Hospital Command Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

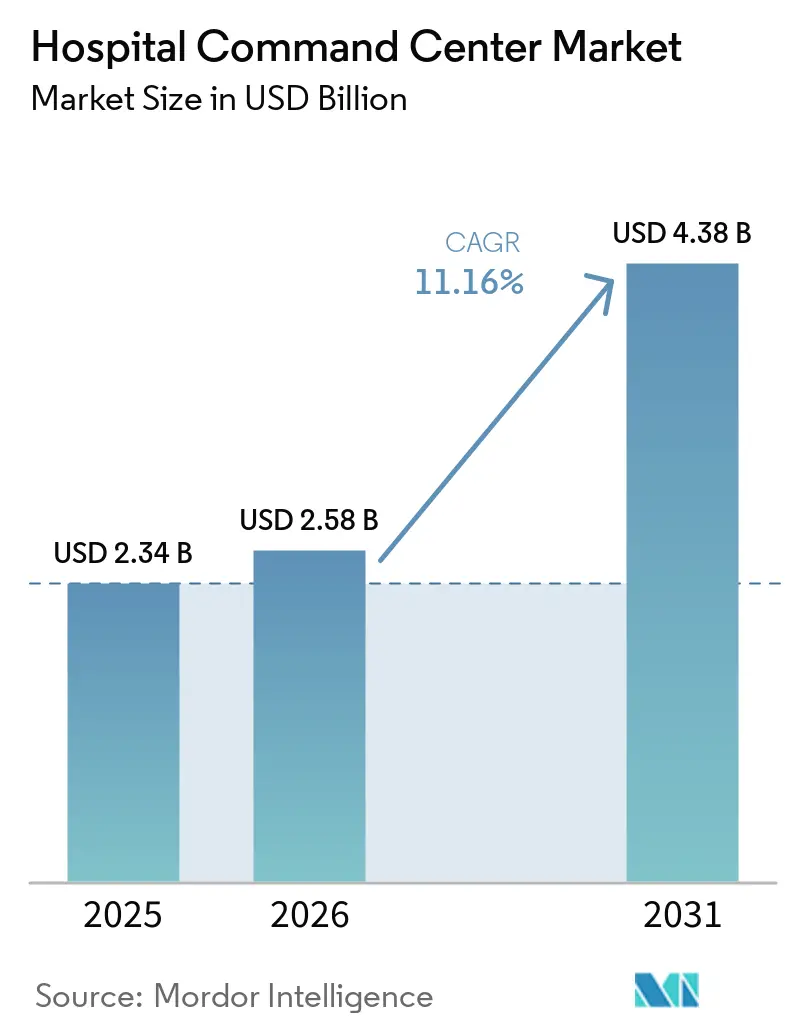

| Market Size (2026) | USD 2.58 Billion |

| Market Size (2031) | USD 4.38 Billion |

| Growth Rate (2026 - 2031) | 11.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospital Command Center Market Analysis by Mordor Intelligence

The hospital command center market is expected to increase from USD 2.34 billion in 2025 to USD 2.58 billion in 2026 and reach USD 4.38 billion by 2031, growing at a CAGR of 11.16% over 2026-2031. Demand is tied to a structural gap between available hospital capacity and patient volumes, which has raised the need for tools that improve throughput without adding new beds. In the United States, staffed beds fell to 674,000 after the pandemic from 802,000 before it, and occupancy above 85% has been linked with emergency department boarding that exceeds 4 hours. That imbalance has made command center software a more practical near-term response than brick-and-mortar expansion, especially in systems facing capital limits and regulatory friction around bed additions. The hospital command center market is also moving from simple visibility tools toward predictive and workflow-driven operations, which is raising the value of orchestration, analytics, and automation across health systems. Cyber exposure remains the main headline risk because the command layer concentrates real-time feeds from several hospital systems in one operating environment.

Key Report Takeaways

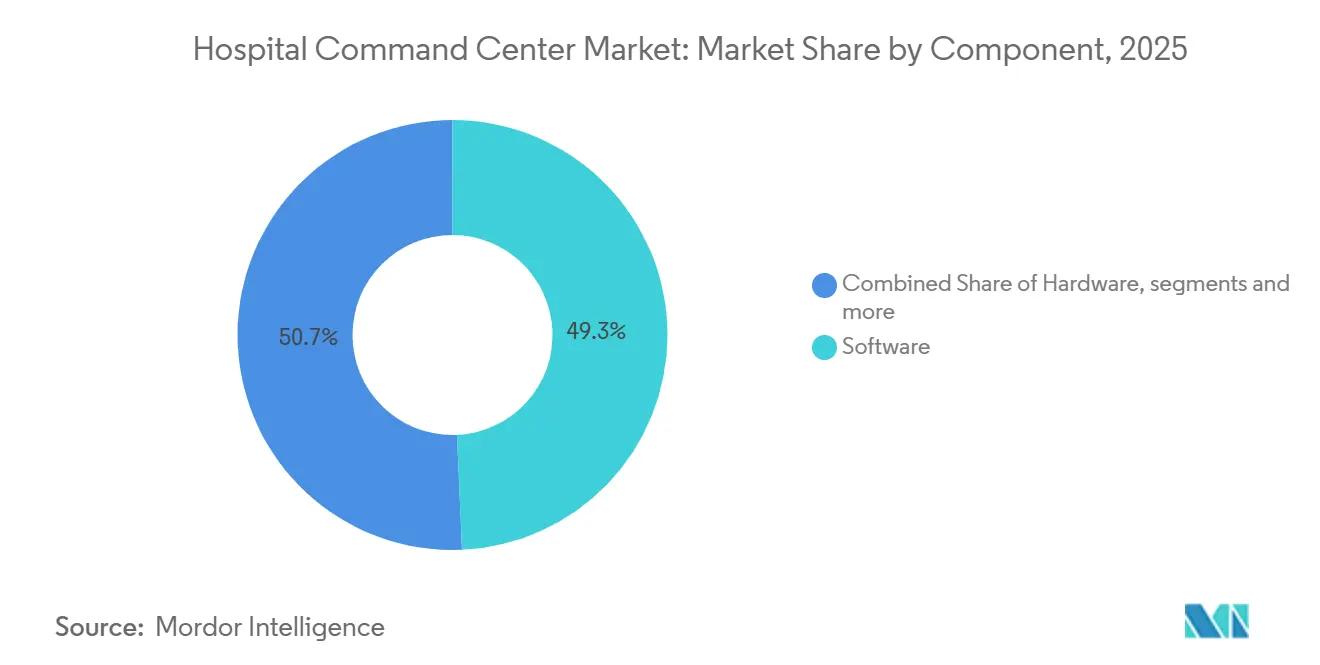

- By component, software led with 49.27% revenue share in 2025, while services are projected to expand at an 11.55% CAGR through 2031.

- By deployment mode, cloud-based platforms held 50.13% of revenue in 2025, while hybrid deployments are forecasted to grow at a 12.19% CAGR through 2031.

- By command center type, capacity and bed management centers accounted for 45.29% of revenue in 2025, while centralized clinical command centers are projected to advance at an 11.84% CAGR through 2031.

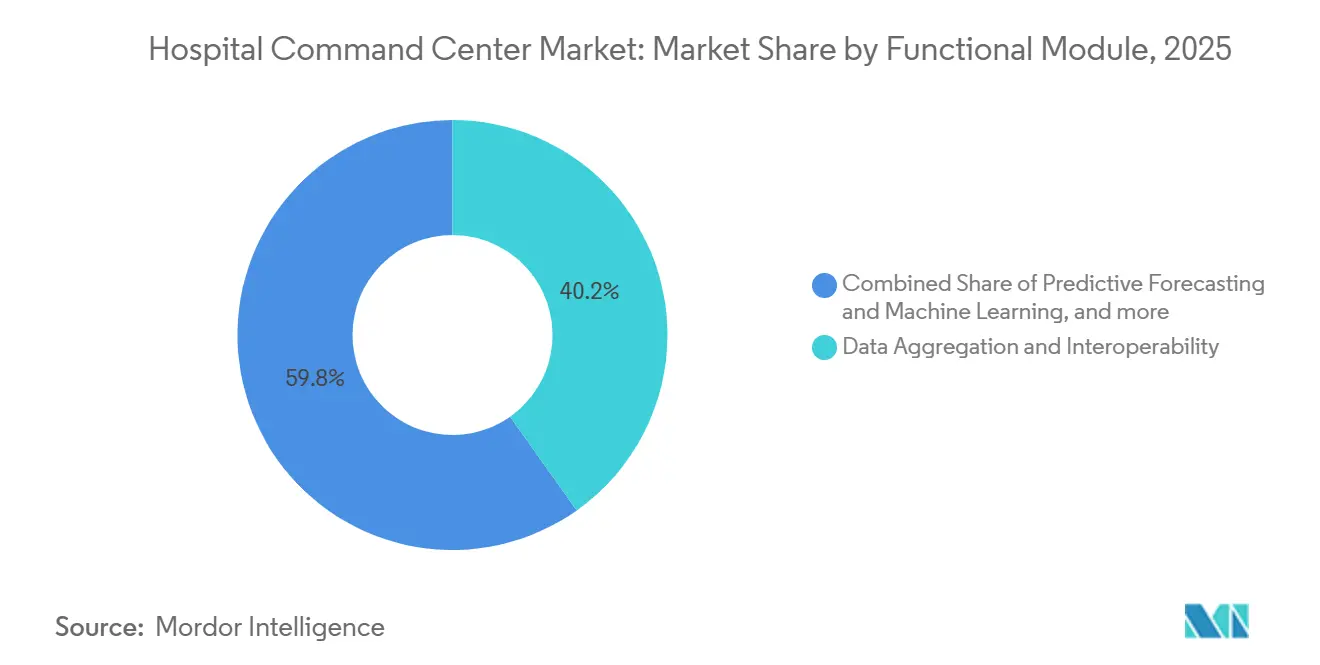

- By functional module, data aggregation and interoperability held 40.16% of revenue in 2025, while performance and KPI reporting and business intelligence are projected to grow at a 12.34% CAGR through 2031.

- By end-user, large health systems and multi-hospital networks held 39.48% of revenue in 2025, while tertiary and academic medical centers are projected to record an 11.71% CAGR through 2031.

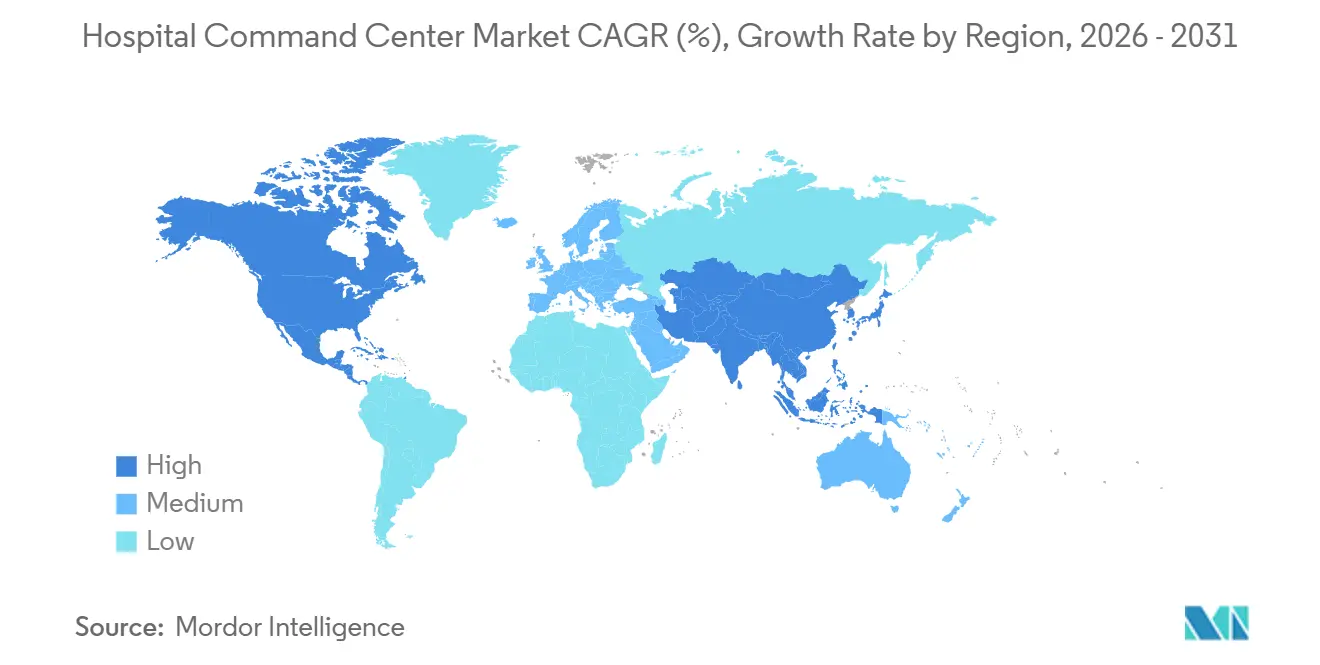

- By geography, North America held 42.41% of revenue in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 13.62% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hospital Command Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Real-Time Patient Flow Orchestration | +2.6% | Global | Short term (≤ 2 years) |

| Expansion of Virtual Care and Hospital-at-Home Coordination | +1.7% | North America primary, EU and Australia spill-over | Medium term (2-4 years) |

| Operational Pressure from ED Boarding and Capacity Constraints | +2.0% | North America, Western Europe | Short term (≤ 2 years) |

| Adoption of AI-Enabled Predictive Hospital Operations | +2.3% | North America, Western Europe, APAC core | Medium term (2-4 years) |

| Interoperability Demand Across Multi-Hospital Networks | +1.5% | North America and EU, APAC emerging | Medium term (2-4 years) |

| Need for Resilient Emergency Preparedness and Surge Management | +0.7% | Global, with early gains in APAC and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Real-Time Patient Flow Orchestration

The hospital command center market is being shaped by evidence that these systems act as capacity multipliers rather than passive dashboards. The Queen's Health Systems in Hawaii reported a 63.9% reduction in emergency department boarding, equal to 503 fewer patients each month after deployment. The same deployment reduced average length of stay by 1.07 days and generated an estimated USD 20 million in first-year savings without adding physical bed capacity. Results like these show why hospitals are treating flow management as a systemwide capacity and margin issue rather than a unit-level staffing problem. In the hospital command center market, that makes throughput improvement from existing infrastructure a more attractive path than regulated and capital-heavy bed expansion.

Expansion of Virtual Care and Hospital-at-Home Coordination

The hospital command center market is also expanding through virtual care programs that require centralized remote coordination. As of September 2025, 419 hospitals across 147 health systems in 39 U.S. states had CMS approval to provide Hospital-at-Home services.[1]American Hospital Association, “Fact Sheet: Extending the Hospital-at-Home Program,” American Hospital Association, aha.org In December 2025, the U.S. House of Representatives passed the Hospital Inpatient Services Modernization Act, which would extend the waiver through 2030 and support more permanent planning around these programs. Each enrolled patient needs continuous monitoring, care coordination, and escalation support, which ties program scale directly to demand for a virtual command layer. Hackensack Meridian Health expanded its Hospital From Home program to two more hospitals in 2025, which shows how health systems are moving these services into broader operational use.[2]Hackensack Meridian Health, “HMH Expands Hospital From Home Program to Two More Hospitals,” Hackensack Meridian Health News, hackensackmeridianhealth.org As this care model shifts from pilot status to a longer-term service line, the hospital command center market is extending beyond inpatient flow into remote clinical coordination.

Operational Pressure from ED Boarding and Capacity Constraints

The hospital command center market continues to gain support from worsening emergency department boarding and persistent capacity strain. In 2025, the Emergency Nurses Association and the Agency for Healthcare Research and Quality called for national action on crowding, boarding, and patient throughput, including more centralized and standardized resource tracking.[3]Emergency Nurses Association, “Crowding, Boarding, and Patient Throughput in the Emergency Department Position Statement,” Emergency Nurses Association, ena.org The supply side of the problem remains severe because staffed U.S. hospital beds stood at 674,000 after the pandemic compared with 802,000 before it. Hospitals that operate near or above full inpatient capacity are often forced to use the emergency department as overflow space, which raises the value of centralized bed, discharge, and transfer coordination. In the hospital command center market, this makes operational intelligence the most scalable near-term response where bed additions remain slow, expensive, or restricted by local approval processes.

Adoption of AI-Enabled Predictive Hospital Operations

The hospital command center market is shifting from retrospective visibility toward forward-looking operations built on prediction and automation. GE HealthCare research teams are developing an N-BEATS neural network model that predicts hospital pressure levels across multiple operating dimensions up to 72 hours in advance. That time window gives hospitals more room to adjust staffing, elective scheduling, and diversion planning before congestion peaks. TeleTracking announced a partnership with Faculty in January 2025 and a partnership with Palantir in June 2025 to strengthen AI-powered hospital operations, which shows that vendors are actively building this capability into their platforms. The next step is workflow execution rather than alert display alone, and that shift is likely to separate leaders from legacy operators in the hospital command center market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy Hospital IT | -1.4% | Global, most acute in South America and MEA | Short term (≤ 2 years) |

| Cybersecurity and Data Privacy Exposure | -1.1% | Global | Short term (≤ 2 years) |

| Change Management and Clinical Workflow Resistance | -0.8% | Global, especially community and regional hospitals | Medium term (2-4 years) |

| Capital Intensity for Display, Network, and Analytics Infrastructure | -0.7% | APAC, South America, MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Hospital IT

The hospital command center market still faces a major deployment barrier from legacy hospital IT environments. Many hospitals run decades of customized HL7 v2 interfaces across large numbers of clinical systems, which makes integration slow and highly dependent on local workflow mapping. Migration toward FHIR-based architectures can take 1-3 years and requires coordination across IT teams, clinical informatics leaders, and EHR vendors. Health system consolidation adds another layer of difficulty because multi-EHR environments often delay platform harmonization and push out the timing of realized value. In the hospital command center market, vendors with pre-built connectors and more standardized deployment methods are better placed to reduce this friction and shorten the path to adoption.

Cybersecurity and Data Privacy Exposure

Cybersecurity and privacy exposure remain a clear restraint on the hospital command center market because the operating layer concentrates high-value clinical and operational data. The American Hospital Association reported continued breach activity and strong emphasis on defensive measures across health systems in 2025. Command centers aggregate feeds from EHRs, staffing systems, RTLS tools, bed management platforms, and connected devices, which creates a broad attack surface if controls are weak. A breach at this layer can disrupt multiple workflows at once and carry wider operating consequences than a compromise of a single source application. Procurement teams are therefore placing more weight on formal security controls, certified operating practices, and zero-trust deployment models when they evaluate hospital command center market vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals Market Maturation

In the hospital command center market, software held 49.27% of revenue in 2025 and remained the core platform layer across deployment models. Buyers usually start with a platform that can connect data, support decisions, and present systemwide flow conditions in one operating view. Hardware still matters because video walls, display systems, workstations, and RTLS devices support physical command center environments, but that layer no longer drives the bulk of spending.

In the hospital command center market, services are projected to grow at an 11.52% CAGR through 2031, which reflects the need for implementation support, workflow redesign, and adoption management. The services layer becomes more important after first-generation rollouts because hospitals often expand from one module into additional operational use cases over time. That creates a stickier revenue stream than a one-time software deployment because the relationship continues through optimization, training, and change support. The hospital command center industry is therefore moving from an installation cycle toward a longer operating partnership model in which vendors remain involved well beyond go-live.

By Deployment Mode: Hybrid Momentum Reflects Data Sovereignty Demands

In the hospital command center market, cloud-based deployment held 50.13% of revenue in 2025 because health systems favored vendor-managed scalability, faster rollouts, and lower infrastructure burden. This model fits well with health systems that prefer ongoing vendor support and need a flexible base for analytics and orchestration. It also lowers the need for large up-front infrastructure commitments, which is important when command center programs start with a focused operational scope.

In the hospital command center market, hybrid deployment is projected to grow at a 12.19% CAGR through 2031 as data governance needs become more important. Academic medical centers with research obligations and active clinical trial activity often need to keep sensitive datasets on local infrastructure while still using cloud analytics for broader coordination. That requirement is sustaining the role of on-premises nodes in high-security environments such as government and military hospitals. A clear deployment pattern is emerging in which cloud-native analytics sits above on-premises operational stores, allowing the hospital command center market to combine AI capability with tighter control of sensitive data.

By Command Center Type: Bed Management Anchors Entry; Clinical Centers Drive Next Growth

Capacity and bed management centers held 45.3% of the hospital command center market share in 2025 and stayed central because bed assignment, discharge timing, and transfer coordination are the most visible pain points in hospital operations. These centers also give buyers a clearer return case because results can be tracked through boarding time, length of stay, and throughput metrics. As a result, many hospitals still begin with bed management before they add broader clinical or enterprise functions.

In the hospital command center market, centralized clinical command centers are projected to grow at an 11.84% CAGR through 2031 as health systems look for a stronger clinical and operational case in one hub. These centers combine real-time acuity tracking, deterioration alerts, and clinical support with broader operational management. Operations and resource orchestration centers are also widening their role to include operating room scheduling, transport, and workforce coordination. The hospital command center industry is moving toward more integrated models, and centralized clinical centers stand out because they can support both patient outcomes and efficiency targets in value-based care settings.

By Functional Module: KPI Reporting Captures Governance Demand

In the hospital command center market, data aggregation and interoperability held 40.16% of revenue in 2025 because every other module depends on connected data flows. Hospitals cannot run predictive models, escalation workflows, or executive dashboards without first bringing operational and clinical data into a common structure. That makes integration capability the functional base of the product stack. It also explains why many early deployments concentrate investment on foundational data layers before more advanced applications are activated.

In the hospital command center market, performance and KPI reporting and business intelligence are projected to grow at a 12.34% CAGR through 2031 as executives demand clearer proof of value. Boards and leadership teams increasingly want direct visibility into throughput, discharge performance, clinical outcomes, and financial return from command center programs. Predictive forecasting and machine learning are gaining ground as vendors place forecasting tools inside operational workflows instead of offering them as separate analytics products. Alerting and workflow automation are also moving beyond rule-based notifications, while simulation and digital twin tools are advancing through projects such as the Central Hospital of Wuhan digital twin infrastructure and broader RTLS and IoT integration for remote patient oversight.

By End-User: Large Health Systems Set Scale; Academic Centers Lead Innovation

In the hospital command center market, large health systems and multi-hospital networks held 39.48% of revenue in 2025 because centralized coordination delivers greater returns when it spans several hospitals. These organizations can spread a command center across broad transfer networks, elective scheduling, and enterprise bed management. Their scale also supports larger implementation teams and more formal operating redesign. That combination makes them the natural early adopters of enterprise command center platforms.

In the hospital command center market, tertiary and academic medical centers are projected to grow at an 11.71% CAGR through 2031 because they manage complex referrals and place high value on data-rich operating environments. Their high-acuity case mix raises the need for tighter intake, transfer, and escalation processes, while their research orientation supports investment in advanced analytics. Community and regional hospitals are gaining access through vendor-managed cloud offerings that reduce the local IT burden. Third-party virtual command center operators are also emerging as a relevant model, especially where health systems want 24/7 remote monitoring capacity without building the full function internally.

Geography Analysis

North America held 42.41% of hospital command center market share in 2025 because the region combines severe capacity pressure with reimbursement models that reward efficiency and penalize avoidable delays. The United States represented the large majority of installed activity, and major delivery networks have already shown multi-year command center use across throughput and care coordination programs. Canada is moving through provincial consolidation efforts that support more centralized operational management, while Mexico remains earlier in adoption and is seeing more activity from private hospital groups. A separate North American demand tailwind comes from interoperability policy, which is steadily improving API readiness and reducing friction for future platform connections.

In the hospital command center market, Europe remained the second-largest regional cluster, led by Germany, the United Kingdom, and France. National health service structures create a natural case for centralized coordination across hospital networks, especially when public systems need to use existing assets more efficiently. Germany and France are benefiting from digital health modernization efforts that support infrastructure upgrades and improve the funding case for command center projects. Italy, Spain, and the rest of Europe are still earlier in the rollout curve, while the Middle East and Africa show a split picture between Gulf smart hospital projects and much earlier-stage adoption across much of Sub-Saharan Africa.

In the hospital command center market, Asia-Pacific is projected to grow at a 13.62% CAGR through 2031 and remains the fastest-growing region. Growth is being supported by government-backed digital health programs, smart hospital investment, and broader acceptance of AI-enabled hospital operations across major economies. Japan is also building real-world command center references, including the first National Hospital Organization deployment announced by GE HealthCare Japan in 2025. South America, led by Brazil, remains in an early growth phase where private hospital groups and insurers are beginning to adopt models shaped by North American experience.

Competitive Landscape

The hospital command center market has a moderately fragmented structure, with no single vendor controlling the full cross-segment landscape. Specialist companies such as TeleTracking Technologies, LeanTaaS, Qventus, Care Logistics, and ABOUT Healthcare compete on operational depth, change management, and proof of clinical and financial outcomes. Larger healthcare technology companies such as GE HealthCare, Koninklijke Philips, Siemens Healthineers, Oracle, and Epic extend command center capability from adjacent positions in patient monitoring, EHR infrastructure, imaging, and hospital software. That mix creates a market in which specialists often lead on focused workflow use cases while diversified vendors benefit from broader installed bases. The result is steady competition between best-of-breed execution and platform adjacency across the hospital command center market.

White space remains strongest in virtual command centers for hospital-at-home networks, digital twin and simulation modules for predictive capacity planning, and service-led offerings for smaller hospitals that cannot staff a full internal operations center. The hospital command center market is also moving toward automation that executes tasks inside workflow rather than only presenting alerts, which raises the strategic value of AI-ready platforms. Procurement standards are tightening at the same time, and interoperability readiness is becoming a more important filter as hospitals prefer vendors that can fit into complex enterprise environments with less custom work. That combination favors vendors that can pair strong operating outcomes with easier integration and lower deployment risk.

Recent strategic moves show how leading suppliers are building this position. Philips introduced its Enterprise Command and Care Coordination Center in May 2026 for Asian hospitals facing workforce shortages, while Qventus continued to expand its AI position through its Solution Factory and operating assistant approach. These actions show that the hospital command center market is increasingly being shaped by platform breadth, AI execution, and the ability to deliver measurable operational change.

Hospital Command Center Industry Leaders

GE HealthCare

Koninklijke Philips N.V.

Siemens Healthineers AG

TeleTracking Technologies, Inc.

Epic Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: WellSpan Health and Koninklijke Philips announced a landmark strategic alliance establishing Philips as the preferred imaging vendor across all 12 WellSpan hospitals, with coordinated technology lifecycle management and a structured foundation for integrated service delivery, creating a data infrastructure that will support command center expansion across the Pennsylvania and Maryland network.

- May 2026: Koninklijke Philips unveiled its Enterprise Command and Care Coordination Center at the HIMSS APAC summit, combining wireless cardiac monitoring, AI-based arrhythmia detection, and centralized alarm management into a unified command infrastructure designed to address workforce shortages in Asian healthcare systems.

- April 2026: Qventus launched a Care Gap and Coding Automation Suite incorporating AI Operational Assistants, targeting USD 4 million in annual revenue uplift for an early academic medical center client by automating documentation, identifying coding gaps, and triggering care pathway interventions directly within the EHR.

Global Hospital Command Center Market Report Scope

According to the report’s scope, the hospital command center market refers to the market for centralized platforms, technologies, and services that provide real-time visibility into hospital operations, patient flow, bed capacity, staffing, and resource utilization. These solutions integrate data from multiple hospital systems to support operational decision-making, improve care coordination, optimize capacity management, and enhance overall healthcare delivery efficiency.

The hospital command center market is segmented into component, deployment mode, command center type, functional module, end-user, and geography. By component, the market is segmented into software, hardware, and services. By deployment mode, the market is segmented into cloud-based, hybrid, and on-premises. By command center type, the market is segmented into capacity and bed management centers, operations and resource orchestration centers, centralized clinical command centers, incident response and emergency operations centers, and security and facilities operations centers. By functional module, the market is segmented into data aggregation and interoperability, real-time operational intelligence and dashboards, predictive forecasting and machine learning, alerting, escalation, and workflow automation, simulation and digital twin, performance and KPI reporting and business intelligence, and RTLS and IoT integration. By end-user, the market is segmented into large health systems and multi-hospital networks, tertiary and academic medical centers, community and regional hospitals, ambulatory surgery centers and integrated clinics, and third-party virtual command center operators. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Hardware |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Capacity and Bed Management Centers |

| Operations and Resource Orchestration Centers |

| Centralized Clinical Command Centers |

| Incident Response and Emergency Operations Centers |

| Security and Facilities Operations Centers |

| Data Aggregation and Interoperability |

| Real-Time Operational Intelligence and Dashboards |

| Predictive Forecasting and Machine Learning |

| Alerting, Escalation, and Workflow Automation |

| Simulation and Digital Twin |

| Performance and KPI Reporting and Business Intelligence |

| RTLS and IoT Integration |

| Large Health Systems and Multi-Hospital Networks |

| Tertiary and Academic Medical Centers |

| Community and Regional Hospitals |

| Ambulatory Surgery Centers and Integrated Clinics |

| Third-Party Virtual Command Center Operators |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Deployment Mode | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Command Center Type | Capacity and Bed Management Centers | |

| Operations and Resource Orchestration Centers | ||

| Centralized Clinical Command Centers | ||

| Incident Response and Emergency Operations Centers | ||

| Security and Facilities Operations Centers | ||

| By Functional Module | Data Aggregation and Interoperability | |

| Real-Time Operational Intelligence and Dashboards | ||

| Predictive Forecasting and Machine Learning | ||

| Alerting, Escalation, and Workflow Automation | ||

| Simulation and Digital Twin | ||

| Performance and KPI Reporting and Business Intelligence | ||

| RTLS and IoT Integration | ||

| By End-User | Large Health Systems and Multi-Hospital Networks | |

| Tertiary and Academic Medical Centers | ||

| Community and Regional Hospitals | ||

| Ambulatory Surgery Centers and Integrated Clinics | ||

| Third-Party Virtual Command Center Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the hospital command center space expected to become by 2031?

The hospital command center market size is projected to reach USD 4.38 billion by 2031 from USD 2.58 billion in 2026, with an 11.16% CAGR over the forecast period.

Which deployment model is gaining the most traction?

Cloud-based systems led in 2025 with 50.13% of revenue, but hybrid deployment is anticipated to grow faster at a 12.19% CAGR because many hospitals need both scalable analytics and local data control.

Why are services growing faster than software in this space?

Services are projected to grow at an 11.52% CAGR because hospitals need change management, workflow redesign, training, and ongoing optimization after the initial platform goes live.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific is projected to be the fastest regional outlook with a 13.62% CAGR, supported by smart hospital investment, digital health programs, and rising use of AI-enabled operations across major healthcare systems.

Page last updated on: