Pakistan Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

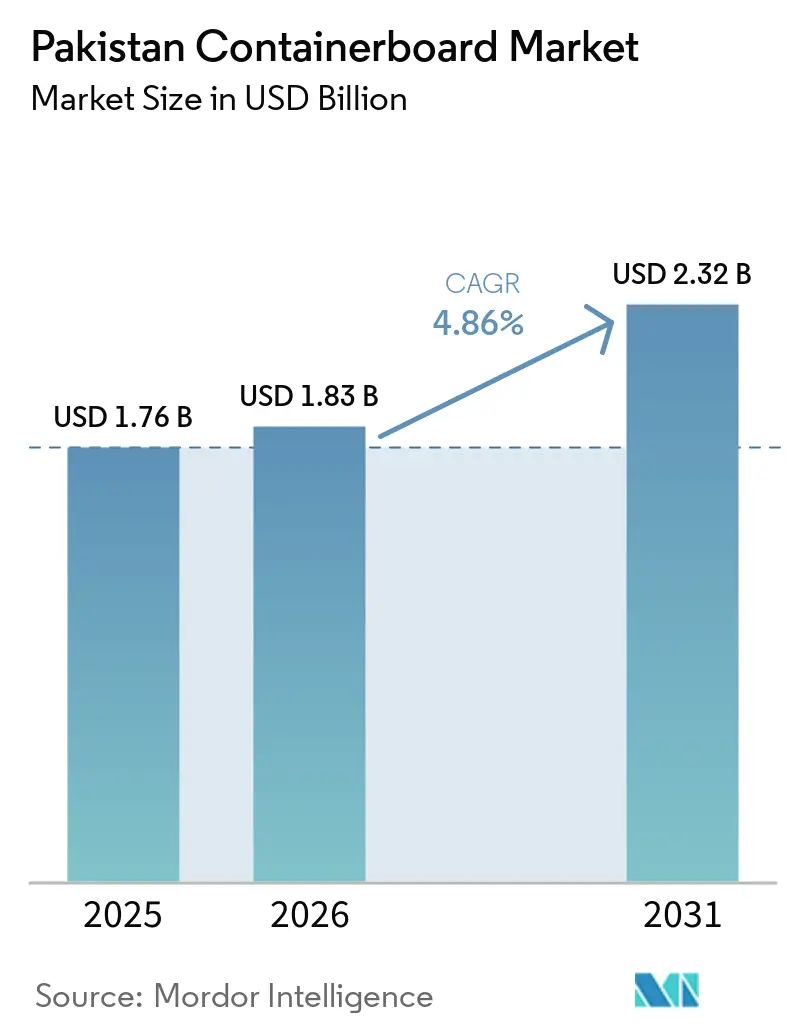

| Base Year Market Size (2025) | USD 1.76 Billion |

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.32 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

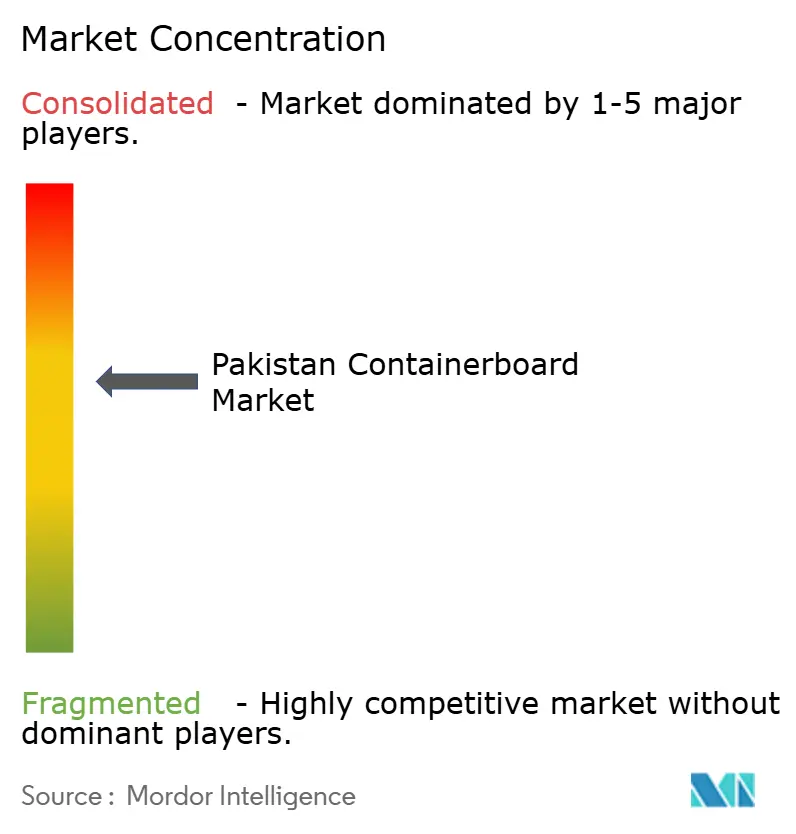

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Containerboard Market Analysis by Mordor Intelligence

The Pakistan Containerboard Market size is expected to increase from USD 1.76 billion in 2025 to USD 1.83 billion in 2026 and reach USD 2.32 billion by 2031, growing at a CAGR of 4.86% over 2026-2031.

Demand is supported by a larger packaged consumption base, steady growth in corrugated box conversion, and a feedstock mix that still leans heavily on recycled fiber. Pakistan’s paper production had grown faster than the current forecast range in the earlier period, but the slowdown reflects pressure from energy costs and raw material financing rather than any clear weakness in end demand. The Pakistan containerboard market is also being shaped by stricter quality expectations from export-oriented converters and multinational FMCG buyers that need more consistent board strength and print performance. That is creating room for premium grades to expand even while recycled material remains central to cost economics. Competitive advantage is likely to stay with producers that can secure fiber, manage power costs, and improve conversion efficiency with better integration and automation.

Key Report Takeaways

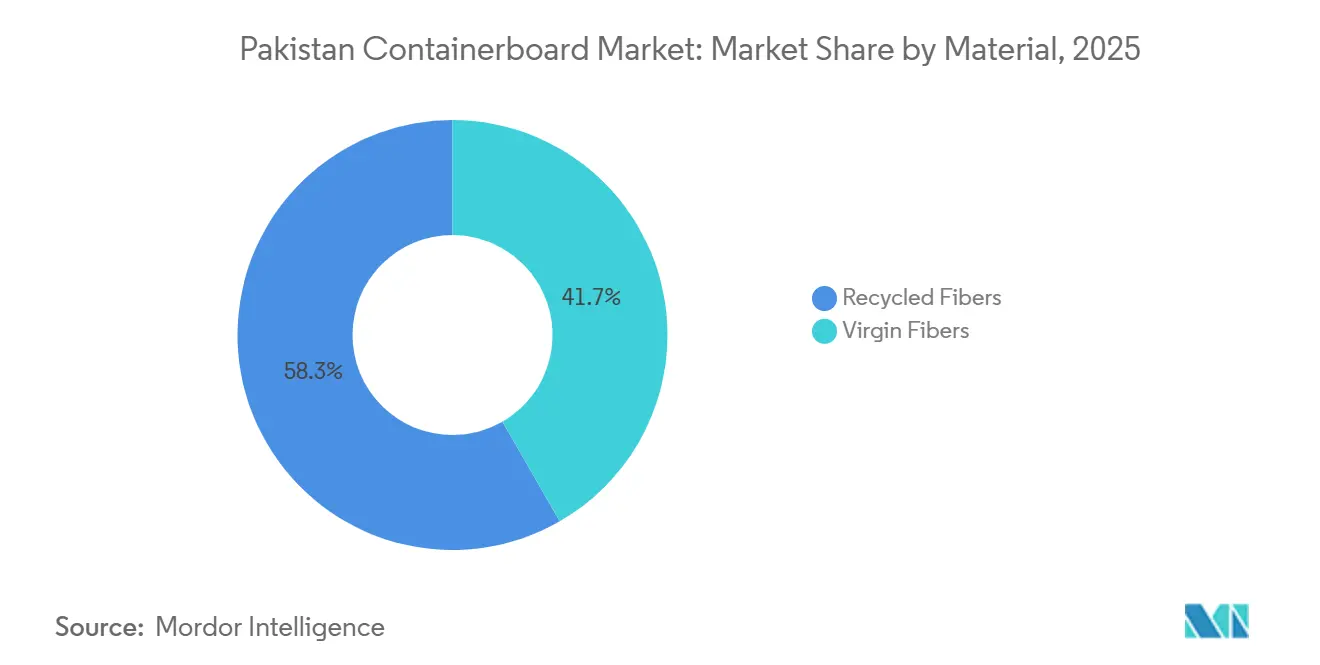

- By material, recycled fibers captured 58.32% of the Pakistan containerboard market share in 2025, while virgin fibers are projected to record the fastest growth at a 5.37% CAGR through 2031.

- By product type, kraftliners accounted for 46.43% share of the Pakistan containerboard market size in 2025, while flutings are set to expand at a 5.69% CAGR through 2031.

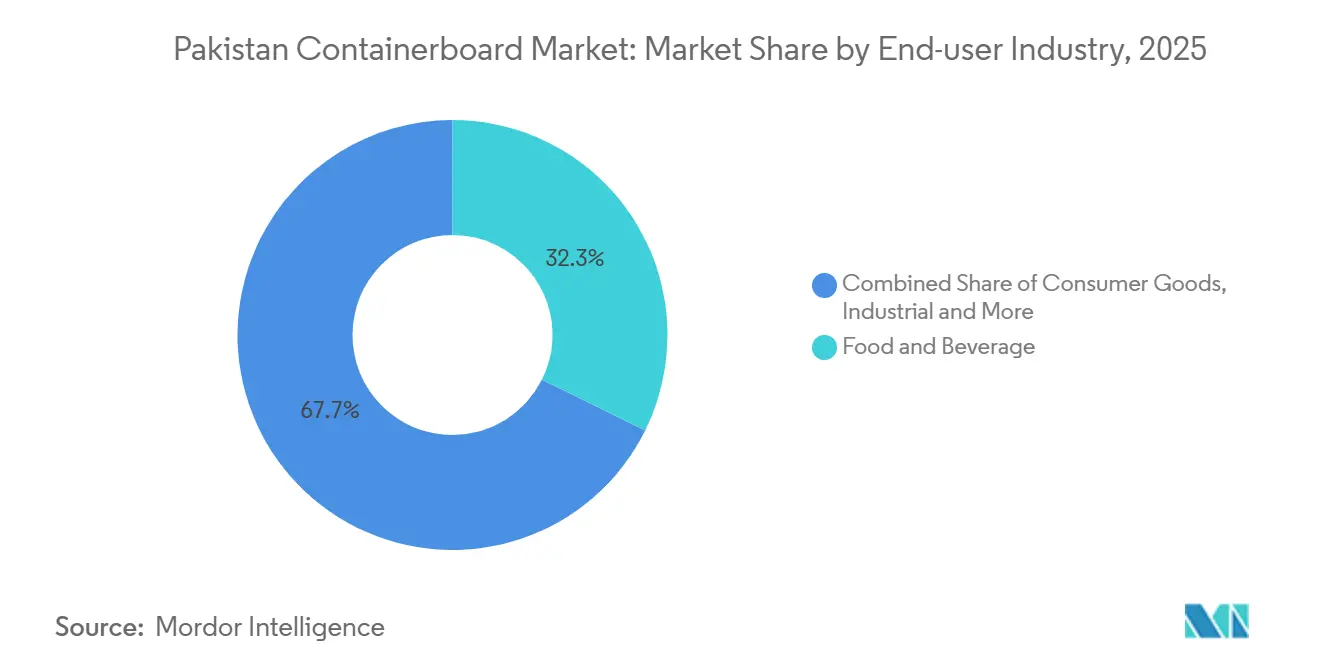

- By end-user industry, food and beverage held 32.32% of demand in 2025, while industrial applications are forecast to grow fastest at a 6.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Pakistan Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth In Packaged Food And Beverage Output | +1.5% | National, with primary concentration in Punjab, Lahore and Faisalabad, and Sindh, Karachi | Medium term (2-4 years) |

| E-commerce And Modern Retail Logistics Expansion | +1.1% | National, with early intensity in Lahore, Karachi, and Islamabad | Short term (≤ 2 years) |

| Sustainability-Driven Shift Toward Recyclable Fiber Packaging | +0.8% | National, accelerated in Karachi and Lahore industrial corridors | Long term (≥ 4 years) |

| Rising Corrugated Demand From Consumer Goods Supply Chains | +0.6% | National, with spillover into Gujranwala, Sialkot, and Faisalabad export clusters | Medium term (2-4 years) |

| Export Cartonization For Fruit, Textile, And Industrial Shipments | +0.4% | Punjab for textile exports, Sindh for mango and rice export belts | Short term (≤ 2 years) to Medium term (2-4 years) |

| Investment In Automated Corrugation And High-Performance Board Conversion | +0.3% | Punjab industrial estates and Karachi port-adjacent converter hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Packaged Food and Beverage Output

Growth in packaged food and beverage output remained the strongest demand support for the Pakistan containerboard market in 2026. Listed food and beverage companies reported Q1 2026 revenue growth of 5% and profit after tax growth of 15%, while the beverages category alone posted 17% revenue growth as consumer purchasing power improved from the earlier inflation peak. Nestlé Pakistan increased quarterly sales by 7%, and FrieslandCampina Engro Pakistan increased sales by 10%, which showed that packaging-heavy categories were moving more units through retail and distribution channels. Higher dairy, beverage, and packaged food volumes usually require more large-format corrugated secondary packs, so mills and converters see stronger pull for kraftliner and testliner grades. Pakistan’s listed consumer sector profit rose 28% to PKR 244 billion, USD 872.4 million, using the 2025 State Bank of Pakistan exchange reference of PKR 279.7 per USD, which gave major brand owners more room to standardize packaging and expand dispatch volumes. That backdrop keeps board demand tied to everyday packaged consumption rather than discretionary cycles alone.

E-commerce and Modern Retail Logistics Expansion

E-commerce and modern retail logistics expansion is widening the Pakistan containerboard market beyond its older food-led base. Pakistan’s e-commerce market reached USD 5.5 billion in 2024 and was projected to grow at 17% annually through 2027, which created new corrugated demand in electronics, apparel, SME goods, and social commerce orders. That shift matters because fulfillment requirements on drop resistance and ring-crush performance are pushing a meaningful share of shipments toward stronger board specifications rather than the lighter boxes used in traditional retail channels. Platforms such as Daraz also require tighter packaging compliance from fulfillment partners, which encourages converters to upgrade from simple single-wall formats where shipment conditions demand better protection. Regional warehouse expansion by delivery and fulfillment firms is spreading corrugated consumption into secondary cities, so box demand is no longer limited to Karachi and Lahore. For the Pakistan containerboard market, the practical effect is higher fluting consumption, faster reorder cycles, and more demand from businesses that previously did not rely on corrugated transit packaging.

Sustainability-Driven Shift Toward Recyclable Fiber Packaging

Sustainability-linked packaging change is still gradual, but it is becoming a firmer support for the Pakistan containerboard market. In 2025, food and beverage companies, NGOs, recyclers, and packaging firms formed the CoRE Alliance and began working with government representatives on a Pakistan-specific Extended Producer Responsibility framework. The proposal included a 5-year tax exemption for Packaging Recovery Organizations and a zero-tariff regime on recycling equipment, which would improve the economics of fiber recovery and recycled board production if implemented. That policy direction is important because it favors materials with established recycling pathways, and containerboard is already positioned within that system more clearly than many plastic formats. In 2026, plastic packaging prices in Asia moved to 4-year highs amid Iran-conflict-related supply disruption, which accelerated substitution inquiries toward paper-based formats from brand owners that had previously delayed material shifts. Over time, that combination of regulatory pressure and cost pressure should strengthen demand for recycled-fiber solutions across food, consumer goods, and transport packaging.

Rising Corrugated Demand From Consumer Goods Supply Chains

Rising corrugated demand from consumer goods supply chains continues to support the Pakistan containerboard market as national distribution networks extend deeper into lower-tier cities. Pakistan’s consumer staples companies posted combined profit of PKR 110 billion in 2025, USD 393.3 million at the 2025 State Bank of Pakistan exchange reference, up 13% from the prior year.[1]Profit Desk, “Consumer Purchasing Power Recovery Boosts Profits at Food and Beverage Companies,” Profit by Pakistan Today, profit.pakistantoday.com.pk That profit improvement points to stronger reinvestment capacity in supply chain standardization, including better secondary packaging for national distribution. Ismail Industries reported gross sales of PKR 61.5 billion in July-December 2025, equivalent to USD 219.9 million at the same exchange reference, and its multi-brand portfolio depends on standardized corrugated carton specifications across broad distribution networks. As modern trade and organized retail expand, more goods move in individual corrugated SKUs instead of informal bulk dispatch, which raises the need for consistent crush strength, print quality, and handling performance. This favors organized converters that can deliver repeatable board quality at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy Tariff Inflation And Captive Power Cost Pressure | -1.2% | National, with highest impact on grid-dependent mills in Punjab and Sindh | Short term (≤ 2 years) to Medium term (2-4 years) |

| Rupee Volatility And Imported Fiber Cost Exposure | -0.9% | National, acute at Karachi-based OCC and pulp importers | Medium term (2-4 years) |

| Recovered Paper Collection Inefficiency And Fiber Quality Variability | -0.5% | National, with collection concentrated in Lahore, Karachi, Faisalabad, and Sheikhupura | Long term (≥ 4 years) |

| Limited Price Pass-Through In A Buyer-Resistant Conversion Market | -0.3% | National, most acute in the fragmented small-converter segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy Tariff Inflation and Captive Power Cost Pressure

Energy tariff pressure remains one of the clearest constraints on the Pakistan containerboard market because continuous paper-making processes require uninterrupted steam and power. Industrial pre-tax electricity tariffs stood at PKR 49.19 per unit, USD 0.18, in March 2024 and declined to PKR 34.75 per unit, USD 0.12, by March 2026 after the revised industrial tariff took effect. NEPRA’s February 2026 revision reduced the industrial base rate from PKR 33.58 per unit, USD 0.12, to PKR 29.54 per unit, USD 0.11, which provided some relief for grid-dependent operators.[2]Pakistan Energy Ministry, “Pakistan Cuts Industrial Power Tariffs by Up to Rs 4.58 Per Unit,” ProPakistani, propakistani.pk Even after that cut, the cross-subsidy burden carried by industrial users keeps Pakistan’s power costs less competitive than subsidized Chinese manufacturing tariffs, which weakens local mills when buyers compare landed board prices. Century Paper’s CoGen-1 and CoGen-2 units, at 12.3 MW and 22 MW, show why captive generation matters so much for cost control and margin resilience. The result is a widening gap between integrated producers with self-generation and smaller converters that remain exposed to grid pricing.

Rupee Volatility and Imported Fiber Cost Exposure

Rupee volatility and imported fiber dependence continue to limit earnings visibility across the Pakistan containerboard market. Paper accounts for nearly 70% of total raw material cost in packaging production, so shifts in OCC, virgin kraft pulp, and chemical wood pulp prices move quickly into mill economics. Pakistan’s currency averaged PKR 279.7 per USD in 2025, which was more stable than stress periods but still elevated against the pre-2022 range. PACRA also noted that chemical wood pulp imports declined in value terms in 2025, which reflected a pullback in procurement as input costs became harder to absorb. The squeeze is more serious because the same currency weakness that raises imported fiber costs also reduces buyer willingness to accept higher board prices in local currency. That leaves margin-thin converters caught between globally priced inputs and a domestic market that resists full price pass-through.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominance Masks a Quality-Driven Virgin Fiber Resurgence

Recycled fibers captured 58.32% of demand in 2025, which kept them in the lead across the Pakistan containerboard market by material. The segment’s strength came from the economics of locally recovered paper and imported OCC, both of which remain more workable for the domestic mill base than large-scale dependence on virgin pulp. Most mid-scale producers in Punjab’s industrial estates continue to run recycled-fiber furnishes, because a shift toward imported virgin input would raise cost exposure sharply under current exchange conditions. Virgin fibers, while smaller in current volume, are projected to grow at a 5.37% CAGR from 2026-2031 as export-facing converters and multinational FMCG buyers ask for better burst strength and ring-crush performance. The Pakistan containerboard industry is therefore dividing into a high-volume recycled segment and a premium-quality virgin segment, with both expanding for different reasons.

Bulleh Shah Packaging’s August 2025 MoU with Tetra Pak Pakistan created a channel to recycle used beverage cartons into liner, fluting, and kraft paper, which added a more structured source of domestic recovered fiber. That step matters because it directly addresses the OCC import dependence that has often compressed margins when global recovered-fiber prices tighten. Digital traceability in the collection-to-production chain also fits the compliance direction of the proposed EPR framework, which increasingly favors transparent recovery systems. At the same time, Bulleh Shah Packaging continued importing chemical pulp from Canadian suppliers, which showed that premium grades in the Pakistan containerboard market still rely on international fiber procurement networks when performance requirements exceed recycled furnish capability.

By Product Type: Kraftliners Lead While Flutings Reflect Corrugator Expansion

Kraftliners held 46.43% of the Pakistan containerboard market by product type in 2025, which reflected their central role as the outer facing layer in corrugated board construction. That leadership is tied to the structure of Pakistan’s packaging demand, because food, consumer goods, industrial shipments, and export cartons all depend on reliable outer-liner strength. Testliners also retained a meaningful position in standard and medium-grade boxes where printing and moisture demands are lower than in premium applications. Flutings are forecast to grow at the fastest rate, 5.69% through 2031, as corrugator throughput rises and converters process more shipment volumes across e-commerce and consumer goods channels. In practical terms, rising fluting demand is often the first sign that new corrugator capacity is coming into operation in the Pakistan containerboard industry.

Roshan Packages’ vertical integration plan through Roshan Sun Tao Paper Mills targeted 100,000 tons of annual brown paper production, with a clear focus on both kraftliner and fluting grades. The project’s Special Economic Zone location also provided a 10-year tax exemption and lower import duties on plant and machinery, which improves structural cost competitiveness once operations scale up. That strategy shows why product mix is becoming more important, because converters want upstream access to the grades that move fastest when logistics intensity rises. BOBST’s 2025 launch of a fully automated corrugated production line also signaled the wider technology direction, and Pakistan’s larger converters are now assessing similar automation paths as labor, quality, and throughput pressures increase.

By End-User Industry: Food and Beverage Anchors Volume While Industrial Demand Accelerates

Food and beverage accounted for 32.32% of demand in 2025, which made it the largest end-user base in the Pakistan containerboard market. The segment’s scale rests on continuous FMCG output, regular replenishment cycles, and a wider spread of chilled, frozen, and ambient packaged products across retail channels. Q1 2026 performance reinforced that position, with beverage revenue up 17% and condiments and culinary products up 16%, which pointed to stronger secondary packaging throughput. Consumer goods also provide stable board demand because household and personal care categories continue to move even when macro conditions are uneven. Other end-user industries, including pharmaceuticals and agro-chemical distribution, remain smaller but supply a steady base load for corrugated packaging demand.

Industrial applications are projected to grow at a 6.15% CAGR from 2026-2031, which gives them the fastest expansion profile among end-user categories. That growth reflects rising packaging needs in cement, hardware, automotive parts, and agricultural chemical distribution, where heavier corrugated formats are used for transport protection and handling consistency. The pattern is notable because it broadens the Pakistan containerboard market beyond food-led demand and ties future growth more closely to domestic manufacturing activity. Industrial customers are also moving away from informal and heavier packaging formats when corrugated board offers better cost per shipment, lower weight, and easier handling across regional distribution routes. As that shift continues, organized converters with tighter board specifications and dependable supply will be better placed than small operators that compete mainly on short-term price.

Geography Analysis

Production and consumption in the Pakistan containerboard market remained concentrated in Punjab and Sindh, with the Lahore-Kasur-Sheikhupura corridor and Karachi serving as the main mill and converter centers. Century Paper and Board Mills operates its integrated production base near Kasur on the Lahore-Multan highway, which keeps it close to inland demand centers and agricultural residue supply. Bulleh Shah Packaging’s main production footprint and Roshan Packages’ operating base around Lahore’s industrial zone reinforce Punjab’s role as the strongest manufacturing cluster for board and corrugated conversion. Punjab also carries a large share of downstream demand because it is home to major food processing, consumer goods, and textile production centers that need continuous secondary packaging. Pakistan’s textile exports rose to USD 10.9 billion in 2025-26, which supports carton demand from export-oriented manufacturing belts such as Faisalabad, Gujranwala, and Sialkot.

Sindh, led by Karachi, functions as the main import and distribution gateway for OCC and chemical pulp, and that gives it a different role in the Pakistan containerboard market. Karachi-based manufacturers benefit from direct access to port logistics, which lowers inland freight on imported fiber compared with mills farther north. Bulleh Shah’s customer mix, which includes Unilever, Nestlé, Coca-Cola, and Pepsi, also shows how important large national distribution links are to the southern corridor as goods move through Karachi’s commercial network. Karachi’s demand mix is more exposed to industrial and export activity than some inland centers, because the city sits at the intersection of FMCG manufacturing, pharmaceuticals, and outward trade flows.

Smaller provinces remain underpenetrated but are becoming more relevant as distribution networks spread and export activity rises outside the main mill corridors. Khyber Pakhtunkhwa and northern producing zones need more export-grade cartons for fruit and vegetable shipments, but much of that supply still moves in from Punjab and Sindh. The Ministry of Commerce’s June 2026 waiver on financial instrument requirements for mango exports to Iran and Central Asian routes is expected to lift seasonal carton demand during the June-September shipping window. Pakistan Fruit and Vegetable Exporters Association’s 125,000-ton mango export target for 2025 also points to stronger cartonization demand in seasonal export belts, which creates room for localized box-making activity outside the traditional hubs.

Competitive Landscape

The Pakistan containerboard market is moderately concentrated at the integrated-mill tier, but it remains fragmented at the conversion level because a long tail of smaller converters competes without backward integration. Bulleh Shah Packaging operates the largest integrated platform in the country, with 240,000 tons of paper and board capacity and annual corrugated box capacity of 210 million units.[3]Bulleh Shah Packaging Pvt. Ltd., “About Us,” Bulleh Shah Packaging Pvt. Ltd., bullehshah.com.pk Century Paper and Board Mills follows closely with 230,000 MT of installed paper-making capacity, integrated pulp operations, and captive power assets that strengthen cost control.[4]Century Paper and Board Mills Limited, “Operations Page,” Century Paper and Board Mills Limited, centurypaper.com.pk Below these integrated players, converters such as Roshan Packages, Jahangir Packages, Sufi Brothers, and Sardar Family Packages compete more on price, location, and turnaround time than on upstream scale.

Vertical integration is becoming the clearest strategic dividing line in the competitive structure. Roshan Packages’ Roshan Sun Tao Paper Mills project, which targets 100,000 tons of annual brown paper output, is designed to reduce reliance on externally sourced board and capture more margin across the value chain. Packages Limited also injected PKR 8 billion, USD 28.6 million using the 2025 State Bank of Pakistan exchange reference, into Bulleh Shah Packaging through a mix of ordinary equity, subordinated debt, and potential loan-to-equity conversion, which shows how strongly the group is backing integrated scale. Bulleh Shah Packaging’s recycling partnership with Tetra Pak Pakistan added another strategic layer by widening access to domestic recovered fiber and reducing dependence on imported OCC in selected grades. Automation is also emerging as a competitive tool, because BOBST-class integrated lines can reduce labor cost per box by 30-40% compared with conventional setups while improving line consistency and speed.

The strongest white-space opportunities still sit in high-performance grades such as moisture-resistant fluting and micro-flute formats for retail-ready packaging. These grades are harder for smaller converters to supply consistently because they require tighter process control and better board input quality. Southern distribution corridors also remain open for larger-scale integrated capacity, since demand is rising but no single player dominates those routes with the same depth seen in Punjab. Overall, the competitive field favors companies that can control fiber sourcing, power economics, conversion quality, and customer service at the same time.

Pakistan Containerboard Industry Leaders

Bulleh Shah Packaging (Pvt.) Limited

Century Paper & Board Mills Limited

Roshan Packages Limited

Sardar Family Packages Pvt. Ltd.

Jahangir Packages (Pvt) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Pakistan's Ministry of Commerce granted a 4-month waiver, June 1-September 30, 2026, on financial instrument requirements for mango exports to Iran and Central Asian states via Iran. The policy directly stimulates demand for export-grade corrugated outer cartons from fruit exporters in Punjab and Sindh during the peak mango season, expanding seasonal cartonization volumes for containerboard converters.

- March 2026: Pakistan's Power Division reported that industrial pre-tax electricity tariffs fell from PKR 49.19 per unit, USD 0.18, in March 2024 to PKR 34.75 per unit, USD 0.12, in March 2026, a cumulative reduction of PKR 14.44 per unit, USD 0.05, providing significant energy cost relief to paper-making operations that account for a structurally large share of per-unit production costs.

- February 2026: NEPRA formally notified the reduction of the industrial base electricity tariff from PKR 33.58 to PKR 29.54 per unit, a reduction of PKR 4.04 per unit, effective February 1, 2026. The revision, which also eliminated the PKR 101 billion cross-subsidy burden on industry, provided operating cost relief to grid-dependent corrugated board manufacturers and converters.

Pakistan Containerboard Market Report Scope

The Pakistan Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Pakistan Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the Pakistan containerboard market size in 2026 and where is it expected to reach by 2031?

The Pakistan containerboard market size stands at USD 1.83 billion in 2026 and is forecast to reach USD 2.32 billion by 2031 at a 4.86% CAGR.

Which material segment leads demand in Pakistan?

Recycled fibers lead demand with a 58.32% share in 2025 because the domestic mill base still relies heavily on recovered paper and imported OCC for cost control.

Which product type is growing the fastest through 2031?

Flutings are projected to grow the fastest at a 5.69% CAGR, supported by higher corrugator throughput and more frequent shipment activity across retail and logistics channels.

Which end-user group creates the largest volume base for containerboard?

Food and beverage remains the largest end-user group with 32.32% of demand in 2025, supported by steady packaged food, dairy, and beverage volumes.

Why are integrated producers better positioned than small converters?

Integrated players have stronger control over fiber sourcing, power economics, and board quality, while smaller converters remain more exposed to raw material volatility and grid-based energy costs.

What are the main risks affecting growth through 2031?

The main risks are energy tariff pressure, rupee volatility, and dependence on imported fiber, all of which limit margin stability and reduce the ability to pass higher costs to buyers.

Page last updated on: