Hospital Bed Management Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.52 Billion |

| Market Size (2031) | USD 4.30 Billion |

| Growth Rate (2026 - 2031) | 11.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Bed Management Systems Market Analysis by Mordor Intelligence

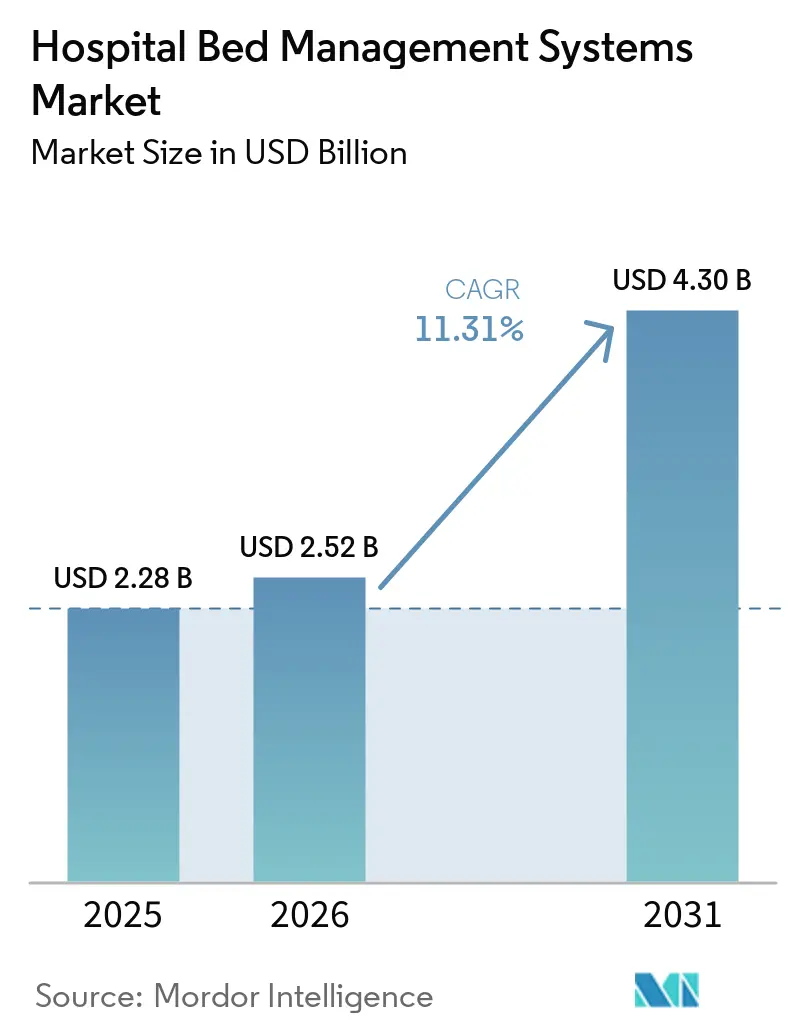

The hospital bed management systems market is expected to increase from USD 2.28 billion in 2025 to USD 2.52 billion in 2026 and reach USD 4.30 billion by 2031, growing at a CAGR of 11.31% over 2026-2031. The hospital bed management systems market is expanding as hospital networks increase spending on real-time operating infrastructure to handle higher inpatient volumes and tighter discharge protocols. The OECD reported that average curative bed occupancy across OECD countries was 72% in 2023, while Ireland and Canada were already above the 85% level that is widely treated as the practical ceiling for surge resilience, which is pushing hospitals toward structured bed management platforms. The hospital bed management systems market has also moved from incremental workflow tooling to an AI-native capacity layer, and peer-reviewed analysis published in 2026 showed that command center deployments can deliver the equivalent of 30 or more additional beds without physical expansion. This change is reducing room for narrow point-solution vendors and pushing larger EHR-adjacent platforms to speed up their capacity-intelligence roadmaps. Growth is still limited by legacy interoperability gaps, budget constraints in public and community hospitals, and rising cybersecurity exposure from live occupancy and patient location data.

Key Report Takeaways

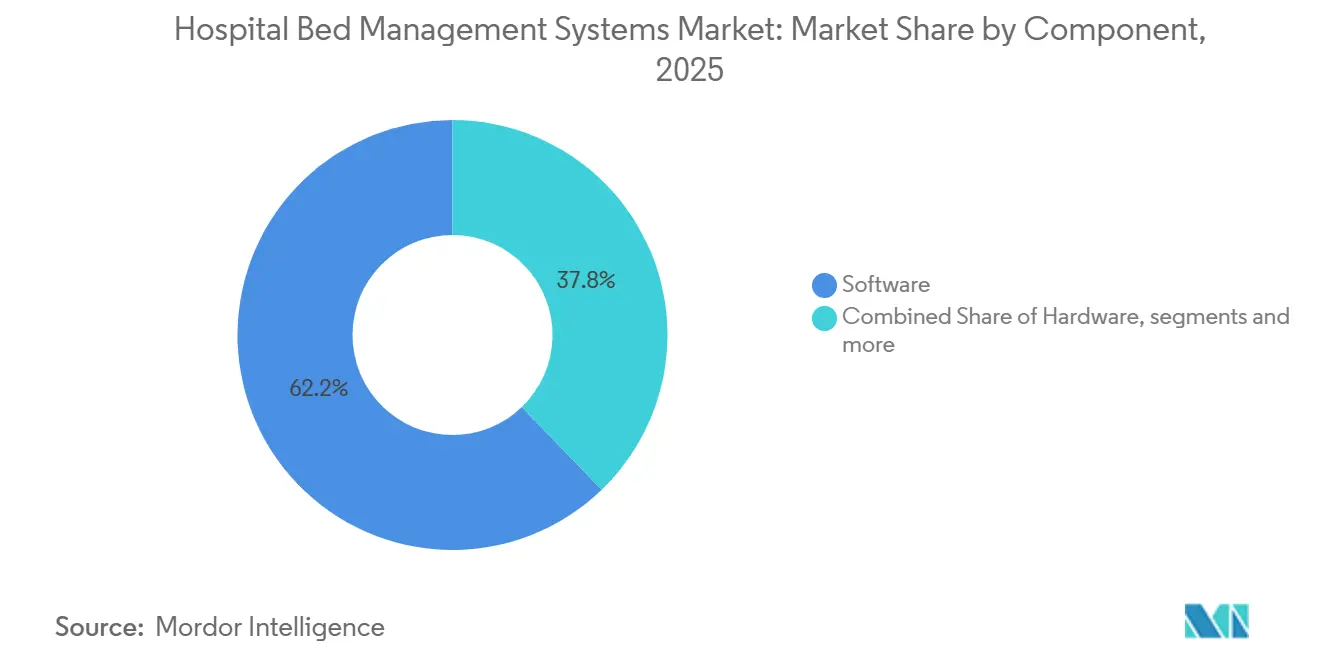

- By component, software led with 62.21% revenue share in 2025, while services recorded the highest projected CAGR at 11.53% through 2031.

- By deployment mode, cloud-based solutions held 65.61% of revenue in 2025 and also posted the highest projected CAGR at 12.65% through 2031.

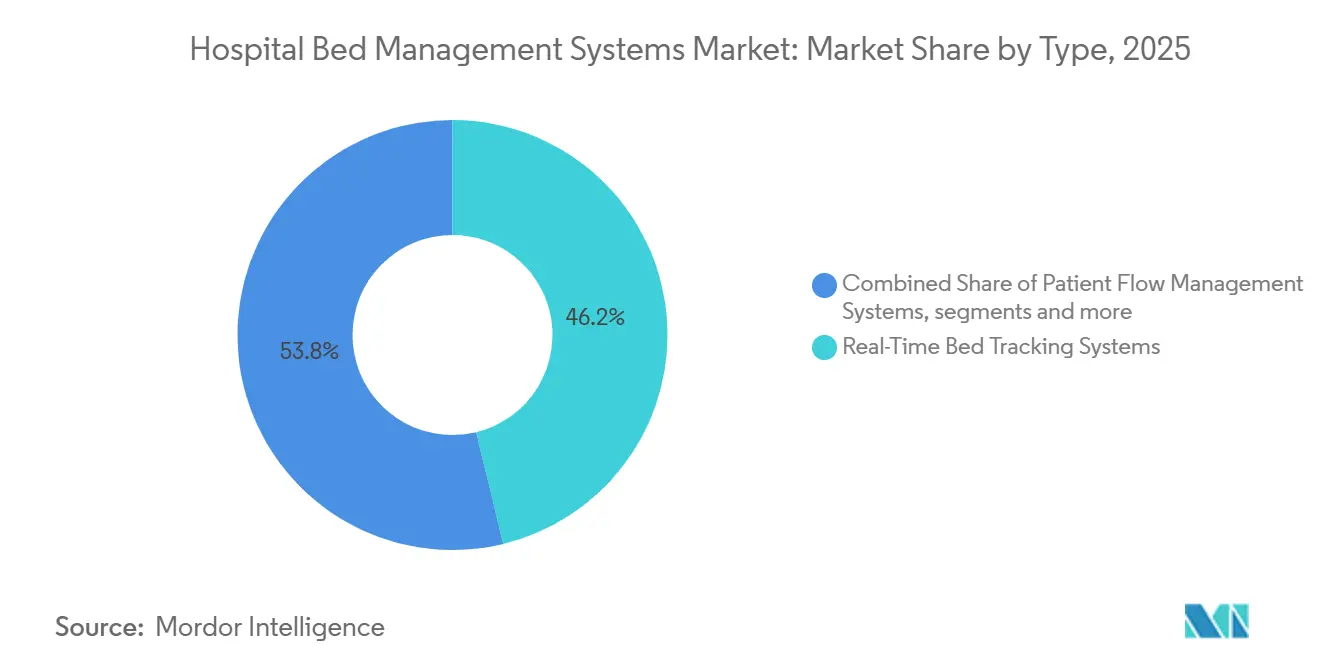

- By type, real-time bed tracking systems accounted for 46.17% of revenue in 2025, while patient flow management systems are forecasted to expand at a 12.88% CAGR through 2031.

- By end-user, general hospitals captured 40.09% of 2025 revenue, while specialty hospitals are projected to grow at a 12.33% CAGR through 2031.

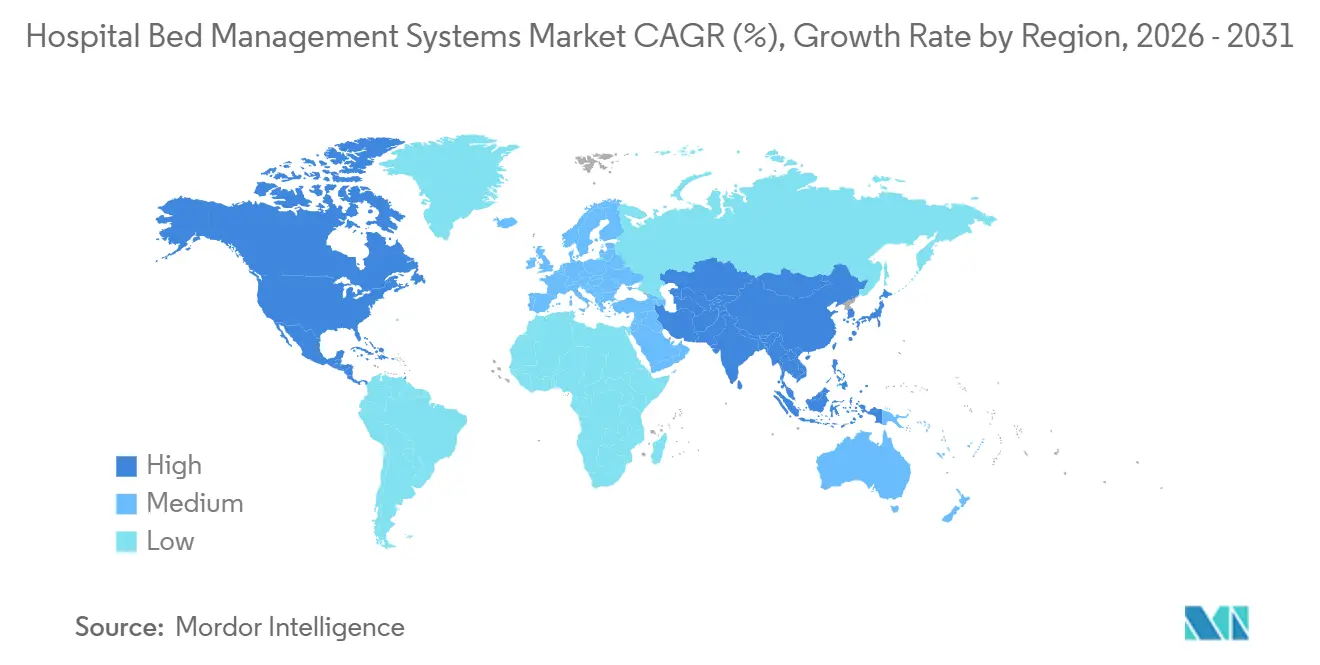

- By geography, North America held 44.25% of the 2025 market, while Asia-Pacific is forecasted to expand at a 13.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hospital Bed Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hospital Admissions and Bed Occupancy Pressure | +2.5% | Global | Short term (≤ 2 years) |

| Need For Faster Patient Flow and Shorter Length of Stay | +2.0% | North America & Europe | Medium term (2-4 years) |

| Expansion of EHR-Integrated Bed Allocation Workflows | +1.9% | North America, core APAC | Medium term (2-4 years) |

| Rapid Shift to Cloud-Based Hospital Operations Platforms | +1.8% | Global | Short term (≤ 2 years) |

| Real-Time Bed Turnover Auditability for Multi-Site Health Systems | +1.2% | North America, Australia | Medium term (2-4 years) |

| Infection-Control Driven Demand for Isolation and Cohort Bed Orchestration | +0.7% | Europe, APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hospital Admissions and Bed Occupancy Pressure

The hospital bed management systems market is gaining support from sustained pressure on hospital capacity and from the limited room many systems have for physical bed expansion. OECD data showed that the average bed-to-population ratio across member countries fell to 4.2 beds per 1,000 people in 2023, extending the longer decline seen across most high-income systems.[1]OECD, “Hospital Beds and Occupancy,” Health at a Glance 2025, oecd.org. Japan and South Korea remained exceptions at 12.5 and 12.6 beds per 1,000 people, but even that larger installed base increases the need for orchestration so distributed bed estates do not become fragmented. Once occupancy rises above the practical resilience ceiling, hospitals are no longer just buying efficiency software and are instead buying operating headroom that helps avoid canceled elective procedures, emergency department diversions, and delayed admission penalties. That dynamic keeps the hospital bed management systems market closely tied to inpatient pressure, regardless of whether a system has a low bed base or a large distributed estate.

Need for Faster Patient Flow and Shorter Length of Stay

The hospital bed management systems market is also being lifted by the need to reduce avoidable bed days and shorten length of stay without adding physical capacity. Queensland Health data cited by Alcidion showed that patients medically ready for discharge but still awaiting coordination represented 25% of inpatient bed days, and the related cost exceeded AUD 6.5 million per 500-bed hospital annually.[2]Alcidion Group Limited, “Patient Flow Evolution, Transforming Queensland Healthcare Through Connected Systems,” Alcidion, alcidion.com. Queen's Health Systems in Hawaii cut patient length of stay by 0.7 days within 6 months of implementing GE HealthCare's Command Center, and it did so without adding any physical beds. Each avoided bed day creates incremental admissions capacity at zero marginal infrastructure cost, which is why patient flow spending is increasingly treated as a revenue and throughput tool rather than only a cost program.

Expansion of EHR-Integrated Bed Allocation Workflows

The hospital bed management systems market is moving toward tighter EHR integration because disconnected bed status tools create avoidable delays between clinical events and bed turnover actions. Epic's patient flow architecture lets care teams act on bed requests from within the main EHR workflow rather than moving between separate systems. Parkview Health reduced turnaround time by 7 minutes per bed by using Epic's integrated housekeeping connectivity, which shows the direct operating benefit of native workflow integration. This makes EHR-linked platforms more attractive than bolt-on tools when hospitals want faster action on discharge, cleaning, transfer, and admission requests. As hospitals connect bed requests, housekeeping triggers, and clinical discharge steps inside one environment, EHR-integrated allocation is becoming a basic operating requirement in the hospital bed management systems market.

Rapid Shift to Cloud-Based Hospital Operations Platforms

The hospital bed management systems market is increasingly centered on cloud deployment. The main case for cloud is not only lower infrastructure burden, but also real-time visibility across multiple facilities through one interface. Health systems can onboard new sites faster, scale workflows more easily, and reduce the server maintenance load on teams that are already occupied by EHR management. Cloud architecture also makes it easier to combine bed management with workforce scheduling, operating room planning, and environmental services data. That broader connectivity turns bed management from a department-level tool into an enterprise operating asset in the hospital bed management systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Integration Costs | -1.6% | Global, especially MEA & Latin America | Medium term (2-4 years) |

| Legacy EHR and HIS Interoperability Complexity | -1.2% | Europe, South & Southeast Asia | Medium term (2-4 years) |

| Limited Digital-Operations Budget in Public and Smaller Hospitals | -0.9% | MEA, South America, rural Asia | Long term (≥ 4 years) |

| Cybersecurity and Data-Privacy Risk Around Real-Time Occupancy Data | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Integration Costs

The hospital bed management systems market still faces a clear barrier from the high upfront cost of implementation across mixed hospital IT estates. Multi-site rollouts often require custom HL7 connectors, workflow redesign, vendor consulting, and extended deployment support, which can stretch payback periods beyond what community and district hospitals can absorb in one budget cycle. The challenge grows when bed management must connect with a primary EHR, laboratory systems, pharmacy platforms, environmental services scheduling, and patient transport tools at the same time. In lower-income settings, that cost burden often limits adoption to the largest private hospital groups with stronger digital budgets. Underfunded early deployments can also stop at the reporting layer, which leaves hospitals with dashboards that describe flow problems but do not automate the workflows needed to correct them.

Cybersecurity and Data-Privacy Risk Around Real-Time Occupancy Data

The hospital bed management systems market also carries higher cybersecurity exposure because real-time platforms transmit continuously updated patient location and occupancy data rather than only static records. RunSafe Security reported in 2025 that 22% of healthcare organizations experienced cyberattacks that directly affected medical devices, and 3 out of 4 of those incidents disrupted patient care operations.[3]RunSafe Security, “2025 Medical Device Cybersecurity Index,” RunSafe Security, runsafesecurity.com. In the United States, the Healthcare Cybersecurity Act of 2025 and the updated HIPAA Security Rule increased the compliance burden around securing live patient data transmission. That means hospitals must spend more on controls, auditability, vendor review, and response planning before they scale real-time capacity tools across sites. Any breach that affects live occupancy feeds can interrupt patient flow operations directly, which makes some providers more cautious about large-scale deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Revenue as Services Scale with Complexity

Software held 62.21% of the hospital bed management systems market share in 2025. That leadership reflects the shift away from hardware-heavy RTLS deployments and toward recurring SaaS subscriptions, configuration-led contracts, and software modules that continue generating revenue after go-live. Predictive analytics, AI-driven discharge orchestration, and multi-site command center dashboards are all software-led capabilities that deepen the role of digital operating intelligence. Hardware still supports real-time tracking through RTLS tags, BLE sensors, and bedside terminals, but it is losing relative weight as existing networks and cloud APIs take over more of the data layer.

The hospital bed management systems market is expected to see the services segment expand at an 11.53% CAGR through 2031. That pace reflects the difficulty of integrating bed management platforms with EHRs, workforce scheduling tools, environmental services workflows, and RTLS hardware from several vendors. Services growth also shows that hospitals need workflow redesign and clinical process support, not only software configuration, if they want sustained throughput gains. This revenue mix favors vendors that can combine technology delivery with operational change management, and it supports continued reinvestment into AI features that increase platform stickiness.

By Deployment Mode: Cloud Consolidates Operational Agility Across Sites

Cloud-based deployment accounted for 65.61% share of the hospital bed management systems market size in 2025. That dual lead in adoption and scale shows that the market has already moved beyond the early inflection point for cloud infrastructure. A cloud model gives health systems one view across a network, faster site activation, and less internal server maintenance for IT teams that are already stretched by large clinical platforms. It also supports easier expansion into multi-facility command center models, which depend on fast and consistent data exchange across hospitals.

The hospital bed management systems market is anticipated to see cloud-based deployment grow at a 12.65% CAGR through 2031. On-premises systems still keep a residual role in public health settings with strict data sovereignty rules and in high-security hospitals where data residency remains a hard requirement. Even so, the choice of deployment mode now shapes how widely bed management can connect with staffing, surgery scheduling, and environmental services workflows. Cloud therefore acts as a strategic operating choice rather than only an IT preference.

By Type: Real-Time Tracking Leads, Patient Flow Intelligence Commands Future Growth

Real-time bed tracking systems represented 46.17% of 2025 revenue in the hospital bed management systems market. They remain the core visibility layer because accurate occupancy status is required before hospitals can run more advanced functions such as discharge prediction, cohort placement, and infection-control routing. In practical terms, these tools create the live operating picture that command centers and transfer teams need to make consistent bed decisions. Bed capacity planning systems hold a narrower but important position for multi-campus organizations that model demand across weeks instead of only hours.

The hospital bed management systems market size for patient flow management systems is projected to expand at a 12.88% CAGR through 2031. That is the strongest growth rate among type segments and it shows that hospitals are shifting from passive status monitoring toward predictive discharge orchestration. Integrated platforms that combine tracking, flow management, and planning are also drawing increasing vendor investment because providers want one operating source of truth instead of separate point solutions. The fastest growth is therefore moving to tools that can manage changing patient trajectories rather than only record static bed states.

By End-User: General Hospitals Anchor Volume, Specialty Settings Accelerate Demand

General hospitals held 40.09% of the hospital bed management systems market share in 2025. They generate the largest contracted volume because they dominate the acute-care base and because they manage emergency, elective, surgical, and transfer queues at the same time. This broad operating load makes bed management a daily control point rather than an occasional optimization tool. Rehabilitation centers and long-term care settings also matter as connected end users because transfer coordination increasingly depends on interoperability with acute-care bed workflows.

The hospital bed management systems market size for specialty hospitals is forecasted to rise at a 12.33% CAGR through 2031. Oncology, cardiac, and orthopedic facilities need more precise cohort placement, sterile environment sequencing, and post-surgical isolation tiering than standard admit-discharge-transfer workflows can provide. That gives niche-capable platforms room to grow faster where bed logic must reflect service-line complexity rather than only general acute throughput. Value-based reimbursement pressure and the cost of avoidable readmissions are also pushing specialty providers to invest in discharge planning and post-acute handoff tools.

Geography Analysis

North America accounted for 44.25% share of the hospital bed management systems market size in 2025. The region benefits from dense multi-site health systems, mature EHR environments, and an operating culture that links bed performance to reimbursement outcomes under value-based care. The United States remains the largest country market in the region, and the strong installed base of Epic Systems and Oracle Health gives EHR-native bed management tools a meaningful distribution advantage. In Canada, acute-care occupancy already exceeded 85% in multiple provinces according to OECD data, which is pushing procurement of real-time capacity tools beyond the traditionally cautious public procurement cycle. Mexico is moving forward through public hospital modernization, although adoption remains slower outside major metropolitan systems because of budget limits.

Europe is the second-largest regional block in the hospital bed management systems market. Germany, the United Kingdom, and France anchor demand, with the United Kingdom standing out because persistent discharge delays and chronic bed shortages create a clear case for digital patient flow tools. Alcidion reported that its Miya Precision deployment across Herefordshire and Worcestershire Health and Care NHS Trust delivered a 5-day reduction in average length of stay during the first program phase. Across the region, procurement is shaped not only by throughput needs but also by compliance with national health data rules and broader cybersecurity requirements.

Asia-Pacific is projected to be the fastest-growing region in the hospital bed management systems market, with a projected CAGR of 13.76% through 2031. In China and India, government-backed hospital modernization creates greenfield openings for cloud-native deployment because legacy integration barriers are often lighter than in mature Western systems. Australia continues to act as an early adopter, and GE HealthCare's Command Center deployment across The Alfred, Caulfield, and Sandringham hospitals in Melbourne gives the region a reference case for broader adoption. Middle East and Africa and South America remain earlier-stage markets, but growth potential is supported by GCC hospital construction programs, Saudi Arabia's healthcare infrastructure agenda, and private hospital investments in Brazil and Argentina.

Competitive Landscape

The hospital bed management systems market shows moderate concentration at the enterprise tier and much heavier fragmentation in the mid-market and specialty tiers. TeleTracking Technologies, GE HealthCare Command Center, and Epic's Grand Central remain the most visible anchors in the installed enterprise base, while a larger field of regional and niche vendors competes for cloud-oriented buyers outside that top layer. Competitive position now depends less on simple bed status visibility and more on whether a platform can support predictive discharge, live command center workflows, and multi-site capacity orchestration.

This is why the market has moved from incremental workflow software toward an AI-led operations layer. It also explains why EHR-adjacent vendors are moving faster to add capacity intelligence inside their broader hospital operating platforms. The hospital bed management systems market is seeing strategic expansion moves that widen platform scope rather than only add features. GE HealthCare continues to strengthen its position in the hospital bed management systems market through command center reference deployments and workflow outcomes that are tied to census forecasting and staffing decisions.

Epic also benefits from native workflow depth, and Parkview Health's 7-minute per-bed turnaround improvement shows how strong EHR embedding can defend share against stand-alone tools. Qventus is gaining attention by linking AI capacity tools to measurable operating outcomes, including reduced excess bed days and time savings for care teams. Vendors that can manage isolation, step-down, surgical, and transfer cohorts inside one coordinated workflow are positioned best as buyers seek fewer platforms with broader operating depth.

Hospital Bed Management Systems Industry Leaders

Epic Systems Corporation

Oracle

TeleTracking Technologies, Inc.

LeanTaaS, Inc.

McKesson Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: TeleTracking Technologies launched Operations IQ Ambulatory, extending its enterprise healthcare operations platform into outpatient access and referral management for the first time in the company's 35-year history. Carilion Clinic is the inaugural deployment site. This expansion directly targets outpatient throughput bottlenecks as surgical volume continues migrating away from inpatient settings, materially widening TeleTracking's addressable market.

- May 2026: Alcidion Group Limited signed an Asset Sale Agreement to acquire Kyra Patient Flow Manager, Kyra Queue Manager, and Kyra IQ from Telstra Health for approximately AUD 3 million (approximately USD 1.95 million), adding over 30 new healthcare provider customers and substantially expanding its presence across Queensland, Victoria, Western Australia, and Tasmania. The Miya Precision platform now supports more than 400 hospitals and 50,000 beds globally.

- March 2026: MEDITECH announced at HIMSS26 the expansion of its Expanse AI portfolio, including native ambient intelligence for physicians and nurses, AI-enabled claim denial agents, and agentic AI capabilities designed to automate operational and revenue cycle workflows. These capabilities directly support bed management by reducing documentation burden that currently delays discharge confirmations.

- February 2026: Erlanger Health System reported 5x annualized ROI from its Qventus Surgical Growth Solution deployment across four sites, with nearly 12 additional OR cases per week and break-even achieved in under three months, demonstrating the financial return profile that is accelerating specialty hospital adoption of AI-based capacity platforms.

Global Hospital Bed Management Systems Market Report Scope

According to the report’s scope, the hospital bed management systems market refers to digital platforms that use real‑time bed visibility, workflow automation, and predictive capacity planning to track bed occupancy, streamline admissions and discharges, reduce wait times, and optimize patient flow across hospital units, improving operational efficiency and resource utilization.

The hospital bed management systems market is segmented into component, deployment mode, type, end-user, and geography. By component, the market is segmented into software, hardware, and services. By deployment mode, the market is segmented into cloud-based and on-premises. By type, the market is segmented into real-time bed tracking systems, patient flow management systems, bed capacity planning systems, and integrated bed management platforms. By end-user, the market is segmented into general hospitals, specialty hospitals, ambulatory surgical centers, and other end-users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Hardware |

| Services |

| Cloud-Based |

| On-Premises |

| Real-Time Bed Tracking Systems |

| Patient Flow Management Systems |

| Bed Capacity Planning Systems |

| Integrated Bed Management Platforms |

| General Hospitals |

| Specialty Hospitals |

| Ambulatory Surgical Centers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Type | Real-Time Bed Tracking Systems | |

| Patient Flow Management Systems | ||

| Bed Capacity Planning Systems | ||

| Integrated Bed Management Platforms | ||

| By End-User | General Hospitals | |

| Specialty Hospitals | ||

| Ambulatory Surgical Centers | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for hospital bed management systems?

The hospital bed management systems market is projected to reach USD 4.30 billion by 2031 from USD 2.28 billion in 2025 to USD 2.52 billion in 2026, growing at an 11.31% CAGR over 2026-2031.

Which deployment mode is growing fastest in hospital bed management systems?

Cloud-based deployment mode leads the market with 65.61% revenue share in 2025 and is also projected to be the fastest-growing deployment mode at a 12.65% CAGR through 2031.

Which end-users are driving demand the most?

General hospitals held 40.09% of 2025 revenue because they manage the broadest mix of emergency, elective, surgical, and transfer bed queues. Specialty hospitals are expected to grow faster at a 12.33% CAGR because they need more precise cohort and isolation logic.

Which region leads adoption and which region is expanding fastest?

North America led with 44.25% share in 2025, supported by dense health systems and mature EHR environments. Asia-Pacific is anticipated to be the fastest-growing region with a 13.76% CAGR through 2031.

Page last updated on: