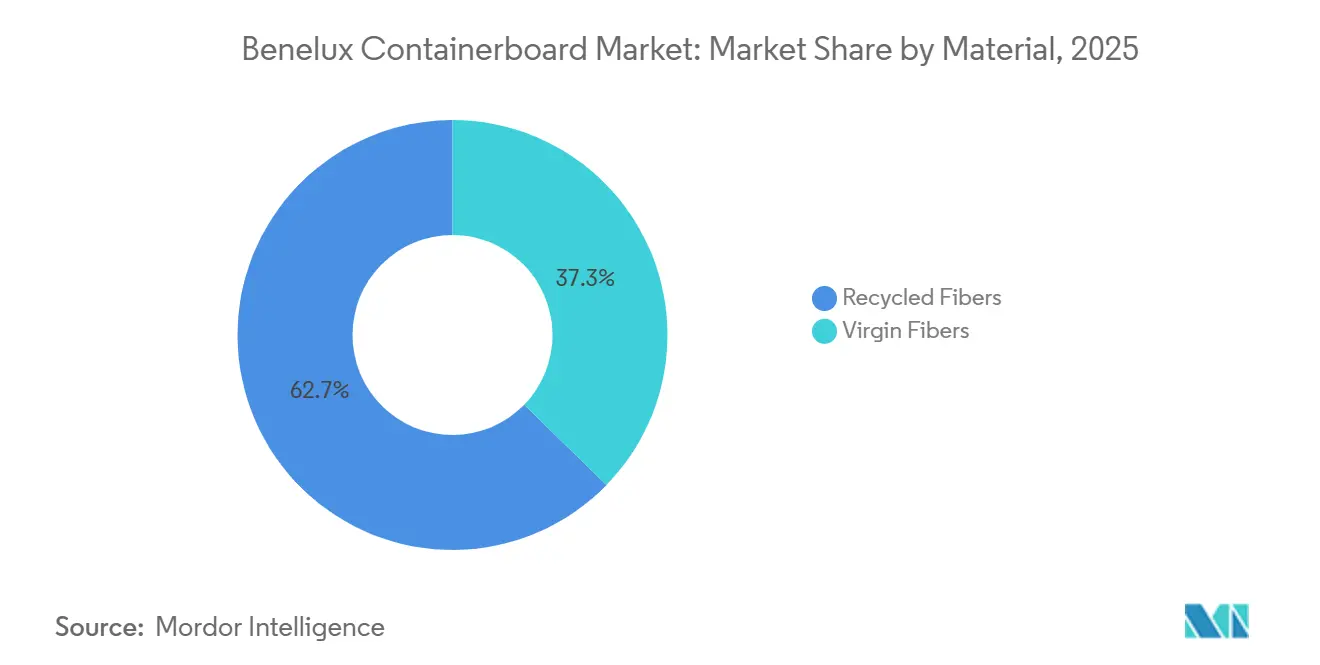

- By material, recycled fibers captured 62.71% of the Benelux containerboard market share in 2025.

- By product type, the Benelux containerboard market size for the kraftliners segment is forecast to advance at a 3.12% CAGR through 2031.

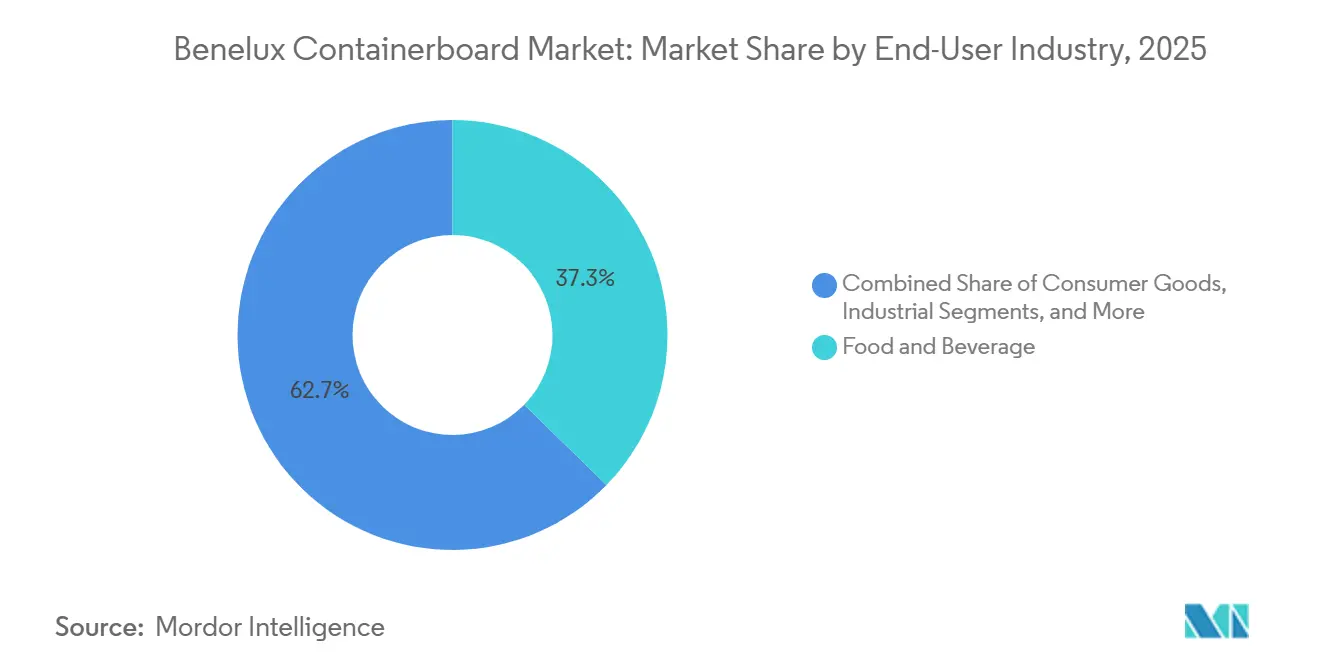

- By end-user industry, food and beverage captured 37.28% of the Benelux containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Benelux Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food Service And Grocery Fiber Substitution Under PPWR | +0.8% | EU-wide mandate, with strongest commercial effect in Belgium and the Netherlands | Short term (≤ 2 years) |

| Benelux E-Commerce Parcel Density Supporting Box Throughput | +0.7% | Strongest in the Netherlands and Belgium, with spillover to Luxembourg | Short term (≤ 2 years) |

| High Paper And Cardboard Recovery Rates Supporting Recycled Fiber Supply | +0.5% | Belgium and the Netherlands, with wider benefit across Western Europe | Medium term (2-4 years) |

| Port-Centric Export Flows Supporting Heavy-Duty Containerboard Demand | +0.4% | Rotterdam and Antwerp-Bruges industrial and export corridors | Medium term (2-4 years) |

| PFAS-Free Barrier Redesign Favoring Fiber-Based Transit Packs | +0.3% | EU-wide, especially food service and grocery applications | Short term (≤ 2 years) |

| Lightweight Box Engineering Increasing High-Performance Fluting Intensity | +0.2% | Mainly the Netherlands and Belgium logistics corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food Service And Grocery Fiber Substitution Under PPWR

The PPWR Article 5 PFAS restriction, effective August 12, 2026, is pushing food service operators and grocery supply chains to move away from fluoropolymer-coated plastic and laminated paper formats toward fiber-based transit packaging more quickly. The same regulation also prohibits selected single-use plastic packaging for fresh produce and hospitality food service from January 1, 2030, while cardboard boxes are excluded from the 40% transport packaging reuse target, which gives corrugated formats a clearer regulatory position than reusable plastic crate alternatives. Sabert launched its PFAS-free PulpUltra range across Europe in January 2026 and directly linked the move to PPWR Article 5 compliance, showing that the substitution cycle is already underway before the enforcement date. Belgium and the Netherlands are major hubs for food processing, retail, and hospitality distribution, so the pipeline for packaging reformulation is deeper here than in many other EU markets. That shifts food transit packs from a secondary source of board demand into an active redesign area for the Benelux containerboard market over the next few years. It also means demand is likely to be pulled forward into 2026-2028 instead of building gradually across the whole forecast period.

Benelux E-Commerce Parcel Density Supporting Box Throughput

The Netherlands’ online trade surpassed EUR 36 billion (USD 40.6 billion) in 2024, and that scale continues to support high parcel throughput across the Benelux containerboard market. The Randstad corridor accounted for 62% of Dutch corrugated demand, which gives local box plants shorter runs, faster changeovers, and better utilization than many comparable Western European clusters. Secondary e-commerce packaging volumes for paper-based void fill and kraft paper materials in Western Europe are growing at 3.9% annually, which directly supports testliner and fluting demand at the mill level. VPK Group’s new corrugator at Erembodegem lifted board capacity from 100 million m2 to 170 million m2, which shows that established regional players are still investing behind e-commerce demand. The Netherlands also ranked first in the EU for circular material use at 32.7%, which encourages online retailers to specify recycled-content packaging and raises the quality bar for recovered fiber supply. Together, those conditions keep parcel activity a near-term volume support for the Benelux containerboard market even as box design becomes more material efficient.

High Paper And Cardboard Recovery Rates Supporting Recycled Fiber Supply

Belgium’s industrial paper and cardboard recycling rate reached 107.7% in 2024, which signaled a structurally net-positive recovered fiber pool relative to declared packaging volumes placed on the market.[1]Valipac, “Activity Report 2024,” Valipac, valipac.be The Netherlands also reported 88% overall packaging recycling in 2023, well above its national legal target of 72% and the EU benchmark of 65%. This matters because European paper for recycling net exports outside the continent fell by 26.2% in 2024, reducing the amount of quality OCC leaving Europe and improving feedstock availability for regional producers. In Belgium, Valipac and Fost Plus have been operating under a more aligned management structure since September 2024, which has strengthened coordination around PPWR-related recycled content requirements.[2]European Paper Recycling Council, “Monitoring Report 2024: European Declaration on Paper Recycling 2021-2030,” CEPI, cepi.orgEuropean Paper Recycling Council, “Monitoring Report 2024: European Declaration on Paper Recycling 2021-2030,” CEPI, cepi.org That institutional setup gives the Benelux containerboard market a better recycling backbone than many neighboring markets. It also improves the quality profile of OCC streams because commercial waste in Belgium and the Netherlands contains a high share of premium corrugated and kraft packaging.

Port-Centric Export Flows Supporting Heavy-Duty Containerboard Demand

The Port of Antwerp-Bruges recorded a 48% surge in paper and pulp cargo in Q1 2025, while container throughput rose 4.5% to 3.44 million TEUs, which temporarily lifted Antwerp ahead of Rotterdam on container volumes.[3]Port of Antwerp-Bruges, “Port of Antwerp-Bruges Factsheet Throughput Figures Q1 2025,” Port of Antwerp-Bruges, newsroom.portofantwerpbruges.com That trade mix supports heavier export packaging needs for chemicals, agricultural machinery, and precision goods that move through the Antwerp-Rotterdam-Rhine-Ruhr Area. The ports of Rotterdam and Antwerp-Bruges together generated EUR 50 billion (USD 56.4 billion) in annual added value and supported 350,000 direct jobs, providing the Benelux containerboard market with a durable industrial demand base. Export logistics also favor corrugated pallet boxes in some time-sensitive flows because they avoid delays associated with ISPM-15 requirements for wood fumigation. Rotterdam and Antwerp also serve as entry points for containerboard-grade pulp from Scandinavia and South America, strengthening the region’s role as both an input hub and an export corridor for the wider European trade. These conditions keep heavy-duty transport packaging an important support for the Benelux containerboard market even when consumer-facing demand softens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy And Recovered Paper Cost Volatility | -0.4% | Highest near-term exposure in the Netherlands and Belgium, with wider EU spillover | Short term (≤ 2 years) |

| European Containerboard Overcapacity And Margin Pressure | -0.3% | EU-wide, especially Western Europe and Benelux-positioned producers | Medium term (2-4 years) |

| PPWR Empty-Space Caps Lowering Board Intensity Per Shipment | -0.2% | EU-wide, strongest in Dutch and Belgian parcel flows | Long term (≥ 4 years) |

| Reusable Crate Lock-In In Fresh Produce Logistics | -0.1% | Belgium and the Netherlands, with spillover to Luxembourg trade | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy And Recovered Paper Cost Volatility

Recycled testliner, the dominant grade by volume in the Benelux containerboard market, carries around 68% dependence on natural gas as a primary energy source, which leaves it highly exposed to TTF gas movements. In 2026, the Dutch TTF benchmark rose by more than 60% from the low EUR 30 (USD 33.8) per MWh to above EUR 68 (USD 76.7) per MWh, and each EUR 10 (USD 11.2) per MWh increase can raise testliner production costs by up to EUR 20 (USD 22.5) per tonne. OCC prices in the Rotterdam area also fluctuated between EUR 80 (USD 90.2) and EUR 140 (USD 158.01) per tonne during 2024 and 2025, making raw material planning difficult for non-integrated converters. That double cost pressure limits spending on coating reformulation, recyclability certification, and other upgrades that are becoming more important under PPWR. It also raises the pressure on mid-tier independents that do not have the same hedging and multi-mill balancing options as integrated groups. As a result, the Benelux containerboard market faces a cost-side squeeze that can slow investment even when end-market demand remains stable.

European Containerboard Overcapacity And Margin Pressure

Europe has been dealing with structural containerboard overcapacity since 2022, and new recycled-grade additions through 2024 and 2025, including Norske Skog’s 550,000 tonnes per year Golbey mill and Mondi’s 420,000 tonnes per year Duino mill, added more supply into an already heavy market. Western European operating ratios fell below 80% in the summer of 2025 and then recovered to an 88% three-month moving average by November 2025, which was better than midyear but still below the level usually linked to lasting pricing power. Mondi’s chief executive said in 2026 that more recycled containerboard closures were still needed, which showed that voluntary rationalization had not yet corrected the supply imbalance. For producers serving the Benelux containerboard market, lower-priced imports moving through Rotterdam and Antwerp add to the pressure on commodity testliner lines. That is why many producers are shifting their portfolios toward Kraftliner, moisture-resistant semi-chemical fluting, and printable white-top testliner. The strategy improves differentiation, but it also shows that volume growth alone is not enough to restore margins in the Benelux containerboard market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Virgin Fibers Gain Ground As Energy Costs Reshape Grade Economics

Recycled fibers held 62.71% of the Benelux containerboard market share in 2025, while the Benelux containerboard market size for virgin fibers is projected to expand at 3.04% CAGR between 2026 and 2031. That split shows a market where recycled grades still dominate, but cost inflation is changing how buyers compare performance and price. When gas prices lift recycled testliner conversion costs, procurement teams are more willing to shift selected volumes toward virgin-fiber grades for moisture-sensitive and export-critical uses. Stora Enso stated in its Q2 2025 presentation that kraftliner pricing held firmer than recycled grades during periods of operating-rate pressure, which fits the grade pattern seen across the Benelux containerboard market.

Belgium’s 107.7% industrial paper and cardboard recycling rate in 2024 keeps domestic OCC supply structurally strong and explains why recycled fibers still hold the leading position. Even so, secondary fiber still faces performance limitations in heavy export applications, such as chemical transit packaging, agricultural machinery, and precision goods moving through the ARRRA corridor. That leaves virgin-fiber grades with a durable role where board consistency and moisture resistance cannot vary. Investments in better fiber cleaning and stock preparation should narrow the performance gap over time, but the premium for virgin specifications is likely to remain in the Benelux containerboard market through 2031.[4]Stora Enso, “Financial Results Q2 2025,” Stora Enso, storaenso.com

By Product Type: Testliners Lead While Kraftliners Capture The Performance Premium

Testliners accounted for 41.13% of the Benelux containerboard market size in 2025, while kraftliners are set to grow at a 3.12% CAGR through 2031. Testliners remain the largest product type because the region has strong OCC recovery, a wide installed base of recycled-grade production, and a converter network geared to FMCG and retail flows. Kraftliners are growing faster because export-facing sectors need stronger and more moisture-resistant board. Dutch horticulture and fresh produce exports exceeded EUR 36 billion (USD 40.6 billion) annually, supporting ongoing demand for high-performance facings and semi-chemical media in humidity-sensitive logistics.

Fluting also plays a strategically important role in the Benelux containerboard market, as lightweight double-wall designs in e-commerce hubs require greater compression strength without adding unnecessary weight. Automated parcel handling is raising the value of fluting grades that perform more consistently under fast sortation conditions. Billerud completed a headbox rebuild at its Gruvön mill in April 2026 to improve fiber orientation and sheet uniformity in its primary-fiber fluting grade, and that type of upgrade fits the performance demands of Benelux export and produce buyers. Across product types, the mix is gradually moving toward higher-grammage, performance-enhanced grades, which supports value growth in the Benelux containerboard market even as total tonnage rises at a measured pace.

By End-User Industry: Consumer Goods Lead Growth While Food And Beverage Hold The Volume Base

Food and beverage captured 37.28% of the Benelux containerboard market size in 2025, while the Benelux containerboard market size for consumer goods is projected to expand at 3.18% CAGR between 2026 and 2031. Food and beverage remains the largest end-user because the region combines food processing, grocery distribution, and mature retail networks that generate steady box demand. Consumer goods are growing faster because e-commerce shipment volumes keep rising and retailers are replacing more plastic secondary packaging with fiber-based formats. Paper-based void fill volumes in Western Europe are increasing by 3.9% annually, supporting increased demand for testliner and fluting used in online retail packaging.

Industrial users such as chemicals, machinery, and electronics moving through Antwerp-Bruges provide a stable base for heavier-duty grades within the Benelux containerboard market. Other end-user industries include pharmaceuticals and agricultural packaging, where humidity control and compression strength matter more than low cost alone. This mix maintains a broad demand floor across the Benelux containerboard industry, even as discretionary retail trends soften. It also means that incremental growth in the Benelux containerboard industry is shifting toward higher-value grades rather than commodity board alone.

Geography Analysis

The Netherlands is the largest demand center in the Benelux containerboard market because it combines the region’s biggest e-commerce flow base with its most concentrated logistics network. Online trade in the country surpassed EUR 36 billion (USD 40.6 billion) in 2024, which keeps parcel-related packaging demand structurally high. The Randstad corridor, including Amsterdam, Rotterdam, Utrecht, and The Hague, accounted for 62% of national corrugated demand, creating a strong local pull for recycled-grade board. The Port of Rotterdam handled 103.7 million tonnes of cargo in Q1 2025 and posted 2.2% year-on-year growth in container volumes, which reinforced its role as Northern Europe’s main trade gateway. The Netherlands also ranked first in the EU for circular material use at 32.7% and reported 88% packaging recycling in 2023, but its high natural gas exposure means Dutch-linked supply remains among the most sensitive in Europe to TTF spikes.

Belgium serves as the main supply-side anchor in the Benelux containerboard market, combining strong mill capacity with unusually high fiber recovery. The Port of Antwerp-Bruges posted a 48% increase in paper and pulp cargo in Q1 2025 and 4.5% growth in container throughput, which strengthened its role as a hub for export-oriented corrugated flows. That position makes Antwerp a key entry point for pulp and a major origination point for heavy-duty packaging demand tied to chemicals and industrial goods. Belgium’s industrial paper and cardboard recycling rate reached 107.7% in 2024, and its total packaging recycling rate stood at 80% in 2022, which gives local mills a better domestic OCC base than many regional peers. VPK Group’s Oudegem site, with 500,000 tonnes of recycled paper capacity across 3 paper machines, shows how central Belgium is to supply within the Benelux containerboard market.

Luxembourg remains the smallest contributor to the Benelux containerboard market demand by volume, but its trade intensity gives it a larger role in heavy-duty industrial flows than its size suggests. The country recorded a total packaging recycling rate of 76.96% in 2022, which stayed above the EU’s 65% target. Most of its demand is served through Belgian and German production systems, with Antwerp acting as a practical supply pipeline for many flows. Taken together, the 3 Benelux countries give the Benelux containerboard market a resilient geographic structure built on strong recycling systems, dense logistics infrastructure, and stable e-commerce activity, although Dutch gas exposure remains the clearest regional cost risk.

Competitive Landscape

The Benelux containerboard market has a moderately concentrated upstream structure, in which large, integrated pan-European producers supply much of the regional demand, while regional independents and specialist converters compete on service speed, local relationships, and format flexibility. Competition is still intense because European overcapacity keeps pressure on testliner pricing and limits producers' ability to fully pass through cost shocks. FEFCO’s 2024 corrugated packaging recyclability guidelines are becoming a practical compliance framework for grade development, benefiting larger producers that can respond more quickly to design-for-recyclability workstreams. Producers with Benelux mill footprints or short-haul access to Randstad and Antwerp-area customers also retain a meaningful service advantage that imported commodity boards cannot easily match. Stora Enso’s Langerbrugge presence in Belgium remains a visible example of how direct regional assets help large groups stay close to demand in the Benelux containerboard market.

White-space opportunities are strongest in barrier-coated containerboard that combines structural performance with PFAS-free moisture and grease resistance for food service and produce packaging. Smurfit Westrock said in its Q1 2026 update that EMEA demand was improving, customer wins were increasing, and AI-enabled packaging design capabilities were being deployed across its European customer network, which shows that digital tools are becoming part of commercial differentiation. The company also launched updated Better Planet sustainability targets in May 2026 and introduced a glueline-free packaging prototype, demonstrating how environmental compliance and design performance are converging in the Benelux containerboard market. At the same time, converted newsprint mills entering recycled testliner supply with lower-cost energy setups are adding to the margin pressure that established producers already face.

M&A remains an active strategic tool because scale and network reach matter more when markets are oversupplied. International Paper agreed in April 2026 to acquire NORPAC for USD 360 million, expanding its lightweight, high-performance recycled containerboard capabilities following the DS Smith integration. VPK Group also increased its stake in Ribble Packaging to 50% in January 2026, further strengthening its position in e-commerce fanfold and expanding its links to faster-growing packaging formats. These moves show that the Benelux containerboard market is rewarding scale, adjacency to high-growth packaging formats, and tighter customer integration, while smaller players are being pushed toward service-led niches.

Benelux Containerboard Industry Leaders

Smurfit Westrock plc

VPK Group NV

Stora Enso Oyj

International Paper Company

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smurfit Westrock launched its updated Better Planet sustainability targets, reporting 2025 achievements in carbon emissions reduction across its European recycled paper mills and integrating AI-enabled packaging design capabilities into its pan-European customer innovation network.

- April 2026: Smurfit Westrock reported Q1 2026 results noting EMEA containerboard price increases in March and April 2026 in response to higher energy costs, with further corrugated price rises expected in H2 2026. The company also opened formal consultations on the closure of 4 converting facilities in the United Kingdom and the Netherlands as part of its asset optimization program.

- April 2026: International Paper entered an agreement to acquire North Pacific Paper Company, NORPAC, from One Rock Capital Partners for USD 360 million, adding approximately 1 million tonnes of annual containerboard capacity and expanding the company’s lightweight, high-performance recycled containerboard capabilities following its integration of DS Smith.

- February 2026: Smurfit Westrock announced a decarbonization initiative for its European recycled paper mills in partnership with SLR and RIZM, deploying digital twin modeling and AI-driven energy optimization to develop site-level transition roadmaps addressing EU Emissions Trading System carbon cost exposure.

Benelux Containerboard Market Report Scope

The Benelux Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The increasing demand for sustainable, lightweight, and durable packaging solutions drives the market.

The Benelux Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the expected size of the Benelux containerboard market by 2031?

The Benelux containerboard market is forecast to reach USD 2.95 billion by 2031, rising from USD 2.57 billion in 2026 at a 2.79% CAGR over 2026-2031.

Which material category is growing fastest in Benelux containerboard?

Virgin fibers are the fastest-growing material segment, with a projected 3.04% CAGR from 2026 to 2031, even though recycled fibers held the largest 62.71% share in 2025.

Why does food and beverage remain the largest demand base for containerboard in Benelux?

Food and beverage held 37.28% of demand in 2025 because the region has strong food processing, grocery distribution, and retail networks that generate stable packaging volumes.

How is PPWR affecting containerboard demand in Benelux?

PPWR is accelerating the move from plastic and laminated formats toward fiber-based transit packaging, especially in food service and grocery applications, while cardboard's exclusion from the transport reuse target supports corrugated demand.

Which country is most important to regional demand and logistics flows?

The Netherlands leads on e-commerce and parcel density, while Belgium is the key supply and recycling anchor. Together they shape most of the region's demand and fiber flow patterns.

What is limiting faster growth across Benelux containerboard?

Energy price volatility, OCC cost swings, and continued European overcapacity are the main constraints, even though e-commerce growth and high recycling rates continue to support steady underlying demand.

Page last updated on: