South Africa Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

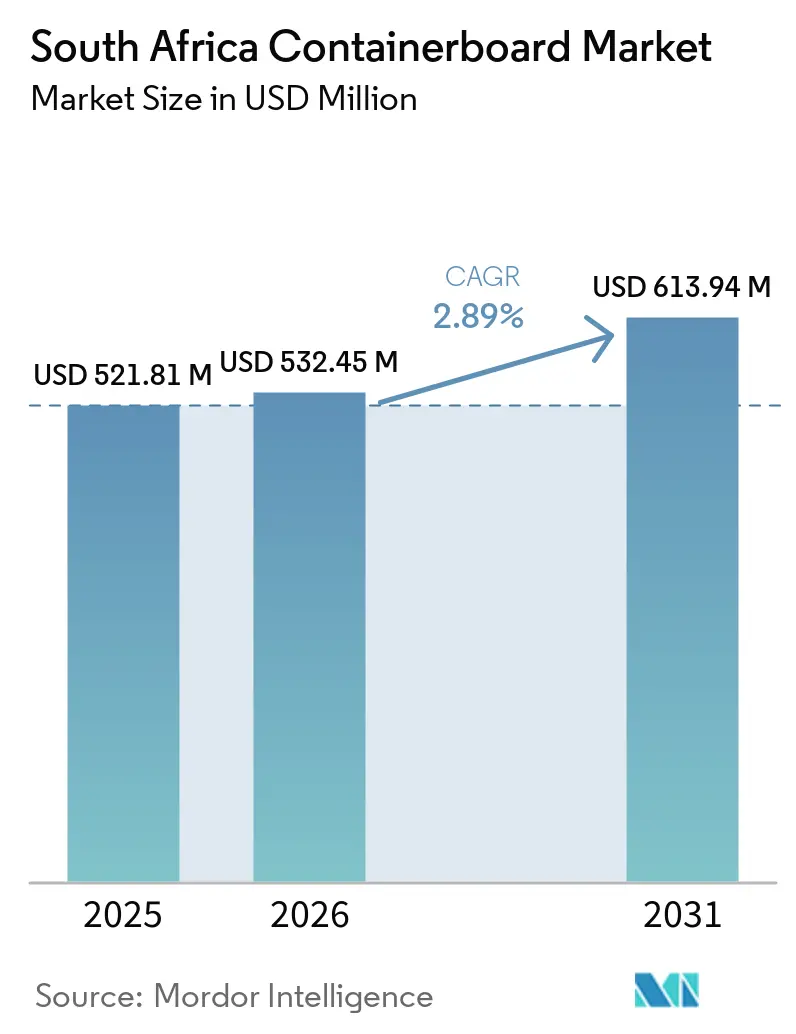

| Base Year Market Size (2025) | USD 521.81 Million |

| Market Size (2026) | USD 532.45 Million |

| Market Size (2031) | USD 613.94 Million |

| Growth Rate (2026 - 2031) | 2.89% CAGR |

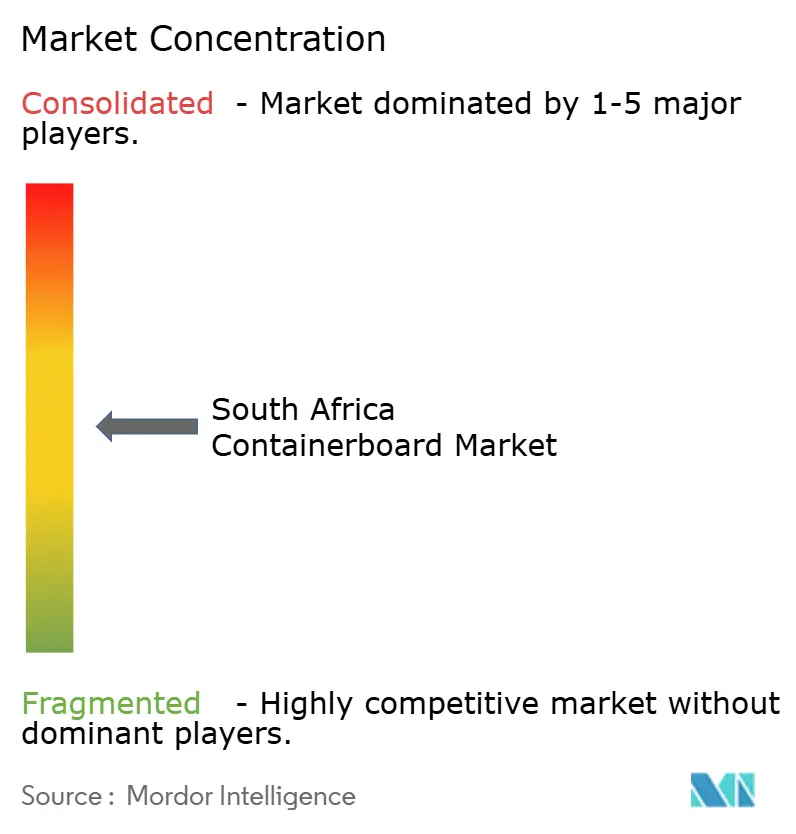

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Containerboard Market Analysis by Mordor Intelligence

The South Africa containerboard market size was valued at USD 521.81 million in 2025 and estimated to grow from USD 532.45 million in 2026 to reach USD 613.94 million by 2031, at a CAGR of 2.89% during the forecast period (2026-2031). The South Africa containerboard market is being supported by steady demand from agricultural export packaging, where fruit shipments continue to require a reliable carton supply through each export season. The outlook remains restrained because weaker household spending and softer industrial activity continue to limit domestic corrugated demand outside export-linked uses. Import pressure has become a structural issue, and the early 2026 discontinuation of production at Mpact's Springs cartonboard mill showed how exposed standard grades are when offshore material lands below local production costs. At the same time, mill upgrades and product engineering are shifting part of the South Africa containerboard market toward higher-performance grades used in cold-chain and moisture-sensitive applications. This leaves the South Africa containerboard market with a narrow but visible opportunity set centered on export-aligned capacity, recyclable formats, and differentiated board grades rather than volume growth in commodity products.

Key Report Takeaways

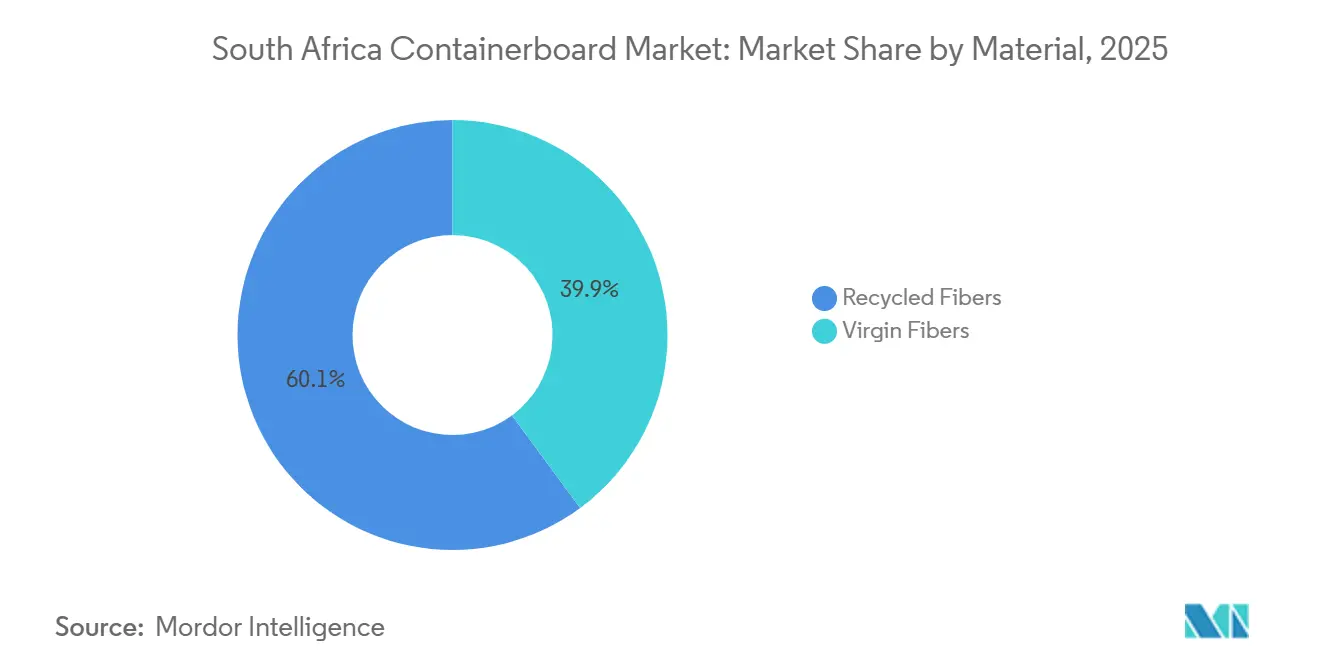

- By material, recycled fibers captured 60.13% of the South Africa containerboard market share in 2025.

- By product type, the South Africa containerboard market size for the kraftliners segment is forecast to advance at a 3.27% CAGR through 2031.

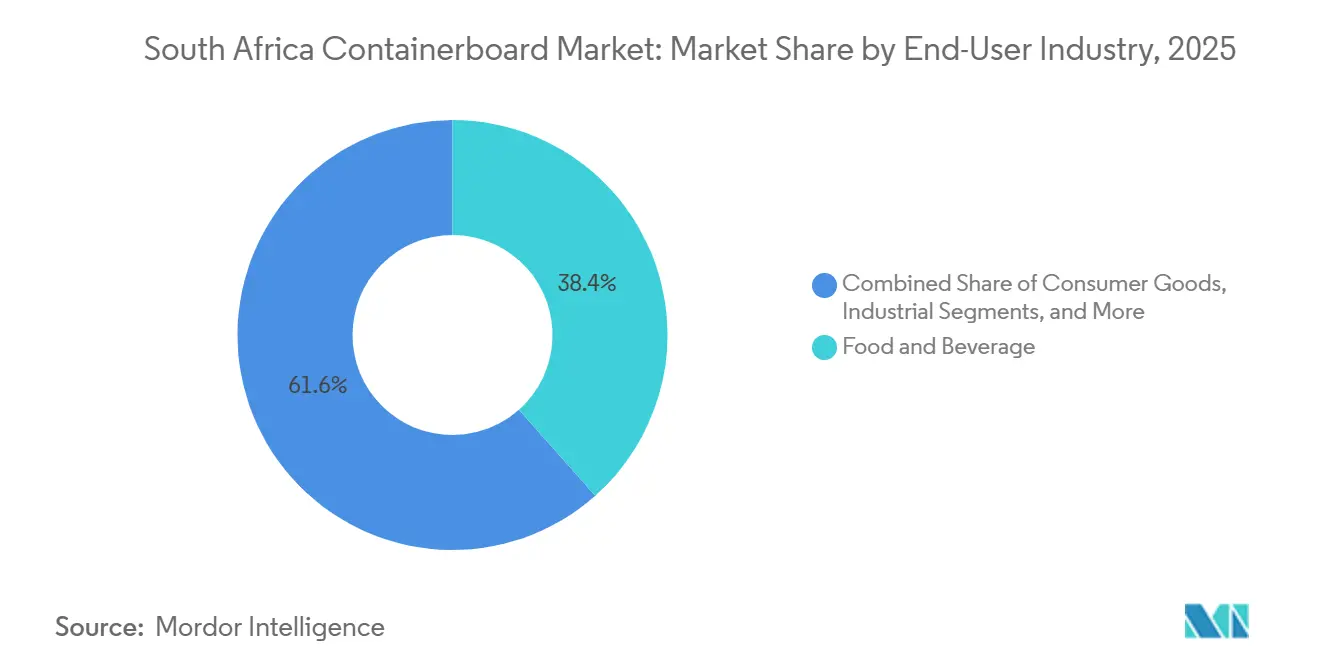

- By end-user industry, food and beverage captured 38.44% of the South Africa containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Fresh Produce Export Carton Demand | +1.1% | Western Cape, Northern Cape, Eastern Cape, spill-over to KwaZulu-Natal port corridors | Short term (≤ 2 years) |

| Shift From Plastic Packaging to Recyclable Paper Formats | +0.7% | National, with strongest traction in Gauteng and Western Cape FMCG clusters | Medium term (2-4 years) |

| Expanding Food Delivery and Convenience Packaging Demand | +0.4% | Gauteng, Cape Town, Durban metropolitan corridors | Short term (≤ 2 years) |

| Strong Recovered-Fiber Collection Base | +0.3% | National, concentrated in Gauteng and KwaZulu-Natal industrial zones | Long term (≥ 4 years) |

| Mill Upgrades Supporting Higher-Performance Export Grades | +0.2% | Mpumalanga (Mkhondo), KwaZulu-Natal (Felixton), Gauteng (Rosslyn) | Medium term (2-4 years) |

| Moisture-Resistant Box Demand From Cold-Chain Logistics | +0.2% | Western Cape packhouses, reefer export corridors to EU and Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Fresh Produce Export Carton Demand

Export-oriented fruit packaging remained the clearest demand support for the South Africa containerboard market in 2025 and 2026, as agricultural exports reached a record USD 15.1 billion in 2025. Fruits and nuts accounted for 26% of total agricultural export value in Q4 2025, keeping carton demand firm across major packhouse belts even as local industrial demand remained soft. This demand is especially supportive for producers supplying boxes that can handle cooling, stacking, and long shipping cycles in export channels. The packaging requirement is not only for volume, but also for board consistency, moisture control, and compression strength through cold-chain movement. That makes agricultural exports a steadier planning base for the South Africa containerboard market than domestic consumer packaging.[1]Mpact Group Limited, “Annual Results FY2025: Mpact Delivers Revenue Growth and Higher NAV, EBITDA Resilient in Challenging Conditions,” Mpact, mpact.co.za It also helps explain why capacity tied to export grades is attracting more attention than standard domestic commodity supply.

Shift From Plastic Packaging to Recyclable Paper Formats

The move from plastic packaging to paper-based formats is being reinforced by South Africa's EPR framework, which has been in force under NEMWA since May 2021 and remains a live compliance issue in 2026.[2]PRO Alliance, “Extended Producer Responsibility (EPR),” PRO Alliance, proalliance.org.za This is pushing brand owners to review transit and secondary packaging choices with a stronger focus on recyclability and end-of-life accountability. South Africa's paper recycling rate reached 63.3% in 2025, up from 60% in 2024, which strengthened the circular case for containerboard formats. That improvement matters because procurement teams increasingly need packaging materials that fit both internal sustainability reporting and external compliance expectations. In the South Africa containerboard market, the result is a broader-format opportunity in food service, e-commerce, and retail transit packaging, where paper can replace harder-to-recycle plastic formats. This shift is gradual rather than abrupt, but it is giving domestic mills and converters a structural demand tailwind that is tied to regulation as much as branding.[3]South African Institute of Chartered Recyclers Association, “EPR Regulation,” SAICRA, saicra.co.za

Expanding Food Delivery and Convenience Packaging Demand

Food delivery and convenience retail are driving recurring corrugated demand in large urban corridors, even though this part of the South African containerboard market is smaller than the agricultural packaging market. Pick'n Pay reported 60% year-on-year growth in on-demand grocery delivery for the fiscal year ended March 2025, showing that digital ordering is pulling more packaging through local fulfillment networks. The company also reported 40% growth in on-demand grocery sales in H1 FY2026 following its app relaunch, suggesting continued momentum in 2026. Uber Eats reported a ZAR 17 billion (USD 0.95 billion) economic impact in South Africa, reflecting the scale of food delivery activity that feeds disposable corrugated demand in metropolitan areas. These use cases favor packaging with reliable edge strength and efficient conversion rather than the heavier board structures used in export produce. Over time, that creates a useful outlet for domestic producers seeking demand exposure beyond agriculture without relying solely on traditional industrial customers.

Strong Recovered-Fiber Collection Base

The recovered-fiber base remains a meaningful cost support for the South Africa containerboard market because it lowers dependence on virgin input in standard grades. Mpact's recycling operations collected 639 million kilograms of recyclable materials in 2025, up from 588 million kilograms in 2024, which shows the scale of the domestic collection system feeding paper mills. The national paper recycling rate also improved to 63.3% in 2025, which supports the supply base for recycled testliner and fluting. This collection strength matters most in price-sensitive grades where domestic producers need an input-cost advantage to offset freight and currency swings tied to imported board. It also supports EPR-linked procurement because recycled content and traceability are easier to demonstrate within domestic collection loops. Even so, fiber quality remains uneven across waste streams, which limits how far recycled furnish can move into the highest-performance export applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pressure From Low-Priced Containerboard Imports | -1.3% | National, most acute in Gauteng industrial and consumer goods packaging sectors | Short term (≤ 2 years) |

| Weak Domestic Consumer and Industrial Demand | -0.7% | National, concentrated in Gauteng manufacturing belt and KwaZulu-Natal FMCG | Medium term (2-4 years) |

| Port and Inland Logistics Disruption for Fruit Exports | -0.3% | Cape Town, Gqeberha, Durban port corridors and associated rail links | Short term (≤ 2 years) |

| Utility and Water Reliability Constraints | -0.4% | Gauteng (Ekurhuleni), secondary impact in Mpumalanga and KwaZulu-Natal | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pressure From Low-Priced Containerboard Imports

Low-priced imports remain the sharpest restraint on the South Africa containerboard market because they target the very grades where domestic mills have the least room to protect margins. Mpact disclosed in early 2026 that its largest Springs customer shifted to imported material priced around 20% below domestic production costs, prompting the discontinuation process at the mill. World Bank WITS trade data show that Germany, China, and India historically accounted for the largest shares of South Africa's corrugated paper import value, which explains the origin of much of this pricing pressure. This is not just a temporary pricing cycle, because offshore overcapacity and stronger manufacturing scale keep pressure on standard liner and fluting grades.[4]World Bank, “South Africa: Cartons, Boxes and Cases, of Corrugated Paper Imports by Country, 2023,” WITS, wits.worldbank.org The South Africa containerboard market, therefore, becomes harder to serve profitably in commodity segments unless mills have either cost advantages or tighter customer integration. That is why local investment is moving away from undifferentiated supply and toward grades that are harder to replace through simple import arbitrage.

Weak Domestic Consumer and Industrial Demand

Domestic consumer and industrial demand continues to limit broader volume recovery across the South Africa containerboard market, especially outside export-linked packaging. Mpact's FY2025 results referred to softer demand in certain industrial and consumer-related segments, even as agricultural packaging stayed stronger. Sappi also reported that containerboard net selling prices in Q1 FY2026 were 3% lower year on year, indicating weak pricing conditions in the current market. This means converters tied to domestic FMCG, industrial goods, and light manufacturing remain more exposed to margin pressure than those serving export agriculture. The gap between resilient export demand and softer home-market demand is now one of the defining internal features of the South Africa containerboard market. It also strengthens the case for mills and converters to shift grade mix toward packaging that can command performance-based pricing rather than compete only on volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Leadership, With Virgin Fiber Gaining Quality-Led Demand

Recycled fibers accounted for 60.13% of revenue in 2025, keeping this segment at the center of the South African containerboard market. The segment's lead rests on the country's established paper recovery network and the ability of domestic mills to feed recycled testliner and fluting into local converting demand. South Africa's paper recycling rate reached 63.3% in 2025, reinforcing the raw material base for recycled grades. This part of the South Africa containerboard industry benefits most in cost-sensitive applications where converters prioritize dependable supply and manageable input costs over the highest strength profile.

Virgin fibers are projected to grow at a 3.18% CAGR through 2031, the fastest pace within the material split. That growth reflects tighter export packaging specifications, where moisture resistance, compression strength, and more consistent performance matter more than the lowest delivered cost. Mpact's NSSC expansion at Mkhondo was designed to raise pulping capacity from 225 bdmt/d to 365 bdmt/d, directly supporting higher-performance semi-chemical grades used in export fruit cartons. This quality push does not displace recycled fiber leadership, but it does mean the South Africa containerboard market size for virgin fiber will continue to expand faster, where exporters require stronger and more stable board.

By Product Type: Testliners Hold Scale, While Kraftliners Move Up With Export Demand

Testliners accounted for 41.26% of revenue in 2025, making them the leading product type in the South African containerboard market. Their large installed base reflects the dominance of recycled-content liner production and the price sensitivity of standard corrugated applications. This segment serves a wide range of domestic, FMCG, and industrial packaging demand, where converters need functional grades at competitive prices. The strength of testliners in 2025 also meant they accounted for a large share of the South African containerboard market, tied to local converting activity.

Kraftliners are projected to grow at a 3.27% CAGR through 2031, making them the fastest-growing product category. That growth is tied to export cartons that must tolerate reefer condensation, longer ocean transit, and tighter structural requirements in fruit supply chains. Mpact's Freshflow system showed 30% faster forced-air cooling, 13.8% carton weight reduction, and a 14.3% increase in refrigerated container payload while maintaining performance. That result matters because it shifts part of the South Africa containerboard industry away from price-only competition and toward packaging systems that create value across the export chain.

By End-User Industry: Food and Beverage Leads, While Consumer Goods Builds Faster Growth

Food and beverage accounted for 38.44% of revenue in 2025, making it the largest segment in the South Africa containerboard market. The segment remained resilient, with agricultural exports reaching a record USD 15.1 billion in 2025, with fruits and nuts accounting for a meaningful share of export value. That export base supports regular carton procurement across major fruit-growing regions and limits the effect of weaker local consumption on this segment. In 2025, food and beverage therefore held 38.44% of the South Africa containerboard market share because export-linked packaging demand remained structurally stronger than most domestic industrial uses.

Consumer goods are projected to grow at a 3.34% CAGR through 2031, making this the fastest-growing end-user segment. The demand base is expanding through e-commerce, convenience retail, and food delivery packaging in urban markets. Pick'n Pay's digital grocery performance in FY2025 and H1 FY2026 showed that repeat ordering and app-led fulfillment are creating incremental corrugated demand outside traditional retail channels. This gives the South Africa containerboard industry a second growth lane beside agriculture, even though standard industrial end uses remain under pressure.

Geography Analysis

The Western Cape export corridor carries some of the highest packaging performance requirements in the South Africa containerboard market. The region's demand is linked to fruit exports, where strong agricultural trade flows continued to support carton use through 2025 and into 2026. Producers serving this corridor need boards with stable compression strength, moisture resistance, and reliable converting quality for cold-chain movement. Port and inland logistics disruptions remain a live risk here because shipment timing affects the continuity of carton demand from packhouses to exporters. The result is that Western Cape-linked demand is less about pure volume and more about supplying the right grade at the right point in the export cycle.

Gauteng remains the country's main industrial packaging hub and a major demand center for recycled testliner and fluting in FMCG, warehousing, and light manufacturing. This also makes Gauteng the area most exposed to import substitution in standard grades. The Springs mill discontinuation in early 2026 showed how quickly offshore pricing can reshape local supply economics in this region. Utility and water reliability issues have also raised the operating risk for paper assets in Gauteng, which matters in a market where fixed costs are high and downtime is expensive. For that reason, Gauteng accounts for an outsized share of the South African containerboard market tied to commodity grades, but it also faces the highest exposure to pricing and infrastructure pressures.

KwaZulu-Natal plays a dual role in the South Africa containerboard market as both a port province and a secondary industrial packaging base. Its position supports regional converting demand while also linking domestic production to export flows and intra-African trade. World Bank WITS data show that Namibia, Zimbabwe, and Madagascar were the principal foreign markets for South Africa's corrugated paper and board exports, providing local mills with an outlet beyond the domestic market. That regional role matters because it gives producers an additional route for placing standard grades that face tougher competition at home.

Competitive Landscape

The South Africa containerboard market is moderately concentrated at the production level, with Mpact, Corruseal Group, and Neopak Holdings forming the core domestic supply base. At the same time, the competitive picture is looser downstream because converters and box makers remain numerous, and imported board continues to put pressure on commodity pricing. This means domestic leadership does not automatically translate into pricing power across the full South Africa containerboard market. Standard grades are the most exposed, while premium and specification-driven grades remain harder to replace. That split is shaping how leading companies allocate capital and defend margins.

Mpact has been one of the clearest examples of this strategy shift. Its ZAR 1.3 billion (USD 70 million) Mkhondo upgrade was substantially completed in 2025, and the project expanded NSSC pulping capacity from 225 bdmt/d to 365 bdmt/d to support higher-value paper packaging grades. Mpact also used its Freshflow cold-chain packaging platform to differentiate on system performance, not only on paper grade, in export fruit applications. Neopak took a different route in Q3 2025, commissioning ABB's Ability System 800xA at Rosslyn to improve process control, digital consistency, and mill reliability in recycled containerboard production. Corruseal also pursued operational improvements through the PM6 rebuild at Enstra, aimed at higher capacity and improved fluting and linerboard quality.

These moves show that competition in the South Africa containerboard market is increasingly centered on performance, reliability, and grade mix rather than pure tonnage. Import-led distributors can still offer material from Asian and European mills at lower prices in standard grades, which keeps the floor under price competition. Yet domestic producers maintain an edge in areas where customers need EPR alignment, verified recycled content, or cold-chain performance that directly links to export outcomes. Over the medium term, that suggests fewer viable positions in undifferentiated board and stronger defensibility in export-specification, circular-economy-compliant, and engineering-led packaging systems.

South Africa Containerboard Industry Leaders

Mpact Limited

Corruseal Group (Pty) Ltd

Neopak Holdings (Pty) Ltd

Mondi plc

Sappi Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mpact Limited reported FY2025 annual results disclosing containerboard sales volume growth of 8.8% supported by agricultural sector demand and benefits from capital investments. The ZAR 1.3 billion (USD 70 million) Mkhondo mill upgrade was substantially completed, with the new NSSC pulp digester and sodium lignosulphonate (SLS) plant commissioned. SLS output is targeted to make a meaningful earnings contribution from H2 2026.

- March 2026: Mpact's 2025 Sustainability Report disclosed that its recycling operations collected 639 million kilograms of recyclable materials in 2025, up from 588 million kilograms in 2024, diverting significant quantities of waste paper from landfill and reinforcing the recovered-fiber supply chain for its 3 domestic paper mills.

- March 2026: PAMSA confirmed that South Africa's paper recycling rate reached 63.3% in 2025, up from 60% in 2024, with approximately 1.2 million tonnes of paper and packaging diverted from landfill annually through mills, small recycling businesses, and the informal waste-picker network.

- February 2026: Mpact initiated a Section 189A Labour Relations Act consultation regarding discontinuation of operations at its Springs cartonboard mill after its largest customer switched to imports priced approximately 20% below domestic production costs, placing approximately 400 jobs at risk. Production was expected to cease in March 2026, eliminating South Africa's only domestic cartonboard producer and confirming the severity of global overcapacity and rand-strength import pressure on domestic manufacturing.

South Africa Containerboard Market Report Scope

The South Africa Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The South Africa Containerboard Market Report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the South Africa containerboard market size in 2026 and where is it heading by 2031?

The market stands at USD 532.45 million in 2026 and is forecast to reach USD 613.94 million by 2031, growing at a 2.89% CAGR over 2026-2031.

Which material segment leads demand in South Africa?

Recycled fiber led in 2025 with 60.13% of market value, supported by the country's established recovery and recycling base.

Which product category is growing fastest in containerboard use?

Kraftliners are projected to post the fastest growth at a 3.27% CAGR through 2031 because export fruit cartons need stronger moisture and compression performance.

Why does food and beverage remain the largest end-user base?

Food and beverage held 38.44% of revenue in 2025 because agricultural exports, especially fruit shipments, continue to support steady carton procurement.

What is the main risk facing local producers?

Low-priced imports are the most immediate threat, and the Springs mill discontinuation in early 2026 showed how sharply offshore pricing can disrupt domestic supply economics.

Where are the strongest growth opportunities emerging?

The clearest opportunities are in export-aligned agricultural packaging, cold-chain and moisture-resistant formats, and urban e-commerce and food delivery applications.

Page last updated on: