Australia Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

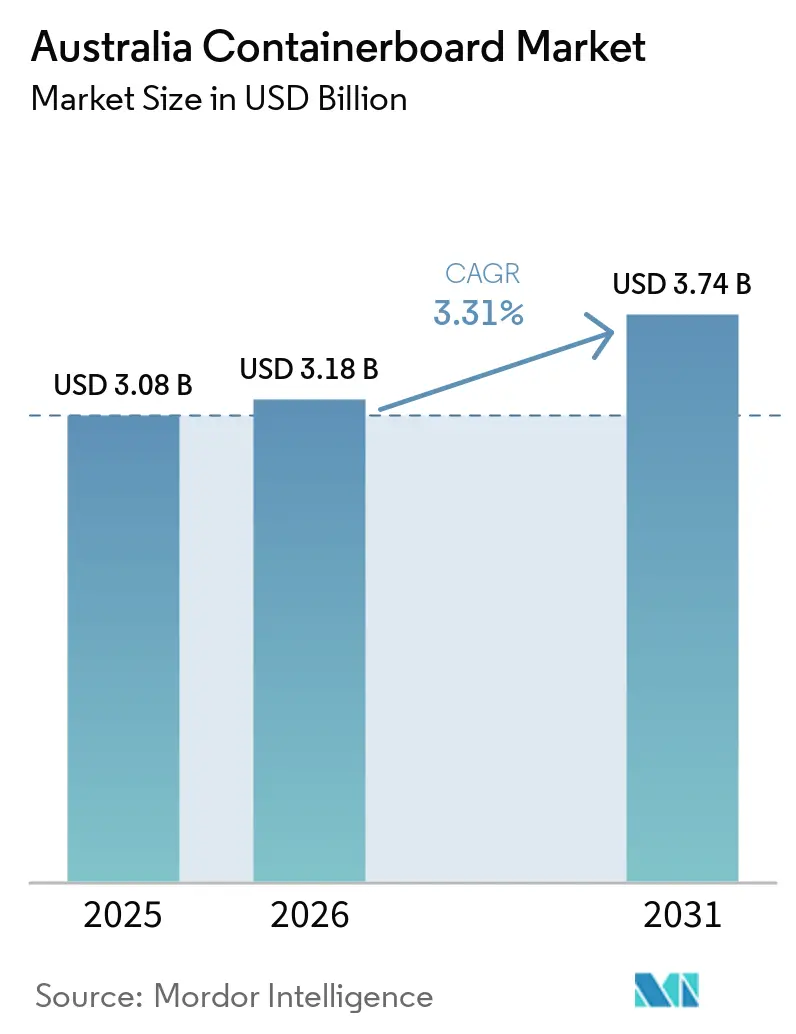

| Base Year Market Size (2025) | USD 3.08 Billion |

| Market Size (2026) | USD 3.18 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

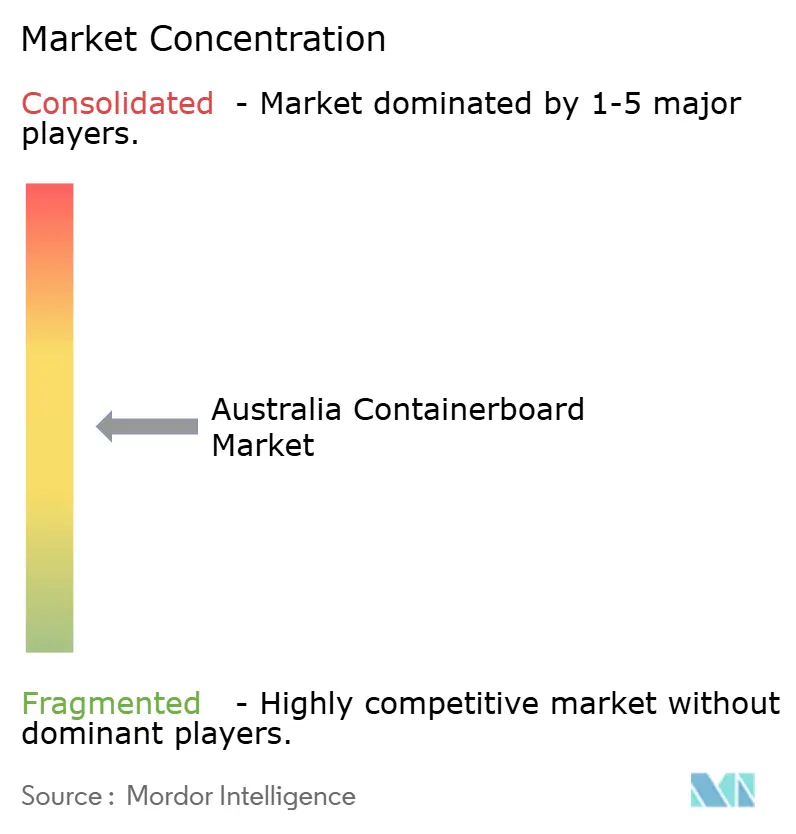

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Containerboard Market Analysis by Mordor Intelligence

The Australia containerboard market size is expected to grow from USD 3.08 billion in 2025 to USD 3.18 billion in 2026 and is forecast to reach USD 3.74 billion by 2031 at 3.31% CAGR over 2026-2031. The Australia containerboard market is being shaped by steady parcel-led packaging demand, rising pressure to replace certain plastic formats, and a deeper shift toward secondary-fiber sourcing. E-commerce expansion is keeping corrugated demand resilient because more retail categories now move through frequent, smaller shipments that require regular box replenishment. Food and beverage manufacturing provides a stable demand floor because export-oriented and domestic distribution chains both rely on corrugated packaging across fresh, processed, and chilled products. At the same time, imported board and pre-converted boxes are tightening pricing conditions for local converters, especially in standardized recycled grades. This leaves the Australia containerboard market positioned around recycled-fiber efficiency, premium performance in export applications, and faster service from integrated domestic suppliers.

Key Report Takeaways

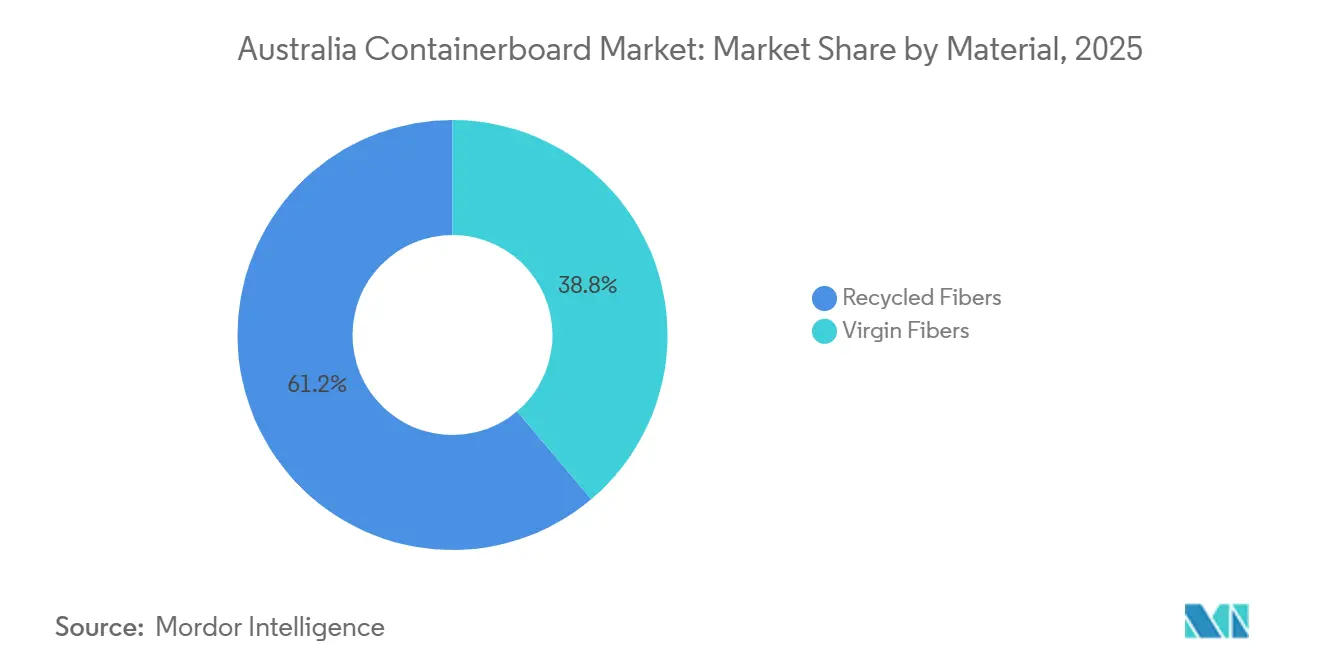

- By material, recycled fibers captured 61.17% of the Australia containerboard market share in 2025.

- By product type, the Australia containerboard market size for the kraftliners segment is forecast to advance at a 3.74% CAGR through 2031.

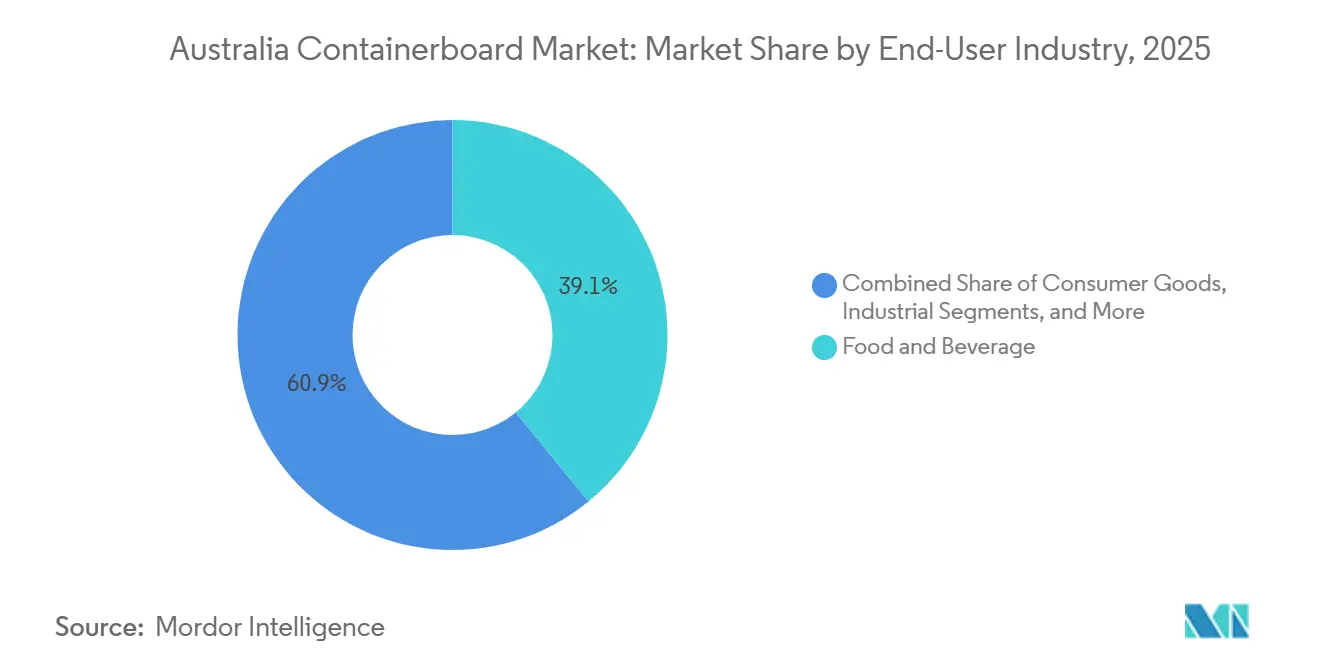

- By end-user industry, food and beverage captured 39.11% of the Australia containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Parcel And Online Grocery Growth | +1.0% | National, concentrated in New South Wales, Victoria, and Queensland | Short term (≤ 2 years) |

| Plastic Substitution And Circular Packaging Commitments | +0.8% | National, early adoption momentum in New South Wales and Victoria | Medium term (2-4 years) |

| Food And Beverage Manufacturing Expansion | +0.6% | National, led by Victoria, New South Wales, and Queensland | Medium term (2-4 years) |

| Rising Recycled Content And Recyclability Requirements | +0.4% | National | Medium term (2-4 years) |

| Export Produce Demand For Ventilated And Moisture-Managed Fiber Packs | +0.3% | Queensland, Victoria, South Australia, and Western Australia | Long term (≥ 4 years) |

| Automation-Compatible Short-Run Box Demand | +0.2% | National, with early gains in major metropolitan markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Parcel And Online Grocery Growth

Online retail accounted for 24% of all retail spend in 2025, indicating that parcel-led packaging demand is now a structural part of the Australian containerboard market.[1]Australia Post, “Australia Post eCommerce Report 2026,” Australia Post, auspost.com Total online household expenditure reached AUD 82.6 billion (USD 53.7 billion), up 14% year on year, which kept corrugated demand elevated across everyday and discretionary categories.[2]Australia Post, “Aussies Add 82.6 Billion to Cart,” Australia Post Newsroom, newsroom.auspost.com.au Australia recorded 9.8 million online shopping households in the year, equal to 82% of all households, which widened the base for direct-to-consumer box demand. Basket size fell to AUD 96 (USD 62.4), while purchase frequency rose by 4 transactions per shopper, suggesting more frequent dispatches with a higher box-to-product ratio than older retail models assumed. The result is a packaging mix that favors shorter runs, more order variability, and a steadier pull for corrugated formats across the Australia containerboard market.

Plastic Substitution And Circular Packaging Commitments

Plastic substitution is moving from voluntary brand language to policy-backed packaging redesign, elevating the role of fiber formats in the Australian containerboard market.[3]Department of Climate Change, Energy, the Environment and Water, “2025 National Packaging Targets,” DCCEEW, dcceew.gov.au The national packaging reform agenda keeps recyclability, recycled content, and producer responsibility at the center of compliance expectations for packaging placed on the market. NSW Plastics Plan 2.0 said loose-fill and void-fill expanded plastic packaging, and EPS-based retail fresh produce trays, would be phased out from 2026-27, creating direct replacement opportunities for corrugated inserts and fiber trays. APCO estimated that replacing EPS tableware, EPS loose-fill, and plastic bags and pouches alone could shift more than 108,000 tonnes of annual packaging demand toward paperboard and corrugated formats. Because brand owners are moving before deadlines, new tooling and sourcing decisions are already being committed in the Australia containerboard market rather than being delayed until the last phase of regulation.

Food And Beverage Manufacturing Expansion

Food and beverage manufacturing provides the Australian containerboard market with a stable demand base, as it combines domestic distribution with export shipping needs across many packaged categories. The Australian Food and Grocery Council said sector turnover grew at a 6.3% CAGR between 2020 and 2026, while real growth was 3.9%, suggesting volume expansion remained positive even after price effects were removed. Food and beverage exports totaled almost AUD 36 billion (USD 24.1 billion) in 2022-23, and that trade mix supports demand for corrugated solutions used in meat, dairy, fresh produce, and processed food flows. Higher-value food manufacturing matters especially because branded export packs and specialty shippers need better print surfaces, moisture performance, and treatment compatibility than basic transit boxes. ABS reported that food, beverage, and tobacco product output rose 1.1% in the September-December 2025 quarter, adding to the packaging workload even as manufacturers remained cautious about other inputs.

Rising Recycled Content And Recyclability Requirements

Recycled content rules are reshaping competitive positioning in the Australian containerboard market by affecting both fiber sourcing decisions and compliance costs. APCO's 2025 packaging targets set a 60% post-consumer recycled content requirement for paper and paperboard packaging, while fiber packaging achieved 55% in 2023-24, up from 49% in 2017-18. APCO's 2030 Strategic Plan proposed eco-modulated member fees from FY2027, which means packaging formats with weaker recycled-content performance are likely to face higher compliance costs. APCO also said that 80% to 100% post-consumer recycled content is technically achievable for non-food-grade corrugated cardboard, leaving room for mills and converters to raise recycled content specifications further. Export restrictions on recovered paper and cardboard since July 2024 have increased the domestic OCC pool, and that supports local recycled containerboard once mills can match supply with traceability and processing quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Containerboard And Converted Box Inflows Pressuring Domestic Pricing | -0.6% | National, most acute in major metropolitan conversion markets | Short term (≤ 2 years) |

| Energy And Recovered Fiber Cost Volatility | -0.4% | National, concentrated near major paper manufacturing sites | Medium term (2-4 years) |

| Recycled Fiber Quality Traceability And Collection Losses | -0.3% | National, most pronounced in regional and remote areas | Medium term (2-4 years) |

| Biosecurity And Treatment Constraints On Coated Or Impermeable Export Packs | -0.2% | Queensland, Western Australia, South Australia, and Victoria | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Containerboard And Converted Box Inflows Pressuring Domestic Pricing

Imported liner, medium, and finished corrugated boxes are putting pricing pressure on the Australia containerboard market, especially in standardized grades sold into major metropolitan conversion markets.[4]Orora Limited, “Orora Annual Report 2025,” Orora Limited, ororagroup.com The challenge is broader than board imports because pre-converted boxes can bypass domestic converting margins and compete directly for routine shipper volumes. That changes procurement behavior because buyers can compare landed-cost offers with local supply for simple specifications, with less dependence on supplier differentiation. Domestic suppliers still hold stronger positions in short runs, precise custom sizes, and export packs that must meet treatment and ventilation rules. Even so, the pricing window available to local mills and converters is narrowing, underscoring the importance of service, speed, and traceable recycled content in the Australian containerboard market.

Energy And Recovered Fiber Cost Volatility

Energy volatility remains a significant brake because integrated paper production relies on large, continuous electricity and heat inputs across the pulping, drying, and converting stages. ABC News reported that the Boyer Paper Mill was spending AUD 44 million (USD 28.6 million) a year on electricity and another AUD 12 million (USD 7.8 million) to source coal from New South Wales when local hydro supply fell short. That example shows how mills can remain exposed to elevated operating costs for extended periods while energy systems are reworked and replacement equipment is phased in. Recovered fiber adds a second layer of risk because mills need stable volumes and usable quality from OCC and kerbside streams, not just higher gross collection numbers. Export waste reduction rules have diverted more recovered paper into domestic channels since July 2024, but without matching reprocessing capacity and chain-of-custody discipline, extra feedstock does not automatically become lower-cost usable input.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Hold The Lead While Virgin Grades Find Premium Openings

Recycled fibers held 61.17% of the Australian containerboard market share in 2025, reflecting the cost advantage of locally collected OCC over imported virgin kraft pulp in commodity corrugated grades. That position is supported by Australia's established recovery system, with old corrugated containers achieving an 84% collection rate in 2023-24. Fiber-based packaging introduced to the Australian market grew at a 4.1% CAGR from 2017-18 through 2023-24, and post-consumer recycled content in fiber packaging reached 55% by 2023-24. The share of fiber packaging relative to competing materials rose from 53% to 58% over the same period, which shows why recycled grades remain the commercial base of the Australian containerboard industry.

The Australia containerboard market for virgin fibers is projected to expand at a 3.66% CAGR from 2026 to 2031, driven by applications where recycled liner still cannot meet performance requirements. These uses include export produce packaging for horticultural, meat, and dairy shipments, where burst resistance, cold-chain performance, and permeability to treatment gases matter. DAFF's packaging suitability guidance states that cardboard boxes used for perishable exports must have ventilation holes and remain permeable to fumigant distribution, which limits the use of waxed and laminated substitutes. Visy's AUD 30 million (USD 19.5 million) Gibson Island upgrade, completed in September 2025, aimed to produce new corrugated paper grades from 100% recycled feedstock, demonstrating how producers are trying to close the functional gap between recycled and virgin grades.

By Product Type: Testliners Keep The Base While Kraftliners Advance Faster

Testliners accounted for 41.65% of the Australian containerboard market size in 2025, making them the largest product type by volume. Their lead matches Australia's OCC-based mill system and the wide use of two-ply and three-ply corrugated formats across FMCG and industrial distribution. APCO reported a 79% recovery rate for old corrugated containers nationally, which supports the economics of testliner production and sourcing. Fluting remained volume-stable alongside box production, while the move toward E and F micro-flutes in smaller e-commerce formats is gradually changing board mix rather than displacing medium demand.

The Australian containerboard market size for kraftliners is projected to expand at a 3.74% CAGR from 2026 to 2031, making them the fastest-growing product type in the forecast period. Their growth is being shaped by export produce packs that need strong virgin kraft performance under cold-chain and fumigation conditions. Australia exported plant and plant products to more than 100 countries and generated more than AUD 12 billion (USD 7.9 billion) in export revenue, which supports demand for certified corrugated formats used in prescribed goods. AFGC said investment in efficiency-enhancing assets, including automated packaging lines, is a core response to rising input costs, and that helps explain the lift in automation-compatible kraftliner shippers across the Australian containerboard market.

By End-User Industry: Food And Beverage Sets The Floor While Consumer Goods Build Speed

Food and beverage accounted for 39.11% of Australia's containerboard market share in 2025, maintaining its position as the largest end-user. Australia's food and beverage manufacturing sector reached USD 112 billion in turnover in 2023-24 and employed 237,000 people, accounting for 25.9% of national manufacturing jobs. That scale creates consistent demand for standard shippers, vented produce boxes, moisture-managed dairy packs, and chilled meat cartons with different liner and flute needs. The segment anchors the Australian containerboard market by linking steady domestic consumption with recurring export activity across multiple food categories.

The Australia containerboard market size for consumer goods is projected to expand at a 3.81% CAGR from 2026 to 2031, making it the fastest-growing end-user segment. Australia Post reported that online consumer electronics spend rose 16% year on year in July-September 2025, while home and garden rose 12%, and both categories rely on protective corrugated packaging in direct-to-consumer fulfillment. Industrial users continue to buy heavy-duty shippers and intermediate bulk corrugated containers for mining consumables, agricultural inputs, and manufacturing parts, which keeps a stable demand layer beneath faster-growing retail categories. Retail, pharmaceutical, logistics, and government users add a steady base load of corrugated demand, which reduces the risk of overreliance on a single end-use channel in the Australia containerboard market.

Geography Analysis

New South Wales and Victoria accounted for the largest regional demand base in the Australian containerboard market, and New South Wales accounted for nearly one-third of national e-commerce parcel volumes in 2025. Online spending in New South Wales reached AUD 28.5 billion (USD 18.5 billion) in 2025, the highest of any state, which reinforced its role as the country's largest parcel and fulfillment market. Victoria remains a leading manufacturing hub for food, pharmaceuticals, and consumer goods, so corrugated demand there is spread across transport packaging, shelf-ready formats, and e-commerce replenishment. Visy's investment footprint, including recycled paper and box operations in Victoria, supports the state's role in domestic supply and conversion activity. South Australia also matters because Detmold is consolidating its Australian operations through a new 5,100-square-meter headquarters at Regency Park in Adelaide, due for completion in October 2026.

Queensland is both a major consumption region and a supply center in the Australian containerboard market, as it combines agricultural exports with recycled paper production. Visy's Gibson Island mill in Brisbane received an AUD 30 million (USD 19.5 million) upgrade in September 2025, expanding the range of corrugated paper grades that can be produced from 100% recycled feedstock. The state's fruit, sugar, meat, macadamia, and aquaculture supply chains require export-grade corrugated boxes that can handle humidity and remain compatible with phytosanitary treatment. In Tasmania, Visy opened a new Packaging Hub in Devonport in February 2026 as part of an AUD 20 million (USD 12.8 million) long-term investment to serve berry and produce growers, breweries, and dairy processors. That move shows that smaller agricultural regions are becoming more relevant to the Australian containerboard market, particularly for growers who need short lead times and dependable local packaging supply.

Western Australia remains an attractive but logistically challenging part of the Australian containerboard market because its distance from eastern production sites increases freight costs and alters converter economics. That cost structure has historically supported imported converted products in standardized formats, even when domestic suppliers remain competitive on service and customization. The Australian Capital Territory and the Northern Territory are smaller demand nodes, but government procurement, services activity, and horticultural exports still support ongoing use of standard and specialized corrugated formats. ABS reported that exports of rural goods rose 6.6% in the September-December 2025 quarter, which supports the case for more export-ready corrugated supply across northern Australia.

Competitive Landscape

The Australian containerboard market is moderately concentrated in upstream production, with Visy Industries, Paper Australia, and Opal Group holding most of the domestic integrated board capacity, while independent converters remain numerous downstream. Visy stands out for vertical integration across recovered paper collection, recycled paper mills, and box plants, which gives it tighter control over fiber sourcing and conversion economics. Its decade-long AUD 2 billion (USD 1.28 billion) investment program includes recycled containerboard capacity at Coolaroo, a new drum pulper that adds 180,000 tonnes of recycling capacity, and the Hemmant Box Plant in Brisbane with output potential of up to 1 million 100% recycled and kraft paper boxes a day. The September 2025 upgrade at Gibson Island expanded the range of corrugated paper grades available to Queensland's agricultural and food chains. Those moves show that scale players are investing across recycling, board production, and box conversion rather than relying on one part of the value chain.

Product development is also expanding beyond standard corrugated grades as companies seek fiber-based substitutes for plastic packaging components. In May 2026, Visy introduced Visycell, a fiber-based insulation product whose lifecycle analysis found that it could have up to 91% lower marine microplastic impact than expanded polystyrene. That extension matters because it lets a board producer participate in protective packaging and cold-chain applications that were once more exposed to plastics. The Australian containerboard market is, therefore, rewarding suppliers that can pair recycled-content capability with application engineering and credible sustainability claims.

Mid-tier converters in the Australian containerboard market are differentiating through specialty formats, shorter runs, and automation-compatible designs, as straight board prices are becoming harder to defend. Export packs remain a defensible niche because treatment compliance, ventilation, and moisture performance are harder to replicate in low-cost imported boxes. Detmold's new Adelaide headquarters, announced in June 2025 and scheduled for completion in October 2026, will consolidate staff and bring corporate and manufacturing functions closer together. Regional expansion also matters because freight costs can quickly erode margins in corrugated supply, making local converting and service reach strategically valuable. As procurement rules tighten around recycled content and traceability, domestic integrated producers are likely to maintain an edge with customers seeking certified, auditable supply chains.

Australia Containerboard Industry Leaders

Visy Industries Australia Pty Ltd

ABBE Corrugated Pty Ltd

Australian Corrugated Packaging Pty Ltd

Pro-Pac Packaging (Aust) Pty Ltd

PACKQUEEN PTY LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Visy developed Visycell, a fibre-based protective insulation product, with independent lifecycle analysis confirming it reduces the impacts of marine microplastics by up to 91% compared to expanded polystyrene. The product positions Visy in the growing market for plastic packaging substitutes in industrial and cold-chain applications.

- February 2026: Visy opened a new Packaging Hub in Devonport, Tasmania, as part of a AUD 20 million (USD 12.8 million) long-term investment, supplying corrugated cardboard packaging to berry and produce growers, breweries, and dairy producers across the state. The hub is expected to reduce lead times and enable just-in-time delivery for Tasmanian agricultural exporters.

- September 2025: Visy completed a AUD 30 million (USD 19.3 million) upgrade to its Gibson Island 100% recycled paper mill in Brisbane, enabling manufacture of new corrugated box paper grades to serve Queensland's agricultural, food, and beverage industries. The project involved 100,000 staff hours and upgrades to sheet formation, drying, and energy systems.

- June 2025: Detmold Group commenced construction of a new 5,100 sqm global headquarters at 260 Regency Road, Regency Park, Adelaide, consolidating up to 240 employees from 8 metropolitan sites and co-locating corporate and manufacturing operations. Completion is targeted for October 2026.

Australia Containerboard Market Report Scope

The Australia Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Australia Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for the Australia containerboard sector?

The Australia containerboard market is expected to grow from USD 3.08 billion in 2025 to USD 3.18 billion in 2026 and reach USD 3.74 billion by 2031 at a 3.31% CAGR.

What is driving box demand in Australia most strongly right now?

E-commerce is the clearest near-term driver. Online retail reached 24% of all retail spend in 2025, and household online spending climbed to AUD 82.6 billion (USD 53.2 billion).

Which material segment leads demand?

Recycled fibers led with a 61.17% share in 2025, supported by strong OCC collection infrastructure and favorable economics in commodity corrugated grades.

Which product type is growing the fastest?

Kraftliners are projected to grow at a 3.74% CAGR through 2031, supported by export produce packaging needs and premium e-commerce presentation requirements.

Which end-user segment matters most for demand stability?

Food and beverage remains the largest end-user segment with 39.11% of 2025 demand, giving the sector a dependable base across domestic and export packaging flows.

What are the main risks for domestic producers and converters?

The key risks are import-led pricing pressure, energy cost exposure at mills, and quality and traceability issues in recovered fiber streams.

Page last updated on: