Hospital Capacity Management Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.35 Billion |

| Market Size (2031) | USD 10.07 Billion |

| Growth Rate (2026 - 2031) | 13.47% CAGR |

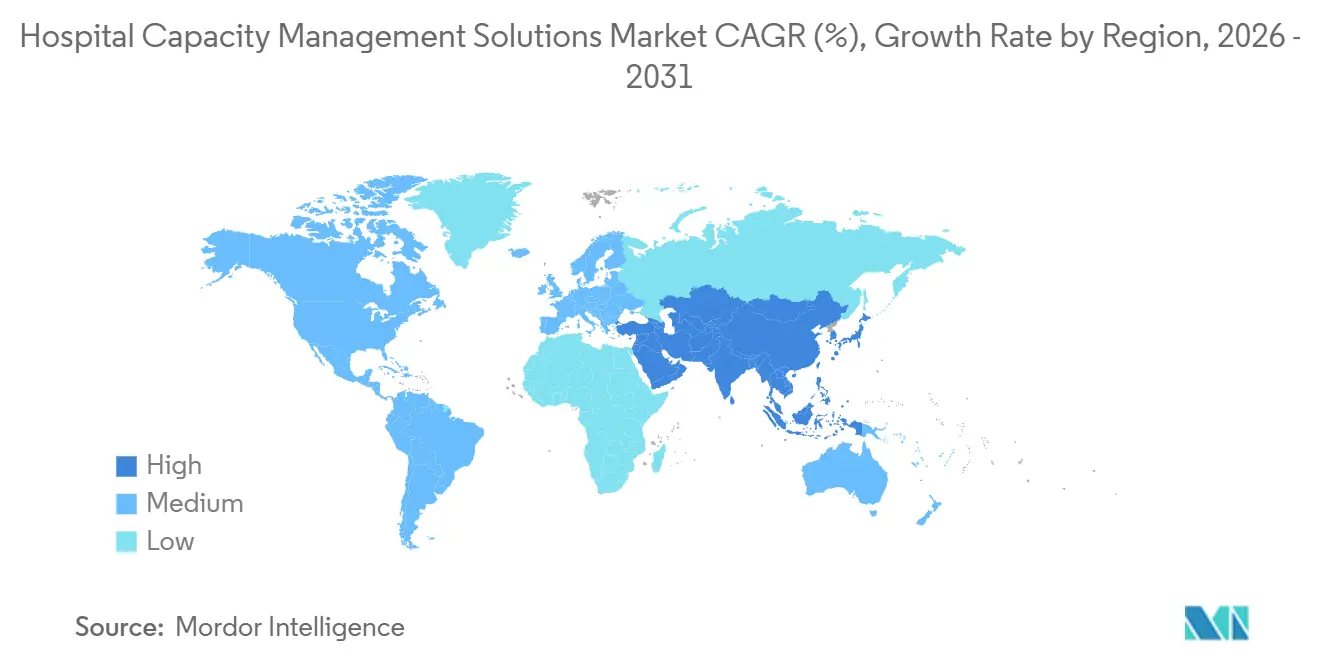

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

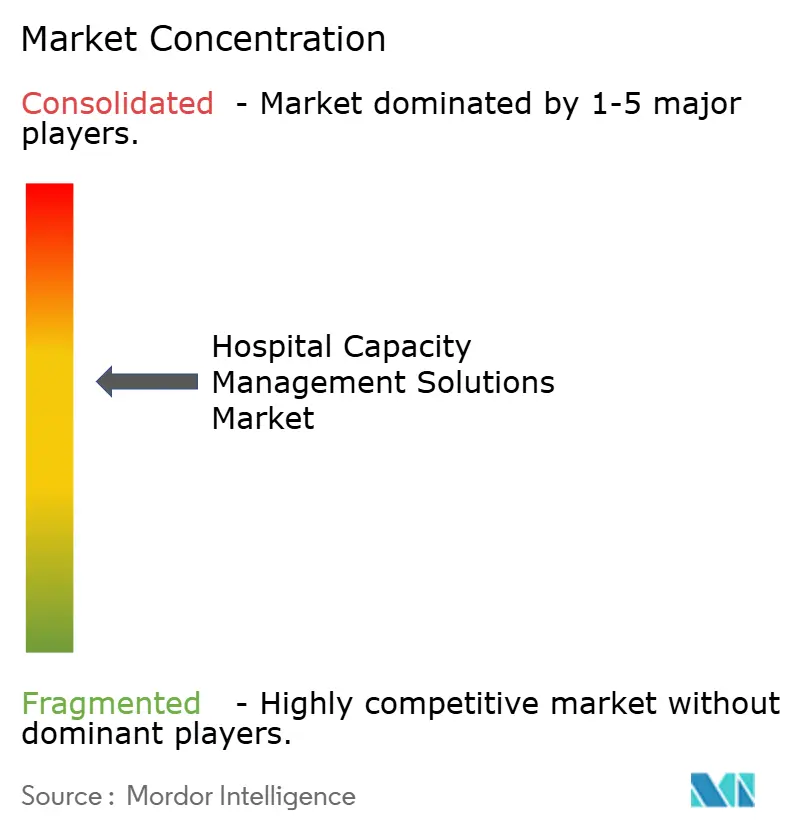

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Capacity Management Solutions Market Analysis by Mordor Intelligence

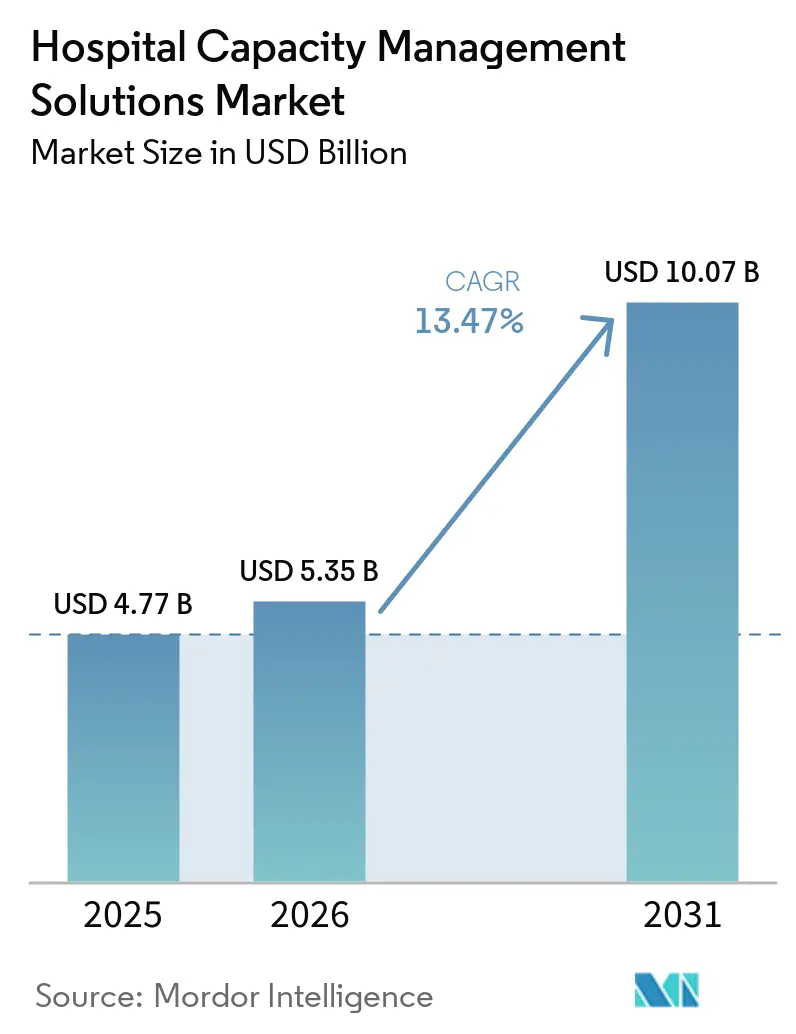

The Hospital Capacity Management Solutions Market size is expected to grow from USD 4.77 billion in 2025 to USD 5.35 billion in 2026 and is forecast to reach USD 10.07 billion by 2031 at 13.47% CAGR over 2026-2031.

The market is expanding because hospitals are operating under sustained bed pressure, and that pressure is turning patient flow tools into a core operating need rather than a discretionary software purchase. A large share of prolonged inpatient days is tied to a small portion of admissions, and that is raising the direct cost of poor coordination for providers and health systems. Payment models that reward shorter stays and regulations that require stronger interoperability are also making real-time orchestration platforms easier to justify during procurement reviews. The competitive environment is defined by established EHR-linked vendors on one side and AI-focused specialists on the other, and that mix is increasing partnership activity, product bundling, and service-led implementation models across the hospital capacity management solutions market. Market opportunities remain strongest where hospital digitization is accelerating, and legacy integration barriers are lower, even as buyers remain cautious about implementation complexity, cyber risk, and return timelines across the hospital capacity management solutions market.

Key Report Takeaways

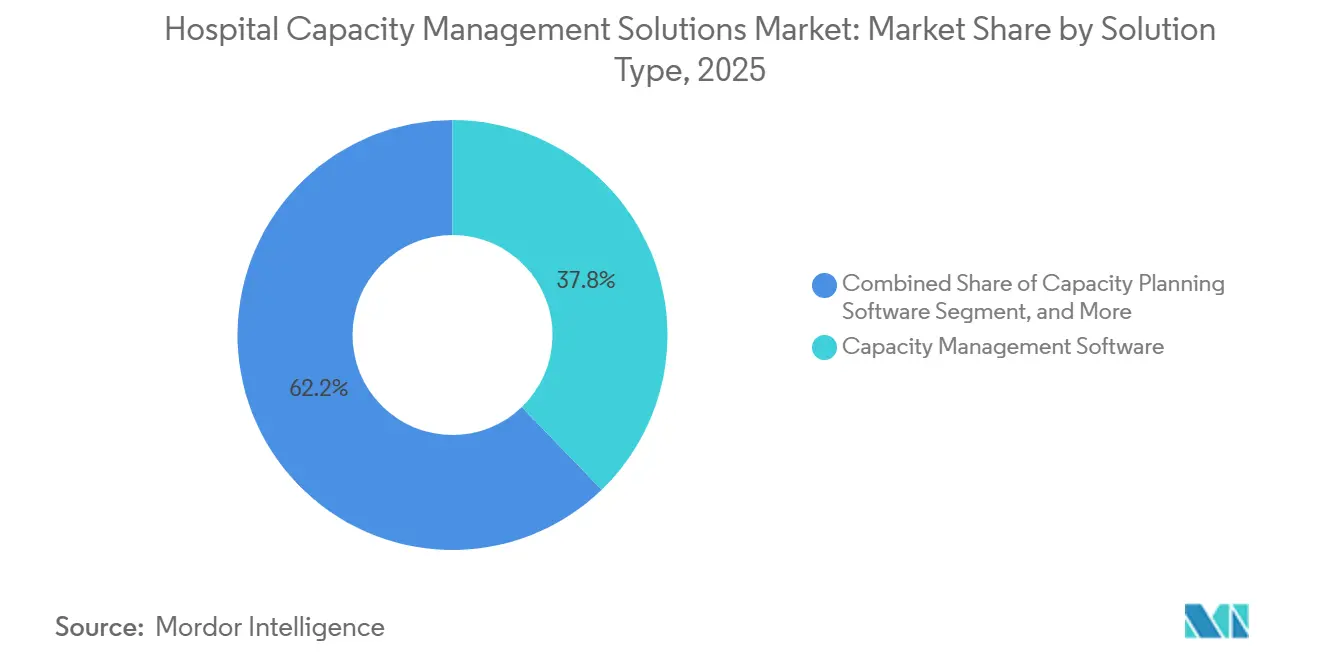

- By solution type, capacity management software led with 37.82% revenue share in 2025, while patient flow management software is projected to expand at 13.89% CAGR through 2031.

- By deployment mode, cloud solutions accounted for 53.41% share in 2026, while cloud-based solutions are projected to grow at 14.19% CAGR through 2031.

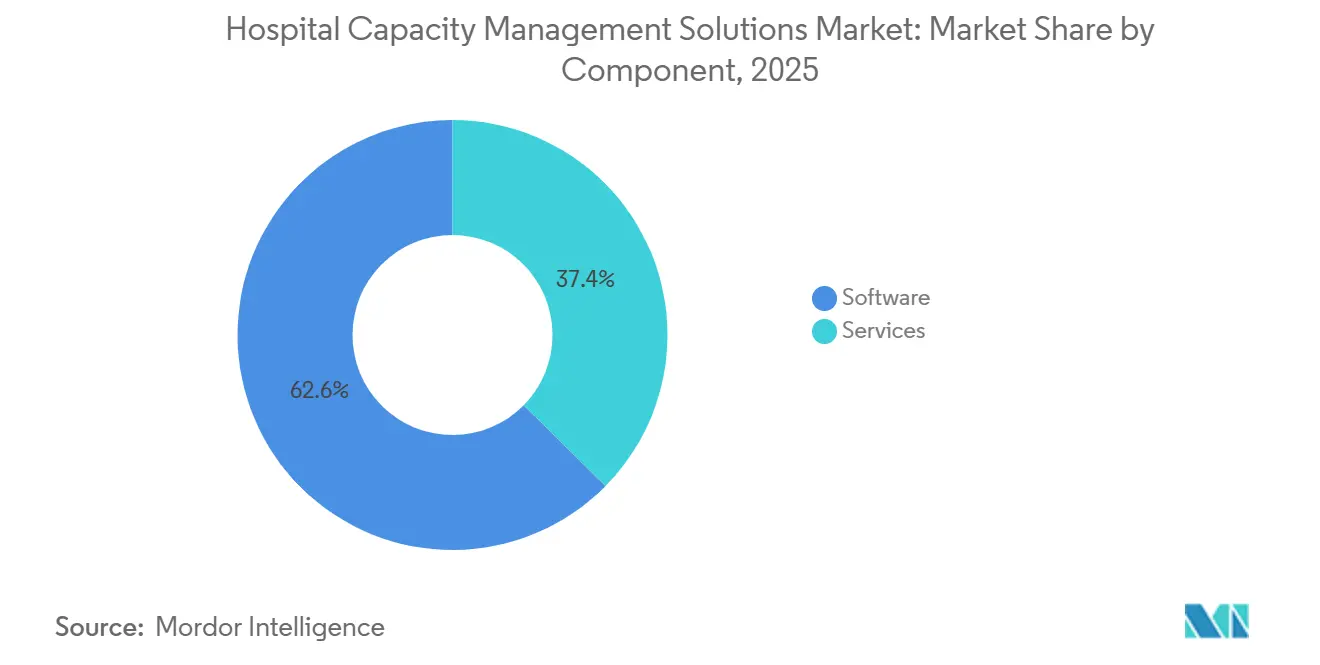

- By component, software represented 62.64% of revenue in 2025, while services are forecast to grow at 14.95% CAGR through 2031.

- By end user, hospitals held 53.03% of revenue in 2025, while ambulatory surgical centers are forecast to record the fastest growth at 16.57% CAGR through 2031.

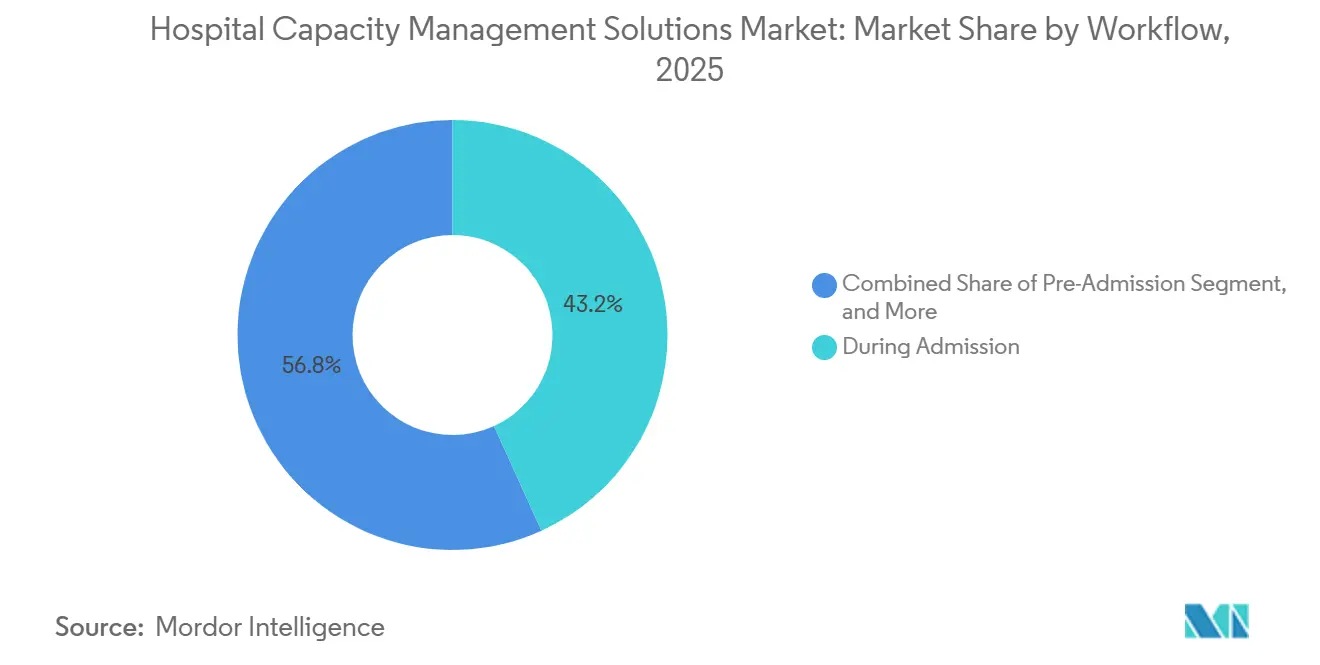

- By workflow, during admission solutions held 43.19% share in 2025, while post-discharge solutions are projected to advance at 13.72% CAGR through 2031.

- By geography, North America led with 48.41% share in 2025, while Asia-Pacific is projected to grow at 15.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hospital Capacity Management Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Inpatient Throughput Pressure and Bed Turnover Constraints | +2.8% | Global, most acute in North America, Western Europe, and urban APAC | Short term (≤ 2 years) |

| Value-Based Care and Length-Of-Stay Reduction Programs | +2.4% | North America and EU | Medium term (2-4 years) |

| AI-Driven Predictive Capacity Orchestration | +2.2% | Global, with early concentration in North America and APAC | Medium term (2-4 years) |

| Interoperability Mandates Across EHR, ADT, RTLS, and Staffing Systems | +1.8% | North America and EU | Medium term (2-4 years) |

| Workforce Scarcity and Nurse Scheduling Optimization Needs | +1.5% | Global, critical shortfalls in North America and rural APAC | Short term (≤ 2 years) |

| Real-Time Command Center Adoption Across Multi-Site Health Systems | +1.3% | North America, Western Europe, GCC, and emerging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Inpatient Throughput Pressure And Bed Turnover Constraints

The hospital capacity management solutions market is benefiting from a basic operating problem inside acute care settings, which is that patient inflow is rising faster than discharge coordination can respond. NHS England data showed general and acute bed occupancy at 92.5% in Q4 2024/25, which was above both the 90% ceiling recommended by NICE and normal NHS operating guidance.[1]Nuffield Trust, “Hospital Bed Occupancy,” Nuffield Trust, nuffieldtrust.org.uk Vizient also reported in May 2026 that global hospital occupancy is projected to move above the 85.0% safety threshold by 2032 if current coordination patterns continue. The same analysis found that 2% of admissions account for 15% of prolonged inpatient days, and those excess days add USD 2,093 per day in avoidable costs. Only 36% of surveyed hospitals had standardized discharge escalation protocols across most inpatient units, and only 33% of academic medical centers reported full case manager-led interdisciplinary rounding, which shows that many delays still come from fragmented coordination rather than pure bed shortage. That pattern is pushing the hospital capacity management solutions market toward platforms that combine escalation logic, social needs review, and discharge workflow automation in one operating layer instead of adding another isolated dashboard.

Value-Based Care And Length-Of-Stay Reduction Programs

The hospital capacity management solutions market is also being supported by payment frameworks that connect reimbursement more directly to efficiency and patient progression. CMS confirmed through the FY2025 IPPS final rule that hospital performance is assessed across outcomes, safety, efficiency, and patient experience, which keeps length of stay management close to the financial core of hospital operations.[2]Centers for Medicare & Medicaid Services, “FY 2025 IPPS Final Rule Home Page,” Centers for Medicare & Medicaid Services, cms.gov A quality initiative conducted across 7 facilities and 283,517 discharges between August 2024 and July 2025 reduced the observed-to-expected length of stay ratio from 1.07 to 0.99, increased discharges by 3,863, and lowered emergency department boarding hours from 14.1 to 10.4. Those results show that discharge planning and progression management can produce operational gains at a scale that finance teams can recognize. The hospital capacity management solutions market is therefore seeing more combined buying of capacity tools and care coordination software as hospitals evaluate software return through reimbursement improvement, as well as labor and throughput performance. This is making operational software part of value-based care execution rather than a separate IT spending line.

AI-Driven Predictive Capacity Orchestration

The hospital capacity management solutions market is moving from descriptive monitoring toward systems that recommend and trigger specific actions during a patient's stay. Sutter Health reported that its Epic command center pilot launched in January 2025 reduced excess length of stay days by 27%, improved emergency department throughput by 8% despite a 5% volume increase, and cut excess days by 44% against comparable hospitals outside the pilot. GE HealthCare stated that Duke Health created capacity for 500 additional patients each year and reduced temporary labor demand by 50% through its command center deployment, while Oregon Health & Science University reported a 10% reduction in emergency department walkouts and a 0.5-day reduction in surgical length of stay during the first year. Baptist Health in Arkansas also increased accepted patient transfers by 178% between 2021 and 2025 after command center deployment and iQueue integration, which shows that predictive orchestration can support growth as well as cost control. These cases are changing how buyers define value in the hospital capacity management solutions market because the benefit is no longer limited to bed visibility alone. Vendors that can automate response across perioperative, inpatient, transfer, and discharge workflows are gaining a stronger position in new buying cycles.

Interoperability Mandates Across EHR, ADT, RTLS, And Staffing Systems

The hospital capacity management solutions market is gaining support from interoperability rules that reduce one of the oldest barriers to implementation. ONC stated that the HTI-4 final rule, effective October 1, 2025, sets certification requirements for API functionality, electronic prior authorization, and clinical data exchange under the FY2026 CMS IPPS framework.[3]Office of the National Coordinator for Health Information Technology, “2026 Interoperability Standards Advisory Reference Edition,” U.S. Department of Health and Human Services, healthit.gov ONC also required support for HL7 FHIR US Core 6.1.0 by December 31, 2025 and targeted the final USCDI v7 release for July 2026, which raises the baseline for machine-readable data exchange across certified health IT. This lowers the cost of connecting ADT feeds, RTLS systems, EHR modules, and staffing platforms, and it reduces part of the historical advantage that embedded EHR vendors held in the hospital capacity management solutions market. At the same time, broader interoperability increases the amount of patient-level data moving between systems, which expands cyber and governance obligations for hospitals and vendors. Vendors that already offer FHIR-native architecture and pre-certified connectors are gaining ground with buyers who are modernizing several systems at once across the hospital capacity management solutions market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity With Legacy Hospital IT Stacks | -0.7% | Global, most severe in mature markets such as North America and Western Europe | Short term (≤ 2 years) |

| Upfront Implementation Cost and Long ROI Payback Cycles | -0.5% | Global, most pronounced in public hospital systems in Europe and South America | Medium term (2-4 years) |

| Data Governance, Cybersecurity, and Consent Management Burden | -0.3% | Global, with highest regulatory intensity in Europe and North America | Medium term (2-4 years) |

| Change Resistance From Clinicians and Operations Teams | -0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity With Legacy Hospital IT Stacks

The hospital capacity management solutions market still faces a major slowdown from the technical difficulty of working across mixed hospital IT environments. Many acute care providers operate with 4 to 6 separate clinical and operational systems, including EHR, ADT, RTLS, staffing, and bed management applications, and those systems were often purchased years apart. When a capacity platform needs deep bidirectional integration across that stack, implementation in a large health system can take 12 to 24 months. ONC has tried to reduce this friction through information blocking rules, yet the December 2025 HTI-5 proposed rule showed that certification and exchange requirements still need revision, which suggests that interoperability challenges have not been fully resolved. This gives embedded EHR module vendors a practical advantage in the hospital capacity management solutions market, even when specialist tools show strong pilot outcomes. Vendors that provide pre-built FHIR connectors, modular rollouts, and managed integration support are therefore improving their position in the hospital capacity management solutions market.

Upfront Implementation Cost And Long ROI Payback Cycles

The hospital capacity management solutions market is also limited by the large upfront spending required for enterprise deployments. Full platform rollouts can require investment from several hundred thousand to multiple millions of USD once implementation services, retraining, and workflow redesign are included. Return timelines often extend to 3 to 5 years in large public hospital networks, and that timing does not fit well with annual budget cycles or politically constrained capital plans. Another challenge is that the strongest published return cases usually come from large academic medical centers with robust analytics resources, so smaller hospitals often question whether those outcomes can be repeated in their own settings. Fujitsu reported that its AI-based hospital management deployment for Genkyukai in Nagasaki Prefecture was completed in 3 months and was projected to raise annual revenue by 10% through bed optimization and compliance automation, which shows why modular and faster deployment models may gain traction across the hospital capacity management solutions market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Patient Flow Software Redefines Capacity Management's Core Use Case

Capacity management software held 37.82% of the hospital capacity management solutions market share in 2025, which reflects long-standing hospital spending on bed tracking, census monitoring, and transfer coordination tools. The hospital capacity management solutions market is now showing a clear shift in buyer preference because Patient Flow Management Software is projected to expand at 13.89% CAGR through 2031. That gap shows that hospitals want systems that manage the full movement of a patient rather than only showing the current bed status. The change is important because it moves software demand from reactive visibility toward coordinated action across the patient stay.

Patient flow management software is gaining momentum because discharge planning, care coordination analytics, and multi-step progression management have become more urgent operating tasks across the hospital capacity management solutions market. LeanTaaS launched iQueue for Surgical Clinics in June 2025 as an end-to-end platform that connects surgical clinic activity with operating room scheduling, and early adopters reported 10% case growth and USD 300,000 in added revenue per surgeon each year. That example shows how workflow tools in the hospital capacity management solutions industry are increasingly framed as revenue support tools instead of simple operating aids. Capacity planning software remains relevant for long-range bed and asset planning, while resource management software supports staffing efficiency, and scheduling software is gaining ground as nurse and operating room utilization comes under more pressure. The hospital capacity management solutions market is therefore moving toward platforms that connect patient movement with staff and room availability rather than treating those tasks as separate categories.

By Deployment Mode: Cloud Migration Accelerates Despite Installed Base Dominance

Cloud solutions accounted for 53.41% of revenue in 2026, which shows that the hospital capacity management solutions market still carries a large installed base from earlier procurement cycles. The largest current share belongs to these platforms because many health systems adopted them before enterprise SaaS pricing and cloud compliance models became more established. At the same time, cloud-based deployment is forecast to grow at 14.19% CAGR through 2031 across the hospital capacity management solutions market. This growth is coming from greenfield hospitals and ambulatory settings that want faster deployment and lower infrastructure overhead.

The hospital capacity management solutions market is seeing cloud demand rise because providers can reduce local hardware spending and shorten implementation timelines when cloud hosting is acceptable. On-premises deployment still matters in countries that have strict data residency rules, especially Germany and France, where public providers often favor local hosting because of sovereignty and GDPR requirements. This has created room for hybrid models that keep clinical data on local systems but run orchestration and analytics in the cloud. LeanTaaS reported that 60% of its customer base uses Epic and 30% uses Oracle Cerner, and that concentration shapes integration roadmaps and vendor dependency patterns inside the hospital capacity management solutions market. The result is not a simple move from one deployment model to another, but a more selective migration based on compliance, installed base, and speed of rollout.

By Component: Services Growth Signals Deepening Vendor Engagement Models

Software represented 62.64% of revenue in 2025, which confirms that license and subscription income still forms the main commercial base of the hospital capacity management solutions market. The category holds the largest share because hospitals continue to spend first on platform access and core workflow functionality. Even so, the hospital capacity management solutions market size for services is projected to grow at 14.95% CAGR through 2031, which is faster than the overall market. That faster pace shows that buyers increasingly need vendors to support integration, redesign, training, and optimization over a longer period.

The hospital capacity management solutions market is placing more value on services because many providers no longer want to carry implementation risk on internal teams alone. Qventus launched its AI Solution Factory in December 2025 with Allina Health as the first client, and that model centers on co-developing custom automation workflows on a shared platform. Qventus also stated that its inpatient capacity clients removed more than 35,000 excess days and nearly 4 million EHR clicks during 2025, which shows how performance delivery is now being contracted as an ongoing service outcome rather than only as software functionality. This changes the revenue mix within the hospital capacity management solutions industry because implementation, analytics support, and workflow tuning are becoming more central to vendor economics. The shift also strengthens vendors that can stay embedded after go-live and continue to prove results through operational metrics.

By End User: ASC Growth Outpaces The Overall Market As Surgical Volume Migrates Outpatient

Hospitals generated 53.03% of revenue in 2025, which keeps them as the largest end-user group in the hospital capacity management solutions market. That leading share reflects the depth of workflow complexity across public, private, specialty, teaching, and children's hospitals. The hospital capacity management solutions market size for ambulatory surgical centers is projected to grow at 16.57% CAGR through 2031, which is the fastest rate among all segmentation types in the report. That pace shows that capacity tools are spreading into settings that were once considered too narrow for enterprise operational software.

The United States had more than 6,000 Medicare-certified ambulatory surgical centers in 2025, and CMS certified 168 new facilities in 2024, which points to a large and growing installed base for scheduling and throughput tools. Procedure volumes at these centers are forecast to grow 21% by 2035, and that growth is supporting demand for block management, scheduling, and perioperative coordination platforms across the hospital capacity management solutions market. CMS documentation requirements are also tightening the compliance case for integrated perioperative systems in multi-specialty chains, which means adoption is being driven by reimbursement readiness as well as throughput needs. Specialty clinics and other care facilities remain smaller today, yet they are adding relevance as health systems build multi-site ambulatory campuses and apply patient flow logic outside the inpatient setting. This broadens the hospital capacity management solutions market by taking technology built for hospitals and adapting it to shorter-stay and procedure-focused care environments.

By Workflow: Post-Discharge Solutions Gain Share As Integration Depth Becomes A Buying Priority

During admission workflows held 43.19% share in 2025, which made them the largest workflow category in the hospital capacity management solutions market. The segment led because inpatient bed placement, progression review, and real-time status management were the earliest and most mature use cases for these tools. Post-Discharge solutions are projected to grow at 13.72% CAGR through 2031 in the hospital capacity management solutions market. That faster growth shows a stronger buyer preference for continuity across pre-admission, inpatient, and post-discharge stages.

Pre-Admission workflows are gaining importance because readiness screening, prior authorization, and patient preparation often shape what happens later in the stay. Post-Discharge workflows are also becoming more important as hospitals face pressure to manage transitions, referral quality, and avoidable readmissions. A 2025 JMIR Formative Research study found that 62% of nurses said AI-based scheduling systems improved efficiency and fairness, and 76% preferred tools that offered flexibility and autonomy, which supports the case for workflow-integrated systems rather than isolated point tools. The hospital capacity management solutions market is therefore shifting toward platforms that connect staff behavior, patient timing, and operating decisions in one sequence. That shift matters because disconnected workflow tools can improve one step and still leave the rest of the patient pathway unchanged.

Geography Analysis

North America accounted for 48.41% of the hospital capacity management solutions market share in 2025, which made it the most commercially mature regional market. The United States drives most of that demand because value-based payment models, interoperability mandates, and a strong base of AI-focused operational vendors support active buying conditions. Canada and Mexico remain smaller demand centers, but both are seeing interest rise as digital health investment and pressure on publicly funded care networks expose the cost of poor throughput. The hospital capacity management solutions market in North America also benefits from dense enterprise health systems that can justify platform standardization across many facilities at once.

Europe remains the second-largest region in the hospital capacity management solutions market, with the United Kingdom, Germany, and France forming the deepest adoption base. In the United Kingdom, general and acute bed occupancy reached 92.5% in Q4 2024/25, which kept patient flow and discharge software high on the operational agenda. Germany is creating opportunities through hospital reform and consolidation, which can concentrate purchasing at the network level and favor vendors that present capacity management as an efficiency layer for merged systems. France added an important reference case in July 2025 when CHRU Nancy formalized the first hospital command centre deployment in the country with Dedalus, which points to wider enterprise interest across public hospital groupings. GDPR and national hosting rules continue to shape architecture choices in the hospital capacity management solutions market, and those rules often favor hybrid or on-premises designs in public settings.

Asia-Pacific is forecast to grow at 15.94% CAGR through 2031, which makes it the fastest-growing regional part of the hospital capacity management solutions market. Japan is showing active demand through command center adoption and broader hospital management digitization, including NEC's hospital management DX service launch in May 2026 and Fujitsu's 2025 deployment for Genkyukai in Nagasaki Prefecture. China and India present large greenfield opportunities because legacy EHR lock-in is lighter than in mature Western hospital systems, which can reduce integration friction during first deployments. Australia continues to serve as an early reference market through command center projects across Melbourne hospitals, while the Middle East and Africa are benefiting from public modernization programs led by GCC states and Saudi Arabia's Vision 2030 agenda. South America is expanding more gradually, with private hospital investment in Brazil and Argentina supporting selective procurement of patient flow and scheduling tools in larger urban networks. The hospital capacity management solutions market is therefore growing fastest where digitization, new facility buildout, and modernization needs combine with fewer legacy constraints.

Competitive Landscape

The hospital capacity management solutions market is moderately consolidated at the platform level, with Epic Systems, Oracle, GE HealthCare, and Siemens Healthineers benefiting from large installed bases and native integration with clinical systems. The same market also includes a specialist tier led by LeanTaaS, Qventus, TeleTracking Technologies, and Alcidion, and those vendors compete by offering deeper AI functionality and tighter workflow focus. This structure means the hospital capacity management solutions market is not controlled by one dominant vendor, but it is also not fully fragmented because several firms already have strong enterprise positions. Competition is increasingly shaped by how well vendors connect automation, interoperability, and measurable throughput outcomes.

LeanTaaS won the Best in KLAS 2026 designation for Capacity Optimization Management with a score of 95.6 out of 100, which shows how quickly AI-focused specialists have moved into the top tier of buyer attention. TeleTracking and Palantir announced a partnership in June 2025 to combine Operations IQ with Foundry and AIP, and that move points to a strategy built around enterprise data infrastructure and near real-time operational intelligence. Qventus used a different route when it introduced the AI Solution Factory with Allina Health in December 2025, because that model ties customers into co-developed workflows that can be harder to replace later. In the hospital capacity management solutions market, these moves show that vendors are no longer selling only software modules, but also operating frameworks that can shape how hospitals manage daily patient progression.

White space in the hospital capacity management solutions market remains strongest in smaller community hospitals and rural health systems that do not have the budget or IT staffing for large enterprise deployments. Another gap remains in cross-continuum coordination, where post-acute and ambulatory data still sit outside many current platform designs. Alcidion expanded its position in Australia and New Zealand by acquiring the Kyra flow product suite from Telstra Health, which reflects a broader pattern of regional vendors buying complementary workflow capability instead of building every function from scratch. Established vendors are also using compliance as a competitive tool, and InterSystems has emphasized enterprise-grade security, role-based authorization, and integrated API management for its IRIS for Health platform. The hospital capacity management solutions market is likely to see more partnership activity and targeted acquisitions because large vendors still need stronger AI execution and specialists still need broader enterprise reach. This keeps the competitive picture active without changing the basic reality that several credible vendors already hold meaningful positions across the hospital capacity management solutions market.

Hospital Capacity Management Solutions Industry Leaders

Epic Systems Corporation

McKesson Corporation

Oracle

Siemens Healthineers AG

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: TeleTracking Technologies launched Operations IQ Ambulatory, extending its Healthcare Operations Platform beyond acute care to outpatient referral management and access coordination. Built on the foundation of its Palantir Foundry integration, the launch addresses what TeleTracking describes as the industry's most persistent "blind spot" — the fragmented outpatient referral journey — and marks the company's first direct entry into ambulatory capacity management.

- May 2026: NEC (Japan) launched its hospital management DX services portfolio, including clinical data visualization, AI management analytics, and a forthcoming AI decision support service using Anthropic's Claude. NEC is targeting a domestic market where approximately 70% of hospitals operate at an annual deficit, with broader rollout to hospitals and groupements planned through fiscal year 2026.

- December 2025: Qventus announced Allina Health as inaugural client of its AI Solution Factory co-development partnership model. Across all Inpatient Capacity Solution clients in 2025, Qventus eliminated over 35,000 excess days and nearly 4 million EHR clicks, freeing approximately 450,000 minutes for inpatient care teams.

- June 2025: LeanTaaS launched iQueue for Surgical Clinics at the Transform Hospital Operations Summit, announced as the industry's first end-to-end surgical coordination platform extending OR-optimization science upstream to surgical clinics. Early adopters reported 10% surgical case volume growth and USD 300,000 in additional revenue per surgeon annually.

Global Hospital Capacity Management Solutions Market Report Scope

Hospital capacity management solutions are specialized healthcare software and services that optimize patient flow, bed allocation, staffing, and medical equipment utilization to maximize facility efficiency. They empower hospitals to reduce wait times, prevent bottlenecks, and proactively respond to patient demand surges.

The Hospital Capacity Management Solutions Market is segmented across several dimensions. By solution type, offerings include Capacity Management Software, Capacity Planning Software, Patient Flow Management Software, Resource Management Software, and Scheduling Software. By deployment mode, solutions are available as Cloud-Based, and On-Premises. By component, the market is divided into Software and Services. In terms of end users, adoption spans Hospitals including Public Hospitals, Private Hospitals, Specialty Hospitals, Teaching Hospitals, and Children’s Hospitals as well as Ambulatory Surgical Centers and Specialty Clinics and Other Care Facilities. By workflow, solutions support Pre-Admission, During Admission, and Post-Discharge.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Capacity Management Software |

| Capacity Planning Software |

| Patient Flow Management Software |

| Resource Management Software |

| Scheduling Software |

| Cloud-Based |

| On-Premises |

| Software |

| Services |

| Hospitals | Public Hospitals |

| Private Hospitals | |

| Specialty Hospitals | |

| Teaching Hospitals | |

| Children’s Hospitals | |

| Ambulatory Surgical Centers/Outpatient Centers | |

| Specialty Clinics and Other Care Facilities |

| Pre-Admission |

| During Admission |

| Post-Discharge |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Capacity Management Software | |

| Capacity Planning Software | ||

| Patient Flow Management Software | ||

| Resource Management Software | ||

| Scheduling Software | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Component | Software | |

| Services | ||

| By End User | Hospitals | Public Hospitals |

| Private Hospitals | ||

| Specialty Hospitals | ||

| Teaching Hospitals | ||

| Children’s Hospitals | ||

| Ambulatory Surgical Centers/Outpatient Centers | ||

| Specialty Clinics and Other Care Facilities | ||

| By Workflow | Pre-Admission | |

| During Admission | ||

| Post-Discharge | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the hospital capacity management solutions market?

The market is valued at USD 5.35 billion in 2026 and is projected to reach USD 10.07 billion by 2031 at a 13.47% CAGR.

Which region leads hospital capacity management solutions adoption?

North America leads with 48.41% share in 2025 because of strong interoperability rules, value-based payment models, and mature health IT deployment.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region with a forecast CAGR of 15.94% through 2031, supported by digitization and lower legacy integration constraints.

Which solution category is expanding fastest?

Patient flow management software is the fastest-growing solution type at 13.89% CAGR as hospitals shift from bed visibility to full patient progression management.

Why are ambulatory surgical centers becoming important buyers?

Ambulatory surgical centers are forecast to grow at 16.57% CAGR because procedure volumes are moving outpatient and centers need better scheduling, block use, and perioperative coordination tools.

What is changing vendor competition in this space?

Competition is being shaped by AI-driven orchestration, co-development service models, and tighter interoperability, with integrated EHR vendors and AI specialists both expanding their capabilities.

Page last updated on: